Please refer to page 10 for important disclosures and analyst certification, or on our website www.macquarie.com/research/disclosures . CHINA/HONG KONG Shanghai VW’s Lavida – China’s top- selling sedan in 1H Source: China Auto Web, September 2014 GWM Haval H6 – China’s top-selling SUV in 1H Source: Macquarie Research, September 2014 Table of coverage, ratings and TPs in order of preference Name Ticker Price Rating TP TSR Great Wall 2333 HK 32.55 OP 52.00 65.3% Dongfeng 489 HK 14.36 OP 17.50 24.7% GAC 2238 HK 8.25 OP 11.50 43.9% Geely 175 HK 2.89 OP 3.80 32.9% Brilliance 1114 HK 13.80 N 15.60 14.2% BYD 1211 HK 56.00 UP 12.80 -77.0% Note: share prices are as of market close 2 Sept 2014. All prices in HK$. Source: FactSet, Macquarie Research, September 2014 Analyst(s) Janet Lewis, CFA +852 3922 5417 [email protected]Zhixuan Lin +86 21 2412 9006 [email protected]Leo Lin +852 3922 1098 [email protected]3 September 2014 Macquarie Capital Securities Limited China autos Gearing up for peak season 1H results reflect bifurcated market favouring JVs Results of the 6 Hong Kong listed Chinese auto OEMs were as bifurcated as recent market trends, with Dongfeng Motor (DFG), Brilliance China (BCA) and Guangzhou Auto (GAC) all reporting strong net profit growth in the 41-79% range, while the 3 domestic OEMs delivered YoY declines, with Great Wall (GWM) surprising with just a 3% decline in NPAT, followed by BYD down 15% and Geely’s NPAT falling 29%. Outlook is for continued strong sales in 2H In the first 7 months of 2014 auto sales are up 8.2% YTD, with passenger vehicles (PV) up 11.0% and commercial vehicles slipping -3.5% reflecting sluggish FAI, especially in the property market and as concrete incentives to encourage replacement of yellow label vehicles have failed to materialise. We have tweaked our sedan forecast from 13.2% growth to 11.1%, mainly on the back of weaker sedan and minibus sales but better MPV demand. Anti-trust investigation – great headlines but limited impact The NDRC-led anti-trust investigation of primarily premium brands like Mercedes-Benz and Jaguar Land-Rover but also Japanese parts suppliers led to nervousness among investors and hopes among consumers that luxury car prices might decline. We believe only a handful of high-priced imported cars will see price cuts; otherwise OEMs are cutting spare parts prices. As this improves the affordability of owning a car, we see it as a positive. Dealers also like the price cuts as consumers will be more likely to return to the dealer for servicing, and margins should remain unchanged. Competition is intense but manageable The international brands continue to launch more products customised for the China market as well as more lower-priced products, which has resulted in intensified pressure on domestic brand sales. OEMs like Great Wall and Geely are responding with higher-quality products, including more equipped with automatic transmission. The results of BCA and DFG would suggest that so far the OEMs are not raising incentives to dealers, who have borne the brunt of higher discounts and inventory in the face of aggressive sales growth targets from the OEMs. NEVs are years away from being meaningful to sales Efforts from various levels of government to increase the penetration have resulted in big percent gains for new energy vehicles (NEVs); sales remain just 0.2% of total PV sales despite heavy government subsidies. Many mainstream OEMs will launch pure electric and hybrid plug-ins over the next year to improve fleet fuel economy, but sales are likely to remain small as a percent of the overall market. Top picks remain Great Wall Motor and Dongfeng Motor Our highest conviction recommendation remains Great Wall Motor, as we believe it will have strong momentum into 2H and 2015, leading to a steady stream of upgrades to earnings targets. Similarly, while Dongfeng’s share price has been the best performer over the past 3 months, we believe consensus upgrades will highlight its attractiveness.

