1 China and Latin America’s Emerging Economies: Debates, Dynamism, and Dependence Carol Wise and Yong Zhang Abstract The tendency in the existing literature on the relationship between China and the Latin American and Caribbean (LAC) countries has been to treat the effect of China’s rise in this region over the past decade as more or less uniform, especially with regard to the South American countries. However, in this analysis of China’s impact on LAC’s top four emerging economies (Argentina, Brazil, Chile, and Mexico) we argue that the effect of China has varied significantly according to a given country’s factor endowments, institutional landscape, and the development trajectory underway at the turn of the new millennium. We begin by considering the main debates that have surrounded the phenomenon of China’s rapid entry into Latin America in the 2000s. In light of these debates, we rely on country sketches to illuminate how growing economic ties with China has shaped the development dynamic within each country. For the most part, we find that the rise of China in Latin America has highlighted a large reform deficit in the microeconomic realm and the urgency with which all four countries considered here need to articulate a much bolder development strategy based on higher spending allocations for science, technology, R&D, education, and infrastructure Paper presented on the panel “The Political Economy of China-Latin American Relations,” ISA-FLACSO Conference, Buenos Aires, Argentina, July 25, 2014.

Transcript

1

China and Latin America’s Emerging Economies:

Debates, Dynamism, and Dependence

Carol Wise and Yong Zhang

Abstract

The tendency in the existing literature on the relationship between China and the Latin American

and Caribbean (LAC) countries has been to treat the effect of China’s rise in this region over the

past decade as more or less uniform, especially with regard to the South American countries.

However, in this analysis of China’s impact on LAC’s top four emerging economies (Argentina,

Brazil, Chile, and Mexico) we argue that the effect of China has varied significantly according to

a given country’s factor endowments, institutional landscape, and the development trajectory

underway at the turn of the new millennium. We begin by considering the main debates that

have surrounded the phenomenon of China’s rapid entry into Latin America in the 2000s. In light

of these debates, we rely on country sketches to illuminate how growing economic ties with

China has shaped the development dynamic within each country. For the most part, we find that

the rise of China in Latin America has highlighted a large reform deficit in the microeconomic

realm and the urgency with which all four countries considered here need to articulate a much

bolder development strategy based on higher spending allocations for science, technology, R&D,

education, and infrastructure

Paper presented on the panel “The Political Economy of China-Latin American Relations,”

ISA-FLACSO Conference, Buenos Aires, Argentina, July 25, 2014.

2

Introduction

It would be difficult to exaggerate the sea change that has occurred within Latin

America’s emerging economies (EEs) as a result of China’s phenomenal rise within the

international political economy over the past two decades. Although a great deal has already

been written about the explosion of trade and investment ties between China and the region’s top

four emerging economies1---Argentina, Brazil, Chile, and Mexico---during the 2000s, less has

been said about the larger political economic dynamic that has evolved within each of these

countries under the thrust of this budding relationship. While empirical analyses of the China-

Latin America relationship confirm that China still represents a small share of trade, foreign

direct investment (FDI) and aid flows to the region, our focus is on the remarkable opportunities

and visible constraints that China’s entry into the region has already augured for the ongoing

development strategy in place within these four emerging economies in the 2000s.

First, is the effect of China’s voracious demand for commodities in the 2000s, as the

beginning of the new millennium marked China’s entry into the World Trade Organization and

its need for massive commodity inports to fuel a new development phase. The result for

Argentina, Brazil, and Chile was a spike in prices for soya, fishmeal, iron ore, copper, tin, zinc,

and oil, all of which are abundant to varying degrees in these countries. Second, although

China’s momentum for outgoing FDI has been slow, it has taken off in two of these Latin

American EEs (Argentina and Brazil) in ways that were simply unimaginable a decade ago (see

1 See, for example, R. Evan Ellis, China in Latin America: The Whats & Wherefores (Boulder and London: Lynne

Rienner Press, 2009); Rhys Jenkins, “China’s Global Expansion and Latin America,” Journal of Latin American

Studies, vol. 42, no. 1 (November 2010), pp. 809-837; Kevin P. Gallagher and Roberto Porzecanski, The Dragon in

the Room: China and the Future of Latin American Industrialization (Stanford: Stanford University Press, 2011);

and, Adrian H. Hearn and José Luis Léon-Manríquez, eds., China Engages Latin America: Tracing the Trajectory

(Boulder and London: Lynne Rienner Press, 2011).

3

tables 1 and 2). Thus far, the bulk of these investments and the loans that have accompanied

them have gone toward resource extraction. Although Latin America now accounts for about 15

percent of Chinese FDI (versus 65 percent for Asia),2 the pattern is a very lopsided one.

<insert tables 1 & 2>

<insert figure 1>

Third, China has become an important engine of growth for Latin America. This became

apparent when the four emerging economies considered in this article rebounded along with

China from the 2008-09 global financial crisis in 2010, while the OECD bloc has remained

mired in recession and financial instability. Although the shocks that hit the region in 2008 were

financial in nature, the recovery was trade-led and China was largely the leader.3 At the same

time, the Chinese government signed currency swap agreements with Argentina (2009) and

Brazil (2012) to facilitate bilateral trade and lower transaction costs, and it negotiated a loan-for-

oil agreement with Brazil in 2009.

On balance, the relationship between these newfound friends has been favorable but

contradictory, rendering debates about the political economy of China-Latin American relations

in the 2000s somewhat bipolar. With this political economy analysis of China’s relationship

with Argentina, Brazil, Chile, and Mexico we seek to steer away from the normative tone of

many assessments, highlight the complexities, and size up the benefits and costs for the countries

involved.4 In so doing we begin with an analysis of the political economy debates over the

2 Eduardo Daniel Oviedo, “Argentina Facing China: Modernization, Interests, and Economic Relations Model,” East

Asia, vol. 30 (2013), p. 27. 3 Su Zhenxing and Yong Zhang, “Guoji jinrongweiji beijingxia de Zhongla jingmao hezuo” (“An Analysis of

Economic Cooperation and Trade between China and Latin America in the Context of the International Financial

Crisis”), Ladingmeizhou he Jialebi fazhan baogao 2009-2010 (Development Report of Latin America and the

Caribbean 2009-2010), (China: Social Sciences Academic Press, 2010). 4 More nuanced assessments can be found in Daniel P. Erikson, “Conflicting US Perceptions of China’s Inroads in

Latin America,” in Adrian H. Hearn and José Luis Léon-Manríquez, eds., China Engages Latin America, pp. 117-

4

evolving China-Latin American relationship, with an eye toward its impact on the development

model of the four countries under study. We then turn to an empirical section which reviews

those patterns of economic performance within these four EEs from 2003-2012. A third section

examines the data from the standpoint of the pitfalls in the China-Latin America relationship,

including the growing concern about Latin America’s over-dependence on Chinese demand.

