34

Charting A New Path To Purchase: Shopper Communication In A Digital Age A markedly less than 3 hour tour…. Bryan Gildenberg Chief Knowledge Officer 1 OR….

Charting A New Path To Purchase:

Shopper Communication InA Digital Age

A markedly less than 3 hour tour….

Bryan GildenbergChief Knowledge Officer

1

OR….

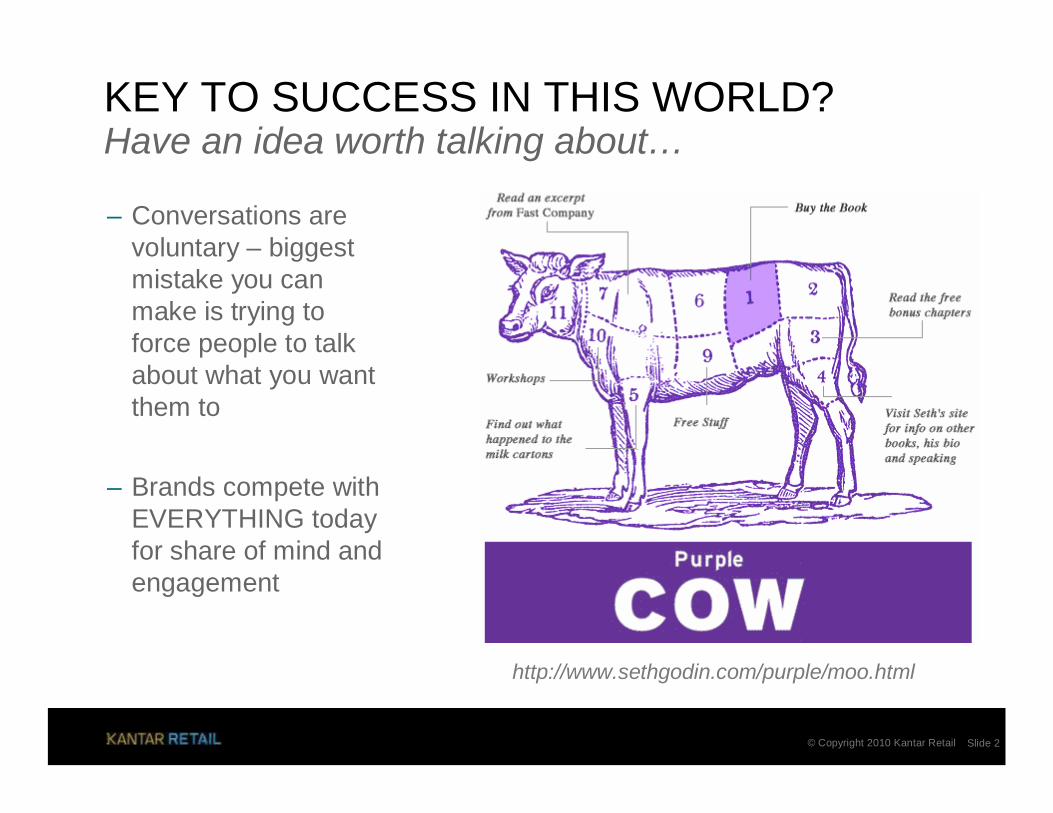

KEY TO SUCCESS IN THIS WORLD?

– Conversations are voluntary – biggest mistake you can make is trying to force people to talk about what you want them to

– Brands compete with EVERYTHING today for share of mind and engagement

Have an idea worth talking about…

© Copyright 2010 Kantar Retail Slide 2

http://www.sethgodin.com/purple/moo.html

Name # of Fans 10 Starbucks 16,222,51215 Coca-Cola 15,562,24018 Victoria's Secret 14,806,29722 Converse 13,924,39726 Oreo 12,423,87728 Skittles 11,751,09535 Red Bull 10,452,69843 Disney 8,866,20461 iTunes 7,294,50384 ZARA 6,171,05985 Pringles 5,977,43095 iPod 5,721,758101 Starburst 5,535,141109 Nutella 5,363,911110 Dr Pepper 5,348,538121 Monster Energy 5,139,716122 Harry Potter 5,120,497133 Adidas Originals 4,946,309150 H&M 4,616,948152 Reese's 4,586,376153 Ferrero Rocher 4,579,902189 McDonald's 3,962,718194 PlayStation 3,896,381220 Xbox 3,600,651221 God 3,580,345222 Walt Disney World 3,579,409

Everyone should spend an hour looking at this whole list…fascinating! But, top cpg/retail brands in terms of fb fan #s

