109

China Purchasing Development Report

(2010)

For more information

Li & Fung Research CentreMember of Li & Fung Group11/F, LiFung Tower,

868 Cheung Sha Wan Road,

Hong Kong

Tel : (852) 2300 2470

Fax : (852) 2635 1598

Email : [email protected]

Website : www.lifunggroup.com

China Federation of Logistics & PurchasingThe Specialized Committee for Purchasing andSupply China ManagementRm 1515 Henghua International Business Centre,

26 Yuetan Beijie, Beijing, China 100045

Phone : (010) 5856 6588 -191 / -195 / -183

Fax : (010) 5856 6579

Website : www.chinawuliu.com.cn

!"#$#%&'(#)*+*,-./#0*'1-* 2

The Report

In view of the growing importance of sourcing in China, the China Federation of Logistics and

Purchasing (CFLP), the most authoritative industry organization in areas of sourcing, logistics

and supply chain management in China, published the !rst and second annual China Purchasing

Development Reports1 in 2008 and 2009. The reports give a comprehensive account of the

latest development of sourcing activities in China, and were well received by the academia and

practitioners. The CFLP publishes the third report in 2010.

Li & Fung Research Centre of the Li & Fung Group is delighted to work jointly with the CFLP

in the China Purchasing Development Report project, and is solely responsible for the content

of the English version of the report. This English version summarizes the key takeaways of the

full report in Chinese. We hope our readers can get an overview of the sourcing environment in

China.

1 The English version of the 2008 and 2009 reports can be found here: http://www.lifunggroup.com/research/pdf/ChinaPurchasingDevelopmentReport08.pdf (2008) and http://www.lifunggroup.com/research/pdf/ChinaPurchasingDevelopmentReport09.pdf (2009).

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=;

! ! Table of Content

! "! #$%!&%'(&#!

! )! #*+,%!(-!.(/#%/#

! 0! *+(1#!#$%!(&2*/34*#3(/5!

! 6! .$3/*!5(1&.3/2!51&7%8!

! 09! */!*/*,8535!(-!'1&.$*53/2!*.#373#3%5!*/:!5(1&.3/2!53#1*#3(/5!;3#$!'<3!*/:!/<3

! 6=! 5(1&.3/2!,32$#><*/1-*.#1&%:!.(/51<%&!'&(:1.#5!3/!.$3/*?!.(5#!#&%/:5!*/:!

(1#,((@

! 9A! #$%!'(5#>-3/*/.3*,!.&3535!5#&*#%23%5!(-!.$3/*B5!<*/1-*.#1&%&5!*/:!5(1&.3/2!

+153/%55%5

! CD=! *''%/:3E?!*+(1#!#$%!CHINA PURCHASING DEVELOPMENT REPORT (CHINESE VERSION)

!"#$#%&'(#)*+*,-./#0*'1-* >

About the organizations

China Federation of Logistics & Purchasing (CFLP) is the !rst logistics and purchasing

industry association approved by the State Council. CFLP’s mission is to promote the

development of the logistics industry and the sourcing businesses of both government and

enterprises, as well as to facilitate the circulation of factors of production in China. The CFLP is

also China’s representative in the Asian-Paci!c Logistics Federation (APLF) and the International

Federation of Purchasing and Materials Management (IFPMM).

China Society of Logistics is a non-pro!t making academic organization comprising experts,

academia and practitioners in the logistics sector in China, with special focuses on logistics

theories, management science of logistics and modernization of logistics technology. The

Society endeavors to channel members’ opinions to relevant government departments, organize

activities for exchanging knowledge and experiences, nurture talents for the sector, and publish

logistics publications and information.

The Li & Fung Group is a Hong Kong-based multinational company with three distinct core

businesses: export trading, distribution and retailing. Founded in Guangzhou in 1906, the Li &

Fung Group achieved an annual turnover exceeding US$16 billion in 2009. Today, the Li & Fung

Group operates in some 40 countries and regions and employs over 35,500 people worldwide.

One of its core competencies is supply chain management.

In 2009, the Li & Fung Group’s revenue in China exceeded USD 8 billion. The extensive sourcing

network of Li & Fung Limited, the export trading arm of the Li & Fung Group, covers over 10,000

suppliers through more than 20 of!ces in China. China has become Li & Fung Limited’s most

important market in global sourcing. In 2009, 54% of its global sourcing was from China.

The Li & Fung Research Centre serves as a knowledge bank for the Li & Fung Group on

China’s economy, industries, logistics and the distribution sector, with its research scope

spanning the entire supply chain, from ideas, production, distribution, retailing to end-

consumers.

The Centre has been actively promoting the application of supply chain management. In

2003, the Centre published the book “Li & Fung: the Orchestrator of Global Supply Chain

Management”. The book is now regarded as a very useful reference among businessmen and

academics in China. The revised and expanded edition was published in August 2009.

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=?

China sourcing survey

The CFLP conducted its !rst annual survey on sourcing activities of enterprises in China in 2008

in order to have a systematic review and analysis of China’s sourcing environment. The 2010

survey is the third exercise. This year, the CFLP expanded the scope of the survey to cover new

aspects such as green sourcing. A total of 204 valid responses were collected. The sampled

enterprises are broadly representative, in terms of industry, ownership structure and size. More

information on the pro!le of the respondents is provided in exhibits 1 to 4.

Several trends are observed. First, during the post-crisis period, the majority of the surveyed

enterprises witnessed growth in sales income. However, unreliable suppliers, increasing

operation costs and on-time delivery to clients were named the biggest challenges for them.

Second, the recognition of importance of sourcing is improving. About 60% of the sourcing

departments of the respondents directly reported to either the general manager or the vice

president overseeing sourcing. 76% of the respondents agreed that the top management had

paid more attention to the development of the sourcing department. The sourcing department

also had in"uences over other departments especially the production department and the

logistics & transportation department. Nonetheless, professional training for sourcing personnel

was inadequate, and the proportion of sourcing staff with formal training was below 50%.

Third, the application of modern management skills, approaches or systems in sourcing received

more attention, but there is still room for improvement. 67.8% of the surveyed enterprises

ful!lled or even outperformed their sourcing plans, showing signi!cant improvement from the

previous year (below 30%). 51.7% of the respondents said the sourcing performance evaluation

was closely integrated with their operational objectives, improving from 49.8% of last year. In

terms of informatization, still, less than 50% of the surveyed enterprises adopted the bar code

system across various businesses and operational units within the enterprises. Also, apart from

Enterprise Resource Planning (ERP), the adoption rate of other information systems such as

Management Information System (MIS) and Decision Support System (DSS) remained low.

Fourth, better supplier management was observed. 51.3% of the respondents thought that their

execution of the supplier evaluation system had been good or very good. 64.2% of the surveyed

enterprises managed to maintain stable relationship with over 50% of their suppliers this year, up

from 48.4% of last year.

!"#$#%&'(#)*+*,-./#0*'1-* @

China sourcing survey

Finally, green sourcing and corporate social responsibility are gaining attention among the

surveyed enterprises. 75.5% of the suppliers of the surveyed enterprises provided products

meeting national green standards. 68.1% of the surveyed enterprises required their suppliers to

comply with certain corporate social responsibility requirements. If their suppliers fail to do so,

the majority of the respondents would require them to make improvements.

1. Pro!le of the surveyed enterprises

Exhibit 1 shows the types of enterprises covered in the 2010 survey. They were mainly from the

manufacturing sector, which accounted for 82.9% of the total. 31.4% engaged in mechanical

equipment, and enterprises engaging in the light industry and electronic communications

equipment accounted for 17.2% and 14.7% respectively (see exhibit 2).

Exhibit 1: Types of Enterprises

SECTOR SHARE OF TOTAL

Manufacturing 82.9%

Services 7.8%

Others (e.g. construction) 9.3%

Exhibit 2: Breakdown of industries of manufacturing sector

INDUSTRY SHARE OF TOTAL

Mechanical equipment 31.4%

Light Industry 17.2%

Electronic communications equipment 14.7%

Metal & non-metal processing 10.8%

Petrochemical (including chemical !bres, 8.8%

rubber, plastics & pharmaceuticals)

Among the surveyed enterprises, 48.0% were private enterprises (PEs); 36.8% were foreign-

invested enterprises (FIEs), which included the Hong Kong- and Taiwan-invested enterprises; and

state-owned enterprises (SOEs) accounted for 9.8% of the total (see exhibit 3).

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=A

Exhibit 3: Forms of ownership of enterprises

Among the respondents, 44.1% were large-sized enterprises, 35.8% were medium-sized

enterprises and 20.1% were small-sized enterprises.1 More information can be found in exhibit 4.

Exhibit 4: Size of enterprises

1 In this survey, enterprises with sales volume over 300 million are classi!ed as “large-sized enterprises”; those with sales volume over 30 million and below 300 million are classi!ed as “medium-sized enterprises”; and with sales volume below 30 million, “small-sized enterprises”.

!"#$#%&'(#)*+*,-./#0*'1-* B

China sourcing survey

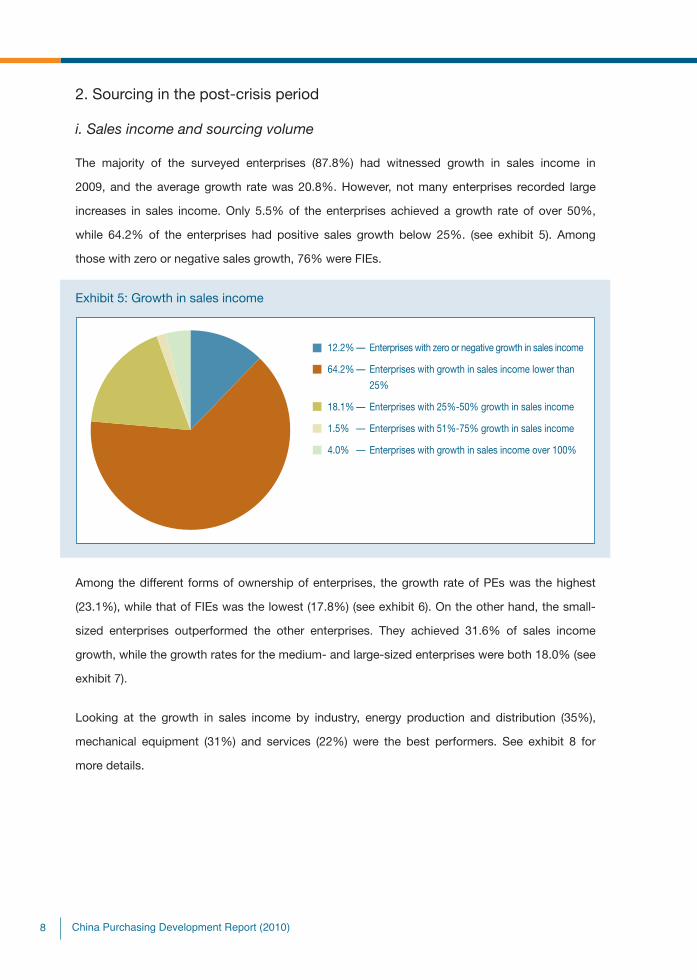

2. Sourcing in the post-crisis period

i. Sales income and sourcing volume

The majority of the surveyed enterprises (87.8%) had witnessed growth in sales income in

2009, and the average growth rate was 20.8%. However, not many enterprises recorded large

increases in sales income. Only 5.5% of the enterprises achieved a growth rate of over 50%,

while 64.2% of the enterprises had positive sales growth below 25%. (see exhibit 5). Among

those with zero or negative sales growth, 76% were FIEs.

