42

C ORPORATE P RESENTATION 2018

C O R P O R AT E P R E S E N TAT I O N 2 0 1 8

FOUNDED IN PIRQUE

Public company since 1933. Main ownership in two families with a long-term vision and passion for wine.

CHILE’S LEADINGWINE PRODUCER

HISTORY

2

HIGHLY RECOGNIZED WINE BRAND

LEADING CHILEAN EXPORTER

• 28.2 % by value• 33.3% by volume

LEADING GLOBAL WINE COMPANY

• SALES ~ US$ 1 BILLION• MARKET CAP. ~ US$ 1.7 BILLION

VIÑA CONCHA Y TORO AT A GLANCE

3

4

GLOBAL WINE COMPANY

CONSOLIDATED SALES

(US$ million)

5

528590

643735

872928 957

1018967 977 994

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

AVERAGE ANNUAL GROWTH RATE 7%

SALES VOLUME

(million 9 liter cases)

6

26.3 27.5 28.8 29.7 30.1 30.6 30.733.2 34.3

36.2 34.8

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

AVERAGE ANNUAL GROWTH RATE 3%

AVERAGE PRICE

CAGR +5%

7

SALES BY ORIGIN

CHILE

ARGENTINA

EEUU

81.6%

6.6%

11.8%

CHILE

ARGENTINA

EEUU

86.1%

6.7%

7.2%

VOLUME VALUE

20.4%CHILE*

8

32.7% EUROPE

19.3% USA & CANADA

15.3% LATIN AMERICA

11.0% ASIA &

OCEANIA

1.3% AFRICA & M.

EAST

BREAKDOWN OF SALES BY GEOGRAPHY

5.17.3 11.9 5.7 4.2 0.6

% OF SALES VALUE

VOLUME IN MILLION CASES

* Chile includes sales of “Other Non-Wine Products”

54,973

83,42593,432 92,701

86,267

2013 2014 2015 2016 2017

EBITDA

9

EBITDA & NET INCOME

33,174

43,051

49,797 47,931 49,575

2013 2014 2015 2016 2017

NET INCOME

(in million Ch$)

US$140 mm US$80.6 mm

Year-end exchange rate: Ch$/US$ 614.75

10

COUNTRY POSITION % ON EXPORTED VALUE OF BOTTLED WINE

China #1 10.6%

USA #1 29.8 %

Japan #1 30.1%

Brazil #1 16.5 %

UK #1 42.3 %

Holland #1 23.9 %

Canada #1 33.2 %

Ireland #2 26.4 %

South Korea #1 22.5 %

Mexico #1 50.2 %

TOTAL BOTTLED WINE #1 28.2%

LEADING EXPORTER OF CHILEAN WINE

28.2% of Chilean exports

by value

Source: Vinos de Chile - December 2017

Top 10 markets for Chilean wine

11

TOP 5 - LARGEST WINE COMPANIES

RANKING COMPANY MARKET SHARE BY VOLUME

1 ° E&J Gallo Winery Inc 3.04%

2 ° Constellation Brands Inc 1.80%

3 ° Wine Group Inc, The 1.35%

4 ° Treasury Wine Estates Ltd 1.21%

5 ° Viña Concha y Toro 1.14%

6 ° Castel Groupe 1.07%

7 ° Accolade Wines Ltd 1.05%

8 ° Pernod Ricard Groupe 0.92%

9 ° Grupo Peñaflor SA 0.91%

10 ° FeCoVitA Coop Ltda 0.87%

Source: Passport Euromonitor, The Company. (2016)

