30

China: The New Land of Opportunity China’s Impact on the Global Optical Communications Industry

China: The New Land of Opportunity

China’s Impact on the Global Optical Communications Industry

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

2

Table of Contents:

Abstract………………………………………………………………………………………...…..4 Executive Summary ……………………………………………………………………….…..….4 Section 1: Telecom Infrastructure Deployments in China……………………….…………....6 Restructuring of service providers…………………………………………………………………………..6 . Continuing Infrastructure Upgrades……………………………………………………….…………..……8

Section 2: The Rise of Domestic Communications Equipment Vendors………………..…10 Huawei Becomes the Dominant Global Telecom Equipment Vendor……………………………...….10

ZTE, Already Strong in Emerging Markets, Plans to Expand into North America and Western Europe……………………………………………….……..……...….….....11 Fiberhome, a full-line equipment supplier, is growing………………………………………….……..….13 Alcatel Lucent Shanghai Bell was the first foreign invested company in China’s telecom market.....14 Other Domestic Equipment Vendors…………………………………………………………………….…15

Section 3: The Emergence of Optical Component and Module Suppliers……………..…..16 Emergence of local suppliers…………………………………………………………………………..…...16

Western companies move production to China………………………………………………….…….....17

Section 4: Challenges and Opportunities Ahead……………………………………………...19 Service provider business and infrastructure projects…………………………………………….….….19

Networking equipment manufacturers……………………………………………………………….…....20 Optical component and module vendors………………………………………………………….……....22

Section 5: Optical Component Vendor Profiles……………………………………………….25 Accelink……………………………………………………………………………………………….…...….25 ATOP Technology……………………………………………………………………………………….......26 Eoptolink Technology……………………………………………………………………………….…........26 Gigalight……………………………………………………………………………………………………....26

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

3

Table of Contents: HG Genuine…………………………………………………………………………………………………..26 Hi-Optel……………………………………………………………………………………………...………..27 HiSense Broadband…………………………………………………………………………………...…….27 Hymax Optoelectronics Inc………………………………………………………………………...……….28 InnoLight…………………………………………………………………………………...…………...…….28 O-Net……………………………………………………………………………………………………...…..28 StarOpto……………………………………………………………………………………………...…...….29 Sunstar Communication Technology……………………………………………………………………...29 WTD…………………………………………………………………………………….………………….....29 Wuxi-ZTE………………………………………………………………………………………………..…...30 Xiamen San-U………………………………………………………………………………………..….…..30

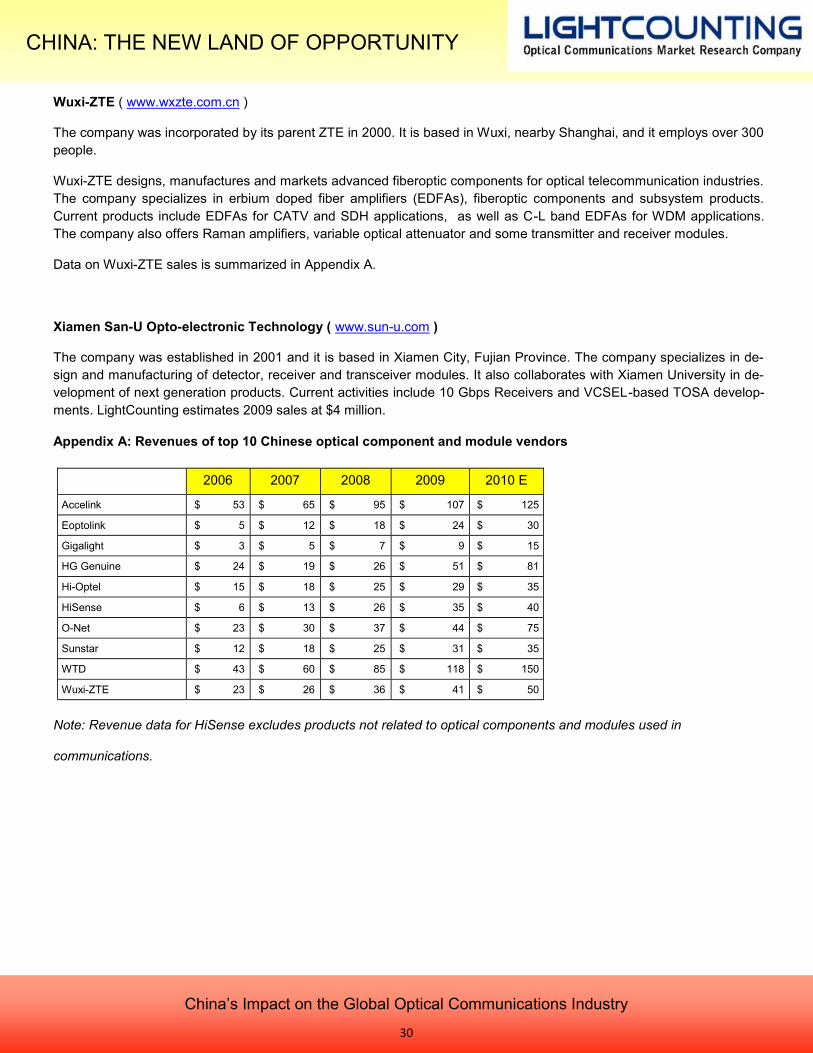

Appendix A: Revenues of the Top 10 Chinese Optical Component and Module Vendors………....…..30

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

4

Abstract:

Impact made by China on the Global Optical Communications Industry over the last decade is remarkable. Increasing

investments in networking infrastructure helped to sustain the global telecom industry during the downturns of 2001-2003

and 2008-2009. Success of Huawei and ZTE has transformed the landscape of the networking equipment market.

Significant portion of manufacturing of optical component and modules has been moved to China after the telecom crash

of 2001 and helped to foster numerous domestic suppliers. This report offers analysis of challenges and opportunities for

Chinese service providers, equipment manufacturers and optical component and module vendors. It also includes

profiles of major optical communication equipment, module and component vendors based in China.

Executive summary:

It is hard to underestimate the impact made by China on the global optical communications industry over the last

decade. Rapid industrial development of the country spearheaded by the Chinese government affected many global

industries, and the optical communications industry is no exception.

China’s impact is observable across the whole supply chain of the industry:

• Domestic infrastructure projects drive demand for optics (from FTTx to wireless backhaul to 40 Gbps systems).

• Chinese network equipment vendors led by Huawei gain market share globally by delivering more cost effective

solutions.

• All major suppliers of optical components and modules move manufacturing to China, and many new local

companies enter the market.

The Chinese government maintained steadily increasing levels of investment into optical networking over the last

decade, while similar projects in many western countries were subjected to delays during economic downturns in 2001–

2003 and 2008–2009. After significant increases in capital expenditures (capex) of three major service providers in

China in 2008–2009, capex has declined by 13% in 2010, as the government tries to slow down growth of the economy.

However, continuing investments in networking infrastructure remain on the top of government agenda. The government

budgeted almost $60 billion for deployment of wireless systems in 2011–2012 and $22 billion for new fiber optic

networks in 2011–2013. While the total capex allocated for 2011-2013 is almost equal to investments made in 2010,

larger fraction of capex is allocated for the latest generations of wireless and broadband access systems.

As the national network system becomes mature, slowdown in networking infrastructure deployments in China is

inevitable. However, progress made by China sets an example for a number of emerging economies that are likely to

increase investments in networking infrastructure as their economies develop. Recognizing this trend, Chinese

equipment manufacturers, lead by Huawei, are increasing focus on these developing economies that are prime for

growth.

Huawei is certainly one of the great success stories in the telecom equipment market. Huawei displaced Alcatel-Lucent

in the number-one position in optical networking two years ago, and it is likely to surpass Ericsson as the largest supplier

of wireline and wireless equipment this year. Despite the phenomenal growth in Huawei’s business, there are certainly

limits to how dominant any company can become. Mature markets are usually dominated by three major players,

creating a stable environment where coalition of two out of the three is strong enough to block any predatory intentions

that the third might have. This suggests that ZTE and FiberHome are likely to gain share in the domestic market and that

Alcatel-Lucent and Ericsson should be able to limit Huawei’s dominance on a global scale.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

5

Local suppliers of optical components and modules used in communication networks have directly benefited from

domestic infrastructure projects and growing global presence of Chinese equipment manufacturers such as Huawei and

ZTE. However, Chinese optical component and module vendors remain smaller than western competitors. Continuing

dominance of the western component and module suppliers is supported by their extensive manufacturing facilities in

China, making their manufacturing cost comparable to Chinese vendors. The western companies have also an

advantage in global presence, while Chinese suppliers are mostly selling into domestic market despite their efforts to

increase global presence. Limited sales of Chinese suppliers to the datacom market segment further limit their business

growth. Building a solid intellectual property base and catching up with competition in 10 Gbps and 40 Gbps

technologies are among many challenges faced by the local manufacturers or optical component and modules.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

6

Section 1: Telecom Infrastructure Deployments in China

As the telecom bubble burst in 2001, most of the infrastructure deployment projects in Europe, Japan, and North

America were put on hold for several years. In contrast, China accelerated infrastructure build-outs during the industry

downturn and continued investing heavily in telecommunication networks as the global industry recovered in 2004–2007.

