49

City of St. Marys, Kansas December 31, 2015 Audit Communication Letter to Governing Body

3

APPENDIX A: MATTERS FOR YOUR CONSIDERATION The following recommendations are submitted to assist in improving accounting, administrative and operational controls and procedures. Cost effectiveness may not warrant the implementation of the items listed. The City should consider the suggestions and prioritize as needed. Financial Statement Preparation (required per audit standards) As we state in our management representation letter signed by the Commission, we assisted management in the preparation of the audited financial statement and related note disclosures for external reporting. Current auditing standards require us to discuss with the Commission and management our involvement in assisting with preparation; while we assisted in the preparation our firm cannot be considered as part of the City’s internal control structure and we cannot perform management functions or make management decisions with regards to the preparation. While the City personnel does not have adequate resources available to them to prepare the financial statements and related footnote disclosures in accordance with the basis of accounting adopted by the City for external purposes, they do have the skill and knowledge to process the basic financial transactions and prepare interim financial statements needed to provide appropriate budget and operating information to the governing body. The City does not have any documented policies and procedures with regards to preparation of external financial statements and related note disclosures and therefore we consider this to be a deficiency under the standards established by the American Institute of Certified Public Accountants. We understand that management and governing body may not find it cost effective to hire personnel on a full-time basis with the expertise or to purchase the additional resources it would require for staff to prepare the financial statements and related notes for external use, and therefore have chosen to rely on the assistance of the auditors and have accepted responsibility for the work performed by the auditors. Recommendations: While it may be cost prohibitive to have full-time staff with the skill, knowledge and expertise and resources to prepare the external financial statements and related notes, there are procedures and policies the City could implement, at relatively low cost, to ensure that the deficiency does not become a material weakness and that staff and management continue to possess adequate skill, knowledge and expertise to accept responsibility for the work performed by the auditors.

We recommend that the governing body and management continue to monitor the policies and procedures over the preparation of external financial statements and note disclosures and consider the following as additional controls to strengthen their controls over financial reporting:

• Stay up to date with KMAAG requirements by obtaining the up to date Kansas Municipal Audit and Accounting Guide (KMAAG), issued by the Kansas Society of Certified Public Accounts and the KMAAG Board.

• Continue to participate in periodic training sessions on governmental and KMAAG financial statement preparation and reporting with guidance pertaining to KMAAG requirements.

• Adopt a policy that annual KMAAG financial statements will be included in the City’s current interim financial statement review prior to being subject to the audit to ensure that all KMAAG related adjustments have been properly made.

City of St. Marys, Kansas December 31, 2015 Audit Communication Letter to Governing Body

4

Golf Course- Record Keeping

In the prior year’s audit, we noted that record keeping for the golf course was incomplete. This year we have noted this issue again. It is our understanding the Golf Course Manager and Advisory Board resigned their positions in 2015 and early 2016, respectively. We were able to obtain records pertaining to the memberships but no other supporting documents were provided with regards to other fees or inventory control. We recognize this particular fund may not be significant to the City’s overall financial statement but having and maintaining records are a vital part of the City’s internal controls for all departments. Recommendation: We recommend that if the City leases this operation to an outside entity to manage or if the City assigns an individual to manage, the necessary procedures, tools and budget must be established to control and maintain proper records and inventory. We also recommend that other supporting documentation (noted in the public property fees resolution) be implemented to account for the various fees charged by the golf course. This will increase controls and assist to ensure that all fees are assessed, collected and turned in to and recorded in the City’s financial records.

AUDITED FINANCIAL STATEMENT AND SUPPLEMENTARY INFORMATION

CITY OF ST. MARYS, KANSAS

December 31, 2015

Reese & Novelly, PA Certified Public Accountants

St. Marys, Kansas

Audited Financial Statement and Supplementary Information City of St. Marys, Kansas Year Ended December 31, 2015 Independent Auditor’s Report ..........................................................................................................1 Regulatory Basis Financial Statement

Summary Statement of Receipts, Expenditures and Unencumbered Cash......................................3 Notes to Financial Statement ...........................................................................................................6 Regulatory – Required Supplementary Information (Regulatory Basis) Schedule 1: Summary of Expenditures - Budget and Actual ........................................................17 Schedule 2: Schedules of Receipts and Expenditures - Budget and Actual: General Fund ...............................................................................................................................18 Bond and Interest Fund ................................................................................................................19 Special Purpose Funds: Special Highway Fund ............................................................................................................20 Special Park and Recreation Fund ...........................................................................................21 Fire Equipment Fund ...............................................................................................................22 County Sales Tax Fund ............................................................................................................23 Summary of Non-budgeted Special Purpose Funds ................................................................24 Summary Schedule of Capital Project Funds (Non-budgeted) ....................................................25 Business Funds: Electric Utility Fund ................................................................................................................26 Water Utility Fund ...................................................................................................................27 Sewer Service Fund .................................................................................................................28 Sewer Debt Service Reserve Fund ...........................................................................................29 Golf Course Fund .....................................................................................................................30 Refuse Utility Fund ..................................................................................................................31 Summary of Non-budgeted Business Funds ............................................................................32 Schedule 3: Summary of Receipts and Disbursements – Agency Funds .....................................33 Other Information Schedule 4: Key Ratios of Financial Condition .............................................................................34

FINANCIAL STATEMENT AND NOTE DISCLOSURES

SUMMARY STATEMENT OF RECEIPTS, EXPENDITURES AND UNENCUMBERED CASHREGULATORY BASIS

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Funds

Beginning Unencumbered Cash Balance

Prior Year Cancelled

Encumbrances Receipts Expenditures

Ending Unencumbered Cash Balance

Add Encumbrances and Accounts

Payable Ending Cash

Balance General Funds:

General 421,681$ $ 1,057,579$ 1,040,800$ 438,460$ 16,052$ 454,512$

Bond and Interest Funds: Bond and Interest 52,138 50,254 45,990 56,402 56,402

Special Purpose Funds:

Special Highway 39,470 101,149 91,410 49,209 524 49,733 Special Parks and Recreation 14,971 40,742 44,487 11,226 910 12,136 Fire Equipment 201,326 84,864 61,051 225,139 225,139 County Sales Tax 559,205 384,990 357,282 586,913 586,913 Crime Prevention 2,482 2,610 2,301 2,791 2,791 Capital Improvements 15,086 135 12,438 2,783 2,783 Equipment Reserve 136,322 33,084 10,191 159,215 159,215

TOTAL SPECIAL PURPOSE 968,862 647,574 579,160 1,037,276 1,434 1,038,710

Capital Projects:

Electric Substation Project 4,864 4,864 4,864

The notes to the financial statement are an integral part of this statement.3

SUMMARY STATEMENT OF RECEIPTS, EXPENDITURES AND UNENCUMBERED CASHREGULATORY BASIS

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Funds

Beginning Unencumbered Cash Balance

Prior Year Cancelled

Encumbrances Receipts Expenditures

Ending Unencumbered Cash Balance

Add Encumbrances and Accounts

Payable Ending Cash

Balance Business Funds:

Electric Utility 796,362 2,140,211 2,089,948 846,625 13,738 860,363 Water Utility 232,368 286,443 346,263 172,548 3,711 176,259 Sewer Service 276,545 526,806 542,304 261,047 1,912 262,959 Sewer Debt Service Reserve 193,275 233,518 233,417 193,376 193,376 Golf Course 4,975 156,629 156,691 4,913 1,213 6,126 Refuse Utility 55,530 240,897 238,696 57,731 6,624 64,355 Sewer Reserve 45,776 40,000 70,066 15,710 15,710

TOTAL BUSINESS FUNDS 1,604,831 3,624,504 3,677,385 1,551,950 27,198 1,579,148

TOTAL REPORTING ENTITY 3,052,376$ -$ 5,379,911$ 5,343,335$ 3,088,952$ 44,684$ 3,133,636$

The notes to the financial statement are an integral part of this statement.4

SUMMARY STATEMENT OF RECEIPTS, EXPENDITURES AND UNENCUMBERED CASHREGULATORY BASIS

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Composition of Cash:Checking accounts 1,081,193$ Money market accounts 1,157,158 Certificates of deposit 943,345 Municipal court 15

TOTAL CASH 3,181,711

Less Agency Funds (per Schedule 3) (48,075)

TOTAL REPORTING ENTITY (EXCLUDING AGENCY FUNDS) 3,133,636$

The notes to the financial statement are an integral part of this statement.5

NOTES TO FINANCIAL STATEMENT CITY OF ST. MARYS, KANSAS FINANCIAL REPORTING ENTIT Y December 31, 2015

6

NOTE A—SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The City of St. Marys, Kansas (Municipality) was chartered October 9, 1869, and operates under a Commission-Manager form of government. The accounting policies of the Municipality conform to the cash-basis and budget laws of Kansas (regulatory basis). The following is a summary of the more significant policies: 1. The Financial Reporting Entity: The financial reporting entity of the City of St. Marys,

Kansas is comprised of the primary government (the Municipality).

