28

US LNG Exports Chris Pedersen LNG Pricing Analyst - Americas

No content below the line No content below the line

US LNG Exports Chris Pedersen

LNG Pricing Analyst - Americas

No content below the line No content below the line

© 2016 by S&P Global Platts, a division of S&P Global Inc. All rights reserved.

The names “S&P Global Platts” and “Platts” and the logo are trademarks of S&P Global Inc. Any commercial use of the S&P Global

Platts logo must be granted in writing by S&P Global Inc.

You may view or otherwise use the information, prices, indices, assessments and other related information, graphs, tables and

images (“Data”) in this material only for your personal and internal use only. You may not publish, reproduce, extract, distribute,

retransmit, resell, create any derivative work from and/or otherwise provide access to the Data or any portion thereof to any person

(either within or outside your company, including as part of or via any internal electronic system or intranet), firm or entity, including

any subsidiary, parent, or other entity that is affiliated with your company, without S&P Global Platts’ prior written consent.

S&P Global Platts, its affiliates and their third-party licensors do not guarantee the adequacy, accuracy, timeliness and/or

completeness of the Data or any component thereof or any communications (whether written, oral, electronic or other format), with

respect thereto and shall not be subject to any damages or liability, including but not limited to any indirect, special, incidental,

punitive or consequential damages. Users of the Data should not rely on the information therein in making any investment, trading,

risk management or other decision.

Any queries or requests pursuant to this notice should be addressed to S&P Global Inc. via email at [email protected].

Disclaimer

No content below the line No content below the line

Agenda

3

• Global LNG

• Infrastructure capabilities

• Supply

• Demand

• US LNG

• Liquefaction Capacity

• US LNG deliveries

• Pricing Mechanisms for Global & US LNG

• Evolution of contracts/prices

No content below the line No content below the line

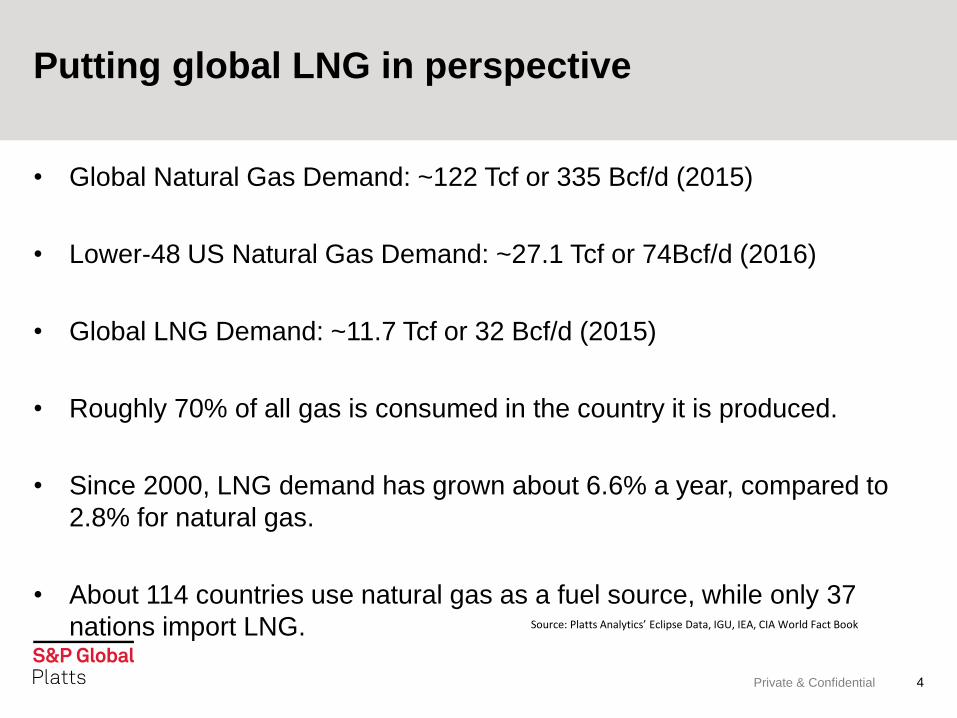

Putting global LNG in perspective

Private & Confidential 4

• Global Natural Gas Demand: ~122 Tcf or 335 Bcf/d (2015)

• Lower-48 US Natural Gas Demand: ~27.1 Tcf or 74Bcf/d (2016)

• Global LNG Demand: ~11.7 Tcf or 32 Bcf/d (2015)

• Roughly 70% of all gas is consumed in the country it is produced.

• Since 2000, LNG demand has grown about 6.6% a year, compared to

2.8% for natural gas.

• About 114 countries use natural gas as a fuel source, while only 37

nations import LNG.

