38

City of Miami General Employees’ and Sanitation Employees’ Retirement Trust Q2 2016

City of Miami General Employees’ and

Sanitation Employees’ Retirement Trust

Q2 2016

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 2

Introduction to Chicago Equity Partners

Experience More than 25 years of institutionally-focused investment management across equities and fixed income

Total of 39 employees with an average professional-level tenure at Chicago Equity Partners of 15 years

$9.6 billion in assets under management for more than 100 institutional clients around the world*

Discipline Focus on clearly-defined and process-oriented strategies which are repeatable and scalable

Deliberate approach to taking investment risks for which we believe our clients will be appropriately compensated

Long-standing commitment to continued innovation in our investment approach

Partnership Entire business platform built around delivering targeted solutions for sophisticated investors: we work with our clients to meet their investment objectives

Exceptional level of client service

Robust operational platform following industry best practices is the cornerstone of our long-term stability

*Assets under management as of June 30, 2016

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 3

Clients are our Top Priority

• AAA Allied Group, Inc.• Advocate Health Care• Bryan Health System• CHS Insurance, Ltd.• Consolidated Edison• The Dow Chemical Company• DTE Energy• Island Insurance Company, Ltd.• Marriott International, Inc.• NAMIC (National Association of Mutual Insurance

Companies)• The Sherwin Williams Company• Tempel Steel• ThedaCare Operating Fund• United Airlines• United Technologies Corporation• University Hospitals Health System• Walgreen Company• The Wooster Brush Company

• The Batchelor Foundation• Catholic Theological Union• Children’s Care Foundation• Diocese of Joliet• Diocese of Saginaw• The Diocese of St. Petersburgh• Dominican Sisters of Kenosha• Elks National Foundation• Friends Fiduciary Corporation• Gottlieb Memorial Foundation• The Hall-Perrine Foundation• Iowa Board of Regents• LaRabida Children’s Hospital• Lloyd A. Fry Foundation• Mennonite Education Agency• Misericordia Home Endowment• Missionary Servants of the Most Blessed Trinity• Moose Foundation

• Northwest Women’s Religious Investment Trust• Oklahoma Medical Research Foundation• Purdue University• The Regents of the University of Colorado• Rosalind Franklin University of Medicine and Science• Rush University Medical Center• Schoenstatt Sisters of Mary• Sisters of Charity of Saint Elizabeth New Jersey• Sisters of St. Casimir• Sisters of Saint Dominic• Sisters of Saint Francis of Assisi• The Smith Center for the Performing Arts• SSM International Finance• St. Procopius Abbey• Virginia Mennonite Retirement Community• Wallace H. Coulter Foundation

• Association of Washington Cities • California State Teachers’ Retirement System• The Chicago Housing Authority• City of Miami General Employees' and Sanitation

Employees' Retirement Trust• City of Springfield Police Pension Fund• Commonwealth of Massachusetts Deferred

Compensation Plan• Cook County Employees’ Annuity and Benefit Fund• Firemen’s Annuity and Benefit Fund of Chicago• Illinois State Board of Investment• Intergovernmental Risk Management Agency• Knox County Retirement System• Lake Forest Police Pension Fund• Los Angeles Fire & Police Pension System• Nevada Higher Education Pre-paid Tuition Program• Nevada State Treasurer• New Orleans (LA) Sewerage & Water Board Pension• Park Employees' Annuity & Benefit Fund of Chicago• Puerto Rico Government Employees and Judiciary

Retirement Systems

• Public School Retirement System of the City of St. Louis

• Retirement Plan for CTA Employees• State Universities Retirement System of Illinois• WorkSafeNB

• Bakery Drivers & Salesman Local 194& Industry Pension Fund

• Chicago Area I.B. Of T. Benefit Trust Funds • Chicago Regional Council of Carpenters Millmen

Pension Fund• Des Moines Iron Workers Local 67• District #9 I.A.M.A.W. Pension Trust• I.B.E.W. Local #9 and Outside Contractors Pension

Fund• Midwest Operating Engineers’ Welfare Fund• North Central Illinois Laborers Health & Welfare Fund• NYC Local 237 International Brotherhood of

Teamsters• Painters and Allied Trades District Council #35 Trust

Funds• Southern States Savings and Retirement Plan Trust• Teamsters Local #705 Pension and

Health & Welfare Funds• Uniformed Firefighter's Association (NYC)

• AMG Funds • Bank of Hawaii• Jackson National Asset Management, LLC

The above client list is a representative sample of clients with assetsof $5 million or greater under management who have given CEPpermission to use their name as of June 30, 2016. It is not knownwhether the listed clients approve or disapprove of Chicago EquityPartners or the advisory services provided.

Corporations

Endowments & Foundations

Public Funds

Taft-Hartley

Mutual Funds / Subadvisory

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 4

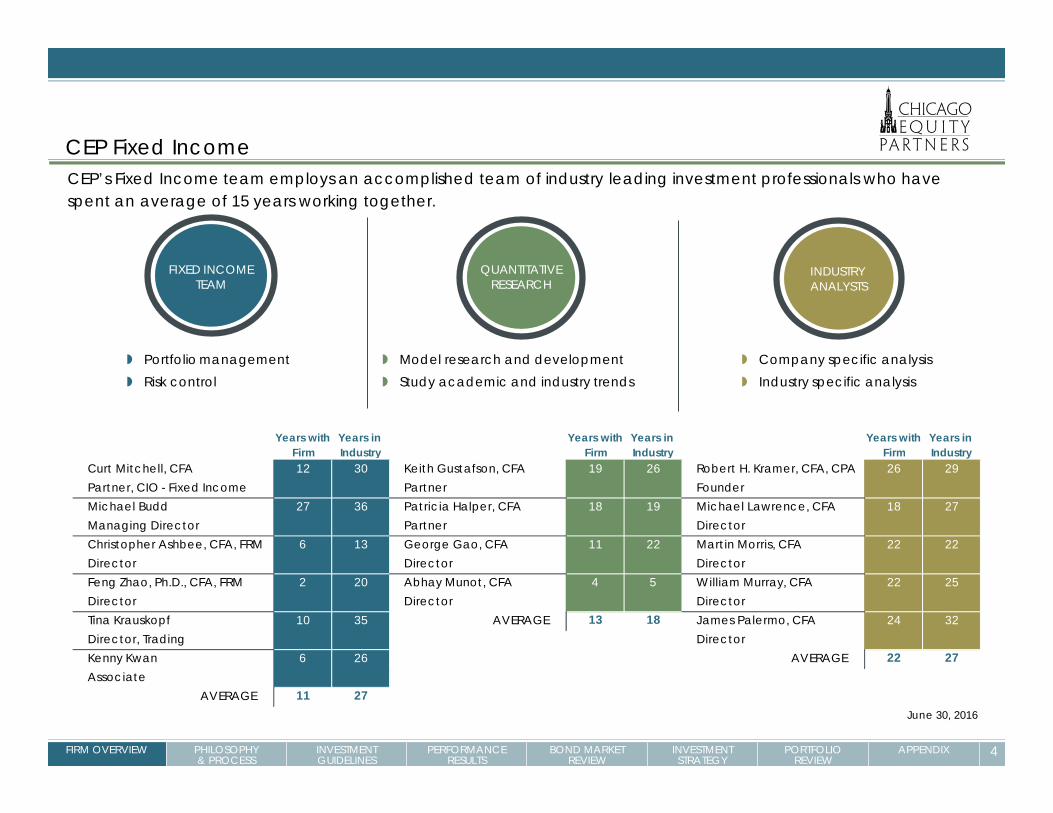

CEP Fixed IncomeCEP’s Fixed Income team employs an accomplished team of industry leading investment professionals who have spent an average of 15 years working together.

FIXED INCOMETEAM

QUANTITATIVERESEARCH

INDUSTRY ANALYSTS

Portfolio management Risk control

Model research and development Study academic and industry trends

Company specific analysis Industry specific analysis

Years with Years in Years with Years in Years with Years in Firm Industry Firm Industry Firm Industry

Curt Mitchell, CFA 12 30 Keith Gustafson, CFA 19 26 Robert H. Kramer, CFA, CPA 26 29Partner, CIO - Fixed Income Partner FounderMichael Budd 27 36 Patricia Halper, CFA 18 19 Michael Lawrence, CFA 18 27Managing Director Partner DirectorChristopher Ashbee, CFA, FRM 6 13 George Gao, CFA 11 22 Martin Morris, CFA 22 22Director Director DirectorFeng Zhao, Ph.D., CFA, FRM 2 20 Abhay Munot, CFA 4 5 William Murray, CFA 22 25Director Director DirectorTina Krauskopf 10 35 AVERAGE 13 18 James Palermo, CFA 24 32Director, Trading DirectorKenny Kwan 6 26 AVERAGE 22 27Associate

AVERAGE 11 27June 30, 2016

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 5

Fixed Income Investment Philosophy

Our Core Beliefs Yield wins over time, but not all the time.Our rigorous research allows us to add value through sector allocation by identifying when we are being appropriately compensated for taking credit risk.

