26

12 JUNE 2007 • OKURA GARDEN HOTEL • SHANGHAI GLOBAL INSIGHT AUTOMOTIVE SEMINAR China’s Automotive Components Industry — Opportunities and Challenges Iping Wong Senior Automotive Consultant

12 JUNE 2007 • OKURA GARDEN HOTEL • SHANGHAI GLOBAL INSIGHT AUTOMOTIVE SEMINAR

China’s Automotive Components Industry —Opportunities and Challenges

Iping WongSenior Automotive Consultant

Copyright © 2007 Global Insight, Inc. 2

• Challenges and opportunity analysis

• Trends in China’s automotive components industry

• Overview of China’s automotive components industry

Contents

Copyright © 2007 Global Insight, Inc. 3

2006 China Auto Components Industry Overview

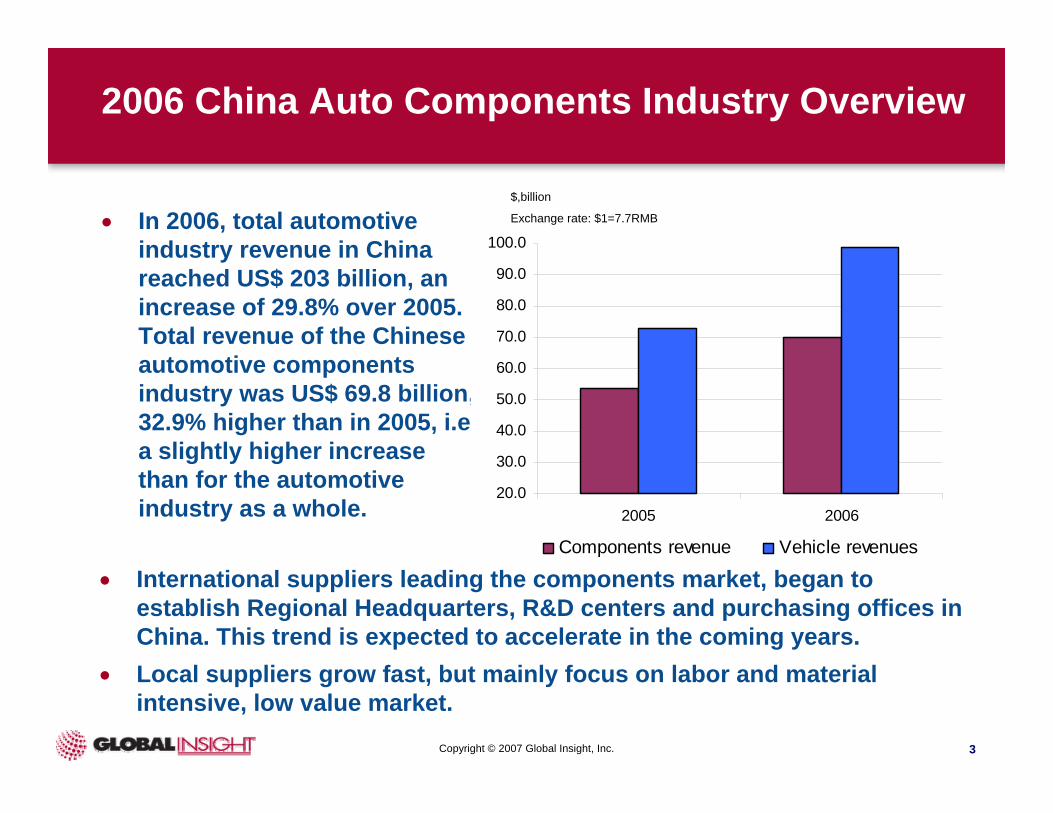

• In 2006, total automotive industry revenue in China reached US$ 203 billion, an increase of 29.8% over 2005.Total revenue of the Chinese automotive components industry was US$ 69.8 billion, 32.9% higher than in 2005, i.e. a slightly higher increase than for the automotive industry as a whole.

• International suppliers leading the components market, began to establish Regional Headquarters, R&D centers and purchasing offices in China. This trend is expected to accelerate in the coming years.

• Local suppliers grow fast, but mainly focus on labor and material intensive, low value market.

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

2005 2006

Components revenue Vehicle revenues

$,billion

Exchange rate: $1=7.7RMB

Copyright © 2007 Global Insight, Inc. 4

Over the Past Six Years, China’s Automotive Components Industry Enjoyed Dramatic Growth

The yearly average growth rate reached 30%. Due to the strong vehicle market this year, it is expected the components industrywill maintain this growth rate also in 2007.