Exhibit 5: Growth in sales income

Among the different forms of ownership of enterprises, the growth rate of PEs was the highest

(23.1%), while that of FIEs was the lowest (17.8%) (see exhibit 6). On the other hand, the small-

sized enterprises outperformed the other enterprises. They achieved 31.6% of sales income

growth, while the growth rates for the medium- and large-sized enterprises were both 18.0% (see

exhibit 7).

Looking at the growth in sales income by industry, energy production and distribution (35%),

mechanical equipment (31%) and services (22%) were the best performers. See exhibit 8 for

more details.

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=C

Exhibit 6: Average growth in sales income by form of ownership of enterprises

Exhibit 7: Average growth in sales income by size of enterprises

Exhibit 8: Average growth in sales income by industry

In terms of sourcing volume, the majority of the surveyed enterprises (88.2%) saw an increase,

and they recorded an average increase of 18.2%. However, not many enterprises had remarkable

growth in sourcing volume. Over 70% of the enterprises reported that their increases in sourcing

volume were lower than 25% (see exhibit 9). Among those with zero or negative growth, 80%

were FIEs.

!"#$#%&'(#)*+*,-./#0*'1-* D

China sourcing survey

Exhibit 9: Growth in sourcing volume

Among different forms of ownership of enterprises, PEs had the biggest increase in sourcing

volume (24.9%), while that of FIEs was the smallest (9.5%) (see exhibit 10). Among the different

sizes of enterprises, the small-sized enterprises outperformed their counterparts. They achieved

a volume increase of 36.0%, compared to 10.8% volume increase of the large-sized enterprises

(see exhibit 11). Among different industries, mechanical equipment (25%) and electronic

communications equipment (24%) were the best performers (see exhibit 12).

Exhibit 10: Average growth in sourcing volume by form of ownership of enterprises

Exhibit 11: Average growth in sourcing volume by size of enterprises

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=2<

Exhibit 12: Average growth in sourcing volume by industry

ii. Major challenges of sourcing management

When asked about the greatest challenge, 51.0% of the respondents named unreliable suppliers.

Increasing operational costs (46.6%) and on-time delivery to clients (44.6%) were also major

challenges faced by the enterprises. Exhibit 13 gives you more information.

Exhibit 13: Major challenges of sourcing management

Note: Multiple responses allowed

Looking at different forms of ownership of enterprises, unreliable suppliers (50.0%), increasing

operational costs (50.0%) and risk management (50.0%) were the biggest challenges for SOEs.

Only 20.0% of SOEs regarded on-time delivery to clients as a major challenge. As for FIEs, their

pressure came mainly from unreliable suppliers (49.3%), on-time delivery to clients (49.3%) and

stiff competition (46.7%). PEs suffered most from unreliable suppliers (51.0%), on-time delivery

to clients (49.3%) and increasing operational costs (49.0%) (see exhibit 14).

!"#$#%&'(#)*+*,-./#0*'1-* 22

China sourcing survey

Exhibit 14: Major challenges of sourcing management by form of ownership of enterprises

Note: Multiple responses allowed

iii. Measures to overcome challenges

As most enterprises considered “unreliable suppliers” their biggest challenge, various measures

were taken to overcome it. Maintaining long term and stable relationship with suppliers (83.3%)

and developing new suppliers (77.3%) were the most commonly named measures. Exhibit 15

gives more information.

Exhibit 15: Measures to overcome challenges

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=2;

3. Strategic importance of sourcing within enterprises

i. Head of the sourcing department

Results revealed that the importance of sourcing was well recognized among the surveyed

enterprises. As shown in exhibit 16, nearly 60% of the sourcing departments of the respondents

reported directly to either the general managers or the vice presidents who oversee sourcing.

Only 9% of the sourcing department of the surveyed enterprises reported to chief procurement

of!cers, chief executive of!cers or chief supply chain of!cers. Also, most of the SOEs did not

have a chief operation of!cer or chief procurement of!cer. It re"ects that sourcing has yet to

develop as a specialized division, especially for SOEs (see exhibit 16).

Exhibit 16: Head of sourcing department

ii. Importance of the sourcing department

In terms of involvement in other business functions, the sourcing department did show its

in"uences over other departments’ decision making, especially the production and logistics &

transportation departments. The proportions of sourcing department having high and medium

involvement in the aforesaid departments were 71.6% and 67.7% respectively (see exhibit 17).

!"#$#%&'(#)*+*,-./#0*'1-* 2>

China sourcing survey

Exhibit 17: Involvement of sourcing departments in other business functions

Note: Multiple responses allowed

Among different forms of ownership of enterprises, the sourcing departments in SOEs involved

signi!cantly less in other business functions, when compared with their counterparts in FIEs and

PEs (see exhibit 18). On the other hand, the sourcing departments in small-sized enterprises had

much lower involvement in strategic planning when compared with their counterparts in medium-

and large-sized enterprises. (see exhibit 19).

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=2?

Exhibit 18: Involvement of sourcing departments in other business functions by form of

ownership of enterprises

Other business functions Levels of involvement SOEs PEs FIEs

Information technology High 15.0% 17.3% 6.7%

Medium 50.0% 34.7% 36.0%

Low 10.0% 22.4% 29.3%

No involvement 25.0% 25.5% 28.0%

Logistics & transportation High 30.0% 32.7% 38.7%

Medium 30.0% 33.7% 32.0%

Low 10.0% 16.3% 17.3%

No involvement 30.0% 17.3% 12.0%

Non-production operation High 0.0% 8.2% 8.0%

Medium 35.0% 27.6% 28.0%

Low 25.0% 23.5% 38.7%

No involvement 40.0% 40.8% 25.3%

Production High 40.0% 40.8% 48.0%

Medium 25.0% 27.6% 28.0%

Low 10.0% 13.3% 14.7%

No involvement 25.0% 18.4% 9.3%

Customer support High 15.0% 12.2% 16.0%

Medium 25.0% 32.7% 22.7%

Low 15.0% 26.5% 26.7%

No involvement 45.0% 28.6% 34.7%

Marketing & advertising High 0.0% 4.1% 1.3%

Medium 10.0% 17.3% 13.3%

Low 30.0% 30.6% 29.3%

No involvement 60.0% 48.0% 56.0%

Sales & business development High 10.0% 22.4% 5.3%

Medium 10.0% 25.5% 34.7%

Low 35.0% 20.4% 24.0%

No involvement 45.0% 31.6% 36.0%

Product & service development High 15.0% 23.5% 16.0%

Medium 35.0% 26.5% 42.7%

Low 25.0% 28.6% 26.7%

No involvement 25.0% 21.4% 14.7%

Research & development High 15.0% 24.5% 25.3%

Medium 15.0% 22.4% 29.3%

Low 45.0% 28.6% 26.7%

No involvement 25.0% 24.5% 18.7%

Strategic planning High 10.0% 16.3% 17.6%

Medium 45.0% 42.9% 39.2%

Low 10.0% 17.3% 25.7%

No involvement 35.0% 23.5% 17.6%

!"#$#%&'(#)*+*,-./#0*'1-* 2@

China sourcing survey

Exhibit 19: Involvement of sourcing departments in other business functions by size of

enterprises

Other business Levels of Large-sized Medium-sized Small-sized

functions involvement enterprises enterprises enterprises

Information technology High 13.3% 11.0% 14.6% Medium 34.4% 53.4% 14.6% Low 28.9% 20.5% 17.1% No involvement 23.3% 15.1% 53.7%Logistics & transportation High 31.1% 45.2% 26.8% Medium 35.6% 28.8% 31.7% Low 16.7% 15.1% 12.2% No involvement 16.7% 11.0% 29.3%Non-production operation High 6.7% 9.6% 2.4% Medium 26.7% 39.7% 14.6% Low 38.9% 21.9% 19.5% No involvement 27.8% 28.8% 63.4%Production High 47.8% 49.3% 29.3% Medium 27.8% 26.0% 26.8% Low 12.2% 12.3% 14.6% No involvement 12.2% 12.3% 29.3%Customer support High 14.4% 16.4% 7.3% Medium 25.6% 34.2% 26.8% Low 25.6% 23.3% 24.4% No involvement 34.4% 26.0% 41.5%Marketing & advertising High 4.4% 1.4% 0.0% Medium 13.3% 16.4% 19.5% Low 34.4% 28.8% 17.1% No involvement 47.8% 53.4% 63.4%Sales & business development High 13.3% 12.3% 19.5% Medium 25.6% 34.2% 22.0% Low 27.8% 24.7% 12.2% No involvement 33.3% 28.8% 46.3%Product & service development High 22.2% 21.9% 14.6% Medium 30.0% 42.5% 26.8% Low 30.0% 23.3% 24.4% No involvement 17.8% 12.3% 34.1%Research & development High 25.6% 28.8% 19.5% Medium 26.7% 19.2% 26.8% Low 30.0% 28.8% 22.0% No involvement 17.8% 23.3% 31.7%Strategic planning High 14.4% 13.9% 31.7% Medium 43.3% 44.4% 26.8% Low 23.3% 19.4% 12.2% No involvement 18.9% 22.2% 29.3%

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=2A

In general, the importance of the sourcing department has grown signi!cantly in recent years.

It can be proved by the fact that 76% of the respondents agreed that the top management had

paid more attention to the development of the sourcing department.

iii. Contribution of the sourcing department to enterprises

According to the survey, the most important contribution of the sourcing department to

enterprises lay in cost control, followed by quality improvement and risk management.

4. Sourcing Performance

I. Criteria of sourcing performance evaluation

i. Implementation of sourcing plan

67.8% of the surveyed enterprises ful!lled or even outperformed their sourcing plans. However,

32.2% of respondents were not sure if they had ful!lled their sourcing plans (see exhibit 20).

Among different forms of ownership of enterprises, FIEs did better than other enterprises, with

78.9% of FIEs ful!lled or outperformed their sourcing plans (see exhibit 21). Large- and medium-

sized enterprises also had a higher implementation rate of their sourcing plans (see exhibit 22).

Exhibit 20: Implementation rate of sourcing plan

!"#$#%&'(#)*+*,-./#0*'1-* 2B

China sourcing survey

Exhibit 21: Implementation rate of sourcing plan by form of ownership of enterprises

Exhibit 22: Implementation rate of sourcing plan by size of enterprises

ii. Accuracy of order processing

Exhibit 23 demonstrates the accuracy rate of order processing of the surveyed enterprises. In

overall terms, 86.1% of orders were processed accurately. Among different forms of ownership of

enterprises, FIEs again outperformed SOEs and PEs (see exhibit 23). When it comes to different

size of enterprises, small-sized enterprises noticeably lagged behind their counterparts (see

exhibit 24).

Exhibit 23: Accuracy rate of order processing by form of ownership of enterprises

Exhibit 24: Accuracy rate of order processing by size of enterprises

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=2C

II. Sourcing performance management

i. Indicators for sourcing performance evaluation

When asked about the indicators for sourcing performance evaluation, most respondents of all

forms of ownership chose price/cost: FIEs (98.6%), PEs (94.9%) and SOEs (100%). Product

quality, inventory and continuity of supply were also important. By contrast, technology,

innovation and introduction of new products was the least chosen indicator by the respondents

(see exhibit 25).

