29

Cheque Fraud Partnering Session & Mitigating Fraud , Bank Offered Solutions Hosted by: Global Transaction Solutions June 23rd, 2007.

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | kiya-waits |

| View: | 219 times |

| Download: | 2 times |

Cheque Fraud Partnering Session&

Mitigating Fraud , Bank Offered Solutions

Hosted by:

Global Transaction Solutions

June 23rd, 2007.

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

2

•The Basics of Cash Management

•Cheque fraud prevention

•Mitigating Fraud , Bank Offered Solutions

•Questions & Answers

Introductions & Agenda

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

3

Cash Management Solutions

Information & Control SolutionsEnables your business to assign varying levels of online permissions and

authorities to individual users and allow them to monitor and manage financial transactions in their current account, helping them to operate their business

more efficiently and mitigate risk effectively

Disbursement SolutionsEnable your business to more efficiently

manage corporate payments and increase control over the timing of payments

Supplier PaymentsPayroll

Money Flows Out

Collection SolutionsProvides your business with greater certainty around the timing of deposits and allows you to accelerate cash inflows through increased

efficiencies & alternate payment options

Money Flows In

Customer payments Company

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

4

What is Cheque Fraud?

Fraud on the frontCounterfeit - A fake cheque that has been completely reproduced or copied to resemble a legitimate or authentic cheque. Altered - An unauthorized change to an original and legitimate cheque, such as the payee, sum payable, and date or cheque number. The alterations are made prior to being presented for negotiation.Forged Drawer/Maker– The payer signature on the front of the cheque is not the legitimate signature (forged) of the account owner/signing officer.

Fraud on the backForged Endorsement - A forged payee signature on the reverse of the item (person cashing the cheque)

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

5

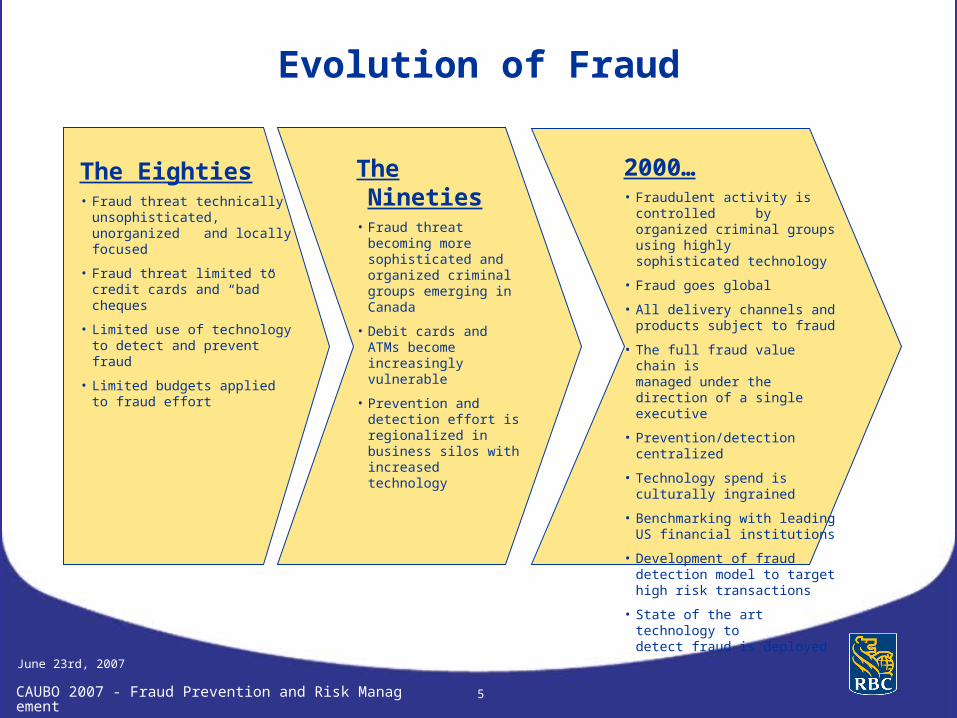

The Eighties• Fraud threat technically

unsophisticated, unorganized and locally focused

• Fraud threat limited to credit cards and “bad” cheques

• Limited use of technology to detect and prevent fraud

• Limited budgets applied to fraud effort

2000…• Fraudulent activity is controlled

by organized criminal groups using highly sophisticated technology

• Fraud goes global

• All delivery channels and products subject to fraud

• The full fraud value chain is managed under the direction of a single executive

• Prevention/detection centralized

• Technology spend is culturally ingrained

• Benchmarking with leading US financial institutions

• Development of fraud detection model to target high risk transactions

• State of the art technology to detect fraud is deployed

The Nineties• Fraud threat becoming

more sophisticated and organized criminal groups emerging in Canada

• Debit cards and ATMs become increasingly vulnerable

• Prevention and detection effort is regionalized in business silos with increased technology

Evolution of Fraud

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

6

Cheque Fraud Evolution

Stolen cheque stock with forged signaturesCounterfeit cheques Altered amounts/payeesForged and improper endorsements

How cheques are compromised?Theft from the mail and couriersInternal employee theft or selling of account informationDumpster diving

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

7

Responsibility for Prevention

The Issuer

The Receiver

The Bank

Cheque Fraud Detection Partnership

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

8

The Numbers

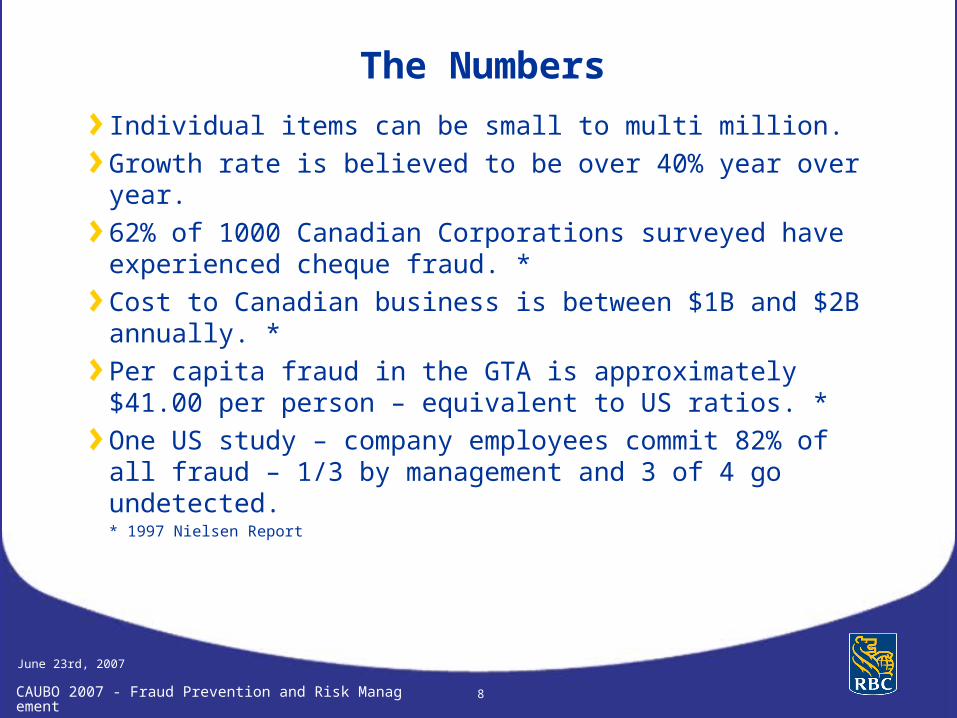

Individual items can be small to multi million.Growth rate is believed to be over 40% year over year.62% of 1000 Canadian Corporations surveyed have experienced cheque fraud. *Cost to Canadian business is between $1B and $2B annually. *Per capita fraud in the GTA is approximately $41.00 per person – equivalent to US ratios. *One US study – company employees commit 82% of all fraud – 1/3 by management and 3 of 4 go undetected.

* 1997 Nielsen Report

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

9

Impact of Cheque Fraud in Canada

5,000 cheque fraud attempts annually totalling $300MM*Some frauds are over $1 millionOne RBC client had 10 incidents totalling >$2 million in 6 monthsBusiness cheques are a favourite target – acceptability As senior clients implement protective procedures, fraudsters move down marketNorthbound migration of cheque fraud techniques

* Extrapolated from RBC experience

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

10

What does cheque fraud mean to business clients?

Time/expense of investigations and risk mitigationRepeated reconciliation, Investigation, police report, tracing documentsCosts per occurrence can run to 4-figures before the write-off Affidavits; new accounts required, new cheques to be printed

Governance issues for larger clientsShareholder/board oversight for larger clientsExpanded audit scope = longer time = higher fees

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

11

Cheques issuedReconciliation is complicatedComplicity investigation risks staff moraleRisk to Vendor relationship

Cheques deposited:Revenue risk: Reluctant to accept any chequeLoss risk: Bank may return cheque after fraudster obtains goods

What does cheque fraud mean to business clients?

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

12

How does Cheque Fraud work?

Pick a bank…some weakness shown in the past, does not pursue police action

Pick a company…good reputation = high acceptability

Test the waters…Try a small cheque

Full counterfeitRaise the amountAlter the payee

Try some big ones…or a really big one

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

13

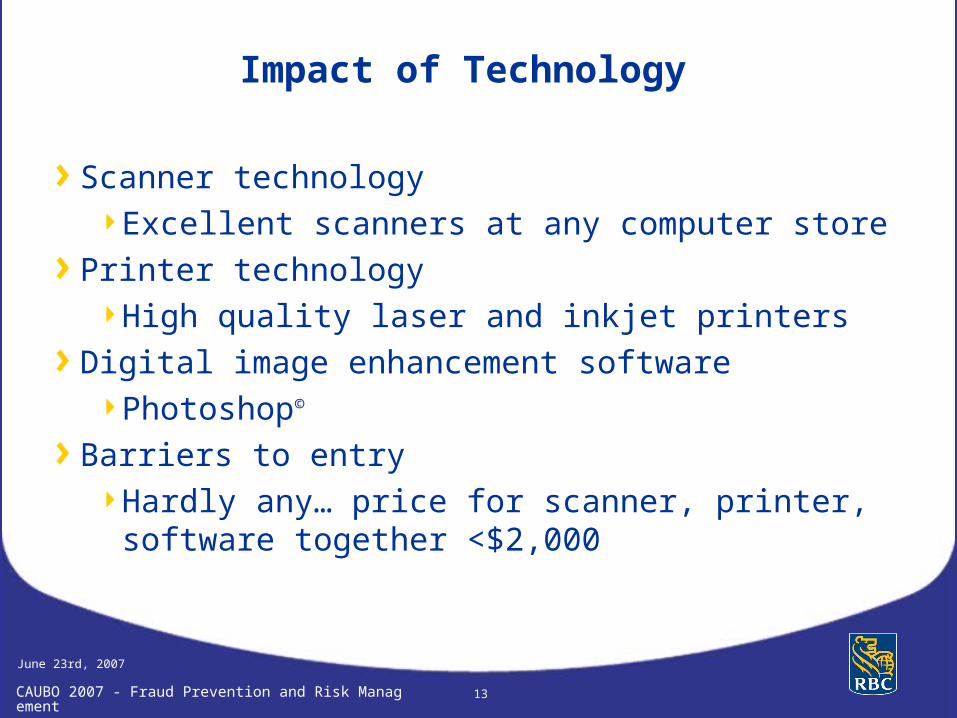

Impact of Technology

Scanner technology Excellent scanners at any computer store

Printer technology High quality laser and inkjet printers

Digital image enhancement softwarePhotoshop©

Barriers to entryHardly any… price for scanner, printer, software together <$2,000

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

14

CompaniesSegregated responsibilitiesRisk assessmentSecure cheque stock, unissued and paidSeparate accounts for high-valueMaximize use of bank’s verification toolsOtherwise, self-verify

BankMitigation tools

Positive Pay reconciliation toolPayee Name Match

Self-verification toolsExisting Web availability of both MICR-line and imagesHigh-volume MICR-line option

Cheque Fraud Image Partnership

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

15

National Fraud Detection Group (NFDG)

NFDG is located in Toronto and operates 24/7

They look after the prevention, detection, and investigation of fraud for client card, cheques, online banking, and branch transactions.