Changes in fundamentals drive security selection returns.The analysis of forward-looking measures of credit quality allows us to identify companies that we believe will outperform and avoid those that will underperform.

Risk management is critical to success.Minimizing downside risk and avoiding permanent loss of principal are primary goals.

Outcomes Our research-oriented and disciplined investment process focuses on fundamentals and valuations.

A countercyclical, value-driven approach produces excess returns primarily through sector allocation and security selection rather than a static overweight to risky positions or interest rate timing.

Returns are highly correlated to the overall bond market, but excess returns are generally often lowly or negatively correlated to bond manager peers.

We believe the role of fixed income is to provide principal preservation, income, and risk reduction through diversification.

This philosophy is the foundation of our investment process and makes our firm unique.

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 6

Fixed Income Investment Process

SectorAllocation

Sector and quality decisions incorporate fundamental, valuation, and momentum / sentiment market conditions.

Security Selection

Risk-budgeting framework measures magnitude of each excess return strategy on a forward-looking basis, while attribution provides real-time feedback.

2

Risk Management

3

1STRUCTURED

ANDDISCIPLINED

Security and industry selection research combines quantitative equity-based inputs with qualitative insight from analysts.

We combine multiple strategies in areas where we have repeatedly demonstrated skill to produce consistent results.

TOP DOWN BOTTOM UP

DOWNSIDE PROTECTION

Our investment process produces consistent returns while limiting risk.

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 7

Investment Guidelines

High Quality Intermediate Fixed Income

Benchmark Barclays Intermediate Government Credit Index

Fixed Income Securities

The fixed income portion of the Trust shall be invested in marketable, fixed income securities. Corporate bond issues shall be diversified by industry and in number so that no investment in the securities of a single issue shall exceed 7% (at market) of the value of the portfolio. Single industry weightings will be a maximum of 25%, except US Government and agency securities.

Fixed income investments are expected to preserve capital and provide a high level of income on a consistent basis.

The fixed income investments shall be appropriately diversified although the investment manager may engage in "active" bond management. It is therefore anticipated that there may be turnover as shifts are made between and within sectors, quality and maturity.

Average duration of the fixed income asset class will be targeted within a range of three to ten years. Each manager is expected to keep duration at +/- one year of the benchmark duration.

Permissible Direct Investments:

Commercial Paper of only the highest quality shall be used when invested on an individual basis Certificates of Deposit of the top 100 national banks, so long as they are stated on the Controller's list Bankers Acceptances United States Treasury Bonds, Notes and Bills

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 8

Investment Guidelines

Permissible Direct Investments:

Repurchase agreements with U.S. Treasury Securities and agencies of the U.S. Government as collateral (marking to the market daily). The investment policy shall require all approved institutions and dealers transacting repurchase agreements to execute and perform as stated in the Master Repurchase Agreement. All repurchase agreement transactions shall adhere to the requirements of the Master Repurchase Agreement.

Debt instruments issued or backed by agencies of/or guaranteed by the U.S. Government All investment grade corporate debt issues including those rated Baa3/BBB- better by Moody's Investors

Services and/or Standard and Poors Corporation. In the case of a split rating, the higher rating shall apply. Securities downgraded subsequent to purchase resulting in violations of quality guidelines may be held at the manager's discretion subject to the high yield limitations indicated below.

Mortgages, including agency, non-agency, commercial backed securities and CMO’s (as long as all other provisions are met).

Futures (but must not exceed 15% without prior approval by the Board) and Options. However, these securities may not be used to leverage or hedge the portfolio.

Preferred Stock Municipal Bonds Asset backed securities Yankee bonds/foreign credits Commingled and mutual funds Eurodollar bonds 20% maximum of each manager’s portfolio may be invested in aggregate to Yankee bonds, Foreign credits,

Eurodollar bonds and Rule 144A Securities. 20% maximum of each manager’s portfolio may be invested in high yield securities (with ratings of CCC or

better).

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 9

Investment Guidelines

Excluded Direct Investments:Private Placements

Debt to Equity exchanges

Investment managers are not authorized to use derivative securities, or strategies that do not comply with the basic investment objectives of this policy, i.e., an emphasis on the preservation of principal consistent with conservative growth of assets. Managers are specifically prohibited from using derivative or synthetic securities whose characteristics as implemented by the manager include potentially high price volatility and whose returns are speculative or leveraged (when considered together with liquid/short-term securities positions) or whose marketability may be severely limited, without written authority from the Board.

10FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 10

Portfolio Performance

*Trailing periods ending June 30, 2016

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Q2 2016 FYTD** 1 Year 2 Years 3 Years 5 Years SinceInception

Portfolio 1.27% 2.90% 4.25% 3.06% 2.58% 2.60% 3.19%Benchmark 1.58% 3.35% 4.33% 3.00% 2.95% 2.90% 3.40%Excess -0.31% -0.45% -0.08% 0.06% -0.37% -0.30% -0.21%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

YTD2016 2015 2014 2013 2012 2011 2010 2009***

Portfolio 3.75% 1.24% 2.96% -2.05% 2.85% 6.98% 5.97% -0.21%Benchmark 4.07% 1.07% 3.13% -0.86% 3.89% 5.80% 5.89% -0.14%Excess -0.32% 0.17% -0.17% -1.19% -1.04% 1.18% 0.08% -0.07%

Calendar Year Returns

Portfolio Market Value: $38,276,218

Performance results are gross of fees. Periods over one year are annualized.Performance start date: October 31, 2009*Time weighted and year-to-date returns for periods ending June 30, 2016**Fiscal Year-To-Date is as of September 30, 2015***Return is for partial period beginning October 31, 2009 and ending December 31, 2009

Barclays Capital Inter. Govt/Credit

City of Miami GESE

11FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 11

Barclays Excess Return

Sector Excess Returns

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

Sovereign Corporate CMBS Mortgage U.S. Agency

Corporate Maturity Excess Returns

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1-3 Yr 3-5 Yr 5-7 Yr 7-10 Yr 10 Yr > 25 Yr >

Corporate Industry Excess Returns

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

FinancialsUtilitiesIndustrials

Quality Excess Returns

0.0%0.2%0.4%0.6%0.8%1.0%1.2%1.4%1.6%1.8%

Baa A AA

Note: Excess returns shown are for Index sectors within Barclays U.S. Aggregate Index relative to duration equivalent Treasuries. Source: Barclays for 4/1/16-6/30/16

12FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 12

High Quality Intermediate Fixed Income Excess Return

Outperformance

Underperformance

High Quality Intermediate Vs. Barclays Intermediate Government/Credit IndexRolling 5 year gross returns since inception (Q1 1996)*

See attached disclosure in the Appendix. Supplemental information offered is in addition to our performance presentation data and disclosures. Past performance is not indicative of future results. * Data is based on quarterly five year rolling annualized returns since inception through 6.30.16.

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0%

High

Qua

lity

Inte

rmed

iate

Barclays Capital Int Govt/Credit

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 13

Bond Market Review and Outlook

Fed Policy The Fed’s Quantitative Easing program increased the valuation of risk assets but not economic growth.

Policy divergence has caused the dollar to rise, which has led to a significant tightening in global financial conditions.

This tightening has offset additional stimulus efforts from the European Central Bank and Bank of Japan.

The Fed has reduced their projections of rate increases because of global political and economic uncertainty.

There is growing concern that central bank policies are becoming less effective.

Fundamentals Global growth remains weak, especially in Europe, Asia, and emerging markets.

Emerging markets now account for almost half of global demand.

Debt remains a drag on growth as debt-to-GDP ratios have increased in all advanced economies since 2007.

Earnings declines started in commodity-related industries but are now broad-based.

As revenue and earnings turn negative, many companies are using stock buybacks and M&A to appease shareholders.

Credit quality deterioration and tightening lending standards indicate we are well past the peak in the credit cycle.

Valuations Credit spreads are approaching levels that historically have been an attractive entry point.

Treasury yields, while still low by historical standards, offer value when compared to foreign government bond markets.

Momentum /Sentiment

Without a recovery in underlying fundamentals, it will be difficult for the recent outperformance in risk assets to continue.

Increased global uncertainty will lead to continued bouts of volatility and risk aversion.

