City of Miami General Employees’ and l Axiom International Investors LLC Sanitation Employees' Retirement Trust Axiom International Investors LLC Second Quarter, 2011 Portfolio Review as of June 30, 2011 B dl A il D ld K Mill Bradley Amoils Portfolio Manager Andrew H. Jacobson, CFA, CIO Portfolio Manager Donald K. Miller Chairman Jon R. Yenor Director of Client Service & Marketing 33 Benedict Place· Greenwich, CT 06830 · Tel (203) 422-8000 · Fax (203) 422-8090 AXIOM

Transcript

City of Miami General Employees’ and l

Axiom International Investors LLC

Sanitation Employees' Retirement TrustAxiom International Investors LLC

Second Quarter, 2011 Portfolio Reviewas of June 30, 2011

B dl A il D ld K MillBradley AmoilsPortfolio Manager

Andrew H. Jacobson, CFA, CIOPortfolio Manager

Donald K. MillerChairman

Jon R. YenorDirector of Client Service & Marketing

Balance as of 06/30/11: $27,303,387.53 (after fees)

Net Gain: + $16,753,387.53 (after fees)

Annualized CumulativeAxiom Time Weighted Performance for City of Miami GESEInception to Date, (after fees) March 6, 2002 - June 30, 2011 9.1% 125.9%Inception to Date, (after fees) March 6, 2002 June 30, 2011 9.1% 125.9%

MSCI EAFE Index March 6, 2002 - June 30, 2011 7.1% 90.1%

MSCI ACW Ex-US Index March 6, 2002 - June 30, 2011 8.9% 121.3%

US S&P 500 Index March 6, 2002 - June 30, 2011 1.5% 15.2%

AXIOM 2AXIOM Please see performance footnotes at the end of this document.

US S& 500 de a c 6, 00 Ju e 30, 0 .5% 5. %

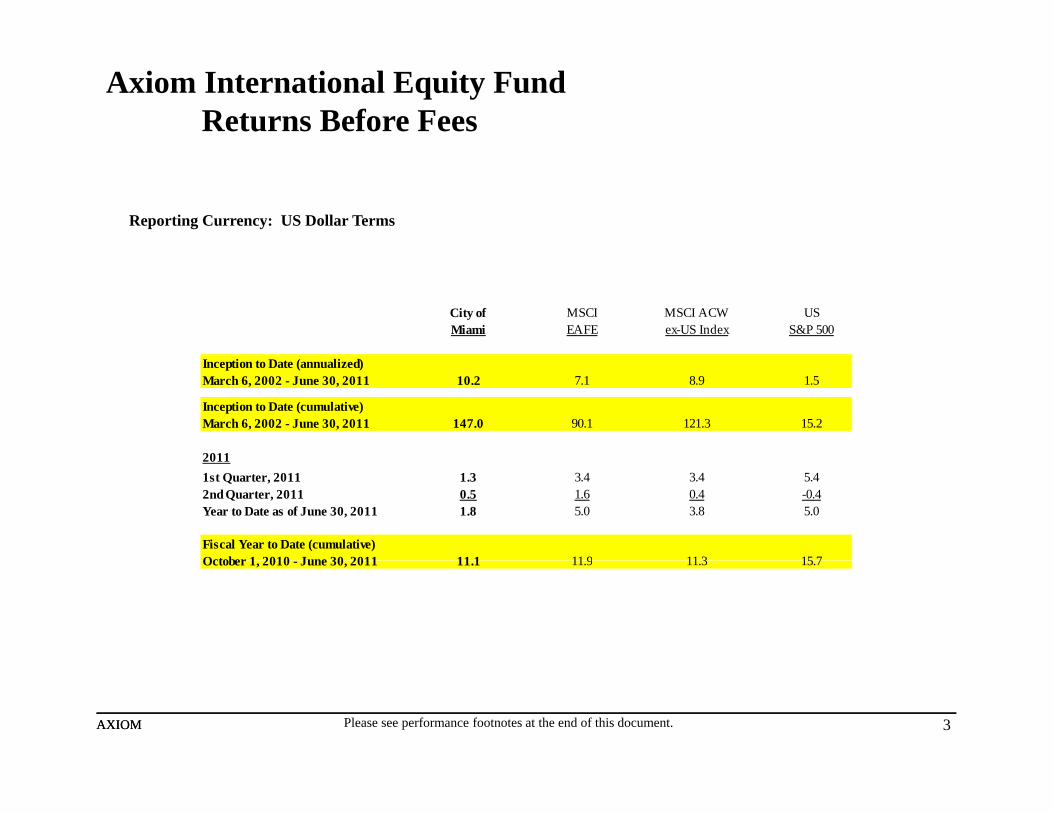

Axiom International Equity FundReturns Before Fees

Reporting Currency: US Dollar Terms

City of Miami

MSCIEAFE

MSCI ACWex-US Index

USS&P 500

Inception to Date (annualized)March 6, 2002 - June 30, 2011 10.2 7.1 8.9 1.5

Inception to Date (cumulative)March 6, 2002 - June 30, 2011 147.0 90.1 121.3 15.2

201120111st Quarter, 2011 1.3 3.4 3.4 5.42nd Quarter, 2011 0.5 1.6 0.4 -0.4Year to Date as of June 30, 2011 1.8 5.0 3.8 5.0

Fiscal Year to Date (cumulative)October 1 2010 June 30 2011 11 1 11 9 11 3 15 7October 1, 2010 - June 30, 2011 11.1 11.9 11.3 15.7

AXIOM 3AXIOM Please see performance footnotes at the end of this document.

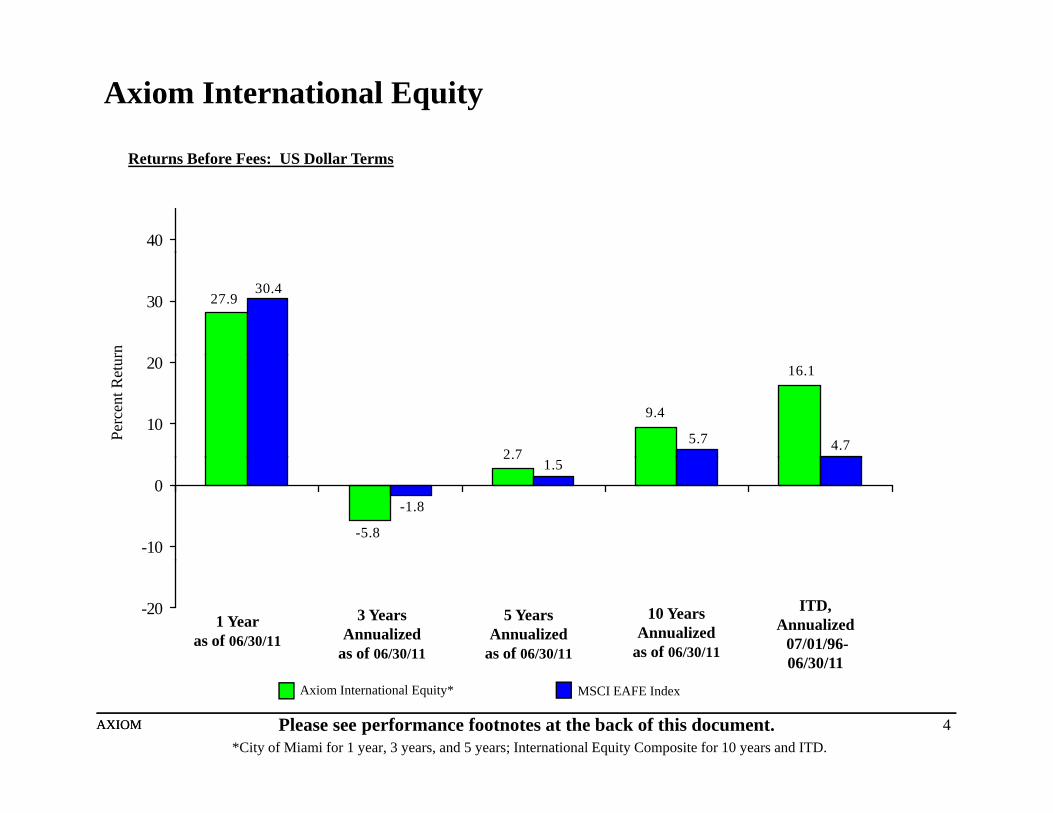

Axiom International Equity

40

Returns Before Fees: US Dollar Terms

27.930.4

30

rn

9.4

2.7

16.1

4.75.710

20

Perc

ent R

etur

-5.8

2.71.5

-1.8

-10

0

-20 ITD,Annualized

07/01/96-06/30/11

5 Years Annualized

as of 06/30/11

3 Years Annualized

as of 06/30/11

1 Year as of 06/30/11

10 Years Annualized

as of 06/30/11

AXIOM 4AXIOM Please see performance footnotes at the back of this document.