© Copyright 2010 Kantar Retail Slide 4

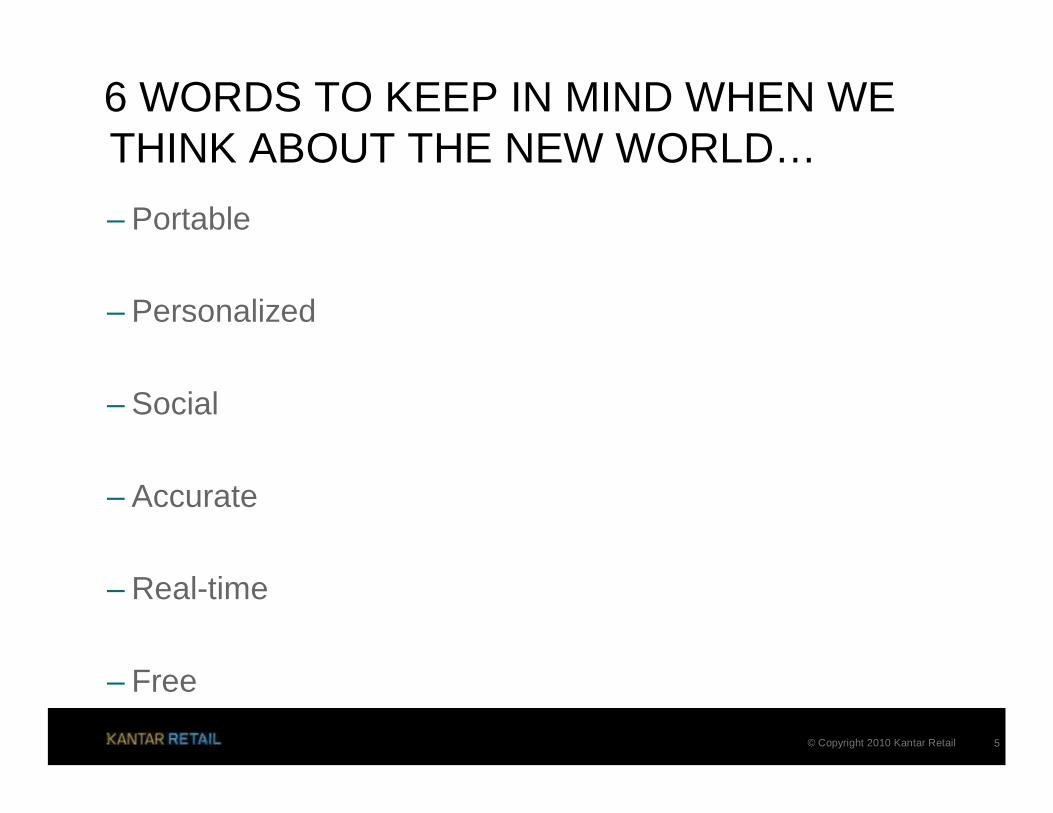

6 WORDS TO KEEP IN MIND WHEN WE THINK ABOUT THE NEW WORLD…– Portable

– Personalized

– Social

– Accurate

– Real-time

– Free

© Copyright 2010 Kantar Retail 5

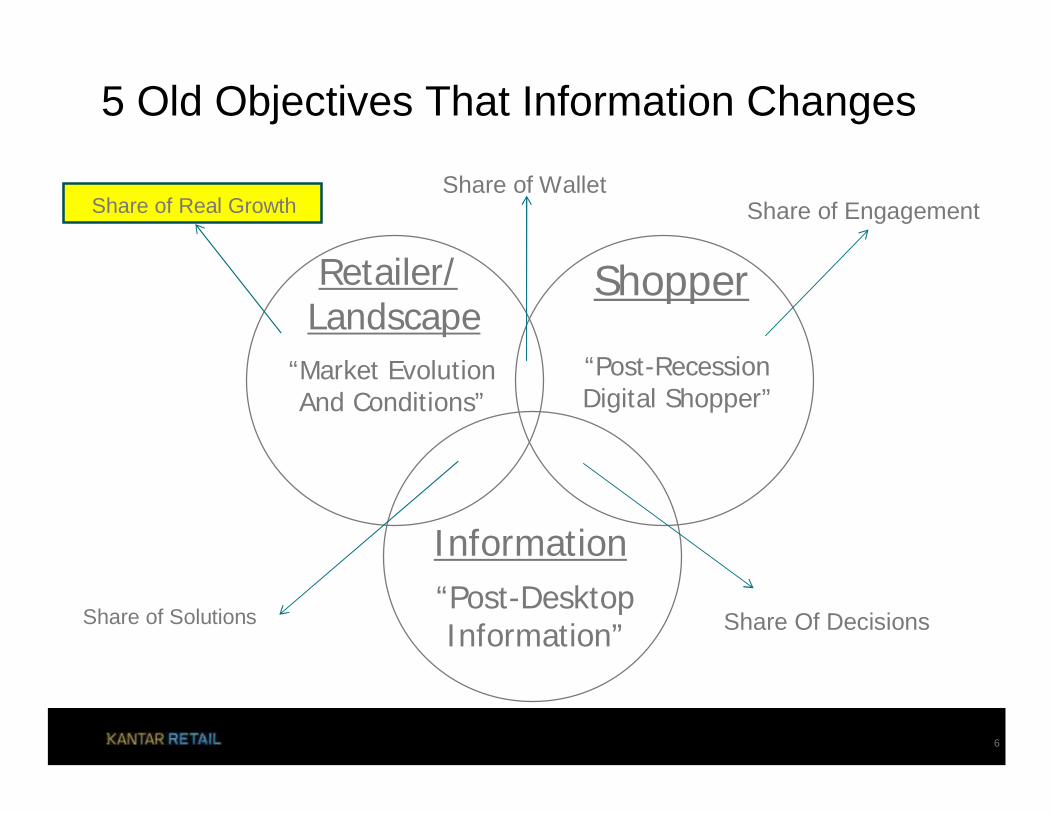

5 Old Objectives That Information Changes

6

“Market Evolution And Conditions”

“Post-Desktop Information”

Information

Retailer/ Landscape

Shopper

“Post-Recession Digital Shopper”

Share Of DecisionsShare of Solutions

Share of WalletShare of Real Growth Share of Engagement

5 KEY CONSUMER/SHOPPER INSIGHTS

– Boomers lost half of their net worth in 5 years in the USA

– Gen Y is growing up digital, broke and on your couch

– Price sensitivity won’t be time constrained• Busy people can be sharp price shoppers

– Shoppers can increasingly find exactly what they are looking for

– Price is becoming increasingly personal and non-public

7

Channel CAGR'05-'10E

CAGR'10E-'15E

Clubs 4.8% 6.1%

Category Specialist 0.4% 4.1%

Convenience 2.6% 3.3%

Department -3.1% 2.6%

Discounter 7.7% 7.3%

Drug 5.6% 4.8%

Supercenter 7.5% 4.4%

Mass Merch (no SC) -2.6% -1.2%

Non-Store Retail 8.9% 11.3%