Source: Platts Analytics’ Eclipse Data, IGU, IEA, CIA World Fact Book

No content below the line No content below the line

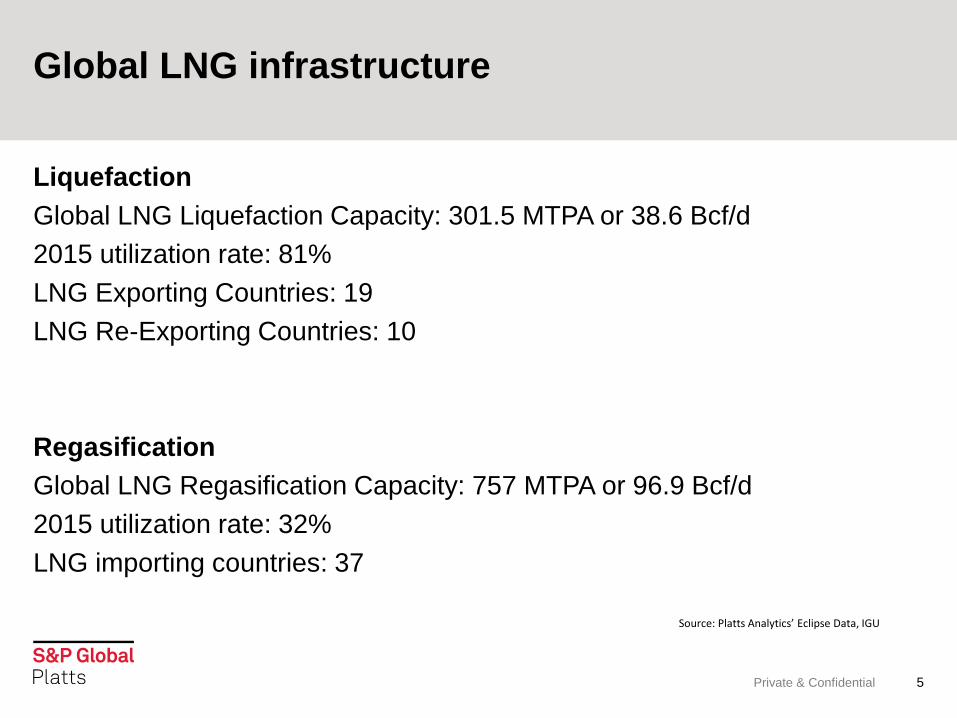

Global LNG infrastructure

Private & Confidential 5

Liquefaction

Global LNG Liquefaction Capacity: 301.5 MTPA or 38.6 Bcf/d

2015 utilization rate: 81%

LNG Exporting Countries: 19

LNG Re-Exporting Countries: 10

Regasification

Global LNG Regasification Capacity: 757 MTPA or 96.9 Bcf/d

2015 utilization rate: 32%

LNG importing countries: 37

Source: Platts Analytics’ Eclipse Data, IGU

No content below the line No content below the line

Natural gas/LNG to play a larger role in the future

Private & Confidential 6

Natural Gas

40% of the growth in global energy demand from 2014-2040 is projected to

be met by natural gas.

LNG

IEA report forecasts liquefaction capacity to grow 45% between 2015-2021.

China, India, Brazil, Mexico, South Africa, Nigeria, Egypt, Turkey, Saudi

Arabia, Iran, Thailand & Indonesia will account for roughly 80% of the new

growth in energy demand through 2040.

Source: Platts Analytics’ Eclipse Data, IGU, IEA, CIA World Fact Book, Exxon

No content below the line No content below the line

Natural Gas

7

0

1000

2000

3000

4000

5000

6000

Asia Pacific Middle East Europe Americas Africa

LNG exports by region

Vo

lum

e (

Bcf

)

Year to Sep 2015 Year to Sep 2016

Source: Platts Analytics’ Eclipse Data

No content below the line No content below the line

Natural Gas

8

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Qatar Australia Malaysia Indonesia United States

LNG exports by country

Year to Sep 2015 Year to Sep 2016

Source: Platts Analytics’ Eclipse Data

Vo

lum

e (

Bcf

)

No content below the line No content below the line

Natural Gas

9

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Japan South Korea Middle East SouthAmerica

Europe China

LNG imports by country

Year to Sep 2015 Year to Sep 2016

Vo

lum

e (

Bcf

)

No content below the line No content below the line

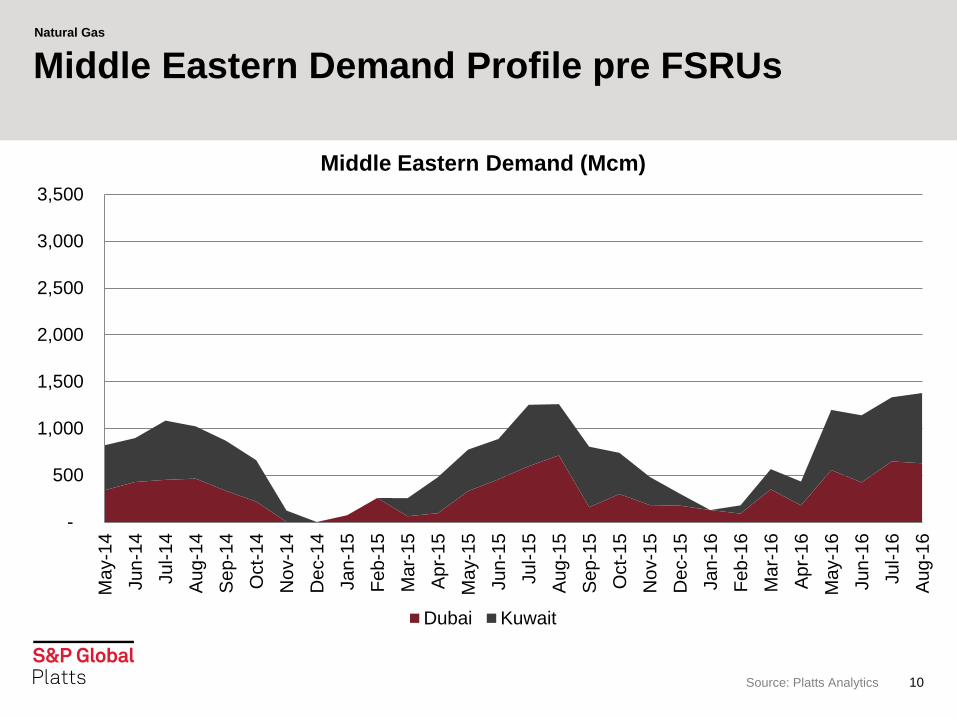

Natural Gas

Source: Platts Analytics 10

Middle Eastern Demand Profile pre FSRUs

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oct-

14

No

v-1

4

De

c-1

4

Ja

n-1

5

Fe

b-1

5

Ma

r-1

5

Ap

r-1

5

Ma

y-1

5

Ju

n-1

5

Ju

l-1

5

Au

g-1

5

Se

p-1

5

Oct-

15

No

v-1

5

De

c-1

5

Ja

n-1

6

Fe

b-1

6

Ma

r-1

6

Ap

r-1

6

Ma

y-1

6

Ju

n-1

6

Ju

l-1

6

Au

g-1

6

Middle Eastern Demand (Mcm)