The basic criterion for including a separate entity in the Municipality's financial reporting entity is the financial accountability of the Municipality for the separate entity. The Municipality is financially accountable if it appoints a voting majority of a related municipal entity’s governing body and if it either has the ability to impose its will on the related municipal entity or there is a potential for the related municipal entity to provide certain financial benefits to, or impose certain financial burdens on, the primary government. There were no related municipal entities.

2. Regulatory Basis Fund Types: The accounts of the Municipality are organized on the basis

of funds, each of which is considered a separate accounting entity. The operations of each fund are accounted for with a separate set of self-balancing accounts that comprise its cash, liabilities, fund balance, receipts, and expenditures. Government resources are allocated to and accounted for in individual funds based upon the purposes for which they are to be spent and the means by which spending activities are controlled. The various funds are grouped, in the financial statement in this report, into generic regulatory basis fund types and broad fund categories as follows:

Governmental Funds The General Fund is the chief operating fund of the Municipality. It is used to account for all financial resources except those that are required to be accounted for in another fund. Special Purpose Funds are used to account for the proceeds of specific tax levies and other specific revenue sources (other than capital project and tax levies for long-term debt) that are intended for specified purposes. Bond and Interest Funds are used to account for the accumulation of resources, including tax levies, transfer from other funds and payment of long-term debt principal, interest, and related costs. Capital Projects Funds are used to account for the debt proceeds and other financial resources to be used for the acquisition or construction of major capital facilities or equipment.

NOTES TO FINANCIAL STATEMENT CITY OF ST. MARYS, KANSAS FINANCIAL REPORTING ENTIT Y December 31, 2015

7

Business Funds

Business Funds are used to account for operations that provide goods or services to the general public on a continuing basis. Such operations are financed and operated in a manner similar to private business entities and (a) are intended to be self supporting through charges to users or (b) the governing body has deemed it appropriate to account for them as business funds for capital maintenance, public policy, management control, accountability, or other purposes. Trust and Agency Funds

Trust Funds are used to report assets held in trust for the benefit of the municipal financial reporting entity (i.e. pension funds, investment trust funds, private purpose trust funds which benefit the municipal reporting entity, scholarship funds, etc.). Agency Funds are used to account for assets held by the municipal reporting entity in a purely custodial capacity (payroll clearing fund, tax collection accounts, etc.).

3. Regulatory Basis of Accounting and Departure from Accounting Principles Generally Accepted in the United States of America: The municipal reporting entity prepares the financial statements using Kansas Municipal Audit and Accounting Guide (KMAAG) regulatory basis of accounting, which is designed to demonstrate compliance with the cash basis and budget laws of the State of Kansas. The KMAAG regulatory basis of accounting involves the recognition of cash, cash equivalents, marketable investments, and certain accounts payable and encumbrance obligations to arrive at a net unencumbered cash and investments balance on a regulatory basis for each fund, and the reporting of changes in unencumbered cash and investments of a fund resulting from the difference in regulatory basis revenues and regulatory basis expenditures for the fiscal year. Receipts are recognized when the cash balance of a fund is increased. For an interfund transaction, a receipt is recorded in the fund receiving cash from another fund, and the expenditure would be charged in the fund from which the transfer is made. All recognized assets and liabilities are measured and reported at cost, unless they have been permanently impaired and have no future cash value or represent no future obligation against cash. The KMAAG regulatory basis does not recognize capital assets, long-term debt, accrued receivables and payables, or any other assets, liabilities or deferred inflow or outflows, other than those mentioned above. The Municipality has approved a resolution that is in compliance with K.S.A. 75-1120a(c), waiving the requirement for application of generally accepted accounting principles and allowing the municipality to use the KMAAG regulatory basis of accounting.

NOTES TO FINANCIAL STATEMENT CITY OF ST. MARYS, KANSAS FINANCIAL REPORTING ENTIT Y December 31, 2015

8

4. Budgetary Information: Kansas statutes require that an annual operating budget be legally adopted for the general fund, special purpose funds (unless specifically exempted by statute), bond and interest funds, and business funds. Although directory rather than mandatory, the statutes provide for the following sequence and timetable in the adoption of the legal annual operating budget:

a. Preparation of the budget for the succeeding calendar year on or before August 1. b. Publication in local newspaper of the proposed budget and notice of public hearing on the

budget on or before August 5. c. Public hearing on or before August 15, but at least ten days after publication of notice of

hearing. d. Adoption of the final budget on or before August 25.

The statutes allow for the governing body to increase the originally adopted budget for previously unbudgeted increases in revenue other than ad valorem property taxes. To do this, a notice of public hearing to amend the budget must be published in the local newspaper. At least ten days after publication the hearing may be held and the governing body may amend the budget at that time. The statutes permit transferring budgeted amounts between line items within an individual fund. However, such statutes prohibit expenditures in excess of the total amount of the adopted budget of expenditures of individual funds. Budget comparison schedules are presented for each fund showing actual receipts and expenditures compared to legally budgeted receipts and expenditures. All legal annual operating budgets are prepared using the regulatory basis of accounting in which revenues are recognized when cash is received and expenditures include disbursements, accounts payable and encumbrances, with disbursements being adjusted for prior year’s accounts payable and encumbrances. Encumbrances are commitments by the municipality for future payments and are supported by a document evidencing the commitment, such as a purchase order or contract. Any unused budgeted expenditure authority lapses at year-end. A legal operating budget is not required for capital project funds, trust funds and the following special purpose and business funds:

Special Purpose Funds: Capital Improvement; Equipment Reserve Business Funds: Sewer Reserve

NOTES TO FINANCIAL STATEMENT CITY OF ST. MARYS, KANSAS FINANCIAL REPORTING ENTIT Y December 31, 2015

9

Spending in funds, which are not subject to the legal annual operating budget requirement, is controlled by federal regulations, other statutes, or by the use of internal spending limits established by the governing body.

5. Special Assessments: Projects financed in part by special assessments are financed through

general obligation bonds of the Municipality and are retired from the bond and interest fund. Special assessments paid prior to the issuance of bonds are recorded as revenue in the appropriate project. Special assessments received after the issuance of bonds are recorded as revenue in the bond and interest fund.

6. Cash and Investments: The Municipality uses an internally pooled cash system in which the

cash balances from all funds are combined and invested to the extent available in certificates of deposit and other authorized investments. Earnings from these investments, unless specifically designated, are allocated to the general fund and the utility funds based upon their average cash balances. Investments are stated at cost, which approximates market.

7. Reimbursements: The Municipality records reimbursable expenditures in the fund that

makes the disbursement and records reimbursements as revenue to the fund. For purposes of budgetary comparisons, the reimbursement is recorded as a qualifying budget credit in the fund receiving the reimbursement.

8. Property Tax: The Pottawatomie County Clerk calculates the final tax levy rates necessary to

finance the budget subject to any legal limitations. After all budgets have been received and tax rates calculated, the clerk certifies the tax roll to, and prepares tax statements for, the County Treasurer who receives payment.

Taxes levied to finance the budget are made available to the Municipality after January 1 and are distributed by the County Treasurer per statutes. At least 50% of the taxes levied are available in January. Delinquent tax collections are distributed throughout the year.

9. Other Related Municipal Entitles (excluded from municipal financial reporting entity): The Municipality Commission is also responsible for appointing the members of the board of the St. Marys Housing Authority, but the Municipality's accountability for this organization does not extend beyond making the appointments and the Municipality Commission makes no appropriations to the Authority.

NOTE B –STEWARDSHIP, COMPLIANCE AND ACCOUNTABILITY 1. Amendments to Legal Budgets: The legal budgets for the Water Fund, Special Parks and

Recreation Fund, and Golf Course Fund were amended during 2015.

NOTES TO FINANCIAL STATEMENT CITY OF ST. MARYS, KANSAS FINANCIAL REPORTING ENTIT Y December 31, 2015

10

NOTE C – DEPOSITS AND INVESTMENTS As of December 31, 2015, the Municipality’s investments consisted of short-term certificates of deposit. K.S.A. 9-1401 establishes the depositories which may be used by the Municipality. The statute requires banks eligible to hold the Municipality’s funds have a main or branch bank in the county in which the Municipality is located, or in an adjoining county if such institution has been designated as an official depository, and the banks provide an acceptable rate of return on funds. In addition, K.S.A. 9-1402 requires the banks to pledge securities for deposits in excess of FDIC coverage. The Municipality has no other policies that would further limit interest rate risk. K.S.A. 12-1675 limits the Municipality’s investment of idle funds to time deposits, open accounts, and certificates of deposit with allowable financial institutions; U.S. government securities; temporary notes; no-fund warrants; repurchase agreements; and the Kansas Municipal Investment Pool. The Municipality has no investment policy that would further limit its investment choices. The Municipality had no investments, other than certificates of deposit which are included in the bank deposits; therefore they do not have a rating.

