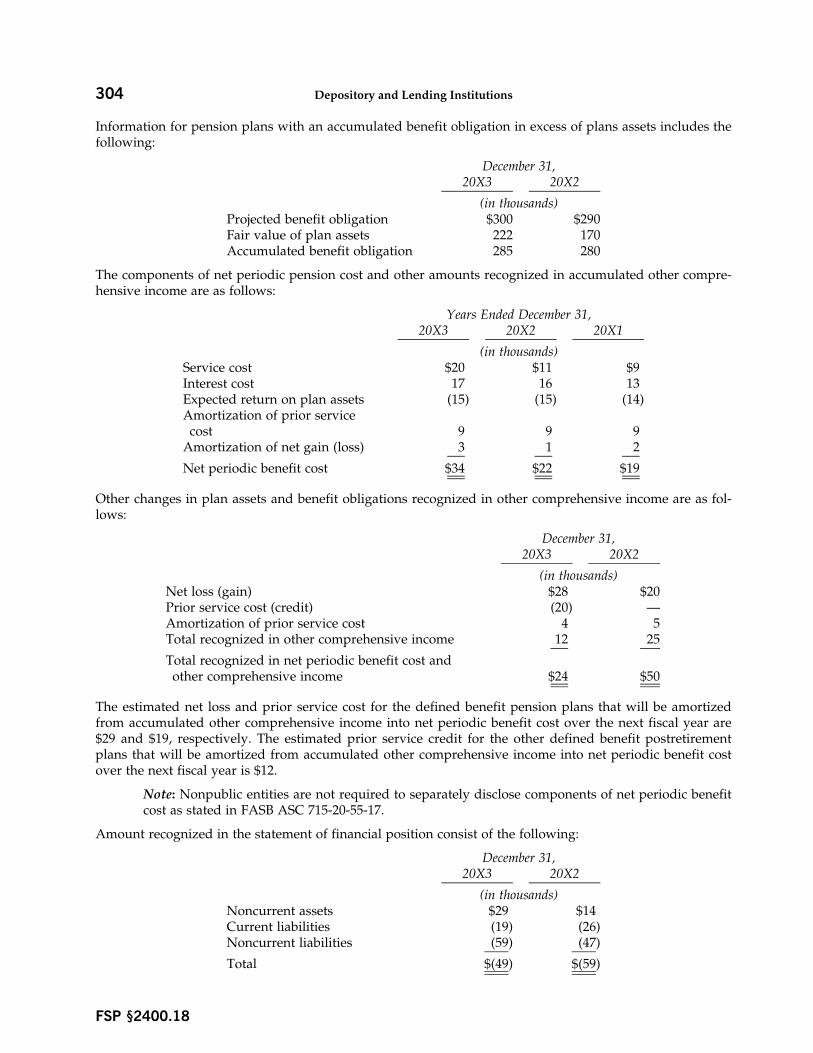

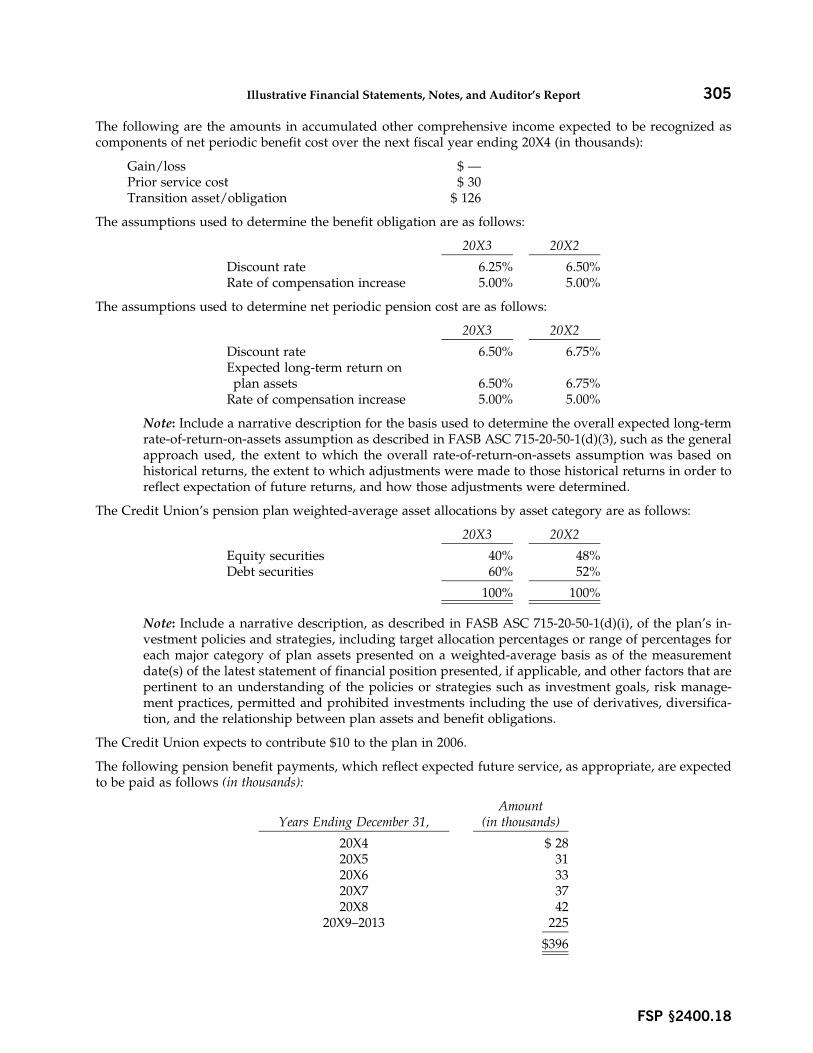

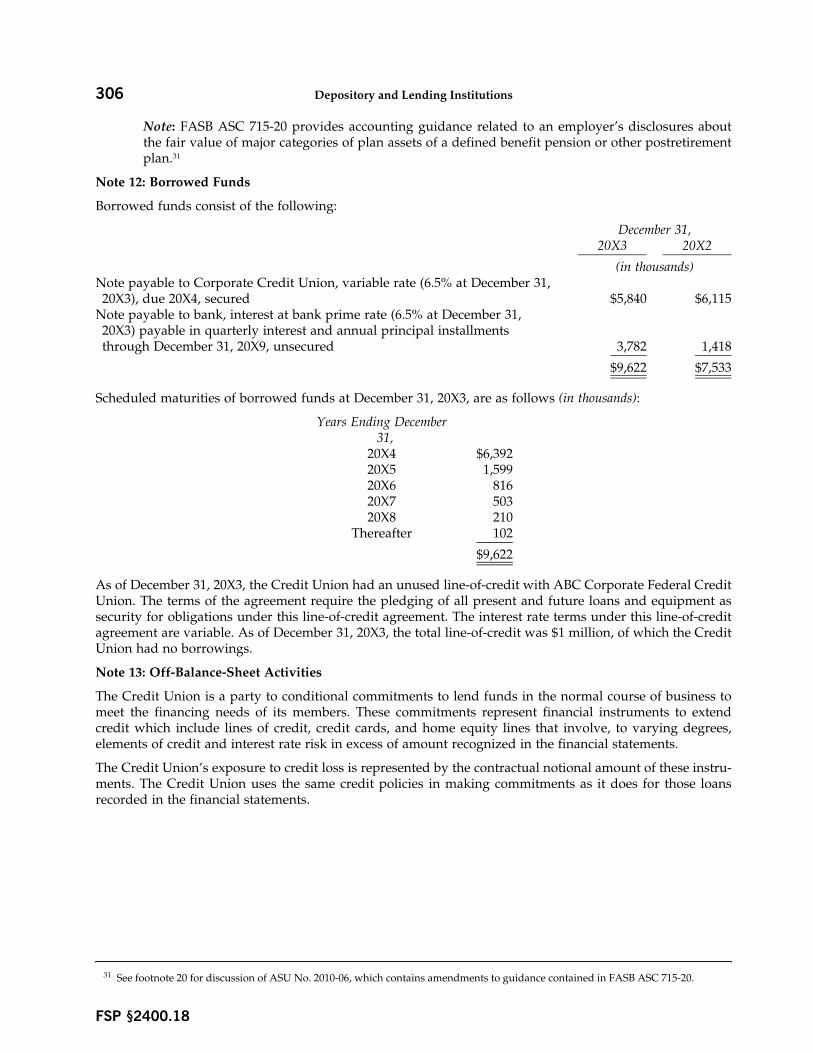

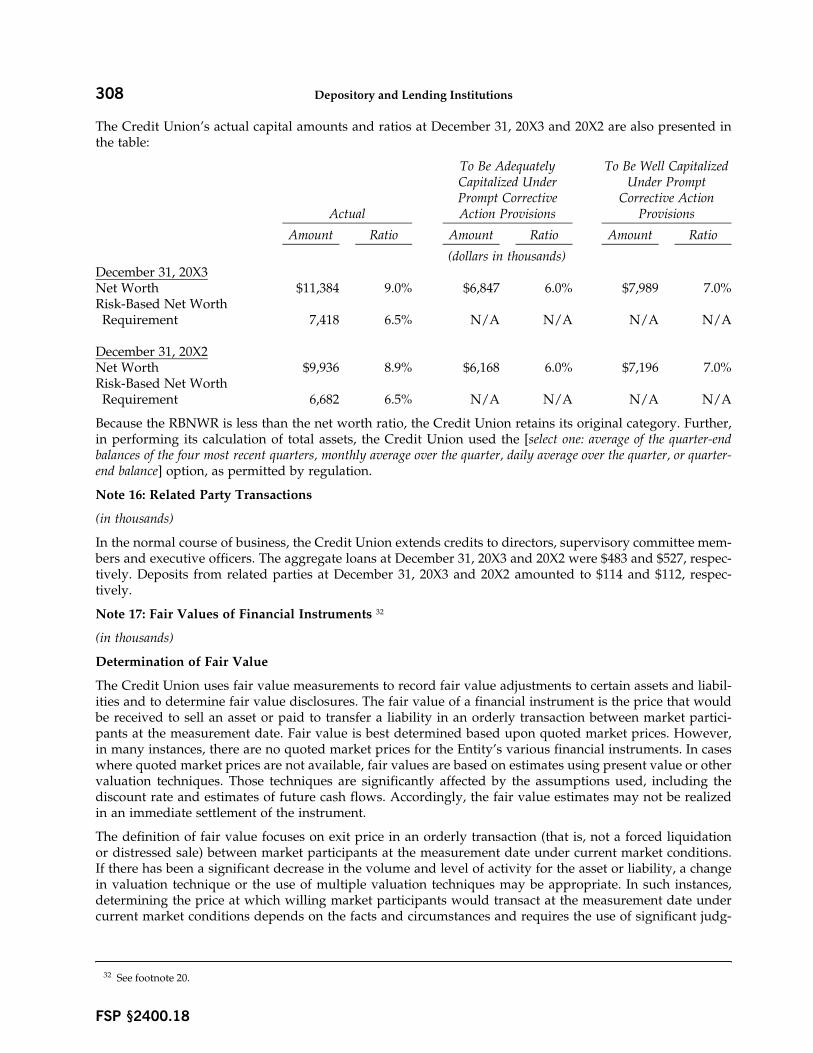

University of Mississippi University of Mississippi eGrove eGrove Industry Guides (AAGs), Risk Alerts, and Checklists American Institute of Certified Public Accountants (AICPA) Historical Collection 2010 Checklists and illustrative financial statements : Depository and Checklists and illustrative financial statements : Depository and lending institutions, September 2010 edition lending institutions, September 2010 edition American Institute of Certified Public Accountants (AICPA) Follow this and additional works at: https://egrove.olemiss.edu/aicpa_indev Part of the Accounting Commons, and the Taxation Commons Recommended Citation Recommended Citation American Institute of Certified Public Accountants (AICPA), "Checklists and illustrative financial statements : Depository and lending institutions, September 2010 edition" (2010). Industry Guides (AAGs), Risk Alerts, and Checklists. 1145. https://egrove.olemiss.edu/aicpa_indev/1145 This Book is brought to you for free and open access by the American Institute of Certified Public Accountants (AICPA) Historical Collection at eGrove. It has been accepted for inclusion in Industry Guides (AAGs), Risk Alerts, and Checklists by an authorized administrator of eGrove. For more information, please contact [email protected].

Transcript

University of Mississippi University of Mississippi

eGrove eGrove

Industry Guides (AAGs), Risk Alerts, and Checklists

American Institute of Certified Public Accountants (AICPA) Historical Collection

2010

Checklists and illustrative financial statements : Depository and Checklists and illustrative financial statements : Depository and

lending institutions, September 2010 edition lending institutions, September 2010 edition

American Institute of Certified Public Accountants (AICPA)

Follow this and additional works at: https://egrove.olemiss.edu/aicpa_indev

Part of the Accounting Commons, and the Taxation Commons

Recommended Citation Recommended Citation American Institute of Certified Public Accountants (AICPA), "Checklists and illustrative financial statements : Depository and lending institutions, September 2010 edition" (2010). Industry Guides (AAGs), Risk Alerts, and Checklists. 1145. https://egrove.olemiss.edu/aicpa_indev/1145

This Book is brought to you for free and open access by the American Institute of Certified Public Accountants (AICPA) Historical Collection at eGrove. It has been accepted for inclusion in Industry Guides (AAGs), Risk Alerts, and Checklists by an authorized administrator of eGrove. For more information, please contact [email protected].

