29

Chapter One THE CENTRAL CONCEPTS OF ECONOMICS

| Date post: | 14-Jan-2017 |

| Category: |

Economy & Finance |

| Upload: | jean-pierre-mulumba |

| View: | 18 times |

| Download: | 0 times |

Chapter OneTHE CENTRAL CONCEPTS OF ECONOMICS

PROF JEAN-PIERRE MULUMBA 2

About This ChapterWhat is economics all about?

How it is organized

How it works as science

We will study some other fundamental problems like economic organizations, society's technological possibilitiesOpportunity cost

PROF JEAN-PIERRE MULUMBA 3

Learning Objectives After studying this chapter students will be able to:

◦ Explain the economic problem and the concepts of scarcity and choices for individuals, organizations and the whole economy.

◦ Define economics. ◦ Define the three primary inputs in the production of outputs: land, labor, and capital.◦ Distinguish between microeconomics from macroeconomic issues and variables.

PROF JEAN-PIERRE MULUMBA 4

Learning Objectives After studying this chapter students will be able to:

◦ Distinguish between positive and normative economics. ◦ Understand the concept of productive efficiency and how it relates to both the use of inputs and the

basic definition of economics. ◦ Use the production-possibility frontier to illustrate the choices that societies face.◦ Introduce the concept of opportunity cost.

PROF JEAN-PIERRE MULUMBA 5

What is Economics? Study of how societies

◦ Use scarce resources to produce valuable commodities and,◦ To distribute them.

Scarcity: Resources are limited◦ Economic goods are scarce or limited in supply.◦ Free goods like air exist in such large quantities. Thus, their market price is zero.

Efficiency: Use resources efficiently ◦ To maximize satisfaction with the given inputs and technology.

Video

PROF JEAN-PIERRE MULUMBA 6

Two Branches Economics is subdivided in two subfields:

◦ Microeconomics◦ Behavior of individual entities: households, firms, or markets.

◦ Macroeconomics◦ The overall performance of the economy.

PROF JEAN-PIERRE MULUMBA 7

The Logic of Economics Scientific Approach to understand economic life Involving

◦ Observation of the economic life◦ Data collection◦ Or historical record inquiries

◦ Based on those observations: hypothesis elaboration◦ Testing hypothesis◦ Accepting or rejecting and modifying hypothesis◦ Theories, economic principles, economic law.

PROF JEAN-PIERRE MULUMBA 8

The Logic of Economics (1) Theoretical approaches allow economists to make broad generalizations

Economists have developed econometrics◦ Application of statistics to economic problems

PROF JEAN-PIERRE MULUMBA 9

The Logic of Economics (2) Avoid common pitfalls in economic reasoning

◦ Post Hoc Fallacy: because one event occurred before another, then, the first event caused the second.◦ Failure to hold other things constant: may lead to false conclusions.◦ The fallacy of composition: what is true for one individual is true for the whole.

PROF JEAN-PIERRE MULUMBA 10

Positive and Normative Analysis Statements possible in macroeconomics and in microeconomics.

Positive economics deals with questions resolved by analysis and empirical evidence. ◦ Is the analysis of facts and behavior in an economy, ◦ Or “the way things are.”

Normative economics involves ethical precepts and norms of fairness.◦ It considers “what ought to be”—value judgments, or goals.

PROF JEAN-PIERRE MULUMBA 11

The Three Questions of Economic Organization: What, How, & For Whom

Every society is confronted to three essential economic problems it has to resolve:

What question: what commodities to produce and consume?

How are goods produced? ◦ Society would know what inputs and technology to use?

For Whom are goods produced?

PROF JEAN-PIERRE MULUMBA 12

Economic Organizations The three questions above prefigure economic organizations.

◦ The ways societies try to allocate their scarce resources

·Market, Command, and Mixed Economies

PROF JEAN-PIERRE MULUMBA 13

Economics Organizations (1) Command Economy:

◦ Centralized Economy, Planned Economy, Communist or Socialist Economy.◦ Government takes most of the economic decisions.

Market Economy◦ Also called Liberal, Free Market, or Capitalist Economy. ◦ Decisions are made in markets by economic agents

◦ Through prices system

Mixed economy◦ Combines elements of Command and Market economies◦ All contemporary societies are mixed economies.

PROF JEAN-PIERRE MULUMBA 14

Society's Technological Possibilities Problematic

◦ Each economy has a stock of limited resources◦ It must choose to produce different potential bundles of goods and services

◦ Or select different techniques of production.◦ It has to decide about inputs and outputs.

