Jamie Davies Head of Pharmaceuticals & Healthcare Business Monitor International Oscar Mazza Consumer & Healthcare Industry Head Citi Transaction Services Latin America The Pharmaceutical & Healthcare Industry in Latin America Citi’s Online Academy Presents:

Transcript

Jamie Davies Head of Pharmaceuticals & HealthcareBusiness Monitor International

Oscar MazzaConsumer & Healthcare Industry HeadCiti Transaction Services Latin America

The Pharmaceutical & Healthcare Industry in Latin America

Citi’s Online Academy Presents:

Agenda

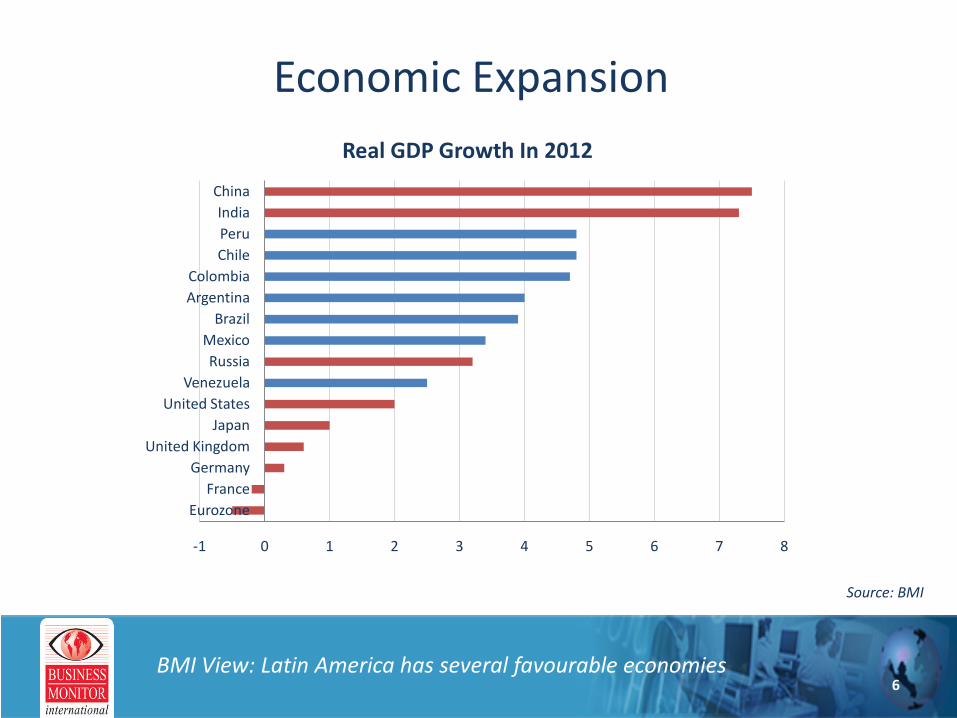

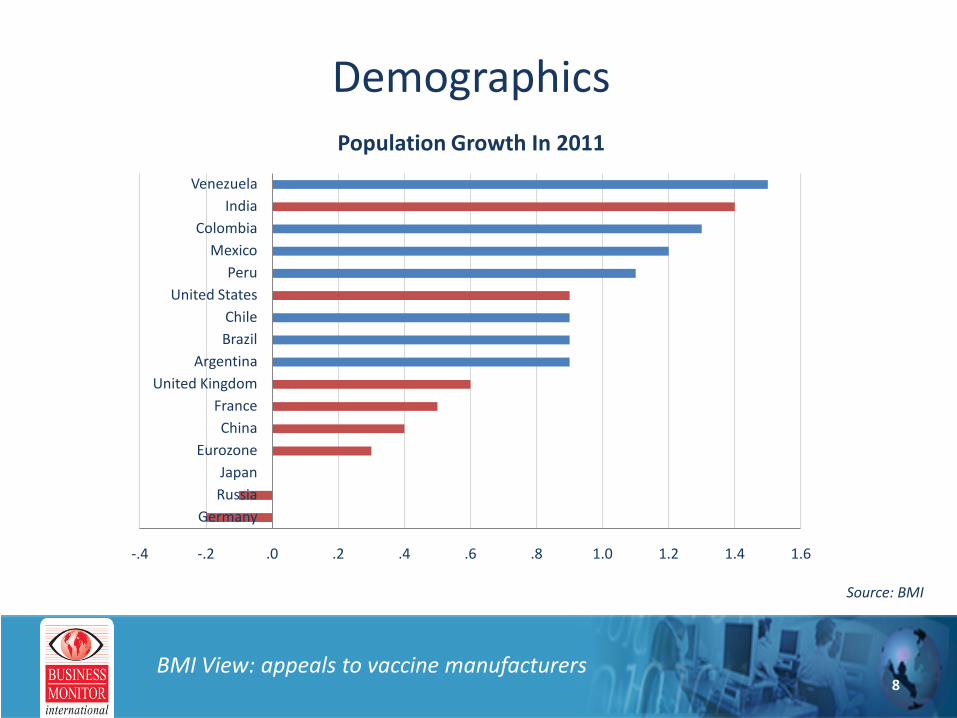

Introduction

Market drivers

Risk/Reward Ratings

Company Activity

Case Studies

Q&A

0 min 30 min

1 2 3 4 5 7

2

Introduction

• Established in 1984.