Concentration of credit risk: State statutes place no limit on the amount the Municipality may invest in any one issuer as long as the investments are adequately secured under K.S.A. 9-1402 and 9-1405. Custodial credit risk – deposits: Custodial credit risk is the risk that in the event of a bank failure, the Municipality’s deposits may not be returned to it. State statutes require the Municipality’s deposits in financial institutions to be entirely covered by federally depository insurance or by collateral held under a joint custody receipt issued by a bank within the State of Kansas, the Federal Reserve Bank of Kansas, or the Federal Home Loan Bank of Topeka, except during designated “peak periods” when required coverage is 50%. The Municipality had no agreements for designated “peak periods.” All deposits were legally secured at December 31, 2015. At December 31, 2015, the carrying amount of the Municipality’s deposits, including certificates of deposit, was $3,181,711 and the bank balance was $3,186,118. The bank balance was held by two banks which resulted in a concentration of credit risk. Of the bank balance, $1,000,000 was covered by federal depository insurance and $2,186,118 was collateralized with securities held by the pledging financial institutions’ agents in the Municipality’s name.

Custodial credit risk – investments: For an investment, this is the risk that, in the event of the failure of the issuer or counterparty, the Municipality will not be able to recover the value of its investments or collateral securities that are in the possession of an outside party. State statutes require investments to be adequately secured.

NOTES TO FINANCIAL STATEMENT CITY OF ST. MARYS, KANSAS FINANCIAL REPORTING ENTIT Y December 31, 2015

11

NOTE D—LONG TERM DEBT The following is a summary of debt transactions of the Municipality for the year ended December 31, 2015. See Notes L and M for the schedules of long-term liabilities and current maturities of long-term debt.

Payable Beginning of Year Issued Retired

Payable End of Year

General Obligation Bonds 195,000$ 40,000$ 155,000$ Revolving Notes 1,960,494 204,942 1,755,552 Capital Leases 72,022 64,828 7,194

Total 2,227,516$ -$ 309,770$ 1,917,746$

Total interest expense for the year was $73,896.

Conduit Debt From time to time, the Municipality has issued industrial revenue bonds to provide financial assistance to private-sector entities for the acquisition and construction of industrial and commercial facilities deemed to be in the public interest. The bonds are generally payable from and secured by the project financed and if needed, additional assets and/or revenues of the private-sector entity served by the bond issuance. Upon repayment of the bonds, ownership of the acquired facilities transfers to the private-sector entity served by the bond issuance. Neither the Municipality, the State, nor any political subdivision thereof is obligated in any manner for repayment of the bonds. Accordingly, the bonds are not reported as liabilities in the accompanying financial statement. As of December 31, 2015, there was one series of industrial revenue bond outstanding. The aggregate principal amount payable at December 31, 2015 could not be determined; however, the original issue amount totaled $2 million. NOTE E—DEFINED BENEFIT PENSION PLAN General Information about the Pension Plan Plan Description: The City of St. Marys, Kansas participates in the Kansas Public Employees Retirement System (KPERS), a cost-sharing, multiple-employer defined benefit pension plan as provided by K.S.A 74-4901, et. seq. Kansas law establishes and amends benefit provisions. KPERS issues a publically available financial report that includes financial statements and required supplementary information. KPERS’ financial statements are included in its Comprehensive Annual Financial Report which can be found on the KPERS website at www.kpers.org or by writing to KPERS (611 South Kansas, Suite 100; Topeka, KS 66603) or by calling 1-888-275-5737.

NOTES TO FINANCIAL STATEMENT CITY OF ST. MARYS, KANSAS FINANCIAL REPORTING ENTIT Y December 31, 2015

12

Contributions: K.S.A. 74-4919 and K.S.A. 74-49,210 establish the KPERS member-employee contribution rates. KPERS has multiple benefit structures and contribution rates depending on whether the employee is a KPERS 1, KPERS 2, or KPERS 3 member. KPERS 1 members are active and contributing members hired before July 1, 2009. KPERS 2 members were first employed in a covered position on or after July 1, 2009, and KPERS 3 members were first employed in a covered position on or after January 1, 2015. Effective January 1, 2015, Kansas law established the KPERS member-employee contribution rate at six percent of covered salary for KPERS 1, KPERS 2 and KPERS 3. Member contributions are withheld by their employer and paid to KPERS according to the provisions of Section 414(h) of the Internal Revenue Code. State law provides that the employer contribution rates for KPERS 1, KPERS 2, and KPERS 3 be determined based on the results of each annual actuarial valuation. Kansas law sets a limitation on annual increases in the employer contribution rates. The actuarially determined employer contribution rate (not including the 0,85% contribution rate for Death and Disability Program) and the statutory contribution rate was 9.48% for the fiscal year ended December 31, 2015. Contributions to the pension plan from City of St. Marys, Kansas were $107,144 for the year ended December 31, 2015. Net Pension Liability At December 31, 2015, the City of St. Marys, Kansas’s proportionate share of the collective net pension liability reported by KPERS was $784,334. The net pension liability was measured as of June 30, 2015, and the total pension liability used to calculate the net pension liability was determined by an actuarial valuation as of December 31, 2014, which was rolled forward to June 30, 2015. The Municipality’s proportion of the net pension liability was based on the ratio of the Municipality’s contributions to KPERS, relative to the total employer and non-employer contributions of the Local subgroup within KPERS. Since the KMAAG regulatory basis of accounting does not recognize long-term debt, this liability is not reported in this financial statement. The complete actuarial valuation report including all actuarial assumptions and methods, and the report on the allocation of the KPERS collective net pension liability to all participating employers are publicly available on the website at www.kpers.org or can be obtained as described above. NOTE F—DEFERRED COMPENSATION The Municipality participates in the Kansas Public Employees Deferred Compensation Plan, as authorized by K.S.A. 75-5529a and 75-5529b. The City of St. Marys, Kansas is a joint contract owner with the State of Kansas of the group annuity contract issued by ING Life Insurance and Annuity Company in conjunction with the Kansas Public Employees Deferred Compensation Plan. The Municipality annually determines whether matching funds will be paid into employees’ accounts. For the year ended December 31, 2015, the Municipality paid $10,040 in matching contributions.

NOTES TO FINANCIAL STATEMENT CITY OF ST. MARYS, KANSAS FINANCIAL REPORTING ENTIT Y December 31, 2015

13

The Municipality is not responsible for any loss incurred by an employee under the Municipality’s deferred compensation plan. All conditions of the plan shall be controlling. NOTE G—OTHER POST EMPLOYMENT BENEFIT As provided by K.S.A. 12-5040, the municipality allows retirees to participate in the group health insurance plan. While each retiree pays the full amount of the applicable premium, conceptually, the municipality is subsidizing the retirees because each participant is charged a level of premium regardless of age. However, the cost of this subsidy has not been quantified in these financial statements. Under the Consolidated Budget Reconciliation Act (COBRA), the municipality makes health care benefits available to eligible former employees and eligible dependents. Certain requirements are outlined by the federal government for this coverage. The premium is paid in full by the insured. NOTE H—COMPENSATED ABSENCES The Municipality maintains a policy of providing vacation and sick leave to its full-time employees, granted in varying amounts depending on length of service and date of hire. Vacation days are vesting and accumulate but accumulation is subject to various limits. Sick leave is non-vesting and accumulates up to a maximum of 720 hours for employees hired after January 1, 2005. Employees hired prior to January 1, 2005 have unlimited accumulation of sick leave. At December 31, 2015, the Municipality’s liability for unused vacation time is approximately $67,776 attributable to governmental and proprietary funds. NOTE I—COMMITMENTS AND CONTINGENCIES Construction Contracts: At December 31, 2015, the Municipality had several pending construction project contracts. Commitments related to significant contracts include contracts for the Municipality’s street improvements. Risk Management: The Municipality is exposed to various risks of loss related to torts; theft of, damage to, or destruction of assets; errors and omissions; injuries to employees; and natural disasters. The Municipality manages these various risks of loss through commercial insurance with varying deductibles. All deductibles are $1,000 or less. Settled claims have not exceeded this commercial coverage in any of the past three fiscal years.

