1 Date:_______4/24/13________ Analyst:_____Kyle Temple ________ CIF Sector Recommendation Report (Fall 2012) Sector _____Technology___________ Review Period________4/8-4/19 ______________ Section (A) Sector Performance Review During the review period of 4/8/13 to 4/19/13 the technology sector greatly underperformed the market by 1.38%. This was mostly due to the sell off the sector saw on the last two trading days of the review period. Some of the largest holdings in the sector ETF such as Apple, IBM, and AT&T all were down big the last few days of the review period, bringing down the entire technology sector with them. It is currently earnings season, and the technology sector looks to be in a very volatile stage as some major companies are reported misses while others are beating analyst estimates. Domestic sales and Asia exposure have been fairly stable for companies so far, with much focus on the recession on Europe. The market will look to digest a few more earnings reports from the likes of Apple and Qualcomm before it settles in one direction. Being a very cyclical and volatile sector, the technology sector could see greater declines than the overall market if there is a market correction in the near future. 4/8- 4/19 TECH Ticker Current Beg. Stop-loss Target % Cap # Shares Current vs. Sector vs. S&P 500 Price Price Price Price Gain Value S&P 500 $INX 1555.25 1552.67 0.17% Sector ETF XLK $29.35 $29.71 -1.21% 8430 $247,420.50 -1.38% Current Holdings CSCO 20.46 $ 20.69 $ $19.50 $24.00 -1.11% 1940 $39,692.40 0.10% -1.28% V 163.96 $ 165.64 $ 150.00 $ 185.15 $ -1.01% 290 $47,548.40 0.20% -1.18% SNDK 52.31 $ 54.76 $ 47.00 $ 62.79 $ -4.47% 260 $13,600.60 -3.26% -4.64% Sold 4/18 EMC 22.35 24.66 -9.30% The rest of the spreadsheet is calculated automatically Please read "Sector Review Guidelines" document carefully Cougar Investment Fund Sector Review Spreadsheet Template Please download and save this template to your own storage device You only need to input values to cells highlighted in "yellow"

Cougar Investment Fund Sector Review Spreadsheet Template

Please download and save this template to your own storage device

You only need to input values to cells highlighted in "yellow"

2

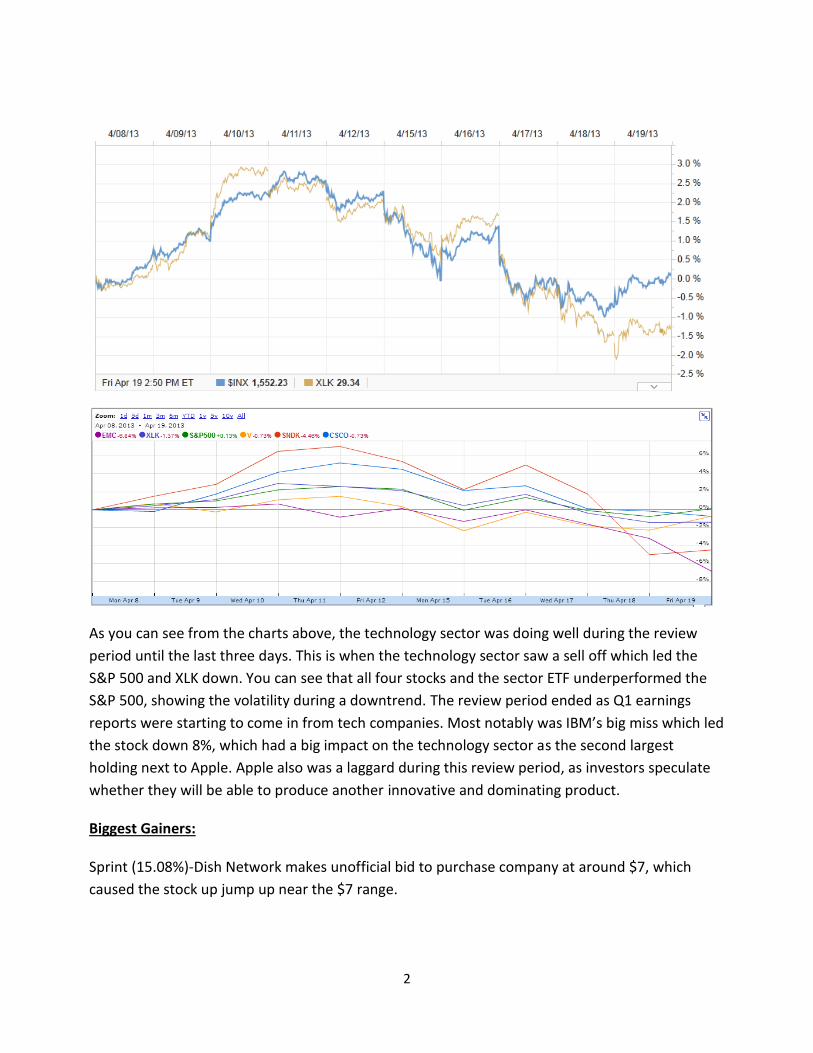

As you can see from the charts above, the technology sector was doing well during the review

period until the last three days. This is when the technology sector saw a sell off which led the

S&P 500 and XLK down. You can see that all four stocks and the sector ETF underperformed the

S&P 500, showing the volatility during a downtrend. The review period ended as Q1 earnings

reports were starting to come in from tech companies. Most notably was IBM’s big miss which led

the stock down 8%, which had a big impact on the technology sector as the second largest

holding next to Apple. Apple also was a laggard during this review period, as investors speculate

whether they will be able to produce another innovative and dominating product.

Biggest Gainers:

Sprint (15.08%)-Dish Network makes unofficial bid to purchase company at around $7, which

caused the stock up jump up near the $7 range.

3

Intel (7.16%)- Intel announced earnings on 4/16 meeting analyst expectations. The stock rose

after management reiterated revenue expectations for the year.

Verizon (5.42%)- Verizon announced earnings on 4/18 beating EPS estimates and matching

revenue expectations. Investors were impressed with VZ’s ability to get customers on data plans.

Biggest Losers:

HPQ(-10.97%)- The stock had been trending down ever since a report came out that person

computer sales were at the lowest level in almost 20 years. Investors are worried HPQ will not be

able to adapt to these market trends. The company was also dragged down by negative earnings

news from companies like IBM.

IBM (-9.26%)- On 4/18 IBM posted quarterly earnings and suffered a big miss. Management

blamed the falling yen in Japan, slowing hardware sales, and a lack of closing major deals in the

U.S. and Europe as the key problems.

Apple (-7.71%)- Apple has continued the downward trend as investors are anticipating more bad

news when they report 4/24. Macbook sales are down, and investors are worried that Apple is

slowly losing its loyal consumer base to competitors such as Samsung.

Largest Holders:

Apple (13.21%)- Apple is easily the largest holding in the technology sector with 13.21% of the weight.

Unfortunately for the tech sector ETF, Apple had been on a free fall recently going from over $700 to

dipping below $400 just this week. Investors are having a hard time picturing the future for the company,

especially with the amount of cash it has been holding on to. Investors are also worried that CEO Tim Cook

does not have the innovative vision that Steve Jobs had which led to Apple’s market dominance. Since Tim

Cook took over, the iPhone is no longer considered the best phone on the market like it was for many

years. On top of this the iPad has seen growing competition from companies like Microsoft and Samsung.

Lastly, Apple’s MacBook sales have also seen decreasing sales as consumers are spending money on smart

phone’s and tablets. Consumers wait as Apple decides what is going to be the new product they want to

launch. Apple announces earnings on 4/24 on what should be a very important day for the entire

technology sector.

IBM ( 7.62%)- IBM is the second largest stock in the technology sector and had been performing well until

just recently when they announced earnings. The company dropped over 8% after a big miss caught Wall

Street by surprise. The hardware segment has been slowing down for IBM, which also had an impact on

companies like EMC. The report wasn’t all bad, with the company’s service segment growing, which

accounted for around 60% of revenue.

4

Short-term Outlook:

The short-term outlook for the technology sector looks neutral. As earnings season is kicking off,

there were mixed results from major technology companies. Companies like Google and

Microsoft reporting good numbers, while other large companies like IBM have reported negative

news. The market will be paying close attention to upcoming reports of companies like Apple and

AT&T. These earnings could determine the future for the technology sector. Also due to the

recent bull run of the market, any correction could have a greater impact on the volatile

technology sector.

Section (B) Sector Holding Updates

Company #1: EMC Corp EMC

Date Recommended: 02/03/2013

Date Re-evaluated: 04/18/2013

Company Update

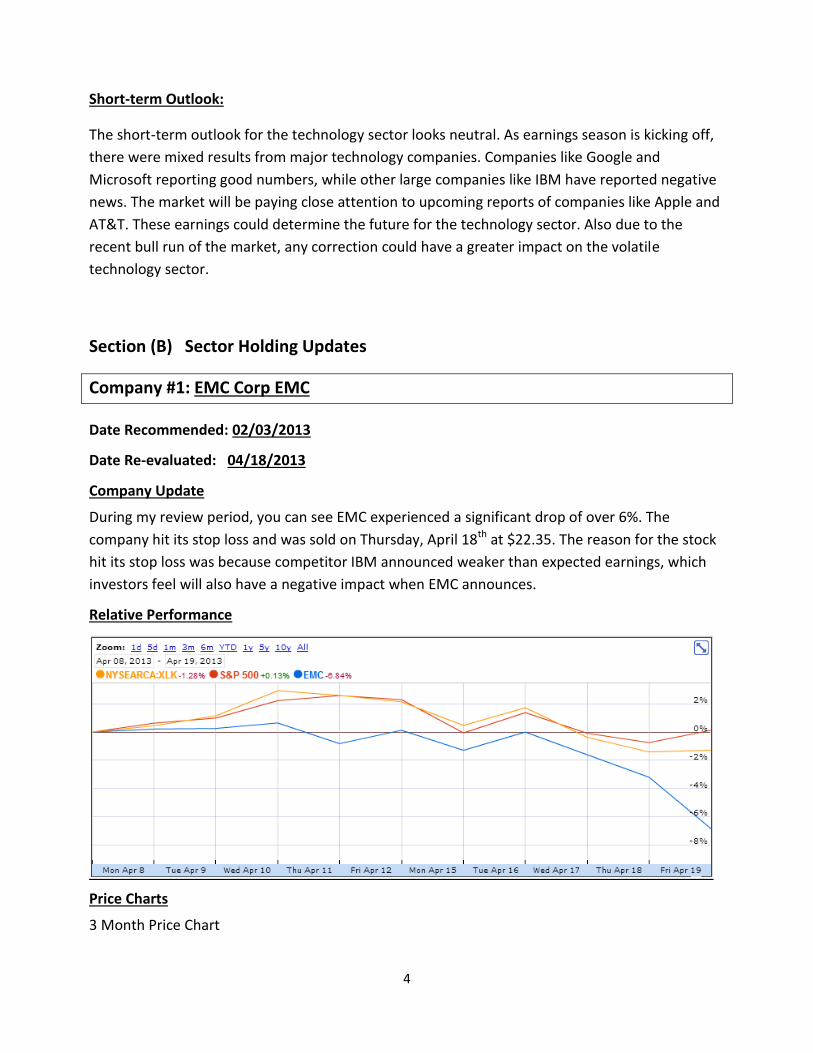

During my review period, you can see EMC experienced a significant drop of over 6%. The

company hit its stop loss and was sold on Thursday, April 18th at $22.35. The reason for the stock

hit its stop loss was because competitor IBM announced weaker than expected earnings, which

investors feel will also have a negative impact when EMC announces.