Exhibit 25: Indicators for sourcing performance evaluation by form of ownership of

enterprises

Note: Multiple responses allowed

ii. Integration between sourcing performance evaluation and the overall

operational objectives

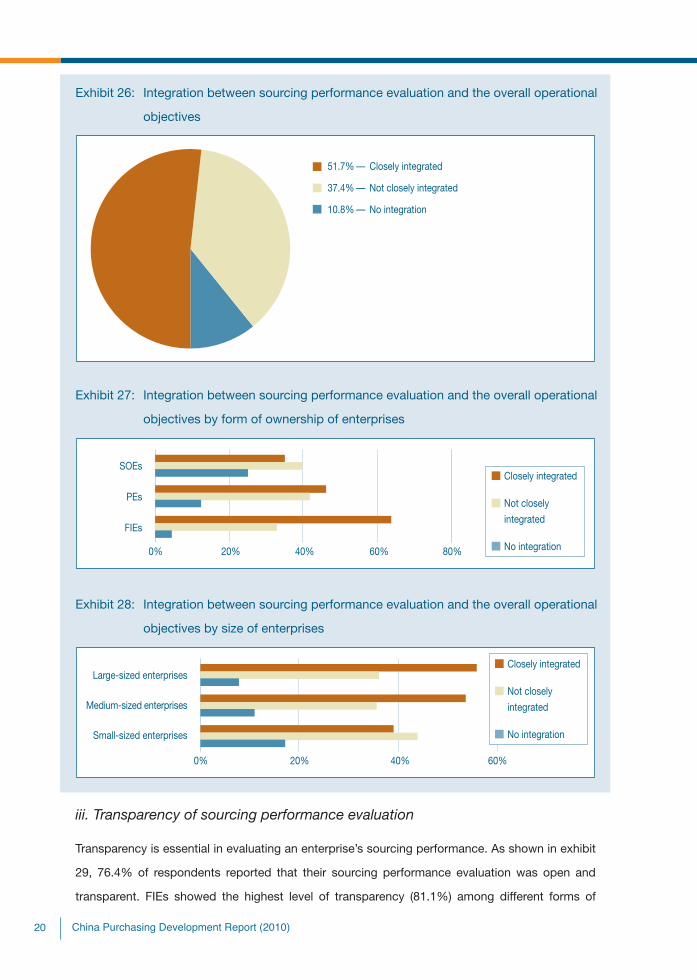

Integrating sourcing performance evaluation with the overall operational objectives is another

important sourcing management strategy. About half of the surveyed enterprises said the

sourcing performance evaluation was closely integrated with their operational objectives. Exhibit

26 gives a more detailed picture. Among different forms of ownership and sizes of enterprises,

FIEs again outperformed PEs and SOEs (see exhibit 27), while large-sized enterprises did better

than medium- and small-sized enterprises (see exhibit 28).

!"#$#%&'(#)*+*,-./#0*'1-* 2D

China sourcing survey

Exhibit 26: Integration between sourcing performance evaluation and the overall operational

objectives

Exhibit 27: Integration between sourcing performance evaluation and the overall operational

objectives by form of ownership of enterprises

Exhibit 28: Integration between sourcing performance evaluation and the overall operational

objectives by size of enterprises

iii. Transparency of sourcing performance evaluation

Transparency is essential in evaluating an enterprise’s sourcing performance. As shown in exhibit

29, 76.4% of respondents reported that their sourcing performance evaluation was open and

transparent. FIEs showed the highest level of transparency (81.1%) among different forms of

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=;<

ownership of enterprises (see exhibit 30). According to the survey, the larger the enterprise, the

higher level of transparency was observed (see exhibit 31).

Exhibit 29: Transparency of sourcing performance evaluation

Exhibit 30: Transparency of sourcing performance evaluation by form of ownership of

enterprises

Exhibit 31: Transparency of sourcing performance evaluation by size of enterprises

!"#$#%&'(#)*+*,-./#0*'1-* ;2

China sourcing survey

5. Sourcing management

i. Degree of centralization of sourcing activities

Exhibit 32 gives a brief picture on the degree of centralization of sourcing activities within

the enterprises surveyed. Most of them (63.7%) adopted both centralized and decentralized

approaches. It is believed that enterprises opted for more "exible sourcing approaches to

cope with the challenging business environment. Besides, SOEs have the highest tendency to

implement centralized sourcing, which could be explained by their larger size.

Exhibit 32: Degree of centralization of sourcing activities

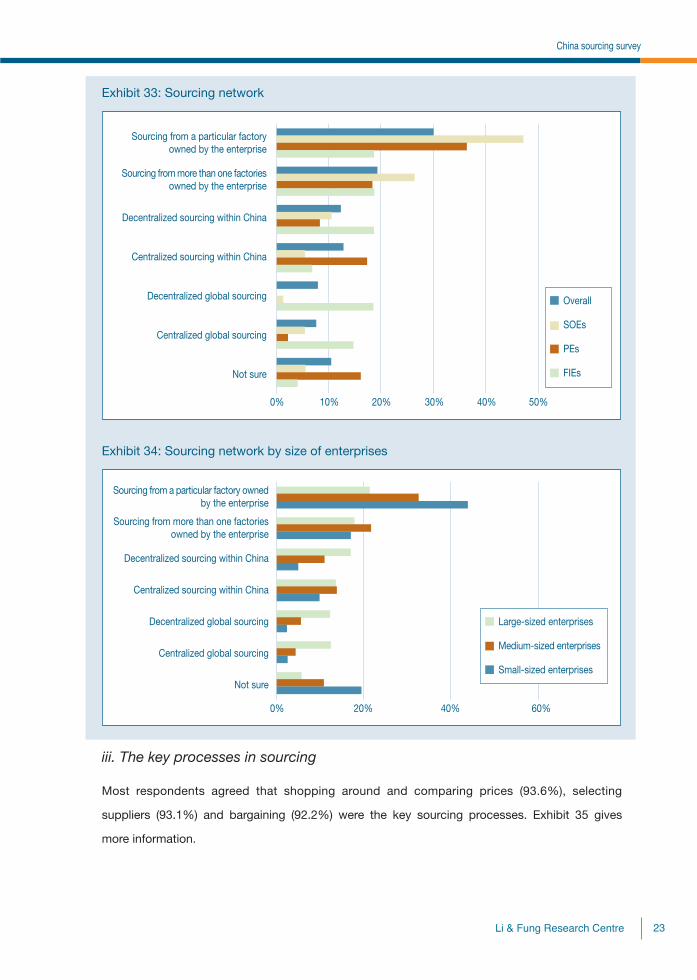

ii. Sourcing network

The majority of the surveyed enterprises (74.3%) sourced within China. About half of the

respondents adopted internal sourcing (sourcing from the factories owned by the enterprises).

Among various forms of ownership of enterprises, it is not surprising that FIEs practised global

sourcing the most given their global network and relevant experience. Large-sized enterprises

were also more active in global sourcing than medium- and small-sized enterprises (see exhibits

33 and 34).

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=;;

Exhibit 33: Sourcing network

Exhibit 34: Sourcing network by size of enterprises

iii. The key processes in sourcing

Most respondents agreed that shopping around and comparing prices (93.6%), selecting

suppliers (93.1%) and bargaining (92.2%) were the key sourcing processes. Exhibit 35 gives

more information.

!"#$#%&'(#)*+*,-./#0*'1-* ;>

China sourcing survey

Exhibit 35: The key processes in sourcing

Note: Multiple responses allowed

iv. Means of cost control in sourcing

Cost control is always the top priority in sourcing, especially at times of economic turbulence.

Same as last year’s results, the traditional way of shopping around and sorting out the most

competitive offer was the most common way of cost control in sourcing for nearly all sizes and

forms of ownerships of enterprises. Forming strategic alliance with reliable suppliers came

second, with 74.4% of respondents chose it as a means of cost control. Exhibits 36 and 37

present a more detailed picture.

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=;?

Exhibit 36: Means of cost control by form of ownership of enterprises

Note: Multiple responses allowed

Exhibit 37: Means of cost control by size of enterprises

Note: Multiple responses allowed

!"#$#%&'(#)*+*,-./#0*'1-* ;@

China sourcing survey

v. Outsourcing sourcing functions

45.8% of the surveyed enterprises did outsource their sourcing functions. FIEs were more

receptive to the concept of outsourcing, which was less welcomed by PEs (see exhibit 38).

Exhibit 38: Outsourcing sourcing functions

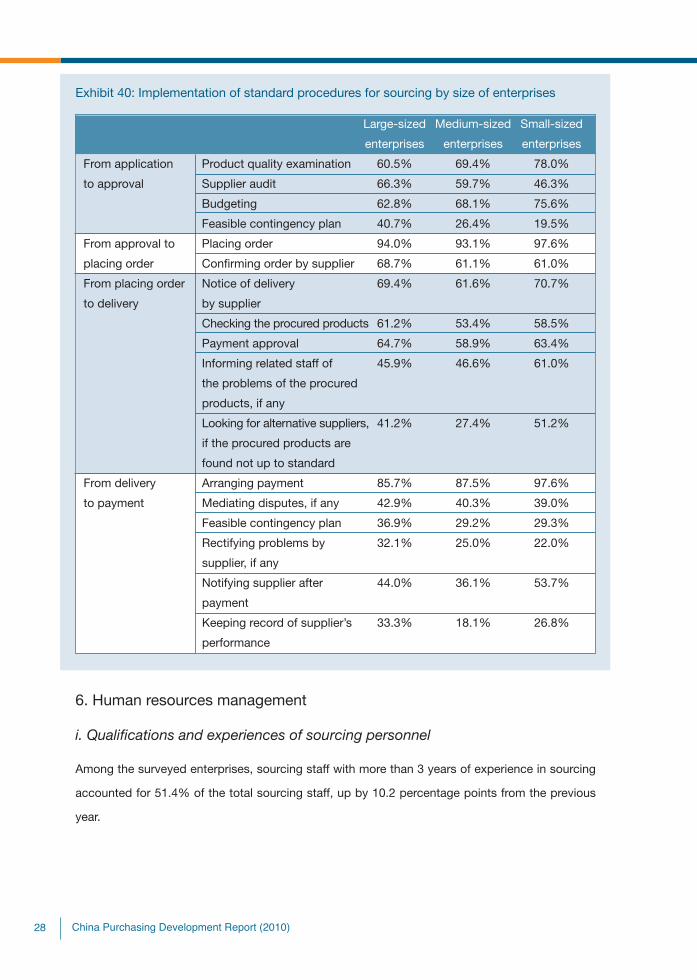

vi. Implementation of standard procedures for sourcing

The standard procedures for sourcing can be divided into four stages: “from application

to approval”, “from approval to placing order”, ‘from placing order to delivery” and “from

delivery to payment”. In general, the surveyed enterprises did not do a good job in following

the standard procedures of sourcing. The situation was even worse when they were asked

about the contingency measures in the face of problems such as delivery of !nal products with

substandard quality. Enterprises are advised to enhance the implementation of the standard

procedures for sourcing, especially developing contingency plans for different sourcing stages

(see exhibits 39 and 40).