NOTES TO FINANCIAL STATEMENT CITY OF ST. MARYS, KANSAS FINANCIAL REPORTING ENTIT Y December 31, 2015

14

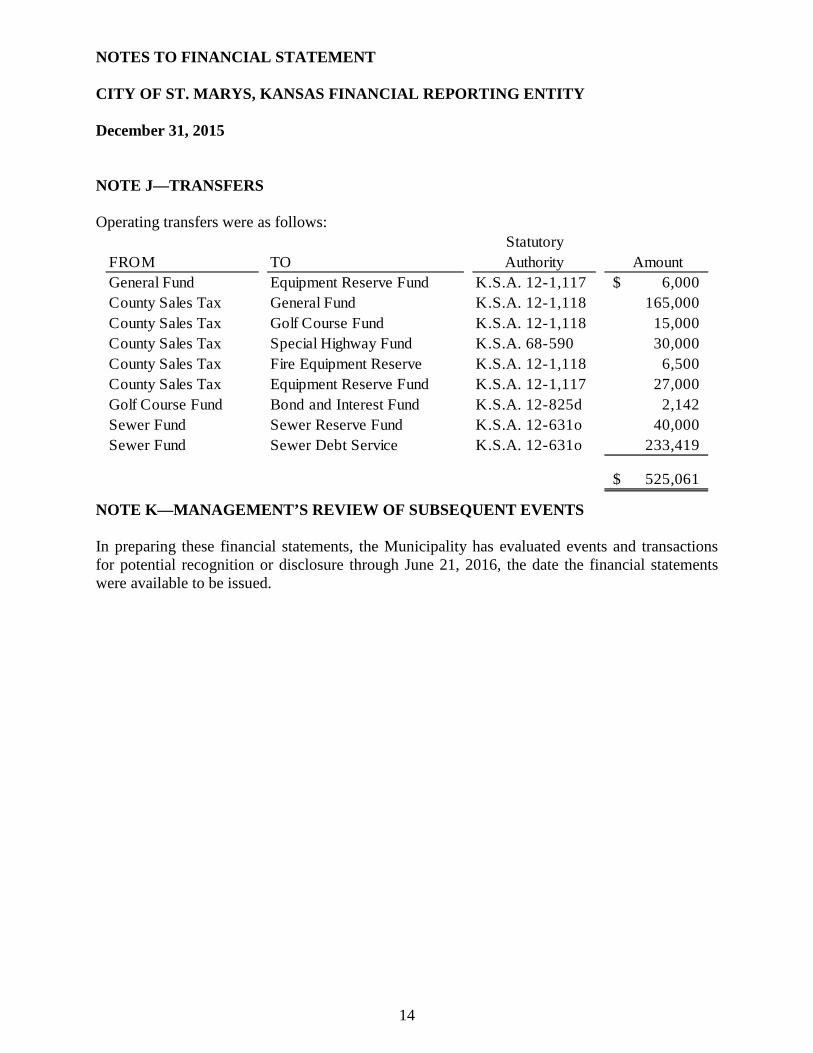

NOTE J—TRANSFERS Operating transfers were as follows:

FROM TOStatutory Authority Amount

General Fund Equipment Reserve Fund K.S.A. 12-1,117 6,000$ County Sales Tax General Fund K.S.A. 12-1,118 165,000 County Sales Tax Golf Course Fund K.S.A. 12-1,118 15,000 County Sales Tax Special Highway Fund K.S.A. 68-590 30,000 County Sales Tax Fire Equipment Reserve K.S.A. 12-1,118 6,500 County Sales Tax Equipment Reserve Fund K.S.A. 12-1,117 27,000 Golf Course Fund Bond and Interest Fund K.S.A. 12-825d 2,142 Sewer Fund Sewer Reserve Fund K.S.A. 12-631o 40,000 Sewer Fund Sewer Debt Service K.S.A. 12-631o 233,419

525,061$

NOTE K—MANAGEMENT’S REVIEW OF SUBSEQUENT EVENTS In preparing these financial statements, the Municipality has evaluated events and transactions for potential recognition or disclosure through June 21, 2016, the date the financial statements were available to be issued.

NOTES TO FINANCIAL STATEMENT

CITY OF ST. MARYS, KANSAS

NOTE L - SCHEDULE OF LONG-TERM DEBT

The following is a schedule of changes in long term debt for the City for the year endedDecember 31, 2015

Interest Rate

Date of Issue

Original Amount

Date of Final

Maturity Beginning

Balance Issued Retired Net Change Ending Balance Interest Paid

General Obligation BondsSeries 2011 Refinance 1.0/3.40% 2/16/2011 375,000 10/1/2019 195,000 40,000 (40,000) 155,000 5,990

TOTAL GENERAL OBLIGATION BONDS 375,000 195,000 - 40,000 (40,000) 155,000 5,990

KDHE Revolving LoanWastewater Treatment Plant 3.49% 8/22/2000 3,385,268 3/1/2022 1,528,630 181,640 (181,640) 1,346,990 51,778 Water Supply 3.51% 2/13/2008 546,673 2/1/2029 431,864 23,302 (23,302) 408,562 14,956

TOTAL REVOLVING LOANS 3,931,941 1,960,494 204,942 (204,942) 1,755,552 66,734

Capital Leases2012 Fire Truck 1.30% 1/15/2013 119,761 1/15/2015 60,267 60,267 (60,267) - 784 John Deere 997 Mower 4.00% 8/1/2014 14,015 8/1/2017 11,755 4,561 (4,561) 7,194 388

TOTAL CAPITAL LEASES 133,776 72,022 64,828 (64,828) 7,194 1,172

TOTAL INDEBTEDNESS 4,440,717$ 2,227,516$ -$ 309,770$ (309,770)$ 1,917,746$ 73,896$

15

NOTES TO FINANCIAL STATEMENT

CITY OF ST. MARYS, KANSAS

NOTE M: SCHEDULE OF MATURITY OF LONG TERM DEBT

The current maturities of long term debt and interest for the next five years and in five year increments through maturity is as follows:

2016 2017 2018 2019 2020 2021-2025 2026-2030 TotalPRINCIPAL

General obligation bonds 40,000$ 40,000$ 40,000$ 35,000$ 155,000$ Revolving loans 212,162 219,635 227,372 235,382 243,675 492,349 124,977 1,755,552 Capital leases 4,747 2,447 7,194

TOTAL PRINCIPAL 256,909 262,082 267,372 270,382 243,675 492,349 124,977 1,917,746

INTERESTGeneral obligation bonds 4,950 3,750 2,490 1,190 12,380 Revolving loans 59,515 52,040 44,303 36,293 28,002 49,068 8,926 278,147 Capital leases 201 29 230

TOTAL INTEREST 64,666 55,819 46,793 37,483 28,002 49,068 8,926 290,757

TOTAL PRINCIPAL AND INTEREST 321,575$ 317,901$ 314,165$ 307,865$ 271,677$ 541,417$ 133,903$ 2,208,503$

16

REGULATORY-REQUIRED SUPPLEMENTARY INFORMATION

SUMMARY OF EXPENDITURES - BUDGET AND ACTUALBUDGETED FUNDS ONLY (SCHEDULE 1)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Certified Budget

(As Amended)

Adjustment for Qualifying

Budget Credits Total Budget

for Comparison

Expenditures Chargeable to Current Year

Favorable (Unfavorable)

Variance General Funds:

General 1,174,414$ $ 1,174,414$ 1,040,800$ 133,614$ Bond and Interest Funds:

Bond and Interest 102,091 102,091 45,990 56,101 Special Purpose Funds:

Special Highway 157,511 157,511 91,410 66,101 Special Park and Recreation 50,000 50,000 44,487 5,513 Fire Equipment 193,608 193,608 61,051 132,557 County Sales Tax 1,007,945 1,007,945 357,282 650,663

Business Funds:Electric Utility 2,287,378 2,287,378 2,089,948 197,430 Water Utility 350,000 350,000 346,263 3,737 Sewer Service 592,108 592,108 542,304 49,804 Sewer Debt Service 233,417 233,417 233,417 - Golf Course 161,000 161,000 156,691 4,309 Refuse Utility 274,235 274,235 238,696 35,539

See independent auditor's report.17

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASISGENERAL FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Taxes and shared revenues 452,376$ 458,345$ 5,969$ Intergovernmental revenue 11,650 12,207 557 Sales tax 250,000 298,858 48,858 Fines, forfeitures, and penalties 17,500 29,823 12,323 Licenses, permits, and fees 30,280 29,616 (664) Charges for services 21,500 22,056 556 Use of money and property 11,880 18,054 6,174 Reimbursements and grants 6,000 16,542 10,542 Miscellaneous 4,125 7,078 2,953 Operating transfers 165,000 165,000 -

TOTAL CASH RECEIPTS 970,311 1,057,579 87,268

Expenditures:Personnel expenditures 779,047 731,946 47,101 General 64,572 75,766 (11,194) Public safety 135,899 105,076 30,823 Municipal court 6,644 4,015 2,629 Street department 157,172 93,590 63,582 Public buildings and grounds 11,500 5,323 6,177 Swimming pool 13,580 19,084 (5,504) Operating transfers 6,000 6,000 -

TOTAL EXPENDITURES 1,174,414 1,040,800 133,614

RECEIPTS OVER (UNDER) EXPENDITURES (204,103) 16,779

Beginning Unencumbered Cash Balance 204,103 421,681

ENDING UNENCUMBERED CASH BALANCE -$ 438,460$

See independent auditor's report.18

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - BOND & INTERESTBOND AND INTEREST FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Taxes and shared revenues 45,995$ 48,112$ 2,117$ Operating transfers 2,142 2,142 -