All rights reserved. Checklists and sample documents contained herein may be reproduced and distributed as part of professional services or within the context of professional practice, provided that reproduced materials are not in any way directly offered for sale or profit. For information about the procedure for requesting permission to make copies of any part of this work, please visit www.copyright.com or call (978) 750-8400.

1 2 3 4 5 6 7 8 9 0 AAP 1 9 8 7 6 5 4 3 2 1

ISBN 978-0-87051-947-5

iii

TABLE OF CONTENTS

PAGE

FSP 2000—Checklists and Illustrative Financial Statements for Depository and Lending Institutions:Banks and Savings Institutions, Credit Unions, and Mortgage Companies .................................. 1

Letter to Customers ............................................................................................................. 1

General .............................................................................................................................. 1

FSP 2300—Supplemental Information for Depository and Lending Institutions That Are Securities andExchange Commission Registrants ........................................................................................... 213

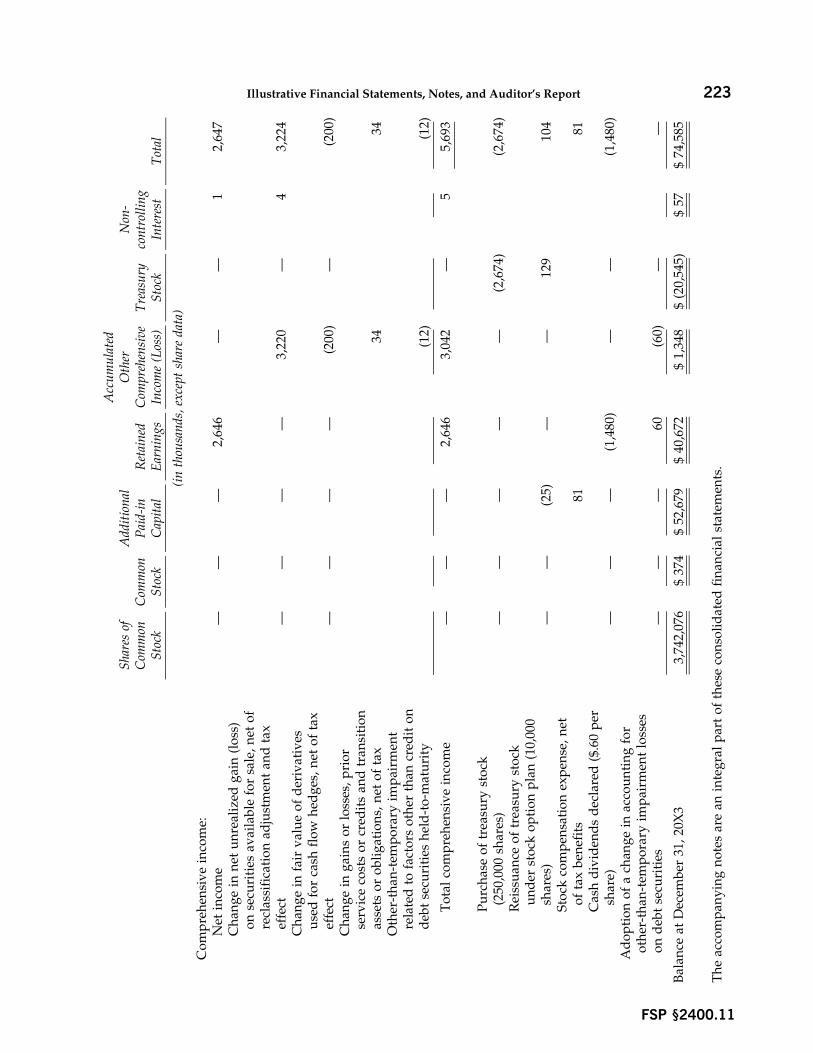

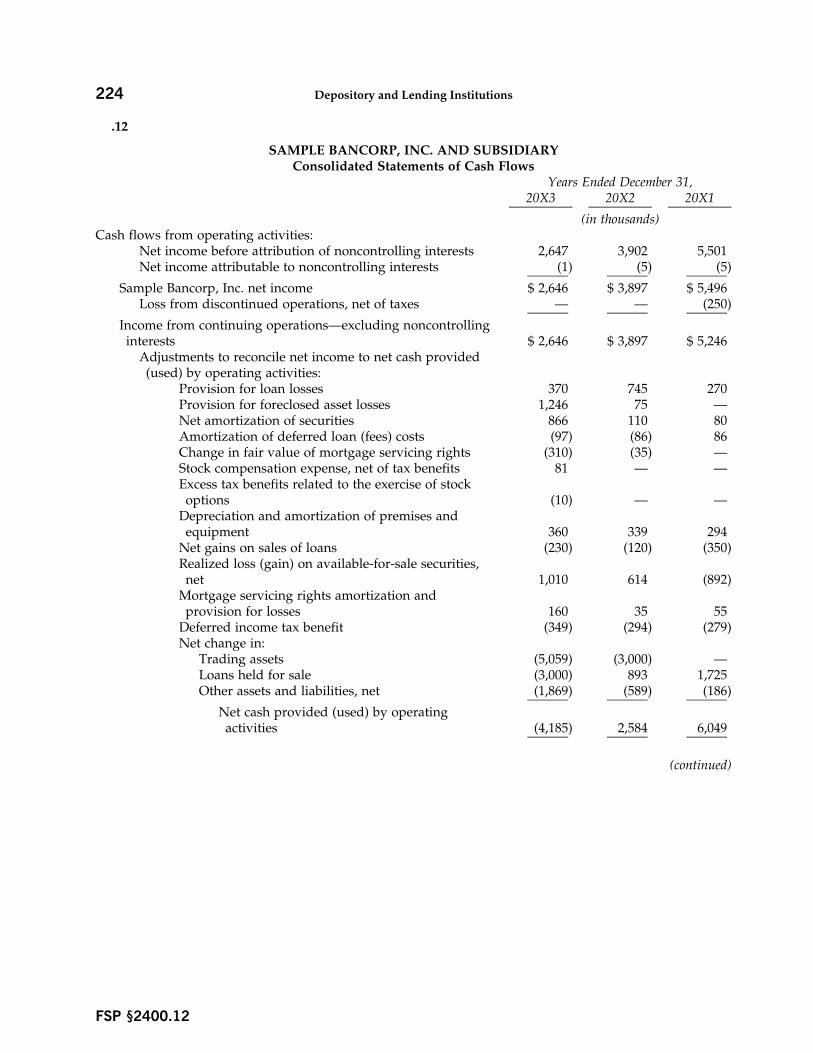

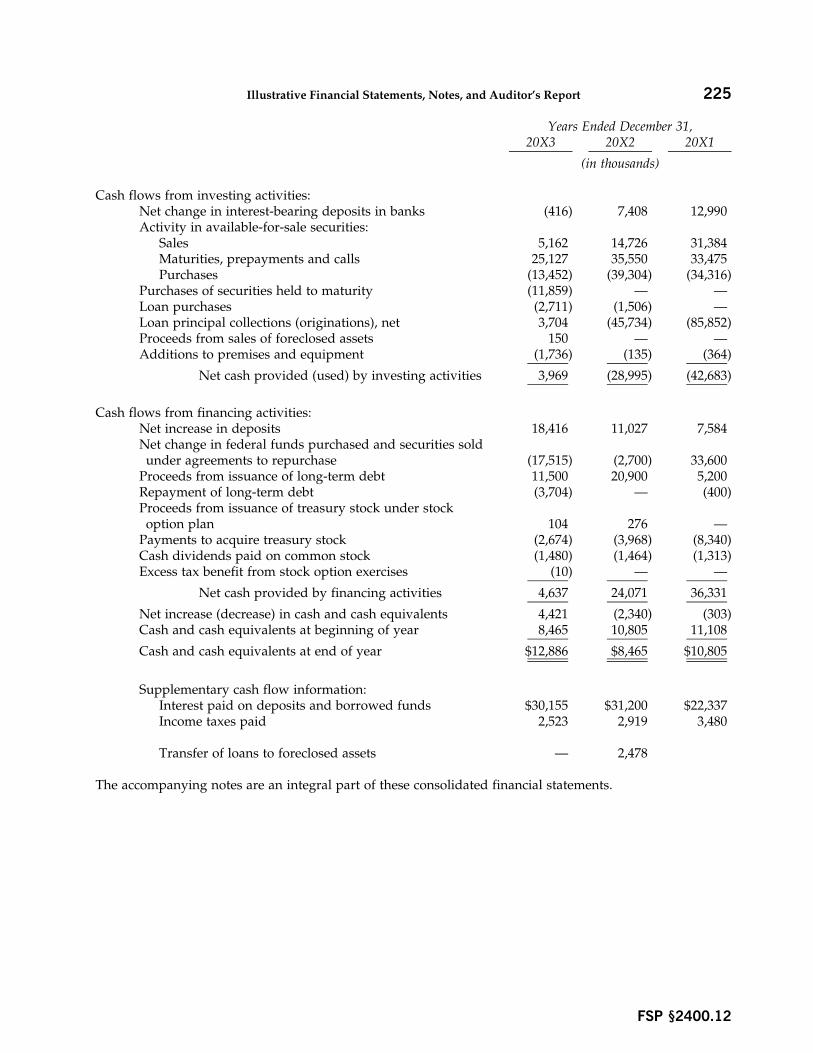

FSP 2400—Illustrative Financial Statements, Notes, and Auditor’s Report ....................................... 215

Illustrative Financial Statements for Banks and Savings Institutions ........................................ 217

Illustrative Financial Statements for Credit Unions ................................................................ 284

Illustrative Financial Statements for Mortgage Companies ..................................................... 313

1Checklists and Illustrative Financial Statements for Depository and Lending Institutions

FSP §2300.01

FSP Section 2000

Checklists and Illustrative FinancialStatements for Depository and LendingInstitutions: Banks and Savings Institutions,Credit Unions, and Mortgage Companies

Letter to Customers

Dear Valued Customer,

The following checklists and illustrative materials have been developed by the AICPA Accounting and Au-diting Publications Staff to serve as nonauthoritative practice aids for use by preparers of financial state-ments and by practitioners who audit, review, or compile financial statements. The auditor’s and account-ant’s report checklists address those requirements most likely to be encountered when reporting on financialstatements of a depository and lending institution prepared in conformity with U.S. generally accepted ac-counting principles.

Relevant financial statement reporting and disclosure guidance issued through December 31, 2010, has beenconsidered in the development of this edition of the checklist. The accounting guidance in this checklist hasbeen conformed to reflect reference to FASB Accounting Standards Codificatione as it existed on December 31,2010.

Any guidance issued subsequent to December 31, 2010, has not been included in this checklist; therefore, ifyour entity has a fiscal year-end after December 31, 2010, you need to consider the applicability of suchguidance. In determining the applicability of newly issued guidance, its effective date also should be consid-ered.

We hope you find this checklist helpful as you perform your audit and compilation and review engage-ments. We would greatly appreciate your feedback on this checklist. You may e-mail these comments toA&[email protected] or write to

A&A PublicationsAICPA

220 Leigh Farm RoadDurham, NC 27707-8110

General

.01 This publication includes the following information:

● Financial Statements and Notes Checklist (FSP section 2100)—For use by preparers of financialstatements and by practitioners who audit them as they evaluate the adequacy of disclosures.

● Auditors’ Report Checklist (FSP section 2200)—For use by auditors in reporting on auditedfinancial statements.

2 Depository and Lending Institutions

FSP §2300.02

● Supplemental Information for Depository and Lending Institutions That Are Securities and

Exchange Commission Registrants (FSP section 2300)—For use by auditors of Securities andExchange Commission (SEC) registrants.

.02 This checklist is intended to be used in connection with engagements of nonpublic institutions andis not intended to be used in connection with audits of public entities that are required to be audited understandards established by the Public Company Accounting Oversight Board (PCAOB).

.03 These checklists and illustrative materials have been developed by the AICPA Accounting and Au-diting Publications staff to serve as nonauthoritative practice aids for use by preparers of financial state-ments and by practitioners who audit them. The auditor’s and accountant’s report checklists address thoserequirements most likely to be encountered when reporting on financial statements of a depository andlending institution prepared in conformity with accounting principles generally accepted in the UnitedStates (U.S. GAAP). They do not include reporting requirements relating to other matters such as internalcontrol or agreed-upon procedures. The financial statement and notes checklist includes disclosure consid-erations applicable to depository and lending institutions in preparing financial statements in conformitywith U.S. GAAP.

.04 Users of the financial statements and notes checklist should remember that it is a disclosure checklistonly and not a comprehensive U.S. GAAP application or measurement checklist. Accordingly, applicationand measurement issues related to preparing financial statements in conformity with U.S. GAAP are notincluded in the checklist.

.05 The checklists and illustrative financial statements should be used by, or under the supervision of,persons having adequate technical training and proficiency in the application of U.S. GAAP, generally ac-cepted auditing standards, and other relevant technical guidance.

.06 The AICPA Accounting and Auditing Publications staff has included guidance from the FinancialAccounting Standards Board (FASB) Accounting Standards Codificatione (ASC) as it existed on December 31,2010. Questions are derived primarily from the content of the “Presentation” (section 45) and “Disclosure”(section 50) sections of FASB ASC. The AICPA Accounting and Auditing Publications staff has includedpresentation and disclosure items deemed most likely to be encountered when reporting on the financialstatements of a depository and lending institution prepared in conformity with U.S. GAAP. Thus, not allparagraphs of the “Presentation” and “Disclosure” sections of FASB ASC have been included. Users shouldevaluate whether circumstances exist for which the relevant presentation and disclosure guidance is notprovided in these checklists and illustrative materials and refer directly to FASB ASC as appropriate. Thesechecklists and illustrative materials note significant areas for which “Presentation” and “Disclosure” para-graphs were deemed too specific for this general publication and, where noted, users are urged to consultFASB ASC as necessary.