Relative Performance

Price Charts

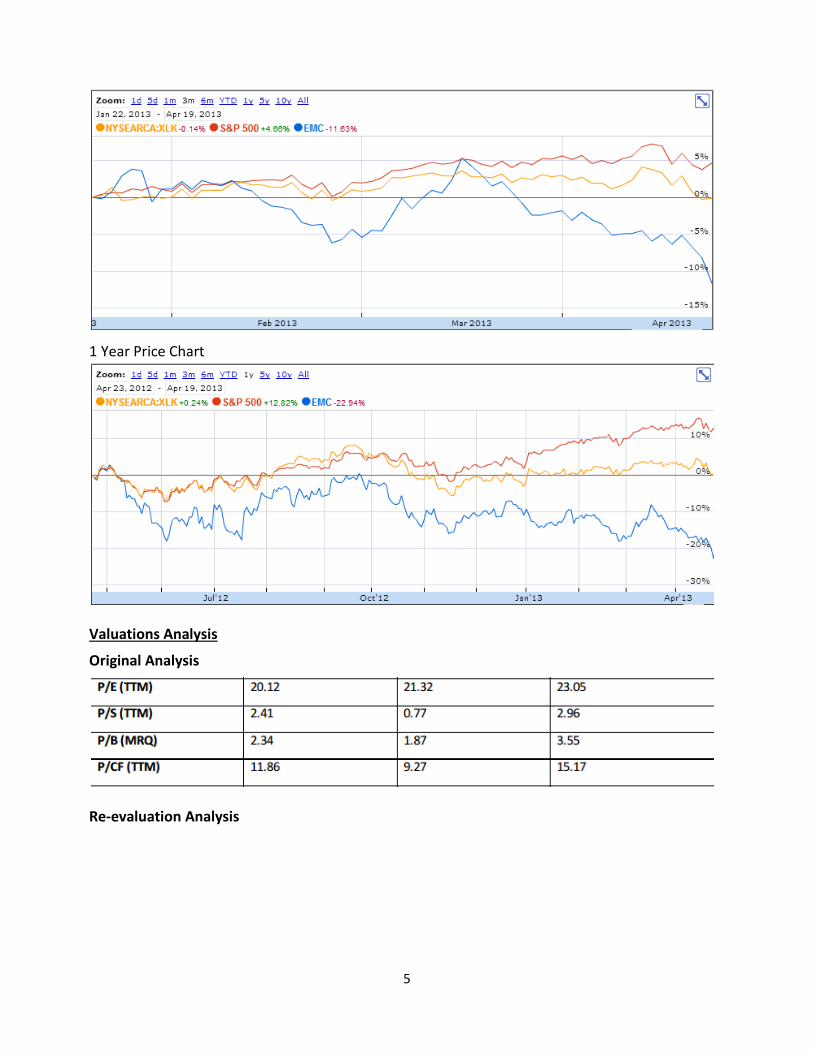

3 Month Price Chart

5

1 Year Price Chart

Valuations Analysis

Original Analysis

Re-evaluation Analysis

6

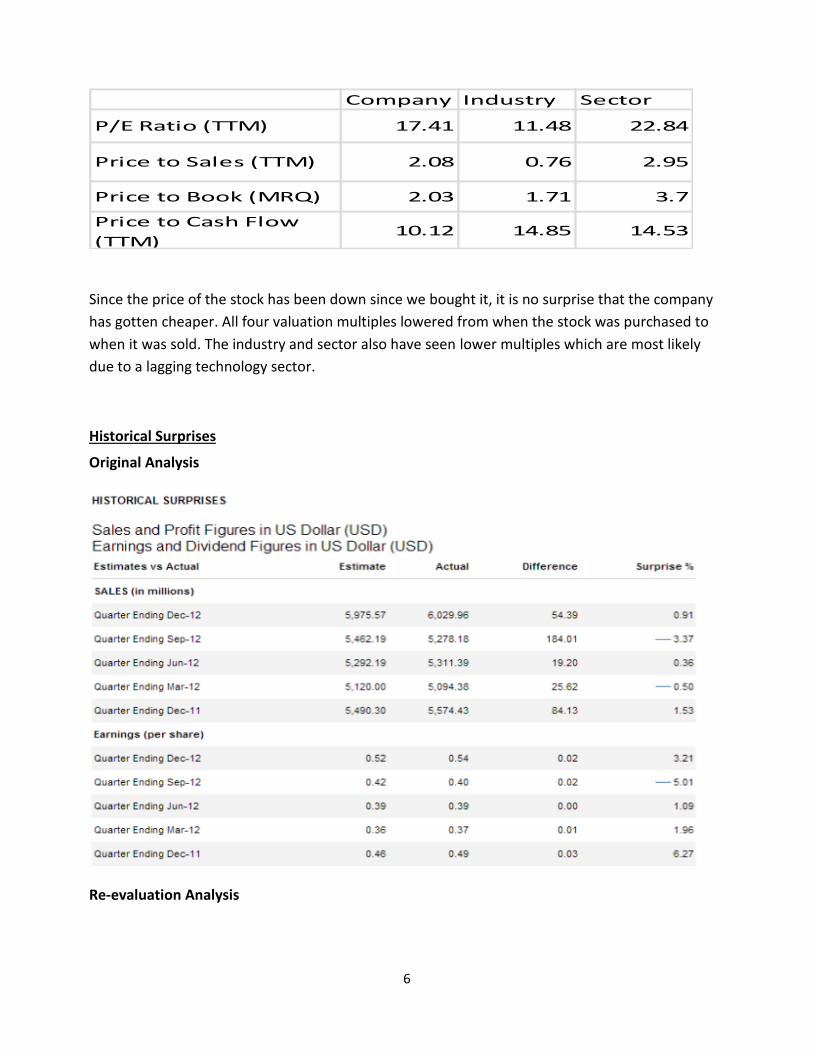

Since the price of the stock has been down since we bought it, it is no surprise that the company

has gotten cheaper. All four valuation multiples lowered from when the stock was purchased to

when it was sold. The industry and sector also have seen lower multiples which are most likely

due to a lagging technology sector.

Historical Surprises

Original Analysis

Re-evaluation Analysis

Company Industry Sector

P/E Ratio (TTM) 17.41 11.48 22.84

Price to Sales (TTM) 2.08 0.76 2.95

Price to Book (MRQ) 2.03 1.71 3.7

Price to Cash Flow

(TTM)10.12 14.85 14.53

7

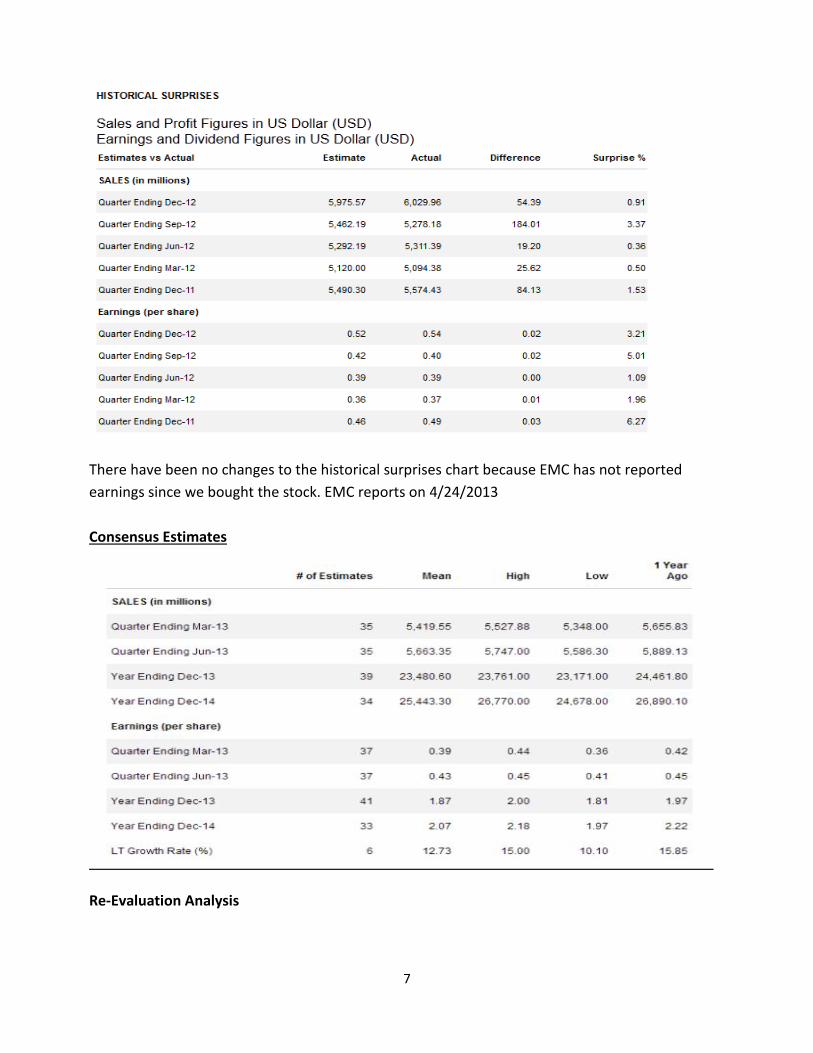

There have been no changes to the historical surprises chart because EMC has not reported

earnings since we bought the stock. EMC reports on 4/24/2013

Consensus Estimates

Re-Evaluation Analysis

8

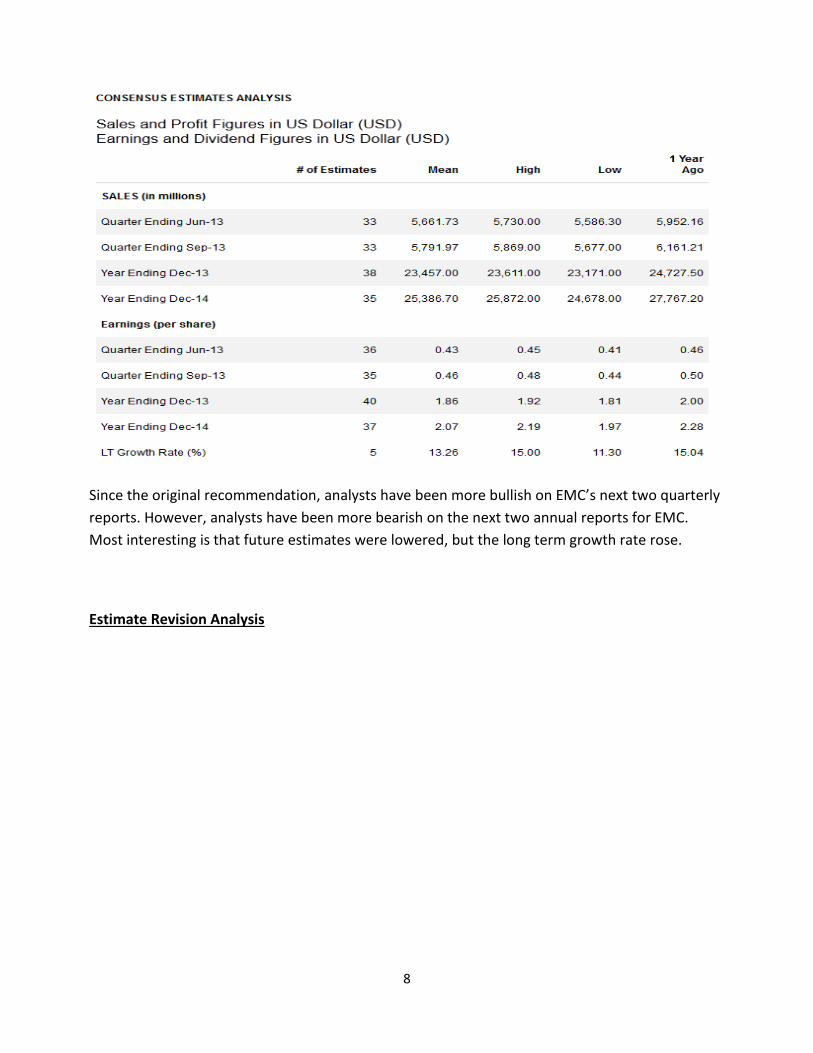

Since the original recommendation, analysts have been more bullish on EMC’s next two quarterly

reports. However, analysts have been more bearish on the next two annual reports for EMC.

Most interesting is that future estimates were lowered, but the long term growth rate rose.

Estimate Revision Analysis

9

Re-Evaluation Analysis

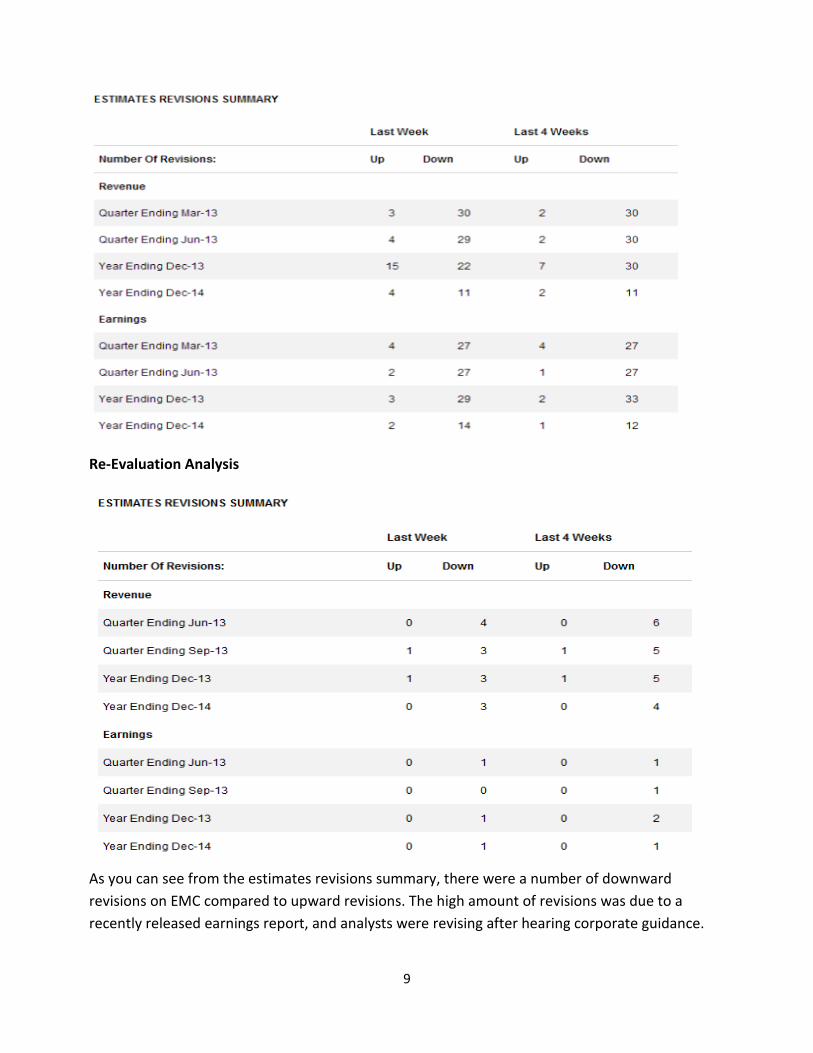

As you can see from the estimates revisions summary, there were a number of downward

revisions on EMC compared to upward revisions. The high amount of revisions was due to a

recently released earnings report, and analysts were revising after hearing corporate guidance.

10

Recently EMC has seen just a few downward revisions which are most likely due to IMB’s recent

miss.