Dubai Kuwait

No content below the line No content below the line

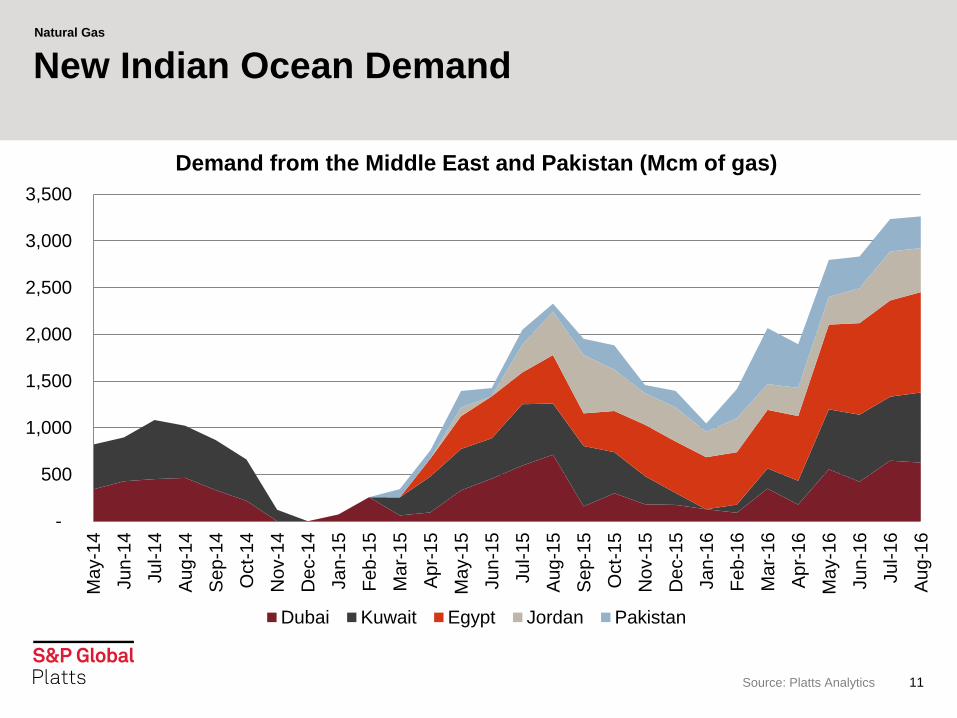

Natural Gas

Source: Platts Analytics 11

New Indian Ocean Demand

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oct-

14

No

v-1

4

De

c-1

4

Ja

n-1

5

Fe

b-1

5

Ma

r-1

5

Ap

r-1

5

Ma

y-1

5

Ju

n-1

5

Ju

l-1

5

Au

g-1

5

Se

p-1

5

Oct-

15

No

v-1

5

Dec-1

5

Ja

n-1

6

Fe

b-1

6

Ma

r-1

6

Ap

r-1

6

Ma

y-1

6

Ju

n-1

6

Ju

l-1

6

Au

g-1

6

Demand from the Middle East and Pakistan (Mcm of gas)

Dubai Kuwait Egypt Jordan Pakistan

No content below the line No content below the line

Natural Gas

Source: Platts. Private & Confidential. 12

New Indian Ocean Demand

-

1,000

2,000

3,000

4,000

5,000

6,000

Middle Eastern and South Asian Demand (Mcm of gas)

India Dubai Kuwait Egypt Jordan Pakistan

No content below the line No content below the line

Natural Gas

13

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

20

14

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

US LNG Export Overview AEO 2005 US Net Natural Gas Imports AEO 2016 US Net Natural Gas Imports