Supermarket 2.3% 3.7%

MVI Channel Totals 2.7% 4.5%

US Sales by Format: Fragmenting Growth :

9115699

122160

20283

94

107

42

48

56

394

401

491117

157

420312 349

60119

105

319

256179

40

58110

92

0

300

600

900

1,200

1,500

1,800

2,100

2005 2010E 2015E

Clubs

Category Specialist

Convenience

Department

Discounter

Drug

Supercenter

Mass Merch (no SC)

Non-Store Retail

Supermarket

Source: MVI-Insights.com

$1,470$1,680

$2,088USD Billions

8

75% of growth from WMT, Supermarket, Drug

New Growth Equation:Club + Discount + Online > Sctr, Smkt, Drug (exRX)

BEST WAY TO MANAGE SHARE OF REAL GROWTH? PROACTIVE CHANGE

“It’s much easier to change when you plan to, rather than when you have to. It costs less. You have more time”

-Paul Otellini, CEO Intel

9

“It Takes A Village” To Earn New Growth…

10

– Core areas of stress-testing• Does our company kill low performing SKUs BEFORE our

customers?

• Can we understand what happens if we DON’T do something, not just if we do?

• Are we really prepared for a world where Walmart is 10% of US retail and 8% of US retail growth?– And where 50% of the growth is coming from formats that make us

uncomfortable?