Axiom International Equity*

06/30/11

MSCI EAFE Index

*City of Miami for 1 year, 3 years, and 5 years; International Equity Composite for 10 years and ITD.

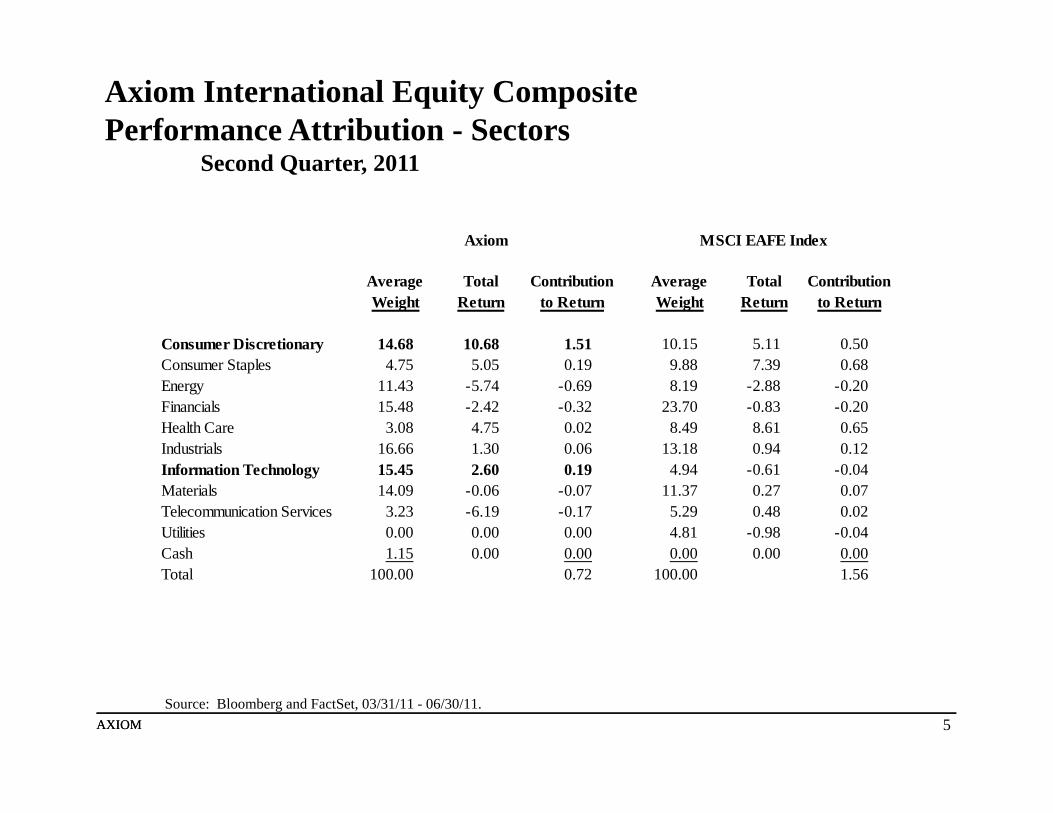

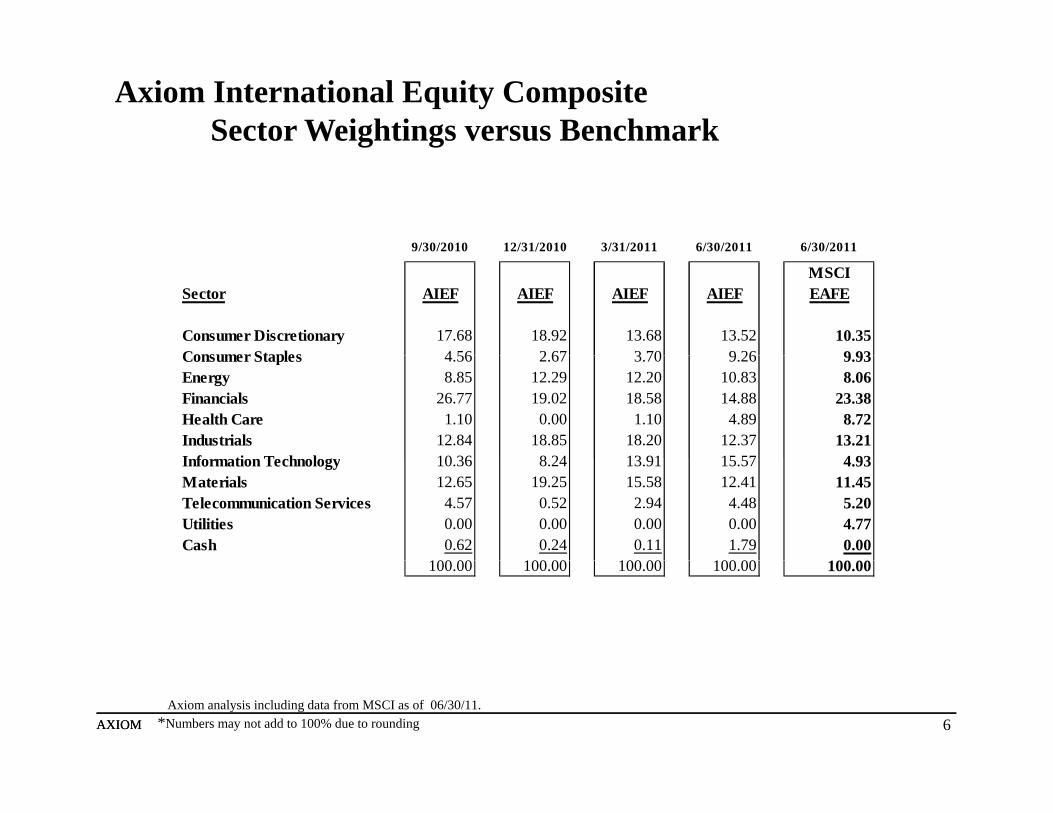

Axiom International Equity CompositePerformance Attribution - Sectors

AXIOM 8AXIOM Source: Factset Data Service and Axiom analysis from inception July 1, 1996 through June 30, 2011.

Axiom International Equity CompositePerformance Attribution - Regions

Second Quarter, 2011

Axiom MSCI EAFE Index

Average Total Contribution Average Total Contribution

Europe & UK 50.02 2.75 1.37 66.96 2.42 1.62Americas ex US 11.00 -7.35 -0.81 0.00 0.00 0.00Japan 12.87 -0.82 -0.21 19.73 -0.20 -0.04

Weight Return to Return Weight Return to Return

Asia Pacific ex Japan 24.96 1.46 0.36 13.31 -0.15 -0.02Cash 1.15 0.00 0.00 0.00 0.00 0.00Total 100.00 0.72 100.00 1.56

AXIOM 9AXIOMSource: Bloomberg and FactSet, 03/31/11 - 06/30/11.