Transcript

Please refer to page 10 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

CHINA/HONG KONG

Shanghai VW’s Lavida – China’s top-selling sedan in 1H

Source: China Auto Web, September 2014

GWM Haval H6 – China’s top-selling SUV in 1H

Source: Macquarie Research, September 2014

Table of coverage, ratings and TPs in order of preference

Name Ticker Price Rating TP TSR

Great Wall 2333 HK 32.55 OP 52.00 65.3% Dongfeng 489 HK 14.36 OP 17.50 24.7% GAC 2238 HK 8.25 OP 11.50 43.9% Geely 175 HK 2.89 OP 3.80 32.9% Brilliance 1114 HK 13.80 N 15.60 14.2% BYD 1211 HK 56.00 UP 12.80 -77.0%

Note: share prices are as of market close 2 Sept 2014. All prices in HK$. Source: FactSet, Macquarie Research, September 2014

Source: Company data, Macquarie Research, September 2014

Tale of two markets – international brands gain, domestic brands lose

Winners and losers: Looking at the results of 1H from the Chinese OEMs the winners were

clearly the JV brands, while the losers were the domestic brands.

Geely took the hardest hit among the companies in our coverage, with revenues down 19.6%

YoY as it reorganised its brands and dropped weaker models.

BYD’s auto business reported a 6.5% decline in revenues as the higher ASP on its NEVs

helped to offset the 20% decline in unit sales.

Great Wall posted an 8% increase in revenue despite a 6% volume decline helped by the

improvement in model mix led by strong sales of the H6 SUV.

BMW Brilliance reported the biggest volume increase among the JVs, up 33%, while revenue

rose 29.5% YoY.

Dongfeng Motor posted a 25.5% revenue increase for passenger vehicles (+28.3% for whole

vehicles) on a 21.5% rise in PV volumes and 30.3% higher revenue including commercial

vehicles.

GAC’s revenues from its JVs rose 9.1% YoY and 13.7% for the group overall including its own

vehicles as volumes increased 18.7%.

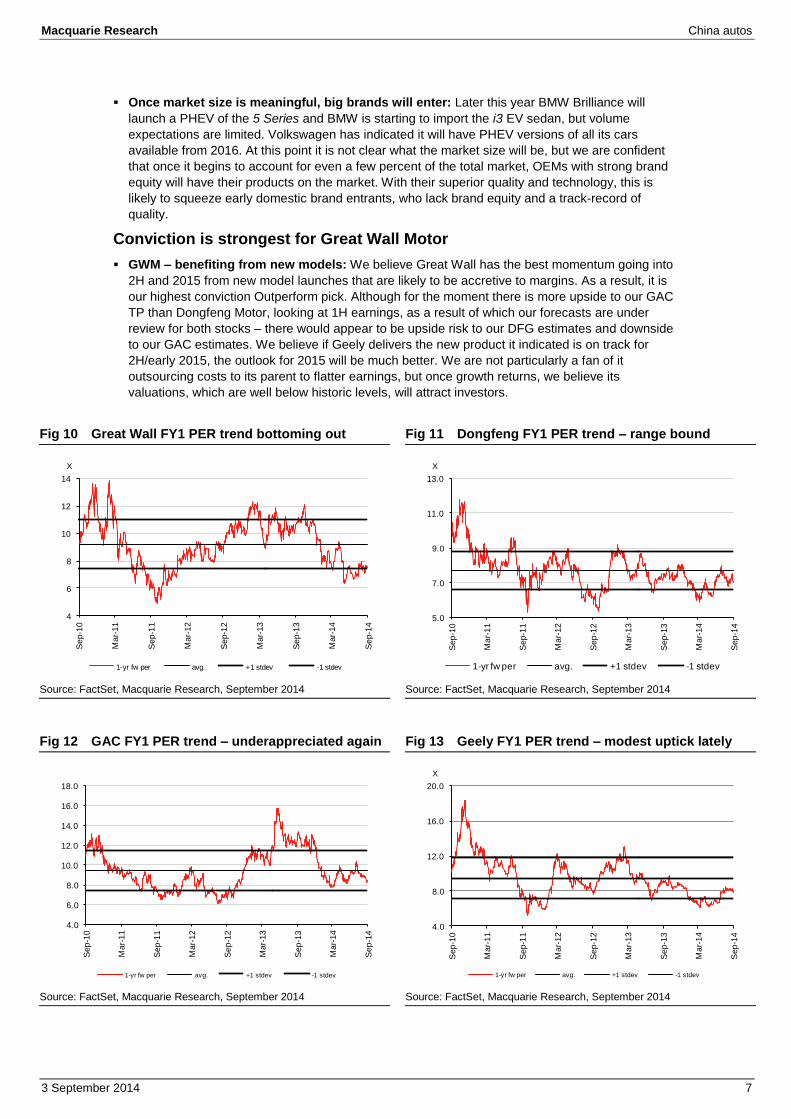

Outlook for 2H is more mixed – GWM likely to resume growth: We expect more varied