0

1

2

3

4

5

6

7

8

9

10

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

20

20

20

22

20

24

Source: EIA Annual Energy Outlook 2005 & 2016

Pipeline LNG

No content below the line No content below the line

Natural Gas

0

2

4

6

8

10

12

14

16

18

20

2010 2011 2012 2013 2014 2015 2016

$/M

MB

tu

Regional Gas Prices

JKM NBP Henry Hub

Private & Confidential 14

Market prices reflect change

Tight period Supply growth

Source: Platts Analytics’ Bentek Data & Eclipse Data

No content below the line No content below the line

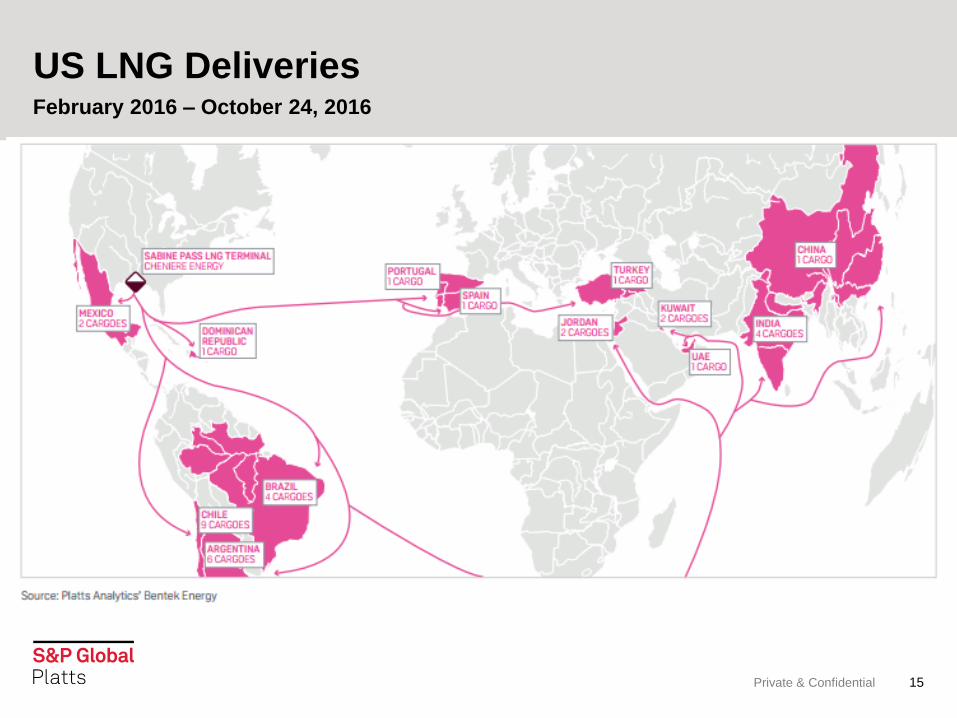

US LNG Deliveries

Private & Confidential 15

February 2016 – October 24, 2016

No content below the line No content below the line

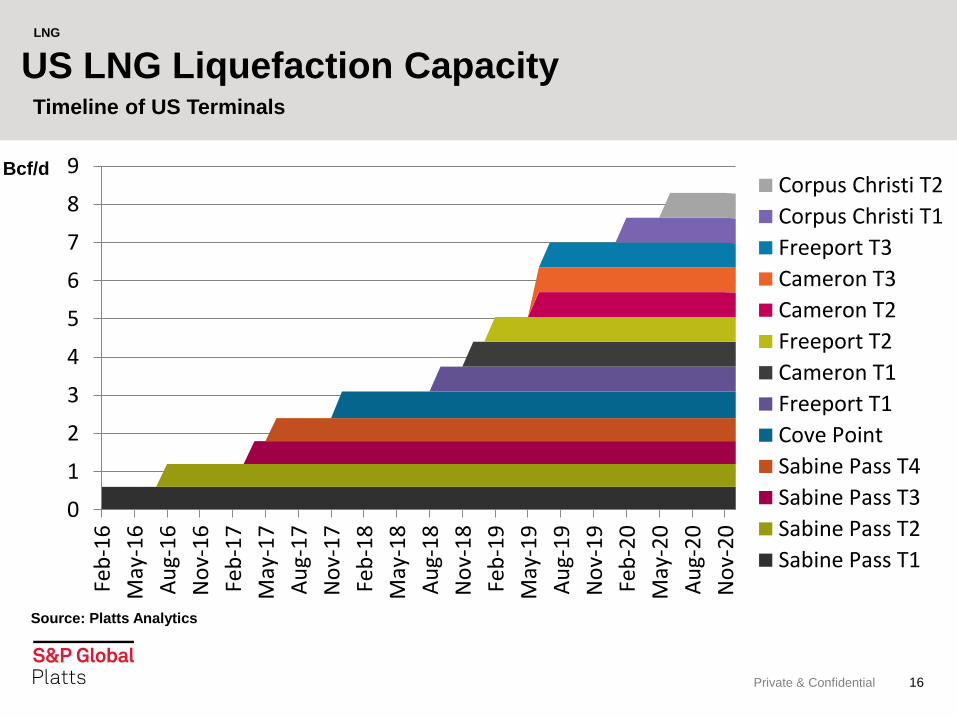

US LNG Liquefaction Capacity

Private & Confidential 16

Timeline of US Terminals

LNG

0

1

2

3

4

5

6

7

8

9

Feb

-16

May

-16

Au

g-1

6

No

v-1

6

Feb

-17

May

-17

Au

g-1

7

No

v-1

7

Feb

-18

May

-18

Au

g-1

8

No

v-1

8

Feb

-19

May

-19

Au

g-1

9

No

v-1

9

Feb

-20

May

-20

Au

g-2

0

No

v-2

0

Corpus Christi T2

Corpus Christi T1

Freeport T3

Cameron T3

Cameron T2

Freeport T2

Cameron T1

Freeport T1

Cove Point

Sabine Pass T4

Sabine Pass T3

Sabine Pass T2

Sabine Pass T1

Bcf/d

Source: Platts Analytics

No content below the line No content below the line

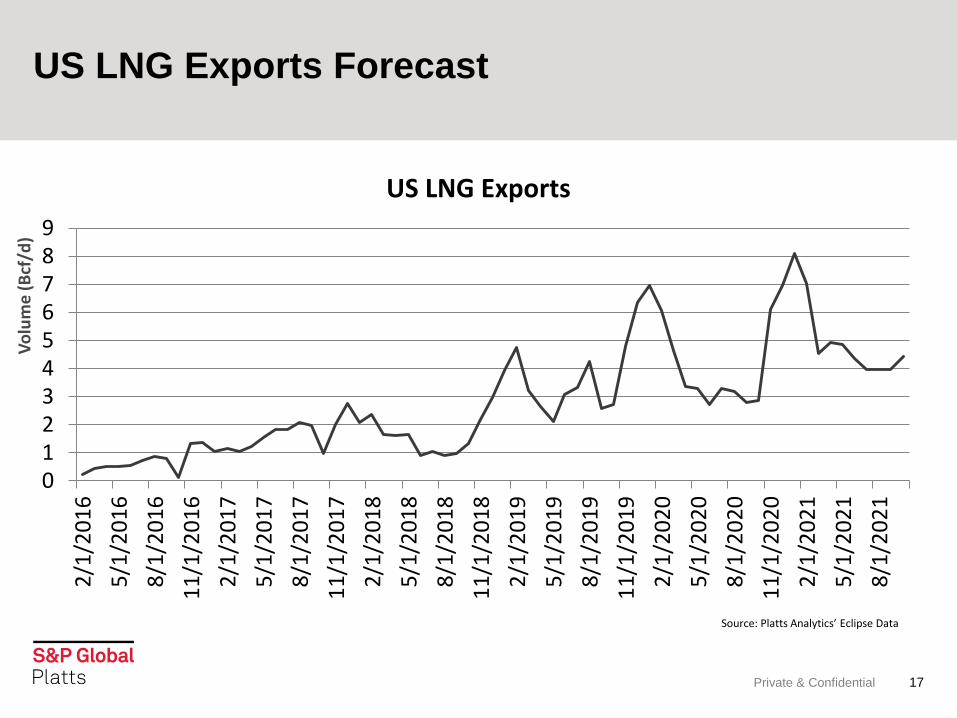

US LNG Exports Forecast

Private & Confidential 17

0123456789

2/1

/20

16

5/1

/20

16

8/1

/20

16

11

/1/2

01

6

2/1

/20

17

5/1

/20

17

8/1

/20

17

11

/1/2

01

7

2/1

/20

18

5/1

/20

18

8/1

/20

18

11

/1/2

01

8

2/1

/20

19

5/1

/20

19

8/1

/20

19

11

/1/2

01

9

2/1

/20

20

5/1

/20

20

8/1

/20

20

11

/1/2

02

0

2/1

/20

21

5/1

/20

21

8/1

/20

21

US LNG Exports

Source: Platts Analytics’ Eclipse Data

Vo

lum

e (

Bcf

/d)