.07 In some cases, this checklist uses the terms Additional Presentation Information and Additional Disclo-sure Information to further illustrate an item. In such cases, the information contained under those headingscontinues to be authoritative guidance and is included to further clarify a presentation or disclosure require-ment or to add useful information

.08 In some cases, this checklist uses the term Encouraged, but not required. In such cases, although thereis no authoritative guidance to support such a disclosure for nonpublic entities, it has become a commonpractice that such disclosures are made. Entities should evaluate whether such items warrant disclosure intheir financial statements.

.09 Relevant financial statement reporting and disclosure guidance issued through December 31, 2010,has been considered in the development of this edition of the checklist. This includes relevant guidanceissued up to and including the following:

● FASB Accounting Standards Updates issued through December 31, 2010

● Statement on Auditing Standards No. 120, Required Supplementary Information (AICPA, Profes-sional Standards, AU sec. 558)

3Checklists and Illustrative Financial Statements for Depository and Lending Institutions

FSP §2300.13

● Interpretation No. 4, “Appropriateness of Identifying No Significant Deficiencies or No MaterialWeaknesses in an Interim Communication,” of AU section 325, Communicating Internal ControlRelated Matters Identified in an Audit (AICPA, Professional Standards, AU sec. 9325 par. .11–.13)

● Statements on Standards for Attestation Engagements No. 16, Reporting on Controls at a ServiceOrganization (AICPA, Professional Standards, AT sec. 801)

● Interpretation No. 8, “Including a Description of Tests of Controls or Other Procedures, and theResults Thereof, in an Examination Report,” of AT section 101, Attest Engagements (AICPA, Pro-fessional Standards, AT sec. 9101 par. .70–.72)

● Interpretation No. 16, “Preparation of Financial Statements for Use by an Entity’s Auditors,” ofAR section 80, Compilation of Financial Statements (AICPA, Professional Standards, AR sec. 9080par. .61-.62)

.10 Any guidance issued subsequent to December 31, 2010, has not been included in this checklist; there-fore, if your entity has a fiscal year-end after December 31, 2010, you need to consider the applicability ofsuch guidance. In determining the applicability of newly issued guidance, its effective date should also beconsidered.

.11 These checklists contain numerous references to accounting and auditing guidance. Abbreviationsand acronyms used in such references include the following:

AAG-DEP5 Audit and Accounting Guide Depository and Lending Institutions: Banks and Sav-ings Institutions, Credit Unions, Finance Companies and Mortgage Companies (newedition as of June 1, 2010)

AR5 Reference to a section number in AICPA Professional Standards for compilationand review standards

AT5 Reference to a section number in AICPA Professional Standards for Statements onStandards for Attestation Engagements

AU5 Reference to a section number in AICPA Professional Standards for U.S. auditingstandards that are applicable to nonissuers

AUD5 Reference to a section number in AICPA Technical Practice Aids, Statements ofPosition—Auditing and Attestation

FASB ASC5 Reference to a topic, subtopic, section, or paragraph in Financial AccountingStandards Board Accounting Standards Codificatione

SOP5 AICPA Statement of Position

.12 On June 30, 2009, FASB issued FASB Statement No. 168, The FASB Accounting Standards Codifica-tione and the Hierarchy of Generally Accepted Accounting Principles—a replacement of FASB Statement No. 162,which is codified in FASB ASC 105, Generally Accepted Accounting Principles. On the effective date of thisstatement, FASB ASC is the authoritative source of U.S. accounting and reporting standards for nongovern-mental entities, in addition to guidance issued by the SEC. At that time, FASB ASC supersedes all then-existing, non-SEC accounting and reporting standards for nongovernmental entities. Once effective, all othernongrandfathered, non-SEC accounting literature not included in FASB ASC is nonauthoritative. This state-ment is effective for financial statements issued for interim and annual periods ending after September 15,2009. See the FASB website at www.fasb.org for further information.

Instructions

.13 Within these checklists are a number of questions or statements that are accompanied by referencesto applicable authoritative guidance. The financial statements and notes checklist is organized into seven

4 Depository and Lending Institutions

FSP §2300.14

discrete sections. Disclosures listed in the “Presentation,” “Assets,” “Liabilities,” “Equity,” “Revenue,” and“Expenses” sections are common to most depository and lending institutions. Those listed in the “Transac-tion Specific Considerations” sections are required when circumstances dictate.

.14 The checklists provide spaces for checking off or initialing each question or for indicating that it hasbeen addressed. Carefully review the topics listed and consider whether they represent potential disclosureitems for the reporting entity for which you are preparing financial statements or auditing them. Usersshould check or initial

● Yes—If the disclosure is required and has been made appropriately.

● No—If the disclosure is required but has not been made.

● N/A (Not Applicable)—If the disclosure is not applicable to the entity.

.15 It is important that the effect of any “No” response be considered on the auditor’s or accountant’sreport. For audited financial statements, a “No” response that is material to the financial statements maywarrant a departure from an unqualified opinion as discussed in paragraphs .20–.64 of AU section 508,Reports on Audited Financial Statements (AICPA, Professional Standards). If a “No” response is indicated, theauthors recommend that a notation be made in the margin to explain why the disclosure was not made (forexample, because the item was not considered to be material to the financial statements).

.16 Users may find it helpful to use the right margin for certain other remarks and comments as appro-priate, including the following:

a. For each disclosure for which a “Yes” is indicated, a notation regarding where the disclosure islocated in the financial statements and a cross-reference to the applicable working papers wherethe support to a disclosure may be found

b. For items marked as “N/A,” the reasons for which they do not apply in the circumstances ofthe particular report

c. For each disclosure for which a “No” response is indicated, a notation regarding why the dis-closure was not made (for example, because the item was not considered to be material to thefinancial statements)

.17 These checklists and illustrative materials have been prepared by the AICPA Accounting and Au-diting Publications staff. They have not been reviewed, approved, disapproved, or otherwise acted on byany senior technical committee of the AICPA and do not represent official positions or pronouncements ofthe AICPA.

.18 The use of these or any other checklists requires the exercise of individual professional judgment.These checklists are not substitutes for the original authoritative guidance. Users of these checklists andillustrative materials should refer directly to applicable authoritative guidance when appropriate. The check-lists and illustrative materials may not include all disclosures and presentation items promulgated, nor dothey represent minimum standards or requirements. Additionally, users of the checklists and illustrativematerials should tailor them as required to meet specific circumstances. As an additional resource, membersmay call the AICPA Technical Hotline at 877-242-7212.

.19 Depository and lending institutions operate under comprehensive state and federal regulations.These regulations greatly influence accounting and financial reporting. Depository and lending institutionsare also subject to examination by federal and state bank examiners and periodic examinations by the insti-tution’s board of directors. Common accounting and reporting features of depository and lending institu-tions are described in the AICPA Audit and Accounting Guide Depository and Lending Institutions: Banks andSavings Institutions, Credit Unions, Finance Companies and Mortgage Companies (new edition as of June 1, 2010).Readers are encouraged to review the following guidance for additional information, as applicable:

● The NCUA Accounting manual for Federal Credit Unions at www.ncua.gov/GenInfo/GuidesManuals/accountingpmanuals/index.aspx

5Checklists and Illustrative Financial Statements for Depository and Lending Institutions

FSP §2300.21

● The Office of the Thrift Supervision Thrift Financial Report Instruction Manuals atwww.ots.treas.gov/?p5InstructionsQAs

● The Federal Deposit Insurance Corporation Reports of Condition and Income Forms and UserGuides at www.fdic.gov/regulations/resources/call/Index.html

.20 As used in this checklist, the term depository institutions means banks, credit unions, and savingsinstitutions. The terms financial institutions or institutions refer to all entities covered by the AICPA Auditand Accounting Guide Depository and Lending Institutions: Banks and Savings Institutions, Credit Unions, Fi-nance Companies and Mortgage Companies.

.21 We hope you find this checklist helpful as you perform your audit engagements. We would greatlyappreciate your feedback on this checklist. You may e-mail these comments to A&[email protected].