Here, we argue that it is less an issue of LAC’s increased structural dependence on China that

endangers growth and development in these EEs and more a matter of path dependence, whereby

current policy choices are limited by “an initial set of institutions that provide disincentives to

productive activity.”5 A fourth section of the papers offers conclusions.

Debates

China’s Impact on the Development Strategies of Latin American EEs?

As tempting as it was for the US Treasury Department and international financial

institutions (IFIs) to chide Latin American policy makers for falling off the neoliberal

bandwagon in the wake of the Argentine financial crisis in the early 2000s,6 by that time market

reforms based on privatization, liberalization and deregulation had actually run their course in

the region with very mixed results. 7 With the exception of Brazil, the path followed by the other

three EEs could perhaps best be described as the polar opposite of the Chinese way.8 The highly

135; and, Jiang Shixue, “The Chinese Foreign Policy Perspective,” in Riordan Roett and Guadalupe Paz, eds., China’s

Expansion into the Western Hemisphere (Washington, DC: Brookings Institution Press, 2008). 5 Douglass North, Institutions, Institutional Change, and Economic Performance (Cambridge: Cambridge

University Press, 1990), p. 99. 6 Paul Blustein, And the Money Kept Rolling In (And Out) (New York: Public Affairs Books, 2005). 7 Nancy Birdsall and Augusto de la Torre, Washington Contentious (Washington, DC: Carnegie Endowment for

International Peace, 2001). 8 Barry Naughton, The Chinese Economy: Transitions and Growth (Cambridge: The MIT Press, 2006); and, Robert

Devlin, “China’s Economic Rise,” in Riordan Roett and Guadalupe Paz, eds. China's Expansion into the Western

Hemisphere.

5

diverse outcomes of market reform in Latin America makes it difficult to entirely dispense with

this so-called neoliberal model; yet, the region’s comparatively lower performance in terms of

per capita growth, investment, productivity, and technological innovation suggests that the more

beneficial path forward lies in the moderated reform pace and hands-on public policy

interventions that has characterized the Chinese model. At play here is the exhaustion of rigid or

dogmatic notions of laissez-faire in LAC and the demonstration effect of China’s indisputable

success with more proactive approaches.9

In Argentina, Brazil, and Mexico, for example, the rapid and simultaneous liberalization

of trade and finance in the early 1990s and the failure to coordinate these policies with ongoing

efforts at privatization and deregulation proved to be explosive. The Mexican currency crisis of

1994 quickly drove home the difficulties of exchange rate management under new conditions of

high capital mobility based on securitized financial instruments. Even Brazil, which moved

more cautiously with privatization and the liberalization of trade and the capital account,10 could

not avoid its own devaluation crisis in 1999. The Argentine financial blow-up of 2001-02 was a

more drastic variation on this theme, the result being a US$100 billion default on the country’s

publicly held debt and a massive rejection of market reforms at the polls. In all of these cases,

the loss of real income at the level of working people tarnished the neoliberal mantle, even if a

considerable part of the problem was half-hearted implementation and reckless risk-taking by

economic decision-makers, especially in Argentina and Mexico.

Unequal Exchange and the Shadow of the Past?

9 Jiang Shixue, “Lamei jingji he Zhongguo yinsu” (“Latin American Economies and the China Factor”), Dangdai

shijie (The Contemporary World, no. 12, 2012). 10 Albert Fishlow, Starting Over: Brazil since 1985 (Washington, DC: Brookings Institution Press, 2011).

6

Some of the best scholars now writing on the political economy of China-Latin American

relations have expressed concern that today’s pattern of exchange harkens back to the turn of the

last century, a time when LAC’s primary exports to the North were offset by the import of

manufactured and intermediate capital goods back from the developed countries.11 Yet, whereas

the earlier experience with this pattern of trade invoked policies of import-substitution and a

widespread critique concerning the unfavorable terms of trade for the region12---as the price of

manufactured imports continued to rise while commodity exports were plagued by cyclical price

downturns---the structural conditions that now prevail within most of these economies are

markedly different. With the exception of Chile, considerable inroads have been made with

industrialization and manufactured goods now account for some 40 percent of all regional

exports. Moreover, the terms of trade for all four countries have held quite steady in the 2000s.

The issue this time around is that the nature of those goods being imported is higher in

knowledge content, value-added and technological inputs, and China accounts for a steadily

increasing share in these domestic markets. What has not held steady is the ability of the four

LAC EEs in this study to keep pace with the competitiveness gains that China has registered in

its manufacturing sector over the past twenty years, advances which are the result of highly

focused expenditures and policies that have promoted science, technological adaptation,

advanced education in hard science fields, and research and development since the early 1980s.13

11 See, for example, Jaime Ortiz, “Déjà vu: Latin America and Its New Trade Dependency…This Time with China,”

Latin American Research Review, vol. 47, no. 3 (2012), pp. 175-190; and, Ruben Gonzalez-Vicente, “The Political

Economy of Sino-Peruvian Relations: A New Dependency?” Journal of Current Chinese Affairs, vol 41, no. 1

(2012), pp. 98-131. 12 The seminal work on this is Raúl Prebisch, The Economic Development of Latin America and Its Principal

Problems (New York: United Nations, Department of Social Affairs, 1950). 13 See Sunil Mani, “Have China and India Become More Innovative since the Onset of Reforms in the Two

Countries?” in Amiya Kumar Bagchi and Anthony P. D’Costa, eds., Transformation and Development: The

Political Economy of Transition in India and China (New Delhi: Oxford University Press, 2012); and, Kevin P.

Gallagher and Roberto Porzecanski, The Dragon in the Room, chapter 3.

7

In numerous interviews that we conducted for this study, with policy makers, producers, and

local private sector analysts in all four countries, one of the most frequently mentioned themes

was the conviction that all of these countries should be trying harder to export non-traditional

higher-value-added products to the Chinese market. Remarkably, however, with the exception

of Chile, any serious national public debate along these lines seems to have been eclipsed by the

aura of plenty that has prevailed for most of the 2000s.

Moreover, due to higher costs, geographical disadvantages, and technological deficits, the

ability of these countries to export higher value-added goods to China is not likely, at least not in

the near future. Rather, the current juncture is a time for these countries to take stock of their

own export and production capabilities and to focus on the very features of the Chinese strategy

that could enhance their competitiveness in regional and world markets overall. At a minimum,

this would include the articulation of a longer-term vision for strengthening domestic productive

capacity, one based on higher spending allocations on science, technology, R&D, education, and

infrastructure.14 Based on his econometric analysis, Ortiz argues that LAC “has reached a point

in its production possibilities frontier at which it is not feasible to further increase its level of

output unless technology and innovation come into play. Latin America must broaden its

productivity base, move into more sophisticated endeavors, and diversify its export basket to

gain market share.”15 Even the earlier theorists of unequal exchange advocated technology

adaptation and export diversification.16 It’s the delay in going full speed ahead with these policy

reforms that calls up images of path dependence in twenty-first century Latin America.