No content below the line No content below the line

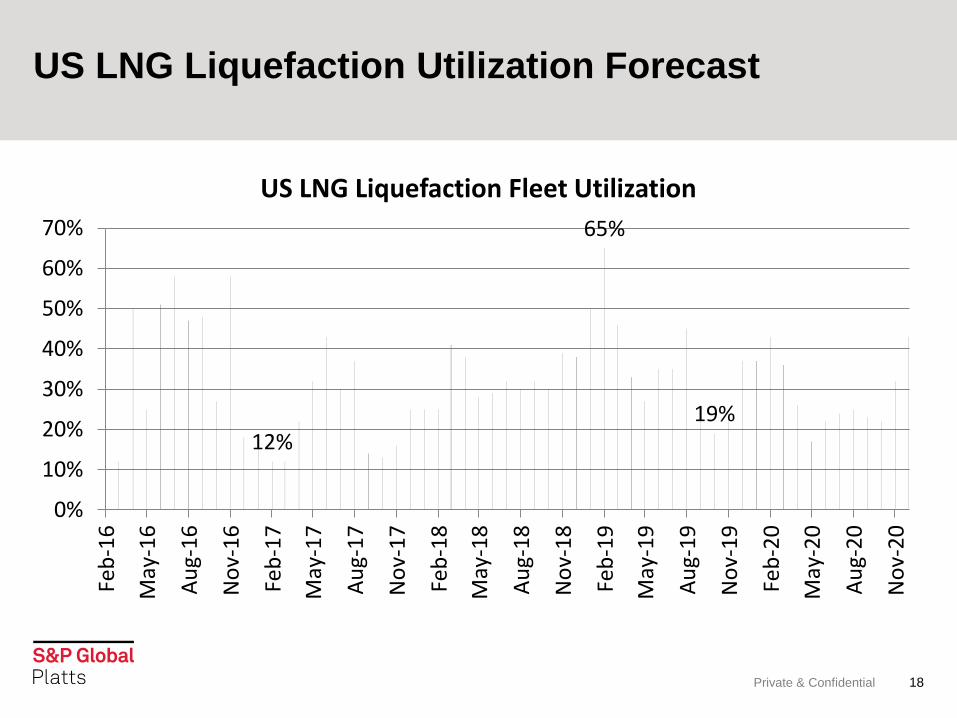

US LNG Liquefaction Utilization Forecast

Private & Confidential 18

12%

65%

19%

0%

10%

20%

30%

40%

50%

60%

70%

Feb

-16

May

-16

Au

g-1

6

No

v-1

6

Feb

-17

May

-17

Au

g-1

7

No

v-1

7

Feb

-18

May

-18

Au

g-1

8

No

v-1

8

Feb

-19

May

-19

Au

g-1

9

No

v-1

9

Feb

-20

May

-20

Au

g-2

0

No

v-2

0

US LNG Liquefaction Fleet Utilization

No content below the line No content below the line

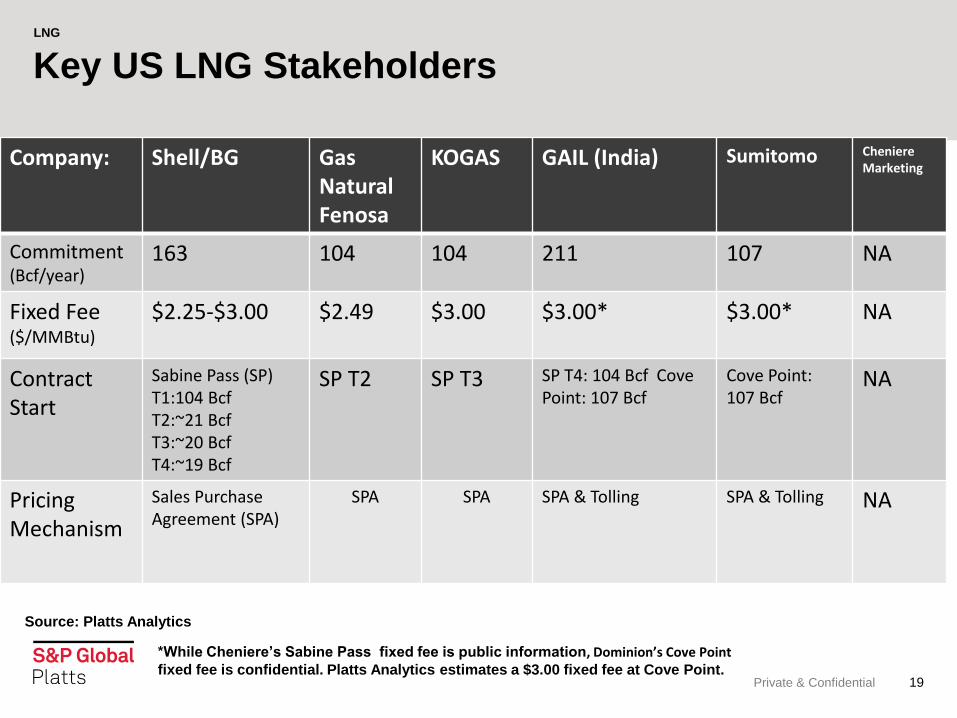

Key US LNG Stakeholders

Private & Confidential 19

Company: Shell/BG Gas Natural Fenosa

KOGAS GAIL (India) Sumitomo Cheniere Marketing

Commitment (Bcf/year)

163 104 104 211 107 NA

Fixed Fee ($/MMBtu)

$2.25-$3.00 $2.49

$3.00 $3.00* $3.00* NA

Contract Start

Sabine Pass (SP) T1:104 Bcf T2:~21 Bcf T3:~20 Bcf T4:~19 Bcf

SP T2 SP T3 SP T4: 104 Bcf Cove Point: 107 Bcf

Cove Point: 107 Bcf

NA

Pricing Mechanism

Sales Purchase Agreement (SPA)

SPA

SPA

SPA & Tolling SPA & Tolling

NA

LNG