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 14

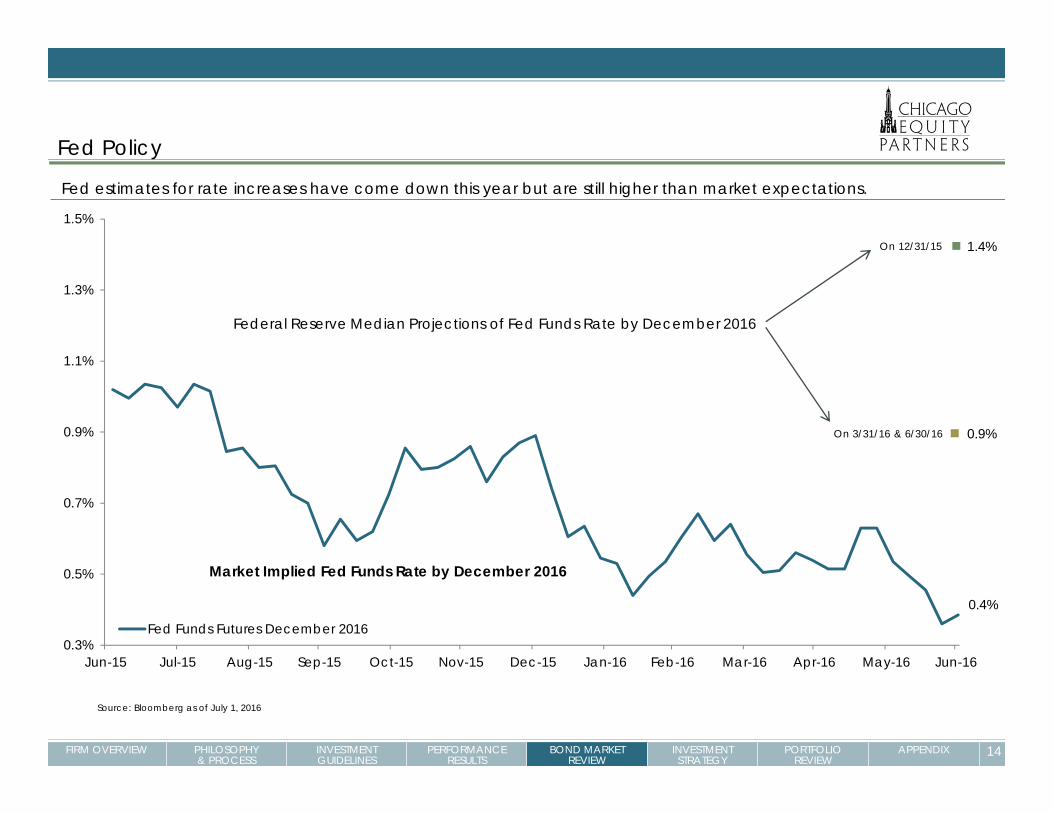

Fed Policy

Fed estimates for rate increases have come down this year but are still higher than market expectations.

0.3%

0.5%

0.7%

0.9%

1.1%

1.3%

1.5%

Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

Fed Funds Futures December 2016

Market Implied Fed Funds Rate by December 2016

Federal Reserve Median Projections of Fed Funds Rate by December 2016

Source: Bloomberg as of July 1, 2016

0.9%

0.4%

1.4%On 12/31/15

On 3/31/16 & 6/30/16

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 15

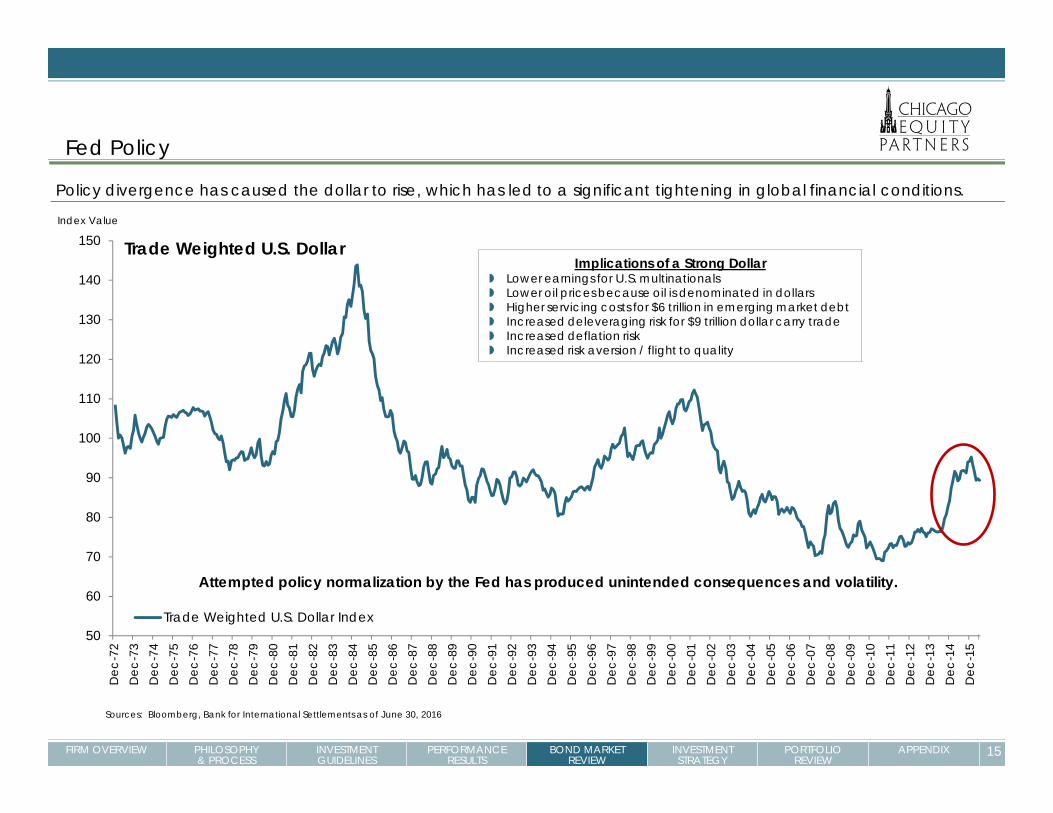

Policy divergence has caused the dollar to rise, which has led to a significant tightening in global financial conditions.

50

60

70

80

90

100

110

120

130

140

150

Dec

-72

Dec

-73

Dec

-74

Dec

-75

Dec

-76

Dec

-77

Dec

-78

Dec

-79

Dec

-80

Dec

-81

Dec

-82

Dec

-83

Dec

-84

Dec

-85

Dec

-86

Dec

-87

Dec

-88

Dec

-89

Dec

-90

Dec

-91

Dec

-92

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Trade Weighted U.S. Dollar Index

Implications of a Strong Dollar Lower earnings for U.S. multinationals Lower oil prices because oil is denominated in dollars Higher servicing costs for $6 trillion in emerging market debt Increased deleveraging risk for $9 trillion dollar carry trade Increased deflation risk Increased risk aversion / flight to quality

Sources: Bloomberg, Bank for International Settlements as of June 30, 2016

Attempted policy normalization by the Fed has produced unintended consequences and volatility.

Index Value

Trade Weighted U.S. Dollar

Fed Policy

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 16

Fundamentals

Growth in government and nonfinancial corporate debt has offset deleveraging in the financial and household sectors.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Dec

-90

Dec

-92

Dec

-94

Dec

-96

Dec

-98

Dec

-00

Dec

-02

Dec

-04

Dec

-06

Dec

-08

Dec

-10

Dec

-12

Dec

-14

Government Debt

Financial Corporate DebtHousehold Debt

Non-Financial Corporate Debt

Sources: Federal Reserve, Bloomberg as of March 31, 2016

$Billions

Leverage

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 17

FundamentalsOutside of recessions, significant earnings declines in the S&P 500 are rare.

Source: Standard & Poor’s, NBER, and FactSet as of June 30, 2016

-11.6%

-80% -70% -60% -50% -40% -30% -20% -10% 0% 10%

TelecomConsumer Disc

UtilitiesHealthcare

Consumer StaplesIndustrialsFinancials

S&P 500Info TechMaterials

Energy

Earnings declines started with commodity-related industries but are now broad-based.S&P 500 Q2 2016 Earnings Estimates

S&P 500 12-Month Operating EPS Year-over-Year Percent Change

Shaded areas represent recessions-50%

-25%

0%

25%

50%

75%

100%

Dec-89 Dec-91 Dec-93 Dec-95 Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 18

Fundamentals

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Jun-

81

Jun-

82

Jun-

83

Jun-

84

Jun-

85

Jun-

86

Jun-

87

Jun-

88

Jun-

89

Jun-

90

Jun-

91

Jun-

92

Jun-

93

Jun-

94

Jun-

95

Jun-

96

Jun-

97

Jun-

98

Jun-

99

Jun-

00

Jun-

01

Jun-

02

Jun-

03

Jun-

04

Jun-

05

Jun-

06

Jun-

07

Jun-

08

Jun-

09

Jun-

10

Jun-

11

Jun-

12

Jun-

13

Jun-

14

Jun-

15

Jun-

16

Chicago Fed National Activity Diffusion Index

Given where we are in the current business cycle, it is prudent to be cautious in the near-term but looking for opportunities over the intermediate-term.

