26

HEMANT ARORA & CO. LLP Chartered Accountants INDIA BUDGET STATEMENT 2019 The Direct Tax Proposals

HEMANT ARORA & CO. LLP Chartered Accountants

INDIA BUDGET STATEMENT 2019

The Direct Tax Proposals

HEMANT ARORA & CO. LLP

Chartered Accountants

Offices

- Gurgaon

1117-19, 11th Floor, DLF Galleria Tower

DLF Phase IV, Gurgaon 122002

Tel.: + 91 124 257 8088

Fax.: + 91 124 257 0888

- Dehradun

1, Tyagi Road, Dehradun 248001

Tel.:+ 91 135 2626795

Fax: + 91 135 2627795

- Roorkee

354B, 30 Civil Lines, Roorkee 247667

Tel.:+ 91 1332 273343

Fax: + 91 1332 277272

- Mumbai

B-304 New India Chambers, MIDC Road, Andheri East, Mumbai 400093

Tel.: + 91 98370 28795

Partners

Hemant K Arora

Jeetan Nagpal

Sanjay Arora

Prabhat Rastogi

Kamal Nagpal

www.hemantarora.in

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 3

Contacts

Hemant K. Arora

+ 91 98370 39666

Jeetan Nagpal

+ 91 98370 28795

Sanjay Arora

+ 91 97562 08586

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 4

This document is a result of our study of the direct tax proposals forming part of the Finance (No.2)

Bill, 2019 and is intended to bring to you the salient proposals in a simple, condensed and

comprehensible manner.

We would like to reiterate that what have been discussed in the following pages are the proposals

pertaining to the direct taxes. The said proposals are open to modifications and alterations during the

course of discussion in the Parliament before they eventually become law upon receiving the assent of

the President of India.

Disclaimer

This document is intended for use by Firm’s personnel and clients only. It summarizes the Direct tax

proposals forming part of the Union Budget 2019.

While due care has been taken during the compilation of this document to ensure that the information

is accurate to the best of our knowledge and belief, the content is not to be construed in any manner

whatsoever as a substitute for professional advice. We do not assume any liability or responsibility for

the outcome of decisions taken as a result of any reliance placed on this publication.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 5

Contents

Foreword ............................................................................................................... 7

At a glance............................................................................................................. 9

Direct Tax Proposals ........................................................................................... 13

Glossary............................................................................................................... 24

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 6

This page has been intentionally left blank.

Foreword

Finance Minister Nirmala Sitharaman

presented the Finance (No.2) Bill 2019 to the

Parliament on July 5, 2019.

In keeping with the firm’s tradition, we are

presenting to you this document which

explains the proposed changes in direct tax

law in a reader friendly and comprehensible

manner and hope you would find it useful.

The major changes for individual tax payers

are the steep increase in surcharge on rich and

super rich which will impose a heavy tax

burden on those having income of over Rs. 1

crore and even greater burden on those having

income of over Rs. 5 crores in a year. Even

though the number of such individuals

declaring income of over Rs. 5 crore is a partly

6,361 [source: Economic Times], the

maximum tax rate for them is now whooping

42.7% which is 7% higher than the earlier

effective tax rate. On the other hand,

additional deductions shall be provided for

interest on loans for affordable housing and

electric vehicles, withdrawals and

contributions from/to National Pension scheme

which are expected to provide some relief to

eligible taxpayers. Certain provisions like the

one mandating TDS by individuals and Hindu

undivided families on payment to contractors

and professionals even for personal use

services would impose an additional

compliance obligation even though the

objective of these provisions may have been to

facilitate enable greater data mining of

transactions by the Government. What is

praiseworthy is introduction of faceless e-

assessment wherein the identity of the officer

will not be known to the taxpayer is intended

to reduce the interface between tax collector

and tax payer. Also, the inter-changeability

between PAN and Aadhar would make

compliance easier.

For corporates having turnover of upto Rs.

400 crores (earlier limit was Rs. 250 crores)

the reduction of tax rate to 25% would be a

welcome relief. For start-ups many of their tax

related concerns have been addressed and at

the same time additional incentives are in the

offing. Also, more tax incentives are now

available for units located in International

Financial Services Centre and to Non-Banking

Finance Companies. Provisions are also

introduced for redressal of certain taxation

issues of distressed companies which are under

resolution with the NCLT.

On the transfer pricing front, clarification on

assessments post filing of modified tax returns

in pursuance of Advance Pricing Agreements

is a welcome move. So also, are the proposals

for aligning transfer pricing provisions with

international best practices in respect of

secondary adjustment and for allowing

adoption of parent entity’s accounting year for

Country by Country Report.

To conclude I would like to borrow and share

with the readers the opening paragraph from

the Foreword to Kanga and Palkhivala’s The

Law and Practice of Income Tax (10th Edition)

which reads as under:

“The power to tax involves the power to

destroy, warned Chief Justice John Marshall.

To which, a century later, the reply of Justice

Holmes was, the power to tax is not the power

to destroy while this Court sits.

Sturdy independence is equally the hallmark of

the Indian courts. By their enlightened

approach to our income-tax law they have

often controlled and sometimes curtailed, its

lethal power.”