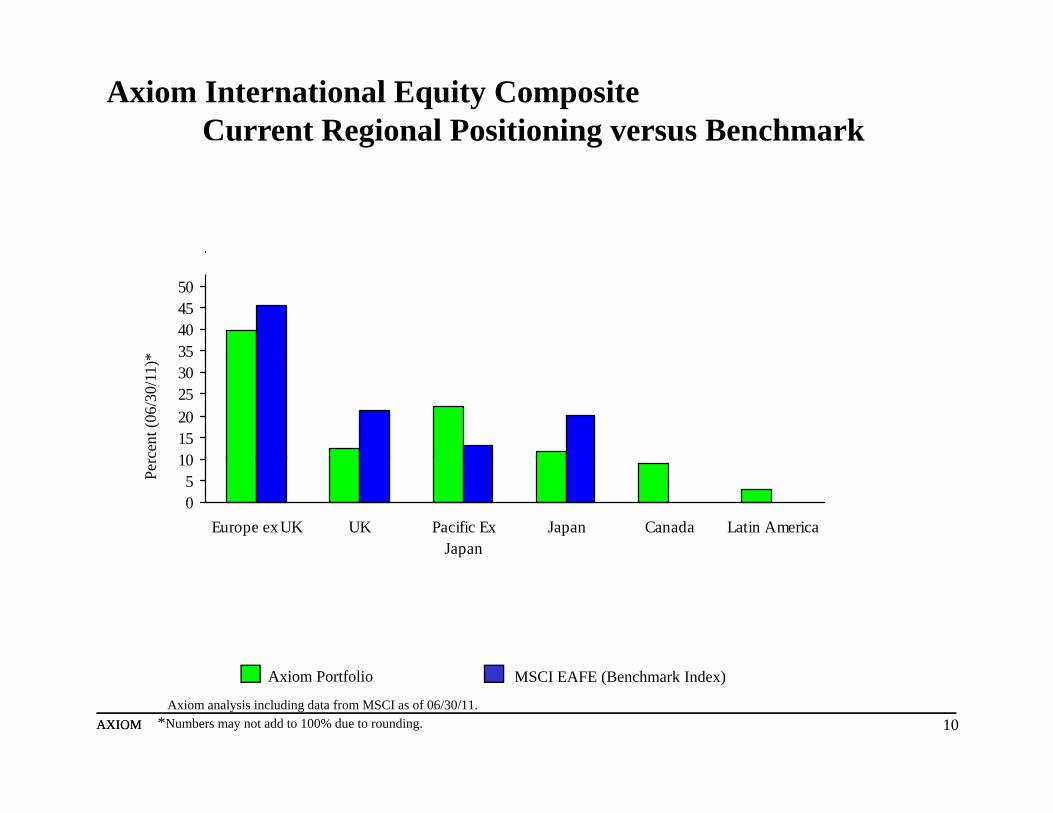

Axiom International Equity Composite Current Regional Positioning versus Benchmark

6065707580

3540455055

*

101520253035

cent

(06/

30/1

1)*

05

10

Europe ex UK UK Pacific ExJapan

Japan Canada Latin America

Per

AXIOM 10AXIOM

Axiom Portfolio MSCI EAFE (Benchmark Index)

Axiom analysis including data from MSCI as of 06/30/11.*Numbers may not add to 100% due to rounding.

Axiom International Equity Composite Portfolio Allocation by Region Since Inception

80

60

o (%

)

40

rcen

t of P

ortfo

li

Europe Ex-UK

20

Pe

Japan

Pacific ex Japan

UK

0

09/9

606

/97

03/9

812

/98

09/9

906

/00

03/0

112

/01

09/0

206

/03

03/0

412

/04

09/0

506

/06

03/0

712

/07

09/0

806

/09

03/1

012

/10

JapanCanadaLatin America

AXIOM 11AXIOM

0 0 0 1 0 0 0 1 0 0 0 1 0 0 0 1 0 0 0 1

Axiom quarter-end regional allocation from inception on July 1, 1996 through June 30, 2011.

Axiom International Equity Composite All Market Capitalizations versus Benchmark

100

60

80

/11)

*

40

Perc

ent (

06/3

0/

20

0>$19 Billion $6-$19 Billion Under $6 Billion

AXIOM 12AXIOM

Axiom Portfolio MSCI EAFE (Benchmark Index)

Axiom analysis including data from MSCI as of 06/30/11.*Numbers may not add to 100% due to rounding.

Axiom International Equity CompositePortfolio Characteristics as of June 30, 2011

HoldingsMarket Capitalization $ 47.9 BMarket Capitalization (Median) $ 36.5 B

81

Daily Trading Volume $ 161.5 MDebt Equity Ratio 20.4 %Price Earnings Ratio (2011 Estimated, Consensus) 13.5Earnings Growth (2011 Estimated, Consensus) 24.3 %g ( )PEG RatioPercent of Portfolio Holdings w/Analysts’ Earnings Revisions Up (3 mo.) %Percent of Portfolio Holdings w/Analysts’ Earnings Revisions Down (3 mo.) %

5941

0.55

AXIOM 13AXIOMSources: Axiom analysis, MSCI, IBES and Worldscope.All values, except where noted, are Average excluding top and bottom 5% outlying values.

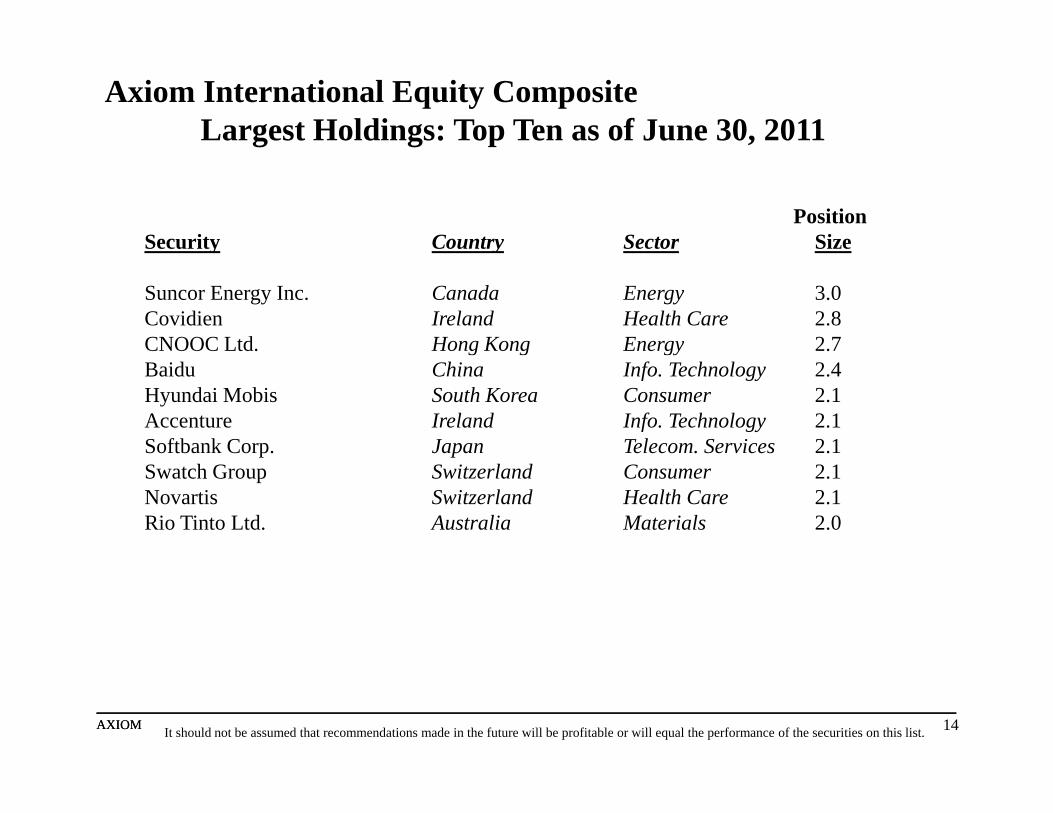

Axiom International Equity Composite Largest Holdings: Top Ten as of June 30, 2011

PositionSecurity Country Sector Sizey y

Suncor Energy Inc. Canada Energy 3.0Covidien Ireland Health Care 2.8CNOOC Ltd. Hong Kong Energy 2.7Baidu China Info. Technology 2.4Hyundai Mobis South Korea Consumer 2.1Accenture Ireland Info. Technology 2.1Softbank Corp. Japan Telecom. Services 2.1Swatch Group Switzerland Consumer 2.1Novartis Switzerland Health Care 2.1Rio Tinto Ltd. Australia Materials 2.0

AXIOM 14AXIOM It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities on this list.