Source: Bloomberg as of June 30, 2016

Mid-Cycle Slowdown Mid-Cycle Slowdown

Mid-Cycle Slowdown

Mid-Cycle Slowdown

RECESSION RECESSION

RECESSION

RECESSION

Recession Threshold

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 19

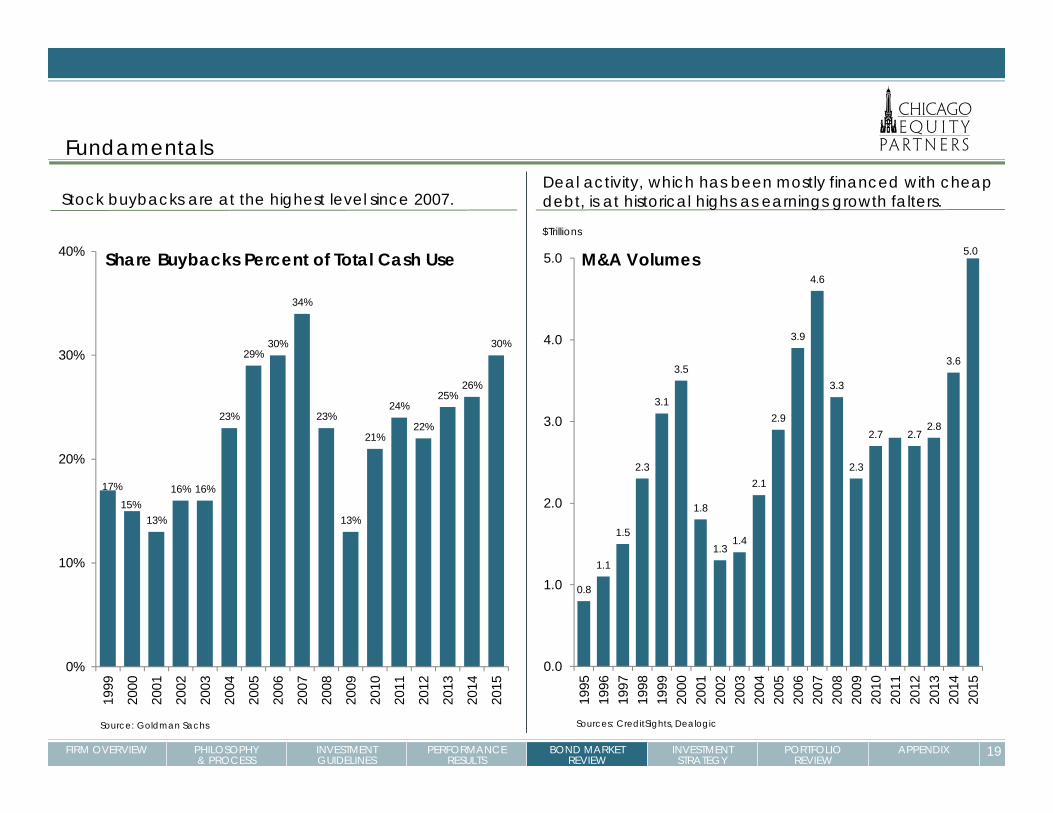

Stock buybacks are at the highest level since 2007.

17%

15%13%

16% 16%

23%

29%30%

34%

23%

13%

21%

24%

22%

25%26%

30%

0%

10%

20%

30%

40%

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Source: Goldman Sachs

0.8

1.1

1.5

2.3

3.1

3.5

1.8

1.31.4

2.1

2.9

3.9

4.6

3.3

2.3

2.7

5.0

2.72.8

3.6

0.0

1.0

2.0

3.0

4.0

5.0

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Sources: CreditSights, Dealogic

$Trillions

Deal activity, which has been mostly financed with cheap debt, is at historical highs as earnings growth falters.

Share Buybacks Percent of Total Cash Use M&A Volumes

Fundamentals

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 20

Fundamentals

We are past the peak in the credit cycle and heading toward the trough.

Sources: Bloomberg, Federal Reserve as of July 31, 2016

100

300

500

700

900

1100

1300

1500

-35

-15

5

25

45

65

85

Oct

-90

Oct

-91

Oct

-92

Oct

-93

Oct

-94

Oct

-95

Oct

-96

Oct

-97

Oct

-98

Oct

-99

Oct

-00

Oct

-01

Oct

-02

Oct

-03

Oct

-04

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

% Banks Tightening Lending forSmall Business Loans (LHS)

High Yield Spread (RHS)

% of Lenders Tightening Basis Points

Banks Tightening Lending Standards versus High Yield Spread

Credit spreads start to widen materially once lending standards move to a net tightening position (above 0).

This occurred in Q4 2015.

Jul-1

6

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 21

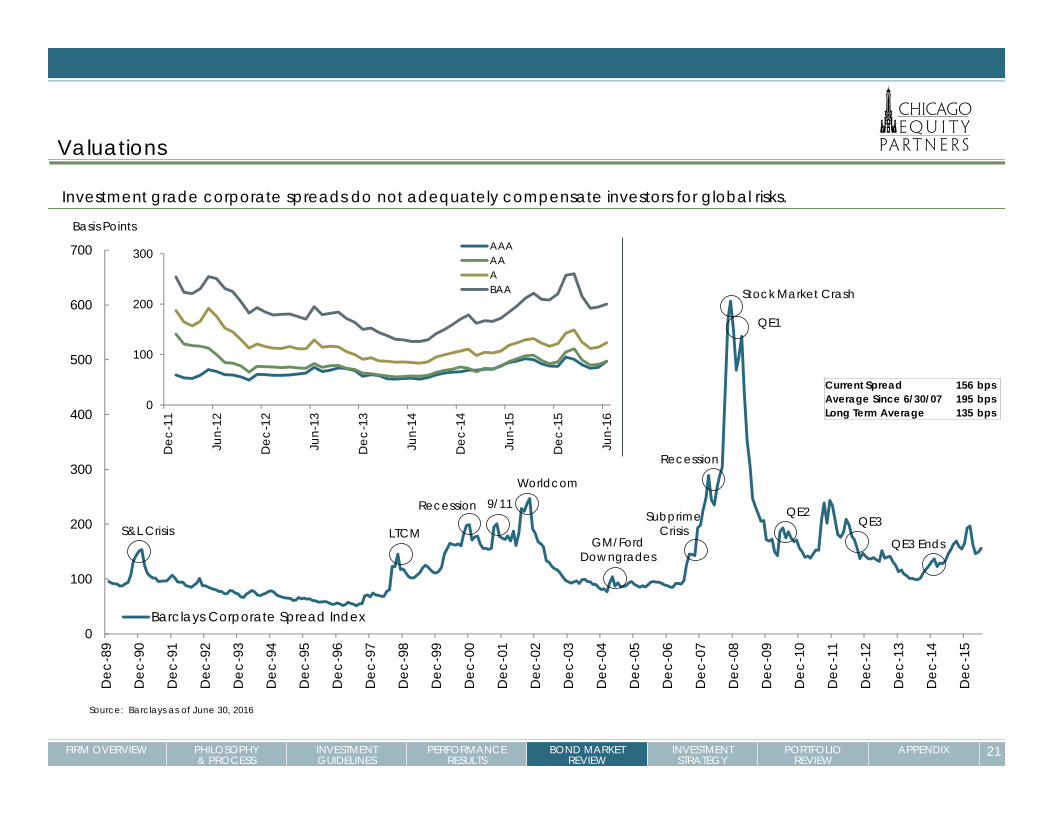

Valuations

0

100

200

300

400

500

600

700

Dec

-89

Dec

-90

Dec

-91

Dec

-92

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Barclays Corporate Spread Index

Investment grade corporate spreads do not adequately compensate investors for global risks.

Basis Points

Stock Market Crash

QE1

Source: Barclays as of June 30, 2016

Recession

Subprime Crisis

Worldcom

Recession

LTCMS&L CrisisQE29/11

QE3

GM/Ford Downgrades

Current Spread 156 bpsAverage Since 6/30/07 195 bpsLong Term Average 135 bps

QE3 Ends

0

100

200

300

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

Jun-

14

Dec

-14

Jun-

15

Dec

-15

Jun-

16

AAAAAABAA

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 22

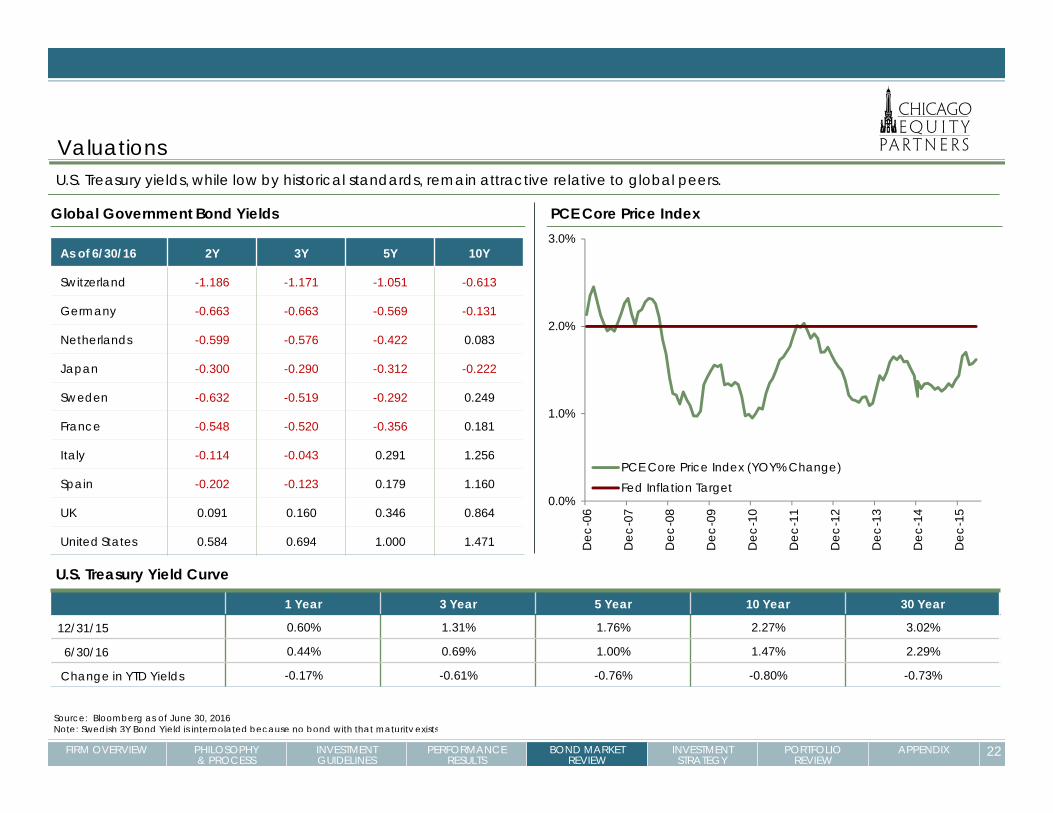

ValuationsU.S. Treasury yields, while low by historical standards, remain attractive relative to global peers.

Source: Bloomberg as of June 30, 2016Note: Swedish 3Y Bond Yield is interpolated because no bond with that maturity exists

1 Year 3 Year 5 Year 10 Year 30 Year

12/31/15 0.60% 1.31% 1.76% 2.27% 3.02%

6/30/16 0.44% 0.69% 1.00% 1.47% 2.29%

Change in YTD Yields -0.17% -0.61% -0.76% -0.80% -0.73%

0.0%

1.0%

2.0%

3.0%

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

PCE Core Price Index (YOY% Change)Fed Inflation Target

Global Government Bond Yields PCE Core Price Index

As of 6/30/16 2Y 3Y 5Y 10Y

Switzerland -1.186 -1.171 -1.051 -0.613

Germany -0.663 -0.663 -0.569 -0.131

Netherlands -0.599 -0.576 -0.422 0.083

Japan -0.300 -0.290 -0.312 -0.222

Sweden -0.632 -0.519 -0.292 0.249

France -0.548 -0.520 -0.356 0.181

Italy -0.114 -0.043 0.291 1.256

Spain -0.202 -0.123 0.179 1.160

UK 0.091 0.160 0.346 0.864

United States 0.584 0.694 1.000 1.471

U.S. Treasury Yield Curve

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 23

Credit Sector Scorecard

Category Indicator Implications for Credit Spreads

Fundamentals Treasury Curve Slope Absolute Level Neutral

Treasury Curve Slope Relative Level Tighter

Credit Curve Slope Wider

Leverage Wider

Lending Standards Wider

Valuations High Yield Market Pricing Tighter

Quality Spread Tighter

Momentum / Sentiment Credit Sector Excess Return Trend Tighter

Stock Market Volatility Wider

Our credit sector scorecard incorporates fundamental, valuation and momentum/sentiment factors.

As of June 30, 2016

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 24

Credit Sector Allocation Decisions: 2006-Present

0

100

200

300

400

500

600

700

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Barclays Investment Grade Corporate Spread

Our disciplined sector allocation process has been successful over full market cycles.

Trend Reversal as Market Reacts to

End of QE

Beginning of Central Bank “whatever it

takes” policies

Our only periods of underperformance

are when investors are “reaching for yield.”

UNDERWEIGHT OVERWEIGHT UNDERWEIGHT

Source: Barclays as of June 30, 2016

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 25

Investment Strategy and Portfolio Positioning

We are selectively adding to credit

Uncertainty remains over the sustainability of an economic recovery without continued government support.

QE distorted the valuation of risk assets and spread levels are now moving wider to better reflect weak fundamentals.

We will monitor inputs to our investment process for indications of improving conditions and opportunities.

Corporate holdings are focused on high quality, liquid issues

Energy has been underweighted and holdings emphasize the major integrated issuers.

Negative event risk from shareholder enhancement and M&A activity continues to be a headwind for credit investors.

Large capitalization issuers have been emphasized.

Underweights include banks, foreign/sovereign, lower quality, and illiquid issuers.

Governments provide liquidity and stability

Governments are overweighted to provide liquidity for opportunities in credit.

This will serve us well in an environment of greatly reduced liquidity.

Duration / Yield Curve

Increased interest rate volatility due to uncertainty regarding the Fed’s actions is likely.

This has led us to maintain duration and maturity distributions close to the benchmark.

We believe we are well-positioned to increase our credit exposure opportunistically in coming months.

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 26

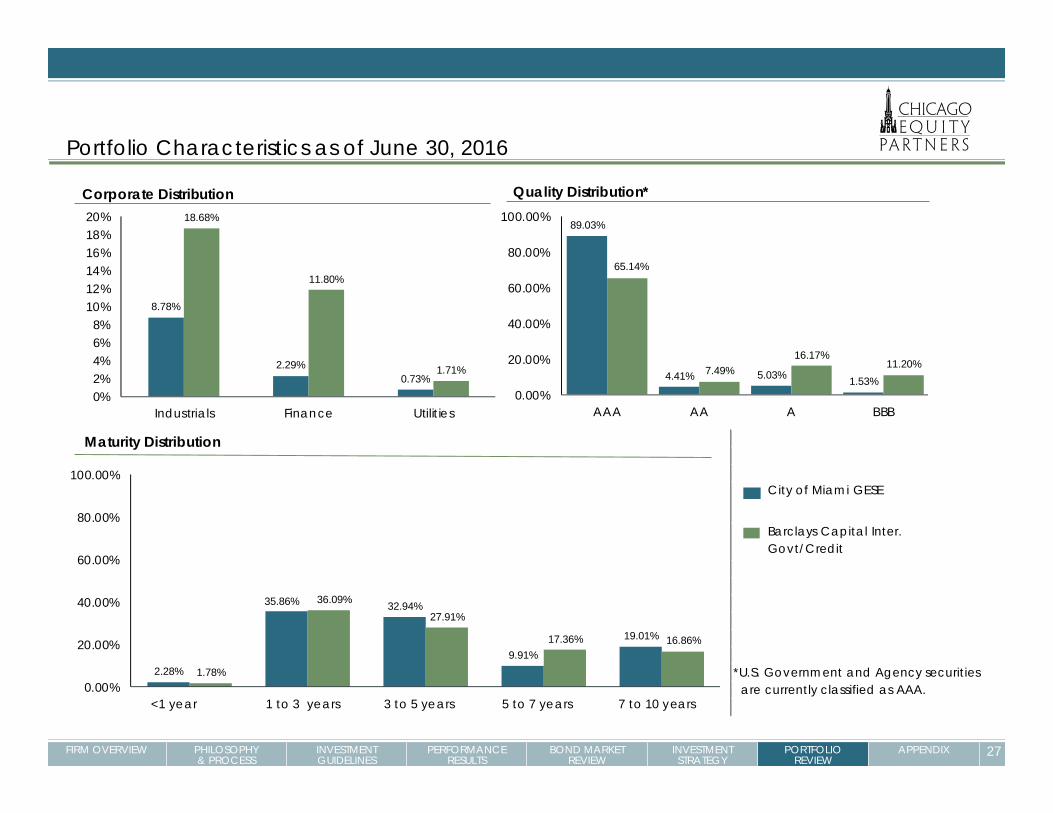

Portfolio Characteristics as of June 30, 2016

Sector +/-Treasury 26.99%U.S. Agency 0.50%Corporate -20.39%Other Credit -7.40%Cash 0.30%

City of Miami GESE

Yield-to-Maturity 0.97%

Duration 4.01

Non-Treasury Sectors 16.67%

Average Quality Aaa

Number Of Issues 68 Other Credit category includes Local Authorities, Sovereigns, Supranationals and Foreign Agency.

Well-diversified

Barclays Capital Inter. Govt/Credit

Barclays Capital Inter. Govt/Credit

+ / - 10%

City of Miami GESE Exposure

Exposure

Lower

Underweight

Higher

1.39%

4.00

43.66%

Aa2

5,113

Treasury83.33%

U.S. Agency4.57%

Corporate11.80%

Cash0.30%

Treasury56.34%

U.S. Agency4.07%

Corporate32.19%

Other Credit7.40%

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 27

Portfolio Characteristics as of June 30, 2016

*U.S. Government and Agency securities are currently classified as AAA.

City of Miami GESE

Barclays Capital Inter. Govt/Credit

8.78%

2.29%0.73%

18.68%

11.80%

1.71%

0%2%4%6%8%

10%12%14%16%18%20%

Industrials Finance Utilities

Corporate Distribution

2.28%

35.86% 32.94%

9.91%

19.01%

1.78%

36.09%27.91%

17.36% 16.86%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

<1 year 1 to 3 years 3 to 5 years 5 to 7 years 7 to 10 years

Maturity Distribution

89.03%

4.41% 5.03% 1.53%

65.14%

7.49%16.17%

11.20%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

AAA AA A BBB

Quality Distribution*

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX 28

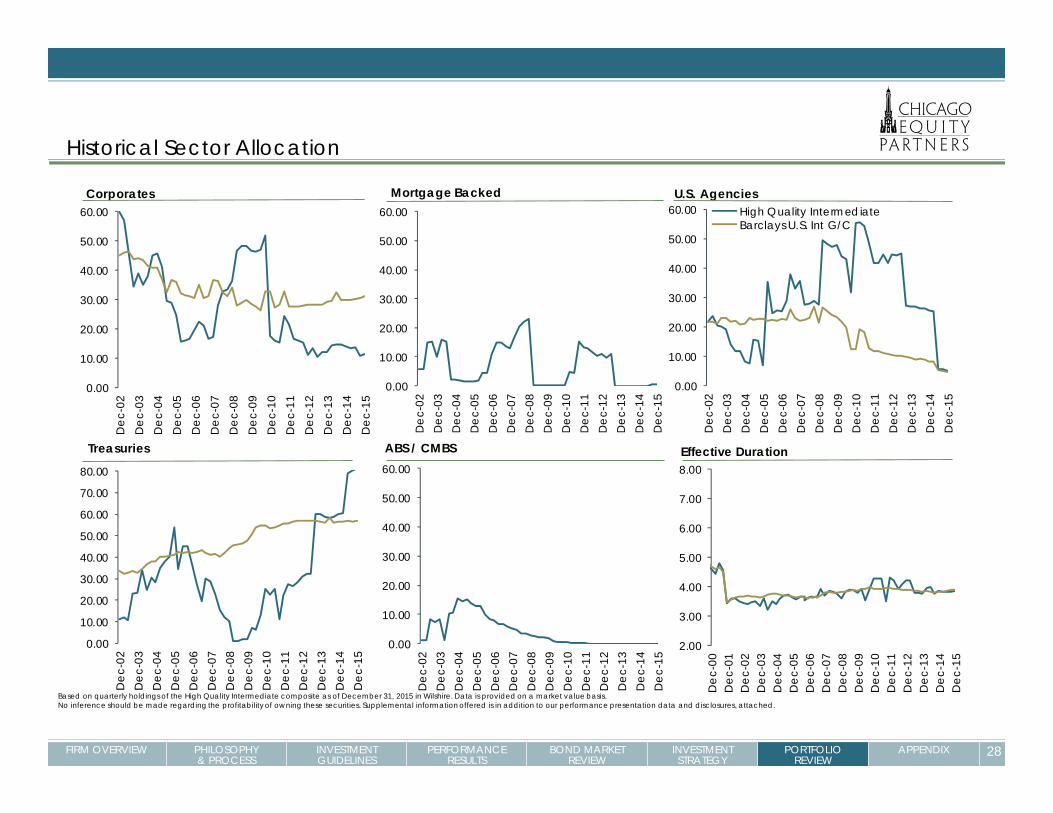

Historical Sector Allocation

Based on quarterly holdings of the High Quality Intermediate composite as of December 31, 2015 in Wilshire. Data is provided on a market value basis.No inference should be made regarding the profitabilityof owning these securities. Supplemental information offered is in addition to our performance presentation data and disclosures, attached.

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Corporates

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Mortgage Backed

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

U.S. AgenciesHigh Quality IntermediateBarclays U.S. Int G/C

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Treasuries

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

ABS / CMBS

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Effective Duration

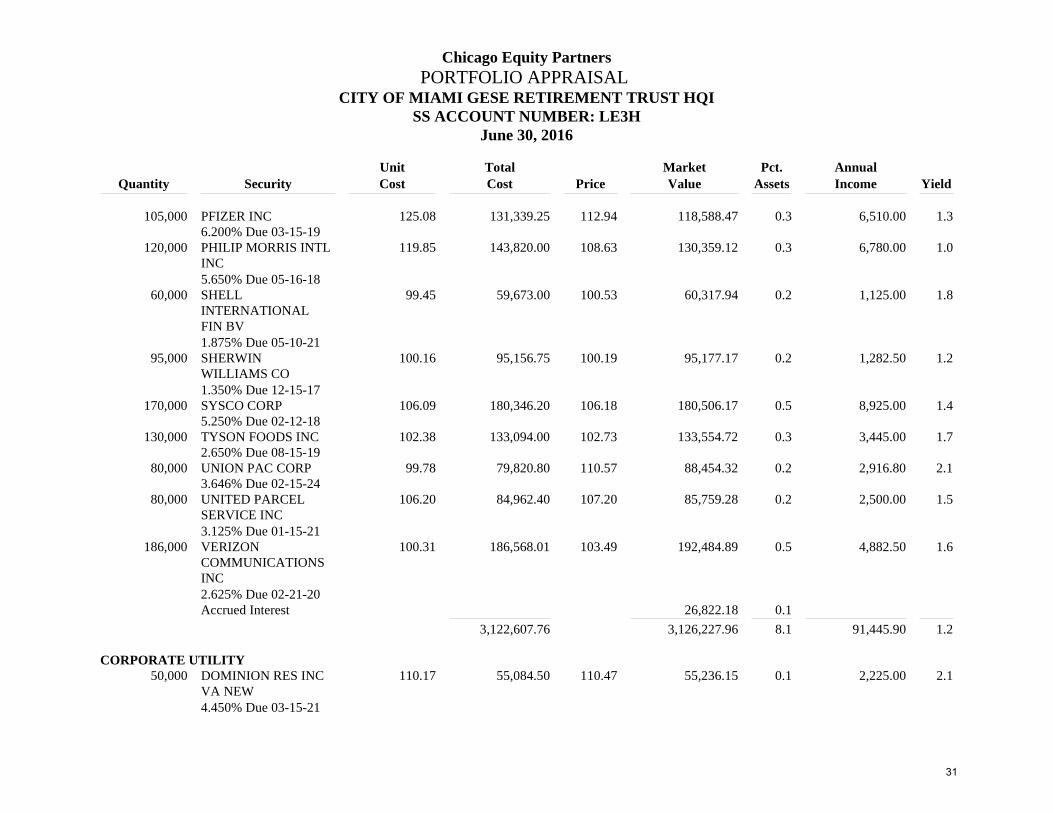

Chicago Equity PartnersPORTFOLIO APPRAISAL

CITY OF MIAMI GESE RETIREMENT TRUST HQISS ACCOUNT NUMBER: LE3H

June 30, 2016

Unit Total Market Pct. AnnualQuantity Security Cost Cost Price Value Assets Income Yield

CORPORATE FINANCIAL120,000 BANK NEW YORK

MTN BK ENT100.02 120,026.40 102.89 123,463.68 0.3 2,940.00 1.8

2.450% Due 11-27-20205,000 CHUBB CORP 122.64 251,409.95 108.48 222,387.69 0.6 11,787.50 1.2

5.750% Due 05-15-18105,000 GENERAL ELEC CAP

CORP MTN BE104.74 109,972.80 101.10 106,155.73 0.3 3,045.00 0.8

2.900% Due 01-09-1745,000 TORONTO

DOMINION BANK101.65 45,740.70 102.62 46,178.14 0.1 1,012.50 1.4

2.250% Due 11-05-19125,000 VISA INC 99.91 124,893.75 103.11 128,885.12 0.3 2,750.00 1.5

2.200% Due 12-14-20300,000 WELLS FARGO & CO

NEW99.98 299,931.00 102.54 307,630.80 0.8 7,500.00 1.9

2.500% Due 03-04-21170,000 WELLS FARGO CO

MTN BE102.00 173,405.10 100.84 171,425.28 0.4 4,462.50 0.8

2.625% Due 12-15-16Accrued Interest 6,161.87 0.0

1,125,379.70 1,112,288.33 2.9 33,497.50 1.4

CORPORATE INDUSTRIAL60,000 3M CO 98.06 58,834.20 102.44 61,464.42 0.2 1,200.00 1.6

2.000% Due 06-26-2285,000 ALTRIA GROUP INC 102.91 87,471.80 103.95 88,361.41 0.2 2,231.25 1.5

2.625% Due 01-14-20110,000 BOEING CO 98.79 108,669.05 103.61 113,970.67 0.3 2,585.00 1.6

2.350% Due 10-30-21

29

Chicago Equity PartnersPORTFOLIO APPRAISAL

CITY OF MIAMI GESE RETIREMENT TRUST HQISS ACCOUNT NUMBER: LE3H

June 30, 2016

Unit Total Market Pct. AnnualQuantity Security Cost Cost Price Value Assets Income Yield

