31

Clarke v Commissioner of Taxation (2009) 240 CLR 272 MP's Superannuation meets State Rights

Clarke v Commissioner of Taxation (2009) 240 CLR 272

MP's Superannuation meets State Rights

• Ralph Clarke, Adelaide City Councillor• Mike Wait, Crown Solicitor's Office

Presenter

• In the first 20 years of Federation the High Court, borrowing from US jurisprudence, developed the implied immunity of instrumentalities.

• Otherwise known as the doctrine of mutual non-interference, it operated to protect states from the operation of Commonwealth laws and vice versa.

Pre-Engineers Immunities

Amalgamated Society of Engineers v Adelaide Steamship Co (1920) 28 CLR 129

• Employees of WA – the engineers – challenged the application of Federal industrial awards to them.

• Doctrine of implied immunity of instrumentalities (together with the reserved powers doctrine) was abandoned.

• Since this time it has been accepted that Commonwealth laws bind the states and vice versa.

Melbourne Corporation v Commonwealth (1947) 74 CLR 31

• Commonwealth passed legislation requiring all states to bank with the newly created Commonwealth Bank.

• Court held the legislation to be invalid.• Court recognised an implied doctrine of

intergovernmental immunity.• Narrower than the pre-Engineers immunity

which had exempted states from all Commonwealth laws.

Foundation of the Melbourne Corporation Doctrine

• Articulated by Dixon J at 82:“The foundation of the Constitution is the conception of a central government and a number of State Governments separately organised. The Constitution predicates their continued existence as independent entities. Among them it distributes powers of governing the country.”

• From this the Court implied a limitation on Commonwealth legislative power.

Breadth of the Doctrine

• Despite this crisp statement of principle, in practice it is difficult to apply. Raises the question – what is meant by “existence as independent entities”?

• We know that the doctrine does not protect the States from Commonwealth laws that merely affect their interests generally (eg Tasmanian Dam Case, Native Title Act Case).

• Rather, doctrine is limited to protecting states from Commonwealth laws “that curtails or interfere with the capacity of the states to function as governments” (Bayside City Council v Telstra (2004) 216 CLR 595 at 626 [31] per the Court).

• This is generally limited to a liberty for the States to order their own constitutional affairs.

The “practical question”

• Application of the doctrine is often said to involve a “practical question”. In Melbourne Corporation Starke J said at 75:

“It is a practical question, whether legislation or executive action thereunder on the part of a Commonwealth or of a State destroys, curtails or interferes with the operations of the other, depending upon the character and operation of the legislation and executive action thereunder. No doubt the nature and extent of the activity affected must be

considered and also whether the interference is or is not discriminatory but in the end the question must be whether the legislation or the executive action curtails or interferes in a substantial manner with the exercise of constitutional power by the other.”

An ambiguity arises…

• It is unclear whether the Melbourne Corporation doctrine is to be applied either:– As a matter of fact and degree – that is, how intrusive is

the impugned Commonwealth law in the particular constitutional arrangements made by a particular state? or

– As a bright line test – that is, does the impugned Commonwealth law intrude into a designated field reserved to the states?

Arguments presented by South Australia in Clarke v Commonwealth

• Straddling this ambiguity two submissions were put on behalf of the Attorney-General attacking the validity of the Commonwealth Superannuation Surcharge laws in so far as they applied to parliamentarians:– First, the laws singled out state parliamentarians (amongst other State

officials) to their financial disadvantage, from the mainstream of high income earners, and thereby impaired the capacity of the states to attract, support and retain the services of parliamentarians; (the fact and degree submission applying Austin) and,

– Second, regardless of any differential treatment brought about by the Surcharge Laws, they impair the capacity of the states to remunerate parliamentarians upon the terms and conditions that they regard as being constitutionally appropriate by imposing a personal liability on parliamentarians by reference to one of the central terms upon which state parliamentarians are engaged (the bright line submission).

The impugned laws – the Superannuation Surcharge Laws

• The surcharge was introduced to apply an additional tax on the super contributions made by higher income earners.

• Contributions could be personal or made by the employer pursuant to the superannuation guarantee legislation.

• In order to avoid any concerns about the Cth applying a tax to the funds of a State (contrary to s 114 of the Constitution) the Cth enacted two separate pieces of legislation to operate the scheme:– Laws of general application that applied to any high income

earner. – Laws specifically applying to employees of State

governments (called “constitutionally protected funds”).

The legislation applies more harshly to highly paid state officials • The general application laws applied differently in that the

liability to pay the super surcharge fell on the superannuation provider – with the intention or understanding that the liability would be passed onto the high income earner as a fee or charge.

• For employees of the states, the liability was personal. That is the high income earner was personally liable for the debt and was required to make payments to the tax office annually or elect to defer and have a lump sum deducted from their payout. Where a person elected to defer – interest was imposed on the deferred amount, compounding on an annual basis.

Austin v Commonwealth of Australia (2003) 215 CLR 185

• The High Court considered the application of the doctrine in the context of the Superannuation Surcharge in Austin.

• In that case, the applicant was a judge of the NSW Supreme Court.

• The Court found that by applying the superannuation surcharge to the judicial pension scheme, the Commonwealth was impermissibly interfering with NSW’s ability to appoint and remunerate its judges.

No separate discrimination limb• Some of the earlier decisions of the Court had decided that there

were two limbs to the Melbourne Corporation doctrine. Commonwealth laws could be invalidated on two bases: first, where the law interfered with the capacity of a state; second, where a law discriminated against a state.

• A majority of the Court in Austin rejected discrimination as a stand alone limb. At [124] Gaudron, Gummow and Hayne JJ stated:

“There is, in our view, but one limitation, though the apparent expression of it varies with the form of the legislation under consideration. The question presented by the doctrine in any given case requires assessment of the impact of particular laws by such criteria as ‘special burden’ and ‘curtailment’ of ‘capacity’ of the States ‘to function as governments’. These criteria are to be applied by consideration not only of the form but also ‘the substance and actual operation’ of the federal law. Further, this inquiry inevitably turns upon matters of evaluation and degree and of ‘constitutional facts’ which are not readily established by objective methods in curial proceedings.”

Surcharge Laws held not to apply to state judges

• Central to the reasoning of the majority in Austin was that the Surcharge laws made it more difficult for states to attract and retain State Judges.

• Applying the decision in Re AEU, the Court considered the State’s ability to determine superannuation of its office holders is a critical issue.

• The nature of the NSW Pension scheme was critical to the decision. In that State, Judge’s pensions were:

– taken as a periodic pension– no option to take a lump sum– once eligible, the quantum did not increase with extended length of service

• If Judges chose to defer super surcharge liability, they would potentially face a large tax liability with no lump sum payment from which to meet that liability.

• The effect was a matter of argument, but included potentially encouraging judges to retire as soon as they qualified for a pension (to avoid the surcharge liability).

• The Court also had regard to amendments made by NSW to the pension scheme (allowing lump sum payments to meet surcharge liability) as evidence of the impact on the State’s chosen remuneration scheme.

Commonwealth attempts to distinguish Austin in Clarke

• In Clarke the Commonwealth attempted to distinguish Austin on several bases:– The way in which the Parliamentary Superannuation Scheme (PSS)

applied was somewhat different to the Judicial Pension Scheme considered in Austin.

• The PSS contained a pre-existing right (prior to the surcharge imposition) for MPs to commute their pension and obtain a lump sum at the time of retirement. However, the commutation rate was designed to penalise the MP, in order to encourage them to take a pension (which had a benefit for managing State finances).

• After the surcharge was introduced, the Parliament amended the legislation to provide an addition right to commute the pension – at a more favourable commutation rate. The commutation for the purposes of the surcharge was introduced, to ensure the MP was not penalised.

– The PSS did not reach a maximum entitlement until after 30 years in Parliament, so whilst surcharge was accruing the MP was also obtaining extra benefits.

– In Austin State Judges were treated differently to Federal Judges and there was no equivalent disparity of treatment in Clark.