This pattern was repeated during the economic downturn of 2008–2009: as global investment in networking

infrastructure dropped, the Chinese government kept funding deployments of wireless and optical networks.

While most western countries rely on indirect ways to stimulate deployments of networking infrastructure, such as

modifying regulations to allow for more competition in the market, China uses a more direct approach; the government is

directly involved in determining capital expenditures of Chinese service providers. Deployments of high-speed wireless

and FTTx access networks are elevated to national programs and budgeted by the government.

Restructuring of service providers

Before 1994, the Ministry of Posts and Telecommunications (MPT) provided telephone services through China Telecom.

To battle inefficiencies at China Telecom, the government created China Unicom in 1994 to provide competition for

China Telecom. However, China Unicom was an ineffective competitor against the much larger China Telecom, so in

1999, the government split the telecom market in China into three segments—fixed line, mobile, and satellite—and

created China Mobile to compete in the mobile market and China Satcom to compete in the satellite communications

market.

Maintaining a tight grip on service providers, the Chinese government further restructured the industry in 2002. The

China Telecom monopoly was broken by transferring 30% of its assets, all located in the northern provinces, to China

Netcom. Regulators had hoped that China Telecom would head north and Netcom would expand to the south, which

could spur competition, but consumers realistically did not have more than one choice when choosing fixed-line services.

This restructuring did not accomplish the goal of encouraging competition and protecting consumers, but it did illustrate

the inner workings of the Chinese system. China Netcom was started as a wholesaler for the high-speed data networks

in 1999, and it was backed by Jiang Mianheng, the son of Jiang Zeming, the former Chinese president. By 2002, China

Netcom’s business was on the verge of bankruptcy, partly because of the monopolistic power of China Telecom at that

time. The government’s decision to grant one-third of China Telecom’s assets to Netcom saved the struggling company.

After splitting up the government monopoly carrier China Telecom, in 2008, the government decided to recombine the

major carriers into three entities on a more-level playing field. China Netcom was merged with China Unicom, the

second largest provider of wireless services in China after China Mobile. As part of that deal, China Unicom sold its

CDMA mobile business to China Telecom, giving it a presence in the wireless market. Broadband internet carrier China

Tietong was merged into China Mobile, giving China Mobile a role in broadband networks.

The telecom industry in China today is dominated by China Mobile, China Telecom, and China Unicom; all three are

state run and directed by the Ministry of Information and Industry (MII), the successor to the MPT. All three carriers now

operate fixed-line/broadband and mobile networks. China Mobile remains the dominant provider of wireless services, but

China Unicom and China Telecom combined account for close to 30% of the market, as illustrated in Figure 1. China

Telecom dominates wireline access business and leads in terms of the number of broadband subscribers. However,

China Unicom’s investments in broadband access are equal to those of China Telecom now, and it is closing the gap in

terms of broadband subscribers with China Telecom. China Mobile is a distant third in terms of the number of broadband

subscribers, but the company has an ambitious plan to deploy FTTB/FTTH networks in the next five years.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

7

Figure 1: Number of Broadband and Mobile Customers by Service Provider, as of September 2010

Strict government regulation of the industry structure and continuous investment in networking infrastructure create a

more stable environment in China than in western countries. The western reliance on market forces combined with

regulations does lead to bubbles, as was the case in the United States in the 1990s, after the U.S. government dissolved

the AT&T monopoly and established regulation that unbundled the local loop and opened up existing fixed lines to

competition. This move certainly benefited consumers, but the resulting proliferation of competitive carriers contributed to

the telecom bubble that famously popped in 2001. Many small- and mid-size service providers, not to mention their

suppliers, went out of business. Network overcapacity built during the boom years depressed the whole supply chain for

nearly a decade. The U.S. government allowed for consolidation in the industry, reestablishing AT&T as a nationwide

service provider. AT&T now competes with cable operators in offering phone, Internet, and even TV services.

Maintaining a balance between regulation and free market policy to ensure continuity in infrastructure upgrades and

allow for enough competition in the market is a challenge for both western and Chinese governments. The current

economic crisis showed that policies of Chinese government are certainly more efficient in stimulating large

infrastructure deployments during downturns, as illustrated in Figure 2. Despite economic stimulus packages offered by

the U.S. and European governments, capital expenditures of major services providers located in these regions declined

significantly in 2009. Investments made in China increased sharply in 2009 to mitigate impact of the global economic

slowdown.

China Mobile

13 mill ion

China Unicom

,

44 million

China Teleco

m,

58 mill ion

Broadband subscribersBroadband subscribers

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

8

Figure 2: Trends in Capital Expenditures of Major Service Providers by Region

Notes: The data accounts for capital expenditures of the following companies: in China: China Mobile, China Unicom,

and China Telecom; in the United States: AT&T and Verizon; and in Europe: Deutsche Telecom, Telefonica, and

Vodafone.

Continuing Infrastructure Upgrades

As network build-outs in China account for an increasingly larger share of the global optical communication market, the

question on everybody’s mind is how long will the Chinese government remain committed to spending on networking

infrastructure?

Anyone who visited China during the last decade would agree that years of steady economic expansion have made a

huge impact on the country. The impact can be readily observed in infrastructure systems, including roads, airports,

housing, and communication systems. In fact, many of the infrastructure build-outs are closely related: massive

deployment of FTTx access networks is largely driven by the housing construction boom, and network cables are often

deployed next to railroads and highways. China’s integrated approach to the infrastructure upgrades is a huge factor in

simplifying logistics and reducing cost. Tight government control of the process eliminates a lot of barriers, such as right -

of-way, encountered by service providers in the western world.

Despite enormous progress in economic development, celebrated by hosting the 2008 Olympic Games and 2010 World

Trade Expo, a lot more needs to be done to elevate standard of living in China to a level comparable to most western

countries. For example, the housing boom has had little impact on the standard of living so far, as new housing prices

remain out of reach for majority of the Chinese people. Programs on improving housing for lower income families and

migrant workers are just starting, and it is very likely that deployments of broadband access, including FTTH, will be part

of these programs. Upgrades to communications infrastructure impacted almost everyone in China, as the number of cell

phone users reached 61% of the population by September 2010. China is also ranked number one in terms of the total

broadband subscribers, which reached 115 million in June 2010. However, the broadband penetration rate in China is

only 6%, compared to 20–30% in developed countries.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

9

Continuing investments in networking infrastructure remain on the top of Chinese government agenda. The government

budgeted almost $60 billion for the deployment of wireless systems in 2011–2012 and $22 billion for new fiber optic

networks in 2011–2013. While the total capex allocated for 2011-2013 is almost equal to investments made in 2010,

larger fraction of capex is allocated for the latest generations of wireless and broadband access systems.

It is hard to predict the timing and rate of slowdowns in networking infrastructure deployments in China, but a slowdown

is inevitable. As the national network system becomes mature, large-scale deployment projects will be replaced with

incremental upgrades, reducing long-term business opportunities for networking equipment vendors within China.

However, progress made by China sets an example for a number of emerging economies that are likely to increase

investments in networking infrastructure as their economies develop. Recognizing this trend, Chinese equipment

manufacturers, lead by Huawei, increasing focus on these developing economies that are prime for growth.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

10

Section 2: The Rise of Chinese Communications Equipment Vendors

Initially China’s telecom networks were built with equipment from international vendors including Alcatel, Lucent, Cisco,

Ericson, Nortel, and Siemens. Foreign investment by equipment vendors was permitted in China, subject to a

requirement for technology transfer. Today, Chinese domestic equipment vendors have come to dominate not only the

Chinese domestic market but the global market.

Huawei Becomes the Dominant Global Telecom Equipment Vendor

Huawei is certainly one of the great success stories in the telecom equipment market. Over the course of a decade, the

company grew from virtually nothing into a dominant supplier with revenues of $21.8 billion in 2009. Huawei is very likely

to reach the number-one position in 2010, as the company’s business continues to grow, while Alcatel-Lucent’s and

Ericsson’s sales are expected to decline in 2010, as shown in Figure 3.

Figure 3: Revenues of Leading Suppliers of Networking Equipment

Notes: 2010 Revenues are estimated on H1 2010 sales and guidance for the rest of the year offered by the vendors.

Growth of Huawei business has been phenomenal: revenue grew by 19% from 2008 to 2009, after growing by 46% from

2007 to 2008. Revenue for its optical business grew even stronger, with 30% growth in 2009 over 2008. Huawei

attributes this to growth in its traditional markets (Asia and emerging markets) as well as growth due to expansion into

Japan, Korea, and North America (where it is capturing LH DWDM and FTTX business at a few smaller carriers and

recently completed testing of 10G GPON with Verizon). Profit levels are strong, with $2.7 billion in reported profit in

2009.