Look for unusual transaction activity on a client’s account.

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

16

NFDG ~ Cheque Fraud TeamWithin NFDG, there is a department that specializes in Cheque Fraud.The Cheque Fraud department has 4 teams: Kiting, Altered, Counterfeit and EndorsementsWith use of system technologies, fraud detection rules, and the experience of each team member, they are responsible to detect and prevent losses due to fraudulent US and CDN RBC cheques.Detection may occur at point of presentment or after in form of a post review.Important to remember, NFDG will only see select items after it has been presented for payment.

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

17

RBC Mitigating Risk Solutions Review

Positive Pay Cheque Matching

Payee Name Match

Cheque Imaging

Electronic Balance & Transaction Reporting

Electronic Payments

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

18

Positive Pay Cheque Matching

Daily reconciliation of all cleared cheques is one of the best defences to protect against cheque fraud.Positive Pay is a reconciliation tool that shifts the onus for daily reconciliation to your financial institution. An input file of cheques needs to be sent to bank when cheques are issued.Any exception items need to be reviewed and decisioned on a daily basis. Some banks offer automatic returns on any exception items.

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

19

Payee Name Match

Payee Name Match helps provides the best possible protection against 'fraud on the face’ of negotiated cheques.

Tighten Operational Risk ControlPayee Name Match helps clients meet more stringent control and governance requirements often required by regulators*, auditors, etc.

For US-owned firms, Sarbanes-Oxley is the regulatory driver. Similar Canadian legislation is expected in the near future.

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

20

Payee Name Match

Protect Vendor/Supplier RelationshipWe have seen in cases where Payee Name Match had identified the payee name fraud, and replacement cheques issued before the beneficiaries knew that the cheques had been stolen

Save Time, Expense And AggravationHandling an altered cheque becomes routine. Saves the time, expense, and aggravation of investigating an item after the fraudster received value or funds.

Your current processes for MICR-line fraud detection (Positive Pay), in-house cheque reconciliation, and stop payments are unchanged.

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

21

How does Payee Match work?

Cheques must meet new CPA Guidelines and must be OCR-compliant.

Customer sends Issued Item information to bank at time of issuance

Payee Name and full Payee Address, as printed on the cheque

The image is captured when the cheque is delivered into bank clearing.

Optical Character Recognition (OCR) is used to digitize payee name and address

The cheque information is compared to issued item information

Exception cheques are presented for customer decisioning

Items are “paid” if not decisionedoption to “return” if not decisioned

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

22

Payee Name Line Match

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

23

Account Imaging Services

With the implementation of the new CPA Standards, banks can now provide access to high quality digital images of items processed through your accounts.

Access to images of cheques and deposits is convenient, saves time, allows you to provide better service to your customers, and can help minimize the risk associated with cheque fraud. Images also provides an economical option to long term cheque storage, and for business continuity purposes.

Account Images can be delivered in the following formats:Daily access via online reporting system.

Delivery via regularly scheduled CD Rom’s (monthly, bi-weekly, etc.).

Daily access via downloaded image file (must have an image archive system to manage images).

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

24

Balance Reporting Services

Balance & Transactions Services can also be an effective way to help protect against cheque fraud.

Often these tools are delivered via an Internet channel, and provide ongoing access to all activity through your bank accounts.

Very often these tools have some type of built in export functionality to allow you to complete your own bank reconciliation on a daily basis.

This is often the most cost effective way to complete a bank reconciliation as long as it can be completed every business day.

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

25

FunctionalityStandard Internet

Banking

Dedicated Cash Management

Platform

Ability to assign user permissions

No Yes

Establish payment approval rules for multiple signing officers

No Yes

Export balance & transaction information to aid in automated reconciliation

Possibly, but often

very limited

functionality

Yes

Reporting for accounts held at different financial institutions.