performance in 2H due to product launches. Great Wall has the best momentum going into 2H on

our view led by the July launch of the H2 SUV, the upcoming launch of the sub-compact H1 SUV

and updated sedan models. It is in the process of making most of its vehicles available with

automatic transmission (AT), which will broaden the potential customer base. Geely should benefit

from the recent launch of the new Emgrand (previously known as the EC7), but overall volumes

are likely to remain negative YoY. BYD is pinning its hopes on NEVs, as it ramps production of the

Qin PHEV and adds the Tang PHEV SUV as well as a new S7 SUV, but overall volumes are likely

to fall YoY.

New models support JVs: In the context of a PV market that is growing 11%, we expect the JVs

to continue to exceed this growth rate. Due to a weak 2H, especially the 4Q around the launch of

the facelift 5 Series, we believe BMW Brilliance’s volume growth could rise 44% YoY and 3.1%

HoH. We are looking for GAC to post 12% YoY growth (up 26% HoH) in 2H helped by new

models from Toyota – the Levin compact sedan – and Honda – the Vezel compact SUV and new

Fit model. We forecast DFG’s JVs to post 14% YoY growth in 2H (13% HoH) helped by recent

launches like the Peugeot 2008 compact SUV, the Nissan X-Trail and new Honda Spirior.