• Headquartered in London, with regional offices in Singapore, Johannesburg and New York City.

• Clients include corporations, investment banks, consultancies, governments and academic institutions.

• Over 100 research analysts.

Image: the City of London

3

The Global Context

BMI View: moderate risk, moderate reward

Pharmaceutical Sales In 2011

Latin America US$70bnEurope US$329bn

Middle East US$16bn

Africa US$19bn

North America US$358bn

Asia US$265bn

Source: BMI

4

The Global Outlook

BMI View: emerging markets to drive industry growth

Latin America Sales (EURmn) (LHS) Latin America sales as % of global sales (RHS)

18

Local Company Case Study: Genomma

BMI View: should concentrate on its domestic market

Source: Bloomberg

0

50

100

150

200

250

300

350

400

450

The Relative Performance Of Genomma Lab Internacional And The Mexico IPC Index

Genomma Mexico IPC Index

19

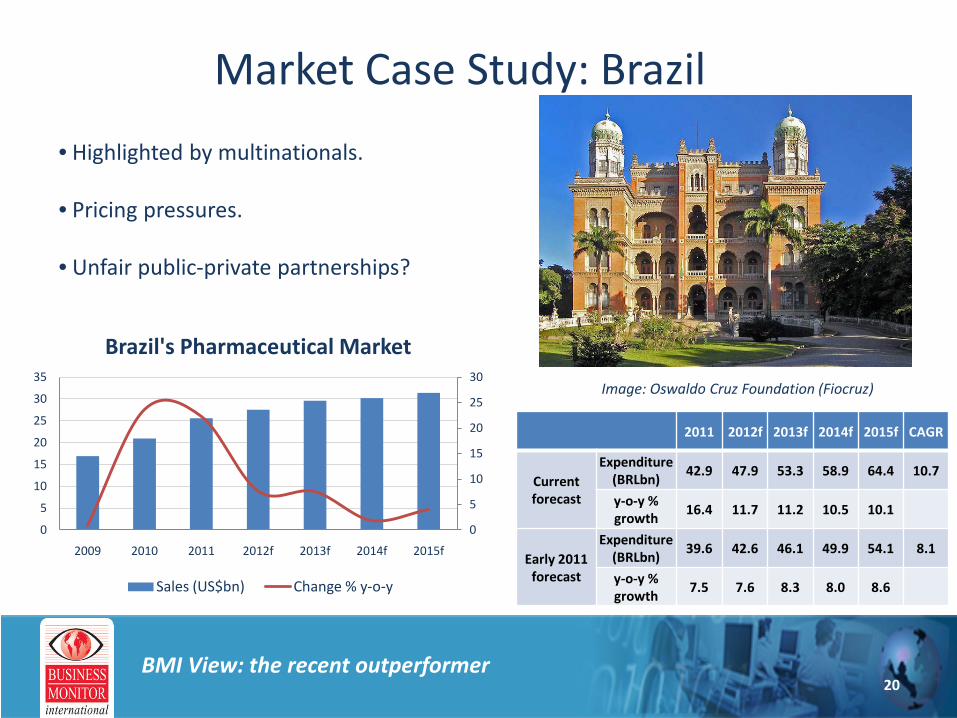

Market Case Study: Brazil

2011 2012f 2013f 2014f 2015f CAGR

Current forecast

Expenditure (BRLbn)

42.9 47.9 53.3 58.9 64.4 10.7

y-o-y % growth

16.4 11.7 11.2 10.5 10.1

Early 2011 forecast

Expenditure (BRLbn)

39.6 42.6 46.1 49.9 54.1 8.1

y-o-y % growth

7.5 7.6 8.3 8.0 8.6

Image: Oswaldo Cruz Foundation (Fiocruz)

BMI View: the recent outperformer

0

5

10

15

20

25

30

0

5

10

15

20

25

30

35

2009 2010 2011 2012f 2013f 2014f 2015f

Brazil's Pharmaceutical Market

Sales (US$bn) Change % y-o-y

• Highlighted by multinationals.

• Pricing pressures.

• Unfair public-private partnerships?

20

Market Case Study: Mexico

2011 2012f 2013f 2014f 2015f CAGR

Current forecast

Expenditure (MXNbn)

161 175 189 204 220 8.0

y-o-y % growth

8.5 8.3 8.1 7.9 7.7

Early 2011 forecast

Expenditure (MXNbn)

152 156 161 165 170 2.8

y-o-y % growth

2.5 2.6 2.8 2.9 2.9

Image: Petróleos Mexicanos (Pemex) oil rig in the Gulf of Mexico

BMI View: a positive surprise

-20

-15

-10

-5

0

5

10

15

0

5

10

15

20

2009 2010 2011 2012f 2013f 2014f 2015f

Mexico's Pharmaceutical Market

Sales (US$bn) Change % y-o-y

• No energy liberalisation?