Absence of evidence

• The Commonwealth also argued that Ralph Clarke and SA had failed to put evidence before the Court to demonstrate the negative effect of the Surcharge Laws on the ability to attract and retain MPs.

• It was argued that the new right of commutation introduced into the PSS was not sufficient evidence of the impact of the Surcharge Laws on the State’s ability to attract and retain MPs.

South Australia sought to draw an analogy with Austin

• In rebuttal South Australia argued that the analogy with Austin was sound.

• Just as the Commonwealth tax impaired our ability to attract and retain good judges, it also affected our ability to attract and retain good parliamentarians. The key point was that the surcharge operated in the same way on MPs as it operated on judges and potentially caused the same type of lump sum liability.

• Not only did it affect MPs financially in the same way as judges, there was an analogous constitutional imperative at play. – It is important to secure the remuneration of judges to bolster their

independence. – It is important to remunerate MPs well so as to attract MPs from all

walks of life.

Court upheld the first submission

• In Clarke the Court unanimously upheld this submission. The appeal was allowed and the imposition of surcharge invalidated on the basis of a direct application of Austin.

French CJ• French CJ delivered a leading judgment. He enunciated the doctrine at [34]:

“In my opinion, the application of the implied limitation requires a multifactorial assessment. Factors relevant to its application include:

– Whether the law in question singles out one or more of the States and imposes a special burden or disability on them which is not imposed on persons generally.

– Whether the operation of a law of general application imposes a particular burden or disability on the States.

– The effect of the law upon the capacity of the States to exercise their constitutional powers.

– The effect of the law upon the exercise of their functions by the States.

– The nature of the capacity or functions affected.

– The subject matter of the law affecting the State or States and in particular the extent to which the constitutional head of power under which the law is made authorises its discriminatory application.”

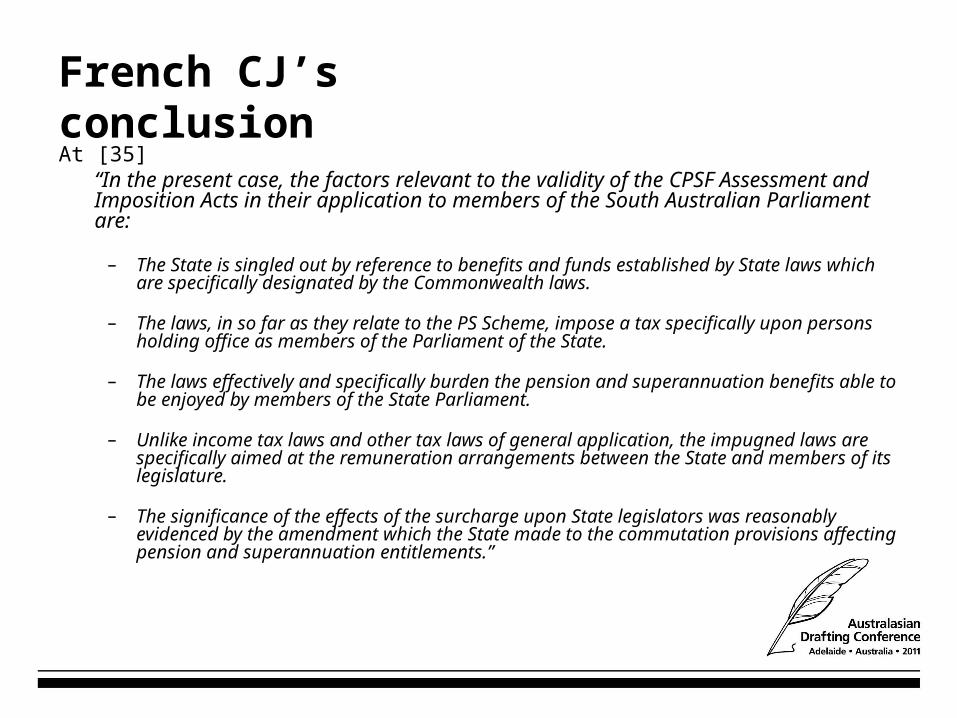

French CJ’s conclusionAt [35]

“In the present case, the factors relevant to the validity of the CPSF Assessment and Imposition Acts in their application to members of the South Australian Parliament are:

– The State is singled out by reference to benefits and funds established by State laws which are specifically designated by the Commonwealth laws.