• Key words – cross-functional, pro-active, risk-embracing

Source: KR analysis

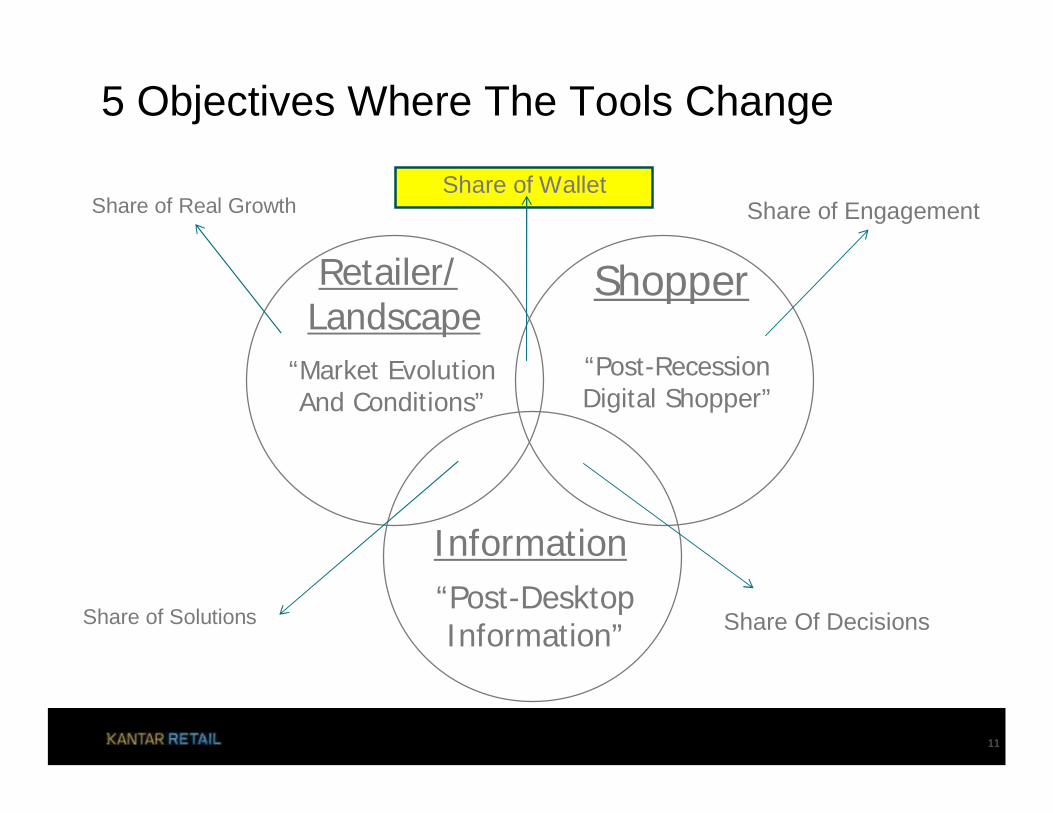

5 Objectives Where The Tools Change

11

“Market Evolution And Conditions”

“Post-Desktop Information”

Information

Retailer/ Landscape

Shopper

“Post-Recession Digital Shopper”

Share Of DecisionsShare of Solutions

Share of WalletShare of Real Growth Share of Engagement

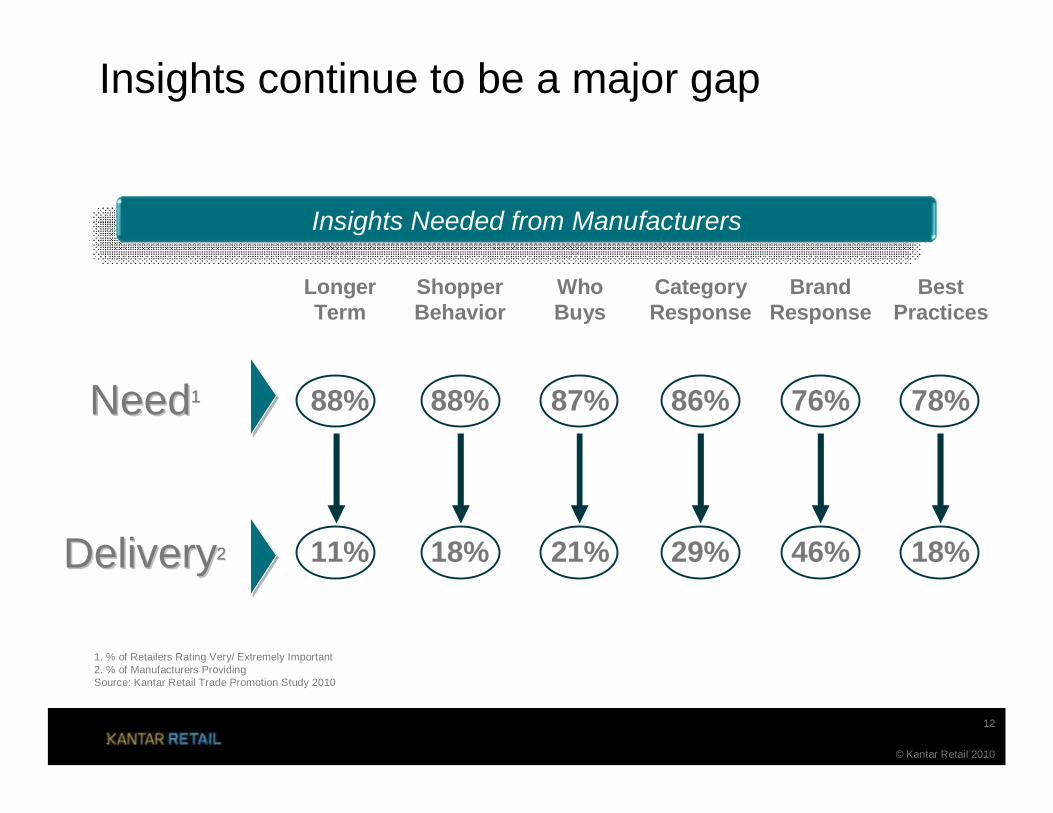

Insights continue to be a major gap

1. % of Retailers Rating Very/ Extremely Important2. % of Manufacturers ProvidingSource: Kantar Retail Trade Promotion Study 2010

Insights Needed from Manufacturers

NeedNeed11

DeliveryDelivery22

© Kantar Retail 2010

12

Longer Term

Shopper Behavior

Who Buys

Category Response

Brand Response

Best Practices

88% 88% 87% 86% 76% 78%

11% 18% 21% 29% 46% 18%

Share of Wallet: Kantar Retail Key CompetencyAnalytics 3.0– Shopper insights

• Justifying cost of the retailer data sets and making it pay off• What will companies do to develop the capability to get great insights?• Ensuring these insights turn into something – the physical manifestation of great ideas• Bigger, whole-store oriented solutions

– Trade spend and promotions – “mutually assured destruction”• Defensible• ROI focused• The blurring of the line between brand and trade – it’s all marketing

– Activating great ATL campaigns in-store/online

• Gap between shelf price and average selling price• MFR funding greater share of promotions in EUR• EUR retailers looking to develop non-promo centric formats• Clearer visuals on promotion

– The increasingly customized and private conversation between retailer and shopper

• More intense public domain/statement pricing• Targeted and more intense promotions – CFR showing 60% off LC promos in Portugal

6-13

Setting Standard for Online MerchandisingPersonalization, Recommendations, 1-Click, Sort Your Way

14

Source: Company website, Kantar Retail analysis

• #1 retailer & #25 company on Inc magazines list of 500 fastest growing companies

• Key traffic driver is free shipping & next day delivery (70% of US)– 2005-2007 built backend

infrastructure, 3 warehouses…marketing 2008+

– Diapers key to every-day relationship with shopper, margin on other items

• Soap.com launched with over 25,000 items– Plans for 40,000 SKUs by end 2010– 100,000 by end 2011

Diapers.com: A Big Success for QuidsiLeverage Distribution Infrastructure for Soap

15

Founded

Source: Kantar Retail analysis, Company websites

Soap.com: Founders of Diapers.com Go After the Broader Replenishment Trip

16

Source: Kantar Retail analysis, Company websites

Once It’s On a List, How Do You Break Thru and Change the Replenishment Purchase?

• Supplier challenge: – Today: how do I get on the list

NOW– Tomorrow: Once shopper makes

the list, how do I break-in and stimulate trial?

• Retailer challenge: – What is the impact on the store if

my core trip drivers move online? – What is the new category role?

17

• As more categories move online, easily becomes replenishment purchase – driven by shopper convenience & retailers aggressively driving these new business models

Source: Kantar Retail analysis, Company websites

War for wallet share: implications

– Core areas of stress-testing• If our customers don’t care

about market share, how will we?

• Can we have a conversation with our best customers about how they will sell more to their most profitable shoppers?

• What tools/vehicles work?

– Core alignment changes• Category growth will

change to category conversion

• Growth stories will need to detail “how” we are going to grow – who is going to buy more? Why?

• 100% ACV becomes an interesting objective here…

© Kantar Retail 201018

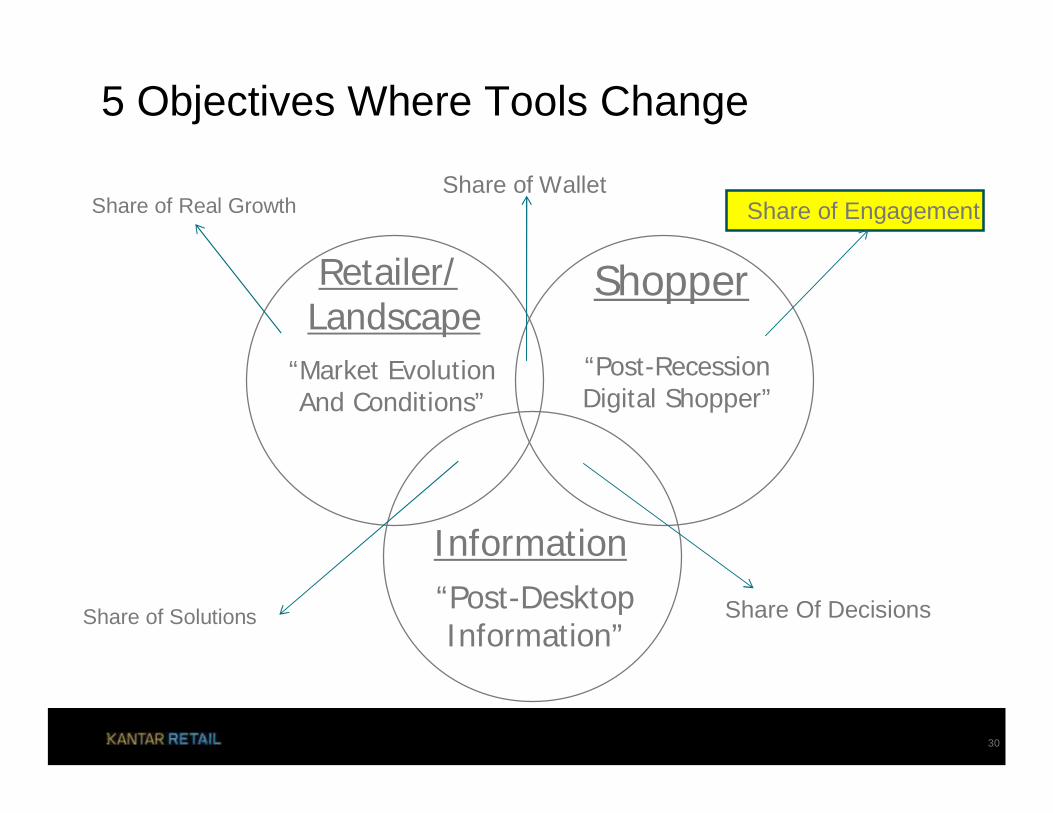

5 Objectives Where Tools Change

19

“Market Evolution And Conditions”