PROF JEAN-PIERRE MULUMBA 15

Inputs, Resources, Factors of Production

Inputs are productive resources used to produce goods and services.

Traditionally:◦ Land: represents, not only the soil, but all natural resources

◦ Labor: time and work effort spent in producing ◦ Capital: good produced used to produce other goods and services ◦ Entrepreneurial ability: super factor of production that organizes other factors.

PROF JEAN-PIERRE MULUMBA 16

Outputs Outputs: fruits obtained from the combination of various inputs

They are goods and services aimed to be consumed,

Or to be used in further production

PROF JEAN-PIERRE MULUMBA 17

Production Possibilities Table The production possibility frontier (table or curve)

◦ maximum amounts of production that can be obtained by an economy, ◦ given its technological knowledge ◦ and quantity of inputs available.

◦ The PPF represents the menu of goods and services available to society Assumptions:•Scarce input and technology

•Considering an economy which produces only two economic goods

•Economy is having full employment.

PROF JEAN-PIERRE MULUMBA 18

Table 1: Alternative Production Possibilities

Possibilities Butter (millions of pounds)

Guns(thousands)

A 0 15

B 1 14

C 2 12

D 3 9

E 4 5

F 5 0

Limitation of Scarce Resources Implies the Guns-Butter Tradeoff

PROF JEAN-PIERRE MULUMBA 19

Graph 1: The Production Possibilities Frontier

PROF JEAN-PIERRE MULUMBA 20

Attainable and Unfeasible Combinations

The PPF marks the limit of possible attainable productions.

It is the maximum production to be produced with

◦ All the resources,◦ And technology available.

Only points on the PPF and inside are attainable.

Outside are points that cannot be produced with current resources and technology.

◦ See point I on the graph.

PROF JEAN-PIERRE MULUMBA 21

Full Employment And Unemployment

The economy utilizes his full productive capacity. ◦ It uses all available factors of production. ◦ The PPF represents the situation of full employment of resources: ◦ The unemployment: the economy leaves idle some factors of production.

◦ Any point inside the PPF: economy unable to attain the state of productive efficiency.

PROF JEAN-PIERRE MULUMBA 22

Tradeoffs and Free Lunches The PPF illustrates the notion of tradeoffs.

A tradeoff: a constraint that forces an exchange or a substitution of one thing for something else.

PROF JEAN-PIERRE MULUMBA 23

Applying the PPF to Society’s Choices

The PPF is the menu of choices from a broad range of economic choices.

It can choose to spend more resources on public highways, and less on private goods.

It can choose to consume more food, and less on clothing.

It can choose to consume more today, and less on its production of capital goods in the future.