Macquarie Research China autos

3 September 2014 3

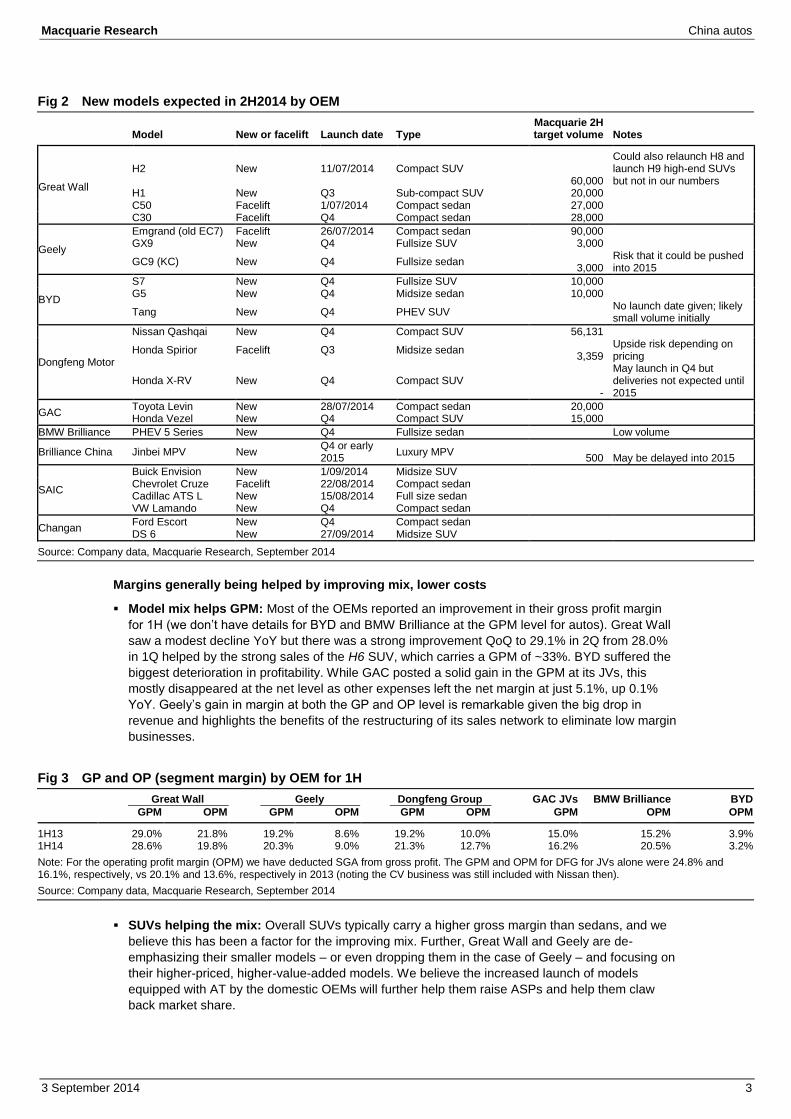

Fig 2 New models expected in 2H2014 by OEM

Model New or facelift Launch date Type

Macquarie 2H target volume Notes

Great Wall

H2 New 11/07/2014 Compact SUV 60,000

Could also relaunch H8 and launch H9 high-end SUVs but not in our numbers

H1 New Q3 Sub-compact SUV 20,000 C50 Facelift 1/07/2014 Compact sedan 27,000 C30 Facelift Q4 Compact sedan 28,000

Geely

Emgrand (old EC7) Facelift 26/07/2014 Compact sedan 90,000 GX9 New Q4 Fullsize SUV 3,000

GC9 (KC) New Q4 Fullsize sedan 3,000

Risk that it could be pushed into 2015

BYD

S7 New Q4 Fullsize SUV 10,000 G5 New Q4 Midsize sedan 10,000

Tang New Q4 PHEV SUV

No launch date given; likely small volume initially

Dongfeng Motor

Nissan Qashqai New Q4 Compact SUV 56,131

Honda Spirior Facelift Q3 Midsize sedan 3,359

Upside risk depending on pricing

Honda X-RV New Q4 Compact SUV -

May launch in Q4 but deliveries not expected until 2015

GAC Toyota Levin New 28/07/2014 Compact sedan 20,000 Honda Vezel New Q4 Compact SUV 15,000

BMW Brilliance PHEV 5 Series New Q4 Fullsize sedan Low volume

Brilliance China Jinbei MPV New Q4 or early 2015

Luxury MPV 500 May be delayed into 2015

SAIC

Buick Envision New 1/09/2014 Midsize SUV Chevrolet Cruze Facelift 22/08/2014 Compact sedan Cadillac ATS L New 15/08/2014 Full size sedan VW Lamando New Q4 Compact sedan

Changan Ford Escort New Q4 Compact sedan DS 6 New 27/09/2014 Midsize SUV

Source: Company data, Macquarie Research, September 2014

Margins generally being helped by improving mix, lower costs

Model mix helps GPM: Most of the OEMs reported an improvement in their gross profit margin

for 1H (we don’t have details for BYD and BMW Brilliance at the GPM level for autos). Great Wall

saw a modest decline YoY but there was a strong improvement QoQ to 29.1% in 2Q from 28.0%

in 1Q helped by the strong sales of the H6 SUV, which carries a GPM of ~33%. BYD suffered the

biggest deterioration in profitability. While GAC posted a solid gain in the GPM at its JVs, this

mostly disappeared at the net level as other expenses left the net margin at just 5.1%, up 0.1%

YoY. Geely’s gain in margin at both the GP and OP level is remarkable given the big drop in

revenue and highlights the benefits of the restructuring of its sales network to eliminate low margin

businesses.

Fig 3 GP and OP (segment margin) by OEM for 1H

Great Wall Geely Dongfeng Group GAC JVs BMW Brilliance BYD

Note: For the operating profit margin (OPM) we have deducted SGA from gross profit. The GPM and OPM for DFG for JVs alone were 24.8% and 16.1%, respectively, vs 20.1% and 13.6%, respectively in 2013 (noting the CV business was still included with Nissan then).

Source: Company data, Macquarie Research, September 2014

SUVs helping the mix: Overall SUVs typically carry a higher gross margin than sedans, and we

believe this has been a factor for the improving mix. Further, Great Wall and Geely are de-

emphasizing their smaller models – or even dropping them in the case of Geely – and focusing on

their higher-priced, higher-value-added models. We believe the increased launch of models

equipped with AT by the domestic OEMs will further help them raise ASPs and help them claw

back market share.