Axiom International Equity Composite Largest Holdings: Top Ten

As of 06/30/11

Suncor Energy Inc. (Energy) - Integrated energy company based in Canada.

Covidien (Health Care) - Company that distributes a diverse range of medical devices and supplies for use in clinical and home settings.

CNOOC Ltd. (Energy) - Explorer, developer, producer, and seller of crude oil and natural gas through its subsidiaries.

Baidu (Info. Technology) - Search engine for websites, audio files, and images.

Hyundai Mobis (Consumer) - Manufactures and markets automotive parts and equipment, and also contracts environmental projects.

Accenture (Info. Technology) - An international resources company.

Softbank Corp. (Telecom. Services) - Operates Asymmetric Digital Subscriber Lines, fiber optic high-speed Internet connections, e-Commerce businesses, and Internet based advertising and auction businesses.

Swatch Group (Consumer) - Swiss manufacturer of watches and watch components.

Novartis (Health Care) - Swiss manufacturer of pharmaceutical and nutrition products.

Rio Tinto Ltd. (Materials) - An international mining company based in Australia

AXIOM 15AXIOM

Rio Tinto Ltd. (Materials) An international mining company based in Australia.

Axiom International InvestorsFirm Update

June 30, 2011 (USD)Assets Inception

Under Management DateLong Only Equities

International All-Cap $7,090.4 MM 7/1/1996Global All-Cap $5,520.1 MM 7/1/2004Emerging Markets All-Cap $1,201.2 MM 8/1/2007e g g a e s Cap $ , 0 . 8/ / 007U.S. Small-Cap $ 13.2 MM 9/1/2006

Long/Short EquitiesInternational All-Cap Opportunity Funds $ 370.3 MM 1/1/1999I t ti l Mi C F d $ 143 3 MM 9/1/2004International Micro-Cap Fund $ 143.3 MM 9/1/2004Global Micro-Cap Fund $ 25.1 MM 2/1/2007

Total $14,363.6 MM

AXIOM 16AXIOM

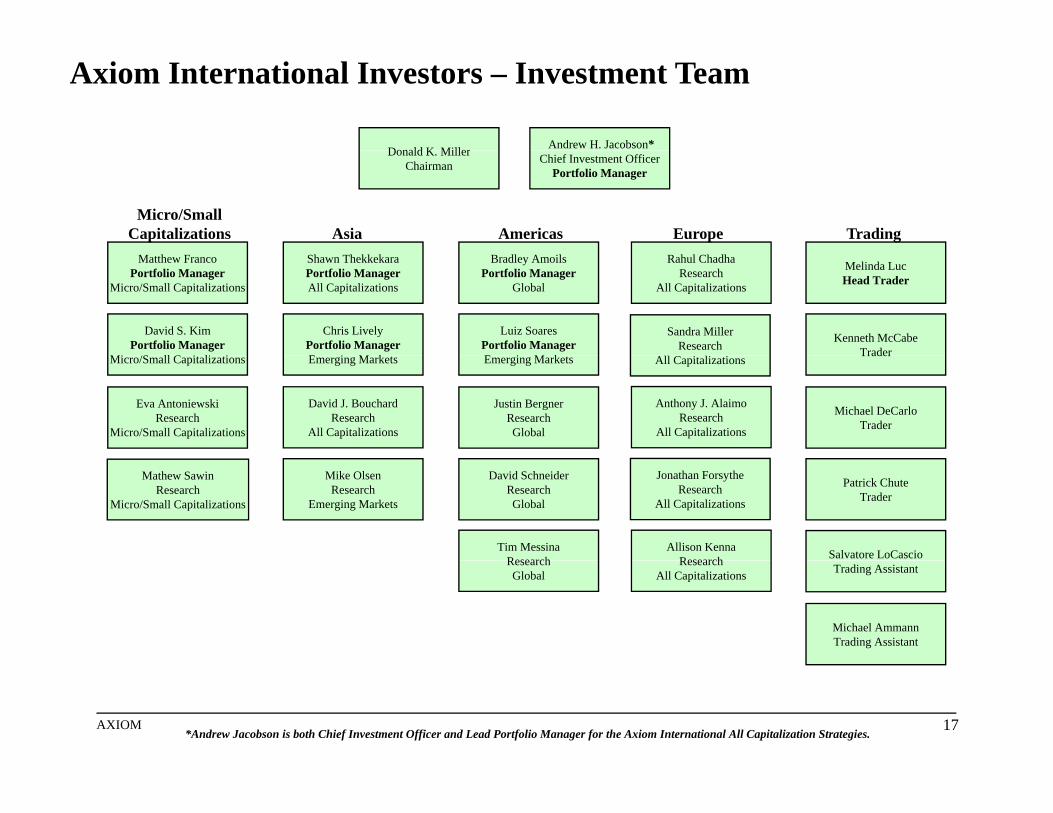

Axiom International Investors – Investment Team

Donald K Miller Andrew H. Jacobson *Donald K. MillerChairman Chief Investment Officer

Emerging Markets Emerging Markets All Capitalizations

Justin BergnerResearchGlobal

Patrick ChuteTrader

Salvatore LoCascio

Jonathan ForsytheResearch

All Capitalizations

Allison KennaResearch

Mike OlsenResearch

Emerging Markets

David SchneiderResearchGlobal

Tim MessinaResearch

Mathew SawinResearch

Micro/Small Capitalizations

Trading Assistant

Michael AmmannTrading Assistant

ResearchAll Capitalizations

ResearchGlobal

17AXIOM*Andrew Jacobson is both Chief Investment Officer and Lead Portfolio Manager for the Axiom International All Capitalization Strategies.