120,000 CATERPILLAR FINL SVCS MTNS BE

100.58 120,699.60 100.05 120,060.96 0.3 1,200.00 0.9

1.000% Due 11-25-16100,000 DISNEY WALT CO

MTNS BE101.71 101,708.00 100.10 100,103.70 0.3 1,350.00 0.5

1.350% Due 08-16-16145,000 EXXON MOBIL CORP 101.16 146,684.90 101.62 147,355.81 0.4 2,476.60 1.1

1.708% Due 03-01-19140,000 GENERAL ELECTRIC

CO106.32 148,845.20 105.94 148,321.74 0.4 7,350.00 1.1

5.250% Due 12-06-17110,000 GENERAL MLS INC 119.94 131,934.00 111.15 122,265.11 0.3 6,215.00 1.3

5.650% Due 02-15-19100,000 HOME DEPOT INC 102.80 102,798.00 102.97 102,974.50 0.3 2,250.00 0.9

2.250% Due 09-10-18170,000 JOHNSON &

JOHNSON100.33 170,557.60 99.93 169,882.87 0.4 1,190.00 0.9

0.700% Due 11-28-16125,000 KIMBERLY CLARK

CORP115.50 144,375.00 105.62 132,030.50 0.3 7,656.25 0.9

6.125% Due 08-01-17170,000 LOCKHEED MARTIN

CORP101.05 171,790.10 101.36 172,306.22 0.4 3,145.00 1.3

1.850% Due 11-23-18205,000 MCDONALDS CORP

MED TERM NT BE107.05 219,460.70 106.94 219,224.54 0.6 10,967.50 1.1

5.350% Due 03-01-1890,000 MEDTRONIC INC 99.88 89,894.70 99.97 89,976.06 0.2 787.50 0.9

0.875% Due 02-27-17225,000 MERCK & CO INC

NEW99.60 224,104.50 100.40 225,905.17 0.6 2,475.00 0.8

1.100% Due 01-31-18

30

Chicago Equity PartnersPORTFOLIO APPRAISAL

CITY OF MIAMI GESE RETIREMENT TRUST HQISS ACCOUNT NUMBER: LE3H

June 30, 2016

Unit Total Market Pct. AnnualQuantity Security Cost Cost Price Value Assets Income Yield

105,000 PFIZER INC 125.08 131,339.25 112.94 118,588.47 0.3 6,510.00 1.36.200% Due 03-15-19

120,000 PHILIP MORRIS INTL INC

119.85 143,820.00 108.63 130,359.12 0.3 6,780.00 1.0

5.650% Due 05-16-1860,000 SHELL

INTERNATIONAL FIN BV

99.45 59,673.00 100.53 60,317.94 0.2 1,125.00 1.8

1.875% Due 05-10-2195,000 SHERWIN

WILLIAMS CO100.16 95,156.75 100.19 95,177.17 0.2 1,282.50 1.2

1.350% Due 12-15-17170,000 SYSCO CORP 106.09 180,346.20 106.18 180,506.17 0.5 8,925.00 1.4

5.250% Due 02-12-18130,000 TYSON FOODS INC 102.38 133,094.00 102.73 133,554.72 0.3 3,445.00 1.7

2.650% Due 08-15-1980,000 UNION PAC CORP 99.78 79,820.80 110.57 88,454.32 0.2 2,916.80 2.1

3.646% Due 02-15-2480,000 UNITED PARCEL

SERVICE INC106.20 84,962.40 107.20 85,759.28 0.2 2,500.00 1.5

3.125% Due 01-15-21186,000 VERIZON

COMMUNICATIONS INC

100.31 186,568.01 103.49 192,484.89 0.5 4,882.50 1.6

2.625% Due 02-21-20Accrued Interest 26,822.18 0.1

3,122,607.76 3,126,227.96 8.1 91,445.90 1.2

CORPORATE UTILITY50,000 DOMINION RES INC

VA NEW110.17 55,084.50 110.47 55,236.15 0.1 2,225.00 2.1

4.450% Due 03-15-21

31

Chicago Equity PartnersPORTFOLIO APPRAISAL

CITY OF MIAMI GESE RETIREMENT TRUST HQISS ACCOUNT NUMBER: LE3H

June 30, 2016

Unit Total Market Pct. AnnualQuantity Security Cost Cost Price Value Assets Income Yield

95,000 MIDAMERICAN ENERGY CO

106.16 100,856.75 109.47 103,992.51 0.3 3,325.00 2.2

3.500% Due 10-15-24112,000 PROGRESS ENERGY

CAROLINA99.97 111,961.74 106.74 119,549.02 0.3 3,360.00 1.6

3.000% Due 09-15-21Accrued Interest 2,346.42 0.0

267,902.99 281,124.10 0.7 8,910.00 2.0

AGENCY55,000 FEDERAL HOME LN

MTG CORP103.78 57,081.47 105.92 58,253.41 0.2 1,306.25 1.3

2.375% Due 01-13-2275,000 FEDERAL HOME LN

MTG CORP98.13 73,597.50 101.51 76,130.70 0.2 1,031.25 1.0

1.375% Due 05-01-20565,000 FEDERAL NATL

MTG ASSN100.20 566,135.65 100.34 566,944.73 1.5 4,943.75 0.7

0.875% Due 03-28-18375,000 FEDERAL NATL

MTG ASSN99.69 373,856.25 100.35 376,324.87 1.0 3,281.25 0.6

0.875% Due 12-20-17570,000 FEDERAL NATL

MTG ASSN96.75 551,491.38 100.40 572,256.06 1.5 4,987.50 0.7

0.875% Due 05-21-1895,000 FEDERAL NATL

MTG ASSN100.82 95,777.35 102.77 97,628.55 0.3 1,781.25 0.8

1.875% Due 02-19-19Accrued Interest 3,366.15 0.0

1,717,939.60 1,750,904.48 4.5 17,331.25 0.7

32

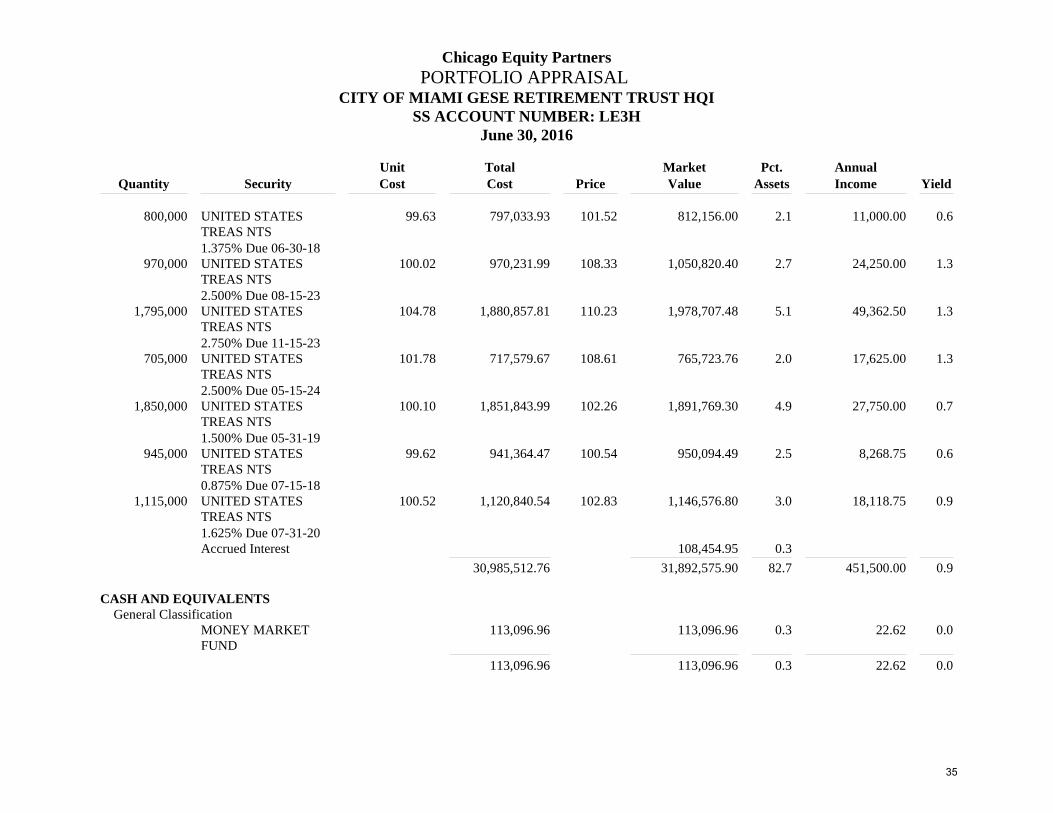

Chicago Equity PartnersPORTFOLIO APPRAISAL

CITY OF MIAMI GESE RETIREMENT TRUST HQISS ACCOUNT NUMBER: LE3H

June 30, 2016

Unit Total Market Pct. AnnualQuantity Security Cost Cost Price Value Assets Income Yield