Analysts’ Recommendations

Original Analysis

Re-Evaluation Analysis

11

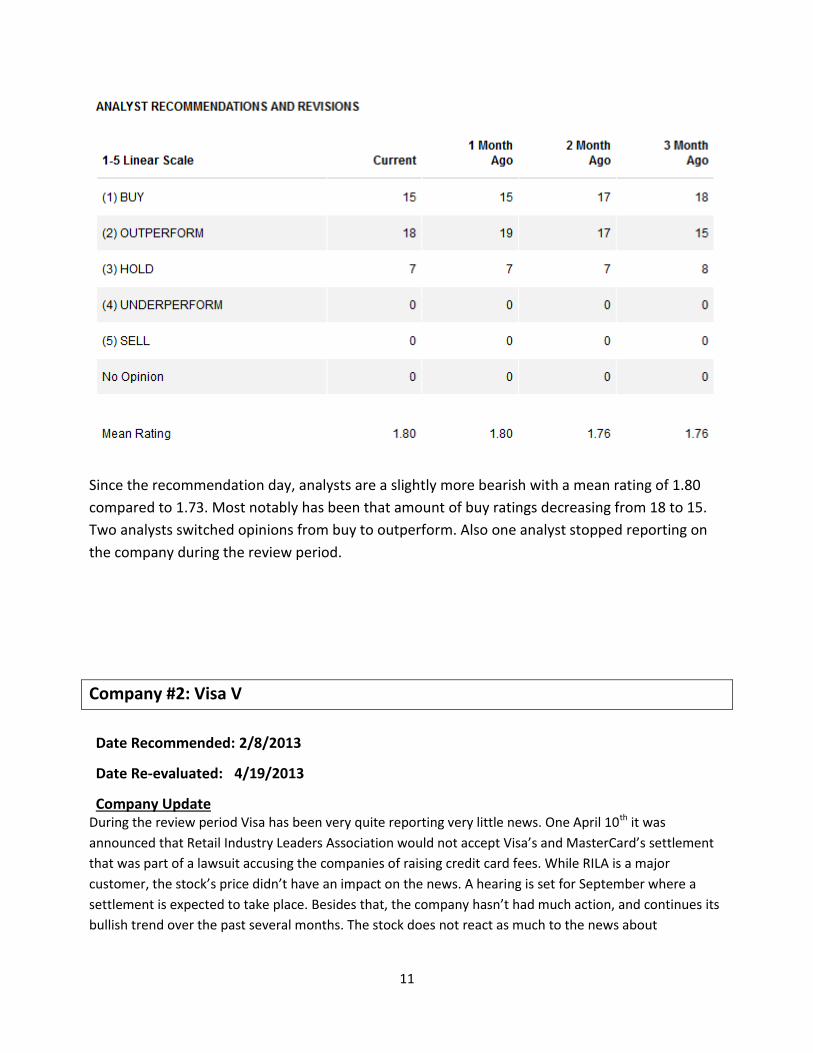

Since the recommendation day, analysts are a slightly more bearish with a mean rating of 1.80

compared to 1.73. Most notably has been that amount of buy ratings decreasing from 18 to 15.

Two analysts switched opinions from buy to outperform. Also one analyst stopped reporting on

the company during the review period.

Company #2: Visa V

Date Recommended: 2/8/2013

Date Re-evaluated: 4/19/2013

Company Update During the review period Visa has been very quite reporting very little news. One April 10th it was

announced that Retail Industry Leaders Association would not accept Visa’s and MasterCard’s settlement

that was part of a lawsuit accusing the companies of raising credit card fees. While RILA is a major

customer, the stock’s price didn’t have an impact on the news. A hearing is set for September where a

settlement is expected to take place. Besides that, the company hasn’t had much action, and continues its

bullish trend over the past several months. The stock does not react as much to the news about

12

technology leaders like Google and Apple because it is in a different industry. The company reports May

1st.

Relative Performance

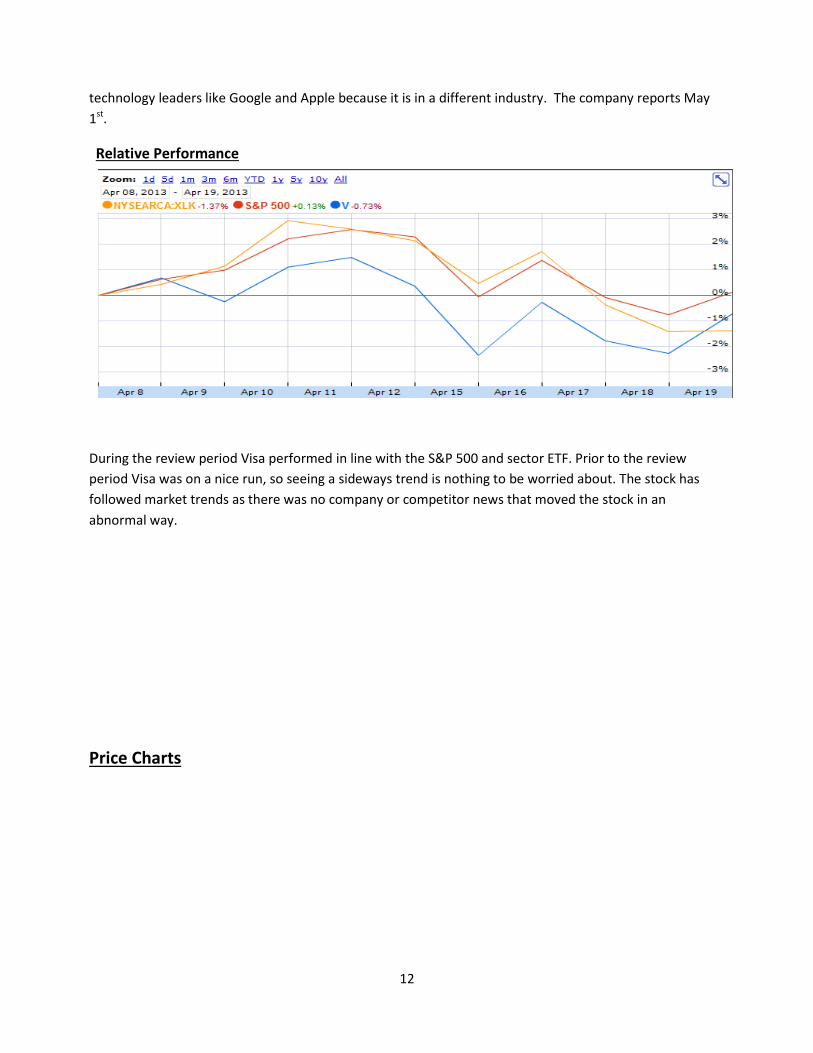

During the review period Visa performed in line with the S&P 500 and sector ETF. Prior to the review

period Visa was on a nice run, so seeing a sideways trend is nothing to be worried about. The stock has

followed market trends as there was no company or competitor news that moved the stock in an

abnormal way.

Price Charts

13

Valuations Analysis

Original Analysis

14

Re-evaluation Analysis

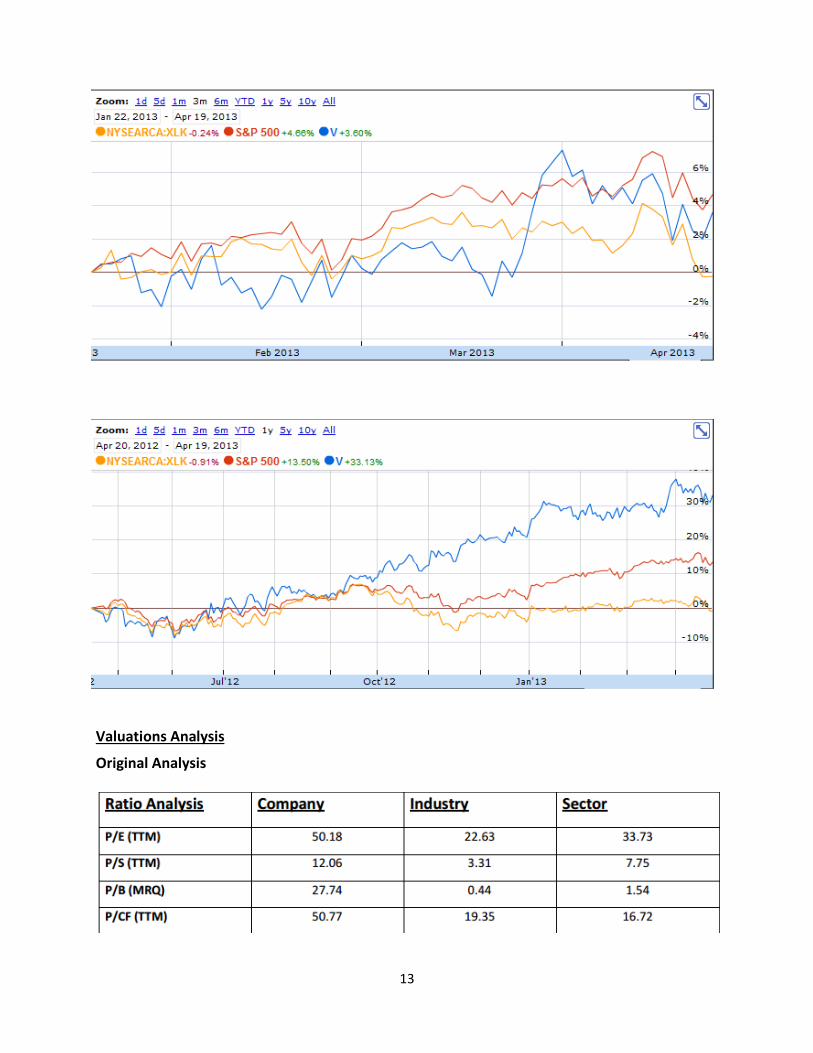

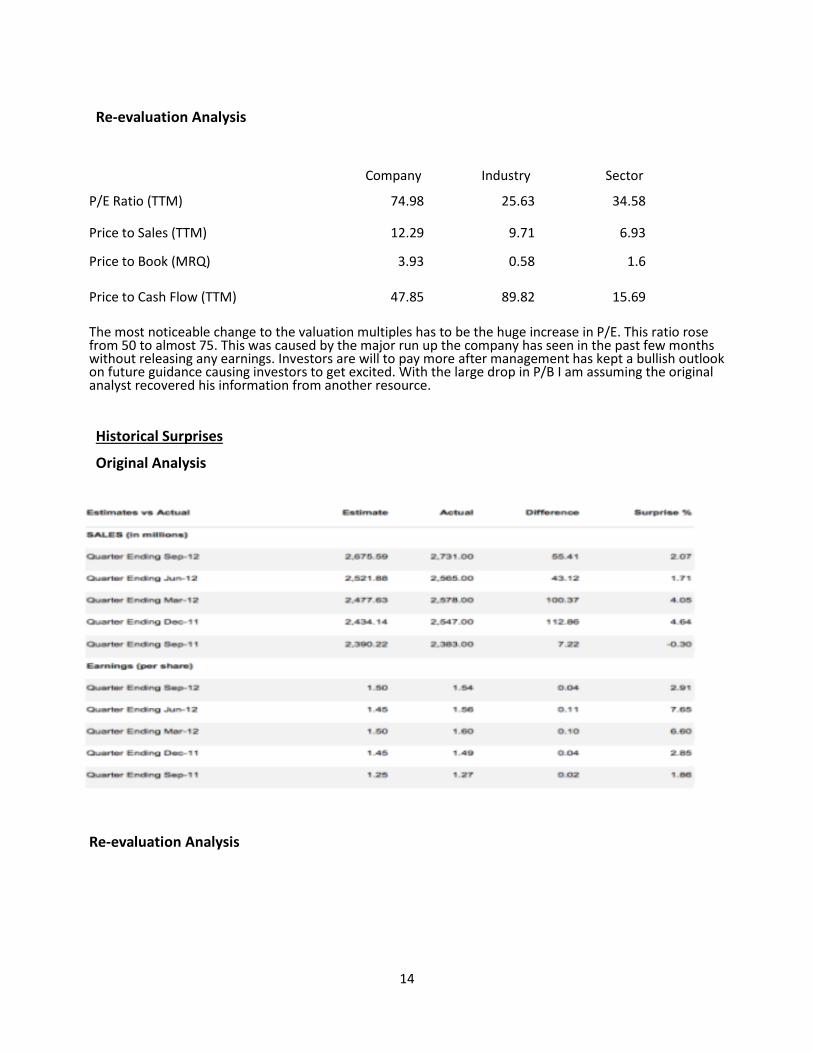

The most noticeable change to the valuation multiples has to be the huge increase in P/E. This ratio rose from 50 to almost 75. This was caused by the major run up the company has seen in the past few months without releasing any earnings. Investors are will to pay more after management has kept a bullish outlook on future guidance causing investors to get excited. With the large drop in P/B I am assuming the original analyst recovered his information from another resource.

Historical Surprises

Original Analysis

Re-evaluation Analysis

Company Industry Sector

P/E Ratio (TTM) 74.98 25.63 34.58

Price to Sales (TTM) 12.29 9.71 6.93

Price to Book (MRQ) 3.93 0.58 1.6

Price to Cash Flow (TTM) 47.85 89.82 15.69

15

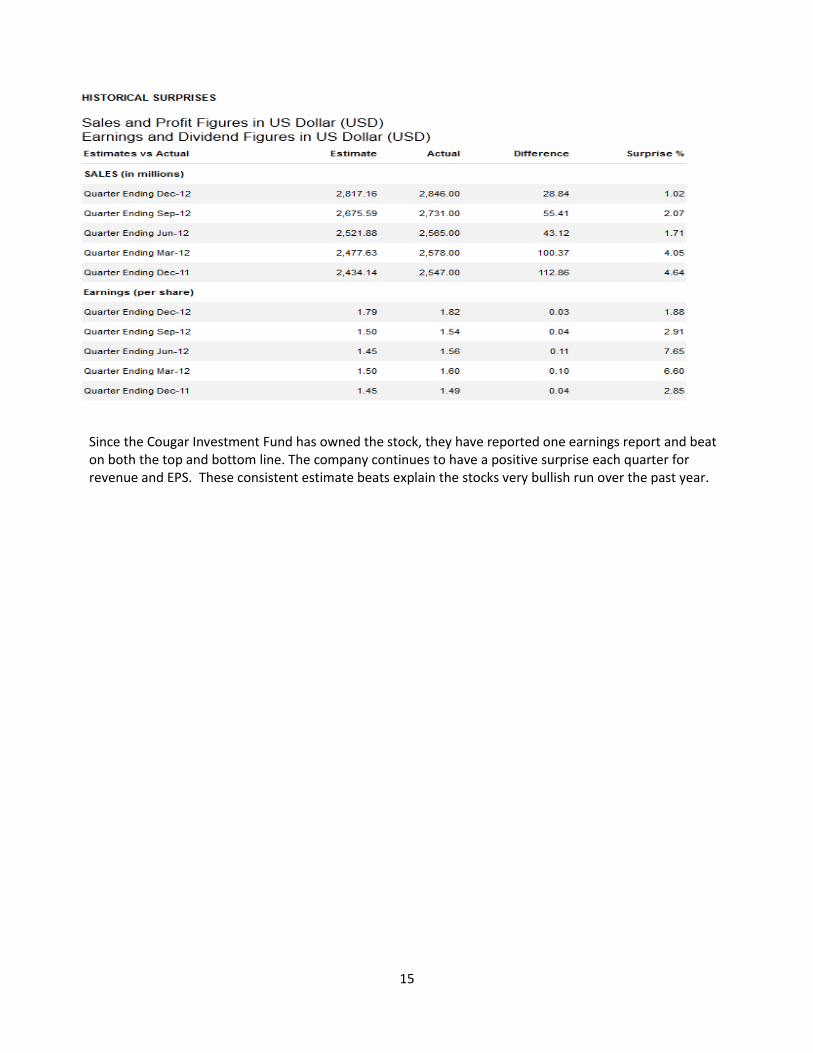

Since the Cougar Investment Fund has owned the stock, they have reported one earnings report and beat on both the top and bottom line. The company continues to have a positive surprise each quarter for revenue and EPS. These consistent estimate beats explain the stocks very bullish run over the past year.