Axiom International Investors

Client Service & Marketing Administrationg

Jon R. YenorDirector, Client

Service & Marketing

Shane McMahonDrew L Zielinski

Administration

Bart TesorieroChief Operating Officer

Denise M ZambardiShane McMahonClient Service &

Marketing

Drew L. ZielinskiClient Service &

Marketing

Sarah PapsunClient Service

Sanja KraljevicClient Service

Jennifer McMackinOperations Manager

Denise M. ZambardiChief Compliance Officer/

Controller

Michael BurshteynOperations

Trade Settlements

Michael MileyCompliance

Marlyn MorrisOperations Specialist

Jennifer OdoardiClient Service

Dean BumbacaOperations

Trade Settlements

Mark KarlsonOperations

Trade Settlements

Ricky JohnsonOperations

Trade Settlements

Stephanie Collura Client Service

Kalin BrackenClient Service

Mi h l D lMichael DealyOperations

Trade Settlements

Cary Yerg Administrative

18AXIOM

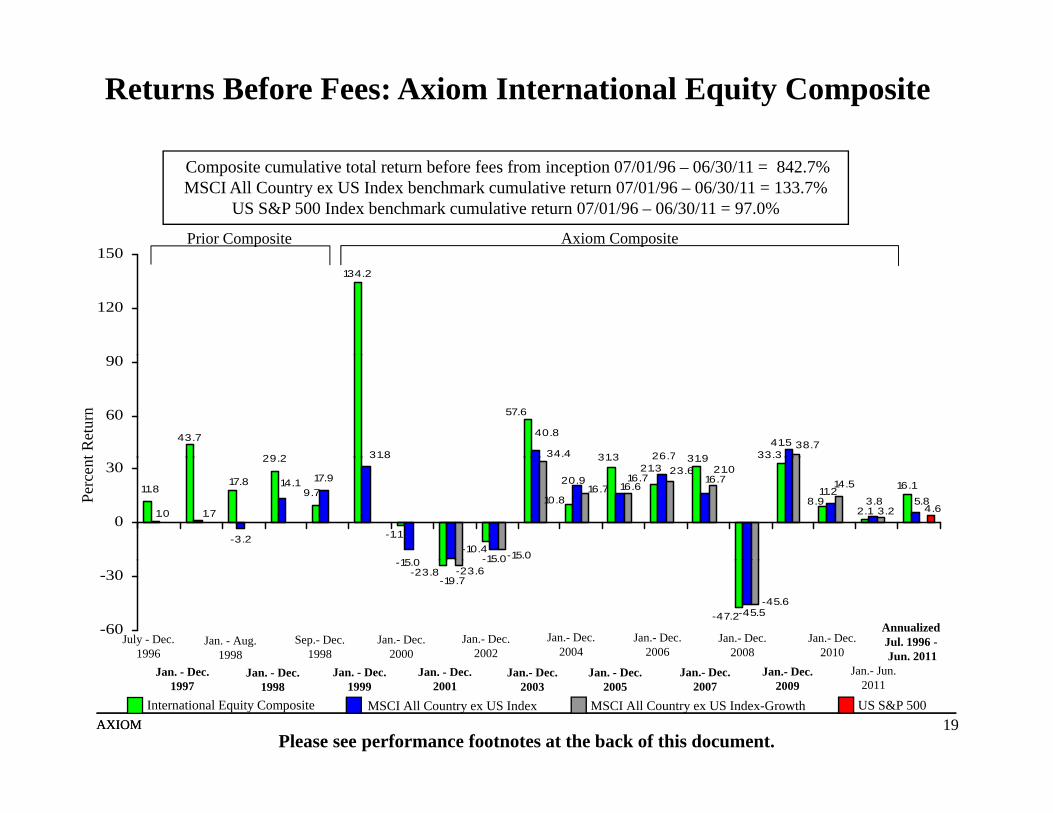

Returns Before Fees: Axiom International Equity Composite

150

Composite cumulative total return before fees from inception 07/01/96 – 06/30/11 = 842.7%MSCI All Country ex US Index benchmark cumulative return 07/01/96 – 06/30/11 = 133.7%

US S&P 500 Index benchmark cumulative return 07/01/96 – 06/30/11 = 97.0%

Prior Composite Axiom Composite

134.2

120

150

29 2 313

43.7

57.6

319 33.326 7

40.8

31.841.5

34.438.7

60

90

t Ret

urn

29.2

-3.2

17.916.1

2.1

21.331.3

10.89.7

-10.4

17.811.8

-1.1

31.9 33 3

8.9 5.8

16.7

26.7

16.620.9

-15 015 0

14.1

3 8

1.71.0

11.23.8

3.2

23.616.7

16.7

-15.0

21.014.5

4.60

30

Perc

ent

-23.8

-47.2

15.0-15.0

-19.7

-45.5

-23.6

-45.6

-60

-30

Sep.- Dec. 1998

Jan. - Aug. 1998

July - Dec. 1996

Jan.- Dec. 2000

AnnualizedJul. 1996 -Jun. 2011

Jan.- Dec.2002

Jan.- Dec. 2004

Jan.- Dec.2006

Jan.- Dec. 2008

Jan.- Dec. 2010

AXIOM 19AXIOMMSCI All Country ex US IndexInternational Equity Composite MSCI All Country ex US Index-Growth US S&P 500

Please see performance footnotes at the back of this document.

Jan. - Dec. 1998

Jan. - Dec. 1997

Jan. - Dec. 1999

Jan. - Dec. 2001

Jan.- Dec. 2003

Jan. - Dec. 2005

Jan.- Dec.2007

Jan.- Dec.2009

Jan.- Jun. 2011

THIS OVERVIEW DOES NOT CONSTITUTE AN OFFERING OF SECURITIES, WHICH CAN ONLY BE MADE BYDELIVERY OF AXIOM’S CONFIDENTIAL OFFERING MEMORANDUM TO QUALIFIED INVESTORS.

International Equity Performance Footnotes (page 1 of 2)

1. Axiom International Investors, LLC (Axiom) was founded on September 1, 1998 when a team of investment professionals separated fromColumbus Circle Investors, an affiliate of PIMCO Advisors Holdings, LP.

2. As of June 30, 2011, the International Equity Long Only Composite Performance is for a composite of 15 tax-exempt portfolios (two arecommingled funds) totaling $6,604.1 million in assets, which represents approximately 45.98% of total firm assets; and 2 taxableportfolios totaling $486.3 million which represents 3.39% of total assets; for a total of $7,090.4 million, representing 49.37% of overall firmassets. This composite (the "Axiom Composite") has been managed by Axiom since September 1, 1998 and is invested primarily ininternational equity securities. For the period July 1, 1996 through August 31, 1998 the composite consisted of five or fewer portfolios ofColumbus Circle Investors an affiliate of PIMCO Advisors Holdings that were managed by Andrew Jacobson with the assistance of othermembers of the Axiom investment team. From September 1, 1998 through February 20, 2000 Axiom continued to manage two portfolios as asub-advisor to the Circle Trust Company, an affiliate of PIMCO Advisors Holdings LP. The Axiom Composite is as of June 30, 2011p y, g p ,and valuation is based on trade date. Cash levels vary depending on a variety of factors including market conditions and investor activity. Itshould not be assumed that the cash levels presented here will necessarily be maintained in the future.

3. Top 10 holdings are for the Axiom International Equity Long Only Composite as June 30, 2011. It should not be assumed that theinvestment in the securities listed were or will be profitable or that recommendations made in the future will be profitable or equal theperformance of the securities on this list.performance of the securities on this list.

4. The results presented here reflect historical performance and are not a guarantee of future performance. Investment return and principal valuewill fluctuate and may be worth more or less than the original amount when liquidated. In addition you should be aware that:a. Performance results are presented before management fees but net of brokerage commissions.b. Results assume the reinvestment of dividends and other earnings.c Returns shown comply with GIPS Performance Presentation Standards for all periods presented and are verified thru 12/31/09c. Returns shown comply with GIPS Performance Presentation Standards for all periods presented and are verified thru 12/31/09.d. Performance results are shown after foreign withholding taxes on dividends, interest and capital gains.e. The Prior Composite and the Axiom Composite consist of investments in countries included in the Morgan Stanley Capital International

(MSCI) All Country World Index Ex US. The MSCI All Country World Index Ex US includes: the MSCI Europe, Australasia and FarEast Index (MSCI EAFE Index), the MSCI Emerging Market Index (the MSCI EM Index) and the MSCI Canada Index.

f. The performance of the benchmark indices represented are Gross Dividends for years prior to 2001 and Net Dividends for years2001 t t

AXIOM 20AXIOM

2001 to present.g. The composite was created on July 1, 1996.

International Equity Performance Footnotes (page 2 of 2)THIS OVERVIEW DOES NOT CONSTITUTE AN OFFERING OF SECURITIES, WHICH CAN ONLY BE MADE BYDELIVERY OF AXIOM’S CONFIDENTIAL OFFERING MEMORANDUM TO QUALIFIED INVESTORS.

4. (cont.)h. A client’s return will be reduced by the advisory fees and any other expenses incurred in the management of the investment advisory

account.i. Investment advisory fees are described in Part II of Axiom’s Form ADV.j. An Axiom International client’s return will be reduced by the investment advisory fee and any other expenses the client may incur in the

management of its investment advisory account. As a representative example of the effect an investment advisory fee, compounded over aperiod of years, could have on the total value of a client's portfolio, consider a $20 million portfolio earning 10% annually. The followingfigures would represent the hypothetical value of the portfolio at the end of the indicated period, presented gross and net of investmentadvisory fees (all figures in millions): First Year: Gross $22.00, Net $21.81. Third Year: Gross $26.62, Net $25.94. Fifth Year: Gross$32.21, Net $30.87. The current quoted fee schedule for International Equity portfolios (which is used in the representative example) is asfollows: 1.00% on the first $10.0 million; 0.90% on the next $15.0 million; 0.80% over $25.0 million.; ;

5. Results for the “Prior Composite” are for a composite of five or fewer portfolios of Columbus Circle Investors, then an affiliate of PIMCOAdvisors Holdings, that were managed by Andrew Jacobson with the assistance of other members of the Axiom investment team.