Total production value

184.2%

Resources: autoinfo.gov.cn

24.6

41.4

51.6 53.5

69.8

32

10

20

30

40

50

60

70

2001 2002 2003 2004 2005 2006

Exchange rate: $1=7.7RMB

$,Billion

Copyright © 2007 Global Insight, Inc. 5

Production Is Mainly Located in Developed Areas or Near OEMs

Jilin

Liaoning

Chongqing

Guangdong

Shandong

Hubei

Hebei

Anhui

Zhejiang

Jiangsu

Tianjin

Shanghai

Beijing

Resources: autoinfo.gov.cn

Hebei3%

Others15%

Zhejiang18%

Jiangsu10%

Shandong9%Guangdong

8%

Chongqing4%

Jilin5%

Liaoning3%

Tianjin4%

Shanghai11%

Hubei5%

Beijing5%

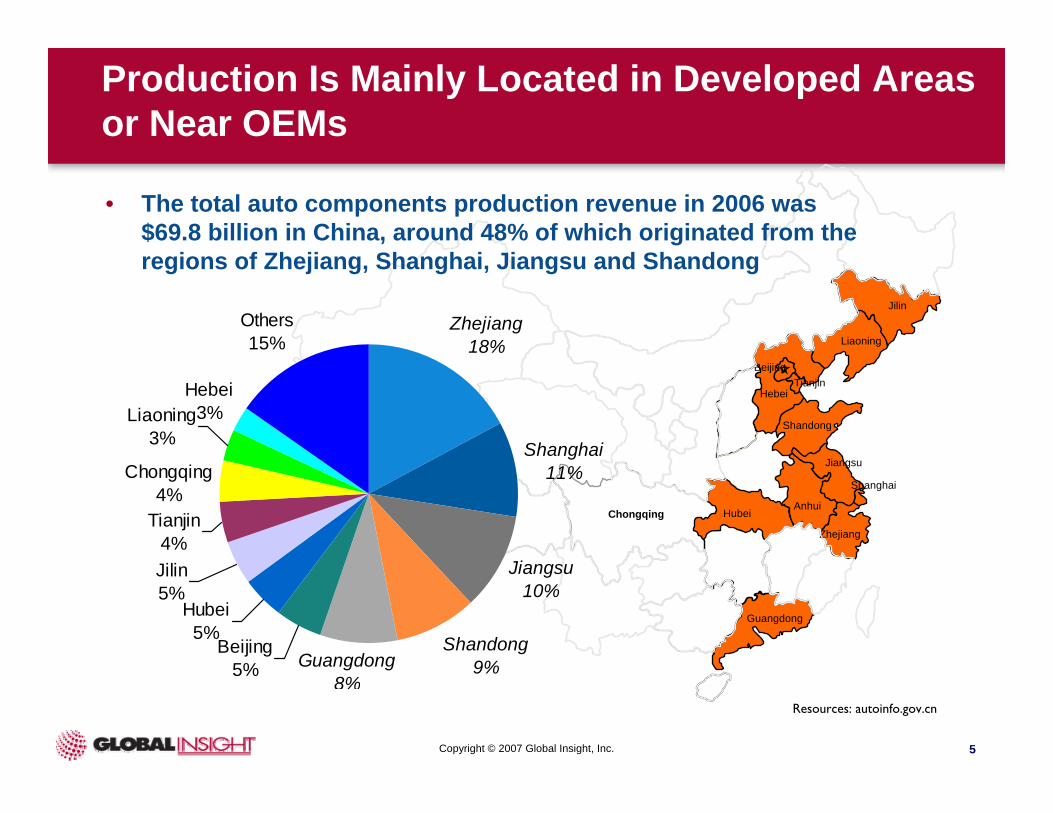

• The total auto components production revenue in 2006 was $69.8 billion in China, around 48% of which originated from the regions of Zhejiang, Shanghai, Jiangsu and Shandong