Initially, Huawei was perceived as a low-quality supplier. It had what many considered a captive market in China, and it

competed mainly on price to win contracts in emerging markets. Starting in 2000, Huawei entered the market in Europe,

and it has developed as a strong competitor, especially in Eastern Europe. These days, Huawei is a global powerhouse

with plenty of glowing testimonials from carriers around the world on the performance of its products. In fact, with the

dispersal of Nortel’s assets, the struggling merger at Alcatel-Lucent, and the disarray at Nokia Siemens Networks,

Huawei is looking like the most financially stable equipment supplier in the market.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

11

As one of the largest telecom equipment suppliers (second only to Ericsson at the moment), Huawei has developed a

broad product line that includes mobile infrastructure, fixed broadband access, IP routing, optical transport segments,

and terminal products. The company is strongest in mobile infrastructure and has used wins in that product area to

enhance its penetration in other product areas. After trying, but failing, to penetrate the North American market through

acquisition (3COM, Nortel’s MEN unit), Huawei seems to be using wireless wins in North America to build its presence in

the only remaining geographic market where it is not a major player. Huawei has contracts with Bell Canada and Telus

for 3G/4G infrastructure, and in 2009, Huawei won contracts with Cox Communications for 3G infrastructure and

Clearwire for WiMAX infrastructure. To further its presence in North America, Huawei recently opened an LTE

development lab in Texas to support North American operations and its first Canadian R&D Center in Ottawa.

Huawei was a leading contender for a contract to expand the wireless broadband network of Sprint Nextel, the third

largest mobile operator in the US. With US politicians lobbying against the deal over national security concerns, Huawei

hired a US consultancy called Amerilink to help overcome these concerns. Amerilink is chaired by the former vice-

chairman of the Joint Chiefs of Staff, William Owens. James Wolfensohn, the former World Bank directors and champion

of globalization joined Amerelink as a director, as well as democrat Richard Gephardt, former House majority leader.

Despite all these efforts, Sprint eliminated Huawei and ZTE from consideration in response to security concerns. This is

a major blow to Huawei’s plans to grow in the North American market. However, Huawei has grown its US-based staff,

and opened new facilities here and can be expected to continue to pursue large deployments with major carriers in North

America. It is only a matter of time before the economic benefits of letting Huawei to compete in the US win over the

politics of keeping Huawei out.

ZTE, Already Strong in Emerging Markets, Plans to Expand into North America and Western Europe

Zhongxing Telecommunications Equipment (ZTE) is publicly traded on the Shenzhen and Hong Kong stock exchanges.

While it is best known for wireless handsets and wireless infrastructure equipment, the company is ranked third in global

market share for optical networking equipment. In 2009, ZTE’s revenue was $8,820.7 million, an astounding 36.08%

increase in revenue over 2008 as a result of strong performance in China and emerging markets, the major markets for

ZTE. Its current market presence in Western Europe, North America and Latin America is small. However, ZTE is

targeting Tier 2/3 carriers to expand its presence in Europe and North America, particularly in wireless. ZTE says the

global financial crisis appeared to be easing in Q1 2010, presenting more opportunities for the company, especially as

some equipment manufacturers left the market. In Q1 2010, ZTE saw only 0.9% growth in carrier networks products

when compared to Q1 2009. In contrast, terminal revenue (wireless handsets) and growth in software, services, and

other products (including enterprise network products) was over 40%. ZTE revenues increased by 10% in Q2 2010,

compared to the same quarter a year ago and the company expects to reach $9.6 billion in total sales for 2010, as

illustrated in Figure 4.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

12

Figure 4: Growth in ZTE Revenues

Just over half of ZTE’s revenue (50.49%) is generated in its home market, the People’s Republic of China, where it trails

Huawei in market share. An additional 21.9% comes from other markets in Asia, while Africa represents 11.4%, and

other regions (North America and Europe) represent 16.3%.

The company has 15 R&D centers globally, including 9 in China and 3 in the United States (in Texas, New Jersey, and

California). ZTE’s North American subsidiary, ZTE USA, has its U.S. headquarters in Richardson, Texas. In 2009, ZTE

established a new long-term evolution (LTE) test laboratory in Richardson to support its wireless solutions with U.S.

carriers. Although ZTE was not included in the first round of LTE equipment selections by U.S. Tier 1 carriers, it expects

to win some LTE business with Tier 2/3 carriers in the Americas. It has a current CDMA/LTE trial with Commnet Wireless

in Arizona, New Mexico, and Utah.

ZTE’s optical equipment is used for backbone and metro networks in China, India, Brazil, Pakistan, Thailand, Romania,

and Portugal. ZTE’s optical products include ULH WDM platforms, like the ZXWM M920 WDM backbone platform and

ZXWM M900 ROADM. These platforms can support up to 96 x 40G channel capacity (or 192 x 10G channels). It also

includes metro optical platforms like the ZXMP M800 (40 x 10G) metro ROADM platform and the ZXMP M600 metro

CWDM platform, multiservice aggregation platforms, like the ZXMP S385/ S380/S330, and access interface platforms

like the ZXMP S385. ZTE introduced the ZXMP M820/M720 packet optical platforms in 2009. These two platforms

provide ROADM, photonic switching, and L2 switching. The ZXMP M820 targets the metro core, and the ZXMP M720

targets metro access and aggregation. All of ZTE’s optical platforms are optimized for SDH standards, which presents a

particular barrier to North American deployment.

ZTE’s 40G optical technology was put into commercial operation by China Telecom and China Unicom in 2009. The 40G

technology operates on current WDM platforms and uses ODB, P-DPSK, or RZ-DQPSK modulation, depending on the

application. In March 2010, ZTE announced that its ZXWM M920 would be used for construction of a 40G long-haul

optical backbone at Optimus, in Portugal.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

13

Fiberhome, a full-line equipment supplier, is growing

FiberHome is the third largest domestic telecommunications carrier equipment vendor in China. The FiberHome Group is

an integrated supplier of communications technology including fiber optic, data networking, and wireless technology. It is

a state supported entity established from work initially undertaken at the Wuhan Research Institute (WRI). WRI was

formed by the Chinese Post and Telecommunications ministry in 1974 and comes under the control of the state-owned

Assets Supervision and Administration Commission of the State Council (SASAC). Mr. Tong Guo Hua is the president

and CEO of both the FiberHome Group and the Wuhan Research Institute of Post and Telecommunications (WRI)

demonstrating the close relationship between these two entities. FiberHome is headquartered in the city of Wuhan, in the

Hongshan District, China’s Optical Valley.

Although China is its primary market, FiberHome products have been exported to countries in Asia, Europe, Africa,

America, and Australia. FiberHome optoelectronic devices are purchased in the United States, Japan, and the European

Union. Its communications systems customers are largely in Asia, Africa, and Latin America, while its optical cable

products have been deployed in Southeast Asia, the Middle East, South Asia, Russia, and Africa. China Mobile is a key

customer of FiberHome, especially for 40Gbps optical transport platforms, PON, mobile backhaul, and 3G wireless

infrastructure.

In June of this year, China Mobile announced the selection of Huawei and FiberHome as its GPON suppliers. As a

result, FiberHome will get 20% of China Mobile’s significant GPON business. FiberHome is already China’s third largest

supplier of PON technology with EPON sales in China, Malaysia, Russia, and Thailand. In July 2010, China Mobile

announced FiberHome would receive 5% of its fourth phase TD-SCDMA (3G) network deployment.

Products available from FiberHome include STM, 16/64/256 ROADM/DWDM optical platforms, Access Equipment

(MSAN, DSLAM, PONs), carrier Ethernet switches and routers, soft switches and media gateways, optical fibers,

optoelectronic components, and 3G mobile communication system technology from Datang Mobile. TD-LTE technology

(4G wireless) is under internal development and FiberHome has announced TD-LTE will be launched 2010.

The FiberHome Group has nearly 10,000 employees, and 38% of them are involved in R&D. The FiberHome group is

comprised of a network of affiliate companies in the form of wholly owned subsidiaries, publicly listed companies, and

joint ventures:

FiberHome Telecommunication Technologies Co., Ltd.

FiberHome Telecommunications Technologies was founded in 1999 as a subsidiary of FiberHome/WRI. It sells transport

systems, intelligent optical switching systems, application servers, media servers, Internet protocol (IP) phone, fiber-optic

cables, electrical wires, and other data network products. The company reported revenue of $687 million (USD) (4,688.4

million CNY) in 2009. In the first half of 2010, FiberHome Telecommunication Technologies received 6.14 million Yuan in

government subsidies.

Wuhan FiberHome Networks Co., Ltd.

Fiberhome Networks products include routers, switches, and carrier-class Ethernet multiservice platforms. The company

was founded in 1999.

Wuhan Hongxin Communication Technologies Co., Ltd.

Wuhan Hongxin Communication Technologies is a subsidiary of WRI/FiberHome. It has 3,600 employees producing RF

repeaters and indoor coverage equipment for communications markets.