6. Results for the “Axiom Composite” are for a composite of the International Equity Long Only Composite (described in #2 above) of AxiomInternational Investors, formed as an independent entity on September 1, 1998.International Investors, formed as an independent entity on September 1, 1998.

7. Dispersion of returns within the Axiom International Equity Long-Only Composite, as of December 31, 2009, is 0.15 on an average annualbasis since inception, July 1, 1996.

AXIOM 21AXIOM

VI. PROXY VOTING

A. Introduction

Rule 206(4)-6 under the Advisers Act requires investment advisers that have voting authority with respect to securities held intheir clients’ accounts to exercise a duty of care by monitoring corporate actions and voting proxies To satisfy its duty of loyalty antheir clients accounts to exercise a duty of care by monitoring corporate actions and voting proxies. To satisfy its duty of loyalty, anadviser must cast proxy votes in the best interests of its clients and not in a way that advances the adviser’s interests above those of itsclients. In addition to these SEC requirements governing registered investment advisers, there are fiduciary standards andresponsibilities for ERISA accounts with respect to proxy voting that are set out in Department of Labor Bulletin 94-2, 29 C.F.R.2509.94-2 (July 29, 1994). Consistent with these requirements, Axiom has established Proxy Voting Policies and Guidelines, whichare attached here as Exhibit G and that apply to all proxy voting matters over which Axiom has voting authority.

A. Client Instructions

Each of the investment advisory contracts between Axiom and its Clients grant Axiom the exclusive right to vote proxies on itsClients’ behalf. However, certain Clients may elect in the future to retain proxy voting authority. Any specific instructions fromClients relating to proxy voting will be documented in the investment advisory contract.

AXIOM 22AXIOM

EXHIBIT G

Proxy Voting Policies and Guidelines

I. General Policies and Potential Conflicts of Interest A. General Policies Axiom International Investors, LLC (“Axiom”) has adopted these proxy voting policies and guidelines (the “Policies”) with respect tosecurities owned by clients for which Axiom serves as investment adviser and has the power to vote proxies. Rule 206(4) 6 under theInvestment Advisers Act of 1940 (the “Advisers Act”) requires investment advisers that have voting authority with respect to securities( ) q g y pheld in their clients’ accounts to exercise a duty of care by monitoring corporate actions and voting proxies. To satisfy its duty ofloyalty, an adviser must cast proxy votes in the best interests of its clients and not in a way that advances the adviser’s interests abovethose of its clients. In addition to these SEC requirements governing registered investment advisers, our proxy voting policies reflectthe long standing fiduciary standards and responsibilities for ERISA accounts set out in Department of Labor Bulletin 94 2, 29 C.F.R.2509.94 2 (July 29, 1994). The Policies are designed to reasonably ensure that Axiom votes proxies in the best interest of clients for which it has voting authority,and describe how Axiom addresses material conflicts between its interests and those of its clients with respect to proxy voting. Underthe Policies, Axiom will generally vote proxies by considering those factors that would affect the value of the securities held in clients’accounts. As a general matter, Axiom maintains a consistent voting position with respect to similar proxy proposals made by various issuers.However, Axiom recognizes that there are certain types of proposals that may result in different voting positions being taken withrespect to the different issuers. Some items that otherwise would be acceptable will be voted against the proponent when it is seekingextremely broad flexibility without offering adequate justification. In addition, Axiom generally votes consistently on the same matterwhen securities of an issuer are held by multiple client accounts. Axiom reviews proxy issues on a case by case basis, and there areinstances when our judgment of the anticipated effect on the best interests of our clients may warrant exceptions to the policies on

AXIOM 23AXIOM

instances when our judgment of the anticipated effect on the best interests of our clients may warrant exceptions to the policies onspecific issues set forth in Section II.

B. Conflicts of Interest Axiom is responsible for identifying potential conflicts of interest in the process of voting proxies on behalf of its clients. Examplesof potential conflicts of interest include situations where Axiom or personnel of Axiom: (1) provide services to a company whosemanagement is soliciting proxies; (2) have a material business relationship with a proponent of a proxy proposal and this businessrelationship may influence how the proxy vote is cast; or (3) have a business or personal relationship with participants in a proxycontest, corporate directors or candidates for directorships. Axiom may address material conflicts between its interests and those of its advisory clients by using any of the following methods: (1)adopting a policy of disclosing the conflict to clients and obtaining their consent before voting; (2) basing the proxy vote on predetermined voting guidelines if the application of the guidelines to the matter presented to clients involves minimal discretion on thedetermined voting guidelines if the application of the guidelines to the matter presented to clients involves minimal discretion on thepart of Axiom; or (3) using the recommendations of an independent third party. II. Axiom’s Policies on Specific Issues A. Golden Parachutes From time to time, shareholders of companies have submitted proxy proposals that would require shareholder approval of anyseverance packages for executive officers that exceed certain predetermined thresholds. Axiom generally votes in favor of suchshareholder proposals when they would require shareholder approval of any severance package for an executive officer that exceeds acertain percentage (e.g., 200%) of such officer’s annual compensation. B. Anti Takeover Measures Axiom generally votes against anti takeover measures. These take many forms from “poison pills” and “shark repellents” to boardclassification and super majority requirements. In general, any proposal that protects management from action by shareholders isvoted against.

AXIOM 24AXIOM

C Reincorporation and Reorganization Proposals C. Reincorporation and Reorganization Proposals When presented with a proposal to reincorporate a company under the laws of a different state, or to affect some other type ofcorporate reorganization, Axiom considers the underlying purpose and ultimate effect of such a proposal in determining whether or notto support such a measure. While Axiom generally votes in favor of appropriate management proposals, Axiom may oppose such ameasure if, for example, the intent or effect would be to create additional inappropriate impediments to possible acquisitions ortakeovers. D. Dilution Reasons for issuance of stock are many and most are legitimate. When a stock option plan (either individually or when aggregatedwith other plans of the same company) would substantially dilute the existing equity Axiom generally votes against the plan In caseswith other plans of the same company) would substantially dilute the existing equity, Axiom generally votes against the plan. In caseswhere management is asking for authorization to issue stock with no reason stated (a “blank check”), Axiom is very likely to voteagainst. In many cases, the unexplained authorization for common or preferred stock could work as a potential anti takeover device, again areason to vote against the authorization. E. Independence of Boards of Directors and Committees Thereof While Axiom acknowledges the potential benefits of a company’s inclusion of directors who are “independent” from management,Axiom generally opposes shareholder proposals that would require that a majority (or a “super majority”) of a company’s board becomprised of “independent” directors. Such proposals could inappropriately reduce a company’s ability to engage in certain types ofp p p p pp p y p y y g g yptransactions, could result in the exclusion of talented directors who are not deemed “independent,” or could result in the unnecessaryaddition of additional “independent” directors to a company’s board. However, in view of the special role and responsibilities of theaudit committee of a board of directors, Axiom generally supports proposals that would require that the audit committee be comprisedentirely of directors who are deemed “independent” of the company.