12

HIGHLY RECOGNIZED WINE BRAND

#1 Most Admired Wine Brands2011- 2012 – 2013

#2 Most Admired Wine Brands 2017 - 2018

#1 World’s Most Powerful Wine Brand2015

FROM A LEADING GLOBAL WINE COMPANY TO A LEADING CONSUMER - CENTRIC PREMIUM WINE COMPANY

STRATEGIC VISION

BUSINESS MODEL

VERTICAL INTEGRATED MODELINVOLVEMENT OVER ALL THE PRODUCTION PROCESS AND SUPPLY CHAIN,

GUARANTEES THE PRODUCTION OF QUALITY WINES

14

VINEYARDS

FROM THE VINEYARD TO THE BRANDS

DISTRIBUTIONWINEMAKING SUPPLY CHAIN

15

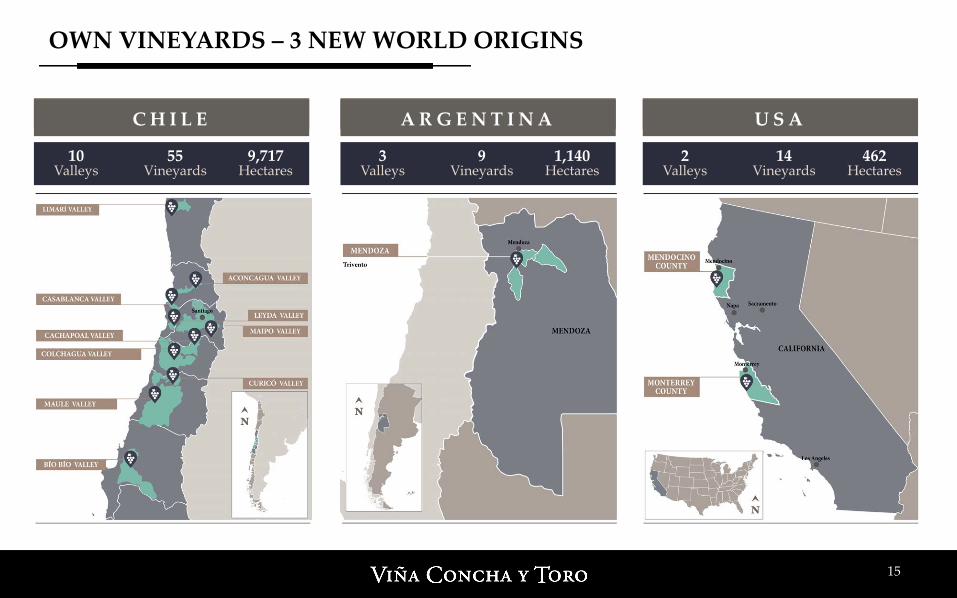

OWN VINEYARDS – 3 NEW WORLD ORIGINS

2 Valleys

14Vineyards

462Hectares

U S A

3 Valleys

9Vineyards

1,140 Hectares

A R G E N T I N A

10 Valleys

55Vineyards

9,717Hectares

C H I L E

Treasury Wine Estates(AUS/USA/NZ/IT)

Constellation (USA/CAD/NZ/IT)

E&J Gallo (USA)

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000

(HECTARES)

11,319

7,247

13,259

VIÑA CONCHA Y TORO (CHI/ARG/USA)

Pernod Ricard (FR/AUS/ARG) 5,611

9,308

TOP 2 - IN TERMS OF SURFACE OF PLANTED VINEYARDS

16

8,782

Efficient and cost-effective operation to deliver world-class products to our customers with high quality standards.

17

SUPPLY CHAIN

U S A A R G E N T I N A

15 Cellar

4Bonling Plants

C H I L E

2 Cellar

1Bonling Plants

1 Cellar

1Bonling Plants

18

KEY MARKETS TO DEVELOP HIGH PERFORMING BRANDS

USA15.7%

CANADA3.5%

MEXICO3.0%

BRAZIL5.6%

CHINA2.7%

JAPAN5.7%

UK17%

NORDICS5.3%

CHILE20.4%

(% of sales by value)

19

• BRAND BUILDING• FOCUS ON VALUE

• Focus in the high-growth and higher-margin segments of the wine industry (>US$10 retail price).

• Brand Matrix: Identifies Potential/Relevance of the brands and aligns sales objectives and marketing investments.

20

SALES & MARKETING STRATEGY - FOCUS ON PREMIUM WINES

2017 SALES MIX (VALUE)

CHILE ARGENTINA USA TOTAL

PREMIUM 41.2% 52.5% 78.5% 46.8%

NON-PREMIUM 58.8% 47.5% 21.5% 53.2%

21

WINERIES AND KEY BRANDS OF THE GROUP

H O L D I N G

CHILE

15.8 MM CAJAS

CHILE

5.1 MM CAJAS

EEUU

2.5 MM CAJAS

ARGENTINA

2.2 MM CAJAS

CHILE

2.2 MM CAJAS

22

CONCHA Y TORO BRAND

FINE WINE PORTFOLIO Heritage and Innovation

CASILLERO DEL DIABLO Premium global brand

23

DON MELCHOR

96 PtsTIM ATKIN

96 PtsWINE SPECTATORHot Wine

94 PtsWINE ENTHUSIASTEditor’s Choice

24

MARQUES DE CASA CONCHA

92 PtsJAMES SUCKLING

90 PtsTIM ATKIN

“Revelation Wine”

93 PtsJAMES SUCKLING

93 PtsTIM ATKIN

93 PtsJAMES SUCKLING

90 PtsTIM ATKIN

CABERNET SAUVIGNONBLACK LABELROSÉ

SUCCESSFUL POSITIONING OF A GLOBAL BRAND IN THE PREMIUM CATEGORY

CASILLERO DEL DIABLO BRAND

USD 205 mm

2017

25

26

CASILLERO DEL DIABLO BRAND

UTRA PREMIUM

SUPER PREMIUM

PREMIUM PLUS

PREMIUM

L E Y E N D A F O B 2 0 0 U S D

R E S E R V A P R I V A D A F O B 6 0 U S D

R E S E R V A F O B 3 5 U S D

D E V I L ’ S C O L L E C T I O N F O B 4 5 U S D

P R E M I U M : 9 3 % U S $ P P , S P , U P : 7 % U S $

3,115 3,3603,777

4,4314,992

5,424 5,224

2011 2012 2013 2014 2015 2016 2017

2017SALES US$: + 2.1% AV. PRICE: + 5.7%

27

CASILLERO DEL DIABLO (THOUSAND CASES)