Jeetan Nagpal

Partner

HEMANT ARORA & CO. LLP

Chartered Accountants

July 6, 2019.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 8

This page has been intentionally left blank.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 9

At a glance

Income Tax

Changes in tax rates

Concessional corporate tax rate of 25% is now applicable to companies having turnover upto

Rs. 400 crores. The earlier turnover limit was Rs. 250 crores.

Super rich individuals having income in excess of Rs. 5 crores to be subjected to 42.74% tax

and those having incomes between Rs. 2 crores to Rs. 5 crores are to be pay tax @ 39%.

Provisions relating to widening and deepening of tax base

Individuals and HUFs not subjected to audit would be required to make TDS at the rate of

five percent on payments for personal or business use to resident contractors and

professionals if the quantum of payments exceed Rs. 50,00,000 in a year.

TDS on consideration for transfer of immovable property at the rate of 1% will also be

required to be deducted on other charges such as club membership, car parking fee, electricity

and water facility fees, maintenance fee etc.

Gifts of money or immovable properties situated in India by an Indian tax resident to a person

outside India shall be deemed to accrue or arise in India and taxable in India.

Persons having income below taxable limits but entering into following specified high value

transactions shall be mandatorily required to file income tax returns:

- On depositing Rs. 1 crore or more in one or more current account

- On incurring expenditure of Rs. 2 lacs or more on foreign travel of self or any other

person

- On incurring expenditure of Rs. 1 lacs or more on electricity bills

Also, persons having income below taxable limit but claiming rollover benefit of capital gains

exemption on investment in house or exemption bond etc. shall be mandatorily required to

file income tax return.

Persons who do not have PAN and enter into high value transactions may quote their Aadhar

in place of PAN and in such case PAN shall be allotted.

If PAN and Aadhar are linked, Aadhar can be used in lieu of PAN.

The ambit of furnishing statement of financial transactions [‘SFT’] is expanded and the

minimum threshold of Rs. 50,000 for reporting in SFTs is removed to facilitate data capturing

for generation of pre-filled income details in tax returns.

Measures to promote less cash economy

Various provisions under the Act which prohibit cash transactions and allow

payments/receipts only through account payee cheque/ bank draft or electronic clearing

system to also permit other prescribed electronic modes of payment.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 10

Businesses having annual turnover in excess of Rs. 50 crores are mandated to provide facility

for accepting payments through prescribed electronic modes.

Aggregate withdrawals in excess of Rs. 1 crore from a bank account in a year will be

subjected to TDS @ 2%.

Tax incentives

Incentives to businesses located in International Financial Services Centre

Following further tax incentives are provided to business carried on from International

Financial Services Centre –

- No capital gains tax on transfer of GDRs or Rupee denominated bond of an Indian

Company/derivative made by Category III Alternative Investment Fund if all unit holders

are non-residents;

- Apart from GDRs and Rupee denominated bonds, other specified securities to also

qualify for capital gains exemption.

- Interest payable to a non-resident by a unit located in IFSC to be tax exempt.

- Exemption from Dividend distribution tax to a company located in IFSC and deriving

income solely in convertible foreign exchange which is presently available on dividends

declared out of current incomes is extended to dividends declared out of accumulated

income.

- No additional income tax on income distributed by Mutual Funds located in IFSC if all

unit holders of such mutual fund are non-residents.

- Income of businesses located in IFSC to be 100% tax exempt for any ten consecutive

years out of fifteen years beginning from the year in which approval is obtained.

Incentives to Non-Banking Finance Companies

- Interest income in relation to bad and doubtful debts received by NBFCs shall be taxable

only in year in which it is actually received or credited to profit and loss account,

whichever is earlier.

- Interest payment on borrowing from NBFCs will be allowable as a deduction if it is

actually paid on or before the due date for filing of income tax return.

Incentive for electric vehicles – a deduction of Rs. 1,50,000 shall be allowed from total

income in respect of interest paid on loan taken for purchase of an electric vehicle.

Tax incentive for affordable housing – a deduction of Rs. 1,50,000 shall also be allowed in

respect of interest paid on loan taken from financial institution for purchase of residential

house property costing less than Rs. 45 lacs.

Incentives to subscribers of National Pension Scheme

- Receipts on closure of or on opting out of an NPS account shall now be exempt to the

extent of sixty percent of the total amount as against forty percent earlier.

- Contribution by the Central Government to the NPS account of its employees to the

extent of 14% of salary shall be eligible for deduction against the income of such

employees.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 11

- Any amount contributed by the Central Government employees to Tier II NPS account

shall be eligible for deduction against such employee’s income.

Incentives for start-ups

- Provisions relating to carry forward and set-off of unabsorbed losses of closely held

eligible start-ups have been rationalised.

- Roll-over benefit in respect of capital gains arising from transfer of residential property

would be available if the net consideration is invested in equity shares of start-ups and the

minimum shareholding/voting power is twenty five percent as against fifty one percent

earlier.

- When capital gains exemption is claimed for investment in start-ups, the lock in period of

five years on acquisition of computer/software purchased by start-ups is relaxed to 3

years.