Copyright © 2007 Global Insight, Inc. 6

Exports Account For Less Than 16% of Total Automotive Industry Revenue

Resoures: autoinfo.gov.cn

Exchange rate: $1=7.7RMB

$,Billion

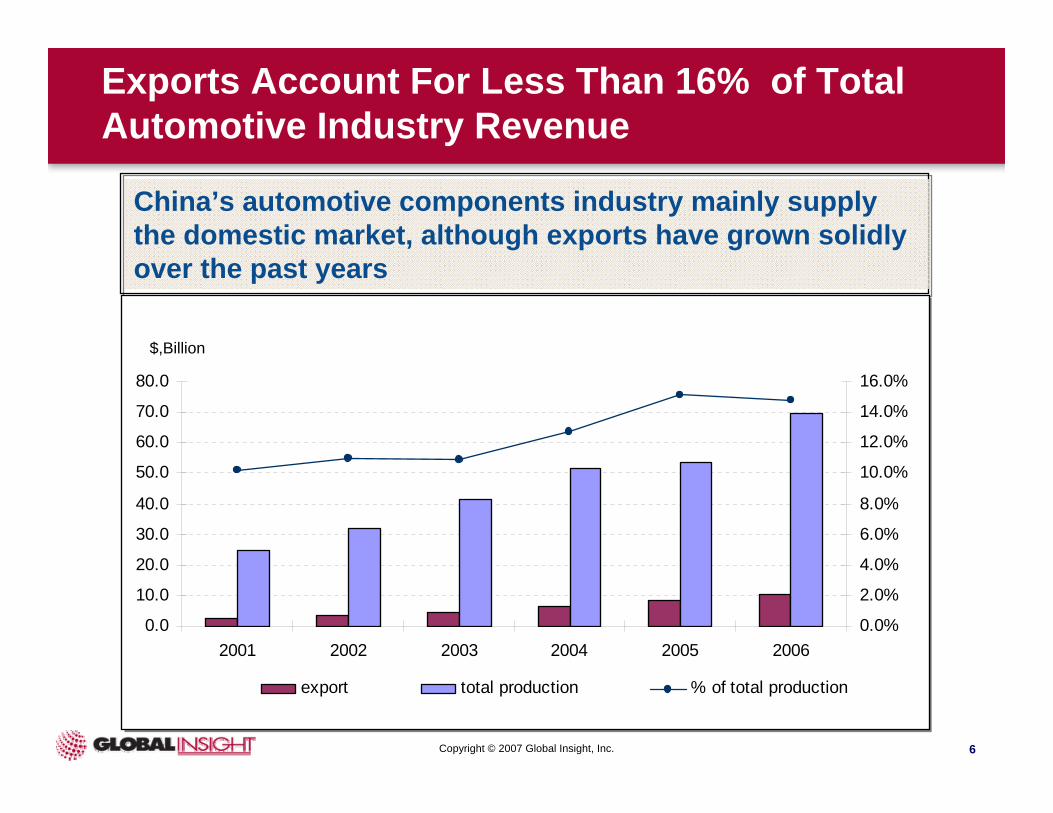

China’s automotive components industry mainly supply the domestic market, although exports have grown solidly over the past years

$,Billion

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2001 2002 2003 2004 2005 20060.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

export total production % of total production

Copyright © 2007 Global Insight, Inc. 7

• Chinese local companies have the strong interest in exporting their products to overseas markets – Currently they mainly supply the aftermarket in some developed

countries, e.g. A/C compressors, aluminum wheels, tires

– Export products are typically labour intensive, e.g. seat trim cover and electronics assembly

– Products which could cause environmental damage or huge energy consumption in developed countries, e.g. castings

• A few of JVs’ products are exported to their parent companies’ plants, then supplied to local OEMs, or to the other world markets where the parent company is not present.

• Small number of JVs and local companies have been successful in some international Platform supply projects

Currently Export Products Are Mainly Labour Intensive and Aimed at Aftermarket or Tier 2 Suppliers

Copyright © 2007 Global Insight, Inc. 8

Foreign Companies and JVs Are the Main Players, and They Dominate the Key Components Supply

• Relatively few Chinese local suppliers are competitive • As SAIC lead the passenger car market since many years, the

component JVs with SAIC/FAW still maintain leadership in the auto components industry