*While Cheniere’s Sabine Pass fixed fee is public information, Dominion’s Cove Point fixed fee is confidential. Platts Analytics estimates a $3.00 fixed fee at Cove Point.

Source: Platts Analytics

No content below the line No content below the line

LNG Pricing Mechanisms

Private & Confidential 20

Oil-Indexed

Example: 13% of Brent or JCC

Gas Hub-Linked

Example: Henry Hub plus 15%, contracts based off of differentials of NBP or TTF

Benchmarks

Example: Platts JKM™

Assessments

Example: Platts GCM, EAM, NWE, DES West India

No content below the line No content below the line

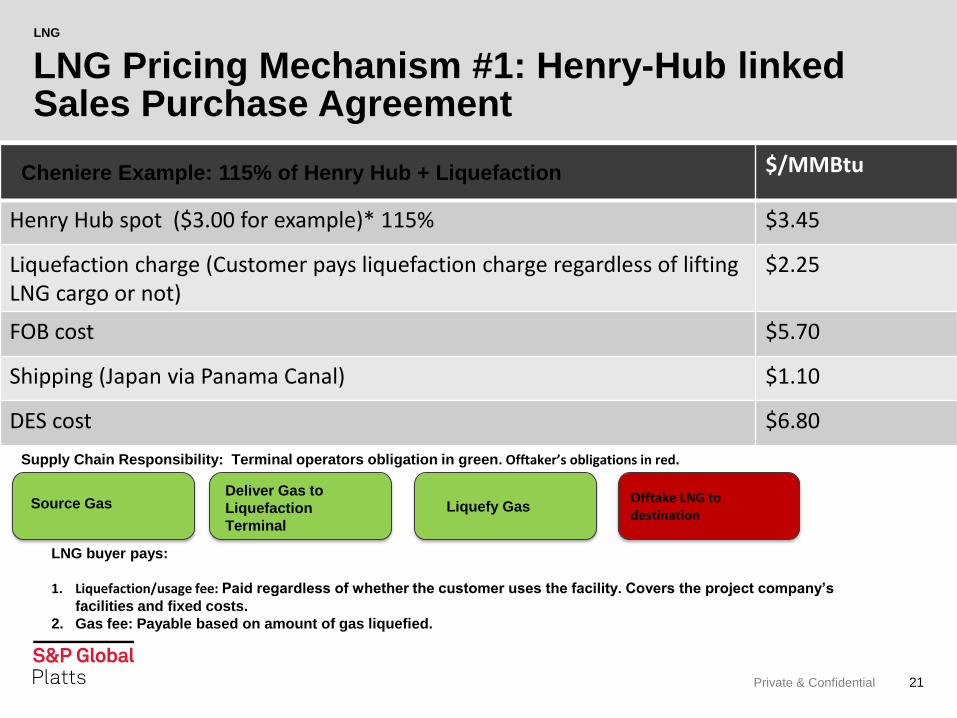

Private & Confidential 21

$/MMBtu

Henry Hub spot ($3.00 for example)* 115% $3.45

Liquefaction charge (Customer pays liquefaction charge regardless of lifting LNG cargo or not)

$2.25

FOB cost $5.70

Shipping (Japan via Panama Canal) $1.10

DES cost $6.80

LNG Pricing Mechanism #1: Henry-Hub linked Sales Purchase Agreement

Cheniere Example: 115% of Henry Hub + Liquefaction

LNG

Supply Chain Responsibility: Terminal operators obligation in green. Offtaker’s obligations in red.