Facilitating Resolution of Distressed Companies

Unabsorbed losses of distressed companies, their subsidiaries/ step down subsidiaries shall be

allowed to be carried forward and set off even if there is a change in the voting power or

shareholding where NCLT has suspended the Board of Directors and appointed new Directors

nominated by the Central Government and the change in shareholding has taken place

pursuant to resolution plan approved by NCLT.

Unabsorbed book profit and depreciation shall also be allowed to be reduced for calculating

the book profit for such companies.

Electronic filing process

An electronic filing and approval process is introduced for determination by the assessing

officer of the tax to be deducted at source on payments to non-residents.

An electronic filing system is also introduced for submissions of statement of transactions of

interest payment to residents on which no tax has been deducted at source.

Strengthening Anti-Abuse Measures

Buyback of shares from a shareholder by a company listed on recognised stock exchange

shall attract levy of additional income tax at the rate of twenty percent. Earlier similar

provision was applicable only to closely held companies. The consequential income arising

from buy back of shares by a company listed on recognised stock exchange shall be tax

exempt in the hands of shareholders.

The registration of a charitable Trust/ Institution for availing exemption of income may be

cancelled on violation of any other law which is material for the purpose of achieving the

objects of such Trust/ Institution.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 12

Removing difficulties faced by taxpayers

For defaults in deduction or deposit of TDS on payments to non-residents, a person shall be

liable to pay interest for the period after the recipient non-resident has filed its return,

disclosed such receipt and paid tax thereon.

The provisions relating to disallowance of expenditure on account of non-deduction of tax

shall not apply if the recipient non-resident has filed its return, disclosed such receipt and paid

tax thereon.

Clarification relating to assessment post filing of modified return of income in pursuance of APA

It has been clarified that in cases where assessment has been completed and modified return

of income has been filed in pursuance of an APA, the assessing officer shall only pass an

order modifying the total income of the relevant year in accordance with the APA.

Clarification relating to secondary adjustments

Amendments are introduced to align transfer pricing provisions with international best

practices in respect of secondary adjustment and for giving an option to the assessee to make

one-time payment for such adjustment.

TDS on non-exempt portion of life insurance pay-out on net basis

Non-exempt payments under a life insurance policy shall now be subject to TDS @ 5% on

income component embedded in such payment i.e. on gross amount as reduced by life

insurance premium paid.

Accounting year in respect of CbCR of an international group

The reporting accounting year for the purpose of Country by Country Report in case of an

alternate reporting entity of an international group, the parent entity of which is not resident in

India shall be the one applicable to such parent entity.

Information and documents to be maintained by a constituent entity of an international group

regardless of whether or not international transactions have been undertaken.

The information and documents are to be kept and maintained by a constituent entity of an

international group and filing of required form shall be mandatory even where there is no

international transaction undertaken by the constituent entity.

Penalty in case of under-reported income

Mechanism relating to determination of under-reported income and quantum of penalty has

been prescribed for cases where return is filed for the first time in response to reassessment

notices.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 13

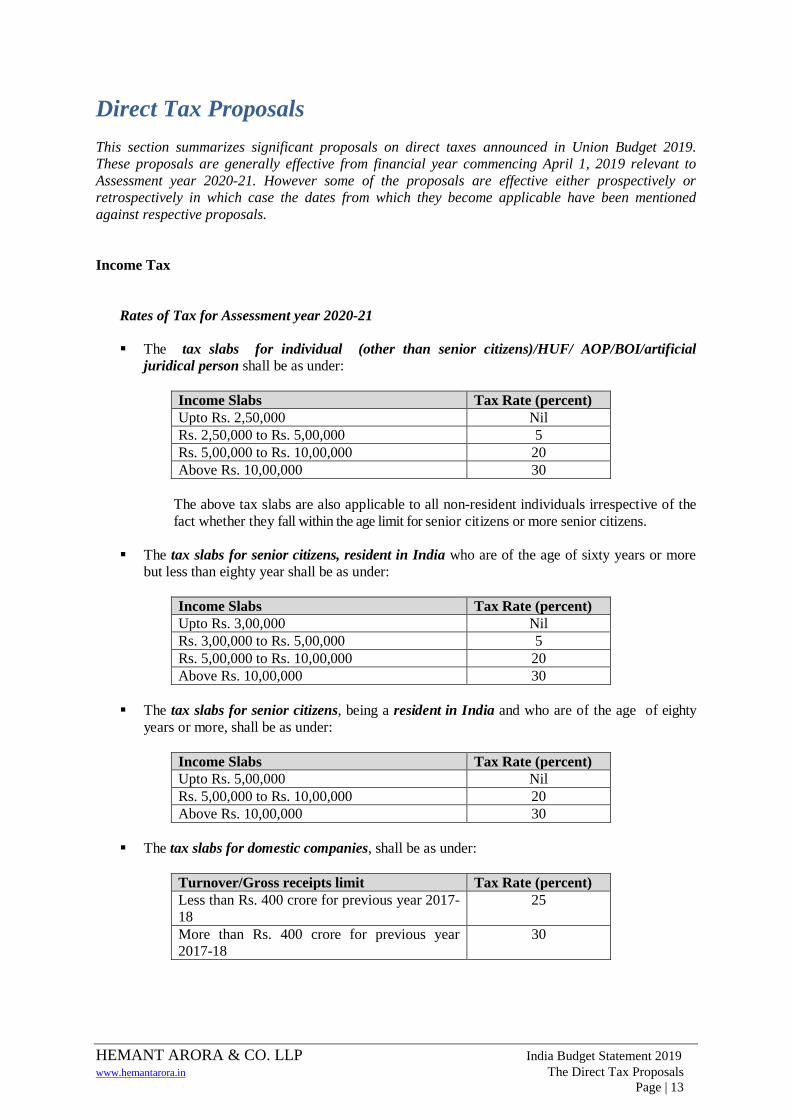

Direct Tax Proposals

This section summarizes significant proposals on direct taxes announced in Union Budget 2019.

These proposals are generally effective from financial year commencing April 1, 2019 relevant to

Assessment year 2020-21. However some of the proposals are effective either prospectively or

retrospectively in which case the dates from which they become applicable have been mentioned

against respective proposals.

Income Tax

Rates of Tax for Assessment year 2020-21

The tax slabs for individual (other than senior citizens)/HUF/ AOP/BOI/artificial

juridical person shall be as under:

Income Slabs Tax Rate (percent)

Upto Rs. 2,50,000 Nil

Rs. 2,50,000 to Rs. 5,00,000 5

Rs. 5,00,000 to Rs. 10,00,000 20

Above Rs. 10,00,000 30

The above tax slabs are also applicable to all non-resident individuals irrespective of the

fact whether they fall within the age limit for senior citizens or more senior citizens.

The tax slabs for senior citizens, resident in India who are of the age of sixty years or more

but less than eighty year shall be as under:

Income Slabs Tax Rate (percent)

Upto Rs. 3,00,000 Nil

Rs. 3,00,000 to Rs. 5,00,000 5

Rs. 5,00,000 to Rs. 10,00,000 20

Above Rs. 10,00,000 30

The tax slabs for senior citizens, being a resident in India and who are of the age of eighty

years or more, shall be as under:

Income Slabs Tax Rate (percent)

Upto Rs. 5,00,000 Nil

Rs. 5,00,000 to Rs. 10,00,000 20

Above Rs. 10,00,000 30

The tax slabs for domestic companies, shall be as under:

Turnover/Gross receipts limit Tax Rate (percent)

Less than Rs. 400 crore for previous year 2017-

18

25

More than Rs. 400 crore for previous year

2017-18

30

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 14

Surcharge on Individuals/ HUF/ AOP/ BOI/ artificial juridical person shall be levied:

Income Slabs Surcharge Rate (percent)

Exceeding Rs. 50,00,000 but less than Rs. 1,00,00,000 10

Exceeding Rs. 1,00,00,000 but less than Rs. 2,00,00,000 15

Exceeding Rs. 2,00,00,000 but less than Rs. 5,00,00,000 25

Exceeding Rs. 5,00,00,000 37

Surcharge on domestic companies having a total income exceeding Rs. 1,00,00,000 but less

than Rs. 10,00,00,000 shall continue to be levied at a rate of 7% and for total income

exceeding Rs.10,00,00,000/- will be levied at a rate of 12%.

Surcharge on foreign companies having a total income exceeding Rs. 1,00,00,000 but less

than Rs. 10,00,00,000 shall continue to be levied at a rate of 2% and for total income

exceeding Rs.10,00,00,000/- will be levied at a rate of 5%.

The Education Cess and the Secondary and Higher Education Cess shall be replaced by

the Health and Education Cess at the rate of 4%

Section 2 – Definitions

It is proposed that for tax-neutral demerger the condition stipulating that the resultant

company should record property and liabilities of the undertaking at the value appearing in

the books of accounts of the demerged company would not be applicable in the case of Ind

AS compliant companies.

Section 9 – Income deemed to accrue or arise in India

It is proposed that income arising from any sum of money paid for any property situated in

India transferred, on or after 5th July 2019 by a person resident in India to a person outside

India shall be deemed to accrue or arise in India.

Section 9A – Certain activities not to constitute business connection in India

The existing provisions provide for safe harbor in respect of offshore funds and accordingly

provide that for an eligible investment fund the mere fund management activity carried out in

India or through an eligible fund manager located in India shall by itself not constitute a

business connection in India. The existing provisions also provide that the eligible investment

fund shall not become resident in India merely because the fund manager is located in India.

The provisions are subject to certain conditions. It is proposed to relax certain conditions so

as to provide that (i) the corpus of fund shall not be less than Rs. 100 crore at the end of the

prescribed period and (ii) the remuneration paid to the eligible manager for fund management

activity is not less than the prescribed limited.

To apply retrospectively w.e.f. 1st April 2019.

Section 10 – Incomes not included in total income

It is proposed to provide that any income by way of interest payable to a non-resident by a

unit located in IFSC in respect of monies borrowed by it on or after 1st September 2019, shall

be exempt.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 15

It is proposed to increase the exemption limit for payment from NPS Trust to an assessee on

closure/opting out of pension scheme to 60% of the total amount (from existing 40%).

Section 13A – Special provisions relating to income of political parties

It is proposed to permit political parties to receive donation exceeding Rs. 2,000 by other

prescribed electronic modes in addition to the existing requirement of receiving such donation

in bank account.