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=;A

Exhibit 39: Implementation of standard procedures for sourcing by form of ownership of

enterprises

Overall SOEs PEs FIEs

From application Product quality examination 67.3% 65.0% 72.4% 61.4%

to approval Supplier audit 59.8% 65.0% 53.1% 70.0%

Budgeting 67.3% 65.0% 64.3% 70.0%

Feasible contingency plan 31.2% 45.0% 30.6% 28.6%

From approval to Placing order 94.4% 95.0% 93.8% 95.6%

placing order Con!rming order by supplier 64.3% 65.0% 59.8% 72.1%

From placing order Notice of delivery by supplier 66.8% 85.0% 71.4% 60.6%

to delivery Checking the procured products 57.8% 65.0% 54.1% 66.2%

Payment approval 62.3% 65.0% 56.1% 67.6%

Informing related staff of the 49.2% 55.0% 56.1% 40.8%

problems of the procured

products, if any

Looking for alternative suppliers, 38.2% 40.0% 36.7% 39.4%

if the procured products are

found not up to standard

From delivery Arranging payment 88.8% 90.0% 85.6% 93.0%

to payment Mediating disputes, if any 41.1% 40.0% 40.2% 43.7%

Feasible contingency plan 32.5% 40.0% 28.9% 35.2%

Rectifying problems by 27.4% 25.0% 25.8% 31.0%

supplier, if any

Notifying supplier after 43.1% 50.0% 46.4% 39.4%

payment

Keeping record of supplier’s 26.4% 20.0% 25.8% 28.2%

performance

!"#$#%&'(#)*+*,-./#0*'1-* ;B

China sourcing survey

Exhibit 40: Implementation of standard procedures for sourcing by size of enterprises

Large-sized Medium-sized Small-sized

enterprises enterprises enterprises

From application Product quality examination 60.5% 69.4% 78.0%

to approval Supplier audit 66.3% 59.7% 46.3%

Budgeting 62.8% 68.1% 75.6%

Feasible contingency plan 40.7% 26.4% 19.5%

From approval to Placing order 94.0% 93.1% 97.6%

placing order Con!rming order by supplier 68.7% 61.1% 61.0%

From placing order Notice of delivery 69.4% 61.6% 70.7%

to delivery by supplier

Checking the procured products 61.2% 53.4% 58.5%

Payment approval 64.7% 58.9% 63.4%

Informing related staff of 45.9% 46.6% 61.0%

the problems of the procured

products, if any

Looking for alternative suppliers, 41.2% 27.4% 51.2%

if the procured products are

found not up to standard

From delivery Arranging payment 85.7% 87.5% 97.6%

to payment Mediating disputes, if any 42.9% 40.3% 39.0%

Feasible contingency plan 36.9% 29.2% 29.3%

Rectifying problems by 32.1% 25.0% 22.0%

supplier, if any

Notifying supplier after 44.0% 36.1% 53.7%

payment

Keeping record of supplier’s 33.3% 18.1% 26.8%

performance

6. Human resources management

i. Qualifications and experiences of sourcing personnel

Among the surveyed enterprises, sourcing staff with more than 3 years of experience in sourcing

accounted for 51.4% of the total sourcing staff, up by 10.2 percentage points from the previous

year.

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=;C

Among different forms of enterprises, PEs had fewer professional sourcing personnel than FIEs

and SOEs. And so did the smaller enterprises. This is probably due to the fact that they had

fewer resources for manpower training and development (see exhibits 41 and 42).

Exhibit 41: Qualifications and experience of soucing personnel by form of ownership of

enterprises

Exhibit 42: Quali!cations and experience of sourcing personnel by size of enterprises

ii. Manpower training awareness

Professional training for sourcing staff was not popular among the surveyed enterprises. Still,

21.6% of them provided no training to their staff, similar to last year’s !gure. PEs and smaller

enterprises allocated relatively fewer resources to their sourcing staff (see exhibits 43 and 44).

Exhibit 43: Proportions of enterprises which provide no training to sourcing staff by form of

ownership of enterprises

!"#$#%&'(#)*+*,-./#0*'1-* ;D

China sourcing survey

Exhibit 44: Proportions of enterprises which provide no training to sourcing staff by size of

enterprises

Among the surveyed enterprises, less than half of them had their sourcing staff formally trained.

Again, PEs and smaller enterprises were equipped with the smallest number of formally trained

staff. Exhibits 45 and 46 show more details.

Exhibit 45: Proportions of staff attended formal training by form of ownership of enterprises

Exhibit 46: Proportions of staff attended formal training by size of enterprises

The average training hours per staff of all surveyed enterprises were 41.7 last year. Staff from

SOEs and large-sized enterprises received the most training. Exhibits 47 and 48 give more

information.

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=><

Exhibit 47: Annual training hours per staff by form of ownership of enterprises

Exhibit 48: Annual training hours per staff by size of enterprises

When asked about the need for training, almost 60% of the respondents thought that there was

no need or no urgent need for their staff to get trained. Among different forms of ownership of

enterprises, SOEs showed the least awareness of the need to train for their sourcing staff (see

exhibits 49 and 50).

Exhibit 49: Perceived need for training

!"#$#%&'(#)*+*,-./#0*'1-* >2

China sourcing survey

Exhibit 50: Perceived need for training by form of ownership of enterprises

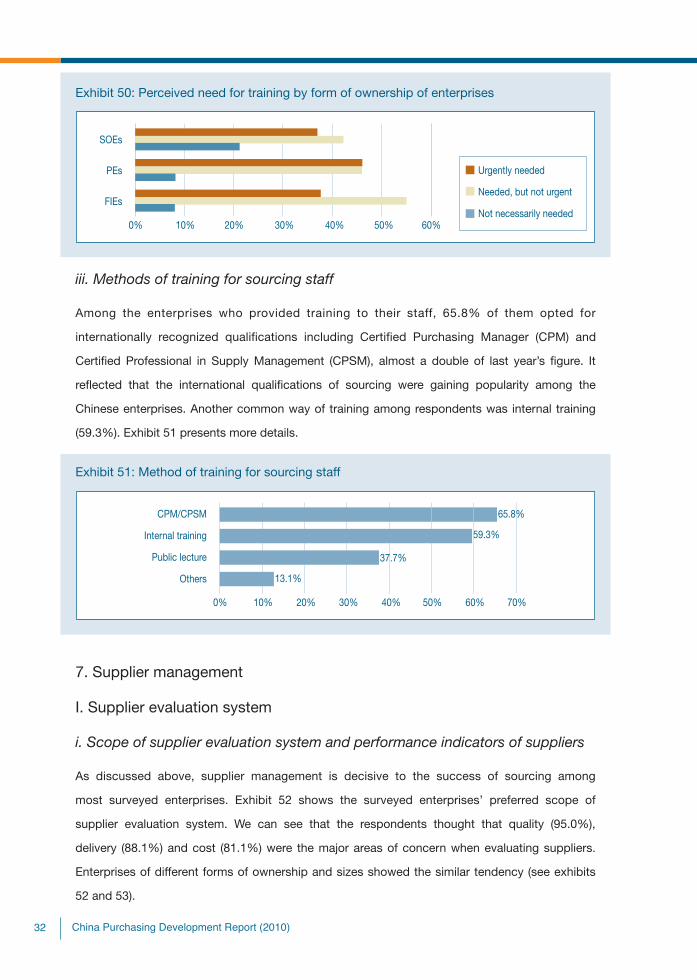

iii. Methods of training for sourcing staff

Among the enterprises who provided training to their staff, 65.8% of them opted for

internationally recognized qualifications including Certified Purchasing Manager (CPM) and

Certi!ed Professional in Supply Management (CPSM), almost a double of last year’s !gure. It

re"ected that the international quali!cations of sourcing were gaining popularity among the

Chinese enterprises. Another common way of training among respondents was internal training

(59.3%). Exhibit 51 presents more details.

Exhibit 51: Method of training for sourcing staff

7. Supplier management

I. Supplier evaluation system

i. Scope of supplier evaluation system and performance indicators of suppliers

As discussed above, supplier management is decisive to the success of sourcing among

most surveyed enterprises. Exhibit 52 shows the surveyed enterprises’ preferred scope of

supplier evaluation system. We can see that the respondents thought that quality (95.0%),

delivery (88.1%) and cost (81.1%) were the major areas of concern when evaluating suppliers.

Enterprises of different forms of ownership and sizes showed the similar tendency (see exhibits

52 and 53).

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=>;

Exhibit 52: Scope of supplier evaluation system by form of ownership of enterprises

Note: Multiple responses allowed

Exhibit 53: Scope of supplier evaluation system by size of enterprises

Note: Multiple responses allowed

When it comes to the performance indicators, more than 90% of the respondents regarded

on-time delivery as the key performance indicators when evaluating suppliers (see exhibit 54).

76.4% of the surveyed enterprises thought cost reduction was an important indicator. Enterprises

of various forms of ownership and sizes showed similar preferences (see exhibits 54 and 55).

!"#$#%&'(#)*+*,-./#0*'1-* >>

China sourcing survey

Exhibit 54: Performance indicators of suppliers by form of ownership of enterprises

Note: Multiple responses allowed

Exhibit 55: Performance indicators of suppliers by size of enterprises

Note: Multiple responses allowed

ii. Execution of supplier evaluation system

Selecting right suppliers and monitoring their ongoing performance greatly rely on the evaluation

system for suppliers. And execution of such system is the key to the effectiveness. According to

the survey, 51.3% of respondents thought that the execution of evaluation system was good or

very good (see exhibit 56). However, the level of execution in SOEs was noteworthy: Over 60% of

respondents from SOEs thought that the execution was poor or just fair. This suggests that more

efforts should be put in boosting their execution power.

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=>?

Exhibit 56: Execution of supplier evaluation system by form of ownership of enterprises

iii. Departments or other parties involved in monitoring supplier performance

According to the survey, besides sourcing department, R&D/ engineering design and production/

manufacturing departments also participated in supplier evaluation in most surveyed enterprises.

Enterprises of various forms of ownership and sizes also showed similar pattern except for

SOEs. As for the case of SOEs, clients played a more signi!cant role in supplier monitoring.

Exhibits 57 and 58 give more information.

Exhibit 57: Departments or other parties involved in monitoring supplier performance by

form of ownership of enterprises

Note: Multiple responses allowed

!"#$#%&'(#)*+*,-./#0*'1-* >@

China sourcing survey

Exhibit 58: Departments or other parties involved in monitoring supplier performance by

size of enterprises

Note: Multiple responses allowed

II. Supplier performance

i. Relationship between enterprises and suppliers

A signi!cant proportion of supplier with stable relationship is one of the indicators re"ecting

whether the sourcing process is well-developed. Last year’s survey suggested that about 48.4%

of the surveyed enterprises had established stable relationships with more than half of their

suppliers. This year, the percentage rose 15.8 percentage points to 64.2%. Moreover, only 12.7%

of the respondents said that they had established stable relationships with less than 10% of their

suppliers, improving greatly from last year (44%). Overall, FIEs and large-sized enterprises did a

better job than their counterparts. Exhibits 59 and 60 give more details.

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=>A

Exhibit 59: Proportion of suppliers with stable relationship by form of ownership of

enterprises

Exhibit 60: Proportion of suppliers with stable relationship by size of enterprises

Proportion of principal suppliers is another important indicator contributing to the success of

enterprises. According to the survey, 14.4% of the surveyed enterprises indicated the proportion

of their principal suppliers increased last year. Among different forms of enterprises, SOEs

performed slightly better than their counterparts. Please see exhibit 61 for more information.