AXIOM 25AXIOM

F. Best Practices Standards Best practices standards have rapidly evolved in the corporate governance areas as a result of recent corporate failures, the SarbanesOxley Act of 2002 and revised listing standards on major stock exchanges. Axiom supports these changes. However, many issues arenot publicly registered, are not subject to these enhanced listing standards or are not operating in an environment that is comparable tothat in the United States. In reviewing proxy proposals under these circumstances, Axiom generally will support the enhancedstandards of corporate governance so long as we believe that within the circumstances of the environment within which the issuersoperate it is consistent with the best long term economic interests of our clients. G. Foreign Issuers – Share Blocking In accordance with local law or business practices, many foreign companies prevent the sales of shares that have been voted for acertain period beginning prior to the shareholder meeting and ending on the day following the meeting (“share blocking”) Dependingcertain period beginning prior to the shareholder meeting and ending on the day following the meeting ( share blocking ). Dependingon the country in which a company is domiciled, the blocking period may begin a stated number of days prior to the meeting (e.g.,one, three or five days) or on a date established by the company. While practices vary, in many countries the block period can becontinued for a longer period if the shareholder meeting is adjourned and postponed to a later date. Similarly, practices vary widely asto the ability of a shareholder to have the “block” restriction lifted early (e.g., in some countries shares generally can be “unblocked”up to two days prior to the meeting whereas in other countries the removal of the block appears to be discretionary with the issuer’s

f ) D h i i A i b l h b fi i li f i i i h i lltransfer agent). Due to these restrictions, Axiom must balance the benefits to its clients of voting proxies against the potentiallyserious portfolio management consequences of a reduced flexibility to sell the underlying shares at the most advantageous time. Inmany cases, the disadvantage of being unable to sell the stock regardless of changing conditions outweighs the advantages of voting atthe shareholder meeting for routine items. Accordingly, Axiom generally will not vote those proxies in the absence of an unusual,highly material vote. III. Procedures for Reviewing and Voting Proxies A. Procedures All proxy solicitations received by Axiom relating to securities held for client accounts are directed to Axiom’s Operations Manager.Upon receipt of a proxy solicitation the Operations Manager will determine whether each proposal in the proxy solicitation presents a

AXIOM 26AXIOM

Upon receipt of a proxy solicitation, the Operations Manager will determine whether each proposal in the proxy solicitation presents aroutine or non routine matter and whether any proposal presents a material conflict of interest between Axiom and its clients.

Any proposal that is determined by the Operations Manager to be routine (i.e., uncontested directors’ elections or appointment ofauditors) and that does not raise a material conflict of interest will be voted in favor of the proposal by the Operations Manager Anyauditors) and that does not raise a material conflict of interest will be voted in favor of the proposal by the Operations Manager. Anymatter determined by the Operations Manager to be non routine will be directed to the Chief Investment Officer and PortfolioManager (“Chief Investment Officer”) for consideration. The Chief Investment Officer, based on any input from personnel withinAxiom’s research group that the Chief Investment Officer determines is appropriate, will determine how proxies should be voted onnon routine matters. For non routine matters which are voted consistently with Axiom’s policies on specific issues in Section II of thePolicies (“Axiom’s Policies on Specific Issues”), the Chief Investment Officer will provide the Operations Manager writteni t ti di h t tinstructions regarding how to vote. For any non routine matter not voted according to Axiom’s Policies on Specific Issues or which is not addressed by Axiom’s Policieson Specific Issues, a memorandum (a “Supporting Memorandum”) that recites the material factors contributing to the voting decisionwith respect to that matter and explains why the vote is in the best interest of Axiom’s client(s) shall be prepared and kept with therecord of the proxy vote. The Operations Manager shall vote such proxies according to the instructions contained in the SupportingMemorandum. Any proposal for which the Operations Manager has determined a material conflict of interest exists between Axiom and its clientswill be directed to the Chief Investment Officer for consideration. The Chief Investment Officer will determine the appropriate votingresponse for such proposal by applying one of the methods identified in Section I.B. of the Policies. For each proposal for which amaterial conflict of interest exists the Chief Investment Officer shall prepare a memorandum (a “Material Conflict Memorandum”) tomaterial conflict of interest exists, the Chief Investment Officer shall prepare a memorandum (a Material Conflict Memorandum ), tobe kept with the record of the proxy vote, that identifies the material conflict of interest and the method used for determining how tovote on the proposal. The Operations Manager shall vote such proxies according to the instructions contained in the Material ConflictMemorandum. 1 Proxies for foreign issuers may contain voting items not typically presented in proxies of U.S. issuers that involve repetitive,

t i l tt d t d b l l l V ti it i l i titi t i l tt ill b d d ti

________________

non-controversial matters mandated by local law. Voting items involving repetitive, non-controversial matters will be deemed routineand the Operations Manager will vote in favor of such proposals by foreign issuers. Repetitive, non-controversial matters in foreignissuers’ proxies include: (i) receiving financial statements or other reports from the board; (ii) approving declarations of dividends;(iii) appointing shareholders to sign board meeting minutes; (iv) discharging management and supervisory boards; and (v) approvingshare repurchase programs.

AXIOM 27AXIOM

B. Amending Axiom’s Policies on Specific Issues

Axiom will periodically review Axiom’s Policies on Specific Issues to ensure that they contain appropriate guidance for determininghow votes will be cast on a variety of matters and the underlying rationale for such determinationhow votes will be cast on a variety of matters and the underlying rationale for such determination.

IV. Recordkeeping and Client Reporting In accordance with Rule 204-2 under the Advisers Act, Axiom shall retain the following documents for not less than five years fromthe end of the year in which the proxies were voted the first two years in Axiom’s office:the end of the year in which the proxies were voted, the first two years in Axiom s office:

1. The Policies and any additional procedures created pursuant to the Policies;

2. a copy of each proxy statement Axiom receives regarding securities held on behalf of its clients;

3. a record of each vote cast by Axiom on behalf of its clients;

4. a copy of any document created by Axiom that was material to making its voting decision or that memorializes the basis for such decision; and

5. a copy of each written request from a client, and response to the client, for information on how Axiom voted the client’s proxies.

Axiom shall provide a copy of Axiom’s Policies or information about how Axiom voted securities held in the client’s account, in eachcase if requested by the client.

AXIOM 28AXIOM

IV. BROKERAGE AND EXECUTION

A. Best Execution

1. Duty to Seek Best Execution

As an investment adviser with the authority to place Client trades, Axiom has a general fiduciary obligation to obtain besti f Cli h S C ll d ib b i d i i i h Cli ’execution for our Clients. The SEC generally describes best execution as a duty to execute securities transactions so that a Client’s

total cost or proceeds in each transaction are the most favorable under the circumstances. The duty begins with a requirement that anadviser should obtain the best price available for the securities in each transaction. After determining best price, an adviser is notnecessarily required to obtain the lowest possible commissions but may instead consider qualitative factors such as the broker’s orderexpertise, reputation, facilities and access to a particular trading market.

2. Selection of Brokers

Axiom selects brokers based on a variety of factors, including price, expertise, and willingness to handle large blocktransactions, the ability to accumulate positions in traded, smaller capitalization securities, execution ability, confidentiality, clearingcapabilities, reliability and financial responsibility. Axiom’s primary objective in the selection of executing brokers is to obtain thebest combination of price and execution in the market or markets involved. Transaction charges, including principal mark ups andp g g p p pmark downs, being a component of price, are also considered as a factor. Commission rates vary by country. Axiom seeks tonegotiate favorable commission rates on an ongoing basis with brokers in a particular country or geographic region. In selectingbrokers, Axiom also considers whether the broker provides support to the investment decision making process by making availableproducts and services that directly assist Axiom’s investment decision-making process. (See “Soft Dollars” below).

3. Monitoring Execution Qualityg Q y

Axiom will monitor the extent to which Clients are receiving best execution, including through the following procedures:

a. The Trading Department will monitor the execution of trade orders on a daily basis by telephone ande-mail. The Trading Department will track each order via live data-feed vendors to determine whetherthe executed price is within a tolerance level of 100 basis points above or below the volume weighted

AXIOM 29AXIOM

p p gaverage price (“VWAP”) for the time interval during which the trade was being worked. If the executed

trade falls outside of the VWAP tolerance level, a member of the Trading Department will call theexecuting broker to discuss the executed tradeexecuting broker to discuss the executed trade.

b. The Trading Department will include notes on the daily trade blotter regarding any trade executions thatthe Trading Department determines are particularly good or bad. The comments on the trade blotter willbe consolidated on a separate spreadsheet. If a broker provides poor execution, Axiom will considerappropriate corrective action, including speaking with the broker regarding the poor execution andredirecting brokerage business to other brokersredirecting brokerage business to other brokers.

c. Axiom monitors the quality of trade execution on an ongoing basis through communications by andamong the Research Department, Portfolio Managers and Trading Department regarding trade executionand related documentation (which may include by way of example documentation maintained by thetrader regarding capabilities of brokers in executing trades in certain countries or geographic regions;records maintained by the Operations Department regarding trade errors and settlement problems with aparticular broker and information from the Research Department regarding the quality of researchcoverage provided by a broker).

d. The Trading Department, Portfolio Managers and research analysts will conduct a review of brokeragetrade execution at least semi-annually. In conducting the review, Axiom will consider informationy g ,regarding the quality of trade execution on the spreadsheet prepared from the daily trade blotter and anyother information. Based on the review, each of the brokers will be ranked based on the quality ofexecution. The review will be documented and a copy of the review will be provided to the CCO and thePresident.

e. Axiom uses Bloomberg Trade Cost Analysis (BTCA) to review post trade execution statistics Thee. Axiom uses Bloomberg Trade Cost Analysis (BTCA) to review post trade execution statistics. Thesoftware allows Axiom to review both Axiom’s trader execution and the executing broker’s performanceagainst a variety of benchmarks including Arrival Price, VWAP, Limit Adjusted Interval VWAP, andMarket Impact Arrival Price. A log is kept of all trades which have both greater than 50 basis pointnegative variance and greater than $5,000 execution loss compared to the Limit Adjusted IntervalVWAP benchmark. The reason behind the variance is investigated and recorded. The log is maintainedb t di d i d b li

AXIOM 30AXIOM

by trading and reviewed by compliance.