Beijing Northern FiberHome Technologies Co., Ltd

Beijing Northern FIberHome Technologies was founded in 2001 to perform R&D on wireless technology. Today, it is the

focus for TD-LTE technology development within FiberHome.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

14

Wuhan FiberHome Mobile Communication Inc.

Wuhan FiberHome Mobile Communication was established in 2005 as a joint venture with NEC to develop products and

services to support the TD-SCDMA market in China. FiberHome has a 65% share of the company; 30% is controlled by

NEC and NEC Telecom China (the remaining 5% is owned by other investors).

Accelink Technologies Inc.

Accelink is a subsidiary of WRI/FiberHome and a passive optical component supplier. A detailed profile of this company

is included in Section 5.

Wuhan Telecommunication Devices Co., Ltd.

WTD produces 850/1310/1550-nm optoelectonic devices such as laser diodes, LEDs, and transmitter/receivers. It was

formed as a joint venture between WRI/FIberHome and Corning Lasertron in 1980. A detailed profile of this company is

included in Section 5.

Wuhan FiberHome International Technologies Co., Ltd.

FiberHome International is the FiberHome Group entity for international sales. FiberHome International has sales and

service centers in Asia, Europe, Africa, North America, and Oceania.

Nanjing Fiberhome Fujikura Optical Communication Ltd.

This subsidiary was founded in Nanking in 1995 as a joint venture with Fujikura to produce fiber and cable.

Alcatel Lucent Shanghai Bell was the first foreign invested company in China’s telecom market

Alcatel Lucent Shanghai Bell (ASB) is the Chinese subsidiary of Alcatel Lucent. The company offers fixed-line, mobile

networking (it has a partnership with Datang Group (Datang Mobile) for TD-SCDMA wireless technology), broadband

access, and optical networking products. It is one of Alcatel Lucent’s global centers for R&D, accounting for about 30%

of Alcatel Lucent’s R&D investment. A wholly owned subsidiary, Alcatel Lucent Shanghai Bell Enterprise

Communications Company (called Shanghai Bell Alcatel Business Systems Company Ltd. before 2009) provides IP

networking solutions to enterprise and government customers.

Alcatel has a controlling interest in ASB, since it holds 50% of the shares of the company plus one share. The remainder

of the company is owned by Chinese government entities. Alcatel Lucent Shanghai Bell was formerly known as Alcatel

Shanghai Bell until January 2009, when the company changed its name and logo to reflect the 2006 merger of Alcatel

and Lucent. In conjunction with this change, the company changed the local Chinese version of its name to Shanghai

Bell. Alcatel Shanghai Bell was formed in 2002 by consolidating Alcatel’s operations in China (Alcatel China, Shanghai

Bell Alcatel Mobile Communications, and Shanghai Bell) in a partnership with the Chinese Ministry of Posts and

Telecommunications (MPT). Alcatel has had an ownership interest in Shanghai Bell since 1984, when that entity was

founded as a joint venture between China, the Belgian Fund for Development, and Alcatel.

ASB’s head office is in the Jinqiao Pudong district of Shanghai and consists of 142,000 square meters (1,528,475

square feet) of space, of which 24,000 square meters (258,000 square feet) is manufacturing space. The company has

over 15,000 employees. In 2009, Alcatel Lucent pulled most of its outsourced manufacturing from Celestica, Flextronics,

and Sanmina and moved the work to the ASB facility.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

15

ASB accounts for about 15% of Alcatel Lucent’s total revenue. Some examples of recent contracts:

In November 2010, Alcatel Lucent announced agreements worth a total €1.18 billion with China Mobile, China

Telecom, and China Unicom.

In August 2010, Alcatel Lucent announced China Telecom would use its equipment for a capacity and coverage

upgrade to the CDMA (3G) network in 56 cities.

In July 2010, ASB was able to arrange a loan from a Chinese bank to TOT, the state-owned carrier in Thailand,

to purchase 19 billion baht ($640 million USD) in equipment and services from ASB for its 3G network.

In July 2009, Alcatel Lucent announced its selection by China Mobile as the sole supplier for a FTTH

deployment in ten cities using the 7342 ISAM FTTU GPON platform.

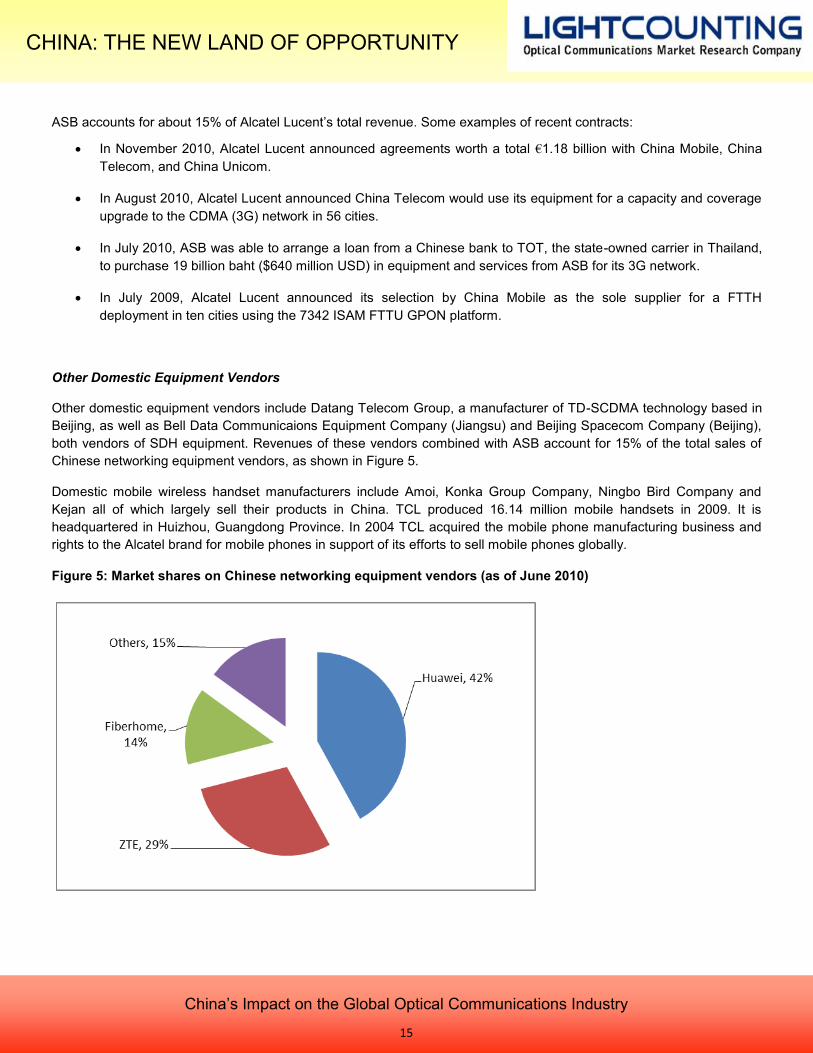

Other Domestic Equipment Vendors

Other domestic equipment vendors include Datang Telecom Group, a manufacturer of TD-SCDMA technology based in

Beijing, as well as Bell Data Communicaions Equipment Company (Jiangsu) and Beijing Spacecom Company (Beijing),

both vendors of SDH equipment. Revenues of these vendors combined with ASB account for 15% of the total sales of

Chinese networking equipment vendors, as shown in Figure 5.

Domestic mobile wireless handset manufacturers include Amoi, Konka Group Company, Ningbo Bird Company and

Kejan all of which largely sell their products in China. TCL produced 16.14 million mobile handsets in 2009. It is

headquartered in Huizhou, Guangdong Province. In 2004 TCL acquired the mobile phone manufacturing business and

rights to the Alcatel brand for mobile phones in support of its efforts to sell mobile phones globally.