16

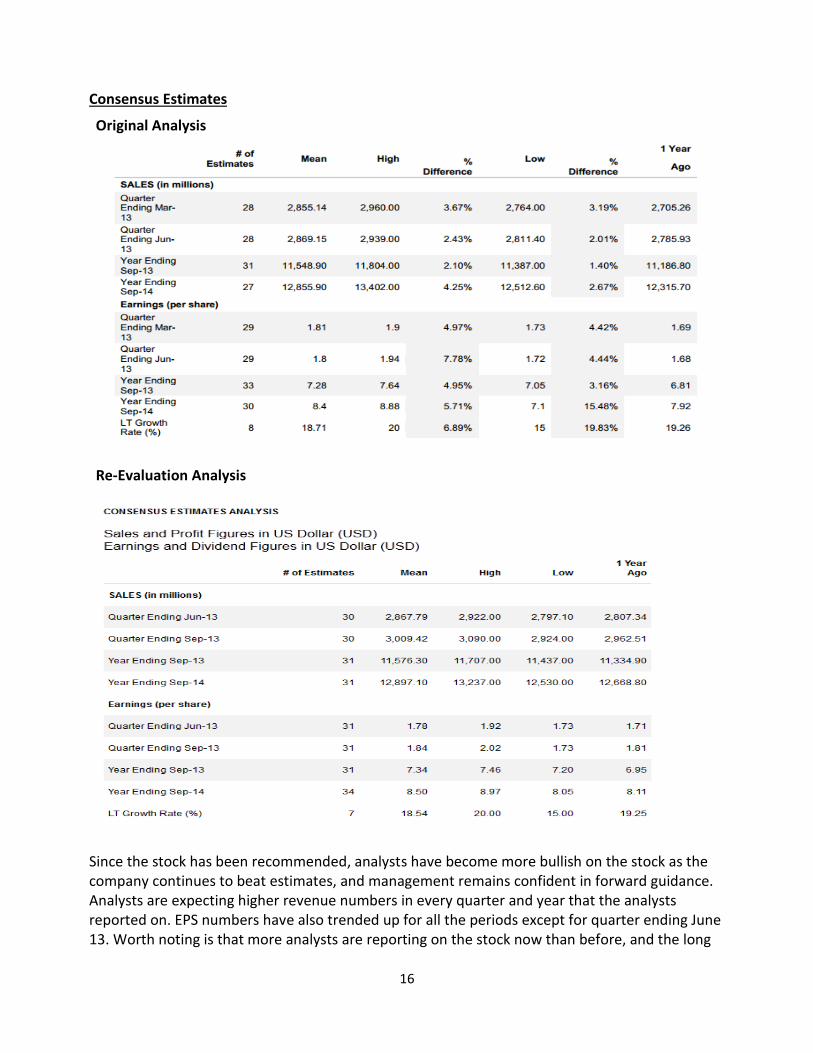

Consensus Estimates

Original Analysis

Re-Evaluation Analysis

Since the stock has been recommended, analysts have become more bullish on the stock as the company continues to beat estimates, and management remains confident in forward guidance. Analysts are expecting higher revenue numbers in every quarter and year that the analysts reported on. EPS numbers have also trended up for all the periods except for quarter ending June 13. Worth noting is that more analysts are reporting on the stock now than before, and the long

17

term growth rate slightly declined after an analyst stopped rating the company.

Estimate Revision Analysis

Original Analysis (2/8/2013

Re-Evaluation Analysis

18

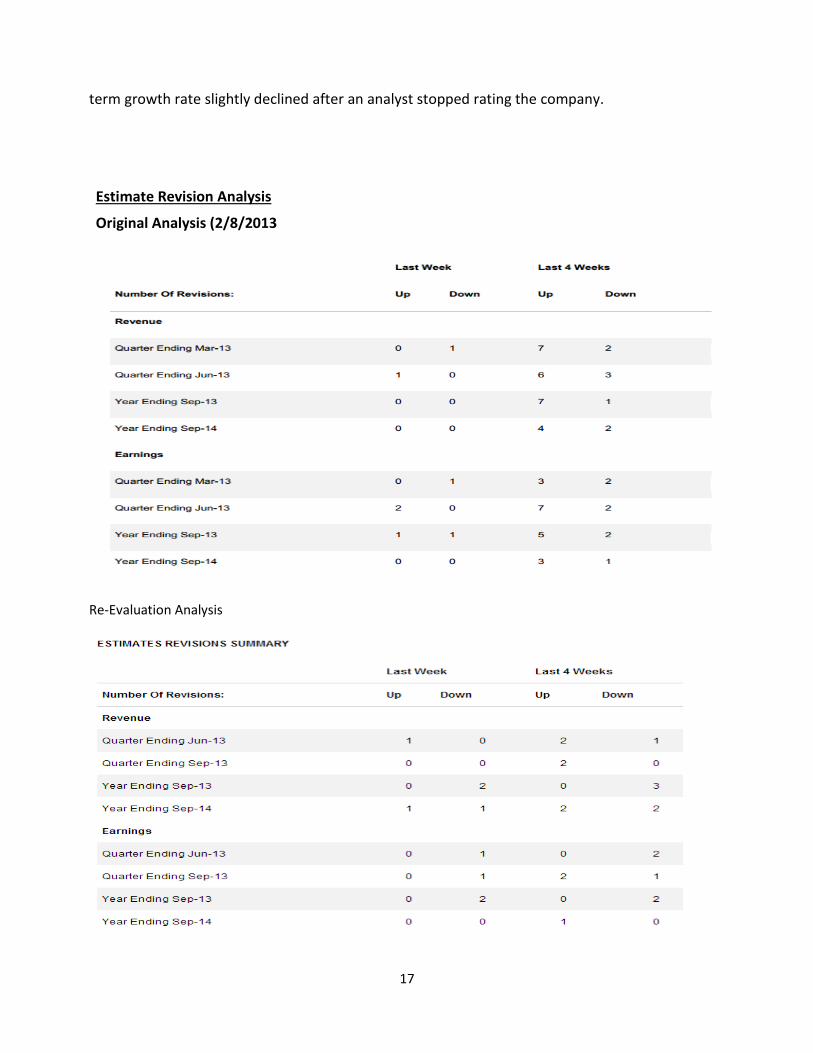

Recently there have been a few revisions for analysts. There doesn’t seem to be a set trend as some analysts are rising expectations while others are lowering guidance. The original estimate revision summary had a number of upward revisions after the company had announced earnings and future guidance. Analysts’ Recommendations

Original Analysis

Re-Evaluation Analysis

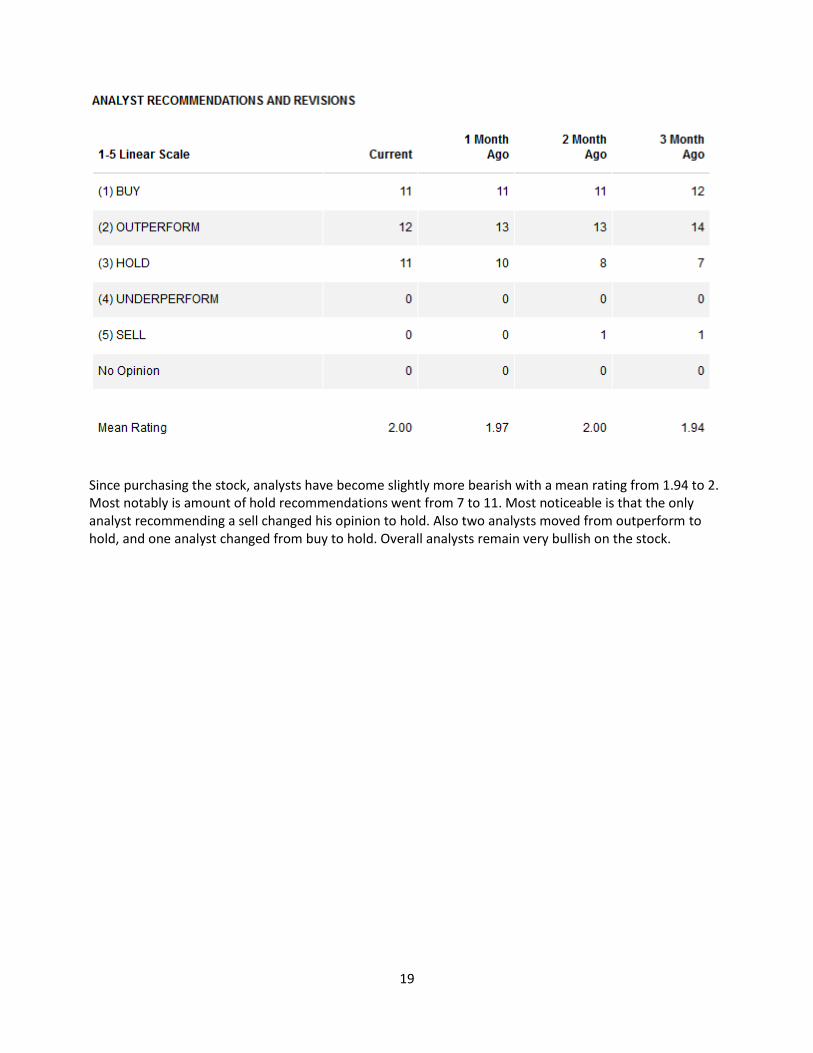

19

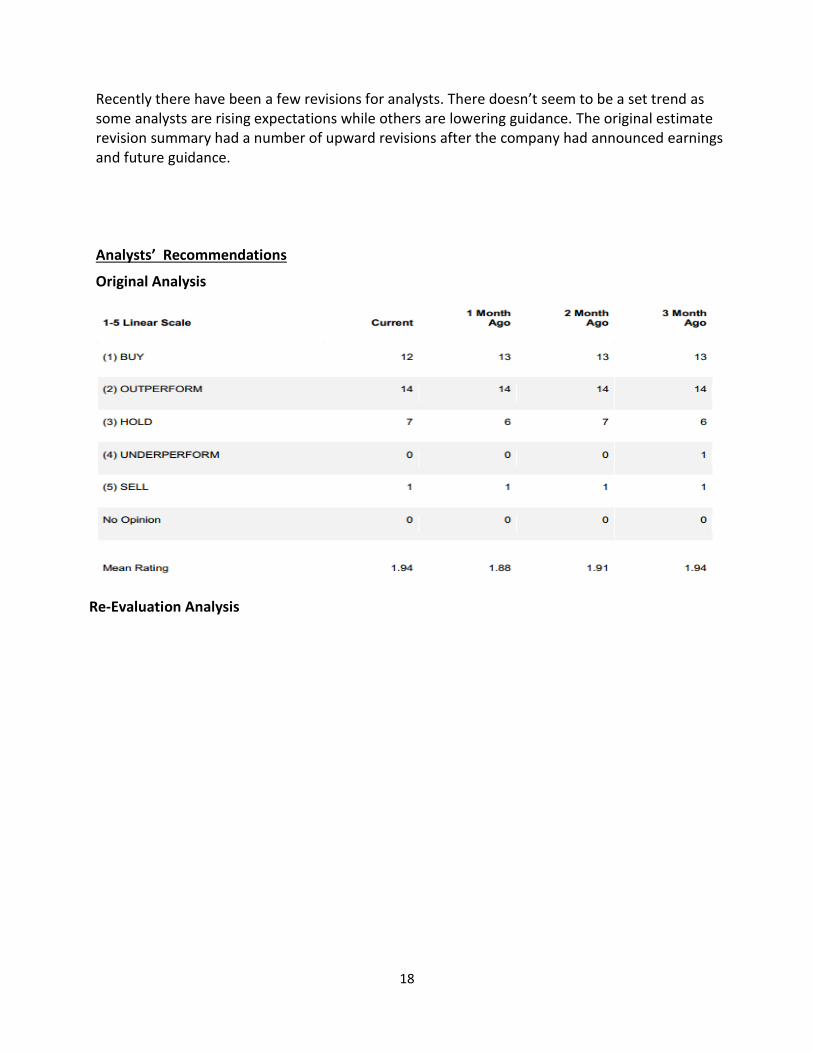

Since purchasing the stock, analysts have become slightly more bearish with a mean rating from 1.94 to 2. Most notably is amount of hold recommendations went from 7 to 11. Most noticeable is that the only analyst recommending a sell changed his opinion to hold. Also two analysts moved from outperform to hold, and one analyst changed from buy to hold. Overall analysts remain very bullish on the stock.