The Trading Department maintains a monthly log that is distributed to the Portfolio Managers, Research Department andDirector of Client Service and Marketing that identifies each brokers, the dollar amount of commissions paid, the year to datepercentage of aggregate brokerage allocated to the broker, the percentage increase or decrease on a year-over-year basis, and dollaramount of soft dollars used.

B. Client Directed Brokerageg

Unless Clients give Axiom specific directions to the contrary, Axiom will select brokers through whom trades are executed.Clients may request that Axiom direct specific amounts of brokerage to a particular broker-dealer in connection with services renderedby those broker-dealers directly to the Client. Axiom adheres to the provisions of Section V of the AIMR Soft Dollar Standards withrespect to directed brokerage. Any Client directed brokerage instructions shall be in writing. Axiom provides disclosure in Part II ofForm ADV to the effect that certain Clients have client-directed brokerage arrangements that Axiom retains the duty to seek bestForm ADV to the effect that certain Clients have client-directed brokerage arrangements, that Axiom retains the duty to seek bestexecution for such Clients, and that any arrangements that require Axiom to commit a specified percentage of brokerage to a specifiedbroker may affect Axiom’s ability to seek to obtain best execution and obtain adequate records. Transactions for Clients with directedbrokerage arrangements should be executed through the broker-dealer selected by the Client to the extent so directed unless Axiomreasonably believes, after consultation with the Portfolio Managers and the CCO that effecting the transaction through the directedbroker may result in a breach of Axiom’s duties as a fiduciary. Client-directed brokerage is generally placed by Axiom at the sametime as trades for other Clients in similar securities are executed through Axiom. The Trading Department maintains a monthly logthat is distributed to the Portfolio Managers that identifies directed brokerage commissions.

C. Soft Dollar Policy

1. Regulatory Background

In general, brokerage commissions are client assets and should be used in accordance with fiduciary principles for the benefit of clients. However, investment advisers are permitted to enter into soft dollar arrangements, subject to certain restrictions. “Soft dollars” are credits that result from arrangements between broker-dealers and investment advisers where the broker provides the

AXIOM 31AXIOM

g padviser with both the execution of client brokerage transactions and research-related products and services. Section 28(e) of the Exchange Act provides a “safe harbor” for investment managers from claims that they breached a fiduciary duty owed to a client by

causing a client to pay higher commission costs in return for receipt of “brokerage and research services” that benefit the investmentmanager.

As a safe harbor, Section 28(e) cannot be violated but offers protection from violations that might otherwise be deemed tooccur under relevant law, including the Employee Retirement Income Security Act of 1974, as amended (“ERISA”). “Brokerage andresearch services” are defined to include any service which (i) furnishes advice, either directly or through publications or writings, asto the value of a security, the advisability of investing in, purchasing or selling a security, and the availability of the security orpurchasers/sellers of the security; (ii) furnishes analysis and reports concerning issuers, industries, securities, economic factors andtrends portfolio strateg and the performance of client acco nts; or (iii) effects sec rities transactions and performs f nctionstrends, portfolio strategy, and the performance of client accounts; or (iii) effects securities transactions and performs functionsincidental thereto (such as clearance settlement or custody) or required in connection with SEC rules or rules of a self-regulatoryorganization. The SEC has interpreted Section 28(e) as applying to products and services, as long as they provide “lawful andappropriate assistance to the money manager in carrying out investment decision-making responsibilities.”1

The SEC has stated that the research and brokerage services may be obtained either directly from the broker that receives thei i ( f f d “ i h”) hi d ( l h b k d h i icommissions (often referred to as “proprietary research”) or a third party (as long as the broker and not the investment manager is

required to pay the third party). The SEC has stated that the term “commission” in Section 28(e) of the Exchange Act includes notonly agency commissions but also a markup, markdown, commission equivalent or other fee paid by a managed account to a dealerfor executing a transaction where the fee and transaction price are fully and separately disclosed on the confirmation and thetransaction is reported under conditions that provide independent and objective verification of the transaction price subject toself-regulatory organization oversight.2g y g g

Axiom adheres to the voluntary AIMR Soft Dollar Standards (the “AIMR Standards”) in its use of soft dollars anduses soft dollars to pay for research services that directly aid in Axiom’s investment decision-making process. A copy of the AIMRStandards is attached to this Manual as Exhibit E.

The Portfolio Manager, the Operations Manager and the CCO must approve all new soft dollar arrangements. Soft dollarg , p g pp garrangements are reviewed on an ongoing basis by the Portfolio Manager, the Operations Manager and the CCO. On an annual basis, 1 The Investment Company Institute has urged the SEC to restrict the use of soft dollars by adopting a revised interpretation under Section 28(e) of theSecurities Exchange Act that would exclude certain products and services from the scope of the safe harbor under Section 28(e). These products and serviceswould include: computer hardware and software and other electronic communications facilities used in connection with trading or investment decision-making;publications including books periodicals newspapers and electronic publications that are available to the general public; and third party research services

________________

AXIOM 32AXIOM

publications, including books, periodicals, newspapers and electronic publications, that are available to the general public; and third-party research services.2 See SEC Interpretation: Commission Guidance on the Scope of Section 28(e) of the Exchange Act. (December 27, 2001).

all services are reviewed by the Portfolio Manager and Operations Manager to determine if those services should be renewed for they g p gnext year. Any services that have the capacity to be used both for the investment decision-making process and other purposes aredesignated as mixed-use products and calculations are done to ensure that only the portion of the overall expense attributable to theinvestment decision-making process is paid through soft dollars. Axiom maintains all mixed use schedules and these are reviewed bythe Operations Manager on a periodic basis. Axiom monitors and reconciles expenses paid and soft dollar commissions generated andmaintains copies of monthly soft dollar brokerage statements. When utilizing soft dollars for any trades, Axiom continues to ensurethat best execution is realized for each orderthat best execution is realized for each order.

Axiom’s soft dollar arrangements are currently provided through three broker dealers: UBS, Citigroup and Knight. Theservices include the following:

Factset: This service provides brokerage analysts’ estimates regarding company-specific items such as earnings, revenues, cashflows etcflows, etc.

Bloomberg: This is a computer system that enables Axiom to obtain real-time quotes of securities that are currently held in theportfolio, or securities looked at for investment purposes. It also enables Axiom to obtain historical pricing information, as well ascurrent and historical news items on securities.

First Call: This service provides company-specific research reports from various sourcesFirst Call: This service provides company specific research reports from various sources.

Note: Soft Dollars represented approximately 6.8% of total commissions for the Second Quarter, 2011 for the Axiom InternationalEquity Fund.

![WELCOME []...Emp B = $2350 Emp C = $500 Emp C = $3500 Emp D = $1500 Lag Quarter Emp D = $500 Claim filed Emp D = $150 The claimant must have been paid sufficient …](https://static.documents.pub/doc/80x56/607bc797dd97122c8938e959/welcome-emp-b-2350-emp-c-500-emp-c-3500-emp-d-1500-lag-quarter.jpg)