TOTAL CASH RECEIPTS 48,137 50,254 2,117

Expenditures:Contractual services and other charges 169 169 Materials and supplies 55,932 55,932 Debt payments:

Principal 40,000 40,000 - Interest 5,990 5,990 -

TOTAL EXPENDITURES 102,091 45,990 56,101

RECEIPTS OVER (UNDER) EXPENDITURES (53,954) 4,264

Beginning Unencumbered Cash Balance 53,954 52,138

ENDING UNENCUMBERED CASH BALANCE -$ 56,402$

See independent auditor's report.19

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - SPECIAL HIGHWAYSPECIAL PURPOSE FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Taxes and shared revenues 68,300$ 70,147$ 1,847$ Reimbursements and grants 592 592 Miscellaneous 410 410 Operating transfers 30,000 30,000 -

TOTAL CASH RECEIPTS 98,300 101,149 2,849

Expenditures:Contractual services and other charges 9,000 2,697 6,303 Materials and supplies 148,250 88,713 59,537 Capital outlay 261 261

TOTAL EXPENDITURES 157,511 91,410 66,101

RECEIPTS OVER (UNDER) EXPENDITURES (59,211) 9,739

Beginning Unencumbered Cash Balance 59,211 39,470

ENDING UNENCUMBERED CASH BALANCE -$ 49,209$

See independent auditor's report.20

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - SPECIAL PARKS AND RECREATIONSPECIAL PURPOSE FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Taxes and shared revenues 14,045$ 15,182$ 1,137$ Charges for services 20,500 22,205 1,705 Use of money and property 810 1,520 710 Reimbursements and grants 35 35 Miscellaneous 71 1,550 1,479 Contract revenue 1,600 250 (1,350)

TOTAL CASH RECEIPTS 37,026 40,742 3,716

Expenditures:Personnel expenditures 17,210 13,645 3,565 Contractual services and other charges 15,490 12,330 3,160 Materials and supplies 9,300 8,176 1,124 Capital outlay 8,000 9,751 (1,751) Miscellaneous 585 (585)

TOTAL EXPENDITURES 50,000 44,487 5,513

RECEIPTS OVER (UNDER) EXPENDITURES (12,974) (3,745)

Beginning Unencumbered Cash Balance 12,974 14,971

ENDING UNENCUMBERED CASH BALANCE -$ 11,226$

See independent auditor's report.21

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - FIRE EQUIPMENTSPECIAL PURPOSE FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Miscellaneous $ 2,700$ 2,700$ Contract revenue 72,800 75,664 2,864 Operating transfers 6,500 6,500 -

TOTAL CASH RECEIPTS 79,300 84,864 5,564

Expenditures:Materials and supplies 15,137 15,137 Capital outlay 178,471 61,051 117,420

TOTAL EXPENDITURES 193,608 61,051 132,557

RECEIPTS OVER (UNDER) EXPENDITURES (114,308) 23,813

Beginning Unencumbered Cash Balance 186,090 201,326

ENDING UNENCUMBERED CASH BALANCE 71,782$ 225,139$

See independent auditor's report.22

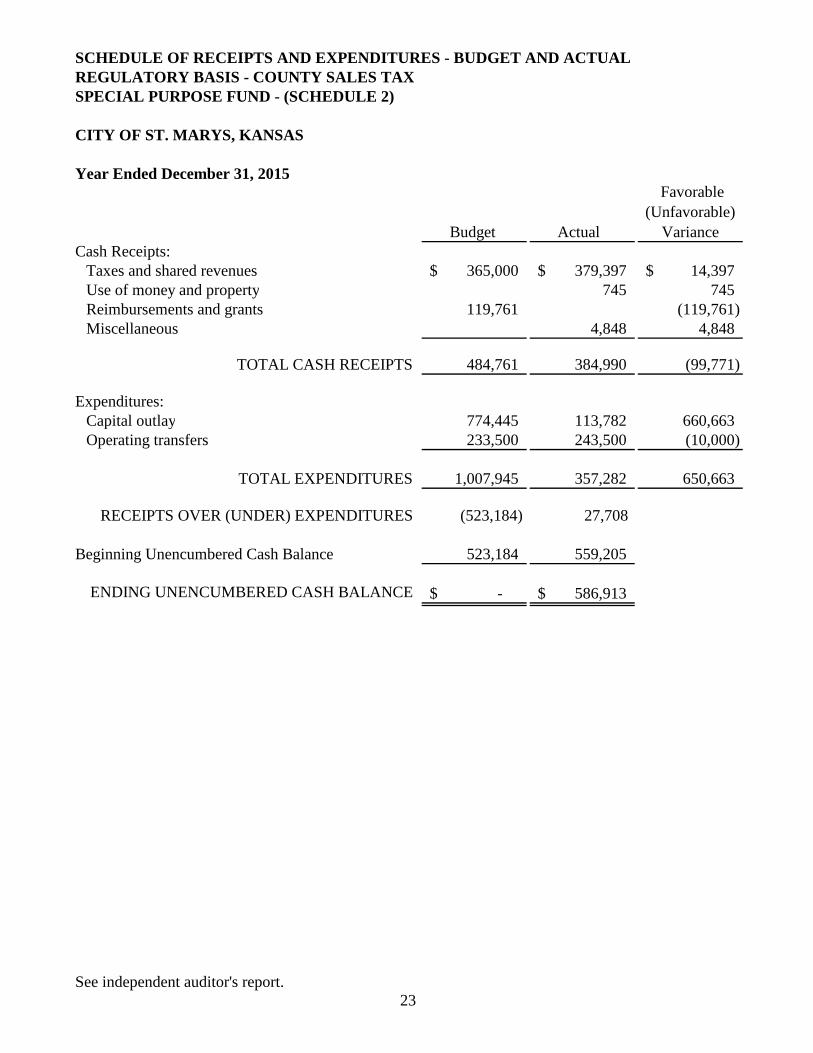

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - COUNTY SALES TAXSPECIAL PURPOSE FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Taxes and shared revenues 365,000$ 379,397$ 14,397$ Use of money and property 745 745 Reimbursements and grants 119,761 (119,761) Miscellaneous 4,848 4,848

TOTAL CASH RECEIPTS 484,761 384,990 (99,771)

Expenditures:Capital outlay 774,445 113,782 660,663 Operating transfers 233,500 243,500 (10,000)

TOTAL EXPENDITURES 1,007,945 357,282 650,663

RECEIPTS OVER (UNDER) EXPENDITURES (523,184) 27,708

Beginning Unencumbered Cash Balance 523,184 559,205

ENDING UNENCUMBERED CASH BALANCE -$ 586,913$

See independent auditor's report.23

SCHEDULE OF RECEIPTS AND EXPENDITURESREGULATORY BASISSUMMARY OF NON-BUDGETED SPECIAL PURPOSE FUNDS - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Crime Prevention

Capital Improvement

Equipment Reserve

Cash Receipts:Licenses, permits, and fees 1,518$ $ $ Use of money and property 135 84 Miscellaneous 1,092 Operating transfers 33,000

TOTAL CASH RECEIPTS 2,610 135 33,084

Expenditures:Materials and supplies 2,495 Capital outlay 2,301 9,943 10,191

TOTAL EXPENDITURES 2,301 12,438 10,191

RECEIPTS OVER (UNDER) EXPENDITURES 309 (12,303) 22,893

Beginning Unencumbered Cash Balance 2,482 15,086 136,322

ENDING UNENCUMBERED CASH BALANCE 2,791$ 2,783$ 159,215$

See independent auditor's report.24

SCHEDULE OF RECEIPTS AND EXPENDITURESREGULATORY BASISSUMMARY SCHEDULE OF CAPITAL PROJECTS FUNDS (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015 Electric

Substation Project

Cash Receipts:

Expenditures:

RECEIPTS OVER (UNDER) EXPENDITURES -

Beginning Unencumbered Cash Balance 4,864

ENDING UNENCUMBERED CASH BALANCE 4,864$

See independent auditor's report.25

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - ELECTRIC UTILITYBUSINESS FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Charges for services 2,089,000$ 2,113,144$ 24,144$ Use of money and property 14,100 6,429 (7,671) Miscellaneous 4,200 19,732 15,532 Contract revenue 1,812 906 (906)

TOTAL CASH RECEIPTS 2,109,112 2,140,211 31,099

Expenditures:Personnel expenditures 328,826 323,333 5,493 Contractual services and other charges 246,202 167,518 78,684 Materials and supplies 1,477,250 1,449,711 27,539 Capital outlay 235,000 149,347 85,653 Miscellaneous 100 39 61