20

Company #3: Cisco Systems, Inc. (CSCO)

Date Recommended: 2/25/2013

Date Re-evaluated: 4/19/2013

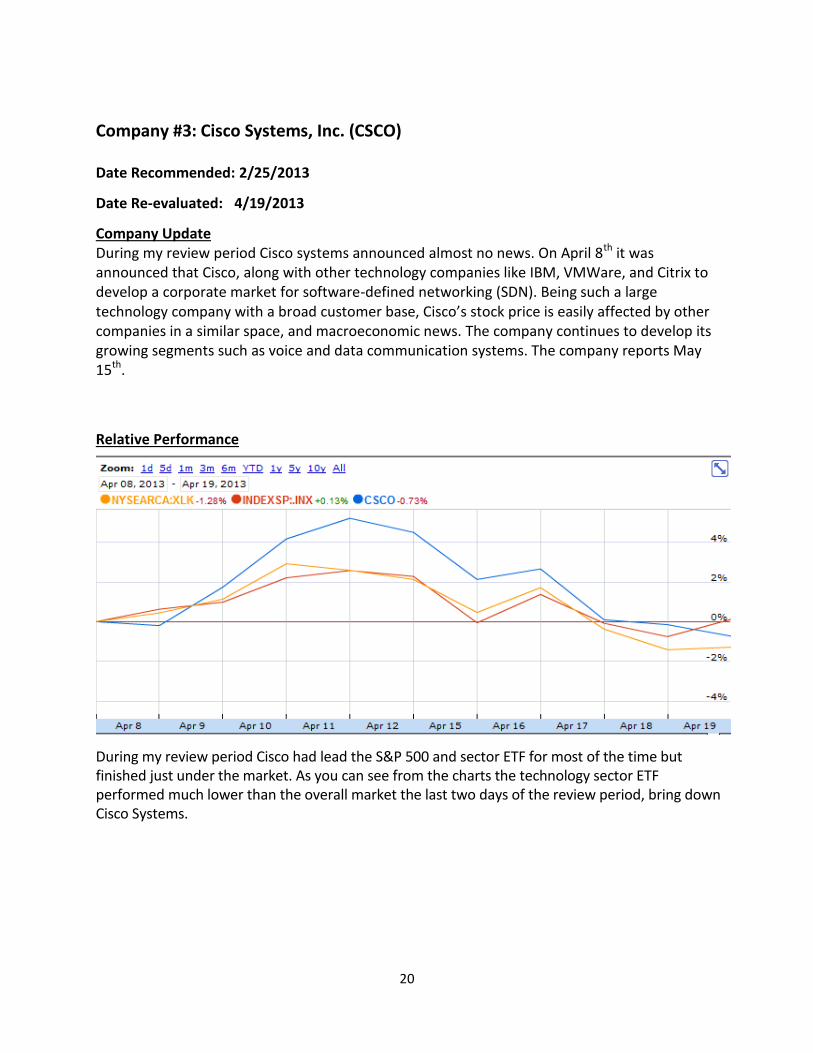

Company Update During my review period Cisco systems announced almost no news. On April 8th it was announced that Cisco, along with other technology companies like IBM, VMWare, and Citrix to develop a corporate market for software-defined networking (SDN). Being such a large technology company with a broad customer base, Cisco’s stock price is easily affected by other companies in a similar space, and macroeconomic news. The company continues to develop its growing segments such as voice and data communication systems. The company reports May 15th.

Relative Performance

During my review period Cisco had lead the S&P 500 and sector ETF for most of the time but finished just under the market. As you can see from the charts the technology sector ETF performed much lower than the overall market the last two days of the review period, bring down Cisco Systems.

21

Price Charts

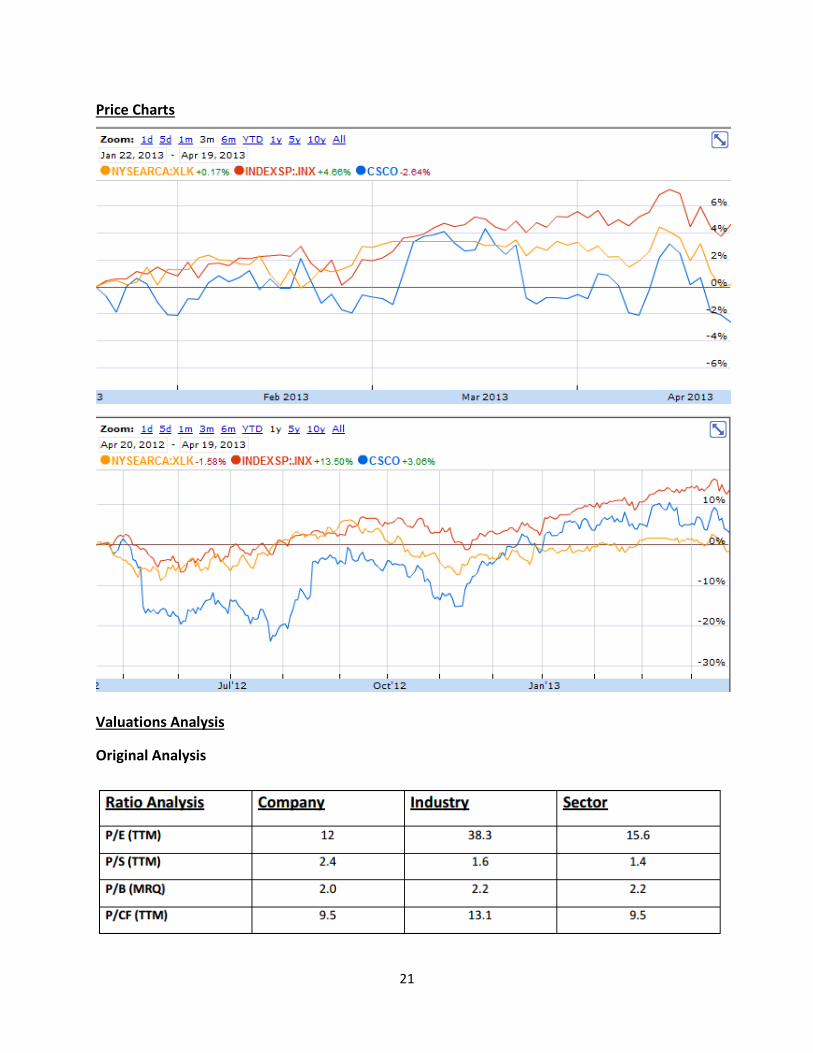

Valuations Analysis

Original Analysis

22

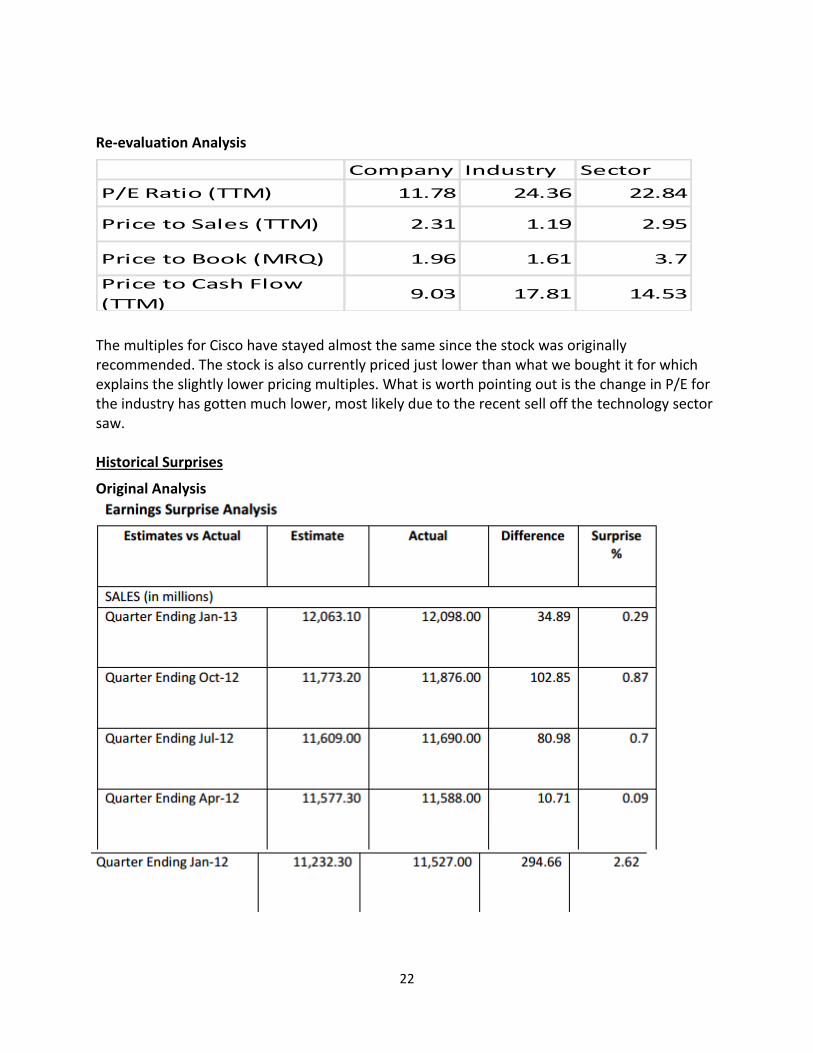

Re-evaluation Analysis

The multiples for Cisco have stayed almost the same since the stock was originally recommended. The stock is also currently priced just lower than what we bought it for which explains the slightly lower pricing multiples. What is worth pointing out is the change in P/E for the industry has gotten much lower, most likely due to the recent sell off the technology sector saw. Historical Surprises

Original Analysis

Company Industry Sector

P/E Ratio (TTM) 11.78 24.36 22.84

Price to Sales (TTM) 2.31 1.19 2.95

Price to Book (MRQ) 1.96 1.61 3.7

Price to Cash Flow

(TTM)9.03 17.81 14.53

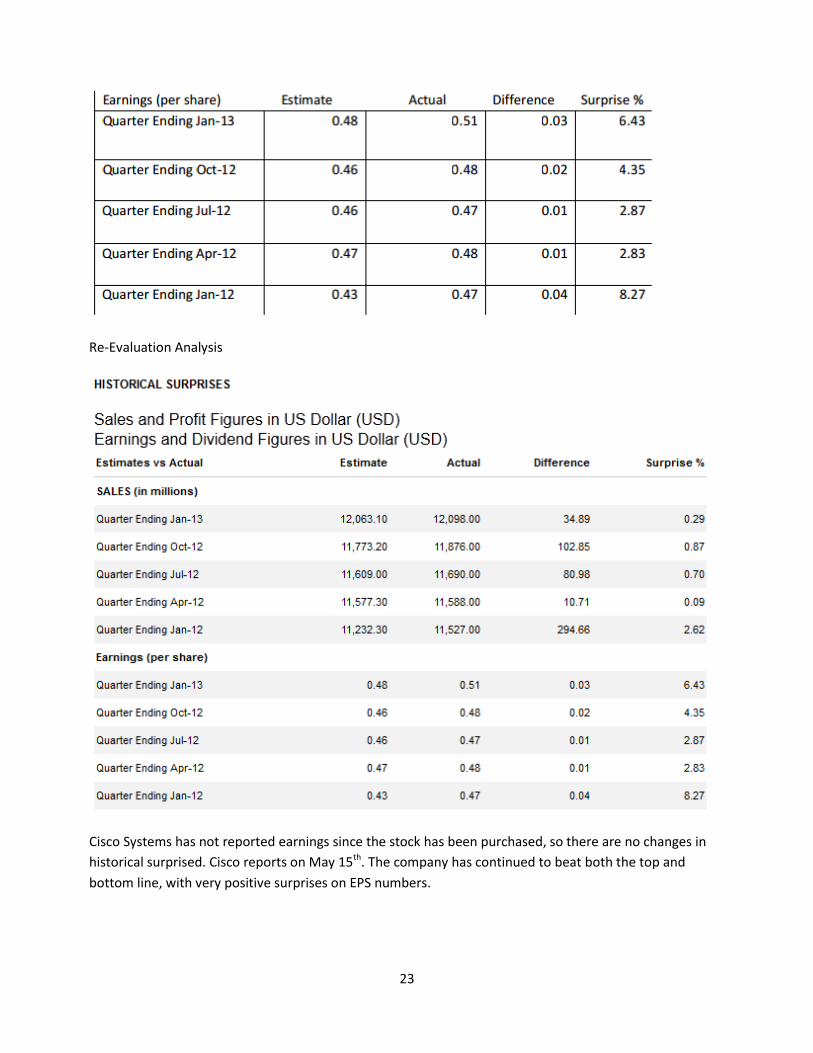

23

Re-Evaluation Analysis

Cisco Systems has not reported earnings since the stock has been purchased, so there are no changes in

historical surprised. Cisco reports on May 15th. The company has continued to beat both the top and

bottom line, with very positive surprises on EPS numbers.

24

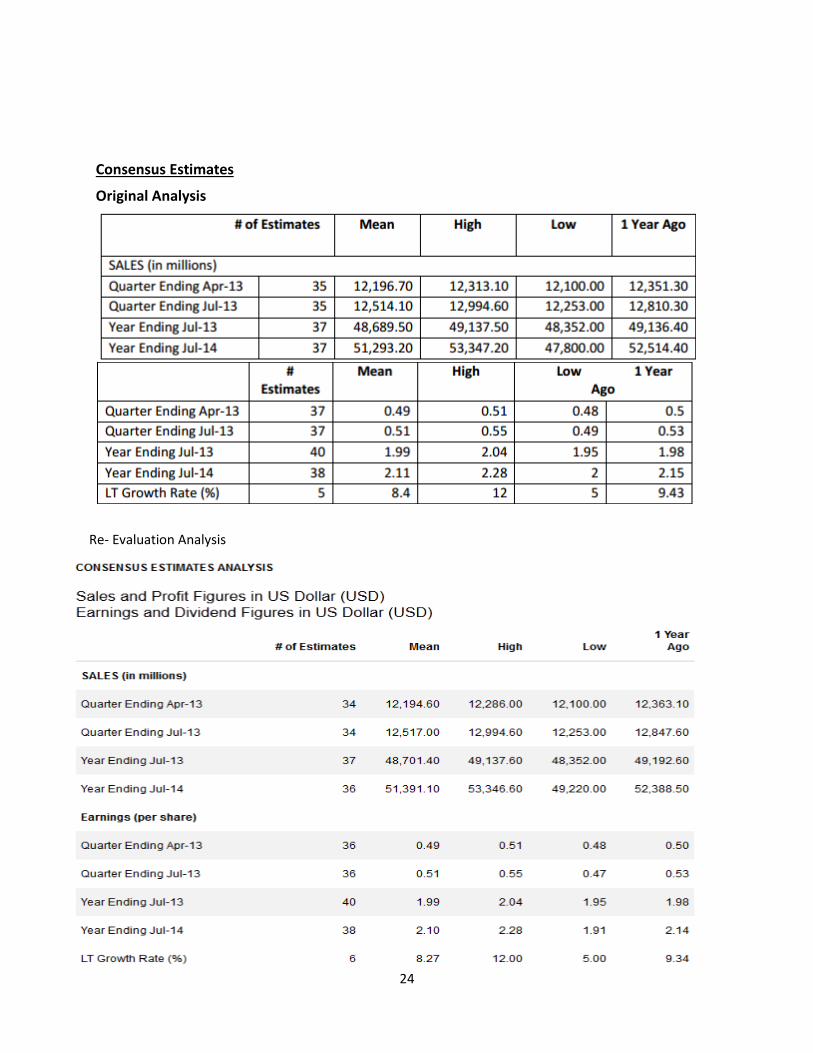

Consensus Estimates

Original Analysis

Re- Evaluation Analysis

25

Since the recommendation date, there have been no major changes in the consensus estimates analysis. Most notably is the upward revision for sales for fiscal year ending July 2014, however EPS estimates dropped a penny during that same period. The long term growth rate dropped slightly as one more analyst rated the stock since the recommendation. There are no real bearish or bullish changes when analyzing these numbers.