Figure 5: Market shares on Chinese networking equipment vendors (as of June 2010)

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

16

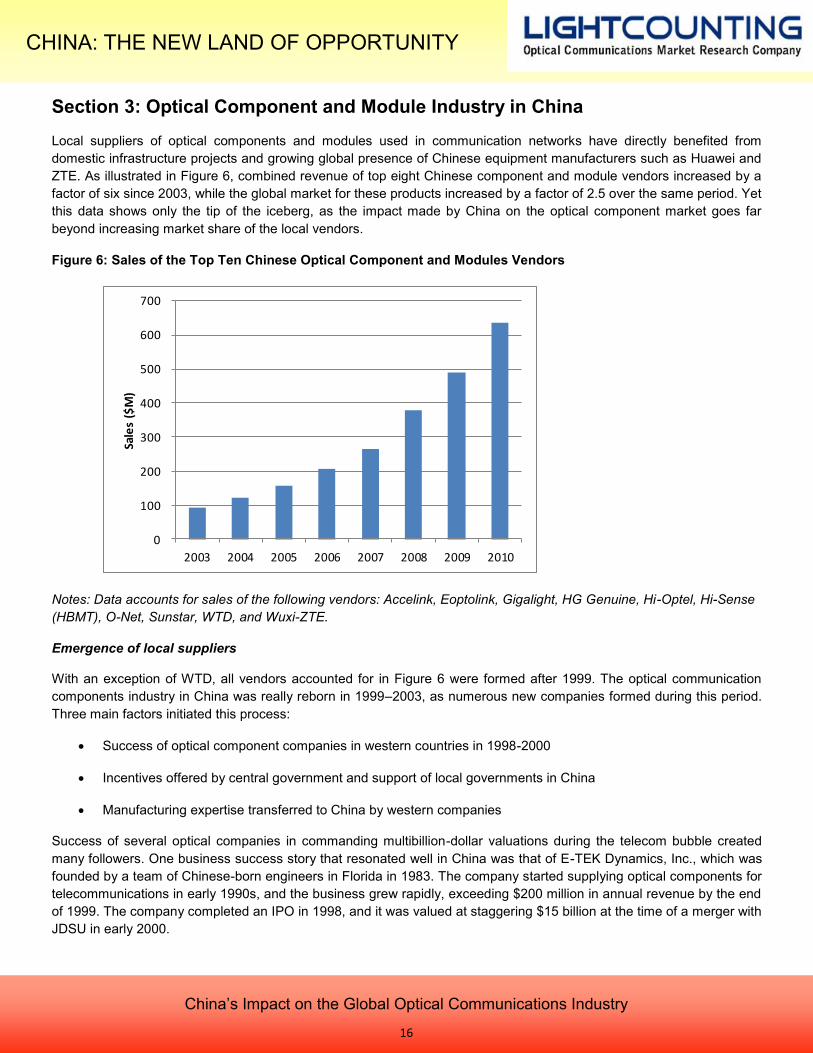

Section 3: Optical Component and Module Industry in China

Local suppliers of optical components and modules used in communication networks have directly benefited from

domestic infrastructure projects and growing global presence of Chinese equipment manufacturers such as Huawei and

ZTE. As illustrated in Figure 6, combined revenue of top eight Chinese component and module vendors increased by a

factor of six since 2003, while the global market for these products increased by a factor of 2.5 over the same period. Yet

this data shows only the tip of the iceberg, as the impact made by China on the optical component market goes far

beyond increasing market share of the local vendors.

Figure 6: Sales of the Top Ten Chinese Optical Component and Modules Vendors

Notes: Data accounts for sales of the following vendors: Accelink, Eoptolink, Gigalight, HG Genuine, Hi-Optel, Hi-Sense

(HBMT), O-Net, Sunstar, WTD, and Wuxi-ZTE.

Emergence of local suppliers

With an exception of WTD, all vendors accounted for in Figure 6 were formed after 1999. The optical communication

components industry in China was really reborn in 1999–2003, as numerous new companies formed during this period.

Three main factors initiated this process:

Success of optical component companies in western countries in 1998-2000

Incentives offered by central government and support of local governments in China

Manufacturing expertise transferred to China by western companies

Success of several optical companies in commanding multibillion-dollar valuations during the telecom bubble created

many followers. One business success story that resonated well in China was that of E-TEK Dynamics, Inc., which was

founded by a team of Chinese-born engineers in Florida in 1983. The company started supplying optical components for

telecommunications in early 1990s, and the business grew rapidly, exceeding $200 million in annual revenue by the end

of 1999. The company completed an IPO in 1998, and it was valued at staggering $15 billion at the time of a merger with

JDSU in early 2000.

0

100

200

300

400

500

600

700

2003 2004 2005 2006 2007 2008 2009 2010

Sale

s ($

M)

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

17

U.S. venture capitalists poured $150 billion into the industry 1999–2000 to fund high-tech start-ups, and many of these

focused on optical communications. However, the funding fell sharply as the market crashed in 2001 and many start-up

companies in the United States folded soon after the crash.

In contrast to the U.S. venture capitalists, Chinese government had a much more long-term outlook for the industry and

continued to offer numerous incentives for high-tech start-ups even after the market crash of 2001. Central and local

governments in China offered tax incentives, land, and loans and even built factories for high-tech start-ups. Supported

by the government policies, start-up companies continued to form in China in 2001–2003, despite a rapidly deteriorating

market.

Three main areas within China emerged as centers of optical communications: Shenzhen, Wuhan and Chengdu.

Shenzhen was set up as an open economic zone in 1980s and has developed rapidly since then, becoming a major

industrial center. Huawei and ZTE are headquartered in Shenzhen, and it remains a prime location for many of their

suppliers. ATOP, Gigalight, Hi-Optel, and O-Net are also based in Shenzhen.

Wuhan is the center of Hubei province, and it is home to Accelink, HG Genuine, and WTD, as well as FiberHome—the

third largest networking equipment vendor in China. Wuhan has a long history in the telecommunications industry, since

Wuhan Research Institute (WRI), established in 1974, remains the main center of excellence in China. WTD was

established in 1970 as a joint venture between WRI and Corning and is known as the first Chinese joint venture with a

United States–based company. Local government offers continuing support to vendors focused on optical

communications, as they offer employment to many people living in Hubei province.

Chengdu, in Sichuan Province, is home to Fiberxon, which was acquired by MRV communication in 2007, and it is part

of privately held Source Photonics now. Several other optical component and module suppliers are based in Chengdu

including Sunstar, Eoptolink, Solorein, Neton, and Superxon. Also fiber and cable manufacturers, such as Futong Group

and Hengtong Group have chosen Chengdu as a production base.

Companies based in Chengu and Wuhan also take advantage of a more stable work force, since most migrant workers

come from local towns, and they tend to be more committed to local employers. In contrast, Shenzhen-based companies

employ migrant workers that come from all over the country, so these people are more likely to look for other

opportunities located closer to their hometowns. Costs of running business tend to be lower in central provinces,

compared to major coastal areas, so increasing number of suppliers move production there.

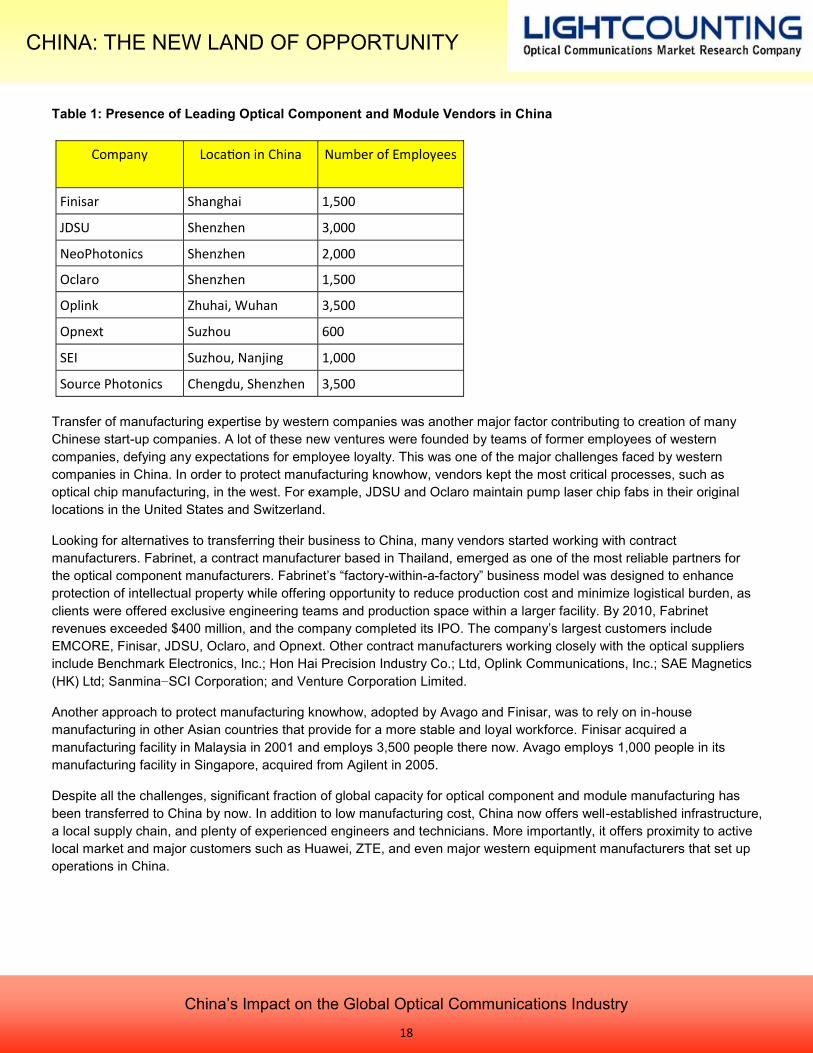

Western companies move production to China

Low manufacturing cost in China was originally the main attraction for many western companies that were struggling to

reduce cost during industry downturn of 2001–2003. All leading optical component and modules vendors started moving

production to China during this period by working with contract manufacturers, establishing partnerships with local

businesses or directly moving their production lines from the west. By now, all these vendors maintain significant portion

of their production lines and even R&D centers in China, as summarized in Table 1.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

18

Table 1: Presence of Leading Optical Component and Module Vendors in China

Transfer of manufacturing expertise by western companies was another major factor contributing to creation of many

Chinese start-up companies. A lot of these new ventures were founded by teams of former employees of western

companies, defying any expectations for employee loyalty. This was one of the major challenges faced by western

companies in China. In order to protect manufacturing knowhow, vendors kept the most critical processes, such as

optical chip manufacturing, in the west. For example, JDSU and Oclaro maintain pump laser chip fabs in their original

locations in the United States and Switzerland.