Section 35AD – Deduction in respect of expenditure on specified businesss

It is proposed to amend the condition for allowing deduction of capital expenditure on

specified business which presently provides that such expenditure in excess of Rs. 10,000

should be paid only through banking channels to also allow payment for capital expenditure

by other prescribed electronic modes.

Section 40 – Amount not deductible

It is proposed to insert a new provision to provide that where an assessee fails to deduct tax

on any such sum but is not deemed to be an assessee in default because the payee has offered

the receipt as income and paid tax thereon, then it shall be deemed that the assessee has

deducted and paid the tax on such sum on date of furnishing of return of income by the payee

and no disallowance shall be made for reasons of non-deduction of TDS.

Further it is proposed to make the above concession available uniformly to resident and non-

resident assessees.

Section 40A – Expenses or payments not deductible in certain circumstances

It is proposed to amend the provision which disallows payments exceeding Rs. 10,000

otherwise than by account payee cheque/bank draft or ECS to permit other prescribed

electronic modes.

Section 43 – Definitions of certain terms relevant to income from profits and gains of business or

profession

It is proposed to amend the provision which provides that payment towards capital

expenditure in excess of Rs. 10,000 made otherwise than by account payee cheque/bank draft

or ECS shall not be included in actual cost of such asset, to also permit such payments by

other prescribed electronic modes.

Section 43B – Certain deductions to be only on actual payment

It is proposed to provide that interest expenditure on any loan or advances taken from a

deposit taking NBFC’s and systematically important non-deposit taking NBFC’s shall be

allowed as deduction if such interest is actually paid on or before the due date of furnishing

the return of income of the relevant previous year.

Section 43CA – Special provisions for full value of consideration for transfer of assessee other than

capital assets in certain cases

The said section provides that where the date of agreement fixing the value of consideration

for transfer of certain capital assets and the date of registration are different, the full value of

consideration shall be the stamp duty value on the date of agreement provided the

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 16

consideration is received by account payee cheque/demand draft of EC. It is proposed to

allow receipt of such consideration payments by other prescribed electronic modes.

Section 43D – Special provisions in case of income of public financial institutions, public

companies, etc.

It is proposed to provide that the interest income of deposit taking NBFCs and systematically

important non-deposit taking NBFCs interest income on bad or doubtful debits shall be

taxable in the year in which interest income is actually received or credited to profit and loss

account whichever is earlier.

Section 44AD – Special provisions for computing profits and gains of business on presumptive

basis

The said section allows a concessional presumptive taxation rate of 6% (as against 8%) to

eligible business if the turnover is received through account payee cheque/bank draft or ECS.

It is proposed to allow receipt of such consideration payments by other prescribed electronic

modes.

Section 47 – Transaction not regarded as transfer

It is proposed to amend the said section so as to provide that any transfer of a specified capital

by an Alternate Investment Fund, of which all the unit holders are non-resident, shall not be

regarded as transfer subject to fulfillment of specified conditions.

It is also proposed to widen the types of securities listed in said clause by empowering the CG

to notify other securities for the purposes of this clause.

Section 50C – Special provision for full value of consideration in certain cases

It is also proposed to include other prescribed electronic mode of payment in addition to the

already existing permissible mode i.e. account payee cheque/bank draft or ECS for the

purpose of receiving consideration for transfer of immovable property.

Section 50CA – Special provision for full value of consideration for transfer of share other than

quoted shares

The said section provides that where the consideration received on account of transfer of

unquoted shares is less than the fair market value of such share determined in such manner as

prescribed, such FMV shall be deemed to be full the value of consideration. It is proposed to

provide that this provision shall not apply to certain cases where consideration has been

approved by certain authorities.

Section 54GB – Capital gain on transfer of residential property not to be charged in certain cases

It is proposed to amend the section to allow further concessions in respect of roll over benefit

of capital gains arising from transfer of residential property which are presently available if

the net consideration is invested in equity shares of an eligible company (start-up). The

proposed amendments provide to (i) extend the sun set date of transfer of residential property

to 31st March 2020, (ii) relax the condition of minimum shareholding of fifty percent of share

capital/voting rights to twenty five percent, and (iii) relax the condition restricting transfer of

new computer/computer software from the current five years to three years.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 17

Section 56 – Income from other sources

The said section provides that where a closely held company issues shares to a resident at

value which is more than the fair market value of such shares the excess shall be chargeable

to tax. Exemption from this is presently provided to venture capital undertaking issuing shares

to venture capital company/fund or notified persons. It is proposed to extend the benefit of

exemption to Category II AIFs.

Section 79 – Carry forward and set off losses in case of certain companies

The said section restricts benefit of carry forward and set off of losses where any change in

shareholding takes place. It is proposed to provide that the benefit of carry forward and set off

of losses shall be available if the change in voting power or shareholding takes place pursuant

to a resolution plan approved under the IBC, 2016 subject to the condition that jurisdictional

Principal Commissioner or Commissioner is provided a reasonable opportunity of being

heard.

Section 80C – Deductions in respect of life insurance premia, deferred annuity, contributions to

PF, subscription to certain equity shares or debentures, etc

It is proposed to provide that any amount paid or deposited by a CG employee as a

contribution to his Tier II account of pension scheme shall be eligible for deduction.