Jiangsu ChenyangTianjin StanleyHubei ValeoHellaShanghai-KoitoLightning

Mando SuzhouZhejiang APWanxiangTRW-LucasSABSABS

MandoTRWFAW-KoyoShanghai ZFSteering

Beijing MonroeFAW-TokicoHuizhong SachsChasis

GKN North ChinaWanxiangNTNDelphi SaginowGKN ShanghaiProp shaft

Changchun TowerPeugeot-CitroenFAW-Kelsey-HayesShanghai HuizhongAxle

Tianjin DensoHuada - ZEXELSSBCompressor

VisteonValeo A/CDensoShanghai BehrDelphiA/C

Changsu InteriorLanbaoLearFawer/JCIYanfeng/VisteonInteriors

ContinentalMarelli/DensoSiemensDelphiUAESEMS

Resources: SAIClocal supplier

Copyright © 2007 Global Insight, Inc. 9

0

100

200

300

400

500

600

Shang

hai

Jiang

suGua

ngdo

ngTian

jinLia

oning

Shand

ong

Zhejia

ngFuji

an Jilin

Others

Foreign Companies Are Mainly Located in Developed Areas or Near OEMs• Around 82% of foreign component suppliers, including JVs, are located in

developed areas, or somewhere not far away from main OEMs

Resoures: FOURIN, April, 2007, Japan

Xinjiang

Gansu

Heilongjiang

Jilin

Liaoning

Taiwan

Tibet

SichuanChongqing

YunnanGuangxi Guangdong

Fujian

Shandong

Hubei

Hunan Jiangxi

Hainan

Inner Mongolia

NingxiaQinghai

HebeiShanxi

Henan

Anhui

Zhejiang

JiangsuShaanxi

Guizhou

Tianjin

Shanghai

Beijing

• Shanghai is the most centralized area, where 22% of these companies are located

The number of foreign companies

Copyright © 2007 Global Insight, Inc. 10

Other, 20.76%

Wholy OE, 35.87%

JV, 43.37%

Among the Foreign Companies, JVs Are Still Most Common

• So far, JVs still account for the largest number of component suppliers. However, foreign wholly controlled subsidiaries are becoming increasingly common.

Japan, 56.02%

Taiwan, 10.83%

Europe/US, 26.06%

Korea, 6.48%

• The major players are from Europe/U.S./Japan. Although larger in number, the scale of the Japanese component suppliers is usually smaller and they mainly supply Japanese OEMs.

By Investment By Origin

The number of foreign companies

The number of foreign companies

Resoures: FOURIN, Japan

Copyright © 2007 Global Insight, Inc. 11

JVs Will Be Split or Replaced By Companies Wholly Owned by Foreign Suppliers

• Local partners are mostly involved in the manufactuing and assemlby only

• Hope to export their products to worldwide market in large volumes

• Learn the core technology, management and grow up to become independent supplier

• Culture difference

China Local Partners

• Control the core departments inside the JVs

• The main purpose to establish a joint venture with local partner is to make products to supply for local OEMs

• Strictly control core technology to transfer to local partners

• Culture difference

International Component Suppliers

Copyright © 2007 Global Insight, Inc. 12

• Challenges and opportunity analysis

• Trends in China’s automotive components industry

• Overview of China’s automotive components industry

Contents

Copyright © 2007 Global Insight, Inc. 13

• To be able to better supply local market and customers• To catch up with the fast growing vehicle market• China’s auto market plays an important role for

international component suppliers

Trends

Production

Prod + R&D + Regional Headquarters

2

• Foreign suppliers are mainly selling their products to JV OEMs, but are now also beginning to supply local Chinese OEMs, such as Chery and Geely

Supply for JV OEMs

Supply for JV OEMs + Local OEMs

1

Parts Supplier

Platform Supplier

• Some of the SAIC Group’s subsidiary joint ventures were successful in GM’s global Epsilon 2 platform project and will supply their products worldwide

3

Copyright © 2007 Global Insight, Inc. 14

• China’s local suppliers are beginning to export their products to international OEMs, in addition to the traditional aftermarket

• More and more foreign component suppliers chose China as their world base for supplying some of their overseas markets

• With the development of advanced technology in electronics, computer and network, some functions previously performed by mechanical systems are going to be replaced by electronics

• Vehicles are becoming more complicated and increasingly requiring electronic technology

• Due to China’s huge auto market, foreign component suppliers begin to sell their products and services to the local Chinese aftermarket, e.g. Bosch and Michelin

Mechanical

Electronic / Infotainment

Trends

OEM Market

OEM + AF Market

Domestic Market

Overseas Market

4

5

6

Copyright © 2007 Global Insight, Inc. 15

Trends

• China’s auto market has become one of the largest in the world

• Chinese customers and OEMs are becoming familiar with automotive technology

Out of Date Tech

Advanced Tech

7

JV

Wholly Controlled

• Foreign companies becoming familiar with Chinese market and investment environment

• The ownership share restriction for foreign companies has been withdrawn for automotive component industry

9

• Some leading suppliers beginning to acquire Chinese local competitors, or control their Chinese local partners, e.g. Bosch control of JV with Weihu

Cooperation

Cooperation + Competition + Merger

8

Copyright © 2007 Global Insight, Inc. 16

Trends

• International OEM’s and major suppliers target low cost manufacturing

• Global sourcing creates opportunities to improve local suppliers’ capabilities in development, cost control and quality

Local Supply

Global Sourcing

10

• Some raw material providers begin to tap into components industry. Bao steel are beginning....