Macquarie Research China autos

3 September 2014 4

Fig 4 International brands – performance by JV (locally made models)

Top 3 selling models Units sold % chg YoY Name % chg YoY Name % chg YoY Name % chg YoY

Brilliance China BMW Brilliance 140,012 32% 5 Series 13% 3 Series 44% X1 120%

Chevrolet 335,486 4% Sail -16% Cruze 16% Malibu 20% Cadillac 14,827 109% Cadillac XTS 367% na

Changan Ford 400,454 39% Focus 8% Kuga 77% Mondeo 124% Mazda 41,553 67% CX-5 New model Mazda 3 -49% Mazda 2 -14% Suzuki 137,873 12% Beidouxing -9% New Alto -10% S-Cross New model

Note: In instances where an older model is still on the market like for the Camry, Mondeo and Focus, we have combined them; we also include both notchback and hatchback when sold under the same name, as with the Focus.

Source: Company data, Macquarie Research, September 2014

Balance sheets are healthy other than BYD: As shown in Figure 1, the balance sheets are

generally healthy other than at BYD. Despite an equity offering in 1H that raised Rmb3.3bn, BYD’s

net debt-equity ratio remains high at 76%. It had a net operating cash outflow of Rmb544m and a

further investing outflow of Rmb3,803m. Great Wall’s net cash position is enabling it to support its

dealers with interest-free inventory for up to 90 days and low rates up to 180 days, which results in

the lowest level of discounts in the industry. SAIC, with the highest net cash position helped by its

mature JVs with VW and GM, has announced it will pay out 50% of profits as a dividend, making it

the highest yielding stock in the sector. Only GAC and Brilliance announced dividends, with GAC

likely to provide a year-end dividend as well. Geely’s balance sheet has been flattered by the shift

Hyundai Motor 5380 KS Outperform 45,527 225,500 290,000 29% -5.7% 0.1% -0.3% FY14/15E 37,110.9 6.1 5.7 4.9 4.6 14.7 Michael Sohn

Kia Motors 270 KS Outperform 23,548 60,100 72,000 20% 0.4% 3.9% -1.9% FY14/15E 8,753.0 6.9 6.6 3.8 3.5 16.2 Michael Sohn

Macquarie Research China autos

3 September 2014 10

Important disclosures:

Recommendation definitions

Macquarie - Australia/New Zealand Outperform – return >3% in excess of benchmark return Neutral – return within 3% of benchmark return Underperform – return >3% below benchmark return Benchmark return is determined by long term nominal GDP growth plus 12 month forward market dividend yield

Macquarie – Asia/Europe

Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie First South - South Africa Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie - Canada

Outperform – return >5% in excess of benchmark return Neutral – return within 5% of benchmark return Underperform – return >5% below benchmark return

Macquarie - USA Outperform (Buy) – return >5% in excess of Russell 3000 index return Neutral (Hold) – return within 5% of Russell 3000 index return Underperform (Sell)– return >5% below Russell 3000 index return

Volatility index definition*

This is calculated from the volatility of historical price movements. Very high–highest risk – Stock should be expected to move up or down 60–100% in a year – investors should be aware this stock is highly speculative. High – stock should be expected to move up or

down at least 40–60% in a year – investors should be aware this stock could be speculative. Medium – stock should be expected to move up or down at least 30–40% in a year. Low–medium – stock should be expected to move up or down at least 25–30% in a year. Low – stock should be expected to move up or down at least 15–25% in a year. * Applicable to Asia/Australian/NZ/Canada stocks only

Recommendations – 12 months Note: Quant recommendations may differ from Fundamental Analyst recommendations

Financial definitions

All "Adjusted" data items have had the following adjustments made: Added back: goodwill amortisation, provision for catastrophe reserves, IFRS derivatives & hedging, IFRS impairments & IFRS interest expense Excluded: non recurring items, asset revals, property revals, appraisal value uplift, preference dividends & minority interests EPS = adjusted net profit / efpowa* ROA = adjusted ebit / average total assets ROA Banks/Insurance = adjusted net profit /average total assets ROE = adjusted net profit / average shareholders funds Gross cashflow = adjusted net profit + depreciation *equivalent fully paid ordinary weighted average number of shares All Reported numbers for Australian/NZ listed stocks are modelled under IFRS (International Financial Reporting Standards).