Section 80CCD – Deductions in respect of contribution to pension scheme of CG

It is proposed to increase the deduction available to an employee on account of contribution

by CG/ other employer to the NPS to the extent of 14% of the contribution made by the CG.

(from present 10%).

Section 80EEA – Deduction in respect of interest on loan taken for certain house property

It is proposed to insert a new section to allow a deduction of upto Rs. 150,000 in respect of

interest paid on loan taken for residential house property from any financial institution subject

to the following conditions:

- Loan is sanctioned between 1st April 2019 and 31

st March 2020.

- the stamp duty value of house property does not exceed Rs. 45,00,000

- Assessee does not own any other residential house property on the date of sanction of

loan.

80EEB – Deduction in respect of purchase of electric vehicles

It is proposed to insert a new section to allow a deduction of upto Rs. 150,000 in respect of

interest paid on loan taken from any financial institution for purchase of electric vehicles

subject to the following conditions:

- Loan is sanctioned between 1st April 2019 and 31

st March 2023.

- Assessee does not own any other electric vehicle on the date of sanction of loan.

Section 80-IBA – Deduction in respect of profits and gains from housing projects

It is proposed to amend the conditions for deduction of income from developing and building

housing projects to provide that:

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 18

(i) the assessee shall be eligible for deduction under the section, in respect of a housing

project if a residential unit in the housing project has carpet area not exceeding 60 square

meter in metropolitan cities or 90 square meter in cities or towns other than metropolitan

cities of Bengaluru, Chennai, Delhi National Capital Region (limited to Delhi, Noida,

Greater Noida, Ghaziabad, Gurgaon, Faridabad), Hyderabad, Kolkata and Mumbai

(whole of Mumbai Metropolitan Region); and

(ii) the stamp duty value of such residential unit in the housing project shall not exceed Rs.

45,00,000

80 JJA – Deduction in respect of employment of new employees

The said section provides for deduction on account of additional employee cost incurred by

an assessee in the course of a specified business provided emoluments are paid by account

payee cheque/bank draft or ECS. It is proposed to also permit payment by other prescribed

electronic modes.

80 LA – Deduction in respect of certain incomes of Offshore Banking Units and International

Financial Services Center

It is proposed to amend the said section so as to provide that any transfer of a capital asset,

specified in the said clause by such AIF, of which all the unit holders are non-resident, are not

regarded as transfer subject to fulfillment of specified conditions.

It is also proposed to widen the types of securities listed in said clause by empowering the

Central Government to notify other securities for the purposes of this clause.

Section 92CD – Effect to Advance Pricing Agreement

It is proposed to clarify that in cases where assessment or reassessment has already been

completed and modified return of income is filed by the assessee in pursuance of an APA the

Assessing Officers shall pass an order modifying the total income of the relevant assessment

year determined in such assessment or reassessment, having regard to and in accordance with

the APA.

To apply w.e.f. 1st September, 2019.

Section 92CE – Secondary Adjustments in certain cases

The following amendments are proposed in provisions relating to carrying out secondary

adjustments where primary adjustment to transfer price has been made by the assessee suo

moto or has been made by the assessing office and accepted by the assessee or made under

APA/Safe harbor rules/MAP-

i) the condition of threshold of Rs. 1 crore and of the primary adjustment made upto

assessment year 2016-17 are alternative conditions;

ii) the assessee shall be required to calculate interest on the excess money or part

thereof;

iii) the provision of this section shall apply to the agreements which have been

signed on or after 1st April, 2017;

iv) the excess money may be repatriated from any of the non-resident AE of the

assessee;

v) in a case where the excess money has not been repatriated in time, the assessee

will have the option to pay additional income-tax at 18% on such excess money

in addition to the existing requirement of calculation of interest till the date of

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 19

payment of this additional tax. The additional tax is proposed to be increased by a

surcharge of 12%;

vi) the tax so paid shall be the final payment of tax and no credit shall be allowed;

vii) the deduction in respect of which such tax has been paid, shall not be allowed

under any other provision;

viii) if the assessee pays the additional income-tax, he shall not be required to make

secondary adjustment or compute interest from the date of such payment.

The amendments listed in para (i) to (iv) above will apply retrospectively from the 1st

April, 2018 and the amendments listed in para (v) to (viii) above will be effective from 1st

September, 2019.

Section 92D – Maintenance of keeping work and keeping information and document by persons

entering into an International Transaction [or Specified Domestic Transaction]

It is proposed to provide that the information and documents which are required to be

maintained by a constituent entity of an international group and also forms that are required to

be filed shall have to be maintained/filed even where there is no international transaction

undertaken by such constituent entity.

Section 111A – Tax on Short Term Capital Gain on certain cases

It is proposed to provide the concessional rate of tax for STCG with respect to transfer of

units of funds setup for disinvestment of CPSE’s.

Section 115A – Tax on dividends, royalty and technical service fees in the case of foreign

companies

It is proposed that the units in an IFSC earning income in the form of dividend, royalty and

fees for technical service are allowed to claim full deduction u/s 80LA.

Section 115JB – Special Provision for payment of tax by certain companies

It is proposed that for distressed companies where any change in voting power or

shareholding takes place pursuant to a resolution plan approved under the IBC, 2016 the

aggregate amount of unabsorbed depreciation and loss (excluding depreciation) brought

forward shall be allowed to be reduced for computing the book profits.