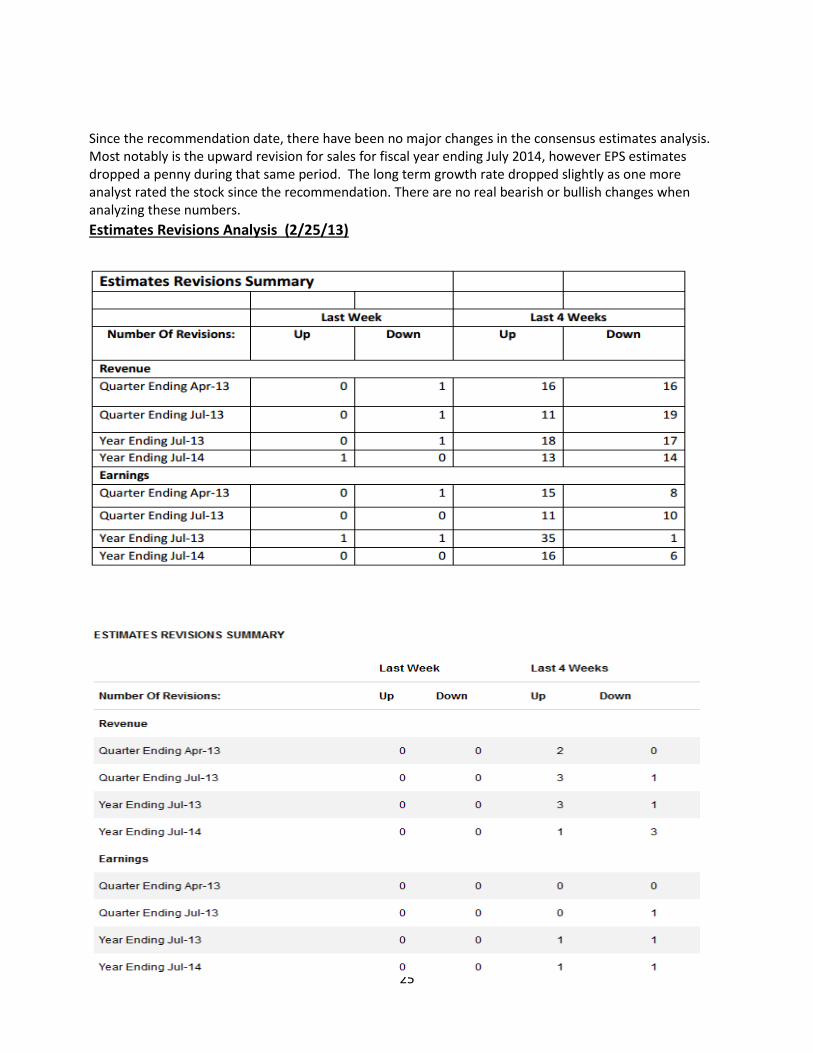

Estimates Revisions Analysis (2/25/13)

26

Over the past few weeks a few analysts have revised their opinions on the stock. There were both bullish and bearish changes in opinion, most notably 3 upward revenue revisions for fiscal year ending July 2013, however there were 3 downward revisions for revenue during fiscal year ending July 2014. When the stock was originally recommended there were many revisions because the company had just reported. At that time analysts seem mixed on future revenue numbers, but were bullish on the future EPS numbers of the company.

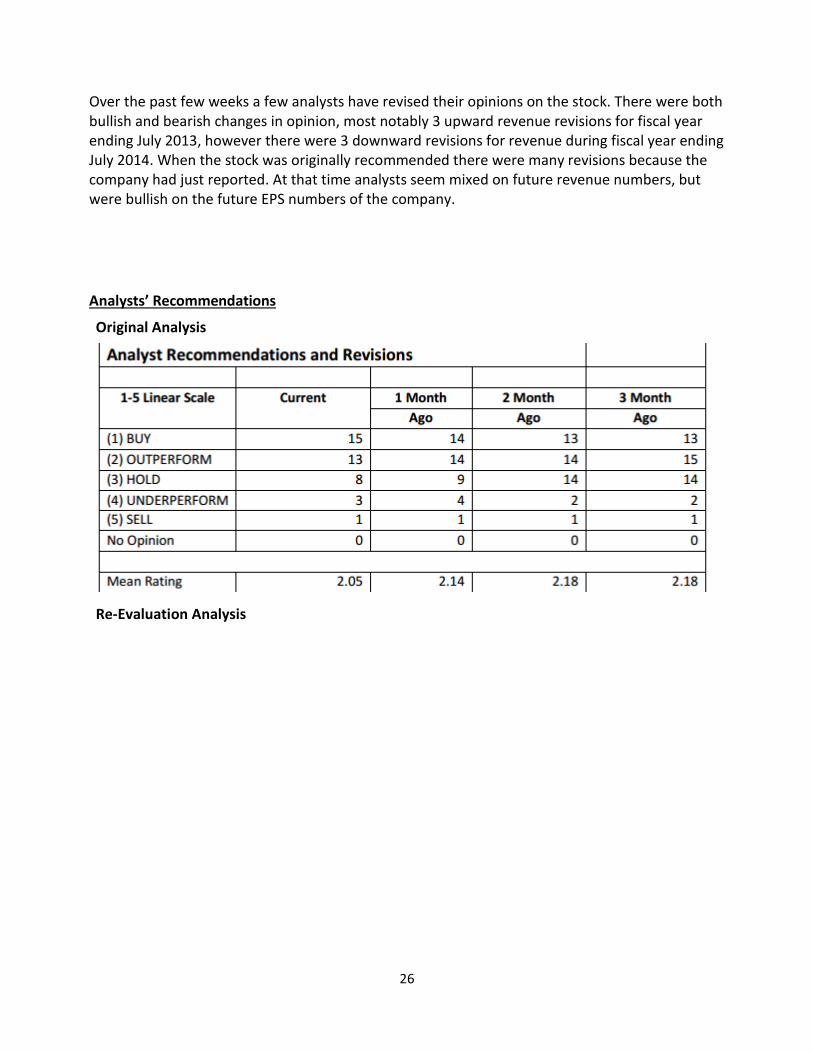

Analysts’ Recommendations

Original Analysis

Re-Evaluation Analysis

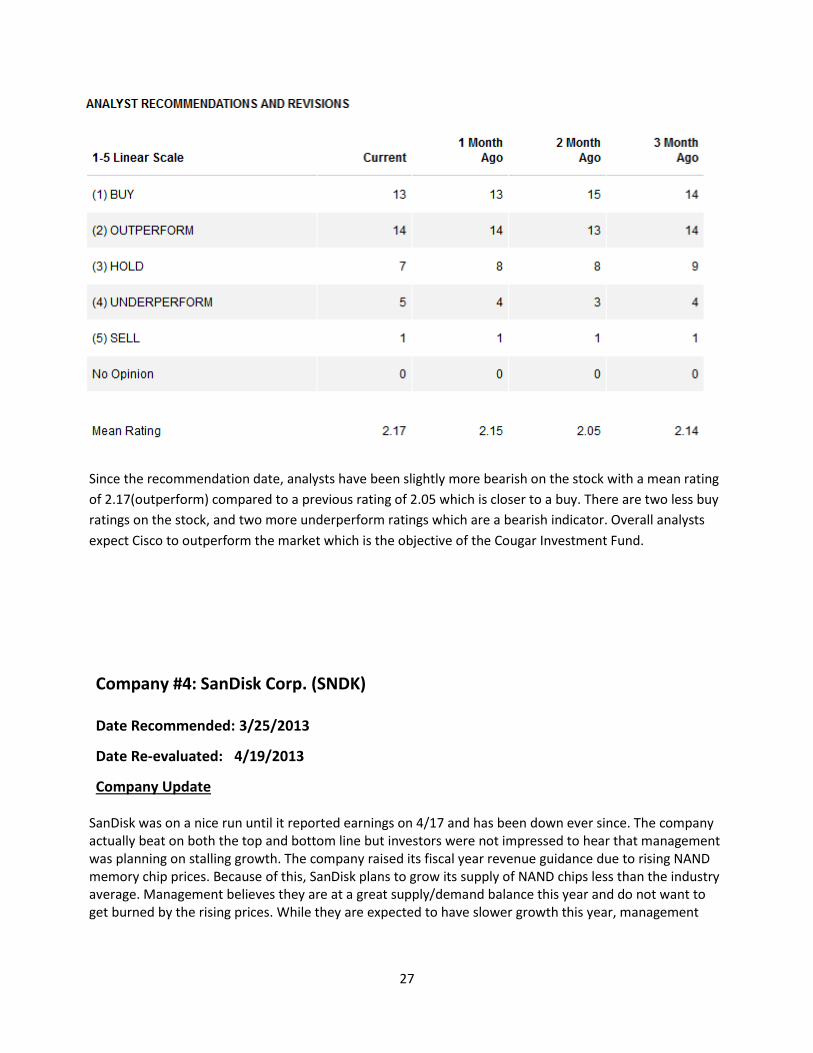

27

Since the recommendation date, analysts have been slightly more bearish on the stock with a mean rating

of 2.17(outperform) compared to a previous rating of 2.05 which is closer to a buy. There are two less buy

ratings on the stock, and two more underperform ratings which are a bearish indicator. Overall analysts

expect Cisco to outperform the market which is the objective of the Cougar Investment Fund.

Company #4: SanDisk Corp. (SNDK)

Date Recommended: 3/25/2013

Date Re-evaluated: 4/19/2013

Company Update SanDisk was on a nice run until it reported earnings on 4/17 and has been down ever since. The company actually beat on both the top and bottom line but investors were not impressed to hear that management was planning on stalling growth. The company raised its fiscal year revenue guidance due to rising NAND memory chip prices. Because of this, SanDisk plans to grow its supply of NAND chips less than the industry average. Management believes they are at a great supply/demand balance this year and do not want to get burned by the rising prices. While they are expected to have slower growth this year, management

28

noted their impressive growth last year and believes they are still in a good position to capitalize on a highly growing market.

Relative Performance

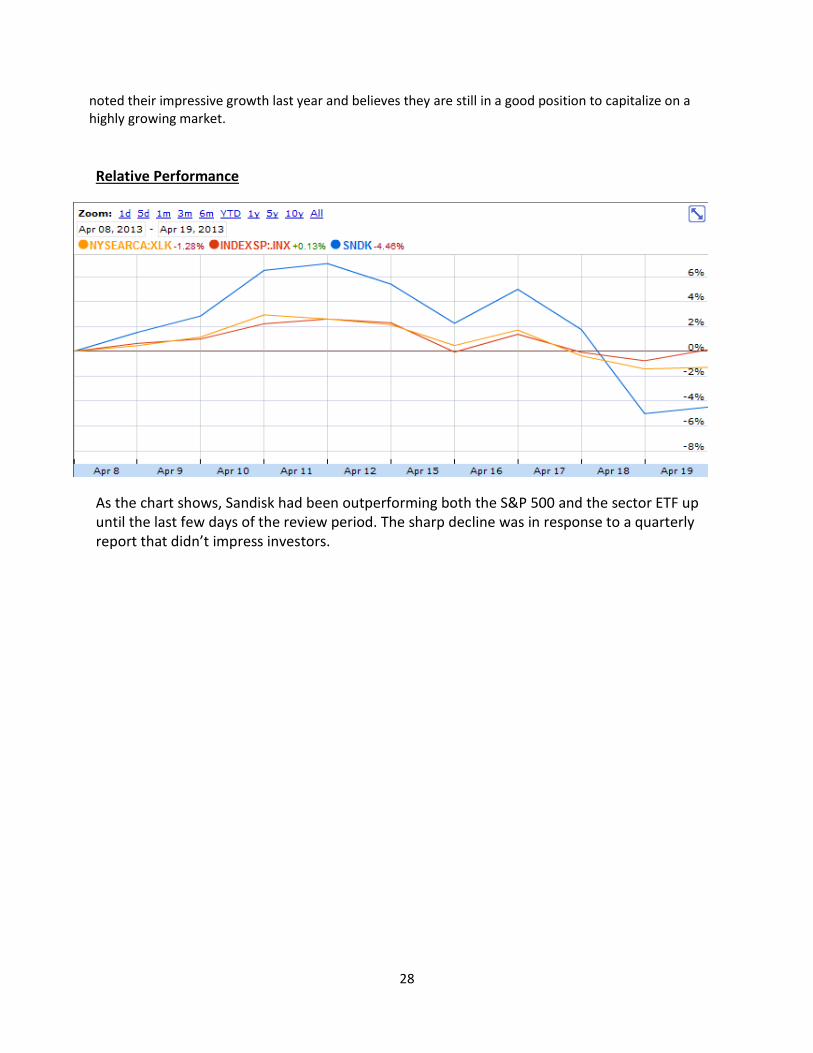

As the chart shows, Sandisk had been outperforming both the S&P 500 and the sector ETF up until the last few days of the review period. The sharp decline was in response to a quarterly report that didn’t impress investors.