TREASURY925,000 UNITED STATES

TREAS NTS100.60 930,531.42 102.14 944,800.55 2.4 13,875.00 0.7

1.500% Due 02-28-191,480,000 UNITED STATES

TREAS NTS101.73 1,505,559.60 102.55 1,517,809.56 3.9 24,050.00 0.7

1.625% Due 04-30-191,860,000 UNITED STATES

TREAS NTS101.75 1,892,614.68 104.13 1,936,870.08 5.0 34,875.00 1.1

1.875% Due 11-30-211,250,000 UNITED STATES

TREAS NTS99.76 1,246,996.41 104.62 1,307,812.50 3.4 25,000.00 1.4

2.000% Due 02-15-251,130,000 UNITED STATES

TREAS NTS99.39 1,123,127.85 101.83 1,150,701.60 3.0 15,537.50 0.9

1.375% Due 08-31-20250,000 UNITED STATES

TREAS NTS100.70 251,758.81 103.17 257,920.00 0.7 4,375.00 1.2

1.750% Due 09-30-22600,000 UNITED STATES

TREAS NTS99.20 595,173.89 100.54 603,211.20 1.6 5,250.00 0.6

0.875% Due 10-15-182,060,000 UNITED STATES

TREAS NTS99.92 2,058,317.05 101.77 2,096,451.70 5.4 28,325.00 1.0

1.375% Due 01-31-211,920,000 UNITED STATES

TREAS NTS97.67 1,875,232.68 101.12 1,941,600.00 5.0 31,200.00 1.5

1.625% Due 02-15-262,040,000 UNITED STATES

TREAS NTS98.79 2,015,383.39 100.70 2,054,343.24 5.3 22,950.00 1.0

1.125% Due 02-28-21

33

Chicago Equity PartnersPORTFOLIO APPRAISAL

CITY OF MIAMI GESE RETIREMENT TRUST HQISS ACCOUNT NUMBER: LE3H

June 30, 2016

Unit Total Market Pct. AnnualQuantity Security Cost Cost Price Value Assets Income Yield

280,000 UNITED STATES TREAS NTS

98.34 275,363.62 103.33 289,329.60 0.8 4,900.00 1.2

1.750% Due 05-15-22270,000 UNITED STATES

TREAS NTS99.57 268,851.29 99.97 269,915.76 0.7 1,350.00 0.5

0.500% Due 07-31-171,330,000 UNITED STATES

TREAS NTS99.84 1,327,822.42 100.41 1,335,455.66 3.5 11,637.50 0.7

0.875% Due 07-31-191,125,000 UNITED STATES

TREAS NTS99.79 1,122,624.91 100.09 1,126,010.25 2.9 7,031.25 0.5

0.625% Due 08-31-171,365,000 UNITED STATES

TREAS NTS100.17 1,367,266.88 100.75 1,375,184.26 3.6 13,650.00 0.8

1.000% Due 09-30-19245,000 UNITED STATES

TREAS NTS99.90 244,752.15 102.36 250,780.53 0.7 3,981.25 1.2

1.625% Due 11-15-222,085,000 UNITED STATES

TREAS NTS100.01 2,085,169.88 100.65 2,098,600.45 5.4 20,850.00 0.8

1.000% Due 11-30-191,130,000 UNITED STATES

TREAS NTS98.24 1,110,159.88 100.26 1,132,957.21 2.9 8,475.00 0.6

0.750% Due 12-31-17800,000 UNITED STATES

TREAS NTS97.61 780,875.00 100.27 802,187.20 2.1 6,000.00 0.6

0.750% Due 03-31-18675,000 UNITED STATES

TREAS NTS93.06 628,178.56 103.16 696,331.35 1.8 11,812.50 1.3

1.750% Due 05-15-23

34

Chicago Equity PartnersPORTFOLIO APPRAISAL

CITY OF MIAMI GESE RETIREMENT TRUST HQISS ACCOUNT NUMBER: LE3H

June 30, 2016

Unit Total Market Pct. AnnualQuantity Security Cost Cost Price Value Assets Income Yield

800,000 UNITED STATES TREAS NTS

99.63 797,033.93 101.52 812,156.00 2.1 11,000.00 0.6

1.375% Due 06-30-18970,000 UNITED STATES

TREAS NTS100.02 970,231.99 108.33 1,050,820.40 2.7 24,250.00 1.3

2.500% Due 08-15-231,795,000 UNITED STATES

TREAS NTS104.78 1,880,857.81 110.23 1,978,707.48 5.1 49,362.50 1.3

2.750% Due 11-15-23705,000 UNITED STATES

TREAS NTS101.78 717,579.67 108.61 765,723.76 2.0 17,625.00 1.3

2.500% Due 05-15-241,850,000 UNITED STATES

TREAS NTS100.10 1,851,843.99 102.26 1,891,769.30 4.9 27,750.00 0.7

1.500% Due 05-31-19945,000 UNITED STATES

TREAS NTS99.62 941,364.47 100.54 950,094.49 2.5 8,268.75 0.6

0.875% Due 07-15-181,115,000 UNITED STATES

TREAS NTS100.52 1,120,840.54 102.83 1,146,576.80 3.0 18,118.75 0.9

1.625% Due 07-31-20Accrued Interest 108,454.95 0.3

30,985,512.76 31,892,575.90 82.7 451,500.00 0.9

CASH AND EQUIVALENTSGeneral Classification

MONEY MARKET FUND

113,096.96 113,096.96 0.3 22.62 0.0

113,096.96 113,096.96 0.3 22.62 0.0

35

Chicago Equity PartnersPORTFOLIO APPRAISAL

CITY OF MIAMI GESE RETIREMENT TRUST HQISS ACCOUNT NUMBER: LE3H

June 30, 2016

Unit Total Market Pct. AnnualQuantity Security Cost Cost Price Value Assets Income Yield

MISCELLANEOUSNot Classified

INCOME CASH FOR WITHDRAWAL

294,792.23 294,792.23 0.8 58.96 0.0

294,792.23 294,792.23 0.8 58.96 0.0

TOTAL PORTFOLIO 37,627,232.00 38,571,009.96 100.0 602,766.23 1.0

36

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX

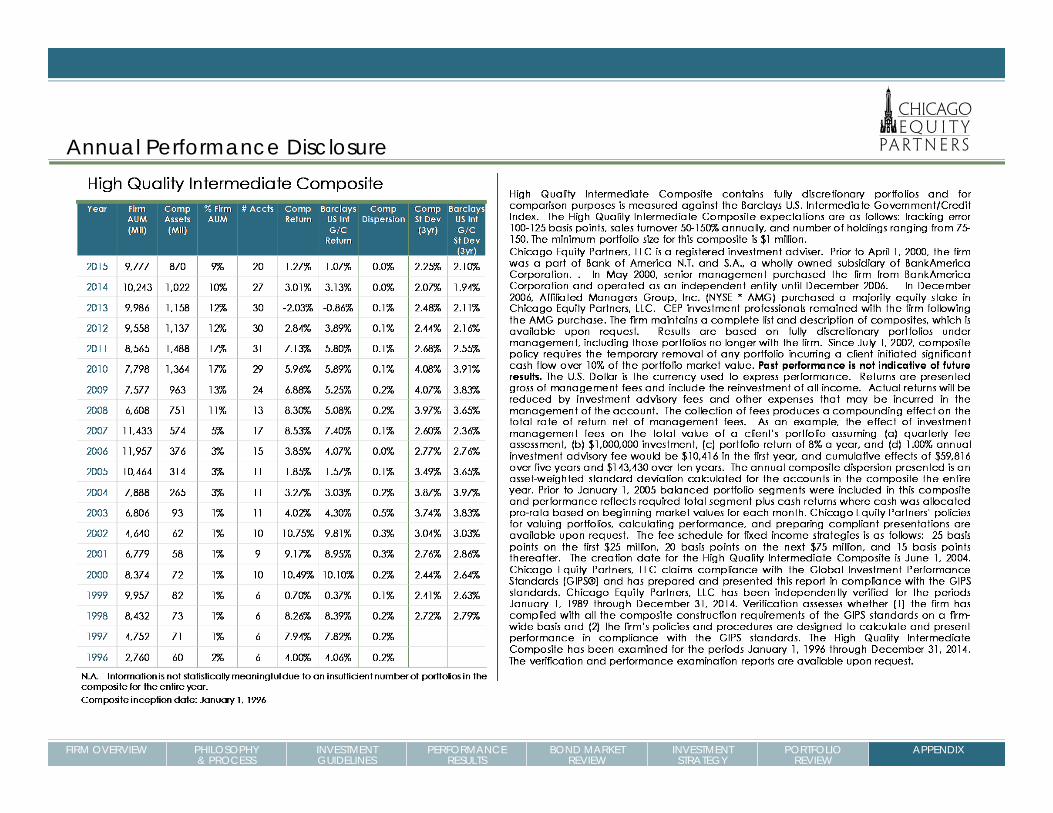

Annual Performance Disclosure

FIRM OVERVIEW PHILOSOPHY& PROCESS

INVESTMENT GUIDELINES

PERFORMANCE RESULTS

BOND MARKET REVIEW

INVESTMENT STRATEGY

PORTFOLIO REVIEW

APPENDIX

Contact Information

Today’s Presenters

Chicago Equity Partners180 N. LaSalle Street, Suite 3800

Chicago, Illinois

Mike Budd

Managing Director

p: 312.629.8506

James A. DeZellar, CFA

Managing Director

p: 312.629.5725