PROF JEAN-PIERRE MULUMBA 24

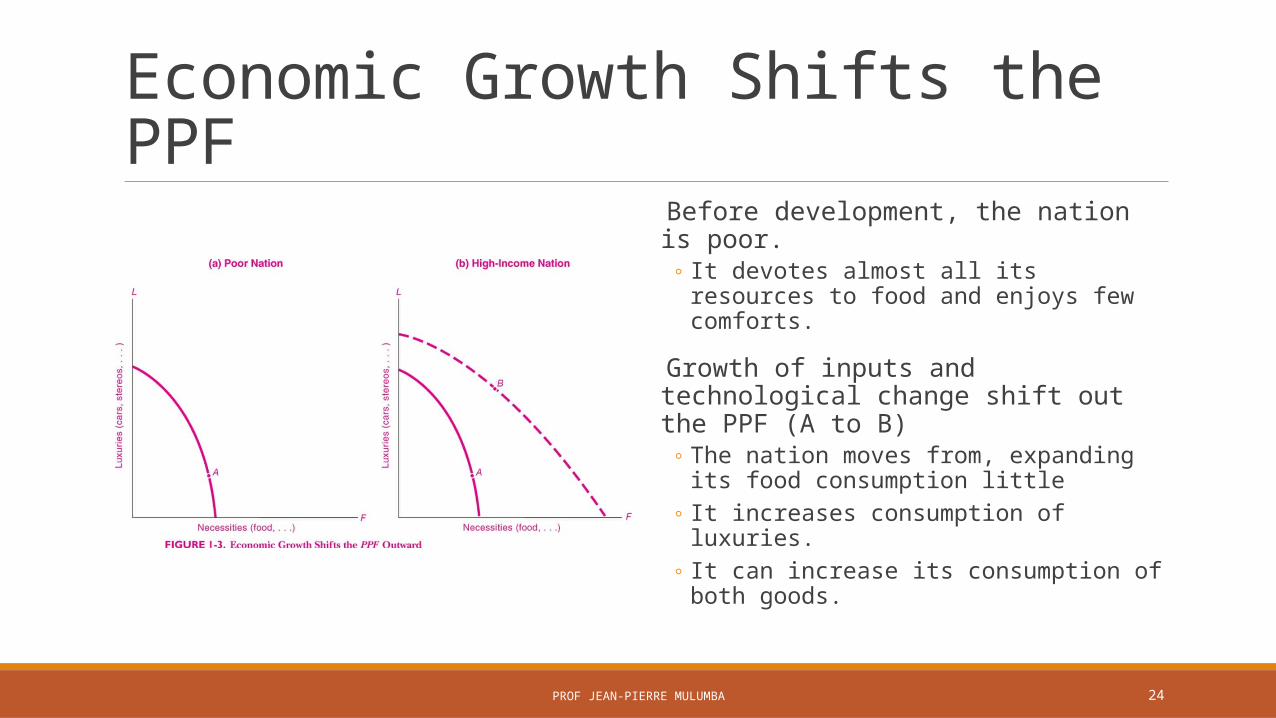

Economic Growth Shifts the PPF Before development, the nation is poor.

◦ It devotes almost all its resources to food and enjoys few comforts.

Growth of inputs and technological change shift out the PPF (A to B)

◦ The nation moves from, expanding its food consumption little

◦ It increases consumption of luxuries. ◦ It can increase its consumption of both goods.

PROF JEAN-PIERRE MULUMBA 25

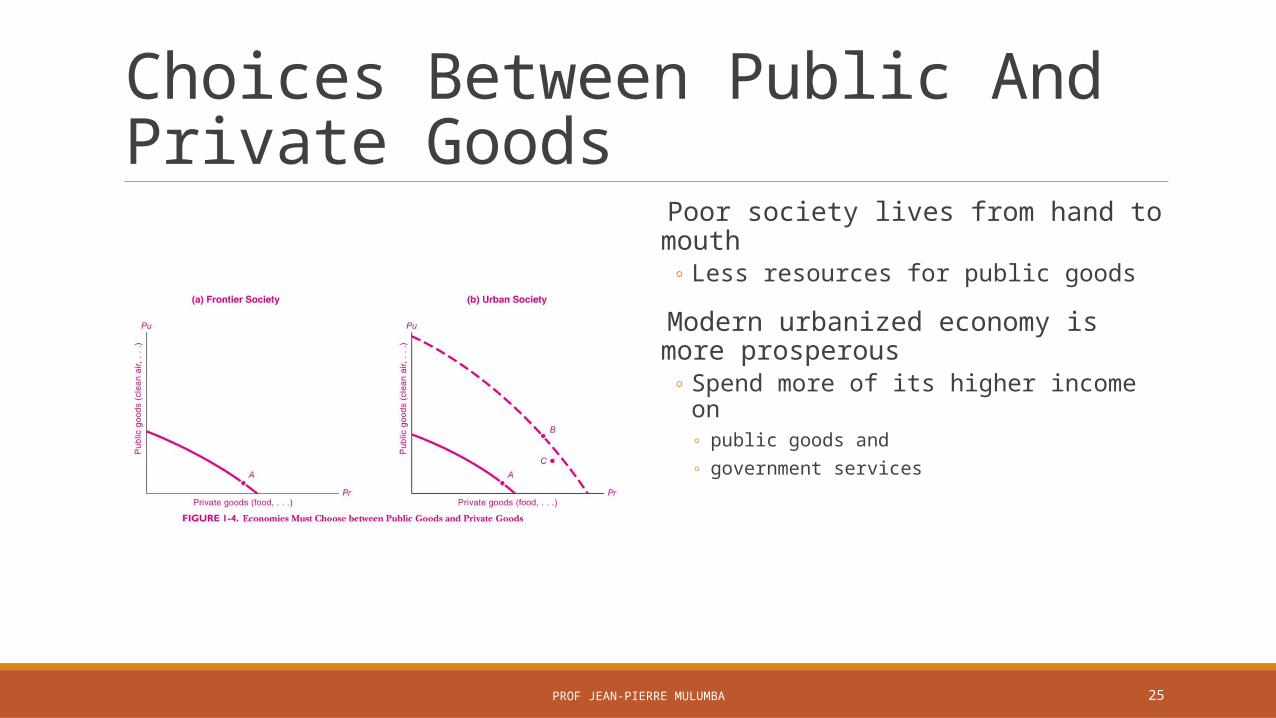

Choices Between Public And Private Goods

Poor society lives from hand to mouth ◦ Less resources for public goods

Modern urbanized economy is more prosperous

◦ Spend more of its higher income on ◦ public goods and ◦ government services

PROF JEAN-PIERRE MULUMBA 26

Present Consumption & Future Consequences

(a) A nation can produce either current-consumption goods (or investment goods).