!"#$#%&'(#)*+*,-./#0*'1-* >B

China sourcing survey

Exhibit 61: Proportion of principal suppliers increased last year

ii. Degree of participation by suppliers in R&D

The degree of cooperation with suppliers in R&D is also important for an enterprise. According

to the survey, over 60% of the respondents reported that the involvement of their suppliers in

the early stage of R&D was none or little, suggesting that most enterprises was yet to recognize

the importance of cooperating with suppliers in the area of R&D. Overall, FIEs and large-sized

enterprises involved suppliers in early stage of R&D in a more actively manner (see exhibits 62

and 63).

Exhibit 62: Degree of participation by suppliers in the early stage of research and

development by form of ownership of enterprises

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=>C

Exhibit 63: Degree of participation by suppliers in the early stage of research and

development by size of enterprises

8. Informatization

i. Adoption of bar code system

Among the surveyed enterprises, 72% of them adopted bar code systems for their raw materials.

However, less than half of them admitted that the usage of bar code was fully incorporated into

all business and operational units. As shown in exhibit 64, in general, the larger the enterprises,

the more widely adoption of bar code system across the enterprises.

Exhibit 64: Adoption of bar code system across various business and operational units

within the enterprise

ii. Use of information technology

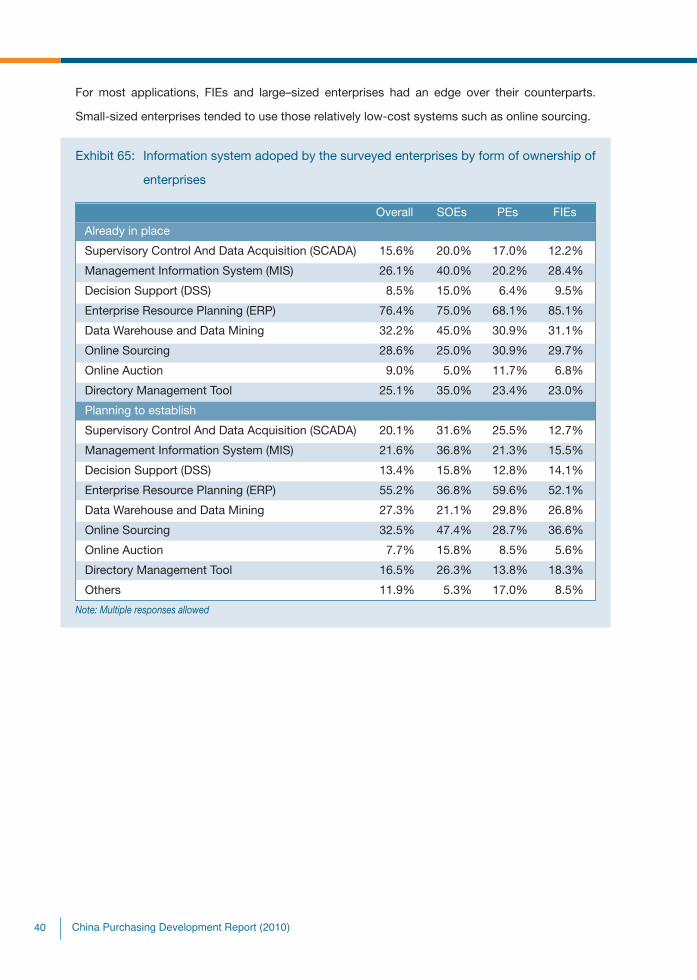

Exhibits 65 and 66 show the application of information system of the surveyed enterprises.

The mostly used information system among the surveyed enterprises was Enterprise Resource

Planning (ERP), with 76.4% of respondents had it already in place. Data Warehouse and Data

Mining came second, with 32.2% of application among the respondents.

!"#$#%&'(#)*+*,-./#0*'1-* >D

China sourcing survey

For most applications, FIEs and large–sized enterprises had an edge over their counterparts.

Small-sized enterprises tended to use those relatively low-cost systems such as online sourcing.

Exhibit 65: Information system adoped by the surveyed enterprises by form of ownership of

enterprises

Overall SOEs PEs FIEs

Already in place

Supervisory Control And Data Acquisition (SCADA) 15.6% 20.0% 17.0% 12.2%

Management Information System (MIS) 26.1% 40.0% 20.2% 28.4%

Decision Support (DSS) 8.5% 15.0% 6.4% 9.5%

Enterprise Resource Planning (ERP) 76.4% 75.0% 68.1% 85.1%

Data Warehouse and Data Mining 32.2% 45.0% 30.9% 31.1%

Online Sourcing 28.6% 25.0% 30.9% 29.7%

Online Auction 9.0% 5.0% 11.7% 6.8%

Directory Management Tool 25.1% 35.0% 23.4% 23.0%

Planning to establish

Supervisory Control And Data Acquisition (SCADA) 20.1% 31.6% 25.5% 12.7%

Management Information System (MIS) 21.6% 36.8% 21.3% 15.5%

Decision Support (DSS) 13.4% 15.8% 12.8% 14.1%

Enterprise Resource Planning (ERP) 55.2% 36.8% 59.6% 52.1%

Data Warehouse and Data Mining 27.3% 21.1% 29.8% 26.8%

Online Sourcing 32.5% 47.4% 28.7% 36.6%

Online Auction 7.7% 15.8% 8.5% 5.6%

Directory Management Tool 16.5% 26.3% 13.8% 18.3%

Others 11.9% 5.3% 17.0% 8.5%

Note: Multiple responses allowed

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=?<

Exhibit 66: Information system adopted by the surveyed enterprises by size of enterprises

Large-sized Medium-sized Small-sized

enterprises enterprises enterprises

Already in place

Supervisory Control And Data Acquisition (SCADA) 14.4% 14.3% 20.5%

Management Information System (MIS) 25.6% 27.1% 25.6%

Decision Support (DSS) 5.6% 11.4% 10.3%

Enterprise Resource Planning (ERP) 87.8% 70.0% 61.5%

Data Warehouse and Data Mining 23.3% 38.6% 41.0%

Online Sourcing 25.6% 28.6% 35.9%

Online Auction 8.9% 7.1% 12.8%

Directory Management Tool 16.7% 25.7% 43.6%

Planning to establish

Supervisory Control And Data Acquisition (SCADA) 18.8% 18.8% 25.0%

Management Information System (MIS) 17.6% 17.4% 37.5%

Decision Support (DSS) 12.9% 10.1% 20.0%

Enterprise Resource Planning (ERP) 51.8% 58.0% 57.5%

Data Warehouse and Data Mining 17.6% 31.9% 40.0%

Online Sourcing 29.4% 36.2% 32.5%

Online Auction 8.2% 5.8% 10.0%

Directory Management Tool 9.4% 23.2% 20.0%

Others 7.1% 15.9% 15.0%

Note: Multiple responses allowed

In general, adoption of online sourcing and online auction were not common among the surveyed

enterprises. In terms of online sourcing and online auction costs, it accounted for 27.6%

and 9.5% of the total sourcing costs respectively for the enterprises. SOEs and small-sized

enterprises spent the most on online sourcing. As for online auction, FIEs and small-sized were

more receptive with this approach. Exhibits 67 and 68 present a more detailed picture.

!"#$#%&'(#)*+*,-./#0*'1-* ?2

China sourcing survey

Exhibit 67: Share of total sourcing costs by online sourcing and online auction by form of

ownership of enterprises

Exhibit 68: Share of total sourcing costs by online sourcing and online auction by size of

enterprises

Overall, 27.4% of the surveyed enterprises said their principal suppliers were capable of online

sourcing. In general, more principal suppliers of SOEs and small-sized enterprises were capable

of online sourcing (see exhibits 69 and 70).

Exhibit 69: Prinicpal suppliers with online sourcing capability by form of ownership of

enterprises

Exhibit 70: Prinicpal suppliers with online sourcing capability by size of enterprises

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=?;

Many enterprises are aware of the important role of informatization in modernizing the sourcing

activities. However, many challenges have to be overcome before they apply these IT systems. The

survey revealed that the major obstacles barring enterprises were lack of talents who know both

business and IT business well (48.8%), dif!culty in identifying appropriate partners for informatization

(43.8%) and inaccurate data (40.4%). The problem of lack of talents was utmost serious among SOEs

and small-sized enterprises. Exhibits 71 and 72 show more details.

Exhibit 71: Major obstacles for infomatization by form of ownership of enterprises

Note: Multiple responses allowed

Exhibit 72: Major obstacles for infomatization by size of enterprises

Note: Multiple responses allowed

!"#$#%&'(#)*+*,-./#0*'1-* ?>

China sourcing survey

9. Green sourcing

i. Products meeting national green standards

Green sourcing is gaining attention among enterprises as consumers are becoming more and

more conscious of green issues. And the Chinese government has been actively promoting

environmental protection as well as sustainable development. According to the survey, more

than half of the respondents said their products met the national green standards. As shown in

exhibits 73 and 74, a larger proportion of SOEs and large-sized enterprises said their products

met the national green standards. 75.5% of the suppliers of the surveyed enterprises provided

products meeting national green standards. FIEs and large-sized enterprises took the lead in

having more suppliers providing products meeting national green standards. Exhibits 75 and 76

give more details.

Exhibit 73: Products meeting national green standards by form of ownership of enterprises

Exhibit 74: Products meeting national green standards by size of enterprises

Exhibit 75: Proportion of suppliers providing products meeting national green standards by

form of ownership of enterprises

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=??

Exhibit 76: Proportion of suppliers providing products meeting national green standards by

size of enterprises

ii. Factors affecting practising green sourcing

The three major factors affecting green sourcing practice were cost (68.5%), new sources of raw

materials (65.0%) and technology and process innovation (61.0%) respectively. Cost was the

core factor of green sourcing adoption across all sizes and forms of ownership of enterprises.

Please see exhibits 77 and 78 for more details.

Exhibit 77: Factors affecting practising green sourcing by form of ownership of enterprises

!"#$#%&'(#)*+*,-./#0*'1-* ?@

China sourcing survey

Exhibit 78: Factors affecting practising green sourcing by size of enterprises

iii. Awareness on environmental protection of enterprises

73% of the surveyed enterprises said they had complied with laws and regulations in toxic

waste disposal. The compliance rate was higher for FIEs, SOEs and large-sized enterprises (see

exhibits 79 and 80).