Recommendation proportions – For quarter ending 30 June 2014

AU/NZ Asia RSA USA CA EUR Outperform 51.67% 60.69% 34.67% 42.33% 55.41% 44.84% (for US coverage by MCUSA, 6.76% of stocks followed are investment banking clients)

Neutral 33.00% 23.93% 38.67% 50.92% 38.51% 35.87% (for US coverage by MCUSA, 7.25% of stocks followed are investment banking clients)

Underperform 15.33% 15.38% 26.67% 6.75% 6.08% 19.28% (for US coverage by MCUSA, 0.48% of stocks followed are investment banking clients)

Company-specific disclosures: Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/disclosures.

Analyst certification: The views expressed in this research accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this research. The analyst principally responsible for the preparation of this research receives compensation based on overall revenues of Macquarie Group Ltd ABN 94 122 169 279 (AFSL No. 318062) (MGL) and its related entities (the Macquarie Group) and has taken reasonable care to achieve and maintain independence and objectivity in making any recommendations. General disclaimers: Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital Markets Canada Ltd; Macquarie Capital Markets North America Ltd; Macquarie Capital (USA) Inc; Macquarie Capital Securities Ltd and its Taiwan branch; Macquarie Capital Securities (Singapore) Pte Ltd; Macquarie Securities (NZ) Ltd; Macquarie First South Securities (Pty) Limited; Macquarie Capital Securities (India) Pvt Ltd; Macquarie Capital Securities (Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and Macquarie Securities (Thailand) Ltd are not authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia), and their obligations do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542 (MBL) or MGL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of any of the above mentioned entities. MGL provides a guarantee to the Monetary Authority of Singapore in respect of the obligations and liabilities of Macquarie Capital Securities (Singapore) Pte Ltd for up to SGD 35 million. This research has been prepared for the general use of the wholesale clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient you must not use or disclose the information in this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. MGL has established and implemented a conflicts policy at group level (which may be revised and updated from time to time) (the "Conflicts Policy") pursuant to regulatory requirements (including the FCA Rules) which sets out how we must seek to identify and manage all material conflicts of interest. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. In preparing this research, we did not take into account your investment objectives, financial situation or particular needs. Macquarie salespeople, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions which are contrary to the opinions expressed in this research. Macquarie Research produces a variety of research products including, but not limited to, fundamental analysis, macro-economic analysis, quantitative analysis, and trade ideas. Recommendations contained in one type of research product may differ from recommendations contained in other types of research, whether as a result of differing time horizons, methodologies, or otherwise. Before making an investment decision on the basis of this research, you need to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of your particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and international stock market or economic conditions, which may adversely affect the value of the investment. This research is based on information obtained from sources believed to be reliable but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice. No member of the Macquarie Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. Clients should contact analysts at, and execute transactions through, a Macquarie Group entity in their home jurisdiction unless governing law permits otherwise. The date and timestamp for above share price and market cap is the closed price of the price date. #CLOSE is the final price at which the security is traded in the relevant exchange on the date indicated. Country-specific disclaimers: Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organisation of the Australian Securities Exchange. New Zealand: In New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm. Canada: In Canada, research is prepared, approved and distributed by Macquarie Capital Markets Canada Ltd, a participating organisation of the Toronto Stock Exchange, TSX Venture Exchange & Montréal Exchange. Macquarie Capital Markets North America Ltd., which is a registered broker-dealer and member of FINRA, accepts responsibility for the contents of reports issued by Macquarie Capital Markets Canada Ltd in the United States

David Gambrill (Thailand) (662) 694 7753 Find our research at Macquarie: www.macquarie.com.au/research Thomson: www.thomson.com/financial Reuters: www.knowledge.reuters.com Bloomberg: MAC GO Factset: http://www.factset.com/home.aspx CapitalIQ www.capitaliq.com Email [email protected] for access