Three countries start out even. ◦ They have the same PPF, shown on the left.◦ But they have different investment rates.

Country 1 does not invest for the future and remains at A 1

Country 2 abstains modestly from consumption and invests at A 2.

Country 3 sacrifices current consumption and invests heavily.

PROF JEAN-PIERRE MULUMBA 27

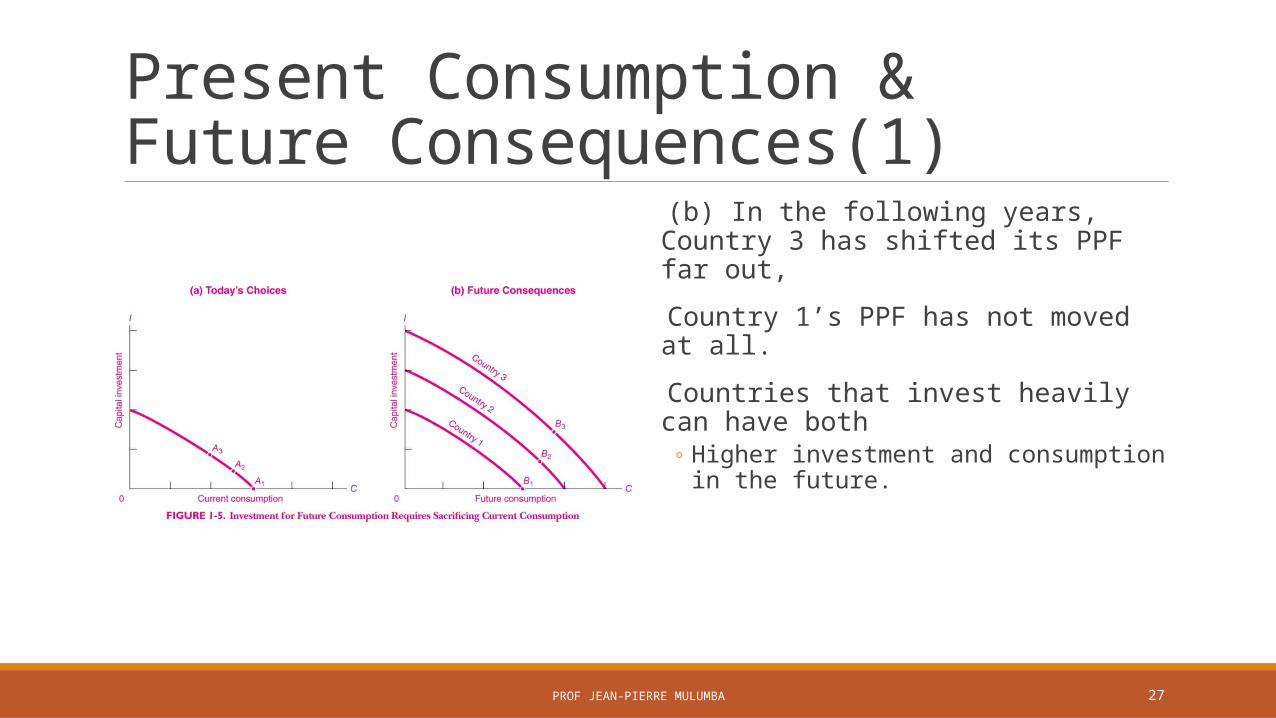

Present Consumption & Future Consequences(1)

(b) In the following years, Country 3 has shifted its PPF far out,

Country 1’s PPF has not moved at all.

Countries that invest heavily can have both◦ Higher investment and consumption in the

future.

PROF JEAN-PIERRE MULUMBA 28

The Concept of Opportunity Cost Life is full of choices.

Because resources are scarce, we must consider how much the choice will cost in terms of forgone opportunities.

In the PPF graph, it is the value of butter production that must be given up to produce the extra guns, and vice-versa.

It is the value of the resources used when measured in terms of their next best alternative.

PROF JEAN-PIERRE MULUMBA 29

Marginal Opportunity Cost Association of the concept of opportunity cost and marginal cost

Marginal cost is the additional cost associated with the production of extra units of a good.

Marginal opportunity cost is the opportunity cost for the production of extra units of a good.

![Chapter 4[1] Motivation Working One](https://static.documents.pub/doc/80x56/577cd95a1a28ab9e78a34da2/chapter-41-motivation-working-one.jpg)