Section 115-O – Tax on distributed profits of Domestic Companies

It is proposed to provide that any dividend paid out of accumulated income derived from

operations in IFSC, after 1st April, 2017 shall also be exempt from dividend distribution tax as

against the earlier provision which provided exemption from DDT to only dividend paid out

of its current income .

Section 115QA – Tax on distributed income to shareholders

It is proposed to extend the applicability of provisions which provide for levy of additional

income tax @ 25% of the distributed profit on account of buy back of shares to all companies

including the companies listed on a recognized stock exchange.

Section 115R – Tax on distributed income to Unit holders

To incentivize relocation of mutual funds in an IFSC it is proposed to provide that no

additional income-tax shall be chargeable on amount of income distributed by a Mutual Fund

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 20

on or after 1st September 2019 provided all its unit holders are non-residents and subject to

certain other conditions.

Section 115UB – Tax on income of Investment Fund and its unit holders

It is proposed to make following amendments in provisions relating to treatment of losses of

investment funds

- the business loss of an investment fund shall be allowed to be carried forward and it shall

not be passed onto the unit holder;

- loss other than business loss shall also not be considered for the purposes of pass through

to its unit holders if such loss has arisen in respect of a unit which has not been held by

the unit holder for a period of at least 12 months;

- the loss other than business loss, accumulated at the level of investment fund as on 31st

March, 2019, shall be deemed to be the loss of a unit holder who held the unit on said

date;

- the loss so deemed in the hands of unit holders shall not be available to the investment

fund for the purposes of set off and carry forward.

Section 139 – Return of Income

It is proposed to provide that that a person shall be mandatorily required to file a return of

income, irrespective of whether or not he has taxable income, if he enters into any of the

following transactions:

- Deposits Rs. 1 crore or more in one or more current account

- Incurs an expenditure of Rs. 2 lacs or more on foreign travel of self or any other person

- Incurs an expenditure of Rs. 1 lacs or more on electricity bills

It is further proposed to provide that a person claiming exemption in respect of capital gain

income, shall necessarily be required to furnish a return.

Section 139A – Permanent account number

It is proposed to provide that every person who is required to quote his PAN but has not been

allotted a PAN may quote Aadhaar number in lieu of PAN.

It is further proposed to provide that every person who has been allotted a PAN, and who has

linked his Aadhaar number to PAN may quote his Aadhaar number in lieu of a PAN,

It is further proposed to cast duty upon the person receiving any document relating to

specified transactions to ensure that PAN or Aadhaar number is duly quoted.

To apply w.e.f. 1st September, 2019.

Section 139AA – Quoting of Aadhaar number

It is proposed to provide that if a person fails to intimate the Aadhaar number in the Income

tax return, the PAN allotted to such person shall be made inoperative.

Section 140A – Self-Assessment

It is proposed to allow relief with respect to arrears of salary for the purpose of determining

final tax liability.

To apply retrospectively w.e.f. 1st April, 2007.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 21

Section 143 – Assessment

This section provides that the income tax liability would be computed after allowing credit for

prepaid taxed and certain reliefs, credits, etc. where the relief with respect to arrears of salary

was not specifically mentioned. It is now proposed to provide that computation of tax liability

shall be made after giving benefit of relief with respect to arrears of salary.

Section 194DA – Payment in respect of life insurance policy

It is proposed to provide TDS @ 5% on the income component (as against TDS on gross

amount earlier) embedded in payment of taxable amounts under the life insurance.

Section 194-IA – Payment on transfer of certain immovable property other than agricultural land

A clarificatory amendment is proposed to provisions relating to TDS on transfer of

immovable property to provide that the term “consideration for immovable property” on

which TDS is required to be made shall include all charges of the nature of club membership

fee, car parking fee, electricity and water facility fees, maintenance fee, advance fee or any

other charges of similar nature, which are incidental to transfer of the immovable property for

the purpose of levy of TDS @ 1%.

Section 194M – Payment of certain sums by certain individual or certain HUFs

It is proposed to cast an obligation on those individuals and HUFs who are not required to get

their accounts audited to deduct TDS at the rate of 5% on the payments exceeding Rs. 50 lacs

made for contractual work or professional fees whether such payments are for personal use or

business purposes.

It is further proposed that such individuals and HUFs shall be able to deposit TDS using PAN

and shall not be required to obtain TAN.

Section 194N – Payment of certain amounts in cash

It is proposed to provide for levy of TDS at the rate of 2% on cash withdrawals in excess of

Rs. 1 crore during the year from a bank account.

The aforesaid proposed amendment also provides exemption from TDS on cash withdrawals

by Government, banking company, certain cooperative society, post office, banking

correspondents and white label ATM operators.

Section 195 – Payment to non-residents

It is proposed to introduce an online process for making an application to the assessing officer

for determination of TDS rate for making payments to non-residents. It is also proposed to

make the approval process online.