14 Robert Devlin, “China’s Economic Rise,” pp. 137-139. 15 Jaime Ortiz, “Déjà vu: Latin America and Its New Trade Dependency,” p. 188. 16 Raúl Prebisch, The Economic Development of Latin America and Its Principal Problems.

8

“Dutch Disease” Latin American-style?

The flip side of large capital inflows to the South American EEs since 2003 and the

accumulation of historically high levels of foreign exchange reserves has been a considerable

overvaluation of their currencies, a phenomenon that some are now referring to as a case of

“financial Dutch-disease.”17 The term Dutch disease first referred to the decline of the Dutch

manufacturing sector in the 1970s due to the discovery and development of natural gas in the late

1950s. As high natural gas prices triggered a foreign exchange boom and in turn, currency

appreciation, industrial exports and jobs languished. The fact that manufactured exports still

account for 40 percent of all LAC exports suggests that it would be premature to diagnose a

generalized case of traditional Dutch disease in the region.18

But financial Dutch disease is another matter. As heavy Chinese demand for South

American commodities continues to push prices upward, and the US Fed’s commitment to a

zero-interest rate policy since 2009 pushes funds outward toward the emerging markets, the

sheer mass of capital inflows and related currency appreciation have placed intense inflationary

pressures on all but Mexico. Chile and Brazil have acted quickly in combating inflation with a

combination of interest rate hikes, sterilizing interventions and capital controls. Argentina, as

can been seen in table 3, has been lax in fighting inflation and on this indicator has fallen back

onto its perilous pre-reform path. Apart from the need to tightly manage inflation, all three

South American countries face the ultimate challenge of channeling these incoming capital flows

into domestic savings and much higher levels of productive investment. However, when

comparing China and the LAC region, the latter’s deficit in terms of Gross Capital Formation

17 Mauricio Cardenas, “Curbing Success in Latin America.” 14 April 2011.

http://www.brookings.edu/opinions/2011/0414_curbing_success_cardenas_yeyati.aspx 18 Yong Zhang, “Development of China’s Trade with Latin America and the Caribbean and Its Challenge,” figure 7.

9

(GCF) is a bit startling. From 2000-2008, for example, LAC’s GCF rate averaged less than 19

percent of GDP; conversely, China’s average rate of GCF between 2000-20012 was over 42

percent, more than double the LAC figure.19

<insert table 3>

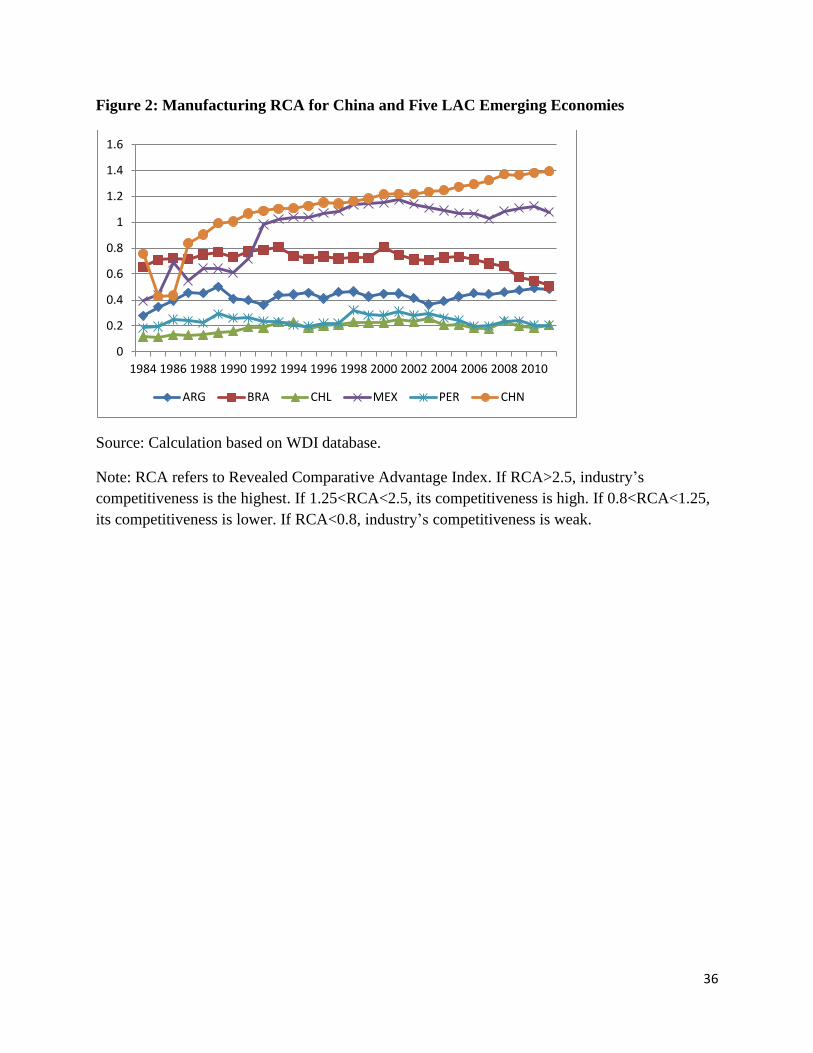

Another wake-up call appears in figure 2, where the “revealed comparative advantage”

(RCA) of Brazil’s manufacturing sector has declined in the 2000s. Some of the more powerful

industrial groups in Sao Paulo have blamed this trend on Chinese manufacturing exports to

Brazil; as a result, the Brazilian government has ratcheted up protectionist measures against

China and the PRC has responded in kind.20 But financial Dutch Disease has also kicked in here,

as the Brazilian real has been steeply over-valued since the onset of hefty capital inflows in the

early 2000s. Although Brazilian policy makers have complained that China’s under-valued

currency has put domestic exporters at a distinct disadvantage, Barry Eichengreen and others

argue that the Chinese yuan has appreciated considerably since 2005.21 It is just as likely that

Brazil’s unduly strong currency that has favored manufactured imports and penalized industrial

exports in the 2000s.22

<insert figure 2>

Dynamism

19 Yong Zhang, “Development of China’s Trade with Latin America and the Caribbean and Its Challenge,” tables 6

and 7. 20 Rhys Jenkins, “China and Brazil: Economic Impacts of a Growing Relationship,” Journal of Current Chinese

Affairs, vol. 41, no. 1 (January 2012), pp. 26-29. 21 Comments made by Prof. Barry Eichengreen on a panel entitled “China and Latin America: Perceptions,

Problems, and Opportunities,” co-sponsored by the Center for Latin American Studies and the Institute of East

Asian Studies, UC Berkeley, February 12, 2013. http://clas.berkeley.edu/event/china-and-latin-america-perceptions-

problems-and-opportunities (Accessed October 12, 2013). 22 Alexandre De Freitas Barbosa, “The Rising China and Its Impacts on Latin America: Strategic Partnership or a