Looking for alternatives to transferring their business to China, many vendors started working with contract

manufacturers. Fabrinet, a contract manufacturer based in Thailand, emerged as one of the most reliable partners for

the optical component manufacturers. Fabrinet’s ―factory-within-a-factory‖ business model was designed to enhance

protection of intellectual property while offering opportunity to reduce production cost and minimize logistical burden, as

clients were offered exclusive engineering teams and production space within a larger facility. By 2010, Fabrinet

revenues exceeded $400 million, and the company completed its IPO. The company’s largest customers include

EMCORE, Finisar, JDSU, Oclaro, and Opnext. Other contract manufacturers working closely with the optical suppliers

include Benchmark Electronics, Inc.; Hon Hai Precision Industry Co.; Ltd, Oplink Communications, Inc.; SAE Magnetics

(HK) Ltd; Sanmina−SCI Corporation; and Venture Corporation Limited.

Another approach to protect manufacturing knowhow, adopted by Avago and Finisar, was to rely on in-house

manufacturing in other Asian countries that provide for a more stable and loyal workforce. Finisar acquired a

manufacturing facility in Malaysia in 2001 and employs 3,500 people there now. Avago employs 1,000 people in its

manufacturing facility in Singapore, acquired from Agilent in 2005.

Despite all the challenges, significant fraction of global capacity for optical component and module manufacturing has

been transferred to China by now. In addition to low manufacturing cost, China now offers well-established infrastructure,

a local supply chain, and plenty of experienced engineers and technicians. More importantly, it offers proximity to active

local market and major customers such as Huawei, ZTE, and even major western equipment manufacturers that set up

operations in China.

Company Location in China Number of Employees

Finisar Shanghai 1,500

JDSU Shenzhen 3,000

NeoPhotonics Shenzhen 2,000

Oclaro Shenzhen 1,500

Oplink Zhuhai, Wuhan 3,500

Opnext Suzhou 600

SEI Suzhou, Nanjing 1,000

Source Photonics Chengdu, Shenzhen 3,500

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

19

Section 4: Challenges and Opportunities Ahead

After three decades of economic expansion, China’s economy is now the second largest in the world. The China gross

domestic product (GDP) is worth $4,909 billion, or 7.9% of the world economy, according to the World Bank. China's

annual GDP growth averaged 9.3% over 1989–2010. The growth rate fluctuated in the past, reaching a historical high of

14.20% in December of 1992 and a record low of 3.80% in December of 1990, but it has been fairly steady over the last

decade. Maintaining steady growth rate of the economy is one of the highest priorities of the Chinese government, since

it is the key factor for ensuring political stability as well.

Whether such a high growth rate is sustainable and for how long are questions addressed by numerous economic

studies, which all point out that there is no single example in the history of a country undergoing such a rapid economic

expansion without a major crisis. Among the most recent challenges faced by the Chinese government is the widely

publicized policy for currency exchange rates. Many western governments, including the United States, argue that

Chinese currency is undervalued to boost the competitiveness of Chinese exports. Demands for currency appreciation

are faced with strong resistance of the Chinese government. The Chinese economy depends very strongly on exports,

despite increases in domestic consumption. Transition from an export-based economy to the one driven by domestic

consumption is another challenge for the country, but it is also a significant objective of the ruling communist party, as

increased domestic consumption means an improved standard of living for the people.

Costs of manufacturing in China will inevitably increase over time as standards of living improve. The government will

certainly make every effort to ensure that this increase is gradual to avoid any abrupt changes in the economic system.

Controlling increase in manufacturing costs will also give extra time to local businesses to build global customer bases

and become more competitive in terms of technology and innovation.

China certainly has a potential to become the global leader in innovation. The country invests heavily in research and

education. About 5 million students graduate from colleges in China every year. The number of graduate students

exceeds 1.3 million now, and it is increasing rapidly. The government offers generous funding to leading research

institutes, which attract many Chinese-born professors who previously worked in western countries. One of the

challenges in putting all these resources to work is establishing an economic environment that encourages and rewards

talent and innovation. Some of this system is in place already, but many high-tech companies remain under government

control, and financial markets are just starting to open up to businesses owned by private entrepreneurs.

The Shenzhen stock exchange was set up a few years ago as a gateway to financial markets for medium-sized

companies owned by private entrepreneurs, as opposed to the state-owned behemoths that typically gravitate to

Shanghai. In the first nine months of 2010, the Shenzhen stock exchange has seen 246 companies raise a record $33.6

billion by new listings, triple last year’s total and much more than the $24.1 billion raised in Shanghai. ChiNext, a

specialized exchange for start-up companies launched in Shenzhen last year, helped 91 companies to raise $11 billion

in the first nine months of 2010. While these numbers are dwarfed by almost $1 trillion in new loans issued by Chinese

banks over the same period, the IPO bonanza represents an important step in the evolution of China’s financial markets.

Let us all hope that this country can learn on mistakes of others and avoid financial bubbles as much as possible.

Service provider business and infrastructure projects

The countries leading service providers will be direct beneficiaries of increasing standards of living in China. Operating in

the most populated country in world, where residents are likely to spend more on services as their expandable incomes

increase, offers great opportunities. However, tight government control makes these businesses less attractive for

investors. Encouraging competition among service providers to the benefits of consumers is certainly on the

government’s agenda, but it is hard to picture a truly free market environment for services in China. Scale is very critical

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

20

for a successful service provider business, and scale often comes with a degree of monopolistic power. Combining

elements of monopoly with a tight government control does not leave much hope for competition.

Infrastructure upgrade projects will continue to be high on the government’s agenda. Providing high-speed access

networks to the majority of the population is part of the plan to improve standards of living. It also offers another avenue

for champion projects: the world fastest optical network would fit well next to the faster train. As the fastest trains travel at

400 km/hour, 400 Gbps looks like the right number for the datarate of the optical network. China leads on installations of

40 Gbps networks today, while many western service providers rely on 10 Gbps now and evaluate 100 Gbps for future

deployments, largely skipping 40 Gbps technology. Would China choose to skip 100 Gbps and move directly to 400

Gbps?

It is possible that high-visibility projects like building the fastest 40 to 100 Gbps or even 400 Gbps core networks will

lead to excess capacity, similar to the post-telecom-bubble situation in the United States. It is also likely that the resulting

network system will have bottlenecks. For example, interconnecting high-speed access and high-capacity core networks

will require investment in local networking infrastructure, which may lag behind the high visibility projects lead by the

central government.

Recent report published by a think tank closely associated with Chinese Academy of Sciences raised concerns on

whether investments in the high speed trains will ever pay off and if the capacity of new train lines will be utilized

effectively. It also questioned if the rest of the transportation system, including airports and roads, will be integrated

efficiently with the new train network. Chinese government is reviewing plans for the high speed train deployments now,

addressing these concerns. Ensuring effectiveness of the communication network may present even more complex task

for the government.

Networking equipment manufacturers

Huawei reached the number-one position in optical networking two years ago, displacing Alcatel-Lucent, and it is likely to

surpass Ericsson as the largest supplier of wireline and wireless equipment this year. Despite the phenomenal growth in

Huawei’s business, there are certainly limits to how dominant any company can become. Mature markets are usually

dominated by three major players, creating a stable environment where coalition of two out of the three is strong enough

to block any predatory intentions that the third might have. This situation suggests that ZTE and Fiberhome are likely to

gain share in the domestic market, and Alcatel-Lucent and Ericsson should be able to limit Huawei’s dominance globally.

There are examples when a single company can reach a clearly dominating position often due to an improved business

model or innovative technology, such as Google now or IBM in the past, but this dominance does not last forever. Big

companies are not protected from competitive market forces, changing business environment, and continuing advances

in technology.

What is the secret of Huawei success? The company followed an approach tested by many other manufacturers in

China: entering the market with low-end products and moving up by learning business and technology from western

competitors. The timing was also perfect, as major competitors were in disarray after the telecom bubble burst in 2001.

Steadily growing demand for networking gear in China was another factor in Huawei’s success. Aggressive entry into

developing countries, where many installations were funded by Chinese banks, added global expertise. Finally, network

operators in the developed countries, struggling to increase network capacity at the lowest cost, could not resist buying

products from Huawei either.