Source Gas Deliver Gas to

Liquefaction

Terminal

Liquefy Gas Offtake LNG to destination

LNG buyer pays:

1. Liquefaction/usage fee: Paid regardless of whether the customer uses the facility. Covers the project company’s

facilities and fixed costs.

2. Gas fee: Payable based on amount of gas liquefied.

No content below the line No content below the line

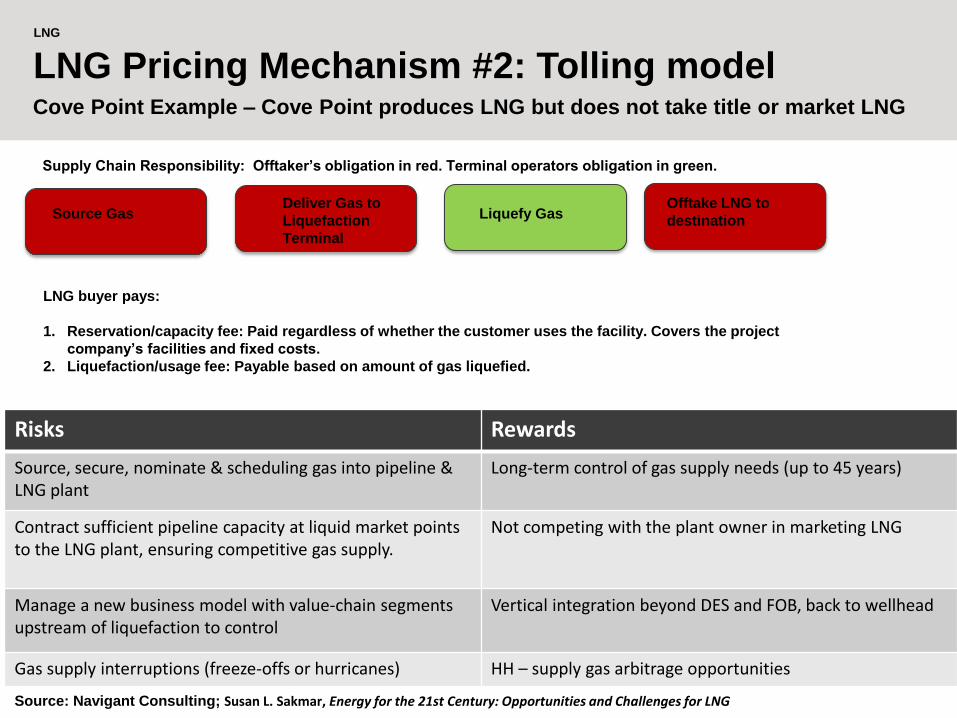

LNG Pricing Mechanism #2: Tolling model

Private & Confidential 22

Cove Point Example – Cove Point produces LNG but does not take title or market LNG

LNG

Risks Rewards

Source, secure, nominate & scheduling gas into pipeline & LNG plant

Long-term control of gas supply needs (up to 45 years)

Contract sufficient pipeline capacity at liquid market points to the LNG plant, ensuring competitive gas supply.

Not competing with the plant owner in marketing LNG

Manage a new business model with value-chain segments upstream of liquefaction to control

Vertical integration beyond DES and FOB, back to wellhead

Gas supply interruptions (freeze-offs or hurricanes) HH – supply gas arbitrage opportunities

Supply Chain Responsibility: Offtaker’s obligation in red. Terminal operators obligation in green.

Source Gas Deliver Gas to

Liquefaction

Terminal

Liquefy Gas Offtake LNG to

destination

LNG buyer pays:

1. Reservation/capacity fee: Paid regardless of whether the customer uses the facility. Covers the project

company’s facilities and fixed costs.

2. Liquefaction/usage fee: Payable based on amount of gas liquefied.

Source: Navigant Consulting; Susan L. Sakmar, Energy for the 21st Century: Opportunities and Challenges for LNG

No content below the line No content below the line

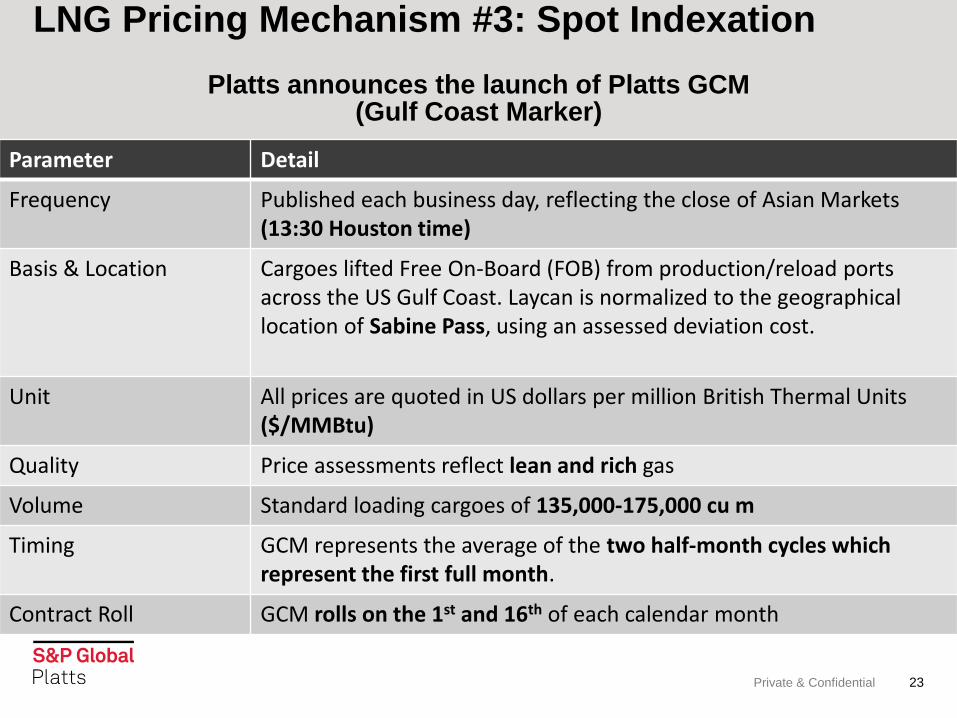

Platts announces the launch of Platts GCM

(Gulf Coast Marker)