New International Trap,” paper presented at the VIII Reunión de la Red de Estudios de América Latina y el Caribe

Macroeconomic Prudence versus Microeconomic Doldrums

At the turn of the new millennium there was little to suggest that a take-off was in the

making for Latin America’s emerging economies. The US had yet to rebound from the 2000

dot.com bust when the 9/11/01 terrorist attacks hit New York and Washington and this worked to

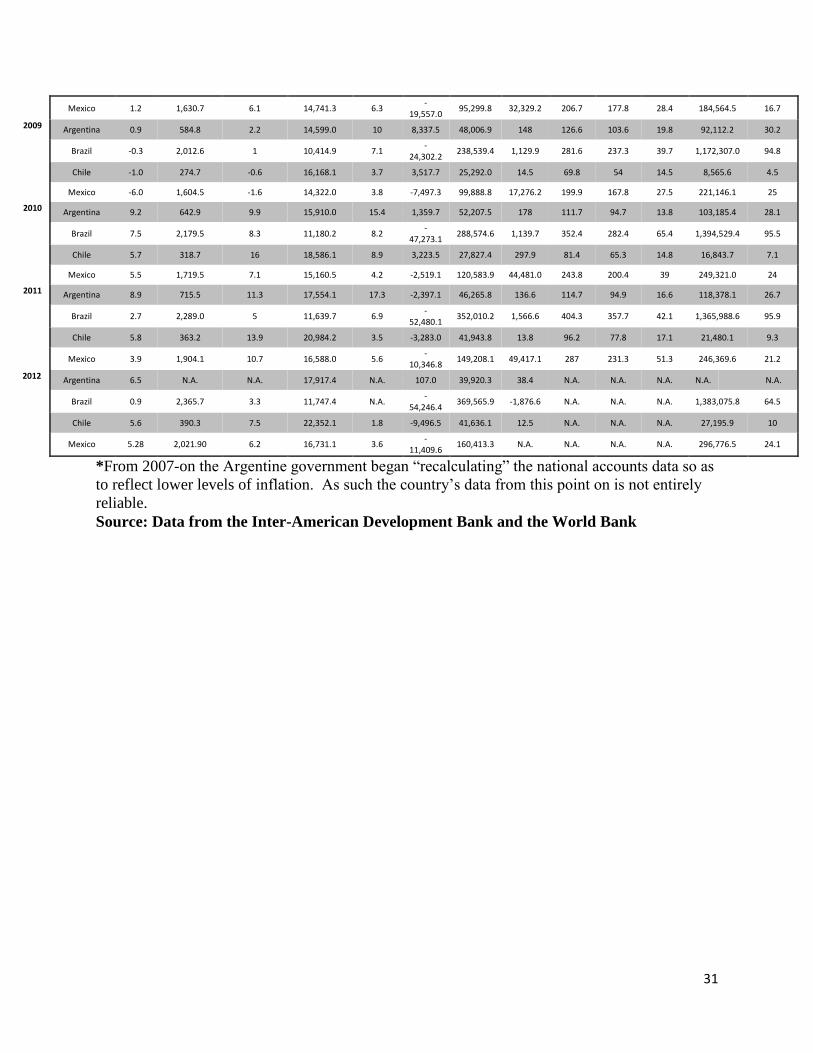

prolong a global recession. The data on average GDP growth rates for the four Latin American

EEs in table 3 ranged from dismal (Argentina) to lackluster (Brazil) between 2000 and 2002.

However, in 2004 China’s trade with all four countries began to climb quickly,23 the result being

LAC’s abrupt exit from the global recession and a higher pace of average aggregate growth than

in the OECD bloc. Again, it is important not to exaggerate the weight of China in Latin

America’s turnaround. In 2007, on the eve of the global financial crisis, Rhys Jenkins estimates

that the net impact of Chinese demand on export earnings for the Latin American region was

between 13 to 23 percent for that year.24 Yet, table 4 shows that for the four emerging

economies analyzed here, the projected effect of Chinese demand on net export earnings in 2007

varied more widely, with Chile’s range of a 28.8 to 47.8 percent net effect versus Argentina’s

range of 6.9 to 11.9 percent.

<insert table 4>

The five year span between 2003 and 2008 was a brief golden age for all four EEs

analyzed here. Mexico rebounded on the strength of global oil prices, with Chinese demand

spurring a petroleum price boom, even if Mexico exported little of its own oil supply to China.

For Argentina, Brazil and Chile, the combination of China’s annual average growth rate of 9-10

percent during this period and the increase in capital inflows due to the US Federal Reserve

23 See figures 1, 2, and 3 in Yong Zhang, “Development of China’s Trade with Latin America and the Caribbean and

Its Challenge.” 24 Rhys Jenkins, “The ‘China Effect’ on Commodity Prices and Latin American Export Earnings,” CEPAL Review,

vol. 103 (April, 2011), p. 84.

11

Bank’s low interest rate policy provided the stimulus for high aggregate growth and an

impressive leap in per capita GDP. Inflation was running in the single digits and reserves were

rapidly accumulating. Despite the vociferous turn away from the Washington Consensus,

particularly in Argentina and Brazil, this period reflected the strength of institutional reforms that

had been implemented in the 1990s in the realm of banking, finance, and macroeconomic policy

making.25

The 2008-09 global financial crisis further tested the extent to which macroeconomic

policy approaches had been institutionalized across Latin America. Alejandro Izquierdo and

Ernesto Talvi offer the following assessment of the region’s macroeconomic fundamentals and

collective ability to hold its own when faced with an external shock of this magnitude:

“In 2007 the region exhibited an overall fiscal surplus of 1.9 percent of

GDP compared to a deficit of 0.9 percent of GDP at the onset of the {1997-98}

Asian/Russian crisis. Public debt-to-GDP ratios plummeted from an average of 52

percent in 2003---the end result of a period of financial crises---to 35 percent by

end-2007….The banking sector also showed significant signs of improvement as

non-performing loans declined sharply, sliding all the way from close to 10

percent of total loans in 2002 to 2.5 percent by end-2007…International reserves,

at around US$140 billion in 2002, more than tripled to US$ 447 billion by June

2008.” 26

Perhaps for the first time ever, the combination of a fiscal surplus, banking sector reform and a

large foreign exchange cushion positioned policy makers within all four of the EEs in table 3 to

respond to the crisis with counter-cyclical policies that eased the pain of adjustment.

25 Leslie Armijo, Carol Wise, and Saori Katada, “Introduction,” in Carol Wise, Leslie Armijo, and Saori Katada,

eds., Unexpected Outcomes: How Emerging Markets Survived the 2008-09 Global Financial Crisis (Washington,

DC: Brookings Institution Press, 2014), pp. 15-20. 26 Alejandro Izquierdo and Ernesto Talvi, Policy Trade-offs for Unprecedented Times: Confronting the Global

Crisis in Latin America and the Caribbean (Washington, DC: Inter-American Development Bank, 2009), p. 5.