• Dependent on US economy.

• General security concerns.

21

Market Case Study: Venezuela

2011 2012f 2013f 2014f 2015f CAGR

Current forecast

Expenditure (VEFbn)

33.3 41.2 49.8 59.3 69.5 20.2

y-o-y % growth

24.6 23.8 21.1 19.0 17.1

Early 2011 forecast

Expenditure (VEFbn)

29.4 36.1 42.8 49.9 57.6 18.3

y-o-y % growth

10.0 23.0 18.4 16.7 15.4

Image: Hugo Chavez

BMI View: October 2012 election is key

-40

-30

-20

-10

0

10

20

30

40

0

2

4

6

8

10

2009 2010 2011 2012f 2013f 2014f 2015f

Venezuela's Pharmaceutical Market

Sales (US$bn) Change % y-o-y

• High oil prices.

• Repatriation of revenues.

• Anti-American sentiment.

22

Market Case Study: Argentina

2011 2012f 2013f 2014f 2015f CAGR

Current forecast

Expenditure (ARSbn)

37.9 45.4 53.7 62.9 72.8 17.7

y-o-y % growth

30.7 19.6 18.4 17.1 15.7

Early 2011 forecast

Expenditure (ARSbn)

34.2 39.9 46.2 53.2 60.9 15.5

y-o-y % growth

17.2 16.7 15.8 15.2 14.3

Image: Instituto Nacional de Estadística y Censos, INDEC

BMI View: consistently defying risks

0

5

10

15

20

25

0

2

4

6

8

10

2009 2010 2011 2012f 2013f 2014f 2015f

Argentina's Pharmaceutical Market

Sales (US$bn) Change % y-o-y

• Under-reporting of inflation.

• Patent approval backlog.

• Import restrictions.

23

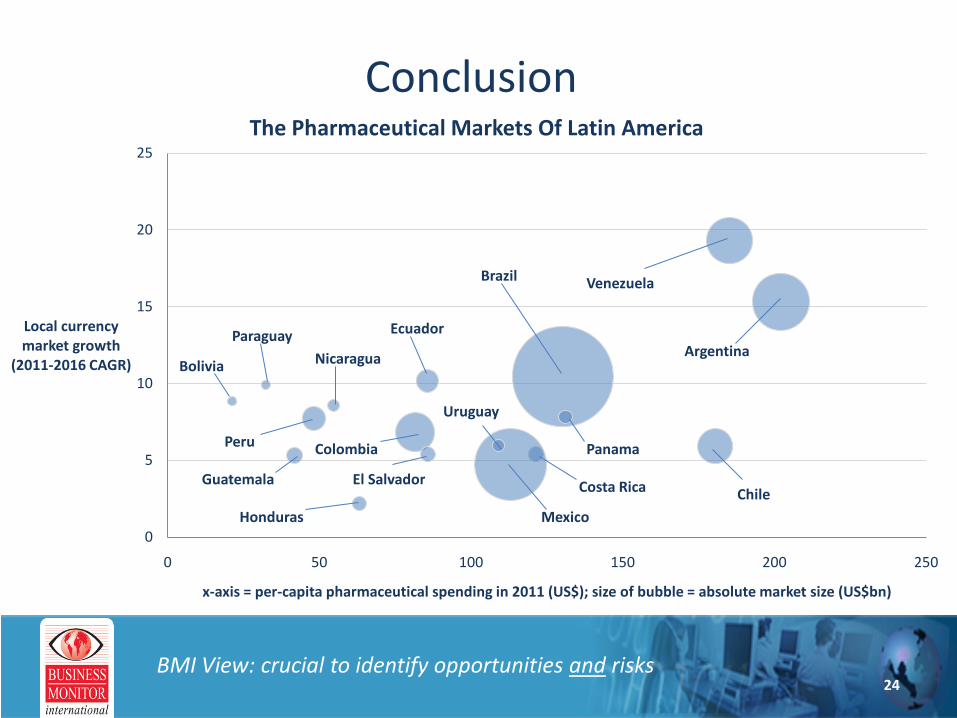

Conclusion

BMI View: crucial to identify opportunities and risks

0

5

10

15

20

25

0 50 100 150 200 250

Local currency market growth

(2011-2016 CAGR)

x-axis = per-capita pharmaceutical spending in 2011 (US$); size of bubble = absolute market size (US$bn)

The Pharmaceutical Markets Of Latin America

Costa Rica

Mexico

Panama

Uruguay

El Salvador

Colombia

Honduras

Guatemala

Peru

Bolivia

ParaguayNicaragua

Ecuador

Brazil

Chile

Argentina

Venezuela

24

Questions

For all questions and inquiries related to Business Monitor International, including interest in a free trial or to obtain more information about our subscription services, please contact: