10

1Q16 Results Conference Call April 29 th , 2016 – 11:00 am (BrT) 10:00 am (NY)/ 3:00 pm (London)

| Date post: | 13-Apr-2017 |

| Category: |

Investor Relations |

| Upload: | cia-hering-ri |

| View: | 263 times |

| Download: | 0 times |

1Q16 Results Conference Call

April 29th, 2016 – 11:00 am (BrT) 10:00 am (NY)/ 3:00 pm (London)

1Q16 Results

DISCLAIMER

This presentation contains forward-looking statements regarding the

prospects of the business, estimates for operating and financial

results, and those regarding Cia. Hering's growth prospects. These are

merely projections and, as such, are based exclusively on the

expectations of Cia. Hering management concerning the future of the

business and its continued access to capital to fund the Company’s

business Plan. Such forward-looking statements depend, substantially,

on changes in market conditions, government regulations,

competitive pressures, the performance of the Brazilian economy and

the industry, among other factors and risks disclosed in Cia. Hering’s

filed disclosure documents and are, therefore, subject to change

without prior notice.

• Financial Performance

• SAP Implementation

• Outlook

• Q&A

2

FINANCIAL PERFORMANCE

GROSS REVENUES AND BREAKDOWN BY BRAND

R$ MILLION

1Q16 1Q15 Change

367.0 405.8 -9.5%

274.6 302.6 -9.2%

45.5 44.9 1.3%

26.0 32.3 -19.7%

14.3 20.9 -31.6%

6.7 5.2 30.3% International

Market

GROSS REVENUES BREAKDOWN PER CHANNEL

DOMESTIC MARKET EX-OTHER REVENUES

1Q16, R$ MILLION – CHANGE 1Q16 X 1Q15

Gross Revenue of R$ 376.1 million in 1Q16, impacted by

both franchise and multibrand performance.

3

HERING STORE NETWORK

GROSS SALES

SELL-OUT, R$ MILLION

Gross revenues of R$ 281.5 million (- 4.8%), reflecting consumer

traffic reduction at the stores and lower number of visits, partially

offset by the net opening of 7 stores LTM.

¹ Stores opened in the last twelve months net from closings.