12

However, in all four EEs in table 3, this macroeconomic dynamism has been offset by a

slippage in global competitiveness rankings between 2007-08 and 2013-14 for all but Brazil.

Table 5 shows the 2013-14 rankings from the World Economic Forum’s annual Global

Competitiveness Report.27 Most notable is China’s 5-point gain since 2007-08, which ranks it as

more competitive than any of the four Latin American EEs in the table. Moreover, as China

moved up in the rankings, Argentina, Chile and Mexico all moved down. Brazil has jumped 16

points in the competitiveness rankings since 2007-08, albeit from a very low starting point.

Other measures of economic modernization and openness are displayed in table 6. Not

surprisingly, China scores poorly on the Heritage Foundation’s “Economic Freedom Index,” but

it does out-perform Argentina on this measure. Moreover, China out-performs all four of the

Latin American EEs on two key measures (registering property and enforcing contracts) in the

World Bank’s “ease of doing business survey,” and it beats out Argentina and Brazil on the

“overall ease of doing business” measure.

<insert tables 5 & 6>

It was on this very question of competitiveness and microeconomic restructuring that

Washington Consensus reforms based on deeper liberalization and deregulation had stalled in the

late 1990s in Argentina, Brazil, and Mexico. A stark reality of this period was the failure of per

capita growth and employment creation to keep pace with the positive aggregate returns. The

2000-03 global recession exacerbated these trends until, seemingly out of nowhere, the

commodity lottery struck; China suddenly became a crucial intervening variable for all four

Latin American EEs analyzed here. The following brief country sketches highlight the profound

but highly variable effects that this evolving economic relationship with China has had on

27 See Klaus Schwab, ed., The Global Competitiveness Report 2013-2014 (Switzerland: World Economic Forum,

2013). Also see: www.weforum.org/gcr.

13

development strategies in each of these four countries. The analysis shows that there is no single

China-Latin America political economy profile, but rather a set of preliminary outcomes that

vary according to a given country’s factor endowments, institutional landscape, and the

development trajectory underway when Chinese trade and investment began to take off in Latin

America in the early 2000s.

Country Sketches: Varieties of Capitalist Development (from North to South)

Mexico

In one of the earliest and most comprehensive reports on China-Latin American relations

in the 2000s Robert Devlin and his co-authors point to Mexico as a potential “loser” due to its

high export similarity index (ESI) with China and the strong overlap in goods that both China

and Mexico are exporting to the US market.28 Indeed, by 2003 China had displaced Mexico as

the second most important US trade partner; over the period 2000-05 Mexico had increased its

share of US imports by 25 percent, while China’s share of US imports grew by 143 percent;29 by

2011, 31 percent of all US imports from Mexico were deemed to be under “direct threat” from

Chinese competition in the US market and some 46 percent of Mexico’s manufacturing exports

to the US were classified in this same category.30 Apart from this head-on competition from

China in the US market, China accounted for around 15 percent of Mexico’s imports in 2011 but

28 Robert Devlin, Antoni Estevadeordal, and Andrés Rodríguez-Clare, eds., The Emergence of China: Opportunities

and Challenges for Latin America and the Caribbean (Cambridge: Harvard University Press, 2006). 29 Ralph Watkins, “Meeting the China Challenge to Manufacturing in Mexico,” in Enrique Dussel Peters, Adrian

Hearn, and Harley Shaiken, eds., China and the New Triangular Relationships in the Americas (Miami: Center for

Latin American Studies, University of Miami, 2013), p. 38. 30 Kevin P. Gallagher and Enrique Dussel Peters, “China’s Economic Effects on the U.S.-Mexico Trade

Relationship. Towards a New Triangular Relationship?” in Enrique Dussel Peters, Adrian Hearn, and Harley

Shaiken, eds., China and the New Triangular Relationships in the Americas, pp. 18-19.

14

just 2 percent of its exports.31 In contrast to the South American EEs, Mexico does not have an

ample supply of oil or other raw materials to sell to China, the result being a burgeoning

manufacturing trade deficit with China in the 2000s (see table 3). Chinese FDI to Mexico lags

far behind Argentina and Brazil (see tables 1 & 2), with a modest presence in computers and

autos, as shown in figure 1.

The irony for Mexico is that policy makers there spent the last twenty years working to

diversify the country’s exports away from primary products. Although they largely succeeded,

they took the market route toward restructuring and did so via Mexico’s entry into the North

American Free Trade Agreement (NAFTA) with Canada and the US in 1994. Under NAFTA,

Mexico’s expectation was that, by liberalizing its trade and investment regimes, it could count on

US FDI and the heightened competition from US imports to force a restructuring of the domestic

industrial sector.32 Industrial policy was tapered off and the tough tasks of technology

acquisition and adaptation were basically turned over to foreign companies operating in export

production zones located in central and northern Mexico. Figure 2 shows that Mexico is the only

Latin American EE that comes close to China in terms of the RCA (revealed comparative

advantage) of its manufacturing sector;33 it has outpaced Brazil on this measure, but is also

struggling to regain the competitiveness peak it had reached at the outset of the 2000s.

Hindsight suggests that Mexico’s entry into NAFTA has been as much a burden as a

blessing. Back in the early 1990s newly converted neoliberal technocrats sought NAFTA entry

as a way to permanently lock-in market reforms and implement new ones. But NAFTA

31 Kevin P. Gallagher and Enrique Dussel Peters, “China’s Economic Effects on the U.S.-Mexico Trade

Relationship. Towards a New Triangular Relationship?” p. 15. 32 Carol Wise, “Unfulfilled Promise: Economic Convergence under NAFTA,” in Isabel Studer and Carol Wise, eds.,

Requiem or Revival? The Promise of North American Integration (Washington, DC: Brookings Institution Press,

2007). 33 Also see Kevin P. Gallagher and Roberto Porzecanski, The Dragon in the Room, p. 68.

15

membership also cemented the country’s overwhelming trade and investment dependence on the

US market. In 2011, 89 percent of Mexican exports that incorporate imported inputs were

destined for the US market.34 Having harnessed the country’s economic fate to NAFTA,

Mexican politicians and policy makers have spent most of the 2000s crafting protectionist tariffs

on Chinese manufacturing imports and stalling on the completion of essential reforms. As

recently as 2012, this reform lag included fiscal policy, utility inputs, oil production, labor

markets, anti-trust, and education35----all of which are essential for the country to climb up the

industrial ladder on par with China.

Despite Mexico’s obvious geographic advantage over China, the latter has gradually

eclipsed Mexico in the US manufacturing market by virtue of its lower overall costs and by

actively deploying public policy in the expansion, upgrading and infusion of technology into its

manufacturing sector.36 The World Economic Forum’s Global Competitiveness Report 2013-

2014 further refines the differences between China and Mexico; with regard to those indicators

(FDI and technology transfer, local supplier quality, and sophistication of production

processes)37 that reflect an industrial model like Mexico’s, with its strong orientation toward FDI

operating in export processing zones, Mexico readily outshines China in the rankings.