TOTAL EXPENDITURES 2,287,378 2,089,948 197,430

RECEIPTS OVER (UNDER) EXPENDITURES (178,266) 50,263

Beginning Unencumbered Cash Balance 790,135 796,362

ENDING UNENCUMBERED CASH BALANCE 611,869$ 846,625$

See independent auditor's report.26

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - WATER UTILITYBUSINESS FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Charges for services 303,900$ 276,527$ (27,373)$ Use of money and property 1,140 3,063 1,923 Miscellaneous 4,800 6,853 2,053

TOTAL CASH RECEIPTS 309,840 286,443 (23,397)

Expenditures:Personnel expenditures 199,912 198,613 1,299 Contractual services and other charges 80,709 82,773 (2,064) Materials and supplies 18,620 15,838 2,782 Capital outlay 12,500 10,772 1,728 Miscellaneous 9 (9) Debt payments:

Principal 21,581 23,303 (1,722) Interest 16,678 14,955 1,723

TOTAL EXPENDITURES 350,000 346,263 3,737

RECEIPTS OVER (UNDER) EXPENDITURES (40,160) (59,820)

Beginning Unencumbered Cash Balance 194,113 232,368

ENDING UNENCUMBERED CASH BALANCE 153,953$ 172,548$

See independent auditor's report.27

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - SEWER SERVICEBUSINESS FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Charges for services 526,450$ 524,049$ (2,401)$ Use of money and property 100 149 49 Miscellaneous 2,608 2,608

TOTAL CASH RECEIPTS 526,550 526,806 256

Expenditures:Personnel expenditures 173,528 159,282 14,246 Contractual services and other charges 62,911 88,792 (25,881) Materials and supplies 19,750 20,798 (1,048) Capital outlay 45,000 45,000 Miscellaneous 13 (13) Operating transfers 290,919 273,419 17,500

TOTAL EXPENDITURES 592,108 542,304 49,804

RECEIPTS OVER (UNDER) EXPENDITURES (65,558) (15,498)

Beginning Unencumbered Cash Balance 195,195 276,545

ENDING UNENCUMBERED CASH BALANCE 129,637$ 261,047$

See independent auditor's report.28

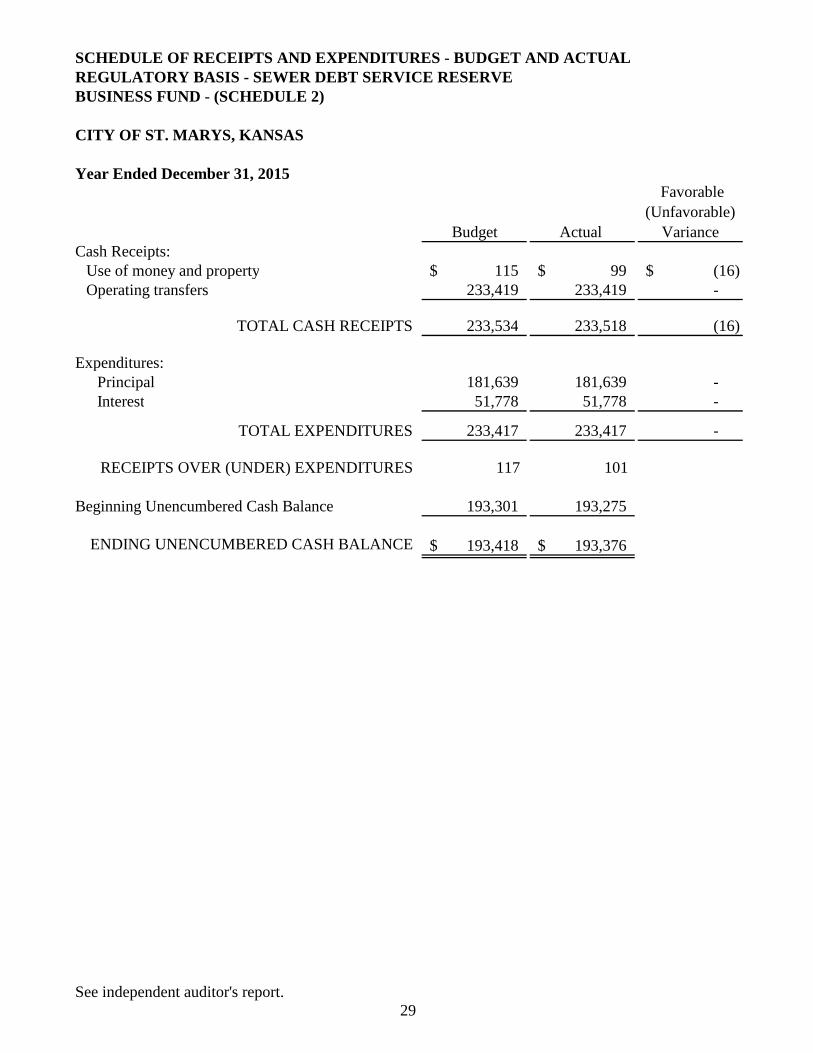

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - SEWER DEBT SERVICE RESERVEBUSINESS FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Use of money and property 115$ 99$ (16)$ Operating transfers 233,419 233,419 -

TOTAL CASH RECEIPTS 233,534 233,518 (16)

Expenditures:Principal 181,639 181,639 - Interest 51,778 51,778 -

TOTAL EXPENDITURES 233,417 233,417 -

RECEIPTS OVER (UNDER) EXPENDITURES 117 101

Beginning Unencumbered Cash Balance 193,301 193,275

ENDING UNENCUMBERED CASH BALANCE 193,418$ 193,376$

See independent auditor's report.29

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - GOLF COURSEBUSINESS FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Charges for services 102,103$ 82,248$ (19,855)$ Use of money and property 20,950 31,403 10,453 Reimbursements and grants 5,010 5,010 Miscellaneous 10,000 18,468 8,468 Contract revenue 4,500 4,500 - Operating transfers 15,000 15,000 -

TOTAL CASH RECEIPTS 152,553 156,629 4,076

Expenditures:Personnel expenditures 109,575 88,647 20,928 Contractual services and other charges 28,264 30,701 (2,437) Materials and supplies 19,000 24,861 (5,861) Capital outlay 4,949 (4,949) Miscellaneous 2,019 5,391 (3,372) Operating transfers 2,142 2,142 -

TOTAL EXPENDITURES 161,000 156,691 4,309

RECEIPTS OVER (UNDER) EXPENDITURES (8,447) (62)

Beginning Unencumbered Cash Balance 15,733 4,975

ENDING UNENCUMBERED CASH BALANCE 7,286$ 4,913$

See independent auditor's report.30

SCHEDULE OF RECEIPTS AND EXPENDITURES - BUDGET AND ACTUALREGULATORY BASIS - REFUSE UTILITYBUSINESS FUND - (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Budget Actual

Favorable (Unfavorable)

Variance Cash Receipts:

Licenses, permits, and fees 9,500$ 11,282$ 1,782$ Charges for services 222,200 226,361 4,161 Miscellaneous 3,500 3,254 (246)

TOTAL CASH RECEIPTS 235,200 240,897 5,697

Expenditures:Personnel expenditures 135,741 136,468 (727) Contractual services and other charges 87,673 90,849 (3,176) Materials and supplies 20,500 10,923 9,577 Capital outlay 10,000 456 9,544 Operating transfers 20,321 20,321

TOTAL EXPENDITURES 274,235 238,696 35,539

RECEIPTS OVER (UNDER) EXPENDITURES (39,035) 2,201

Beginning Unencumbered Cash Balance 39,035 55,530

ENDING UNENCUMBERED CASH BALANCE -$ 57,731$

See independent auditor's report.31

SCHEDULE OF RECEIPTS AND EXPENDITURESREGULATORY BASISSUMMARY OF NON-BUDGETED BUSINESS FUNDS (SCHEDULE 2)

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Sewer Reserve Cash Receipts:

Operating transfers 40,000$

Expenditures:Capital outlay 70,066

RECEIPTS OVER (UNDER) EXPENDITURES (30,066)

Beginning Unencumbered Cash Balance 45,776

ENDING UNENCUMBERED CASH BALANCE 15,710$

See independent auditor's report.32

SUMMARY OF RECEIPTS AND DISBURSEMENTSREGULATORY BASISAGENCY FUNDS (SCHEDULE 3)

CITY OF ST. MARYS, KANSAS

For the Year Ended December 31, 2015

Fund Beginning Cash

Balance Receipts Disbursements Ending Cash

Balance Trust and agency:

Municipal Court ADSAP 15$ $ $ 15$ Municipal Court 36,060 36,060 - Customer deposits 50,277 32,045 34,262 48,060