Recognition

Anne Mundinger, CPATechnical Manager

Accounting and Auditing Publications

Dennis Ridge, CPATechnical Manager

Accounting and Auditing Publications

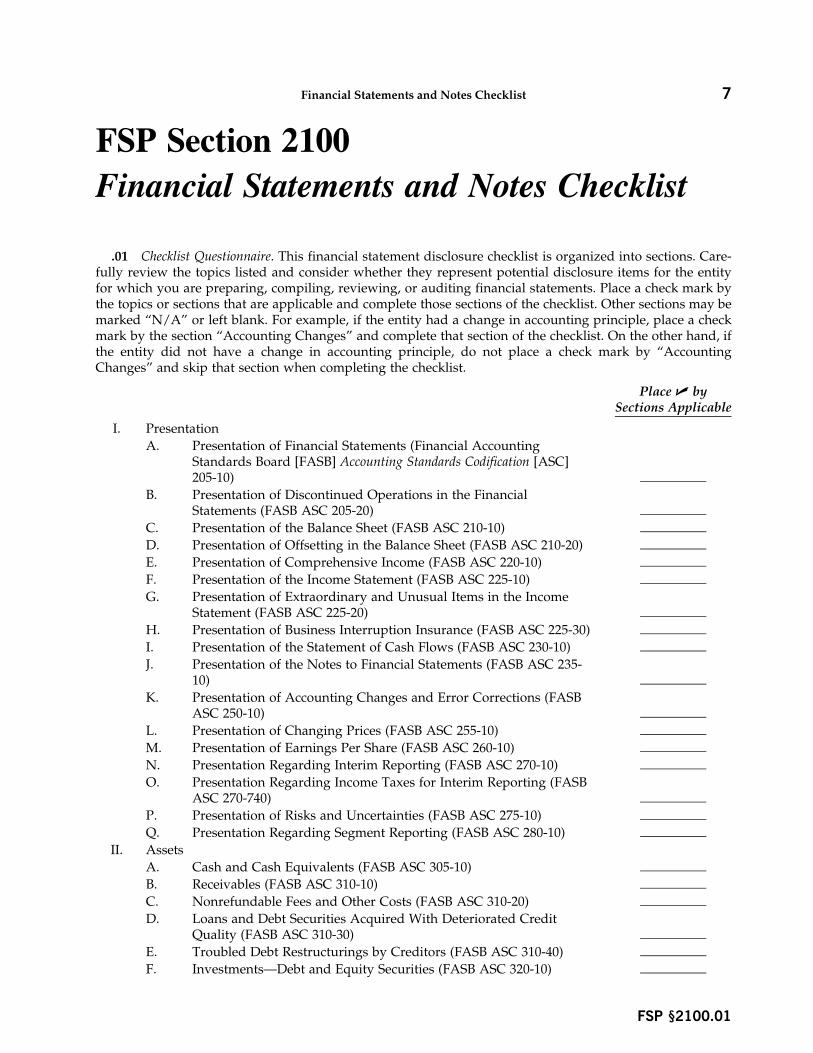

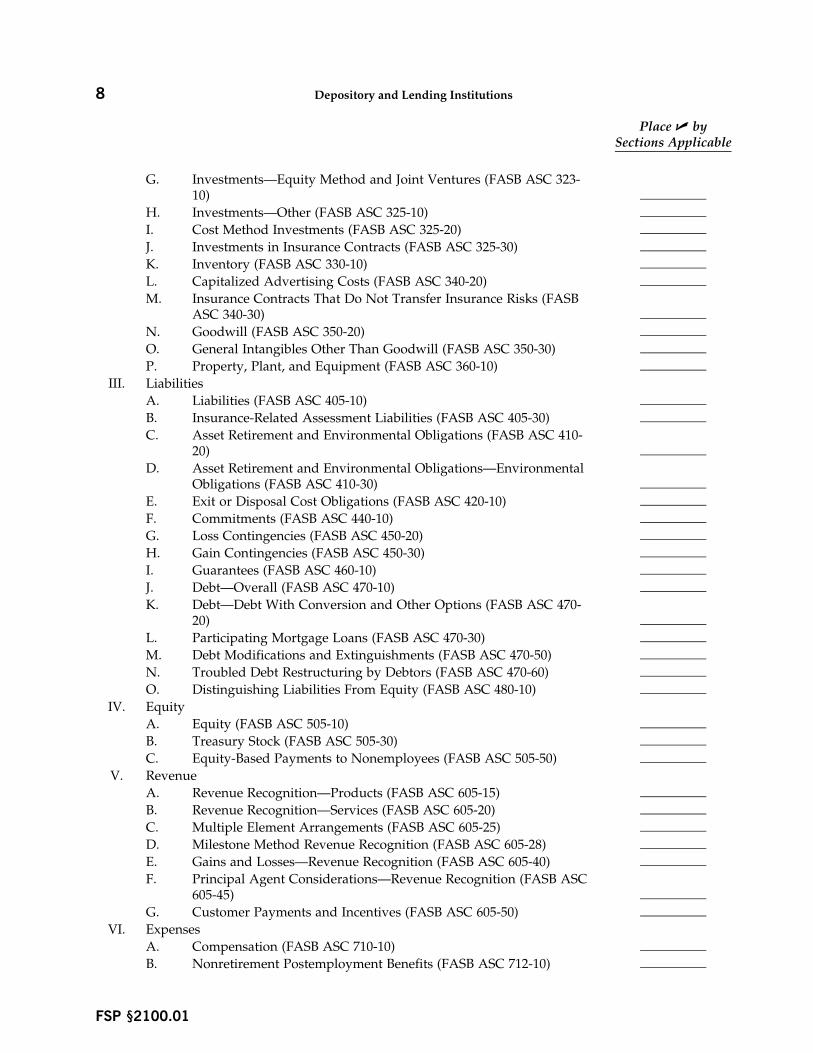

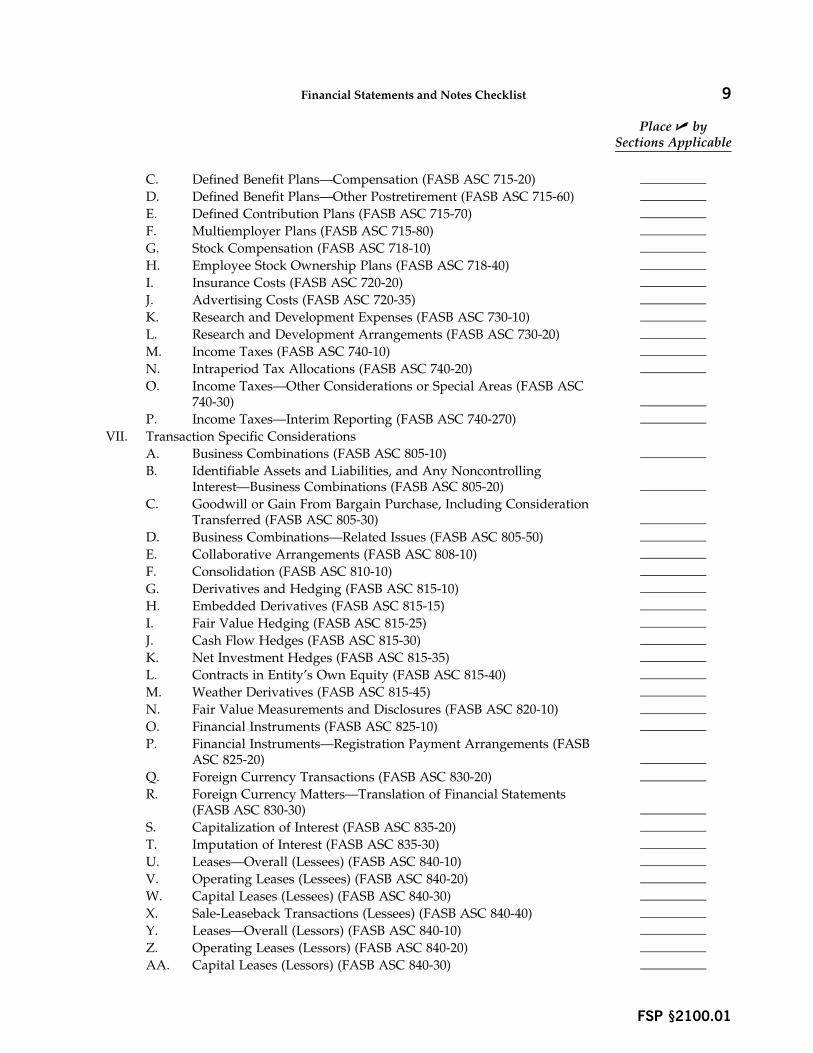

7Financial Statements and Notes Checklist

FSP §2100.01

FSP Section 2100

Financial Statements and Notes Checklist

.01 Checklist Questionnaire. This financial statement disclosure checklist is organized into sections. Care-fully review the topics listed and consider whether they represent potential disclosure items for the entityfor which you are preparing, compiling, reviewing, or auditing financial statements. Place a check mark bythe topics or sections that are applicable and complete those sections of the checklist. Other sections may bemarked “N/A” or left blank. For example, if the entity had a change in accounting principle, place a checkmark by the section “Accounting Changes” and complete that section of the checklist. On the other hand, ifthe entity did not have a change in accounting principle, do not place a check mark by “AccountingChanges” and skip that section when completing the checklist.

Place U bySections Applicable

I. Presentation

A. Presentation of Financial Statements (Financial AccountingStandards Board [FASB] Accounting Standards Codification [ASC]205-10)

B. Presentation of Discontinued Operations in the FinancialStatements (FASB ASC 205-20)

C. Presentation of the Balance Sheet (FASB ASC 210-10)

D. Presentation of Offsetting in the Balance Sheet (FASB ASC 210-20)

E. Presentation of Comprehensive Income (FASB ASC 220-10)

F. Presentation of the Income Statement (FASB ASC 225-10)

G. Presentation of Extraordinary and Unusual Items in the IncomeStatement (FASB ASC 225-20)

H. Presentation of Business Interruption Insurance (FASB ASC 225-30)

I. Presentation of the Statement of Cash Flows (FASB ASC 230-10)

J. Presentation of the Notes to Financial Statements (FASB ASC 235-10)

K. Presentation of Accounting Changes and Error Corrections (FASBASC 250-10)

L. Presentation of Changing Prices (FASB ASC 255-10)

M. Presentation of Earnings Per Share (FASB ASC 260-10)

N. Presentation Regarding Interim Reporting (FASB ASC 270-10)

O. Presentation Regarding Income Taxes for Interim Reporting (FASBASC 270-740)

P. Presentation of Risks and Uncertainties (FASB ASC 275-10)

DD. Reorganizations (FASB ASC 852-10 and FASB ASC 852-20)

EE. Subsequent Events (FASB ASC 855-10)

FF. Transfers and Servicing (FASB ASC 860-10)

GG. Sales of Financial Assets (FASB ASC 860-20)

HH. Secured Borrowing and Collateral (FASB ASC 860-30)

II. Servicing Assets and Liabilities (FASB ASC 860-50)

I. Presentation

Yes No N/AA. Presentation of Financial Statements (FASB ASC 205-10)

Presentation

Comparative Financial Statements

1. Has the entity properly presented the statement of financialposition, the income statement, and the statement of changesin equity for one or more preceding years, as well as for thecurrent year?[FASB ASC 205-10-45-2]

2. Has the entity properly presented appropriate explanationsof changes related to any differences in the manner of or basisfor presenting corresponding items for two or more periods?[FASB ASC 205-10-45-3]

3. Has the entity properly presented, or at least referred to, ifissuing comparative statements, notes and other disclosuresin the financial statements of the preceding year(s) in the cur-rent year, to the extent that they continue to be of signifi-cance?[FASB ASC 205-10-45-4]

Disclosure

Changes Affecting Comparability

4. Has the entity properly disclosed information that will ex-plain a change in the manner of or basis for presenting cor-responding items for two or more periods (for example, anychange in practice that affects comparability of financial state-ments must be disclosed), if changes have occurred?[FASB ASC 205-10-50-1]

Other Guidance

5. Has the entity properly presented, for a full presentation inconformity with accounting principles generally accepted inthe United States (U.S. GAAP), the following financial state-ments:

a. Balance sheet?

b. Statement of income (operations)?

11Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

c. Statement of retained earnings or changes in sharehold-ers’ equity?

d. Statement of cash flows?

e. Description of accounting policies?

f. Notes to the financial statements?[Common Practice]

6. Has the entity properly presented each financial statementwith a suitable title?[Common Practice]

7. Has the entity properly presented a reference to the notes,which are an integral part of the financial statements?[Common Practice]

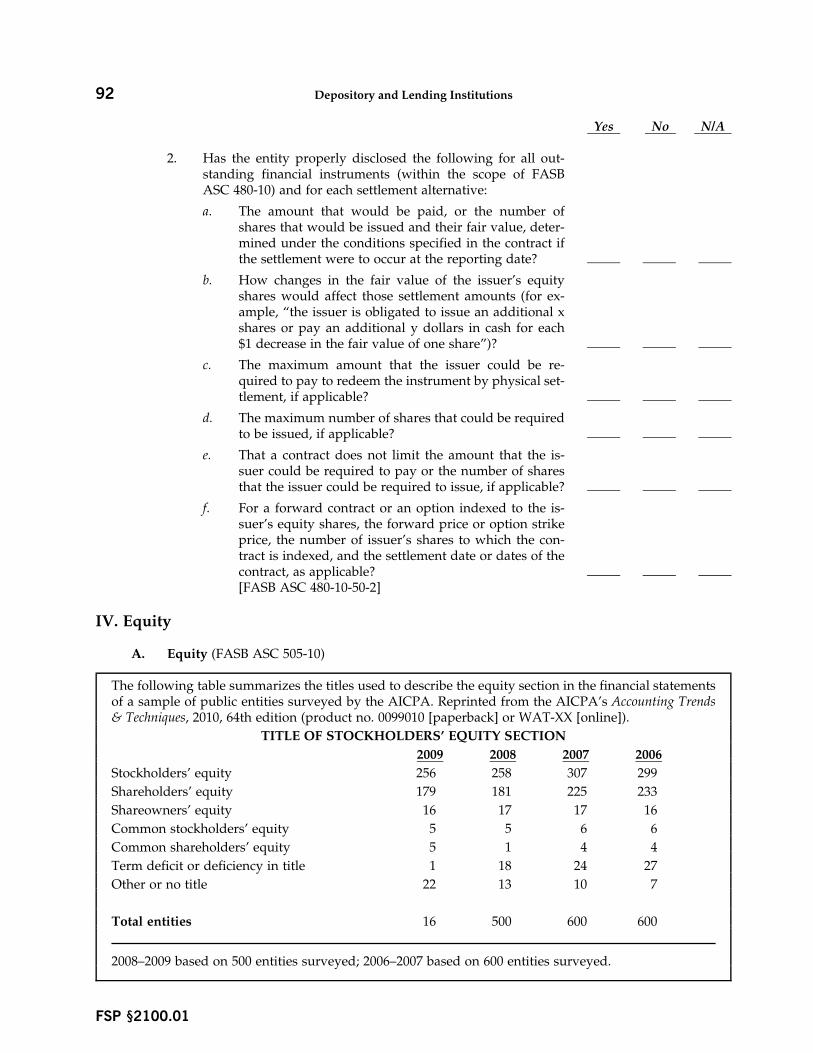

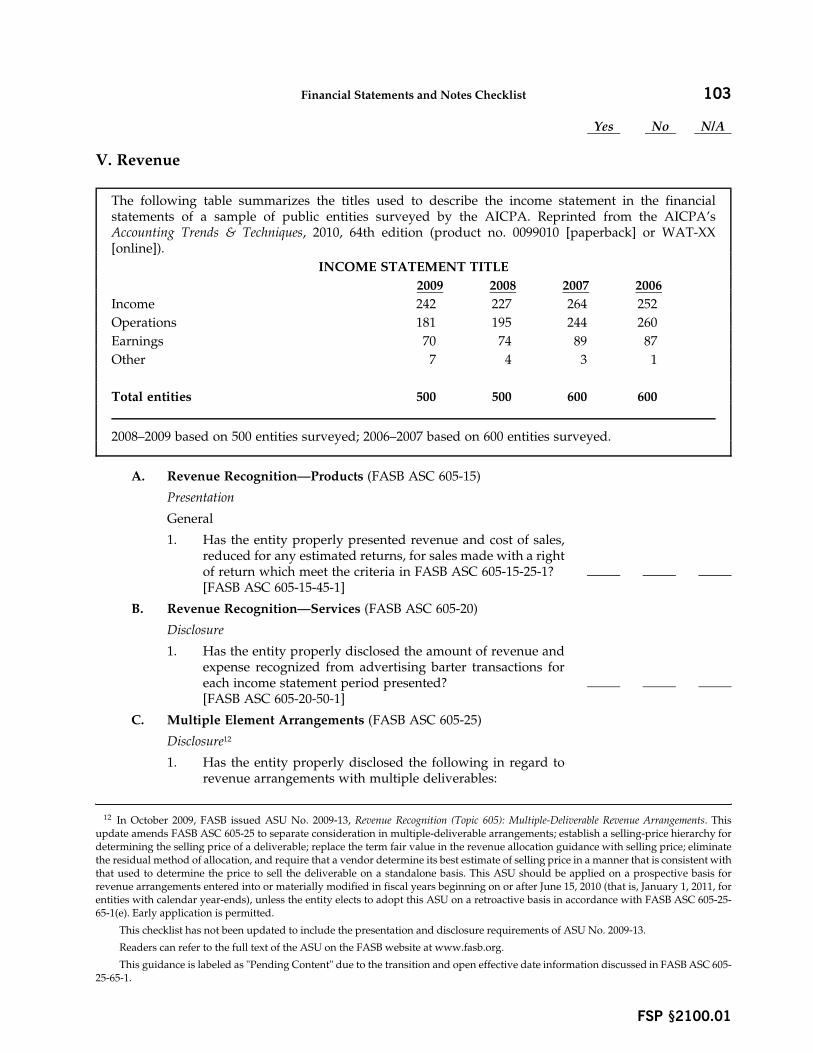

The following table summarizes the titles used to describe the statement of assets, liabilities, and equityin the financial statements a sample of public entities surveyed by the AICPA. Reprinted from theAICPA’s Accounting Trends & Techniques, 2010, 64th edition (product no. 0099010 [paperback] or WAT-XX [online]).

BALANCE SHEET TITLE

2009 2008 2007 2006

Balance sheet 476 478 577 578

Statement of financial position 24 22 23 21

Statement of financial condition — — — 1

Total entities 500 500 600 600

2008–2009 based on 500 entities surveyed; 2006–2007 based on 600 entities surveyed.

B. Presentation of Discontinued Operations in the Financial State-

ments (FASB ASC 205-20)

Presentation

Reporting Discontinued Operations

1. Has the entity properly presented, as discontinued opera-tions, the results of operations of a component of an entity (asthat phrase is defined in the FASB ASC glossary) that eitherhas been disposed of or is classified as held for sale under therequirements of FASB ASC 360-10-45-9, in accordance withFASB ASC 205-20-45-3 if both of the following conditions aremet:

a. The operations and cash flows of the component havebeen (or will be) eliminated from the ongoing opera-tions of the entity as a result of the disposal transac-tion?

b. The entity will not have any significant continuing in-volvement in the operations of the component after thedisposal transaction?[FASB ASC 205-20-45-1]

12 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

2. Has the entity properly presented, in a period in which acomponent of an entity either has been disposed of or is clas-sified as held for sale, in the income statement for current andprior periods, the results of operations of the component (in-cluding any gain or loss recognized in accordance with FASBASC 360-10-35-40 and 360-10-40-5), in discontinued opera-tions?[FASB ASC 205-20-45-3]

3. Has the entity properly presented the results of operations ofa component of an entity classified as held for sale in discon-tinued operations in the period(s) in which they occur?[FASB ASC 205-20-45-3]

4. Has the entity properly presented the results of discontinuedoperations, less applicable income taxes (benefit), as a sepa-rate component of income before extraordinary items?[FASB ASC 205-20-45-3]

5. Has the entity properly presented the gain or loss recognizedon the disposal either on the face of the income statement orin the notes to the financial statements?[FASB ASC 205-20-45-3]

6. Has the entity properly presented adjustments to amountspreviously reported in discontinued operations that are di-rectly related to the disposal of a component of an entity in aprior period and classified them separately in the current pe-riod in discontinued operations?[FASB ASC 205-20-45-4]

Allocation of Interest to Discontinued Operations

7. Has the entity properly presented, as allocated to discontin-ued operations, interest on debt that is to be assumed by thebuyer and interest on debt that is required to be repaid as aresult of a disposal transaction?[FASB ASC 205-20-45-6]

Disposal Group Classified as Held for Sale

8. Has the entity properly presented the assets and liabilities ofa disposal group that is classified as held for sale separatelyin the asset and liability sections, respectively, of the state-ment of financial position? (Note: These assets and liabilitiesshould not be offset and presented as a single amount. Fur-ther, major classes of assets and liabilities classified as heldfor sale should be separately disclosed either on the face ofthe statement of financial position or in the notes to the finan-cial statements.)[FASB ASC 205-20-45-10]

13Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

Disclosure

Assets Sold or Held for Sale

9. Has the entity properly disclosed the following informationin the notes to the financial statement that cover the period inwhich a long-lived asset (disposal group) either has been soldor is classified as held for sale under the requirements ofFASB ASC 360-10-45-9:

a. A description of the facts and circumstances leading tothe expected disposal, the expected manner and timingof that disposal, and, if not separately presented on theface of the statement, the carrying amount(s) of the ma-jor classes of assets and liabilities included as part of adisposal group?

b. The gain or loss recognized in accordance with FASBASC 360-10-35-40 and FASB ASC 360-10-40-5 and if notseparately presented on the face of the income state-ment, the caption in the income statement that includesthat gain or loss?

c. If applicable, amounts of revenue and pretax profit orloss reported in discontinued operations?

d. If applicable, the segment in which the long-lived asset(disposal group) is reported under FASB ASC 280?[FASB ASC 205-20-50-1]

10. Has the entity properly disclosed the major classes of assetsand liabilities classified as held for sale either on the face ofthe statement of financial position or in the notes to the finan-cial statements?[FASB ASC 205-20-50-2]

Change to a Plan of Sale

11. Has the entity properly disclosed, if the entity decides not tosell a long-lived asset previously classified as held for sale,and either FASB ASC 360-10-35-44 or FASB ASC 360-10-35-45applies, is a description of the facts and circumstances lead-ing to the decision to change the plan to sell the long-livedasset (disposal group) and its effect on the results of opera-tions for the period and any prior periods in the notes to thefinancial statements that include the period of that decision?[FASB ASC 205-20-50-3]

Continuing Cash Flows

12. Has the entity properly disclosed the following, for each dis-continued operation that generates continuing cash flows:

a. The nature of the activities that give rise to continuingcash flows?

b. The period of time continuing cash flows are expectedto be generated?

14 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

c. The principal factors used to conclude that the expectedcontinuing cash flows are not direct cash flows of thedisposed component?

d. Additionally, for each discontinued operation in whichthe ongoing entity will engage in a “continuation of ac-tivities” with the disposed component after its disposaland for which the amounts presented in continuing op-erations after the disposal transaction include a contin-uation of revenues and expenses that were intra-entitytransactions before the disposal transaction, are thoseintra-entity amounts before the disposal transactiondisclosed for all periods for comparability purposes?

e. Are the types of continuing involvement, if any, thatthe entity will have after the disposal transaction dis-closed in the period in which the operations are ini-tially classified as discontinued?[FASB ASC 205-20-50-4 and FASB ASC 205-20-55 par.9–12]

13. If the occurrence of a significant event or circumstance at anytime during the assessment period results in an expectationthat the criteria for reporting discontinued operations of acomponent of an entity in FASB ASC 205-20-45-1 will not bemet by the end of the assessment period, is the component’soperations not presented as discontinued operations?[FASB ASC 205-20-55-22]

Adjustments to Previously Reported Amounts

14. Has the entity properly disclosed the nature and amount ofadjustments to amounts previously reported in discontinuedoperations that are directly related to the disposal of a com-ponent of an entity in a prior period?[FASB ASC 205-20-50-5]

Continuing Involvement by Ongoing Entity

15. Has the entity properly disclosed, for each discontinued op-eration in which the ongoing entity will engage in a continu-ation of activities with the disposed component after its dis-posal, and for which the amounts presented in continuingoperations after the disposal transaction include a continua-tion of revenues and expenses that were intraentity transac-tions (eliminated in consolidated financial statements) beforethe disposal transaction, intraentity amounts before the dis-posal transaction for all periods presented? Further, has theentity properly disclosed the types of continuing involve-ment, if any, that the entity will have after the disposal trans-action? (That information should be disclosed in the period inwhich operations are initially classified as discontinued.)[FASB ASC 205-20-50-6]

C. Presentation of the Balance Sheet (FASB ASC 210-10)

Presentation

1. Has the entity presented all of the following in current assets:

15Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

a. Cash available for current operations and items that arecash equivalents?

b. Inventories of merchandise?

c. Trade accounts, notes , and acceptances receivable?

d. Receivables from officers, employees, affiliates and oth-ers, if collectible in one year?

e. Installment of deferred accounts and notes receivable?

f. Marketable securities representing the investment ofcash available for current operations, including invest-ments in debt and equity securities classified as tradingsecurities under FASB ASC 320-10?

g. Prepaid expense including insurance, interest, rents,taxes, unused royalties, current paid advertising servicenot yet received, and operating supplies?[FASB ASC 210-10-45-1]

2. Are assets not expected to be realized during the current op-erating cycle classified as noncurrent?[FASB ASC 210-10-45 par. 3–4]

3. Is any cash restricted as to withdrawal or use for other thancurrent operations excluded from current assets?[FASB ASC 210-10-45-4]

4. If a classified balance sheet is presented, is a total for currentliabilities shown?[FASB ASC 210-10-45-5]

5. Are bank overdrafts reclassified to and presented separatelyin current liabilities?[Encouraged, but not required]

6. Are held checks (those written before but not released untilafter the balance sheet date) reclassified to accounts payable?[Common Practice]

7. Are current portions of debt obligations presented as currentliabilities?[FASB ASC 210-10-45-9]

Disclosure

8. Has the entity properly disclosed the amounts at which cur-rent assets are stated, supplemented by information that re-veals, for the various classifications of inventory items, thebasis upon which their amounts are stated, and where prac-ticable, an indication of the method of determining the cost?[FASB ASC 210-10-50-1]

16 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

D. Presentation of Offsetting in the Balance Sheet (FASB ASC 210-10)

Presentation

Right of Setoff

1. Has the entity properly presented and exercised its option, ifit has a valid right of setoff, to offset the related asset andliability and present the net amount?[FASB ASC 210-20-45-2]

2. Have deposits in other institutions that are material been pre-sented as a separate amount in the balance sheet?[FASB ASC 942-210-45-4]

Credit Life, Credit Accident, and Health Policies

3. Have the unearned premiums and unpaid claims on certaincredit life and credit accident and health insurance policiesissued to finance customers been deducted from finance re-ceivables in the consolidated balance sheet?[FASB ASC 942-210-45-1]

4. Have unearned premiums and unpaid claims for credit lifeand accident and health coverage that have not been appliedin consolidation against related finance receivables for whichthe related receivables are assets of unrelated entities beenpresented as liabilities?[FASB ASC 942-210-45-1]

Property Insurance and Term Life Policies

5. Have unpaid claims for property insurance and level termlife insurance not been offset against related finance receiva-bles in the consolidated financial statements?[FASB ASC 942-210-45-2]

Repurchase and Reverse Repurchase Agreements

6. As permitted by FASB ASC 210, are only payables and receiv-ables representing repos and reverse repos that meet all of theconditions specified in FASB ASC 210 offset in the statementof financial position, and has the guidance not been appliedto securities borrowing or lending transactions?[FASB ASC 942-210-45-3; FASB ASC 210-20-45 par. 11–13]

E. Presentation of Comprehensive Income (FASB ASC 220-10)

Presentation

Reporting Comprehensive Income

1. Has the entity properly presented a full set of financial state-ments for the period which include (a) financial position atthe end of the period, (b) earnings (net income) for the period,(c) comprehensive income (total nonowner changes in equity)for the period, (d) cash flows during the period, and (e) in-vestments by and distributions to owners during the period?[FASB ASC 220-10-45-3]

17Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

2. Has the entity properly presented all components of compre-hensive income in the financial statements in the period inwhich they are recognized and presented them with the com-ponents of other comprehensive income (OCI)?[FASB ASC 220-10-45-5]

Classifications Within Comprehensive Income

3. Has the entity properly presented an amount for net income,even if the entity has no items of OCI and does not presentthat fact?[FASB ASC 220-10-45-6]

Alternative Formats for Reporting Comprehensive Income

4. Has the entity properly presented comprehensive income andits components in a financial statement that is displayed withthe same prominence as other financial statements that con-stitute a full set of financial statements?[FASB ASC 220-10-45-8]

5. Has the entity properly presented the components of OCI andtotal comprehensive income below the total for net income ina statement that reports results of operations or in a separatestatement of comprehensive income that begins with net in-come? (Note: This subtopic does not require a specific format,but the preceding presentation is encouraged.)[FASB ASC 220-10-45-9]

6. Has the entity properly presented the components of OCI ei-ther net of related tax effects, or before related tax effects withone amount shown for the aggregate tax effect related to thetotal of OCI items?[FASB ASC 220-10-45-11]

7. Has the entity properly presented the amount of income taxexpense or benefit allocated to each component of OCI (in-cluding reclassification adjustments) on the face of the state-ment in which those components are displayed or presentedin the notes to the financial statements?[FASB ASC 220-10-45-12]

Reporting OCI in the Equity Section of a Statement of Financial Po-sition

8. Has the entity properly presented the total of OCI for a pe-riod, transferred to a component of equity, separately fromretained earnings and additional paid-in-capital in the bal-ance sheet with a descriptive title such as “accumulated othercomprehensive income?”[FASB ASC 220-10-45-14]

9. Has the entity properly presented accumulated balances foreach classification within accumulated OCI on the face of thebalance sheet, in the statement of changes in shareholders’ eq-uity, or in the notes?[FASB ASC 220-10-45-14]

18 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

Interim-Period Reporting

10. Has the entity properly presented a total for comprehensiveincome in condensed financial statements of interim periods?[FASB ASC 220-10-45-18]

F. Presentation of the Income Statement (FASB ASC 225-10)

Presentation

1. Has the entity properly presented all items of profit and lossrecognized during the period, with the sole exception of errorcorrections as addressed in FASB ASC 250, AccountingChanges and Error Corrections, in order to present net income?[FASB ASC 225-10-45-1]

Disclosure

2. Has the entity disclosed the following information in thenotes to the financial statements in the period(s) in whichbusiness interruption insurance recoveries are recognized:

a. The nature of the event resulting in business interrup-tion losses?

b. The aggregate amount of business interruption insur-ance recoveries recognized during the period and theline item(s) in the statement of operations in whichthose recoveries are classified (including amounts re-ported as an extraordinary item pursuant to FASB ASC225-20)?[FASB ASC 225-30-50-1]

G. Presentation of Extraordinary and Unusual Items in the Income

Statement (FASB ASC 225-20)

Presentation

Presentation of Extraordinary Items

1. Has the entity properly presented extraordinary items segre-gated from the results of ordinary operations and shown sep-arately in the income statement, with disclosure of the natureand amounts thereof?[FASB ASC 225-20-45-9]

2. Has the entity properly presented extraordinary items (in-cluding applicable income taxes) segregated and followingincome before extraordinary items and before net income?[FASB ASC 225-20-45-10]

3. Has the entity properly presented the caption “extraordinaryitems” to identify and present separately the effects of eventsand transactions, other than disposals of components of anentity, that meet the criteria for classification as extraordinaryas discussed in paragraphs 1–6 of FASB ASC 225-20-45?(Note: The nature of an extraordinary event or transactionand the principal items entering into the determination of anextraordinary gain or loss should be described.)[FASB ASC 225-20-45-11]

19Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

4. Has the entity properly presented earnings per share (EPS)data for extraordinary items either on the face of the incomestatement or in the related notes, as prescribed by FASB ASC260-10-45?[FASB ASC 225-20-45-12]

Adjustment of Amounts Reported in Prior Periods

5. Has the entity properly presented any extraordinary itemsthat were reported in prior periods and that have been ad-justed during the current period, including separate presen-tation concerning year of origin, nature, and amount, andhave those items been classified separately in the current pe-riod as an extraordinary item?[FASB ASC 225-20-45-13]

Presentation of Unusual or Infrequently Occurring Items

6. Has the entity properly presented material events or transac-tions that are either unusual in nature or of infrequent occur-rence, but not both (and therefore not meeting the criteria forextraordinary items), (a) as a separate component of incomefrom continuing operations and (b) accompanied by disclo-sure of the nature and financial effects of each event?[FASB ASC 225-20-45-16]

Disclosure

Unusual or Infrequently Occurring Items

7. Has the entity properly disclosed the nature and financial ef-fects of each event or transaction that is unusual in nature oroccurs infrequently, but not both, on the face of the incomestatement, or alternatively, in notes to the financial state-ments?[FASB ASC 225-20-50-3]

Interim Reporting

8. Has the entity properly disclosed extraordinary items sepa-rately and included in the determination of net income for theinterim period or periods in which they occurred?[FASB ASC 225-20-50-4]

H. Presentation of Business Interruption Insurance (FASB ASC 225-30)

Disclosure

1. Has the entity properly disclosed the following informationin the notes to the financial statements in the period(s) inwhich business interruption insurance recoveries are recog-nized:

a. The nature of the event resulting in business interrup-tion losses?

20 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

b. The aggregate amount of business interruption insur-ance recoveries recognized during the period and theline item(s) in the statement of operations in whichthose recoveries are classified (including amounts re-ported as an extraordinary item pursuant to FASB ASC225-20)?[FASB ASC 225-30-50-1]

I. Presentation of the Statement of Cash Flows (FASB ASC 230-10)

Presentation

Cash and Cash Equivalents

1. Has the entity properly presented the change during the pe-riod in cash and cash equivalents and present an explanationfor the change?[FASB ASC 230-10-45-4]

2. When banks, savings institutions, and credit unions consti-tute part of a consolidated entity, are net amounts of cash re-ceipts and cash payments for deposit or lending activities ofthose entities reported separate from gross amounts of cashreceipts and cash payments for other investing and financingactivities of the consolidated entity, including those of a sub-sidiary of a bank, savings institution, or credit union that isnot itself a bank, savings institution, or credit union?[FASB ASC 942-230-45-2]

Cash Flows From Investing Activities

3. Has the entity properly presented cash flows from purchases,sales, and maturities of available-for-sale securities as cashflows from investing activities and presented these amountsas gross amounts in the statement of cash flows?[FASB ASC 230-10-45-11]

Cash Flows from Financing Activities

4. Are cash receipts and cash payments for the following trans-actions classified as cash flows from financing activities:

a. Proceeds from issuing debt?

b. Issuance of equity instruments?

c. Payment of dividends?

d. Repayments for amounts borrowed?

e. Purchases of treasury stock?

f. Other principal payments to creditors who have ex-tended long-term debt?

g. Proceeds received from derivative instruments and dis-tributions to counterparties of derivative instrumentsthat include financing elements at inception (other thana financing element inherently included in an at-the-market derivative instrument with no prepayments)?

21Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

h. Cash retained as a result of the tax deductibility of in-creases in the value of equity instruments issued undershare-based payment arrangements that are not in-cluded in the cost of goods or services that is recogniz-able for financial reporting purposes? For this purpose,excess tax benefits should be determined on an individ-ual award (or a portion thereof) basis.

i. Payments for debt issue costs?[FASB ASC 230-10-45 par. 14–15]

Cash Flows From Operating Activities

5. Has the entity properly presented cash payments made tosettle an asset retirement obligation in the statement of cashflows as an operating activity?[FASB ASC 230-10-45-17(e)]

6. Are cash receipts and cash payments for the following trans-actions classified as cash flows from operating activities:

a. Cash receipts from sales of goods (including certainloans and other debt and equity instruments of otherentities that are acquired specifically for resale, as dis-cussed in FASB ASC 230-10-45-21) or services, includ-ing receipts from sale of accounts and both short-termand long-term notes receivables from customers arisingfrom those sales or cash payments to acquire materialsfor manufacture or goods for resale, including principalpayments on accounts and both short-term and long-term notes payable to suppliers for those materials orgoods?

b. Cash receipts from returns on loans, other debt instru-ments of other entities, and equity securities—interestand dividends?

c. All other cash receipts that do not stem from transac-tions defined as investing or financing activities, suchas amounts received to settle lawsuits; proceeds of in-surance settlements except for those that are directly re-lated to investing or financing activities, such as fromdestruction of a building; and refunds from suppliers?

d. Cash payments to other suppliers and employees forother goods or services?

e. Cash payments to governments for taxes, duties, fines,and other fees or penalties and the cash that wouldhave been paid for income taxes if increases in thevalue of equity instruments issued under share-basedpayment arrangements that are not included in the costof goods or services recognizable for financial reportingpurposes also had not been deductible in determiningtaxable income?

f. Cash payments to lenders and other creditors for inter-est?

22 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

g. All other cash payments that do not stem from trans-actions defined as investing or financing activities, suchas payments to settle lawsuits, cash contributions tocharities, and cash refunds to customers?[FASB ASC 230-10-45 par. 16–17]

Cash Receipts and Payments Related to Hedging Activities

7. If an other-than-insignificant financing element is present atinception, other than a financing element inherently includedin an at-the-market derivative instrument with no prepay-ments (that is, the forward points in an at-the-money forwardcontract), does the borrower report all cash inflows and out-flows associated with that derivative instrument as financingactivities?[FASB ASC 230-10-45-27]

Acquisitions and Sales of Certain Securities and Loans

8. Has the entity properly presented cash receipts and cash pay-ments resulting from purchase and sales of securities classi-fied as trading securities, as prescribed in FASB ASC 320, In-vestments—Debt and Equity Securities, based on the nature andpurpose for which the securities were acquired?[FASB ASC 230-10-45-19]

9. Has the entity properly presented cash receipts and cash pay-ments resulting from the purchase or sale of securities andother assets that were acquired for resale and that are beingcarried at market value in a trading account as operating cashflows?[FASB ASC 230-10-45-20]

10. Has the entity properly presented cash receipts and cash pay-ments resulting from the purchase or sale of loans that wereacquired for resale and that are being carried at market valueor at the lower of cost or market values as operating cashflows?[FASB ASC 230-10-45-21]

Reporting Operating, Investing, and Financing Activities

11. Has the entity properly presented, in the statement of cashflows, net cash provided or used by the operating, investing,and financing activities and the effect of those flows on cashand cash equivalents during the period in a manner that rec-onciles beginning and ending cash and cash equivalents?(Note: Although not required, the entity may present sepa-rate presentation of cash flows pertaining to extraordinaryitems or discontinued operations in those categories providedthat the presentation is consistent for all periods effective.)[FASB ASC 230-10-45-24]

12. Has the entity properly presented the following, if the directmethod of reporting net cash flow from operating activities,as encouraged by FASB ASC 230-10-45-25, is used:

a. Cash received from customers?

23Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

b. Interest and dividends received?

c. Other operating cash receipts?

d. Cash paid to employees and suppliers?

e. Interest paid?

f. Income taxes paid and, separately, the cash that wouldhave been paid for income taxes if increases in thevalue of equity instruments issued under share-basedpayment arrangements that are not recognizable as acost of goods or services for accounting purposes alsohad not been deductible in determining taxable income(FASB ASC 230-10-45-14[e])?

g. Other operating cash payments (if any)?[FASB ASC 230-10-45-25]

13. Except for certain items whose turnover is quick, amounts arelarge, and maturities are short, are cash receipts and cashpayments from investing and financing activities shown sep-arately on the statement of cash flows?[FASB ASC 230-10-45 par. 8 and 26]

14. For certain items, such as demand deposits of a bank and cus-tomer accounts payable of a broker-dealer, that the entity issubstantively holding or disbursing cash on behalf of its cus-tomers, are only the net changes during the period in assetsand liabilities with those characteristics reported?[FASB ASC 230-10-45-8]

15. Providing that the original maturity of the asset or liability isthree months or less, are cash receipts and payments pertain-ing to investments (other than cash equivalents), loans receiv-able, and debt reported on a net basis?[FASB ASC 230-10-45-9]

Reconciliation of Net Income and Net Cash Flow From OperatingActivities

16. Has the entity properly presented, if the direct method of re-porting net cash flow from operating activities is not used,the net cash flow from operating activities indirectly, by ad-justing net income to reconcile it to net cash flow from oper-ating activities?[FASB ASC 230-10-45-28]

17. Has the entity properly presented a reconciliation of net in-come to net cash flow from operating activities, includingseparate reporting of all major classes of reconciling items?[FASB ASC 230-10-45-29]

18. Has the entity properly presented, if the direct method isused, a separate reconciling schedule to reconcile net incometo net cash flow from operating activities?[FASB ASC 230-10-45-30]

24 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

19. Has the entity properly presented, if the indirect method isused, a separate reconciling schedule to reconcile net incometo net cash flow from operating activities either within thestatement of cash flows or in a separate schedule, with thestatement of cash flows presenting only the net cash flowfrom operating activities?[FASB ASC 230-10-45-31]

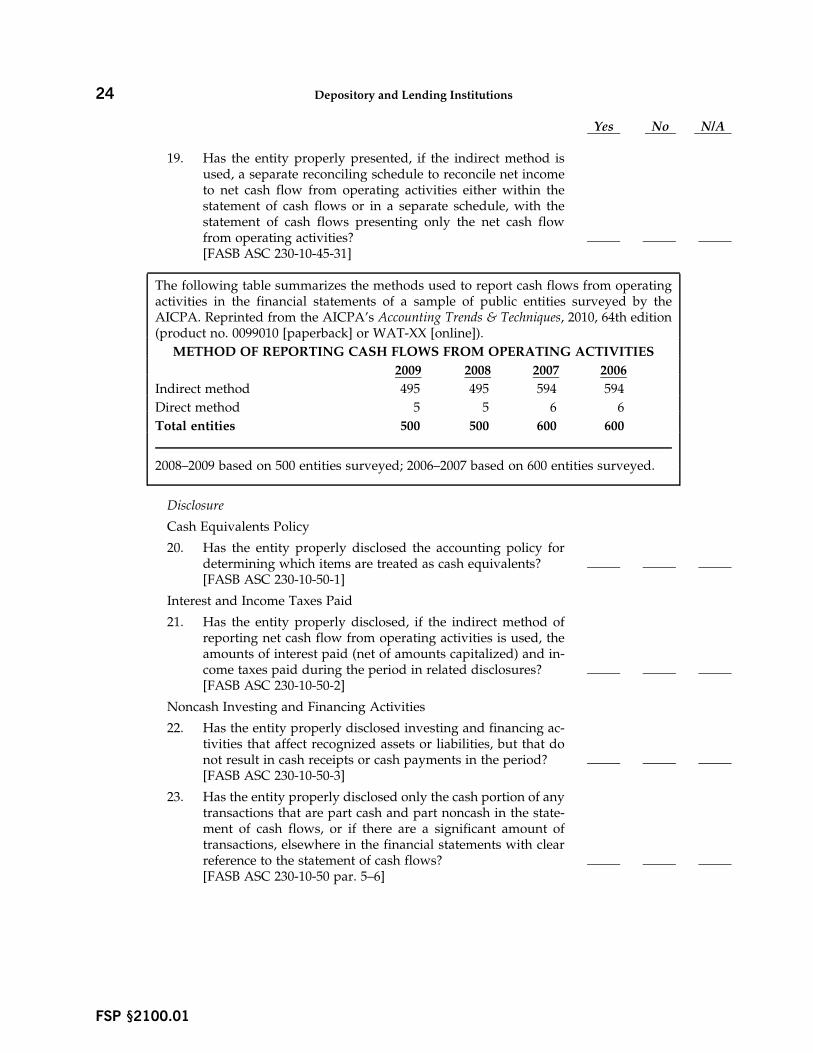

The following table summarizes the methods used to report cash flows from operatingactivities in the financial statements of a sample of public entities surveyed by theAICPA. Reprinted from the AICPA’s Accounting Trends & Techniques, 2010, 64th edition(product no. 0099010 [paperback] or WAT-XX [online]).

METHOD OF REPORTING CASH FLOWS FROM OPERATING ACTIVITIES

2009 2008 2007 2006

Indirect method 495 495 594 594

Direct method 5 5 6 6

Total entities 500 500 600 600

2008–2009 based on 500 entities surveyed; 2006–2007 based on 600 entities surveyed.