“Post-Desktop Information”

Information

Retailer/ Landscape

Shopper

“Post-Recession Digital Shopper”

Share Of DecisionsShare of Solutions

Share of WalletShare of Real Growth Share of Engagement

20

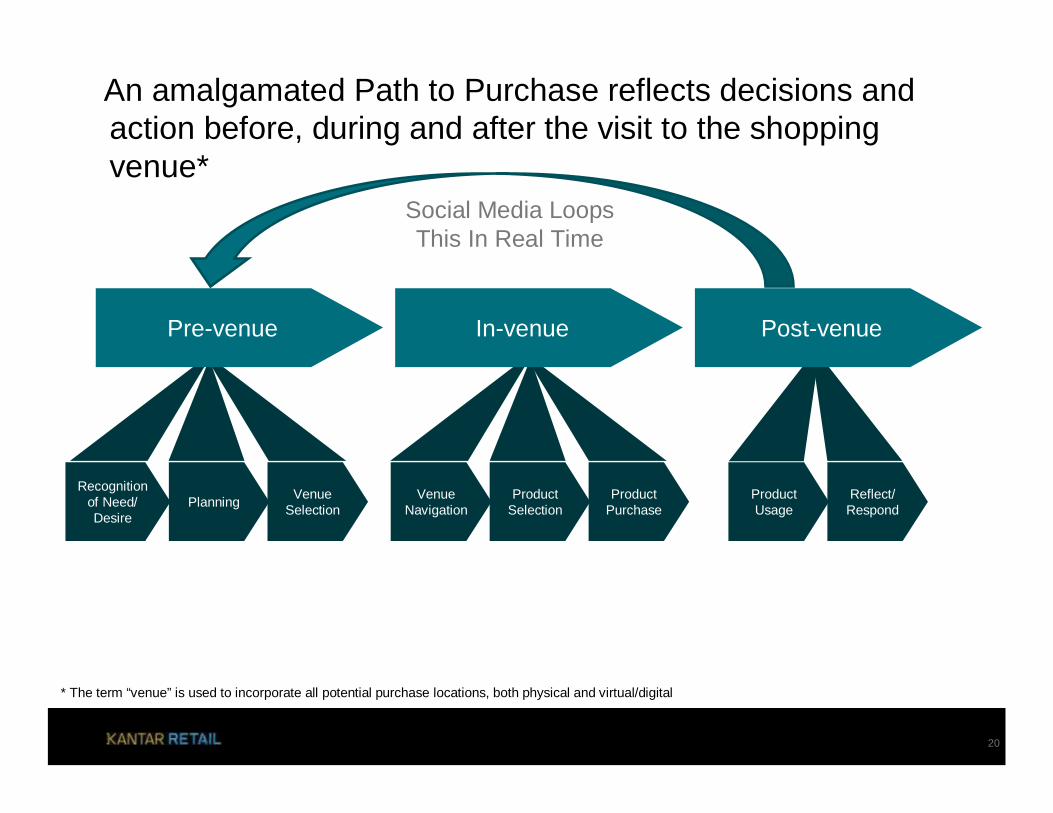

An amalgamated Path to Purchase reflects decisions and action before, during and after the visit to the shopping venue*

Pre-venue In-venue Post-venue

* The term “venue” is used to incorporate all potential purchase locations, both physical and virtual/digital

Recognition of Need/ Desire

Planning Venue Selection

Venue Navigation

Product Selection

Product Purchase

Product Usage

Reflect/ Respond

Social Media Loops This In Real Time

What Happens to Price-Oriented Retailers When They Don’t Own Price Anymore?

21Source: mysupermarket.co.uk

www.mysupermarket.co.uk

– Moments of Truth - July 1, 2010 – CMO Summit, Chicago

– Jim LecinskiManaging Director of U.S. SalesGoogle, Inc.

– From delivering substantial sales margins to earning market share, marketers can drive success for their organizations by understanding where and when purchase decisions are actually made. But knowing is not enough—marketers need to define, adopt, and act on a set of operating principles to make the most of these insights. In his session, Jim Lecinski will propose an actionable framework for connecting with consumers at the "Zero Moment of Truth" and making the most of these highly-profitable engagements.

Companies Preparing For The Zero Moment… Are You?