TOTAL 50,292 68,105 70,322 48,075

See independent auditor's report.33

OTHER INFORMATION

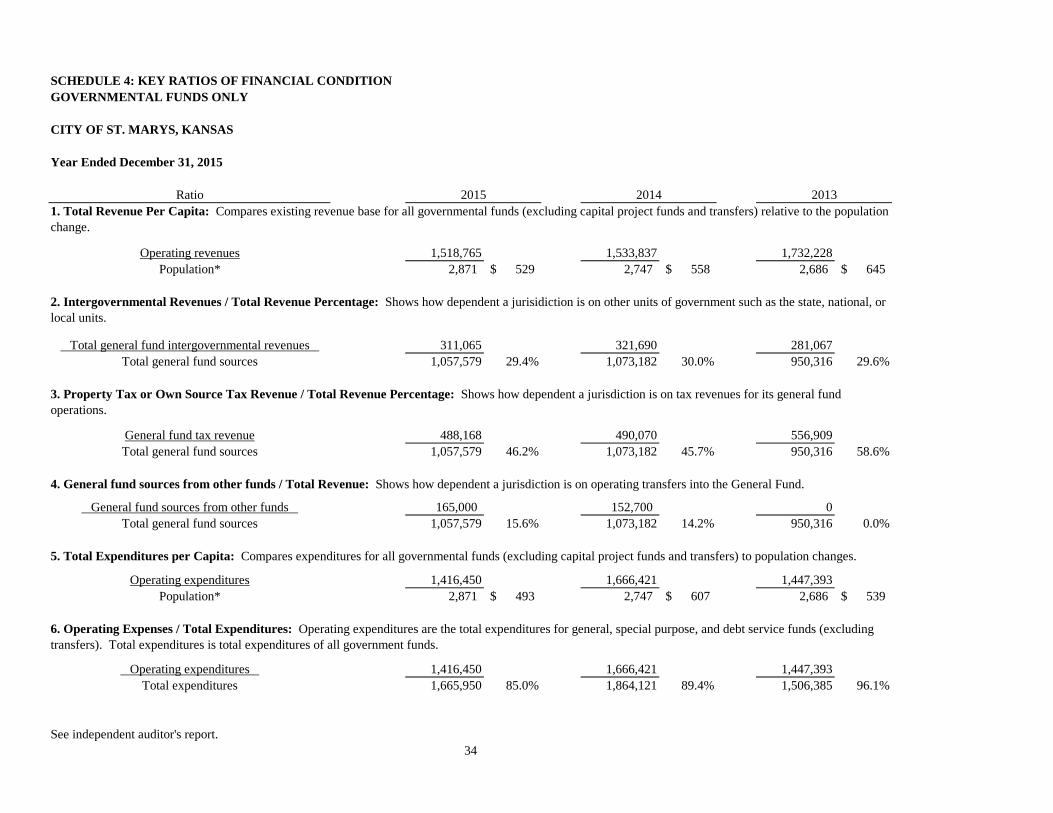

SCHEDULE 4: KEY RATIOS OF FINANCIAL CONDITIONGOVERNMENTAL FUNDS ONLY

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Ratio

Operating revenues 1,518,765 1,533,837 1,732,228Population* 2,871 529$ 2,747 558$ 2,686 645$

Total general fund intergovernmental revenues 311,065 321,690 281,067Total general fund sources 1,057,579 29.4% 1,073,182 30.0% 950,316 29.6%

General fund tax revenue 488,168 490,070 556,909Total general fund sources 1,057,579 46.2% 1,073,182 45.7% 950,316 58.6%

General fund sources from other funds 165,000 152,700 0Total general fund sources 1,057,579 15.6% 1,073,182 14.2% 950,316 0.0%

Operating expenditures 1,416,450 1,666,421 1,447,393Population* 2,871 493$ 2,747 607$ 2,686 539$

Operating expenditures 1,416,450 1,666,421 1,447,393Total expenditures 1,665,950 85.0% 1,864,121 89.4% 1,506,385 96.1%

See independent auditor's report.

2. Intergovernmental Revenues / Total Revenue Percentage: Shows how dependent a jurisidiction is on other units of government such as the state, national, or local units.

3. Property Tax or Own Source Tax Revenue / Total Revenue Percentage: Shows how dependent a jurisdiction is on tax revenues for its general fund operations.

4. General fund sources from other funds / Total Revenue: Shows how dependent a jurisdiction is on operating transfers into the General Fund.

6. Operating Expenses / Total Expenditures: Operating expenditures are the total expenditures for general, special purpose, and debt service funds (excluding transfers). Total expenditures is total expenditures of all government funds.

5. Total Expenditures per Capita: Compares expenditures for all governmental funds (excluding capital project funds and transfers) to population changes.

2013201420151. Total Revenue Per Capita: Compares existing revenue base for all governmental funds (excluding capital project funds and transfers) relative to the population change.

34

SCHEDULE 4: KEY RATIOS OF FINANCIAL CONDITIONGOVERNMENTAL FUNDS ONLY

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Ratio 201320142015

Total revenues 1,755,407 1,758,679 1,798,370Total expenditures 1,665,950 1.054 1,864,121 0.943 1,506,385 1.194

8. Operating Surplus (deficit) / Operating Revenues Percentage: Reflects the results of the general fund operations.

General fund receipts over (under) expenditures 16,779 9,216 -125,787General fund revenue 1,057,579 1.59% 1,073,182 0.86% 950,316 -13.24%

9. General Fund Balance / General Fund Revenues Percentage: Measures a jurisdictions capacity to withstand financial emergencies.

General fund Unencumbered Cash Balance 438,460 421,680 412,464Total general fund revenues 1,057,579 41.46% 1,073,18239.29% 950,316 43.40%

10. General Obligation Debt / Population: Full faith and credit debt of the jurisdiction divided by the population.

General obligation debt 155,000 195,000 235,000Population* 2,871 54$ 2,747 71$ 2,686 87$

11. General Obligation Debt / Assessed Value Percentage: Full faith and credit debt of the jurisdiction divided by the assessed value.

General obligation debt 155,000 195,000 235,000 Assessed Value (per budget) 15,584,369 0.99% 15,157,084 1.29% 14,743,919 1.59%

Debt service 45,990 46,911 63,326Operating revenues 1,518,765 3.03% 1,533,837 3.06% 1,732,228 3.66%

See independent auditor's report.

* Based on 2010 census, average increase per year from 2000 census to 2010 was 2.27% for the City. County wide the population increased 1.86% per year and 6.13% per year statewide.

35

7. Total Revenues / Total Expenditures: Total revenues for all governmental funds and total expenditures for all governmental funds.

12. Debt service / Operating Revenues Percentage: Measures the level of debt service to total general fund revenues.

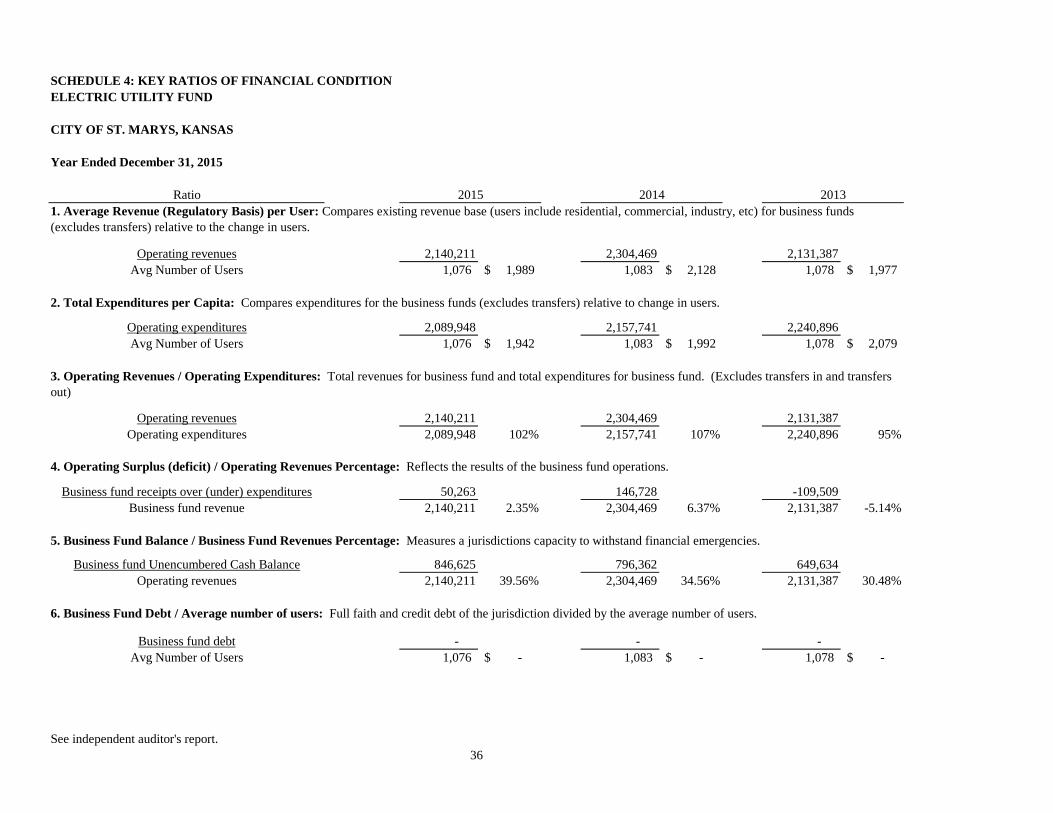

SCHEDULE 4: KEY RATIOS OF FINANCIAL CONDITIONELECTRIC UTILITY FUND

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Ratio

Operating revenues 2,140,211 2,304,469 2,131,387Avg Number of Users 1,076 1,989$ 1,083 2,128$ 1,078 1,977$