Disclosure

Cash Equivalents Policy

20. Has the entity properly disclosed the accounting policy fordetermining which items are treated as cash equivalents?[FASB ASC 230-10-50-1]

Interest and Income Taxes Paid

21. Has the entity properly disclosed, if the indirect method ofreporting net cash flow from operating activities is used, theamounts of interest paid (net of amounts capitalized) and in-come taxes paid during the period in related disclosures?[FASB ASC 230-10-50-2]

Noncash Investing and Financing Activities

22. Has the entity properly disclosed investing and financing ac-tivities that affect recognized assets or liabilities, but that donot result in cash receipts or cash payments in the period?[FASB ASC 230-10-50-3]

23. Has the entity properly disclosed only the cash portion of anytransactions that are part cash and part noncash in the state-ment of cash flows, or if there are a significant amount oftransactions, elsewhere in the financial statements with clearreference to the statement of cash flows?[FASB ASC 230-10-50 par. 5–6]

25Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

J. Presentation of the Notes to Financial Statements (FASB ASC 235-10)

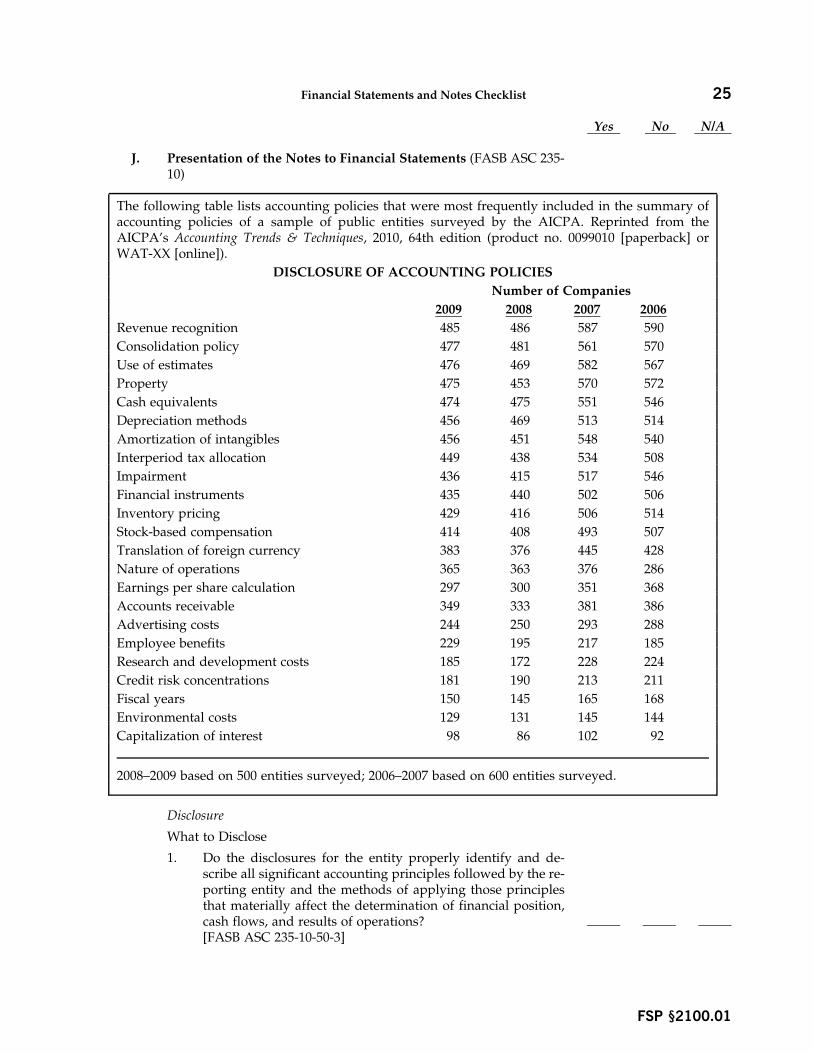

The following table lists accounting policies that were most frequently included in the summary ofaccounting policies of a sample of public entities surveyed by the AICPA. Reprinted from theAICPA’s Accounting Trends & Techniques, 2010, 64th edition (product no. 0099010 [paperback] orWAT-XX [online]).

DISCLOSURE OF ACCOUNTING POLICIES

Number of Companies

2009 2008 2007 2006

Revenue recognition 485 486 587 590

Consolidation policy 477 481 561 570

Use of estimates 476 469 582 567

Property 475 453 570 572

Cash equivalents 474 475 551 546

Depreciation methods 456 469 513 514

Amortization of intangibles 456 451 548 540

Interperiod tax allocation 449 438 534 508

Impairment 436 415 517 546

Financial instruments 435 440 502 506

Inventory pricing 429 416 506 514

Stock-based compensation 414 408 493 507

Translation of foreign currency 383 376 445 428

Nature of operations 365 363 376 286

Earnings per share calculation 297 300 351 368

Accounts receivable 349 333 381 386

Advertising costs 244 250 293 288

Employee benefits 229 195 217 185

Research and development costs 185 172 228 224

Credit risk concentrations 181 190 213 211

Fiscal years 150 145 165 168

Environmental costs 129 131 145 144

Capitalization of interest 98 86 102 92

2008–2009 based on 500 entities surveyed; 2006–2007 based on 600 entities surveyed.

Disclosure

What to Disclose

1. Do the disclosures for the entity properly identify and de-scribe all significant accounting principles followed by the re-porting entity and the methods of applying those principlesthat materially affect the determination of financial position,cash flows, and results of operations?[FASB ASC 235-10-50-3]

26 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

2. Has the entity properly disclosed the following information,when those principles and methods identified in FASB ASC235-10-50-3 include all instances in which there

a. is a selection from existing acceptable alternatives?

b. are principles and methods peculiar to the industry inwhich the reporting entity operates, even if such prin-ciples and methods are predominantly followed in thatindustry?

c. are unusual or innovative applications of U.S. GAAP?[FASB ASC 235-10-50-3]

Avoid Duplicate Details of Disclosures

3. Has the entity properly not disclosed duplicating details (forexample, composition of inventories or of plant assets) pre-sented elsewhere as a part of the financial statements?[FASB ASC 235-10-50-5]

Format

4. Has the entity properly disclosed a description of all signifi-cant accounting policies of the reporting entity, presented aseither a separate summary preceding the notes to the finan-cial statements or as the initial note under the same or similartitle?[FASB ASC 235-10-50-6]

K. Presentation of Accounting Changes and Error Corrections (FASBASC 250-10)

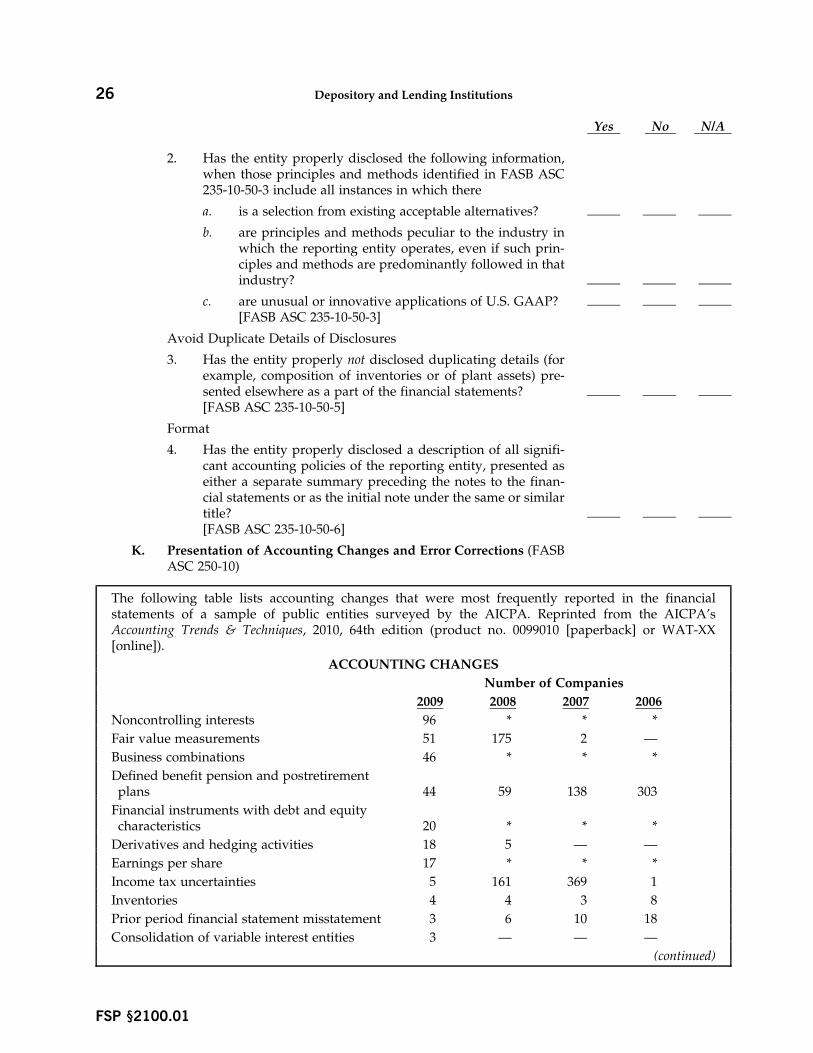

The following table lists accounting changes that were most frequently reported in the financialstatements of a sample of public entities surveyed by the AICPA. Reprinted from the AICPA’sAccounting Trends & Techniques, 2010, 64th edition (product no. 0099010 [paperback] or WAT-XX[online]).

ACCOUNTING CHANGES

Number of Companies

2009 2008 2007 2006

Noncontrolling interests 96 * * *

Fair value measurements 51 175 2 —

Business combinations 46 * * *

Defined benefit pension and postretirementplans 44 59 138 303

Financial instruments with debt and equitycharacteristics 20 * * *

Derivatives and hedging activities 18 5 — —

Earnings per share 17 * * *

Income tax uncertainties 5 161 369 1

Inventories 4 4 3 8

Prior period financial statement misstatement 3 6 10 18

Consolidation of variable interest entities 3 — — —

(continued)

27Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

Number of Companies

2009 2008 2007 2006

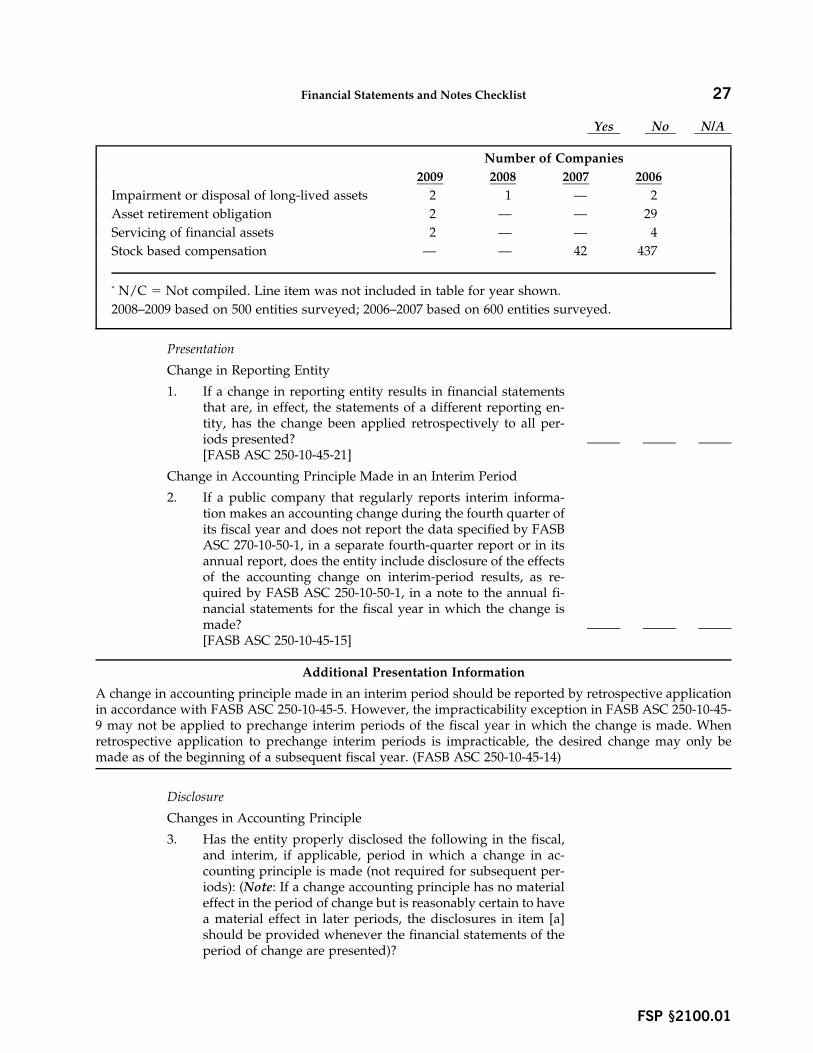

Impairment or disposal of long-lived assets 2 1 — 2

Asset retirement obligation 2 — — 29

Servicing of financial assets 2 — — 4

Stock based compensation — — 42 437

* N/C 5 Not compiled. Line item was not included in table for year shown.

2008–2009 based on 500 entities surveyed; 2006–2007 based on 600 entities surveyed.

Presentation

Change in Reporting Entity

1. If a change in reporting entity results in financial statementsthat are, in effect, the statements of a different reporting en-tity, has the change been applied retrospectively to all per-iods presented?[FASB ASC 250-10-45-21]

Change in Accounting Principle Made in an Interim Period

2. If a public company that regularly reports interim informa-tion makes an accounting change during the fourth quarter ofits fiscal year and does not report the data specified by FASBASC 270-10-50-1, in a separate fourth-quarter report or in itsannual report, does the entity include disclosure of the effectsof the accounting change on interim-period results, as re-quired by FASB ASC 250-10-50-1, in a note to the annual fi-nancial statements for the fiscal year in which the change ismade?[FASB ASC 250-10-45-15]

Additional Presentation Information

A change in accounting principle made in an interim period should be reported by retrospective applicationin accordance with FASB ASC 250-10-45-5. However, the impracticability exception in FASB ASC 250-10-45-9 may not be applied to prechange interim periods of the fiscal year in which the change is made. Whenretrospective application to prechange interim periods is impracticable, the desired change may only bemade as of the beginning of a subsequent fiscal year. (FASB ASC 250-10-45-14)

Disclosure

Changes in Accounting Principle

3. Has the entity properly disclosed the following in the fiscal,and interim, if applicable, period in which a change in ac-counting principle is made (not required for subsequent per-iods): (Note: If a change accounting principle has no materialeffect in the period of change but is reasonably certain to havea material effect in later periods, the disclosures in item [a]should be provided whenever the financial statements of theperiod of change are presented)?