22

Emotion

Interaction

Web Advertising

TV

Source: dmg world media, http://www.youtube.com/watch?v=3wLuA9tPFfE&feature=related

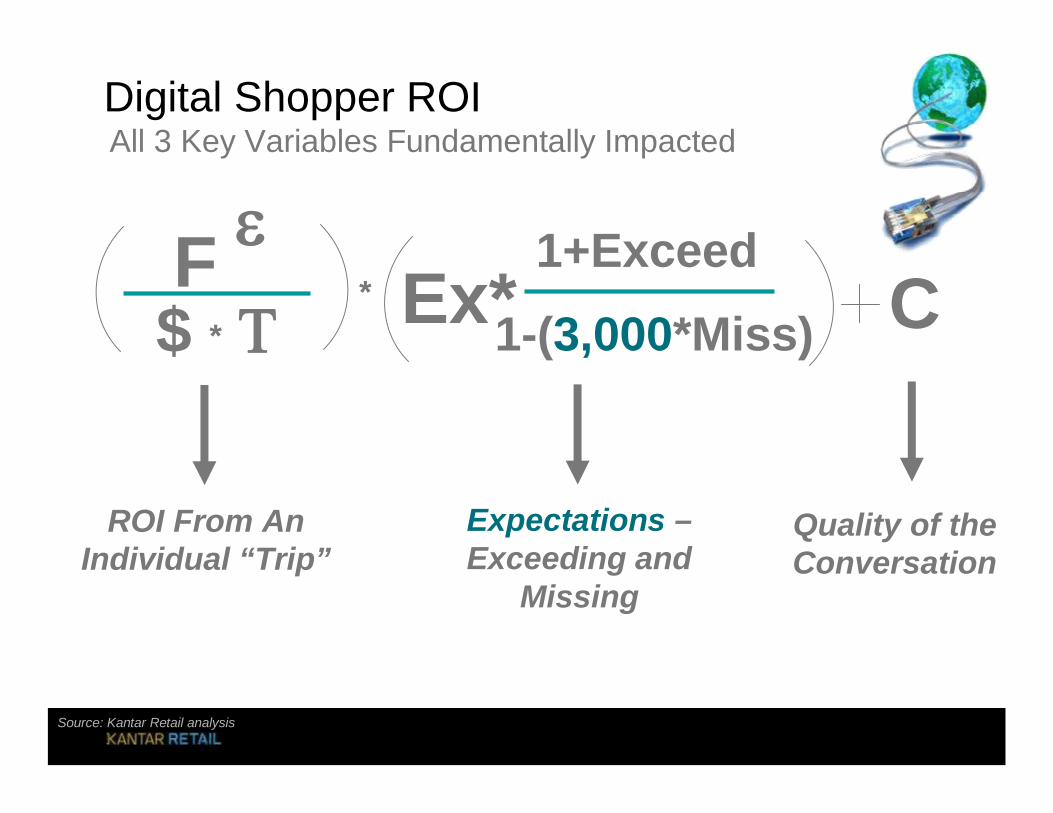

Digital Shopper ROIAll 3 Key Variables Fundamentally Impacted

$ * F * Ex*

1+Exceed

1-(3,000*Miss) C

ROI From An Individual “Trip”

Expectations –Exceeding and

Missing

Quality of the Conversation

Source: Kantar Retail analysis

Share of Decision: Kantar Retail Key CompetenciesMapping and Blazing The New Path To Purchase

– Gen Y and how they will shop• Replacing the boomers with something very, very different• Blurring backwards of the path to purchase • There will in the long term be an increasing separation between

the engagement, inspiration and persuasion of the consumer and inventory

• Efforts to understand the digital impact on the path to purchase• IMPRESSION-ENGAGEMENT-ACTION steps and • Zero moment of truth conversation

– How does a wired world enable different strategies?• Branding and strategy while giving up control• Disruptive competitive models in commerce and information

6-24

– Core areas of stress-testing• Is our biggest issue

irrelevance, not competition?

• How do our customers remain vital parts of the conversation? How do we help them (and yes, we want to help them!)?

• What does a joint conversation look like?

– Core alignment changes• Customer marketing will

become more digital and buzz-oriented

• Brand attributes are more important than brand executions

• How do we reliably measure decision influence? Do we want our brands to be loved or trusted?

War for Decision Share: Implications:“If You Don’t Like Change, You’re Going To Like Irrelevance Even Less”

-General Eric Shinseki

25Source: KR analysis

5 Objectives Where Tools Change

26

“Market Evolution And Conditions”

“Post-Desktop Information”

Information

Retailer/ Landscape

Shopper

“Post-Recession Digital Shopper”