STORE REFURBISHMENT PLAN

• Company’s Incentive Plan

• More than 80 stores adhesions to date

• 05 stores renovated in 1Q16

Pátio Savassi Mall – MG State

4

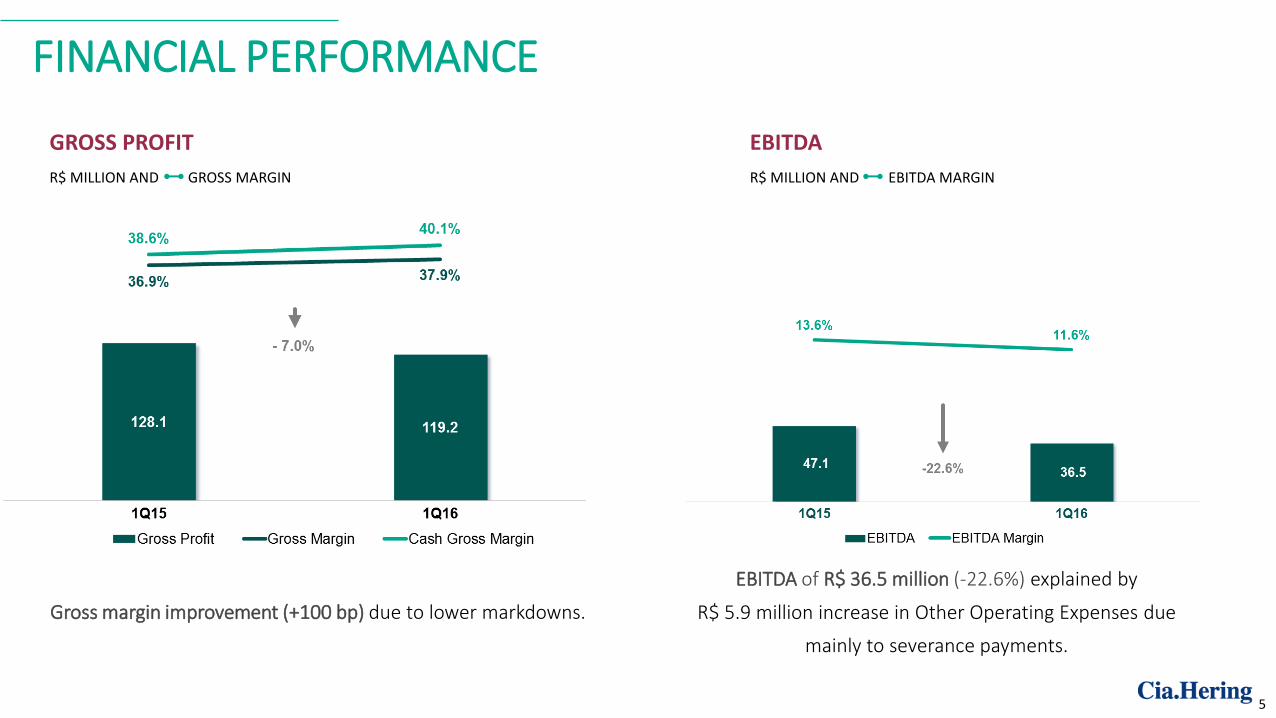

FINANCIAL PERFORMANCE

EBITDA of R$ 36.5 million (-22.6%) explained by

R$ 5.9 million increase in Other Operating Expenses due

mainly to severance payments.

Gross margin improvement (+100 bp) due to lower markdowns.

GROSS PROFIT

R$ MILLION AND GROSS MARGIN

EBITDA

R$ MILLION AND EBITDA MARGIN

5

FINANCIAL PERFORMANCE

NET INCOME

R$ MILLION AND NET MARGIN

CAPEX

R$ MILLION

Retraction coming from lower operating income, partially offset by

lower effective income tax rate.

Lower investments in Industrial Plants (after the launch of

manufacturing plant and DC expansion and modernization in Goiás)

and in IT (conclusion of SAP implementation extension to logistics,

invoicing and ordering process). 6

FINANCIAL PERFORMANCE

Cash flow of R$ 101.6 million, R$ 34.2 million higher than 1Q15, due to a

reduce in working capital needs, notably in inventories, and lower investments.

CASH FLOWS

R$ MILLION

Cash Flow - Consolidated 1Q16 1Q15 Chg.

EBITDA 36,491 47 ,141 (10,650)

No cash items 3,612 12,047 (8,435)

AVP (Adjustment to Present Value) - Clients and Suppliers 5,712 4,975 737

Current Income tax and Social Contribution (3,795) (7,638) 3,843

Working Capital Capex 65,448 24 ,917 40 ,531

Decrease in trade accounts receivable 123,202 117,014 6,188

(Increase) in inventories (10,378) (41,342) 30,964

(Decrease) in accounts payable to suppliers (37,329) (22,955) (14,374)

(Decrease) in taxes payable (6,580) (17,352) 10,772

Refurbishment Project 2016 - Franchisee Financing 2,680 - 2,680

Others (6,147) (10,448) 4,301

CapEx (5 ,834) (13 ,959) 8 ,125

Free Cash Flow 101,634 67,483 34 ,151

7

SAP IMPLEMENTATION

Implementation, without disruptions, to logistic, invoicing and ordering process’ areas