29

Price Charts

Valuations Analysis

Original Analysis

30

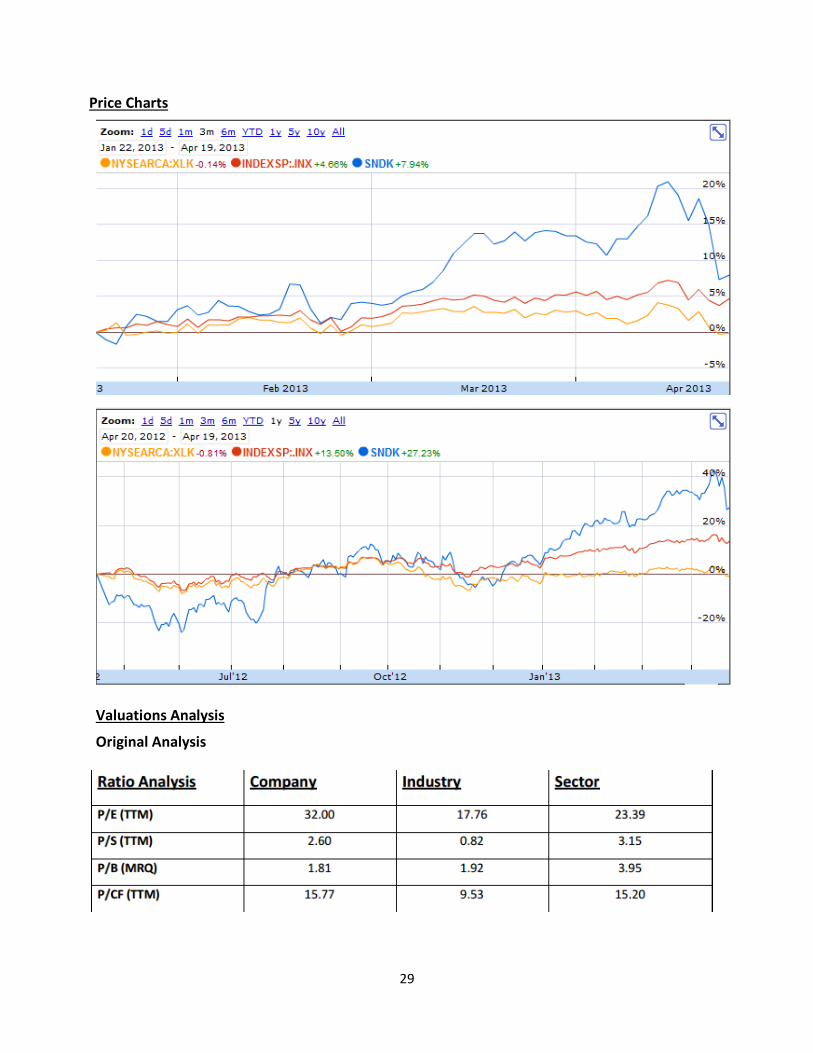

As expected, the pricing multiples of SanDisk got cheaper because of the recent decrease in price. All four multiples are lower than they were on the original day of recommendation. The stock has been following the trends of the industry and sector with stocks being cheaper than they were during the recommendation date. This is most likely related to the recent technology sector sell off.

Historical Surprises

Original Analysis

Re-Evaluation

Company Industry Sector

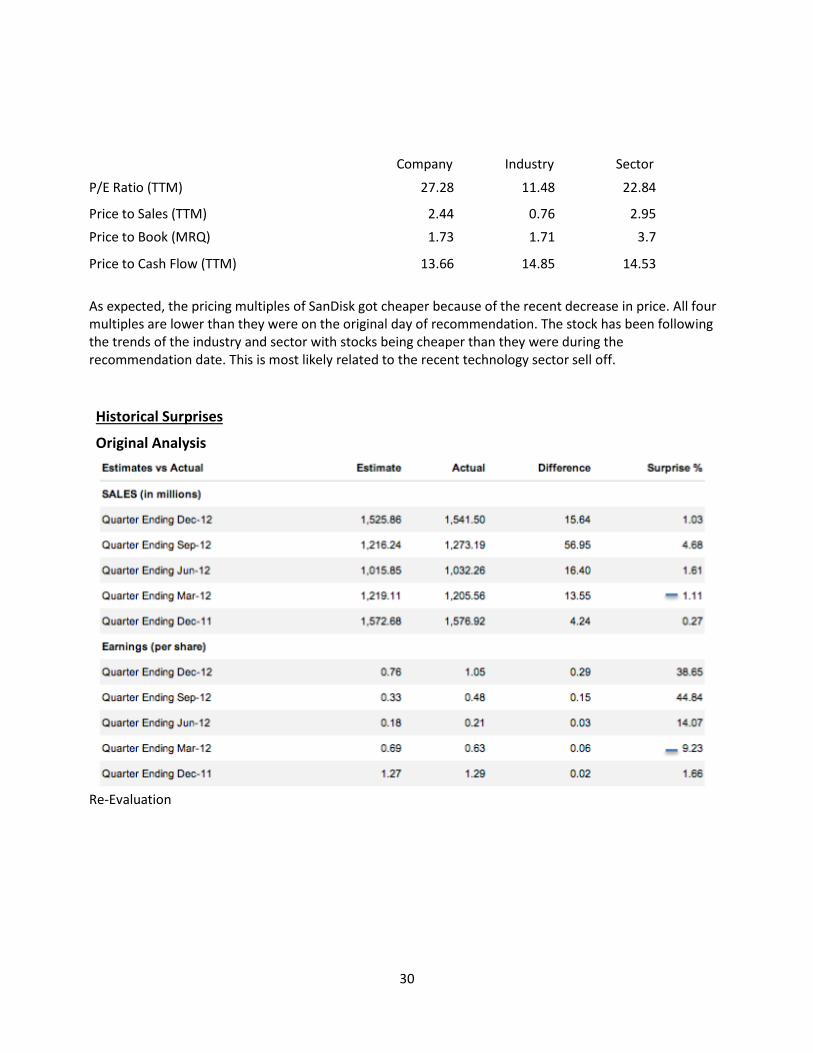

P/E Ratio (TTM) 27.28 11.48 22.84

Price to Sales (TTM) 2.44 0.76 2.95

Price to Book (MRQ) 1.73 1.71 3.7

Price to Cash Flow (TTM) 13.66 14.85 14.53

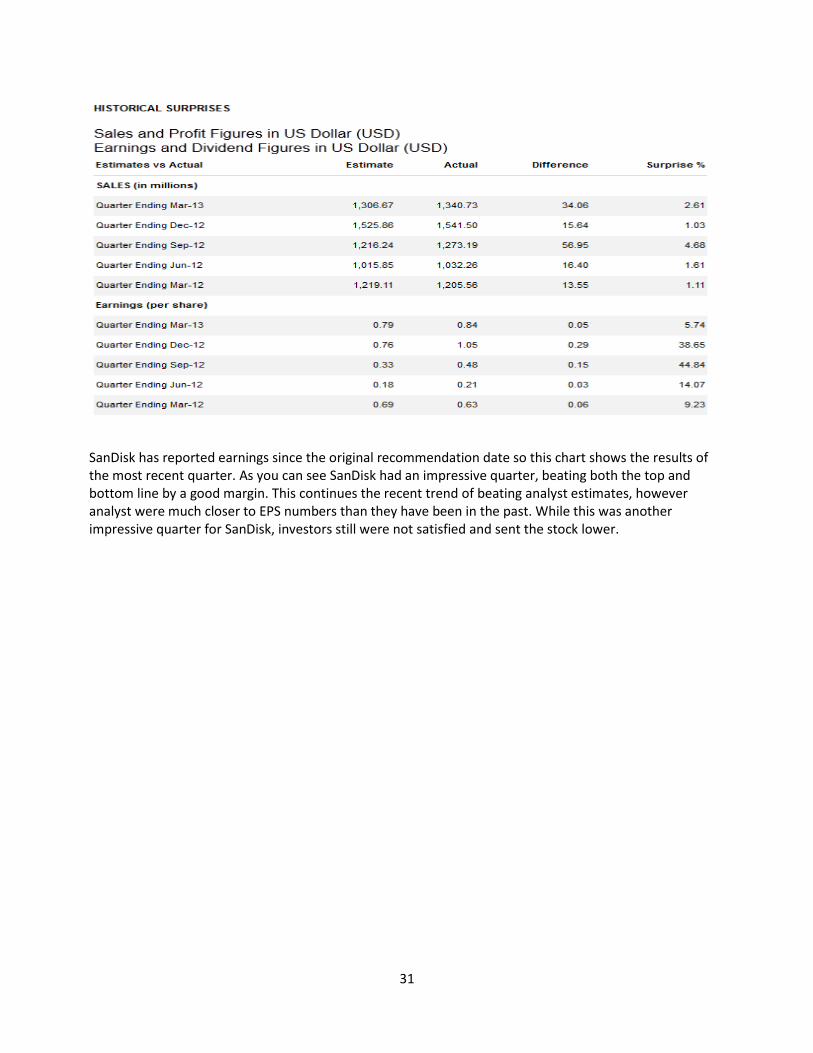

31

SanDisk has reported earnings since the original recommendation date so this chart shows the results of the most recent quarter. As you can see SanDisk had an impressive quarter, beating both the top and bottom line by a good margin. This continues the recent trend of beating analyst estimates, however analyst were much closer to EPS numbers than they have been in the past. While this was another impressive quarter for SanDisk, investors still were not satisfied and sent the stock lower.

32

Consensus Estimates

Original Analysis

Re-Evaluation Analysis

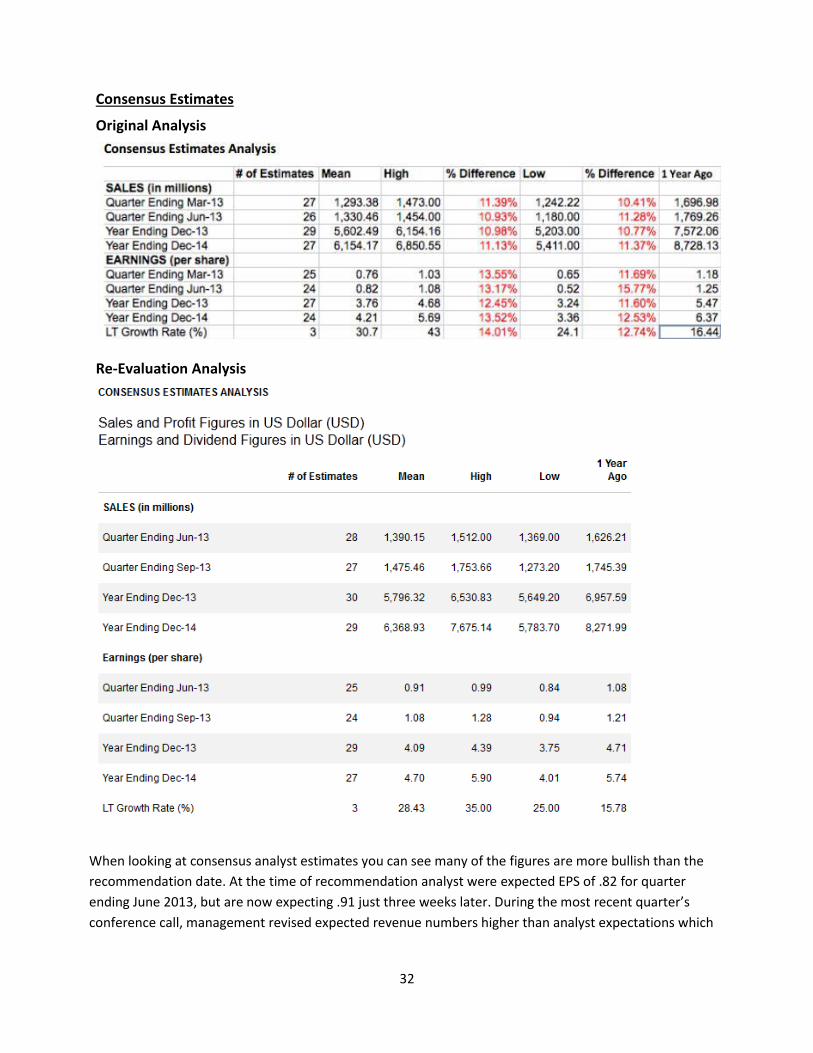

When looking at consensus analyst estimates you can see many of the figures are more bullish than the

recommendation date. At the time of recommendation analyst were expected EPS of .82 for quarter

ending June 2013, but are now expecting .91 just three weeks later. During the most recent quarter’s

conference call, management revised expected revenue numbers higher than analyst expectations which

33

most likely accounted for the bullish trends. However, analysts are expected much less from the company

than they were a year ago.

Estimate Revision Analysis

Original Analysis (3/26/13)

Re-

34

Evaluation Analysis

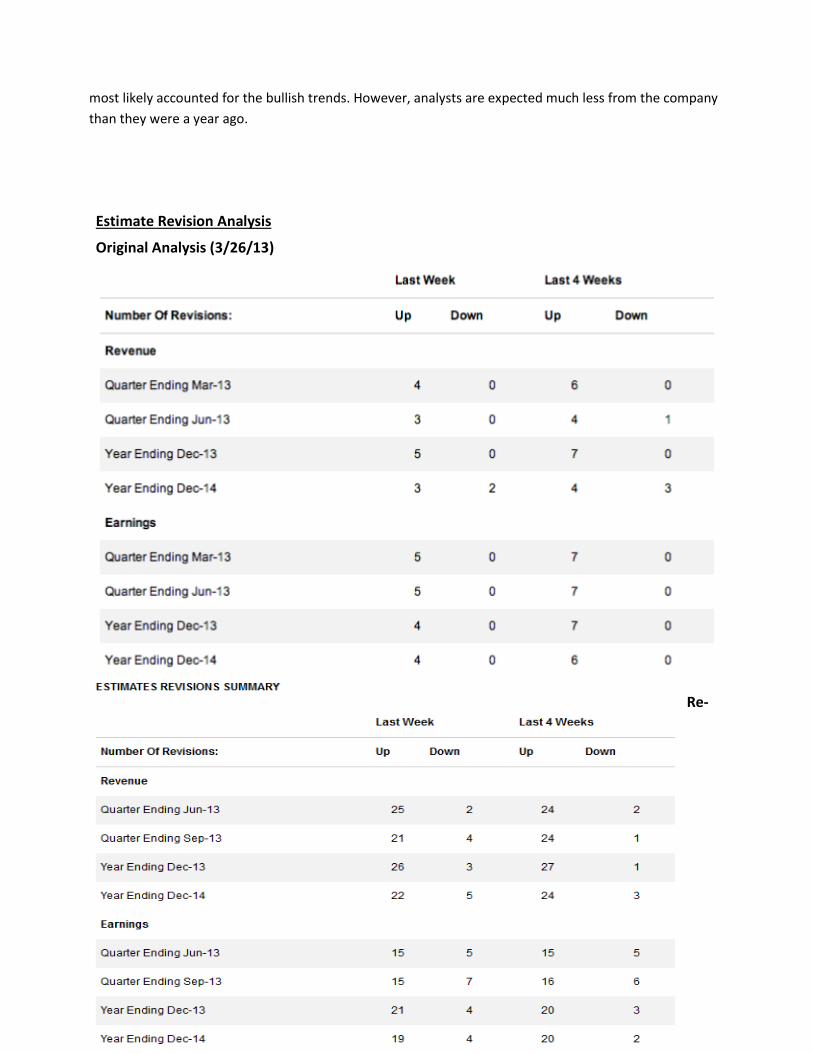

As you can see from the charts, a number of analysts have recently revised their opinions on the stock. A majority of the revisions are upward for both the expected revenue and EPS numbers which is a very bullish sign. Analysts have revised upward for all periods which is a good sign for the future outlook of the company.