Section 197 – Certificate for deduction at lower rates

It is proposed to provide that the sums on which TDS has been deducted u/s 194M (as defined

above) shall also be eligible for certificate for deduction at lower rate.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 22

Section 201 – Consequences of failure to deduct or pay

It is proposed that deductor shall not be deemed to be an assessee in default for failure to

make TDS while making payment to a non-resident if such non-resident has furnished his

return of income and disclosed such payment for computing his income. It is further proposed

that interest for TDS default on such payments shall be restricted till the date of filing of tax

return by the non-resident payee.

Section 206A – Furnishing of statement in respect of payment of any income to residents without

deduction of tax

It is proposed to introduce online electronic filing of statement in respect interest payments to

residents made without TDS.

Section 228A – Recovery of tax in pursuance of agreements with foreign countries

It is proposed to provide for recovery of tax as per treaty obligation with the other country in

cases where details of property of the person, resident in India are not available.

It is further proposed to provide for tax recovery, where details of property of an assessee in

default under the Act are not available but the said assessee is a resident in a foreign country.

Section 234A/234B/234C – Interest Liability

It is proposed to allow relief in respect of arrears salary for the purpose of computing interest

for delayed payment of tax or delayed filing of tax return.

Section 239 – Form of claim for refund and limitations

It is proposed to provide that for every person claiming refund of tax furnish of return of

income shall be sufficient compliance for the purpose.

Section 269SU – Acceptance of payment through prescribed electronic modes

It is proposed to provide that every person whose total sales/turnover/gross receipts in

business exceeds Rs.50 crores shall provide facility for accepting payment through prescribed

electronic modes.

Section 269SS/269ST/269T – Mode of payment/repayments/acceptance of undertaking specified

transactions

It is proposed to provide that where payment/repayment of loans/deposit are to be made by

account payee cheque/bank draft or ECS, other prescribed electronic modes shall also be

allowed for such transactions. Similar amendment is also proposed in provision which

prohibits receiving Rs. 2 lacs or more in any mode other than cheque/bank draft or ECS.

Section 270A – Penalty for under-reporting and misreporting of income

It is proposed to provide manner of computing the quantum of penalty in a case where the

person has under-reported income and furnished his return for the first time during the course

of reassessment proceedings.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 23

Section 271DB – Penalty for failure to comply with provisions of Section 269SU

It is proposed to provide that the penalty of Rs. 5,000 per day shall be imposed in case a

person whose total sales/turnover/gross receipts in business exceeds Rs.50 crores and who

fails to provide facility for receipt through prescribed electronic modes. However, such

penalty shall not be imposed where the person proves that there were good and sufficient

reasons for such failure.

Section 271FAA – Penalty for quoting inaccurate statement of financial transaction

It is proposed to widen the scope of penalty by covering all entities required to furnish SFT.

Section 272B – Penalty for failure to comply with provisions of Section 139A

It is proposed to impose penalty of Rs 10,000 for quoting false Aadhaar number in any

document.

Section 285BA – Obligation to quote statement of financial transaction

It is proposed to expand the scope of furnishing of statement of financial transactions by

including certain prescribed persons to the existing list of persons.

It is further proposed to remove the threshold of Rs.50,000 on aggregate value of transactions

during a financial year required for furnishing of STFs.

It is further proposed that in case defects in the statement of financial transactions are not

rectified within the period of 30 days or such further period so allowed, it shall be treated that

such person had furnished inaccurate information in the statement and consequential penalty

shall be levied.

Section 286 – Quoting of report in respect of International group

It is proposed that the accounting year for the purpose of CbCR in case of an alternate

reporting entity resident in India whose parent entity is not resident in India, shall be the one

applicable to such parent entity.

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 24

Glossary

Act The Income Tax Act, 1961 (except as otherwise stated)

AAR Authority for Advance Ruling

AIF Alternate Investment Fund

AO Assessing Officer

ALP Arm’s Length Price

AMT Alternate Minimum Tax

AOP Association of Persons

APA Advance Pricing Agreement

AY Assessment Year

BOI Body of Individuals

CbCR Country by Country Report

CBDT Central Board of Direct Taxes

DDT Dividend Distribution Tax

DRP Dispute Resolution Panel

DTAA Double Tax Avoidance Agreement

EPFO Employees’ Provident Fund Organization

EPF & MP Act Employees’ Provident Funds & Miscellaneous Provision Act, 1952

FMV Fair Market Value

FPC Farm Producer Companies

GAAR General Anti Avoidance Rules

GDP Gross Domestic Output

HUF Hindu Undivided Family

ICDS Income Computation and Disclosure Standards

IFSC International Financial Services Centre

IPR Intellectual Property Rights

LLP Limited Liability Partnership

MAT Minimum Alternate Tax

NBFC Non-Banking Finance Company

NELP New Exploration Licensing Policy

PE Permanent Establishment

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 25

POEM Place of Effective Management

RBI Reserve Bank of India

SEBI Securities and Exchange Board of India

SEZ Special Economic Zone

SME Small & Medium Enterprises

SPV Special Purpose Vehicle

TCS Tax Collected at Source

TDS Tax Deducted at Source

TPO Transfer Pricing Officer

TRC Tax Residency Certificate

VCC Venture Capital Company

VCF Venture Capital Funds

VCU Venture Capital Undertaking

HEMANT ARORA & CO. LLP India Budget Statement 2019

www.hemantarora.in The Direct Tax Proposals

Page | 26

www.hemantarora.in