‘Go-Live’ with assisted operation during the month

Operation normalization, but still monitored by the project team

Project closure, with operations conducted by the company normally

Jan

Mar

Feb

8

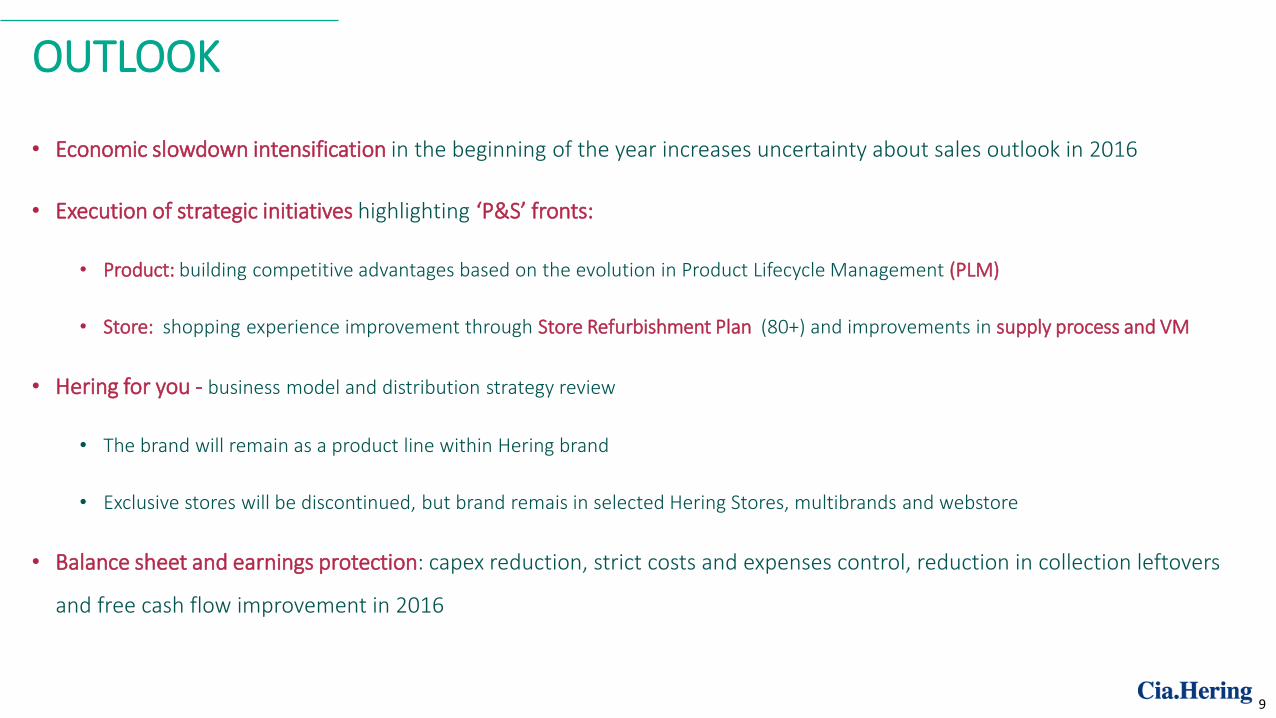

OUTLOOK

• Economic slowdown intensification in the beginning of the year increases uncertainty about sales outlook in 2016

• Execution of strategic initiatives highlighting ‘P&S’ fronts:

• Product: building competitive advantages based on the evolution in Product Lifecycle Management (PLM)

• Store: shopping experience improvement through Store Refurbishment Plan (80+) and improvements in supply process and VM

• Hering for you - business model and distribution strategy review

• The brand will remain as a product line within Hering brand

• Exclusive stores will be discontinued, but brand remais in selected Hering Stores, multibrands and webstore

• Balance sheet and earnings protection: capex reduction, strict costs and expenses control, reduction in collection leftovers

and free cash flow improvement in 2016

9

Fabio Hering – CEO Frederico Oldani – CFO and IRO

Bruno Salem Brasil – IR Manager Caroline Luccarini – IR Analyst

www.ciahering.com.br/ir +55 (11) 3371 – 4867/4805

INVESTOR RELATIONS TEAM