Operating expenditures 2,089,948 2,157,741 2,240,896Avg Number of Users 1,076 1,942$ 1,083 1,992$ 1,078 2,079$

Operating revenues 2,140,211 2,304,469 2,131,387Operating expenditures 2,089,948 102% 2,157,741 107% 2,240,896 95%

4. Operating Surplus (deficit) / Operating Revenues Percentage: Reflects the results of the business fund operations.

Business fund receipts over (under) expenditures 50,263 146,728 -109,509Business fund revenue 2,140,211 2.35% 2,304,469 6.37% 2,131,387 -5.14%

Business fund Unencumbered Cash Balance 846,625 796,362 649,634Operating revenues 2,140,211 39.56% 2,304,469 34.56% 2,131,387 30.48%

Business fund debt - - - Avg Number of Users 1,076 -$ 1,083 -$ 1,078 -$

See independent auditor's report.36

5. Business Fund Balance / Business Fund Revenues Percentage: Measures a jurisdictions capacity to withstand financial emergencies.

2. Total Expenditures per Capita: Compares expenditures for the business funds (excludes transfers) relative to change in users.

3. Operating Revenues / Operating Expenditures: Total revenues for business fund and total expenditures for business fund. (Excludes transfers in and transfers out)

6. Business Fund Debt / Average number of users: Full faith and credit debt of the jurisdiction divided by the average number of users.

2015 2014 20131. Average Revenue (Regulatory Basis) per User: Compares existing revenue base (users include residential, commercial, industry, etc) for business funds (excludes transfers) relative to the change in users.

SCHEDULE 4: KEY RATIOS OF FINANCIAL CONDITIONELECTRIC UTILITY FUND

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Ratio 2015 2014 20137. Debt service expense / Operating Revenues Percentage: Measures the level of debt service to total business fund revenues.

Debt service - - 0Operating revenues 2,140,211 0.00% 2,304,469 0.00% 2,131,387 0.00%

Operating revenues 2,140,211 2,304,469 2,131,387KWH Sold 17,890,389 0.120$ 18,189,136 0.127$ 18,663,203 0.114$

Operating expenditures 2,089,948 2,157,741 2,240,896KWH Sold 17,890,389 0.117$ 18,189,136 0.119$ 18,663,203 0.120$

KWH Purchased - KWH Sold 2,558,756 2,758,864 2,774,797 KWH Purchased 20,449,145 13% 20,948,000 13% 21,438,000 13%

See independent auditor's report.

8. Average Price Per KWH sold: Revenue (Regulatory Basis) / KWH Sold: Compares existing revenue base for business funds (excludes transfers) relative to the change in actual usage.

37

9. Average Cost Per KWH sold: Operating Expenditures / KWH Sold: Compares operating expenditures for business funds (excludes transfers) relative to the change in actual usage.

10. Line Loss: Compares the KWH purchased to what is actually sold, difference being line loss (line loss includes electric power used by City operations, used but not billed)

SCHEDULE 4: KEY RATIOS OF FINANCIAL CONDITIONWATER UTILITY FUND

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Ratio

Operating revenues 286,443 313,009 311,392Avg Number of Users 954 300$ 956 327$ 955 326$

Operating expenditures 346,263 316,063 306,229Avg Number of Users 954 363$ 956 331$ 955 321$

Operating revenues 286,443 313,009 311,392Operating expenditures 346,263 83% 316,063 99% 306,229 102%

4. Operating Surplus (deficit) / Operating Revenues Percentage: Reflects the results of the business fund operations.

Business fund receipts over (under) expenditures -59,820 -3,054 5,163Business fund revenue 286,443 -20.88% 313,009 -0.98% 311,392 1.66%

Business fund Unencumbered Cash Balance 172,548 232,368 235,422Operating revenues 286,443 60.24% 313,009 74.24% 311,392 75.60%

Business fund debt 408,562 431,864 454,370Avg Number of Users 954 428$ 956 452$ 955 476$

See independent auditor's report.

5. Business Fund Balance / Business Fund Revenues Percentage: Measures a jurisdictions capacity to withstand financial emergencies.

1. Average Revenue (Regulatory Basis) per User: Compares existing revenue base (users include residential, commercial, industry, etc) for business funds (excludes transfers) relative to the change in users.

2. Total Expenditures per Capita: Compares expenditures for the business funds (excludes transfers) relative to change in users.

3. Operating Revenues / Operating Expenditures: Total revenues for business fund and total expenditures for business fund. (Excludes transfers in and transfers out)

6. Business Fund Debt / Average number of users: Full faith and credit debt of the jurisdiction divided by the average number of users. Water fund has an oustanding KDHE Public Water Supply revolving loan with an issue date of 2/13/2008 and maturity date of 2/1/2029.

38

2015 2014 2013

SCHEDULE 4: KEY RATIOS OF FINANCIAL CONDITIONWATER UTILITY FUND

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Ratio 2015 2014 20137. Debt service expense / Operating Revenues Percentage: Measures the level of debt service to total business fund revenues.

Debt service 38,258 38,259 38,259 Operating revenues 286,443 13.36% 313,009 12.22% 311,392 12.29%

Operating revenues 286,443 313,009 311,392 Gallons sold 77,158,645 0.0037$ 82,201,236 0.0038$ 84,982,120 0.0037$

Operating expenditures 346,263 316,063 306,229 Gallons sold 77,158,645 0.0045$ 82,201,236 0.0038$ 84,982,120 0.0036$

Gallons pumped - Gallons Sold 12,868,355 9,858,764 6,241,880 Gallons pumped 90,027,000 14% 92,060,000 11% 91,224,000 7%

See independent auditor's report.39

8. Average Price Per Gallon Sold: Revenue (Regulatory Basis) / Gallons Sold: Compares existing revenue base for business funds (excludes transfers) relative to the change in actual usage.

9. Average Cost Per Gallon sold: Operating Expenditures / Gallons Sold: Compares operating expenditures for business funds (excludes transfers) relative to the change in actual usage.

10. Line Loss: Compares the gallons pumped to what is actually sold, difference being line loss (line loss includes water used by City operations, used but not billed)

SCHEDULE 4: KEY RATIOS OF FINANCIAL CONDITIONSEWER UTILITY FUND

CITY OF ST. MARYS, KANSAS

Year Ended December 31, 2015

Ratio

Operating revenue 526,806 539,337 531,611Avg Number of Users 954 552$ 956 564$ 955 557$

Operating expenditures 502,304 467,876 483,591Avg Number of Users 954 527$ 956 489$ 955 506$

Operating revenue 526,806 539,337 531,611Operating expenditures 502,304 105% 467,876 115% 483,591110%

4. Operating Surplus (deficit) / Operating Revenues Percentage: Reflects the results of the business fund operations.

Business fund receipts over (under) expenditures 24,502 71,461 48,020Operating revenue 526,806 4.65% 539,337 13.25% 531,611 9.03%

Business fund Unencumbered Cash Balance 261,047 276,545 250,084Operating revenues 526,806 49.55% 539,337 51.27% 531,61147.04%

Business fund debt 1,346,990 1,528,630 1,704,092Avg Number of Users 954 1,412$ 956 1,599$ 955 1,784$

7. Debt service expense / Operating Revenues Percentage: Measures the level of debt service to total business fund revenues.

Debt service 233,417 233,418 233,417 Operating revenues 526,806 44.31% 539,337 43.28% 531,611 43.91%

See independent auditor's report.40

5. Business Fund Balance / Business Fund Revenues Percentage: Measures a jurisdictions capacity to withstand financial emergencies.

2015 2014 20131. Average Revenue (Regulatory Basis) per User: Compares existing revenue base (users include residential, commercial, industry, etc) for business funds (excludes transfers) relative to the change in users.

2. Total Expenditures per Capita: Compares expenditures for the business funds (includes transfer to sewer debt service fund only) relative to change in users.

3. Operating Revenues / Operating Expenditures: Total revenues for business fund and total expenditures for business fund. (includes transfer to sewer debt service fund only)

6. Business Fund Debt / Average number of users: Full faith and credit debt of the jurisdiction divided by the average number of users. Sewer fund has an outstanding KDHE Water Pollution control revolving loan with an issue date of 8/22/2000 and maturity date of 3/1/2022.