CAGR : 9%

28

LINE EXTENSIONS TO HIGHER PRICE SEGMENTS

29

BRAND RECOGNITION

91 PtsJAMES SUCKLING

90 PtsWINE SPECTATOR

RESERVA PRIVADA

#2 World’s Most Powerful Wine Brand

WINE INTELLIGENCE

93 PtsJAMES SUCKLING

91 PtsROBERT PARKER

LEYENDA

30

Expressive and innovative wines that

convey the spirit of the New World.

WINERIES AND GROUP BRANDS - CONO SUR

Strong commitment with the environment.

Leading producer of Pinot Noir.

#1 Pinot Noir in

the UK

31

706800

928

1,1201,260 1,326 1,394

2011 2012 2013 2014 2015 2016 2017

PREMIUM FOCUS - CONO SUR BICICLETA (THOUSAND CASES) 2017

SALES US$: + 4.8%

CAGR : 12%

32

Europe’s Most Sold Argentine Wine

Brand

WINERIES AND GROUP BRANDS- TRIVENTO

#1 Malbec in the UKTop 3 exporter from Argentina

33

CAGR+64%

PREMIUM FOCUS - TRIVENTO RESERVE (THOUSAND CASES) 2017

SALES US$ + 14.4%

88

199265

469

642713

2012 2013 2014 2015 2016 2017

34

Leading producer of organic grapes

WINERIES AND GROUP BRANDS - FETZER VINEYARDS

Largest wine company B Corp certified

35

PREMIUM FOCUS - BONTERRA

230

310353 377

446486

559

2011 2012 2013 2014 2015 2016 2017

(THOUSAND CASES) 2017:SALES US$ + 16.9%

36

PREMIUM FOCUS - 1000 STORIES (THOUSAND CASES) 2017

SALES US$ + 33.1%VOLUME + 36%

216

84

113

2014 2015 2016 2017

37

STRONG DISTRIBUTION NETWORK

• Diversification of markets and global presence

• Focus the commercial strategy on priority markets: Those important in value today and those with high future potential.

• Define and execute the best RTM for each of the priority markets.

• Develop and maintain strong relationships with key customers and distributors.

38

VISION OF SUSTAINABILITY

THE COMPANY INCORPORATES INITIATIVES WHICH

CONTRIBUTE TO MANAGING ECONOMIC, ENVIRONMENTAL AND SOCIAL FACTORS IN A BALANCED WAY IN THE ENTIRE

PRODUCTION PROCESS.

RATIONAL USE OF NATURAL RESOURCES

RESPONSIBLE WITH THE ENVIRONMENT

COMMITMENT TO PEOPLE AND COMMUNITIES

RESPONSIBLE SUPPLY

CARBON FOOTPRINT Measured since 2007

WATER FOOTPRINT Measured since 2010

RENEWABLE ENERGIES

NATIVE FOREST

39

• Light botles, 99% of total portfolio.• 30% reduction of the Carbon Footprint since 2012.

• 100% drip irrigation system in own vineyards.• Water Footprint 40% lower than the average of the global industry.

65% clean energy supply. moving towards the certification of the Energy Footprint aiming to reach 100% in 2020.

15% of suppliers respond to a program of good social and environmental practices.

Conservation of 3,372 certified and protected hectares, 100% with biodiversity inventories.

2020 Sustainability Strategy aligned with the United Nations SDGs.SUSTAINABILITY STATEGY

DOW JONES SUSTAINABILITY INDEX

Top 10 Beverages categoryViña Concha y Toro

OUR JOURNEY

VISION OF SUSTAINABILITY

BIDA BIOFILTER

· 100% waste water reuse.

· 85% more efficient.

CARBON NEUTRAL

First North American winery certified as “Carbon

Neutral".

40

UNITED NATIONS

Momentum For Change Climate solution Award

2017

FETZER VINEYARDS

First California winery that works completely with renewable energy.

VISION OF SUSTAINABILITY

41

CENTER FOR RESEARCH AND INNOVATION

Unique R+D+i winemaking research

center in Latin America

Scientific-technological innovation to face the

challenges of the business.

Technological development and knowledge exchange, for a more

competitive wine industry.MM $ 2,513

Investment in R+D

• More than 70 R+D projects in course • 54 extension activities during 2017

• 1,500m2 of modern modular building

• Cuning-edge equipment

42

CENTER FOR RESEARCH AND INNOVATION

STATEGIC R+D PROGRAMS

• Plant production health• Quality of grapes and wines• Water resources and climate change

• New product design• Smart wine industry

STATEGIC PARTNERSHIPS