Conversely, on those indicators (capacity for innovation, company spending on R&D,

availability of scientists and engineers, venture capital availability, and ease of access to business

loans)38 that capture the development of an endogenous industrial model like China’s, one that is

34 Ralph Watkins, “Meeting the China Challenge to Manufacturing in Mexico,” p. 43. 35 Carol Wise, “Unfulfilled Promise: Economic Convergence under NAFTA.” 36 Robert Devlin, “China’s Economic Rise,” pp. 137-139. 37 Klaus Schwab, ed., The Global Competitiveness Report 2013-2014, pp. 512, 525, 530. 38 Klaus Schwab, ed., The Global Competitiveness Report 2013-2014, pp. 503, 504, 534, 536, 539.

16

steadily accruing value-added and absorbing new technologies,39 China basically leaves Mexico

in the dust.

Brazil

Now ranked as the world’s sixth largest economy, political and economic elites in Brazil

have converged around a gradualist strategy that has incorporated market norms into a

developmental capitalist framework. Like Mexico, Brazil’s banking and financial sector reforms

have been impressive, as indicated by its timely recovery from the 2008-09 global financial

crisis. On an index of trade openness Brazil’s ranking is 71.6 on a scale of 1-100 (with 100

being the most open), versus 80.2 for Mexico and 85.8 for Chile. Nassif argues that Brazil’s

comparatively higher level of protection reflects how “the country has sacrificed higher and

more productive growth over the past twenty years due to the partial and incomplete nature of its

microeconomic reforms.”40 This statement is borne out by the data on Brazil’s lagging

competitiveness in tables 5 and 6.

All of the various ways of measuring the impact of China on Brazil suggest that the

situation is worlds apart from that which Mexico now faces vis-à-vis China in both its home

market and in the US. Table 4 estimates the effect of Chinese demand on Brazil’s net export

earnings in 2007, which was 16 percent at most and as high as 25 percent from 2007-2012;41 as

39 Bikramjit Sinha, “Increasing Industrialization of R&D in China,” in Amiya Kumar Bagchi and Anthony P.

D’Costa, eds., Transformation and Development. 40 André Nassif, “Brazil and India in the Global Economic Crisis,” in Sebastian Dullien et al. eds., The Financial

and Economic Crisis of 2008-2009 and Developing Countries (New York and Geneva: United Nations, 2010). Also

see Yong Zhang, “Baxi jingji zengzhang fangshi zhuanxing he jiegou yanbian” (“The Transformation and Structural

Reform of the Economic Growth Model in Brazil”), in Veloso Pereira and Zheng Bingwen, eds, Kuayue zhongdeng

shouru xianjing: Baxi de jingyan jiaoxun (Surmounting the Middle Income Trap: the Main Issues for Brazil),

(China: Economy & Management Publishing House, 2013). 41 Rhys Jenkins, “China and Brazil: Economic Impacts of a Growing Relationship.”

17

of 2011 China accounted for about 15 percent of Brazil’s imports and 17 percent of its exports;42

and, from 2000 to 2011 bilateral trade between the two countries grew by more than 2000

percent.43 As of 2012, Brazil’s trade surplus with China was over US$18 billion,44 and China’s

FDI stock in Brazil towered over the other three EEs analyzed in this paper (see table 1). A

sticking point for Brazil is that in 2006 its volume of raw material exports surpassed that of

manufactured goods for the first time since the early 1990s and Brazilian industrial producers are

feeling the pinch in both domestic and third country markets. In 2011Brazil’s GDP growth

dropped by 5 percentage points over the previous year and by 2012 it had all but stalled (see

table 3).

The country’s economic slowdown since 2011 suggests that currency reform, including a

floating exchange rate, and sustained macroeconomic stabilization are necessary conditions for

growth but not entirely sufficient. In this respect, Brazil’s thick regulatory/bureaucratic

overhang reflects the extent to which this version of the developmental capitalist model is still

too much of a drag on growth. Whereas the average South American rate of government

spending as a percent of GDP is about 26 percent, Brazil stands at 40 percent. The private

banking sector, meanwhile, has made itself scare. Interest rates are off the chart and Brazil has

some of the highest risk spreads in the world. In 2012, the private sector provided just 12.8

percent of long-term financing, while the state-owned development bank (BNDES) provided

around 72.4 percent.45 Between 2000-2012 Brazil’s total foreign exchange reserves increased

11-fold and stood close to US$370 billion at the end of 2012. This scenario is precisely what we

42 IDB DataIntal. 43 Daniel Cardoso, “China-Brazil: a Strategic partnership in an Evolving World Order,” East Asia, vol. 30, no. 1

(2013), pp. 31-51. 44 Yong Zhang, “Development of China’s Trade with Latin America and the Caribbean and Its Challenge,” figure 5. 45 Seth Colby, “Brazil’s Second-Best Financial Strategy,” Americas Quarterly, vol. 7, no. 2 (spring 2013), pp. 34-35.

18

mean by Brazil’s possible case of financial Dutch disease, as mentioned in the previous section

of this paper: capital is abundant but absurdly expensive; investment and productivity are flat;

and, bolstered by an overvalued real, domestic consumer spending is running at around 62

percent of GDP.

Where does the impact of China fit into this scenario? For perhaps the first time in the

post-World War II era the Brazilian industrial sector has not been able to shelter itself from the

levels of competition that Chinese manufactured imports are now presenting. On the upside, this

has been a powerful incentive for industrial restructuring and certainly some sub-sectors of

manufacturing are stepping up to the task. On the downside, the losers in this scenario, such as

producers of machinery, electrical equipment, and smaller miscellaneous manufactured goods,46

have succeeded in lobbying for high levels of protection. In 2011, alone, Brazil initiated 50 anti-

dumping investigations against China at the WTO. Debates over the country’s

“deindustrialization” have become commonplace, although the figures thus far do not entirely

support this notion. Jenkins and Barbosa report that only a fifth of Brazil’s total manufacturing is

exported, half of that to Latin American countries.47 Brazil has gone far on an industrial model

that caters mainly to domestic and regional markets; however, as in the case of Mexico, China’s

entry into the Brazilian market has illustrated the urgent need for a number of microeconomic

reforms that can bring down the costs and increase the efficiency and competitiveness of the

Brazilian economy.

46 See figure 9 in Yong Zhang, “Development of China’s Trade with Latin America and the Caribbean and Its

Challenge.” 47 Rhys Jenkins, “China and Brazil: Economic Impacts of a Growing Relationship;” Rhys Jenkins and Alexandre de

Freitas Barbosa, “Fear for Manufacturing? China and the Future of Industry in Brazil and Latin America,” The

China Quarterly, vol. 209 (2012), pp. 59-81.