28 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

a. The nature of and reason for the change in accountingprinciple, including an explanation of why the newlyadopted accounting principle is preferable?

b. The method of applying the change, including all of thefollowing:

i. A description of the prior-period informationthat has been retrospectively adjusted, if any?

ii. The effect of the change on income from contin-uing operations, net income (or other appropriatecaptions of changes in the applicable net assets orperformance indicator), any other affected finan-cial statement line item, and any affected per-share amounts for the current period and anyprior periods retrospectively adjusted? Presenta-tion of the effect on financial statement subtotalsand totals other than income from continuing op-erations and net income (or other appropriatecaptions of changes in the applicable net assets orperformance indicator) is not required.

iii. The cumulative effect of the change on retainedearnings or other components of equity or net as-sets in the statement of financial position as of thebeginning of the earliest period presented?

iv. If retrospective application to all prior periods isimpracticable, disclosure of the reasons therefore,and a description of the alternative method usedto report the change (see paragraphs 5–7 of FASBASC 250-10-45)?

c. If indirect effects of a change in accounting principleare recognized,

i. a description of the indirect effects of a change inaccounting principle, including the amounts thathave been recognized in the current period, andthe related per-share amounts, if applicable?

ii. unless impracticable, the amount of the total rec-ognized indirect effects of the accounting changeand the related per-share amounts, if applicable,that are attributable to each prior period pre-sented?[FASB ASC 250-10-50 par. 1–2]

4. Has the entity properly disclosed in the fiscal year in which anew accounting principle is adopted, financial informationreported for interim periods after the date of adoption, whichincludes disclosure of the effect of the change on income fromcontinuing operations, net income (or other appropriate cap-tions of changes in the applicable net assets or performanceindicator), and related per-share amounts, if applicable, forthose postchange interim periods?[FASB ASC 250-10-50-3]

29Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

Change in Accounting Estimate1

5. Has the entity properly disclosed the effect on income fromcontinuing operations, net income (or other appropriate cap-tions of changes in the applicable net assets or performanceindicator), and any related per-share amounts of the currentperiod for a change in estimate that affects several future per-iods, such as a change in service lives of depreciable assets?(Note: Disclosure of those effects is not necessary for esti-mates made each period in the ordinary course of accountingfor items such as uncollectible accounts or inventory obsoles-cence unless the effect of a change in the estimate is material.)[FASB ASC 250-10-50-4]

6. When the entity effects a change in estimate by changing anaccounting principle, are the disclosures required by ques-tions 2–3 made?[FASB ASC 250-10-50-4]

7. When the entity has a change in estimate that does not havea material effect in the period of change but is reasonably cer-tain to have a material effect in later periods, is a descriptionof that change in estimate disclosed whenever the financialstatements of the period of change are presented?[FASB ASC 250-10-50-4]

Change in Reporting Entity

8. When there has been a change in the reporting entity, do thefinancial statements of the period of the change, provide adescription of the nature of the change, and the reason for it?[FASB ASC 250-10-50-6]

9. Is the effect of the change on income before extraordinaryitems, net income (or other appropriate captions of changesin the applicable net assets or performance indicator), OCI,and any related per-share amounts disclosed for all periodspresented?[FASB ASC 250-10-50-6]

10. If a change in reporting entity does not have a material effectin the period of change but is reasonably certain to have amaterial effect in later periods, the nature of and reason forthe change disclosed whenever the financial statements of theperiod of change are presented?[FASB ASC 250-10-50-6]

Correction of an Error in Previously Issued Financial Statements

11. When financial statements are restated to correct an error, hasthe entity disclosed that its previously issued financial state-ments have been restated, along with a description of the na-ture of the error? Does the entity also properly disclose thefollowing:

1 Per Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 250-10-50-5, the disclosure provisions for achange in accounting estimate are not required for revisions resulting from a change in a valuation technique or its application.

30 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

a. The effect of the correction on each financial statementline item and any per-share amounts affected for eachprior period presented?

b. The cumulative effect of the change on retained earn-ings or other appropriate components of equity or netassets in the statement of financial position, as of thebeginning of the earliest period presented?[FASB ASC 250-10-50-7]

12. Has the entity properly disclosed, if prior period adjustmentshave been recorded, the resulting effects (both gross and netof applicable income tax) on the net income of prior periodsin the annual report for the year in which the adjustments aremade and in interim reports, if applicable, issued during thatyear subsequent to the date of recording the adjustments?(Note: The entity should not repeat the disclosures in subse-quent periods.)[FASB ASC 250-10-50 par. 8 and 10]

13. Has the entity properly disclosed the following prior-periodadjustments and restatements (see also FASB ASC 205-10-45and FASB ASC 205-10-50-1):

a. For single period financial statements, the effects (in-cluding applicable income taxes) of such restatementon the balance of retained earnings at the beginning ofthe period and on the net income of the immediatelypreceding period?

b. For multiple-period financial statements, the effects (in-cluding applicable income taxes) for each of the periodsincluded in the statements, in total and by class, of thecorrection on change in net assets for each of the per-iods presented?[FASB ASC 250-10-50-9]

Error Correction Related to Prior Interim Periods of the Current Fis-cal Year

14. If the entity prepares interim reporting and an adjustment re-lated to a prior period of the current fiscal year has beenmade, has the entity properly disclosed both of the following:

a. The effect on income from continuing operations, netincome, and related per-share amounts for each priorinterim period of the current fiscal year?

b. Income from continuing operations, net income, and re-lated per-share amounts for each prior interim periodrestated in accordance with FASB ASC 250-10-45-26?[FASB ASC 250-10-50-11]

31Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

L. Presentation of Changing Prices (FASB ASC 255-10)

Disclosure

1. Although not required, has the entity properly disclosed, asencouraged, supplementary information on the effects ofchanging prices?[FASB ASC 255-10-50-1]

M. Presentation of Earnings Per Share (FASB ASC 260-10)2

Presentation

Additional Presentation Information

For entities that have issued common stock or potential common stock, if those securities trade in a publicmarket either on a stock exchange or in the over-the-counter market, including securities quoted only locallyor regionally, as discussed in FASB ASC 260-10-15-2, see FASB ASC 260-10-45 for information on properpresentation.

Disclosure

1. Has the entity properly disclosed the following for each pe-riod for which an income statement is presented:

a. A reconciliation of the numerators and denominators ofthe basic and diluted per share computations for in-come from continuing operations?

b. The effect that has been given to preferred dividends inarriving at income available to common shareholders’in computing basic EPS?

c. Securities (including those issuable pursuant to contin-gent stock agreements) that could potentially dilute ba-sic EPS in the future that were not included in the com-putation of diluted EPS because to do so would havebeen antidilutive for the period(s) presented?[FASB ASC 260-10-50-1]

2. Has the entity properly disclosed, for the latest period forwhich an income statement is presented, a description of anytransaction that occurred after the end of the most recent pe-riod but before the financial statements were issued or areavailable to be issued (as discussed in FASB ASC 855-10-25)that would have changed materially the number of commonshares or potential common shares outstanding at the end ofthe period if the transaction had occurred before the end ofthe period?[FASB ASC 260-10-50-2]

2 Per FASB ASC 260-10-15-2, the guidance in FASB ASC 260, Earnings Per Share, requires presentation of earnings per share (EPS) byall entities that have issued common stock or potential common stock (that is, securities such as options, warrants, convertible securities,or contingent stock agreements) if those securities trade in a public market either on a stock exchange (domestic or foreign) or in the over-the-counter market, including securities quoted only locally or regionally. FASB ASC 260 also requires presentation of EPS by an entitythat has made a filing or is in the process of filing with a regulatory agency in preparation for the sale of those securities in a publicmarket.

32 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

3. If the number of common shares outstanding increases as aresult of a stock dividend or stock split (see FASB ASC 505-20) or decreases as a result of a reverse stock split, the com-putations of basic and diluted EPS should be adjusted retro-actively for all periods presented to reflect that change incapital structure. If per-share computations reflect suchchanges in the number of shares, is that fact disclosed?[FASB ASC 260-10-55-12]

4. If changes in common stock resulting from stock dividends,stock splits, or reverse stock splits occur after the close of theperiod but before the financial statements are issued or areavailable to be issued (as discussed in FASB ASC 855-10-25),the per-share computations for those and any prior-period fi-nancial statements presented should be based on the newnumber of shares. If per-share computations reflect suchchanges in the number of shares, is that fact disclosed?[FASB ASC 260-10-55-12]

5. When prior EPS amounts have been restated in compliancewith an accounting standard requiring restatement, is the ef-fect of the restatement, expressed in per share terms, dis-closed in the period of restatement?[FASB ASC 260-10-55-16]

N. Presentation Regarding Interim Reporting (FASB ASC 270-10)3

Disclosure

Additional Disclosure Information

FASB ASC 270-10-50 contains disclosures for both nonpublic and public companies. See the subsection “Pub-lic Entity Disclosures,” following, for required disclosures specific to public entities.

3 In July 2010, FASB issued Accounting Standards Update (ASU) No. 2010-20, Receivables (Topic 310): Disclosures about the Credit Qualityof Financing Receivables and the Allowance for Credit Losses. The effective dates are as follows:

a. For publicly traded companies:

i. The “Pending Content” for disclosures as of the end of a reporting period are effective for the first interim or annualreporting period ending on or after December 15, 2010 (that is, December 31, 2010, for public entities with calendar year-ends).

ii. The “Pending Content” for disclosures about activity that occurs during a reporting period is effective for the first interimor annual reporting period beginning on or after December 15, 2010 (that is, January 1, 2011, for public entities withcalendar year-ends).

b. For nonpublic entities, the “Pending Content” is effective for the first annual reporting period ending on or after December 15,2011 (that is, December 31, 2011, for entities with calendar year-ends).

This checklist has been updated for content applicable to publicly traded companies with interim or annual reporting periodsending after December 15, 2010, but has not been updated to include the presentation and disclosure requirements of ASU No. 2010-20.

Readers can refer to the full text of the ASU on the FASB website at www.fasb.org.

This guidance is labeled as "Pending Content" due to the transition and open effective date information discussed in FASB ASC 310-10-65-2.

33Financial Statements and Notes Checklist

FSP §2100.01

Yes No N/A

Disclosures by Nonpublic Entities

1. Has the entity properly disclosed the following, at a mini-mum, if the publicly traded entity reports summarized finan-cial information at interim dates (including reports on thefourth quarter):

a. Sales or gross revenues, provision for income taxes, ex-traordinary items (including related income tax effects),net income, and comprehensive income?

b. Basic and diluted EPS data for each period presented,determined in accordance with the provisions of FASBASC 260?

c. Seasonal revenue, costs, or expenses?

d. Significant changes in estimates or provisions for in-come taxes?

e. Disposal of a component of an entity and extraordi-nary, unusual or infrequently occurring items?

f. Contingent items?

g. Changes in accounting principles or estimates?

h. Significant changes in financial position?

i. All of the following information about reportable op-erating segments determined according to the provi-sions of FASB ASC 280, including provisions related torestatement of segment information in previously is-sued financial statements:

i. Revenues from external customers?

ii. Intersegment revenues?

iii. A measure of segment profit or loss?

iv. Total assets for which there has been a materialchange from the amount disclosed in the last an-nual report?

v. A description of differences from the last annualreport in the basis of segmentation or in themeasurement of segment profit or loss?

vi. A reconciliation of the total of the reportable seg-ments’ measures of profit or loss to the entity’sconsolidated income before income taxes, ex-traordinary items, and discontinued operations?

j. All of the following information about defined benefitpension plans and other defined benefit postretirementbenefit plans, disclosed for all periods presented pur-suant to the provisions of FASB ASC 715-20:

34 Depository and Lending Institutions

FSP §2100.01

Yes No N/A

i. The amount of net periodic benefit cost recog-nized, for each period for which a statement ofincome is presented, showing separately the ser-vice cost component, the interest cost component,the expected return on plan assets for the period,the gain or loss component, the prior service costor credit component, the transition asset or obli-gation component, and the gain or loss recog-nized due to a settlement or curtailment?

ii. The total amount of the employer’s contributionspaid, and expected to be paid, during the currentfiscal year, if significantly different from amountspreviously disclosed pursuant to FASB ASC 715-20-50-1. Estimated contributions may be pre-sented in the aggregate combining all of the fol-lowing: (1) contributions required by fundingregulations or laws, (2) discretionary contribu-tions, and (3) noncash contributions?

k. The information about the use of fair value to measureassets and liabilities recognized in the statement of fi-nancial position pursuant to paragraphs 1–6 of FASBASC 820-10-50?

l. The information about derivative instruments as re-quired by FASB ASC 815-10-50, 815-20-50, 815-25-50,815-30-50, and 815-35-50?

m. The information about fair value of financial instru-ments as required by FASB ASC 825-10-50?

n. The information about certain investments in debt andequity securities as required by FASB ASC 320-10-50and 942-320-50?

o. The information about other-than-temporary impair-ments as required by FASB ASC 320-10-50, 325-20-50,and 958-320-50?[FASB ASC 270-10-50-1]