Analysts’ Recommendations

Original Analysis

35

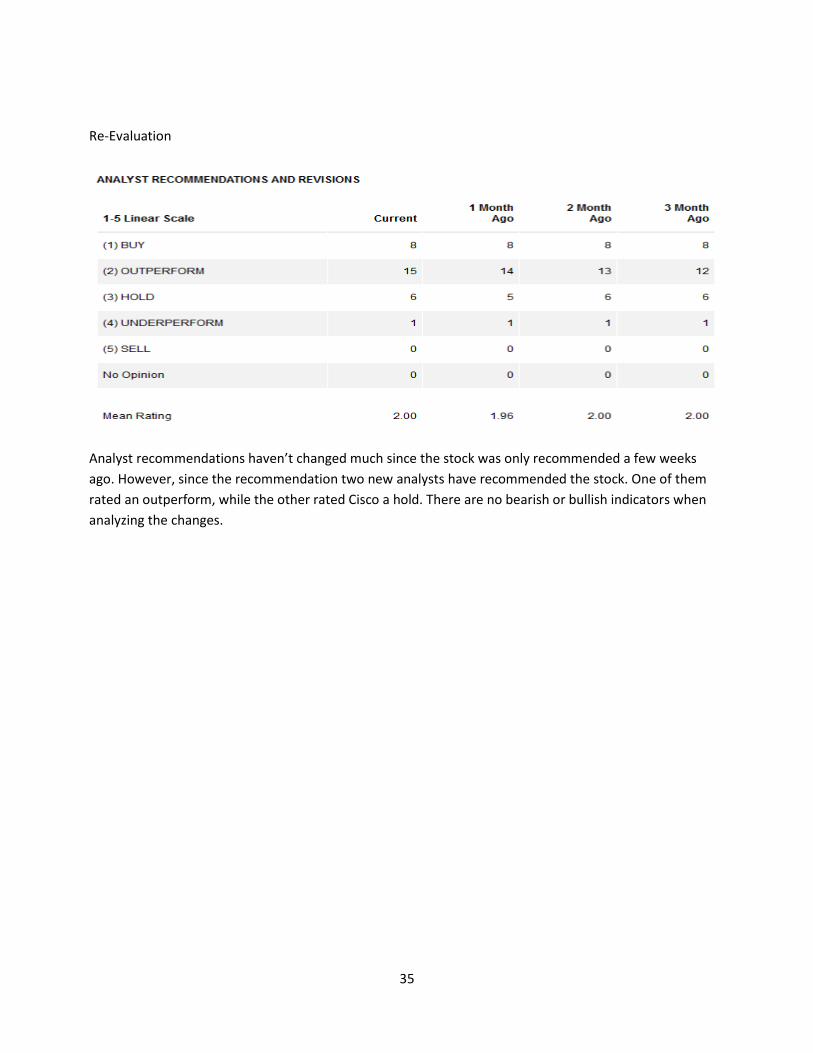

Re-Evaluation

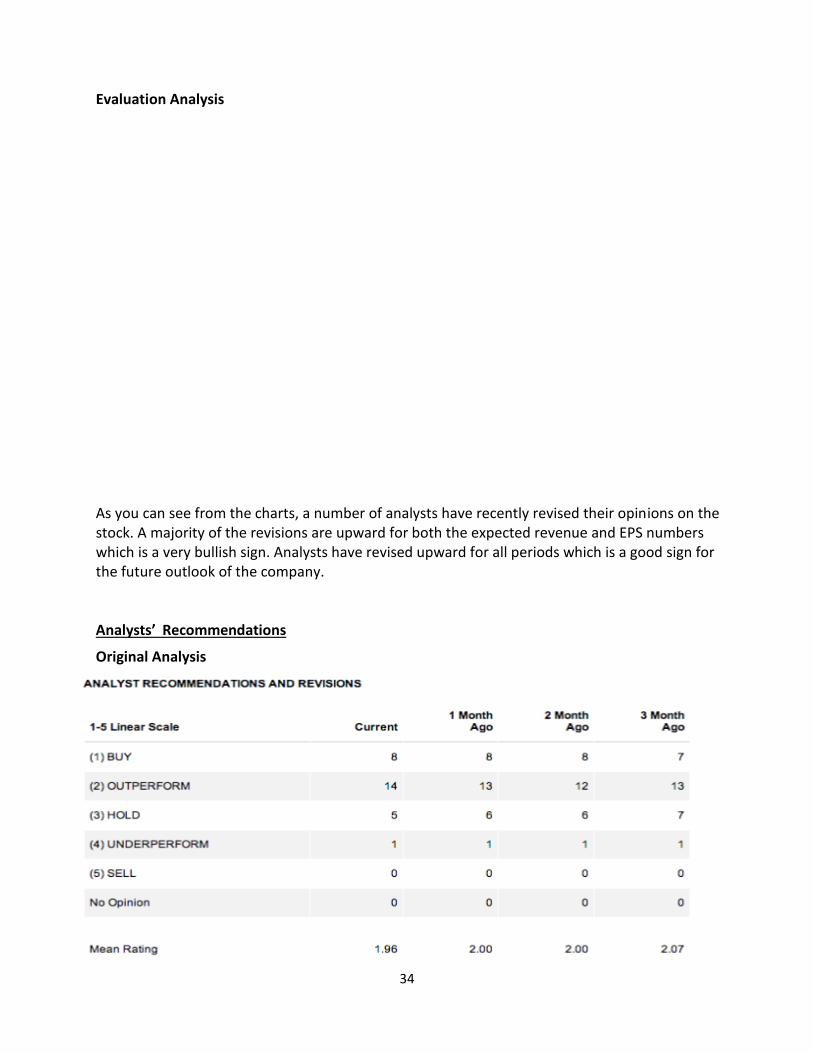

Analyst recommendations haven’t changed much since the stock was only recommended a few weeks

ago. However, since the recommendation two new analysts have recommended the stock. One of them

rated an outperform, while the other rated Cisco a hold. There are no bearish or bullish indicators when

analyzing the changes.

36

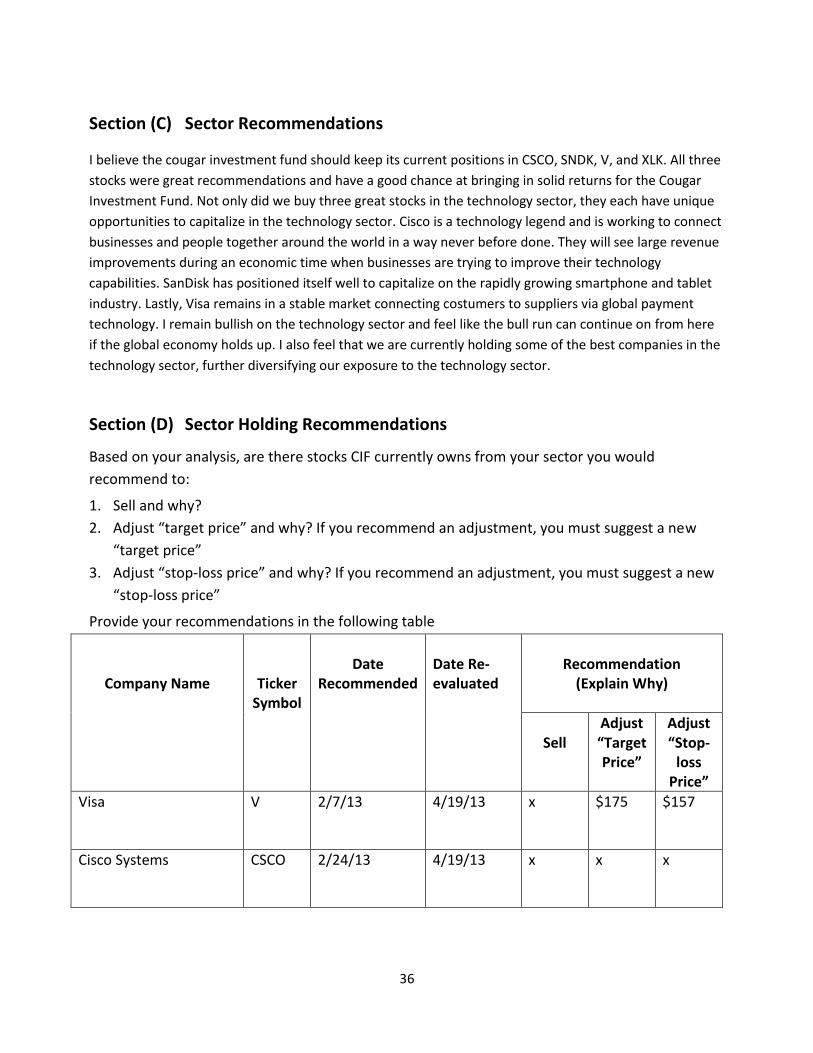

Section (C) Sector Recommendations

I believe the cougar investment fund should keep its current positions in CSCO, SNDK, V, and XLK. All three

stocks were great recommendations and have a good chance at bringing in solid returns for the Cougar

Investment Fund. Not only did we buy three great stocks in the technology sector, they each have unique

opportunities to capitalize in the technology sector. Cisco is a technology legend and is working to connect

businesses and people together around the world in a way never before done. They will see large revenue

improvements during an economic time when businesses are trying to improve their technology

capabilities. SanDisk has positioned itself well to capitalize on the rapidly growing smartphone and tablet

industry. Lastly, Visa remains in a stable market connecting costumers to suppliers via global payment

technology. I remain bullish on the technology sector and feel like the bull run can continue on from here

if the global economy holds up. I also feel that we are currently holding some of the best companies in the

technology sector, further diversifying our exposure to the technology sector.

Section (D) Sector Holding Recommendations

Based on your analysis, are there stocks CIF currently owns from your sector you would

recommend to:

1. Sell and why?

2. Adjust “target price” and why? If you recommend an adjustment, you must suggest a new

“target price”

3. Adjust “stop-loss price” and why? If you recommend an adjustment, you must suggest a new

“stop-loss price”

Provide your recommendations in the following table

Company Name

Ticker

Symbol

Date

Recommended

Date Re-evaluated

Recommendation

(Explain Why)

Sell

Adjust “Target Price”

Adjust “Stop-

loss Price”

Visa V 2/7/13 4/19/13 x $175 $157

Cisco Systems CSCO 2/24/13 4/19/13 x x x

37

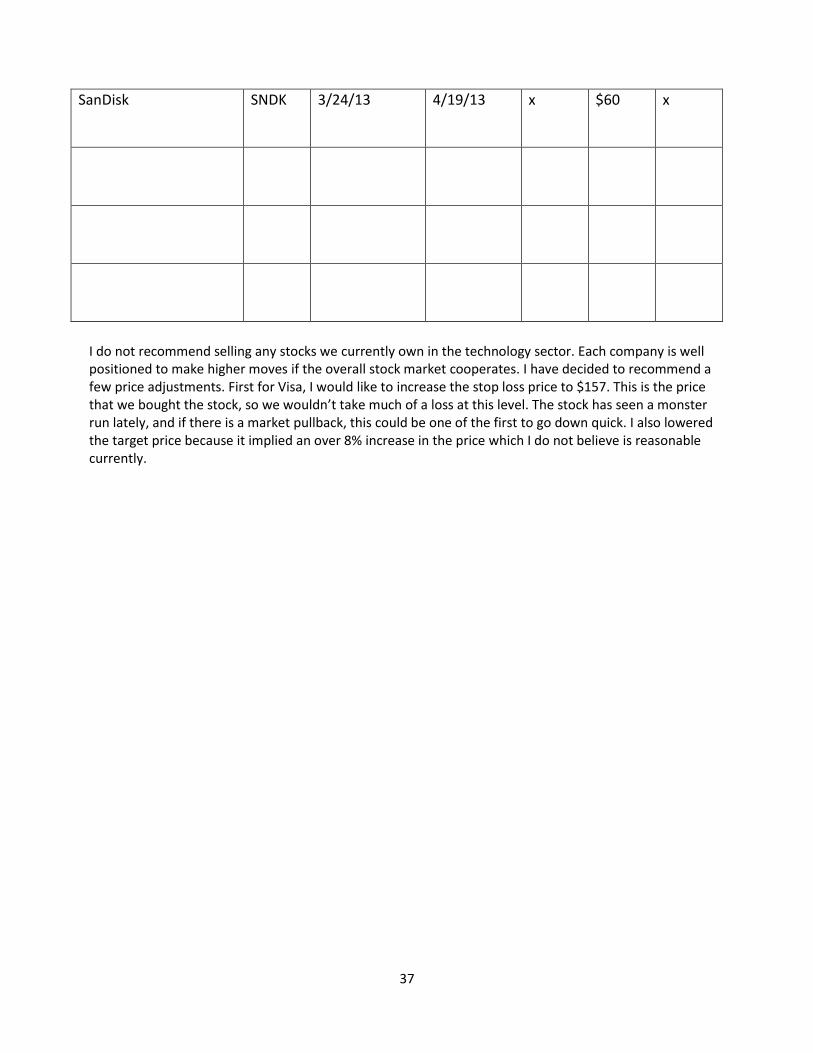

SanDisk SNDK 3/24/13 4/19/13 x $60 x

I do not recommend selling any stocks we currently own in the technology sector. Each company is well positioned to make higher moves if the overall stock market cooperates. I have decided to recommend a few price adjustments. First for Visa, I would like to increase the stop loss price to $157. This is the price that we bought the stock, so we wouldn’t take much of a loss at this level. The stock has seen a monster run lately, and if there is a market pullback, this could be one of the first to go down quick. I also lowered the target price because it implied an over 8% increase in the price which I do not believe is reasonable currently.