Private & Confidential 23

LNG Pricing Mechanism #3: Spot Indexation

Parameter Detail

Frequency Published each business day, reflecting the close of Asian Markets (13:30 Houston time)

Basis & Location Cargoes lifted Free On-Board (FOB) from production/reload ports across the US Gulf Coast. Laycan is normalized to the geographical location of Sabine Pass, using an assessed deviation cost.

Unit All prices are quoted in US dollars per million British Thermal Units ($/MMBtu)

Quality Price assessments reflect lean and rich gas

Volume Standard loading cargoes of 135,000-175,000 cu m

Timing GCM represents the average of the two half-month cycles which represent the first full month.

Contract Roll GCM rolls on the 1st and 16th of each calendar month

No content below the line No content below the line

Natural Gas

Edit Footer in Headers & Footers 24

GCM currently a “netback” assessment

Freight Rates $/MMBtu

Japan/Korea South China/Taiwan

West India

SW Europe NW Europe

Argentina

Brazil

US Gulf Coast (Most Economic)

$1.09 $1.29 $1.19 $0.46 $0.46 $0.63 $0.50

Shipping rates of August 25, 2016

No content below the line No content below the line

Natural Gas

25

Continuous Pricing and Market Coverage

• As each market closes, information is passed onto the next desk in the following time-zone,

allowing for continuous price and market data gathering

• Allows for wider survey of market participants; portfolio players, traders, end-users etc..

Houston:

Gulf Coast

marker

assessed

at 13:30;

LNG Daily

published;

intel sent to

Singapore/

Tokyo

London: Atlantic

markers assessed

at 16:30; intel sent

to Houston Singapore: Platts

JKM™ and West

India assessed at

16:30; intel sent to

London

Source: Platts Analytics’ Eclipse Data, IGU, IEA, CIA World Fact Book

No content below the line No content below the line

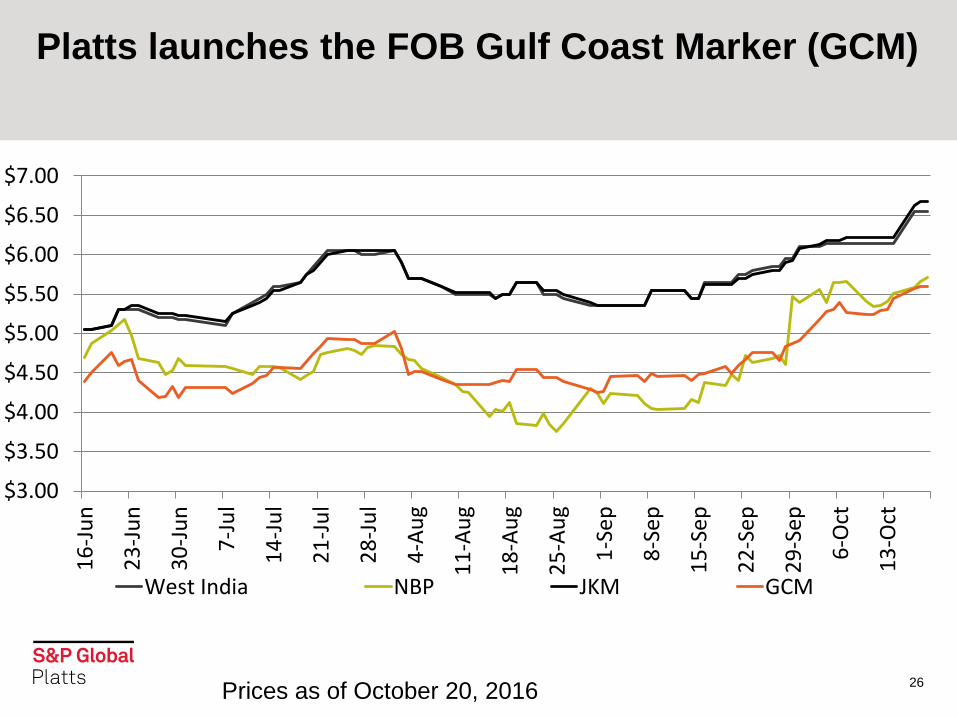

26

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

16

-Ju

n

23

-Ju

n

30

-Ju

n

7-J

ul

14

-Ju

l

21

-Ju

l

28

-Ju

l

4-A

ug

11

-Au

g

18

-Au

g

25

-Au

g

1-S

ep

8-S

ep

15

-Sep

22

-Sep

29

-Sep

6-O

ct

13

-Oct

West India NBP JKM GCM

Prices as of October 20, 2016

Platts launches the FOB Gulf Coast Marker (GCM)

No content below the line No content below the line

Future LNG pricing mechanisms

Private & Confidential 27

- Up to 43% of total global LNG deliveries could be traded on a spot/short-

term basis by 2020, versus around 25% today

No content below the line No content below the line

Thank You Chris Pedersen Pricing Analyst – LNG Americas Managing Editor – LNG Daily S&P Global Platts [email protected]