Exhibit 79: Compliance with laws and regulations in toxic waste disposal by form of

ownership of enterprises

Exhibit 80: Compliance with laws and regulations in toxic waste disposal by size of

enterprises

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=?A

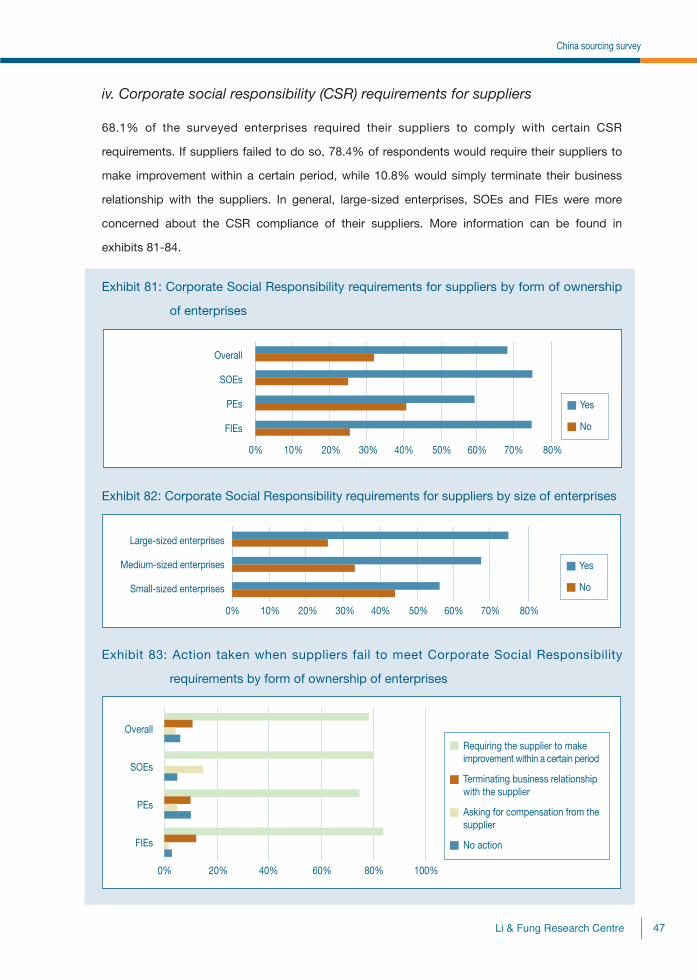

iv. Corporate social responsibility (CSR) requirements for suppliers

68.1% of the surveyed enterprises required their suppliers to comply with certain CSR

requirements. If suppliers failed to do so, 78.4% of respondents would require their suppliers to

make improvement within a certain period, while 10.8% would simply terminate their business

relationship with the suppliers. In general, large-sized enterprises, SOEs and FIEs were more

concerned about the CSR compliance of their suppliers. More information can be found in

exhibits 81-84.

Exhibit 81: Corporate Social Responsibility requirements for suppliers by form of ownership

of enterprises

Exhibit 82: Corporate Social Responsibility requirements for suppliers by size of enterprises

Exhibit 83: Action taken when suppliers fail to meet Corporate Social Responsibility

requirements by form of ownership of enterprises

!"#$#%&'(#)*+*,-./#0*'1-* ?B

China sourcing survey

Exhibit 84: Action taken when suppliers fail to meet Corporate Social Responsibility

requirements by size of enterprises

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=?C

*F!GFGHIJKJ!LM!NOPQRGJKFS!GQTKUKTKVJ!GFW!JLOPQKFS!JKTOGTKLFJ!

XKTR!'<3!GFW!/<3

CY!#RV!ZGFOMGQTOPKFS!JVQTLP

The CFLP China Manufacturing Purchasing Managers’ Index (PMI) provides an early indicator

each month of economic activities in the Chinese manufacturing sector. It is compiled by the

China Federation of Logistics & Purchasing (CFLP) and the China Logistics Information Centre

(CLIC), based on data collected by the National Bureau of Statistics (NBS). The PMI was

launched in January 2005.

Every month questionnaires on their purchasing activities and supply situations are sent to over

800 manufacturing enterprises all over China. There are 11 indicators in the survey: Output, New

Orders, New Export Orders, Backlogs of Orders, Stocks of Finished Goods, Purchases of Inputs,

Imports, Input Prices, Stocks of Major Inputs, Employment and Suppliers’ Delivery Time. An

index reading above 50% indicates an overall positive change in that variable; below 50%, an

overall negative change.

The PMI is a composite index based on the seasonally adjusted diffusion indices for !ve of

the indicators with varying weights: New Orders – 30%; Output – 25%; Employment – 20%;

Suppliers’ Delivery Times – 15%; and Stocks of Major Inputs – 10%. A PMI reading above 50%

indicates an overall expansion in the manufacturing sector; below 50, an overall contraction.

The post-crisis recovery is well on track, yet recent PMI readings indicate

growth moderation in the manufacturing sector

The headline PMI has stayed above the “expansionary 50-mark” for 18 consecutive months,

showing that the post-crisis recovery is suf!ciently solid and self-sustaining (see exhibit 1).

However, the headline PMI has trended downward since April 2010, indicating growth

moderation in the manufacturing sector. Though the headline PMI rebounded from 51.2% in July

to 51.7% in August, the July reading and the August reading were still the lowest and the second

lowest since March 2009. The moderation in industrial activity was attributable to government

tightening on the property sector and local government borrowing, as well as mandatory

requirement to shut down energy-inef!cient factories.

!"#$#%&'(#)*+*,-./#0*'1-* ?D

*F!GFGHIJKJ!LM!NOPQRGJKFS!GQTKUKTKVJ!GFW!JLOPQKFS!JKTOGTKLFJ!XKTR!'<3!GFW!/<3

The modest rebound in the August PMI suggests that the Chinese economy will not slide into

recession. Looking forward, we expect the headline PMI to "uctuate between 52-54 in 4Q10.

Industrial activities will be boosted by Beijing’s accelerated efforts to build public housing. The

improving auto market may become another favourable factor, if the improvement continues in

the coming months. Downside risks, however, include the extent of the slowdown in property

investment by real estate developers, the uncertainties about the global economy and China’s

export growth, as well as the policy intensity to get rid of backward production capacities,

energy-intensive and highly-polluting industries.

We believe the government will keep its ‘neutral’ monetary policy stance unchanged for the rest

of the year. It will continue to regulate local government !nancing vehicles, but is unlikely to raise

interest rate or reserve requirement ratio (RRR). Neither do we think the government will ease its

crackdown measures on real estate speculation, as housing prices have barely gone down this

year. However, to avoid a sharp slowdown in growth, Beijing will increase investment spending

on public housing. We also believe the government will be persistent in pushing forward

structural reforms.

Exhibit 1: Monthly PMI, Jan 2009 – Aug 2010

Source: China Federation of Logistics & Purchasing

The output index re"ects overall production activities of the manufacturing sector. The index has

stayed above the critical level of 50% since February 2009, indicating continuous expansion of

output of the manufacturing sector (see exhibit 2).

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=@<

Exhibit 2: Output index, Jan 2009 – Aug 2010

Source: China Federation of Logistics & Purchasing

Domestic demand recovered earlier and grew faster than foreign demand

The new orders index, which covers both domestic and foreign demand, has stayed above 50%

since February 2009 for 19 months.

The new export orders index has stayed above 50% since May 2009 for 16 months. The two

indices show that both domestic and foreign demand for Chinese manufactured products have

been on the rise (see exhibit 3).

The new orders index rose above the 50%-line earlier than the new export orders index,

implying that domestic demand recovered earlier than foreign demand, boosted by the Chinese

government’s stimulus package to support domestic demand in late 2008. One should also note

that the new orders index was higher than the new export orders index throughout February 2009

to August 2010, indicating that domestic demand grew faster than foreign demand.

!"#$#%&'(#)*+*,-./#0*'1-* @2

*F!GFGHIJKJ!LM!NOPQRGJKFS!GQTKUKTKVJ!GFW!JLOPQKFS!JKTOGTKLFJ!XKTR!'<3!GFW!/<3

Exhibit 3: New orders index and new export orders index, Jan 2009 – Aug 2010

Source: China Federation of Logistics & Purchasing

Chinese manufacturers have faced mounting cost pressure

The input prices index re"ects changes in manufacturers’ production cost. Chinese manufacturers

have faced increasing cost pressure since April 2009 (see exhibit 4). In particular, prices of major

inputs rose at an accelerated pace in December 2009 and January 2010, when the input price index

registered the highest readings since August 2008. Although the index eased a bit in February 2010,

it quickly rebounded in March and then jumped to reach another peak in April 2010. The index

moderated to 58.9% in May and further dropped to 50.4% in July 2010. However, it surged by 10.1

percentage points to 60.5% in August 2010. The latest index reading raises renewed concern about

the problems of production cost pressure and squeezed producers’ margins, as well as suggests

stronger in"ationary pressure on downstream prices in the near and medium term. !

Exhibit 4: Input prices index, Jan 2009 – Aug 2010

Source: China Federation of Logistics & Purchasing

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=@;

2. The non-manufacturing sector

The CFLP China Non-Manufacturing Index (NMI) serves as an early indicator of economic activities

in China’s non-manufacturing sector. Every month, questionnaires are sent to non-manufacturing

enterprises in 20 industries, which are categorized into producer services, consumer services and

construction business. There are 10 indicators in the survey: Business Activity, New Orders, New

Export Orders, Backlogs of Orders, Stocks, Input Prices, Prices Charged, Employment, Suppliers’

Delivery Time and Business Activity Forecast. Survey responses re"ect the change of each indicator,

if any, in the current month compared to the previous month. Unlike the PMI, there is no composite

index for China’s NMI, and the business activity index of every month is quoted as the NMI of the

month. An NMI reading above 50% indicates an overall expansion in the non-manufacturing sector;

below 50%, an overall contraction. Data have been collected since January 2007 and the !rst NMI

was published in January 2008.

Recent NMI readings showed steady recovery of the non-manufacturing sector

Exhibit 5 demonstrates the NMI readings from January 2009 to August 2010. The NMI stayed

above 50% throughout the period (except in February 2009 and February 2010 - the Chinese

New Year - when many businesses were not operating during the holiday), indicating that the

non-manufacturing sector kept expanding.

The NMI has been, in general, higher than the PMI for the past 20 months, denoting a stronger

recovery in the non-manufacturing sector than in the manufacturing sector. !

Exhibit 5: Business activity index, Jan 2009 – Aug 2010

Source: China Federation of Logistics & Purchasing

!"#$#%&'(#)*+*,-./#0*'1-* @>

*F!GFGHIJKJ!LM!NOPQRGJKFS!GQTKUKTKVJ!GFW!JLOPQKFS!JKTOGTKLFJ!XKTR!'<3!GFW!/<3

Domestic demand showed stronger recovery than foreign demand

The new orders index re"ects the overall demand for services, including both domestic and

foreign demand, while the new export orders index covers demand from foreign clients only.

The new orders index averaged at 52.6% in year 2009, showing that demand was growing

steadily. The index peaked in April 2010 (58.7%). It moderated in the following two months, but

then rebounded to 55.8% in July 2010 and further to 56.2% in August 2010 (see exhibit 6).

The new export orders index averaged at 47.2% in 2009, indicating an overall contraction in

orders from foreign clients in the year. The situation has improved this year. The index has stayed

above 50% for six consecutive months since March 2010, con!rming the recovery of foreign

demand for services (see also exhibit 6).

Throughout January 2009 to August 2010, the new orders index has generally been higher than

the new export orders index, indicating that domestic demand has been growing faster than

foreign demand. This is largely a result of the government policy to boost domestic demand.