19

Argentina

Since the launching of the 1991 Convertibility Plan Argentina has run the full gamut

from neoliberal (1991-2001) to developmental or heterodox economic policy approaches (2001

to present). With the country’s 2001 default on some US$100 billion in government-held debt

and the collapse of the decade-long currency board (which tightly pegged the Argentine peso to

the US dollar) in 2002, the situation could not have looked more bleak. Growth was down by

nearly 11 percent in 2002 and inflation, which had been reduced to single digits through the

1990s, spiked to 30 percent this same year (See table 3). By imposing a unilateral restructuring

on about 75 percent of the country’s outstanding external debt, the government reduced its debt

service burden from 8 percent to 2 percent of GDP.48 This, along with a more competitive

exchange rate and significant financial reforms implemented in the 1990s, set the stage for what

looked to be a modest recovery. However, Argentina’s growth rebounded to nearly 9 percent of

GDP in 2003 (see table 3) and would go on to average 7 percent annually between 2003 and

2011. As with Brazil, in 2003 Argentina suddenly began to thrive under the thrust of brisk

Chinese demand and the resulting high world prices for its main commodities (soya beans and

crude petroleum).

In the decade from 2002 to 2011 China advanced to become Argentina’s second most

important trading partner (after Brazil) and total trade between the two countries had increased

nearly twelve-fold to about US$17 billion dollars in 2011.49 Argentina, moreover, is second only

to Brazil as a destination for Chinese FDI in the 2000s (see tables 1 & 2), the bulk of it

48 Ignacio Labaqui, “Living Within our Means: The Role of Financial Policy in the Néstor and Cristina Fernandez de

Kirchner Administrations.” Paper presented at the Latin American Studies Association Annual Meeting, San

Francisco, May 2012. 49 “China-Argentina Trade, Investment Ties Booming,” Xinhua News Agency (Beijing) 8 May 2013.

20

concentrated in natural resources (e.g., oil, iron, wood, gas, copper, gold and lithium).50 In the

first few years following the Argentine default, the country’s leaders embraced China as a new

political and economic ally now that Argentina had basically frozen itself out of Western capital

markets and IFI relations had similarly cooled. And, although perhaps not to the extent that

Argentina had hoped, China has become a source of alternative financing. First, was the

aforementioned US$10 billion currency swap in 2009 and in 2010 China put up US$10 billion in

loans and rolling stocks to modernize Argentina’s railway system.51 Yet, tensions have

gradually arisen as Argentina has sought (unsuccessfully) to increase the value-added of its

primary exports to China, for example, to ship soybean oil rather than solely raw soya beans;52

moreover, Argentina has filed numerous anti-dumping complaints against China over the past

few years on everything from bicycle tires, to textiles, to shoes.53

When we look at the estimated impact of China on the net export earnings of the four

Latin American EEs analyzed here (see table 4), Argentina appears to be the least vulnerable in

this sense. Nevertheless, we would argue that the importance of China has been paramount for

Argentina in the 2000s. It was, after all, Chinese demand that breathed new life into the

collapsed Argentine economy beginning in 2003. More recently, the investment side of the

relationship has picked up considerably as Argentina now accounts of some 40 percent of

Chinese FDI to the region. On the less favorable side, Argentina’s foreign exchange earnings

from high commodity prices, combined with the burst of FDI from China, has prompted a

populist-style spending spree. Whereas Brazil’s ability to productively invest its windfall

50 Ruben Laufer, “Argentina-China: New Courses for an Old Dependency,” Latin American Policy, vol. 4, no. 1

(2013), pp. 123-143. 51 “China/Argentina: China, Argentina Sign 10-bln USD Rail Deal,” Asia News Monitor (Bangkok) 14 July 2010. 52 Eduardo Daniel Oviedo, “Argentina Facing China: Modernization, Interests, and Economic Relations Model,” p.

26. 53 “Latin America/China: Global Crisis Boosted Trade Ties,” Oxford Analytica Daily Brief Service 15 September

2010.

21

earnings is mostly a matter of dense over-regulation and bureaucratic bungling, Argentina is

engaged in one of Latin America’s more dramatic episodes of capital squandering.

The county’s fiscal and current accounts have deteriorated, double-digit inflation is on

the rise, and the government is now resorting to import, price and capital controls. As of 2010

the government began dipping into Central Bank reserves to cover its expenditures, the result

being a precipitous US$12 billion drop in reserves between 2010 and 2012 (see table 3). At this

current juncture, to speak of Argentina’s competitiveness or even a development model proper,

is a moot point, as the country’s rankings in table 5 indicate. However, thanks to its growing

economic ties with China, Argentina could muddle along with macro-profligacy, high inflation,

and sub-optimal returns for some time to come.54

Chile

As the most open, market-oriented, and trade-dependent of the four Latin American EEs

analyzed here, the negotiation of FTAs has been an integral part of Chile’s development strategy

since the 1990s. Chile was the demandeur in the initiation of an FTA with China, which makes

sense given that China has now become the most important export destination for Chilean

copper. Chile’s request to negotiate an FTA was underpinned, first, by the growing conviction

that domestic producers should be trying harder to export non-traditional and higher-value-added

products to the Chinese market; and second, by the goal of attracting Chinese FDI into efficiency

and market-seeking investments, as opposed to resource-seeking investment limited to mineral

extraction.55

54 Albert Fishlow, “Crying for Argentina,” Foreign Policy 11 March 2013. 55 These insights are based on authors’ confidential interviews conducted in Santiago, Chile during June 2011 with a

range of protagonists in the public and private sectors. Former Chilean trade negotiator, Osvaldo Rosales, offered

particularly helpful insights.

22

In principle, both Chile and China saw eye-to-eye on the numerous merits of the FTA.56

In practice, however, the main focus of the 2006 Chile-China FTA is on the WTO’s “old trade

agenda,” including the quest to liberalize market access for agriculture and labor-intensive

manufactures. Moreover, whereas all other Western Hemisphere FTAs have strong provisions

for increased market access in manufacturing production, China actually agreed to numerous

exceptions and restrictions in terms of its access to the Chilean industrial sector.57 Chilean

negotiators were able to completely exclude 152 “sensitive products” (e.g. wheat, flour, sugar,

some textiles and garments, and some major appliances) from this FTA while obtaining

immediate duty-free access to the Chinese market for 92 percent of its products covered by the

agreement.58 More than 90 per cent of Chile's imports from China are manufactured goods, with

over 42 per cent ranking as medium and high-tech;59 these higher-tech Chinese imports grew by

more than 900 percent between 2003 and 2011.60

The importance of copper and minerals in this agreement is highlighted by the fact that

only six of Chile’s abundant agricultural exports are covered by the FTA: apples, grapes, plums,

chicken products, cheese, and cherries.61 The negotiation of a copper deal between China and

China in 2005 was widely seen as a pre-condition for going forward with the FTA. Under this

deal, China Minmetals Corporation and the Chilean state-owned copper company (Codelco)

established a joint venture with an initial investment of US$550 million that could be expanded

to US$2 billion. This is the first time that Chile has allowed a foreign company to invest in its