Raw Material Provider

Component Producer

11

Copyright © 2007 Global Insight, Inc. 17

• Challenges and opportunity analysis

• Trends in China’s automotive components industry

• Overview of China’s automotive components industry

Contents

Copyright © 2007 Global Insight, Inc. 18

Vehicle OEMs

Rising raw material prices

JV, International

original supplier

Low brand, quality,

technology, management

Local component suppliers

Local Suppliers — Struggling ?

OEM pressure to reduce prices, and limited R&D capability are seen as the major challenges in the short term. Uncompetitiveness in high-tech products, lack of core know-how, e.g. in electronics, present huge challenges for the future.

Copyright © 2007 Global Insight, Inc. 19

Local Suppliers — Competitive?

• Some parts 20~30% more expensive due to poor logistics, lack of economies of scale and lack of local sourcing of parts.

• Raw material and labour cost increases, together with intensified competition, restrict margins.

• Can’t compete with funded Tier 1’s.

• Foreign suppliers are penetrating traditional low segment market and taking share.

• Lag behind the international suppliers in high tech fields. Few companies own advanced technology, especially in electronics.

Copyright © 2007 Global Insight, Inc. 20

Local Suppliers — Strengthening?

• Still lower labour cost advantage

• Local suppliers are more familiar with the local market

• Local partners’ engineering capability is raised

• Operating costs are lower than those of JVs and international companies

• Have made big strides in efficiency, quality, product development and management

• Government policy support

• Competitive areas for future: labour and material intensive, technically sophisticated with high labour (e.g. compressor)

Copyright © 2007 Global Insight, Inc. 21

Opportunities For Local Component Suppliers

Local market continues to grow strongly

Aftermarket is becoming larger

Advantage in low segment market

International auto industry transfer

Export, international purchasing

Copyright © 2007 Global Insight, Inc. 22

Explore Overseas Markets Step by Step

Aftermarket /

OEM supply for emerging markets

Phase 1 Phase 2 Phase 3

Tier 1

Tier 2

tirelamp

compressor

wiper

• Technical support• Logistics• Involved in

development

Medium precision

Mechanical Components

• Local technical support• Global concurrent development• Logistics• Deeply involved in development

High precision Core Components and

Modules

Copyright © 2007 Global Insight, Inc. 23

• To be leading Tier 1 supplier for local brand OEMs, and Tier 2 supplier for JVs’ brands

• Long term alliance with local OEMs, especially in key components supply with big OEMs to help develop capability in advanced technology

• Explore domestic and overseas markets

• Increase focus and competitiveness on selected components

• Protect and maintain advantage in domestic aftermarket

• Seek opportunities in alternative energy vehicle development

Conclusions — Local Suppliers

Copyright © 2007 Global Insight, Inc. 24

International Suppliers — Challenges and Strengths

Challenges

• Higher operating costs than local suppliers

• Strong competition from local Chinese suppliers in labor intensive, low value component areas

• Control and lead in core technology in key component areas -particularly European suppliers in electronics, energy saving, efficiency boosting, environment protection and safety

• Higher profitability than local suppliers

• Original supplier overseas priority

Strengths

Copyright © 2007 Global Insight, Inc. 25

Opportunities and Conclusions — International Suppliers

• The second largest auto market in the world• Local aftermarket is growing rapidly, the first summit is coming• Fast growing local brand OEMs• Ability to maintain leading position in China’s automotive

components industry for years to come

Opportunities

Conclusions

• Maintain leading position for brand and core technology• Reduce operating cost through localization• Develop business with local brand OEMs• Take advantage of local low cost opportunities in production,

development and purchasing to support sales in other markets

12 JUNE 2007 • OKURA GARDEN HOTEL • SHANGHAI GLOBAL INSIGHT AUTOMOTIVE SEMINAR

Thank You

Iping WongSenior Automotive Consultant

E-mail: [email protected]