No Yes

Ability to add other services into platform (such as Wire Payments, etc, ACH Direct Deposits or Direct Payments)

No Yes

Internet Banking vs. Cash Management Platform

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

26

Electronic PaymentsThe best overall option available to protect yourself against cheque fraud is to move as many cheques to electronic payments as much as possible.

An electronic payment system:

Can be significantly more cost effective than cheque issuance.

Can save time, speed up reconciliation, and provide better control over outgoing cash flows.

We have seen some clients use an electronic payment system to negotiated better trade discounts with large suppliers because of their ability to pay on any specific date.

Types of electronic payments:

Financial EDI Payments (Corporate Payments)

ACH Direct Deposits (Primarily Retail Payments in Canada, but can also be used for Corporate/Retail Payments into the US.

Wire Payments

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

27

Electronic Payment Solution

ROYAL BANK OF CANADA123 ANY TOWNANY CITY

Other Banks

Sin

gle Paym

ent F

ile

Remittance details

sent to Receiver

$$$$Payments$$$$

Trading Partners

Accounting System

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

28

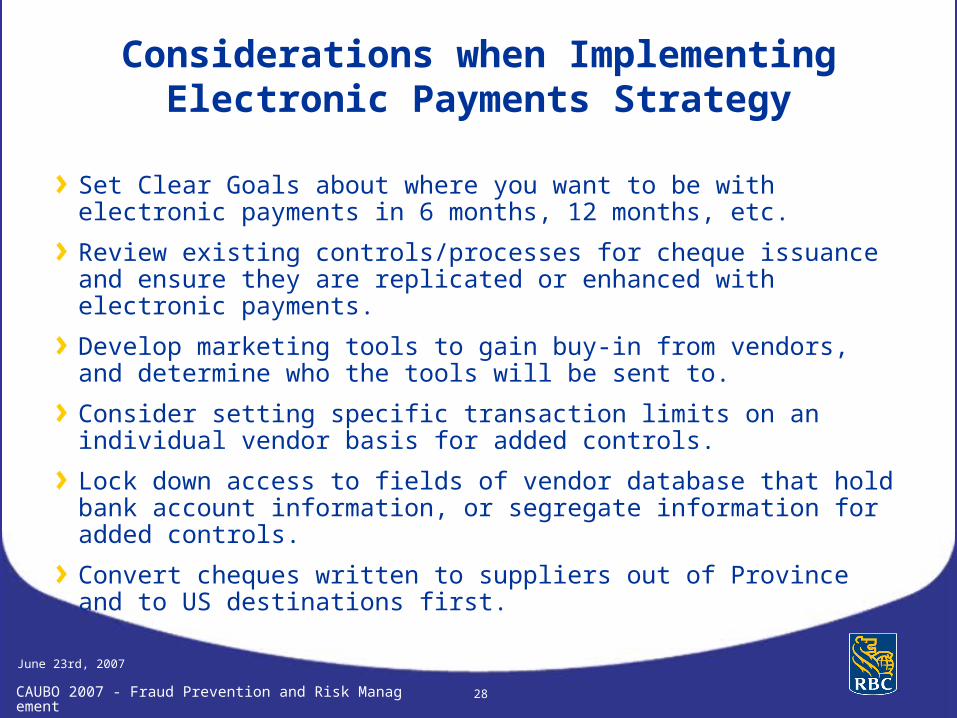

Considerations when Implementing Electronic Payments Strategy

Set Clear Goals about where you want to be with electronic payments in 6 months, 12 months, etc.

Review existing controls/processes for cheque issuance and ensure they are replicated or enhanced with electronic payments.

Develop marketing tools to gain buy-in from vendors, and determine who the tools will be sent to.

Consider setting specific transaction limits on an individual vendor basis for added controls.

Lock down access to fields of vendor database that hold bank account information, or segregate information for added controls.

Convert cheques written to suppliers out of Province and to US destinations first.

CAUBO 2007 - Fraud Prevention and Risk Management

June 23rd, 2007

29

Questions?