56 Stephen Hoadley and Jian Yang, “China’s Cross-Regional FTA Initiatives,” Pacific Affairs, vol. 80, no. 1

(Summer 2007), p. 333. 57 Carol Wise, “Tratados de libre comercio al estilo chino: los TLC Chile-China y Perú-China,” Apuntes: Revista de

Ciencias Sociales, no. 71 (2013), pp. 161-188. 58 Jonathan R. Barton, “The Chilean Case,” in Rhys Jenkins and Enrique Dussel Peters, eds., China and Latin

America: Economic Relations in the Twenty-first Century (Bonn: German Development Institute, 2009), p. 244. 59 Jonathan R. Barton, “The Chilean Case.” 60 Carol Wise, “Tratados de libre comercio al estilo chino: los TLC Chile-China y Perú-China,” pp. 170-171. 61 Evan Ellis, China in Latin America: The Whats and Wherefores, p. 38.

23

copper sector, which accounts for about 37 per cent of world output.62 The new infusion of

capital will enable Codelco to supply China with 55,000 tonnes of copper over a 15-year period,

with beneficial prices to be negotiated periodically. For 2014, for example, Chile set the copper

premium for China at US$138 per tonne, as opposed to the US$198-200 per tonne charged by

other copper suppliers to China.63

While both the US and the EU FTAs heavily emphasize the WTO’s “new trade agenda”

around services and investment liberalization, China’s exceedingly low levels of non-mining

investment and services trade with Chile suggests that the promotion of market- and efficiency-

seeking investments were of less concern from the Chinese standpoint. With Chile’s prompting,

the two governments did sign a “The Supplementary Agreement on Trade in Services of the Free

Trade Agreement in 2008,”64 and in 2012 they completed an agreement on investment. Of note

here are the very few limitations set by Chile in terms of market access for services and national

treatment for investors compared with China’s thick list of restrictions concerning Chile’s access

to its services market, in particular. With Chinese FDI in Chile currently amounting to less than

.02 percent of China’s total FDI (see table 1),65 it seems safe to say that the focus of this FTA on

the old trade agenda will prevail. The bottom line: Chile and China have contractualized a

traditional comparative advantage trade model which shows weak signs of diversifying into a

pattern of more dynamic and competitive exchange between the two countries.

Chile-sign-copper-mining-deal-3423.html. 63 “Chiles Codelco Increases Premium for 2014 Copper Shipments to China,” Global Times 20 November 2013.

http://www.globaltimes.cn/content/826483.shtml#.UpEABXfl7f4. 64 For a summary go to: http://fta.mofcom.gov.cn/topic/enchile.shtml 65 Jude Webber, “Chile and China: No Deals,” Financial Times, 4 October 2011.

24

Douglass North reminds us that path dependence need not be “a story of inevitability in

which the past neatly predicts the future.”66 Rather, in a more positive vein, path dependence

can also be a way to pinpoint the development link between decision-making and policy choice

over time and against a given country’s institutional backdrop. Of the four EEs analyzed in this

paper only Argentina has fallen prey to the path of inevitability in which institutions that

previously provided disincentives to productive activity continue to do so at the present time. In

1991, the size of the Argentine economy was 50 percent that of China’s, but by 2011 it had

dwindled to just 6.1 percent.67 The complementarity of the China-Argentine economic

relationship is such that Argentina’s commodity exports will be in high demand indefinitely,

meaning that the country has a long horizon for muddling through and achieving much less than

is warranted by its rich factor endowments.

Both Brazil and Mexico have moved considerably outside of their traditional

development paths based on import substitution industrialization and financial repression over

the post-World War II era.68 Although the respective routes that each has taken to achieve

macroeconomic stabilization and industrial restructuring are markedly different, the data we have

reviewed here suggest that each has sought to head in the same steady upward direction. The

data in table 6 confirm that Mexico has moved more quickly than Brazil on a competitiveness

agenda, although both trail badly behind China on the majority of policy indicators analyzed in

the Global Competitiveness Report 2013-2014. If anything, the rise of China has confirmed how

much these policies matter: in 1991 Brazil’s total GDP was 107.3 percent the size of China’s, but

66 Douglass North, Institutions, Institutional Change, and Economic Performance, pp. 98-99. 67 Eduardo Daniel Oviedo, “Argentina Facing China: Modernization, Interests, and Economic Relations Model,” p.

17. 68 See Albert Fishlow, Starting Over: Brazil since 1985 and Juan Carlos Moreno-Brid and Jaime Ros, Development

and Growth in the Mexican Economy (New York: Oxford University Press, 2009).

25

just 33.9 percent in 2011; Mexico’s total GDP was 82.8 percent the size of China’s in 1991, but a

mere 15.8 percent in 2011.69

A main response toward China by both Brazil and Mexico has been to raise tariffs

through the roof on Chinese goods coming into these markets. Yet the Brazilian economist,

Alexandre Barbosa, cautions that “China’s ascent cannot serve – as the vague concept of

globalisation once did – as an excuse for fatalistically giving up on national development and

regional integration. On the contrary, it makes these policies more urgent than ever.”70 Clearly,

the reform lag in both countries confirms that there still exist “disincentives to productive

activity” in each.71

Whereas Brazil and Mexico are still struggling against the “inevitability” of sub-optimal

economic performance, Chile has stuck firmly to the open-economy, macro-prudent

development path that it embarked on some forty years ago. It is also the only EE analyzed here

that has taken a proactive stance toward the China phenomenon. The stakes for Chile are high:

table 4 showed how the estimated impact of China on its net export earnings could range

somewhere between 28.8 and 47.8 percent, an exposure that is at least three times higher than for

the other three EEs in table 4; the asymmetries are such that Chile’s total GDP in 2011 was 3.4

percent that of China’s.72 In 2000-05 the government’s income from copper mining averaged

$2.1 billion a year; as Chinese demand accelerated, that rose to $11.5 billion a year between

2005 and 2011.73

69 Eduardo Daniel Oviedo, “Argentina Facing China,” p. 17. 70 Alexandre De Freitas Barbosa, “The Rising China and Its Impacts on Latin America,” p. 22. 71 Douglass North, Institutions, Institutional Change, and Economic Performance, p. 99. 72 Eduardo Daniel Oviedo, “Argentina Facing China,” p. 17. 73 “The Mining Industry has Enriched Chile, but Its Future is Precarious,” The Economist 27 April 2013.

![Brent 2014 Farmland Preservation, Agricultural …web.isanet.org/Web/Conferences/FLACSO-ISA BuenosAires...[Draft only—please do not cite] of farmland (Sokolow, 2002). This paper](https://static.documents.pub/doc/80x56/5e9245094b453964605e083c/brent-2014-farmland-preservation-agricultural-web-buenosaires-draft-onlyaplease.jpg)