Can Huawei maintain its dominance? Continuing reductions in product cost while maintaining technological

competitiveness is certainly the winning strategy. As the gap in labor cost between China and the rest of the world

shrinks, more emphasis will have to be placed on operational efficiency. Huawei has been known for bringing a lot of

manufacturing processes in house to further reduce cost, and this approach is likely to continue. Increasing operations

around the world to support a growing list of customers will certainly impact the cost structure as well. One of the most

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

21

challenging aspects of maintaining the leadership will be to develop new technology using internal R&D, which is very

different from adopting technologies developed in the west. Opening up to the world by becoming a publicly traded

company is another transition that Huawei will have to make.

The competition in technology is heating up with Alcatel-Lucent, Ciena, Cisco, and Juniper, introducing products

equipped with 100 Gbps interfaces. All these suppliers rely heavily on internal developments of this technology, which

requires complex digital signal processing (DSP). Cisco’s acquisition of CoreOptics in 2010 took out the leading external

resource for 100 Gbps DSP, putting more pressure on Huawei.

Cisco has been challenging growth of Huawei in datacom market and aggressively protecting its intellectual property.

Cisco filed a lawsuit in 2003 claiming that Huawei violated at least five of the company's patents and copied Cisco's

Internetwork Operating System source code. Cisco said Huawei used the code in the operating system for its routers

and switches and claimed that Huawei's system contained text strings, file names, and bugs identical to Cisco's source

code. The case was settled in 2004 after Huawei discontinued the sale of products at issue in the suit.

The U.S. government also played a role in trimming Huawei ambitions by blocking a merger of the company with 3COM

in 2008 on concerns related to national security. The same approach has been used to block several smaller deals in the

United States since then, but Huawei keeps trying and slowly gaining ground in the United States. Current bidding for a

large contract with Sprint may be a milestone in this process.

The Indian government blocked orders placed by Indian telecom operators with Huawei and ZTE in early 2010, citing

security concerns. The government subsequently introduced new rules that, among other things, made it mandatory for

all foreign equipment providers to make the source code and designs of their equipment available to the Indian

government for scrutiny. This order is under review by the Department of Telecommunications at the instructions of the

country's Prime Minister's office, after several equipment providers objected to the new rules. Meanwhile, Huawei is

complying with most of these requirements, and some orders from Huawei that were blocked earlier this year are likely

to be cleared soon. Huawei was recently selected as a supplier to mobile operator Tata Teleservices for 3G network

deployments in India. Huawei also announced plans to open a manufacturing facility in India, solidifying its presence in

this large and underdeveloped market.

ZTE and FiberHome are well positioned for growth, building on Huawei successes. ZTE became the third largest

supplier of optical networking in 2010. The company had good success expanding into emerging markets, but it could

use more presence in Europe and North America. FiberHome was awarded significant contracts with China Mobile in

2010. The company is also expanding globally and invests heavily in R&D.

Sales by Shanghai Bell account for only 15% of the total sales of Alcatel-Lucent, but it is becoming the manufacturing

and R&D center for the parent company, which would allow Alcatel-Lucent to compete more effectively with Huawei in

terms of product cost. Presence in China will continue to pay off in terms of growing sales in this country and neighboring

markets. It also brings the operations closer to many suppliers.

Several other equipment manufacturers opened manufacturing and R&D centers in China to take advantage of the

opportunities discussed above. Ericsson established its first sales office in Beijing in 1985. It formed Ericsson China in

1994 and now has production facilities in Beijing, Nanjing, and Chongqing. In 2002 Ericcson set up the China

Development and Research Institiute as an R&D organization for ericsson in China. Nokia China is housed in a 75,000

square meter facility in Beijing. Cisco has a large presence in China with facilities in Shanghai, Hefei, Shenzhen,

Suzhou, and Hangzhou, its market share is significantly lower in China than in other geographic markets. Cisco

established the Cisco China Research and Development Center in 2005 and it is now the 3rd

largest R&D center for

Cisco globally.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

22

Optical component and module vendors

Despite growing market share, Chinese optical component and module vendors remain smaller than western

competitors. Figure 7 shows a comparison of revenues of the two largest Chinese vendors (Accelink and WTD) with

Finisar and Opnext, two of the top five western companies. Finisar and Opnext increased their market presence by

acquisition in 2007–2008, while Accelink and WTD relied exclusively on growing internally. Both Accelink and WTD are

owned by FiberHome Group, which also owns FiberHome Telecommunications Technologies and several other

subsidiaries involved in telecommunications. This ownership structure makes subsidiaries depended on the group

interests, limiting their options for growth. Another example of such dependence is Wuxi-ZTE, which is owned by ZTE.

HiSense Broadband and HG Genuine are subsidiaries of larger companies that are not directly associated with any

companies involved in telecommunications. These businesses are likely to have higher growth potential, since they are

more independent and yet rely on financial and manufacturing resources of larger parent businesses.

Figure 7: Annual revenues of Accelink, Finisar, Opnext and WTD

Continuing dominance of the western component and module suppliers is also supported by these companies’ extensive

manufacturing facilities in China, making their manufacturing costs comparable to domestic vendors. The western

companies have also an advantage in global presence, while Chinese suppliers are mostly selling into domestic market

despite their efforts to increase global presence. Developing business relationships with major western OEM customers

requires local presence and expertise in complying with numerous qualification requirements, which is an extra expense

that not many Chinese vendors are willing to make. Since they have almost no advantage in manufacturing cost, other

expenses related to running the business remains the only differentiator.

Considering limitations of Chinese vendors in terms of global reach, acquisitions of Fiberxon by Source Photonics (part

of MRV Communications at the time) in early 2007 and Photon Technology by NeoPhotonics (a California-based startup)

in 2005–2006 made a lot of sense. As illustrated in Figure 8, revenues of these companies are growing nicely, as low-

cost manufacturing bases in China compliment solid presences in the United States and Europe. NeoPhotonics filed for

IPO in 2010, which should reward founders of Photon Technology, setting up a good example for the other vendors.

Source Photonics also filed for IPO in December 2007, but the financial crisis of 2008–2009 derailed this plan. The

company was recently sold to Francisco Partners, a private equity firm associated with Sequoia Capital, one of Silicon

Valley's most prominent venture capital firms. The company valuation of $146 million, which is well below its estimated

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

23

annual sales of $230 million in 2010, reflects limitations imposed on the company growth by the outcome of recent

litigation with Finisar over patent violations.

Figure 8: Revenues of NeoPhotonics and Source Photonics

Establishing a solid intellectual property base is another challenge for Chinese suppliers aspiring to enter the global

market. It certainly takes time to obtain patents, particularly in the United States where it could take up to three years to

get even an initial response from the patent office. Chinese vendors are just starting to build up their patent portfolios

and catching up quickly in terms of number of patents issued in China, but they are lagging behind in terms of U.S.

patents, as summarized in Table 2.

Table 2: Number of Patents Related to Transceiver Modules Owned by Western and Chinese Vendors

Another challenge faced by Chinese optical component and module vendors is technology gap that still exists. Entering

the market with low-end products, many Chinese transceiver suppliers developed expertise for making 1 to 3 Gbps

modules, but very few of them can reach higher data rates of 10 Gbps and above. Transition to 10 Gbps products was a

big step for the western suppliers ten years ago, and this technology progressed rapidly over the last decade pushed by

tough requirements imposed by powerful customers like Cisco. The Chinese suppliers stayed largely out of this race,

and they will have to catch up now.

One of the reasons for many Chinese vendors lagging behind in 10 Gbps technology is that many of them do not ship

products to the datacom market, which dominated by companies like Cisco. Like many other western customers, Cisco

has very stringent qualification processes that are out of reach for suppliers based in China. Also, the datacom market

relies heavily on VCSEL–based products, which few Chinese vendors offer. The VCSEL–based transceiver market is

dominated by Avago, EMCORE, Finisar, and JDSU, and each of these maintains internal manufacturing of VCSELs.

Western Companies Chinese Companies

Type of patents Finisar Opnext Sumitomo HG-Genuine Hi-Sense WTD

US Patents 381 109 274 0 0 9

Chinese Patents 53 0 116 10 45 96

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

24

Competing with these vendors is very difficult, as there very few other suppliers of VCSELs, but success of many

western companies is partly based on solid presence in the datacom market, which reached $994 million in 2010, as

illustrated in Figure 9. More than 80% of transceivers sold into the datacom market are VCSEL–based products.

Figure 9: Size of Telecom and Datacom Transceiver Markets

Cisco’s policy for marking up optical transceivers by at least a factor of three on sales of these products to ends users

opened up a grey market for transceiver modules, which was exploited by many smaller vendors based in China.

Manufacturing transceivers compatible with Cisco’s equipment, forging Cisco’s label and selling them directly to end

users for a fraction of Cisco’s list price remains a lucrative market for numerous small businesses in China. However,

this is not a winning strategy for any business with global aspirations.

Apart from staying away from the grey market, what are other strategies for growth available to Chinese vendors? These

are a few recommendations:

Increase investment in R&D and closing technology gap with the western competitors.

Build up intellectual property base.

Establish business relationships with major customers around the world.

Take full advantage of emerging financial market in China to fund the growth.