Share Of DecisionsShare of Solutions

Share of WalletShare of Real Growth Share of Engagement

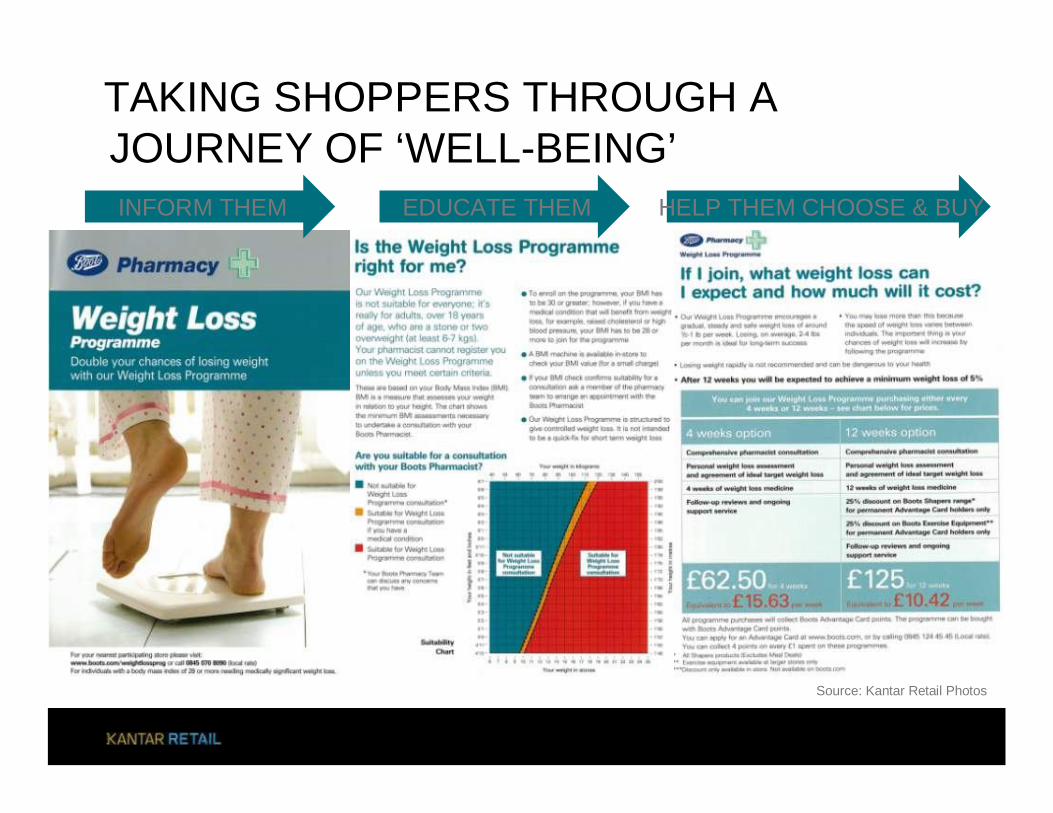

TAKING SHOPPERS THROUGH A JOURNEY OF ‘WELL-BEING’INFORM THEM EDUCATE THEM HELP THEM CHOOSE & BUY

Source: Kantar Retail Photos

28

This Is Solution Share....

Source: MVI photo Tesco Hompelus and Dobbies website

War for solution share: implications

– Core areas of stress-testing• Our customers will become

less concerned with our products – what does this mean to us?

• How do we partner with customers tackling these “bigger issues”?

• What does a multi-channel supply chain look like?

– Core alignment changes• Supply chain flexibility will be

as important as efficiency and cost

• Senior sales leaders will be having really different conversations with customer senior management• Someone has to make

sure the top to top isn’t just about saving the world!

• Realization that fewer, bigger ideas may be required to get noticed

29

5 Objectives Where Tools Change

30

“Market Evolution And Conditions”

“Post-Desktop Information”

Information

Retailer/ Landscape

Shopper

“Post-Recession Digital Shopper”

Share Of DecisionsShare of Solutions

Share of WalletShare of Real Growth Share of Engagement

Would You Have Guessed These Would Be Top Search Items for Walgreens?

31

4 TIPS FROM AN EXCELLENT PRACTITIONER

We don't have a logo," says Dmitri Siegel, executive director ofmarketing for Urban Outfitters. "We don't have a style guide. We

have a spirit.“

– Know who you want to be your friends.– Be a good listener. This point goes hand-in-hand with another point

Dmitri often makes - stop talking about yourself so much. – Ask good questions. Part of being a good listener is asking good

questions, and your customers' answers can inspire your brand long after the question is forgotten.

– Focus on connections, not on numbers. The more connected your customer base is with each other, he says, the better the experience and stronger the community.

Slide 32© Copyright 2010 Kantar Retail

Key Words

– Real Growth: This may look expensive and/or uncertain, but real growth will increasingly come from uncomfortable places

– Wallet Share: Focus energy on how my communication can convert occasionals to loyalists

– Decisions: When in doubt, frame the strategy around a decision you need to influence or want to change

– Solutions: Expand your communication to be a more holistic solution – how can you “improve lives” better?

– Engagement: Fun, humor, offbeat – remember, Skittles has more fans than God does

33

Bryan GildenbergChief Knowledge [email protected]: b bryang_kr

245 First StreetFloor 10Cambridge, MA02142

T +1 617 588 4124C +1 617 512 2866F +1 617 499 2723www.mvi-insights.com

Slide 34© Copyright 2010 Kantar Retail