Exhibit 6: New orders and new export orders indices, Jan 2009 – Aug 2010

Source: China Federation of Logistics & Purchasing

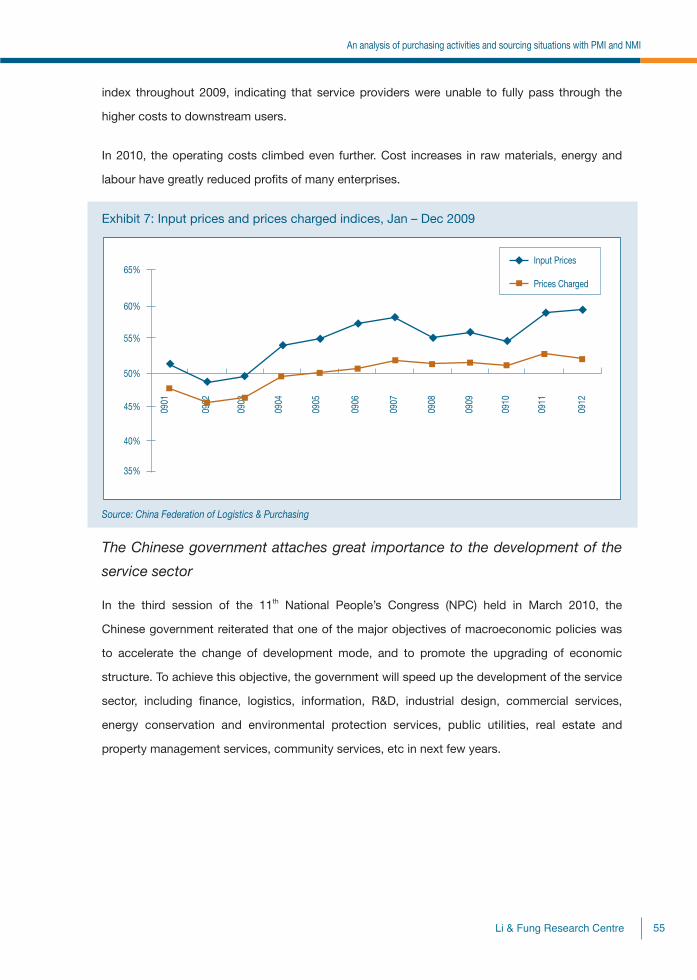

Increasing cost pressure for enterprises in the non-manufacturing sector

The input prices index re"ects the changes in the cost of inputs incurred by the enterprises

surveyed, while the prices charged index re"ects the prices charged when enterprises sell their

services. As shown in exhibit 7, the input prices index was always higher than the prices charged

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=@?

index throughout 2009, indicating that service providers were unable to fully pass through the

higher costs to downstream users.

In 2010, the operating costs climbed even further. Cost increases in raw materials, energy and

labour have greatly reduced pro!ts of many enterprises.

Exhibit 7: Input prices and prices charged indices, Jan – Dec 2009

Source: China Federation of Logistics & Purchasing

The Chinese government attaches great importance to the development of the

service sector

In the third session of the 11th National People’s Congress (NPC) held in March 2010, the

Chinese government reiterated that one of the major objectives of macroeconomic policies was

to accelerate the change of development mode, and to promote the upgrading of economic

structure. To achieve this objective, the government will speed up the development of the service

sector, including !nance, logistics, information, R&D, industrial design, commercial services,

energy conservation and environmental protection services, public utilities, real estate and

property management services, community services, etc in next few years.

!"#$#%&'(#)*+*,-./#0*'1-* @@

*F!GFGHIJKJ!LM!NOPQRGJKFS!GQTKUKTKVJ!GFW!JLOPQKFS!JKTOGTKLFJ!XKTR!'<3!GFW!/<3

Sourcing light-manufactured consumer products in China: cost trends and outlook

Part One: Major Price Indicators

1. China’s CPI growth reached 3.5% yoy in August, the highest in twenty-

two months

The yoy growth rate of China’s consumer price index (CPI)1 softened from 2.7% in February to

2.4% in March, and has been on an upward trend since then. The CPI growth rose to 3.3% yoy

in July and further reached 3.5% yoy in August, the highest in twenty-two months, due largely to

higher prices of vegetables and meat triggered by the recent rainstorms, "oods and hot weather

in China. The price index of food, which weighs 33.2% in the CPI accounting, rose by 7.5% yoy,

whilst that of non-food grew by 1.5% yoy in August. (See exhibit 1 & 2)

Particularly noteworthy is that the month-on-month (mom) growth of CPI has rebounded since

July. The price index registered positive mom growth of 0.4% and 0.6% in July and August

respectively, after dropping by 0.1% mom and 0.6% mom in May and June respectively.

Looking ahead, China’s CPI will be supported by factors such as rising labour costs, pass-

through of upstream price pressures, strengthening domestic demand, the buildup of in"ationary

expectations, tighter food supply due to natural disasters, as well as speculation in agricultural

commodities. It is likely that food prices will go down and the CPI growth will slow, if weather

conditions in China improve. We expect the CPI growth in FY10 to exceed the government target

of 3.0% and hit 4%.

1 The CPI, compiled by the National Bureau of Statistics of China, measures the price of a basket of 600-700 goods and services that a typical household purchases.

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=@A

2 The PPI, compiled by the National Bureau of Statistics of China, measures the prices of industrial products when they are sold for the !rst time after production.

Exhibit 1: China’s CPI growth, Sep 2008 - Aug 2010

Source: National Bureau of Statistics, PRC

Exhibit 2: China’s CPI growth by selected commodity, Mar - Aug 2010

Mar Apr May Jun Jul Aug

yoy growth (%)

Clothing -1.1 -1.3 -1.2 -1.0 -0.8 -1.2

Household services, maintenance and -0.7 -0.5 -0.3 0.0 0.2 0.4

renovation

Recreational, educational products & 0.3 0.4 0.6 0.9 1.1 1.2

services

Source: National Bureau of Statistics, PRC

2. PPI growth peaked in May 2010, and has been on a downward trend

since then

The growth rate of China’s producer price index (PPI)2 rose from 5.9% yoy in March to 6.8% yoy

in April, and peaked at 7.1% yoy in May. Afterwards, it softened to 6.4% yoy in June, 4.8% yoy in

July and 4.3% yoy in August. (See exhibit 3)

Sep-09 -0.8%

Oct -0.5%

Nov 0.6%

Dec 1.9%

Jan-10 1.5%

Feb 2.7%

Mar 2.4%

Apr 2.8%

May 3.1%

Jun 2.9%

Jul 3.3%

Aug 3.5%

!"#$#%&'(#)*+*,-./#0*'1-* @B

Sourcing light-manufactured consumer products in China: cost trends and outlook

Despite the recent decline in PPI growth, we believe ex-factory prices will stay !rm in the near

future, bolstered by improving domestic and export demand, pass-through of upstream price

pressures, and mounting labour costs. It is noteworthy that, as of 10 September 2010, the

minimum wage levels in 28 provinces/municipalities in China have been revised upward. Besides,

there have been a number of strikes in coastal provinces recently, with workers asking for salary

increase. Many employers have offered considerable pay-rise to settle labour disputes. Detailed

discussion can be found in Part four.

Exhibit 3: China’s PPI growth, Sep 2008 - Aug 2010

Source: National Bureau of Statistics, PRC

Exhibit 4: China’s PPI growth by selected industry, Mar - Aug 2010

Mar Apr May Jun Jul Aug

yoy growth (%)

Textile industry 5.3 6.6 7.5 8.2 8.2 8.6

Textile, clothing and footwear production 1.7 1.6 1.8 1.6 1.9 1.3

Leather, furs, down and related products 0.8 1.1 1.6 1.6 2.2 1.9

Timber processing & wood, bamboo, cane, 0.6 1.2 1.7 1.8 1.9 1.9

palm !ber and straw products

Source: National Bureau of Statistics, PRC

Sep-09 -7.0%

Oct -5.8%

Nov 2.1%

Dec 1.7%

Jan-10 4.3%

Feb 5.4%

Mar 5.9%

Apr 6.8%

May 7.1%

Jun 6.4%

Jul 4.8%

Aug 4.3%

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=@C

Part Two: Raw Material Prices

1. The growth rate of China’s purchasing price index of raw material, fuel

and power has declined since May

The yoy growth rate of China’s purchasing price index of raw material, fuel and power3 picked up

from 10.3% in February to 11.5% in March, and then reached 12.0% in April and 12.2% in May,

the highest in twenty months, before declining all the way to 7.5% in August. (See exhibit 5 & 6)

The positive growth of the price index re"ected the increase in prices of production inputs,

underlining the problems of production cost pressure and squeezed margins for Chinese

manufacturers. It also suggests stronger in"ationary pressure on downstream prices in the near

and medium term.

Looking ahead, we do not expect the yoy growth rate of this index to fall much in the near

future, despite the higher comparison base in 4Q09. Some price indicators show that prices

of production inputs have picked up again. For example, the input prices sub-index of China’s

manufacturing PMI rebounded strongly from the recent low of 50.4 in July to 60.5 in August.

Another index indicating input prices compiled by the Ministry of Commerce shows that input

prices have started an upward trend again since mid July and reached the recent peak in late

August, the highest level since late May.

3 The purchasing price index for raw material, fuel and power, compiled by the National Bureau of Statistics of China, measures the prices of production inputs such as raw materials, fuels and power purchased by industrial enterprises.

!"#$#%&'(#)*+*,-./#0*'1-* @D

Sourcing light-manufactured consumer products in China: cost trends and outlook

Exhibit 5: China’s purchasing price index of raw material, fuel and power, Sep 2008 - Aug

2010 (% yoy growth)

Source: National Bureau of Statistics, PRC

Exhibit 6: China’s purchasing price index of raw material, fuel and power by selected

commodity, Mar - Aug 2010

Mar Apr May Jun Jul Aug

yoy growth (%)

Fuel & power 25.6 24.0 23.4 19.5 12.0 10.2

Non-ferrous metals 32.8 29.1 26.0 21.1 19.5 16.6

Raw materials for chemical industry 6.9 7.4 7.8 7.2 6.7 5.9

Timber and paper pulp 1.4 2.7 4.0 3.4 2.7 4.1

Textile raw materials 4.5 5.5 5.7 5.9 6.3 6.1

Source: National Bureau of Statistics, PRC

(i) Purchasing price index of fuel & power

The growth rate of the purchasing price index of fuel & power has been on a downward trend,

declining all the way from 25.6% yoy in March to 10.2% yoy in August. (See exhibit 6)

(ii) Purchasing price index of non-ferrous metals

The growth rate of the purchasing price index of non-ferrous metals came in at 16.6% yoy in

August, having declined for !ve consecutive months. (See exhibit 6)

Sep-09 -10.1%

Oct -8.4%

Nov -3.6%

Dec 3.0%

Jan-10 8.0%

Feb 10.3%

Mar 11.5%

Apr 12.0%

May 12.2%

Jun 10.8%

Jul 8.5%

Aug 7.5%

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=A<

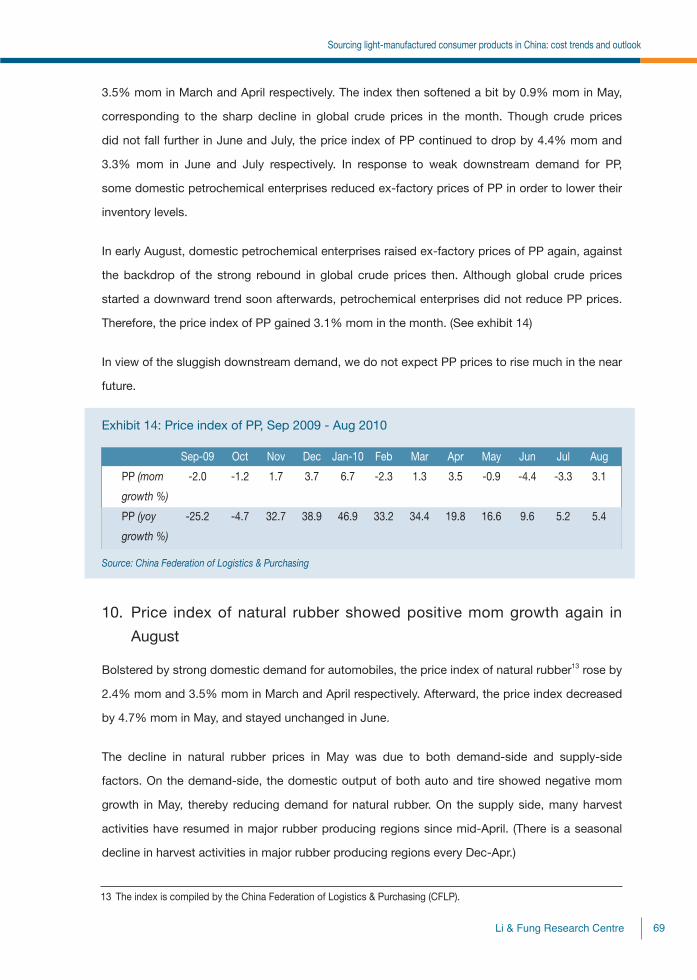

(iii) Purchasing price index of raw materials for chemical industry

The growth rate of purchasing price index of raw materials for chemical industry was on an

upward trend, rising all the way from 5.4% yoy in February to 7.8% yoy in May. Afterwards, the

growth rate of the index fell all the way to 5.9% yoy in August.(See exhibit 6)