Most of the strategies listed above require long-term vision, but companies capable of prioritizing the necessary

investments will be the ones leading the industry in the future.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

25

Section 5: Optical Component and Module Vendor Profiles

Many new companies were formed around the world during the telecom bubble of 1999–2000, as demand for optical

components and modules skyrocketed. Most of the new enterprises formed in western countries closed down as the

market crashed, but companies formed in China have largely stayed in business. Large industrial Chinese companies,

such as HiSense and HG Tech, formed divisions focused on optical components and modules. This section offers brief

profiles of selected vendors

Accelink ( www.accelink.com )

Accelink was established in 2001. It is based in Wuhan and employs 1,900 people. Current manufacturing space

consists of 24,000 square meters, but the company is finishing construction of a new 50,000-square-meter facility. Most

of the construction is funded from $100 million raised during an IPO in Shenzhen in late 2009.

Accelink was established by Soild Device Institute (SDI), which is a subsidiary of Wuhan Research Institute of Post and

Telecommunications (WRI). FiberHome and WDT were also established by WRI, so all these companies are based in

Wuhan and closely related by operating in complimentary market segments.

Accelink specializes in the design and manufacturing of optical amplifiers and a variety of passive components used in

amplifiers. It also provides test and measurement (T&M) equipment for field installations. Close to 50% of its revenue

comes from sales of EDFAs and Raman amplifiers employed in telecom and CATV systems. Sales of passive

components and T&M products account for about 25% each.

The main customer of amplifiers used in telecom systems is ZTE, but Accelink is involved in development projects with

several other vendors in Europe, India, and North America. One of them is BTI, which formally announced a partnership

with Accelink in 2009. Huawei is the mail customer for passive components, but it does not purchase amplifiers, as these

modules are design and assembled at Huawei internally.

Main competitors for the amplifier products are JDSU, Oclaro, and Wuxi/ZTE. JDSU and Oclaro are the only two

suppliers of 980-nm pump lasers, which is an essential component in amplifiers, but they sell pump lasers to other

amplifier vendors including Accelink. Wuxi/ZTE is a significant competitor because of its close ties with ZTE, which is

Accelink’s main customer. Competition for passive components includes JDSU, Oplink, and a number of smaller

vendors.

Accelink business have grown steadily over the years, driven by increasing demand at Huawei and ZTE. Sales of high-

power EDFA amplifiers into growing CATV business also contributed to the company’s growth. While this steady growth

is likely to continue over the years, Accelink is counting on generating more business with new customers worldwide.

Moving into new facilities by the end of 2011 and expanding work force will facilitate these plans.

Accelink enjoys access to a more stable work force in Wuhan than vendors based in Shenzhen do. Most of Accelink

employees come from towns near Wuhan, while Shenzhen-based vendors draw their work force form across China, and

people tend to be less committed to staying with their employers in Shenzhen for more than a year or two.

Data on Accelink sales is summarized in Appendix A.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

26

ATOP Technology ( www.atoptechnology.com )

The company was established in 2000 and is based in Shenzhen. It employs 60 people and has 1,000 square meters of

manufacturing space. ATOP purchased 24,000 square meters of land to build a new factory in 2010, using loans from

the government.

ATOP’s first products were passive optical components for communications, but it added optical transceivers to the

product portfolio in 2007. Company products now include bidirectional transceivers for FTTH applications, SFP modules

for Sonet, as well as Ethernet and Fibre Channel applications focusing on 1300-nm FP and DFB–based modules,

including LR (2–20 km reach) GigE, 4 G FC, and OC-48 modules. ATOP also offers 2.5 Gbps CWDM modules (40–80

km reach).

The company reports success in South Asia and has sales representation in Brazil, Poland, Romania, Sweden, the

United Kingdom, and the United States and developing business in Russia, Spain, and Ukraine.

Eoptolink Technology (www.eoptolink.com )

Eoptolink was originally founded in 2002 and it merged with Comtown Co. in 2007 to form Eoptolink Technology. It is

based in Chendu, Sichaun Province and employs 250 people. The company specializes in manufacturing of optical

transceivers for datacom, telecom and Cable TV markets.

Data on Eoptolink sales is summarized in Appendix A.

Gigalight ( www.gigalight.com.cn )

The company is based in Shenzhen and it was originally founded in 2001 as a distributor of Finisar transceivers in

China. It started manufacturing their own transceivers in 2003 and it was re-established as Shenzhen GigaLight

Technology in 2004. The company specializes in optical transceiver manufacturing, including 10 Gbps products. It

recently obtained $1.3 million credit to expand operations.

Data on Gigalight sales is summarized in Appendix A.

HG Genuine ( www.genuine-opto.com )

HG Genuine is based in Wuhan and employs 1,300 people. The company was established in 2001 as a subsidiary of

HG Tech, which is a supplier of industrial lasers, laser processing equipment, and electronic components. HG Genuine

facilities encompass 12,000 square meters of manufacturing space, including 4,000 square meters of clean rooms.

The company is emerging as one of the major Chinese suppliers of transceivers because of rapidly growing business

with Huawei and ZTE. The company maintains in-house manufacturing of laser chips, TOSAs, ROSAs, and transceiver

modules. Its main products include GigE and OC-48 SFP transceivers, and the company is ramping production of 6 G

SFP+ transceivers for the wireless market and GPON/EPON modules for FTTx applications. A lot of HG Genuine’s

products are custom made for Huawei.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

27

The Chinese domestic market accounted for 80% of sales in 2009, but the company continues to grow business outside

of China as well. It started supplying products to Alcatel-Lucent and Cisco in 2007 and Ericson and NSN in 2009. Among

other customers are Fiberhome and Tejas Networks.

Main competitors include Hi-Sense, Source Phonics, and WTD. As the company develops 10 Gbps products in 2011–

2012, it will start competing with a broader set of suppliers.

Among the main advantages of HG Genuine are very well equipped, vertically integrated production lines. Close

relationships with Huawei and ZTE provide for a steadily growing demand.

Among the main challenges are expanding production lines to higher-data-rate lasers and modules. Keeping up with the

rapid growth in production capacity will require impeccable execution on the management side.

Data on GHG Genuine sales is summarized in Appendix A.

Hi-Optel ( www.hioptel.com )

Hi-Optel was established in 1999 and is based in Shenzhen. It employs more than 500 people and maintains a 10,000-

square-meter facility. Transceivers and related products account for 90% of sales, with 55% of the total revenue coming

from sales outside of China.

Data on Hi-Optel sales is summarized in Appendix A.

HiSense Broadband ( www.hisense.com/en/pds/telco/opco/ )

The company was established in 2002 as a subsidiary of HiSense, one of the leading electronics and home appliance

manufacturers in China, with 60,000 employees and more than $8 billion in revenues. HiSense was originally

established in 1969, when it was known as #2 Radio Factory. The company expanded rapidly during the last two

decades, as it entered refrigerator and air conditioner businesses— the two product lines the company is known for now.

The HiSense Broadband business unit employs 550 people and accounted for less than 1% of the total revenue of the

parent company in 2009. The company is based in Qingdao, China on the old campus that was housing the original #2

Radio Factory.

The company specializes in the design and manufacturing of optical transceivers for FTTx applications, but it is staring to

offer transceivers for other applications as well. This business leverages on surface-mounted technology used for

assembly of other electronics product within HiSense. The parent company also invested heavily in specialized test and

measurement equipment to support transceiver business. The manufacturing lines are designed to support high-volume

business with major OEM customers, and they are well equipment to address the high quality standards required by this

type of customers.

Main competitors include Source Photonics and NeoPhotonics, which also specialize in optical transceivers for FTTx

applications. As HiSense expands product offering in the transceiver market, it will start competing with all other leading

vendors as well. Focused on high volume production, HiSense does not compete with numerous local manufacturers of

transceivers, which are focused on niche market opportunities.

CHINA: THE NEW LAND OF OPPORTUNITY

China’s Impact on the Global Optical Communications Industry

28

Main customers include Huawei and ZTE. HiSense is also doing good business with smaller equipment manufacturers

based in India and other emerging countries. The company has had no success so far in developing business with

equipment manufacturers base in western countries. Ligent Photonics, based in the United States and set up to grow

HiSense business in the United States and Europe, gives the impression of a dormant company, so it clearly had very

little success in business development so far.

HiSense Broadband is well positioned to become one of the leading suppliers of optical transceivers for applications that

require high volume and low cost. Being part of a large electronics supplier, HiSense Broadband benefits from financial

resources and manufacturing and operational expertise of the parent company.

Lack of internal manufacturing of laser and detector chips makes it more challenging for HiSense to develop and

introduce new high-end products, as there are very few suppliers of high-end laser and detector chips on the market.

Growing customer base in the western countries is another challenge for HiSense.

Data on HiSense sales is summarized in Appendix A.

Hymax Optoelectronics Inc. ( www.hymaxinc.com )

The company was established in 2006. It is based in Huailai, Hebei Province and employs 400 people. Hymax maintains

7,000 sq. meter manufacturing facilities, including clean-rooms.