(iv) Purchasing price index of timber and paper pulp

The growth rate of the purchasing price index of timber and paper pulp turned positive in March,

and then "uctuated within the range of 2.7-4.1% yoy throughout April to August 2010. (See

exhibit 6)

(v) Purchasing price index of textile raw materials

The growth rate of the purchasing price index of textile raw materials increased all the way from

1.1% yoy in Dec 2009 to 6.3% yoy in July 2010, before edging down to 6.1% yoy in August. (See

exhibit 6)

2. China’s cotton price indices trended upward throughout mid February to

early July, and have softened since then

After plateauing in January and early February, China’s cotton price indices4 were on an

increasing trend throughout mid February to early July. Since then, the price indices have

moderated. The CC Index 328, for example, climbed from 14912 on 21 February to the recent

peak of 18419 on 9 July, and then moderated to 18005 on 31 August. Overall, the prices of this

type of cotton increased by about 21% in the !rst eight months of 2010. (See exhibit 7)

The sharp rise in domestic cotton prices was driven by strong downstream demand from both

China and foreign countries, falling supply of cotton, as well as increasing global cotton prices.

Due to poor weather and reduction in planting area, China’s cotton output declined by 14.6% yoy

in 2009. The decline is widely expected to continue in 2010.

Global cotton prices have also recorded strong rise so far this year, due largely to the reduction

in global output of cotton, as well as improving demand. The Cotlook A index, one of the major

global price indices of cotton, went up from 78.45 on 4 January 2010 to 94.20 on 31 August.

4 The indices, compiled by the China Cotton Association, track cotton prices quoted from two hundred textile enterprises.

http://www.china-cotton.org/

!"#$#%&'(#)*+*,-./#0*'1-* A2

Sourcing light-manufactured consumer products in China: cost trends and outlook

While China’s cotton output cannot meet the domestic demand, China has continued to import

large amounts of cotton from other countries in recent years. Besides, to increase supply in the

domestic cotton market, the Chinese government raised import quotas of cotton in May and has

released part of the state reserve since early August. It seems that such efforts have contributed

to the recent moderation of cotton prices.

Looking ahead, we do not expect cotton prices to fall much for the rest of the year, especially as

domestic cotton output is set to decrease due to the severe weather conditions.

Exhibit 7: China’s cotton price indices, Sep 2009 - Aug 2010

Source: China Cotton Association

3. Nanjing Wool Market Composite Index rebounded in June, and then

moderated a bit in July

The Nanjing Wool Market Composite Index5, one of the major wool price indices in China, stayed

at high level throughout late January to April 2010. Afterwards, the price index declined from

58.37 yuan per kg at end-April to 55.94 yuan per kg at end-May, but then rebounded to 57.59

yuan per kg at end-June. (See exhibit 8)

5 http://www.woolmarket.com.cn/

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=A;

Note that the Nanjing Wool Market Composite Index would be signi!cantly affected by the

exchange rate movements of the currencies of Australia and New Zealand, the major wool

exporters. The drop in the wool price index in May was largely attributable to the depreciation

of the Australian dollar against the RMB in May. The decline in the Australian Wool Exchange

(AWEX) Eastern market indicator, one of the major wool price indices in Australia, was

comparatively slight in Australia dollar terms.

In July, the Australian dollar appreciated strongly by more than 6% against the RMB, thereby

putting upward pressure on wool prices in RMB terms. However, such impact was offset by the

weak demand from textile manufacturers in the month, traditionally the low season. The wool

price index softened by 0.3% from the previous month to 57.42 yuan per kg at end-July.

Supported by growing downstream demand from advanced economies and tight supply, wool

prices are expected to stay !rm in the short to medium term. Both Australia and New Zealand

have witnessed reduction in wool production in recent years. One major cause is that many wool

producers have switched to meat production in response to higher meat prices.

Exhibit 8: Nanjing Wool Market Composite Index, Aug 2009 - Jul 2010

Aug-09 Sep Oct Nov Dec Jan-10 Feb Mar Apr May Jun Jul

Month-end 48.73 51.20 54.34 54.64 55.36 58.14 57.65 58.14 58.37 55.94 57.59 57.42

index

(yuan/kg)

Source: The Nanjing Wool Market

4. Price indices of polyester moderated in the second half of August

After trending upward in Apr 2010, the price indices of polyester6 moderated in May, due to the

drop in puri!ed terephthalic acid (PTA)7 prices (which in turn was due to the decrease in crude

oil prices). The indices picked up again in the second half of June, as a result of the market

expectation of falling supply of polyester in China, as well as the rebound in crude prices. (See

exhibit 9)

6 The indices are complied by the China Chemical & Fiber Economic Information Network (CCFEI).7 Puri!ed terephthalic acid (PTA) is a commodity chemical used primarily in polyester production.

!"#$#%&'(#)*+*,-./#0*'1-* A>

Sourcing light-manufactured consumer products in China: cost trends and outlook

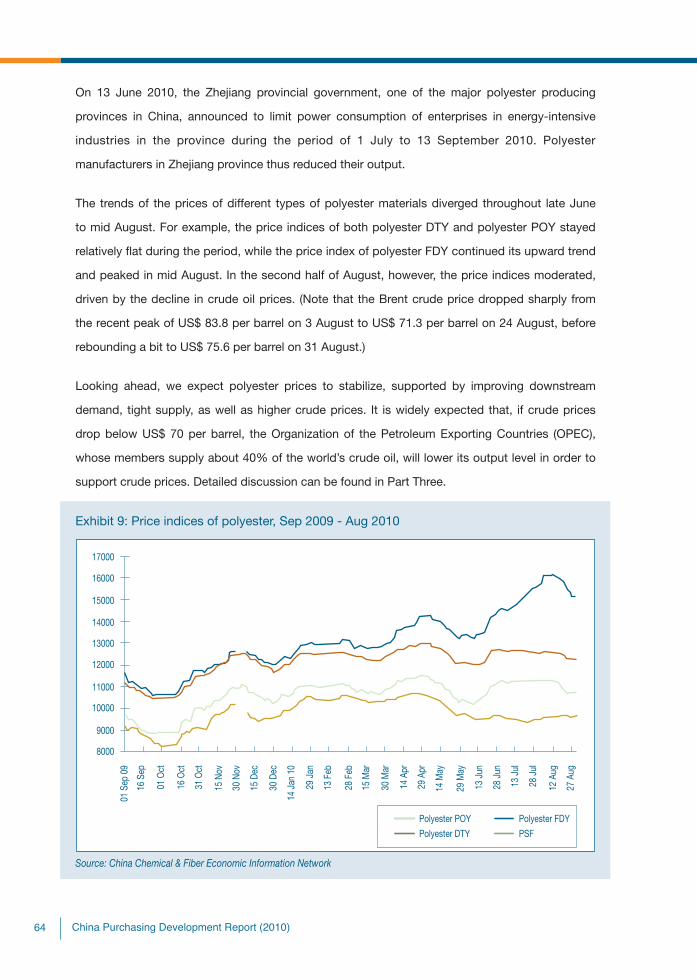

On 13 June 2010, the Zhejiang provincial government, one of the major polyester producing

provinces in China, announced to limit power consumption of enterprises in energy-intensive

industries in the province during the period of 1 July to 13 September 2010. Polyester

manufacturers in Zhejiang province thus reduced their output.

The trends of the prices of different types of polyester materials diverged throughout late June

to mid August. For example, the price indices of both polyester DTY and polyester POY stayed

relatively "at during the period, while the price index of polyester FDY continued its upward trend

and peaked in mid August. In the second half of August, however, the price indices moderated,

driven by the decline in crude oil prices. (Note that the Brent crude price dropped sharply from

the recent peak of US$ 83.8 per barrel on 3 August to US$ 71.3 per barrel on 24 August, before

rebounding a bit to US$ 75.6 per barrel on 31 August.)

Looking ahead, we expect polyester prices to stabilize, supported by improving downstream

demand, tight supply, as well as higher crude prices. It is widely expected that, if crude prices

drop below US$ 70 per barrel, the Organization of the Petroleum Exporting Countries (OPEC),

whose members supply about 40% of the world’s crude oil, will lower its output level in order to

support crude prices. Detailed discussion can be found in Part Three.

Exhibit 9: Price indices of polyester, Sep 2009 - Aug 2010

Source: China Chemical & Fiber Economic Information Network

0/"',#3&-./,+"'(#4*5*6789*'1#)*87-1#:;<2<=A?

5. Price index of acrylic staple !ber stayed stable throughout April to mid

June and has started a downward trend since early July

After rising rapidly in late February and early March, the price index of acrylic staple !ber8 stayed

stable at 22800 throughout April to mid June. Since early July, the price index has started a

downward trend, and moderated to 20700 on 27 August, due largely to the relatively weak

downstream demand, the market expectation of falling acrylic staple !ber prices, as well as

the decline in prices of acrylonitrile, a major raw material of acrylic staple !ber. The supply of

acrylonitrile has increased recently, as many acrylonitrile plants have resumed production after

being shut down for regular maintenance in early 2010. (See exhibit 10)

Note that the downstream demand has improved a bit in recent weeks, according to the local

media. It is expected that prices of acrylic staple !ber will not continue to go down in the near

term.

Exhibit 10: Price indices of acrylic, Sep 2009 - Aug 2010

Source: China Chemical & Fiber Economic Information Network

8 The index is complied by the China Chemical & Fiber Economic Information Network (CCFEI).

!"#$#%&'(#)*+*,-./#0*'1-* A@

Sourcing light-manufactured consumer products in China: cost trends and outlook

6. Price indices of nylon have trended upward again since late July

Driven by the increase in prices of caprolactam, one of the major materials of nylon, as well as

restocking activities, the price indices of nylon9 had trended upward since late February, until

they plateaued in the second half of May. The indices were on a downward trend throughout late

May to late July, along with the moderation of upstream prices. (See exhibit 11)

Besides, it is observed that, in view of high nylon prices, downstream producers tend to be

cautious about placing orders for nylon, and some producers have even switched to use other

!bres as substitutes for nylon.