– The laws, in so far as they relate to the PS Scheme, impose a tax specifically upon persons holding office as members of the Parliament of the State.

– The laws effectively and specifically burden the pension and superannuation benefits able to be enjoyed by members of the State Parliament.

– Unlike income tax laws and other tax laws of general application, the impugned laws are specifically aimed at the remuneration arrangements between the State and members of its legislature.

– The significance of the effects of the surcharge upon State legislators was reasonably evidenced by the amendment which the State made to the commutation provisions affecting pension and superannuation entitlements.”

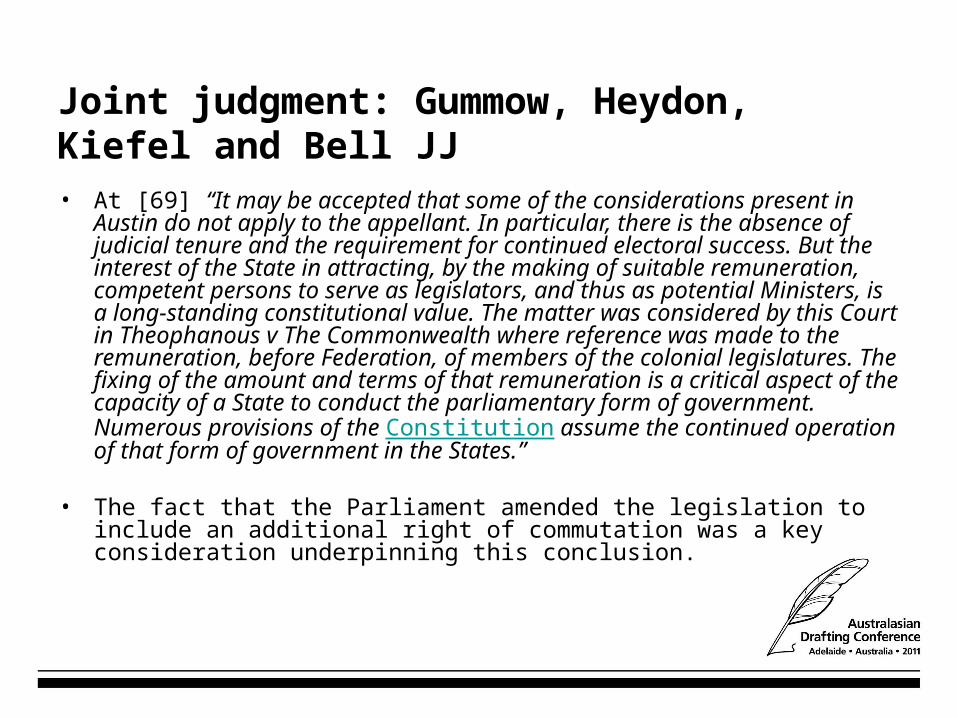

Joint judgment: Gummow, Heydon, Kiefel and Bell JJ• At [69] “It may be accepted that some of the considerations present in

Austin do not apply to the appellant. In particular, there is the absence of judicial tenure and the requirement for continued electoral success. But the interest of the State in attracting, by the making of suitable remuneration, competent persons to serve as legislators, and thus as potential Ministers, is a long-standing constitutional value. The matter was considered by this Court in Theophanous v The Commonwealth where reference was made to the remuneration, before Federation, of members of the colonial legislatures. The fixing of the amount and terms of that remuneration is a critical aspect of the capacity of a State to conduct the parliamentary form of government. Numerous provisions of the Constitution assume the continued operation of that form of government in the States.”

• The fact that the Parliament amended the legislation to include an additional right of commutation was a key consideration underpinning this conclusion.

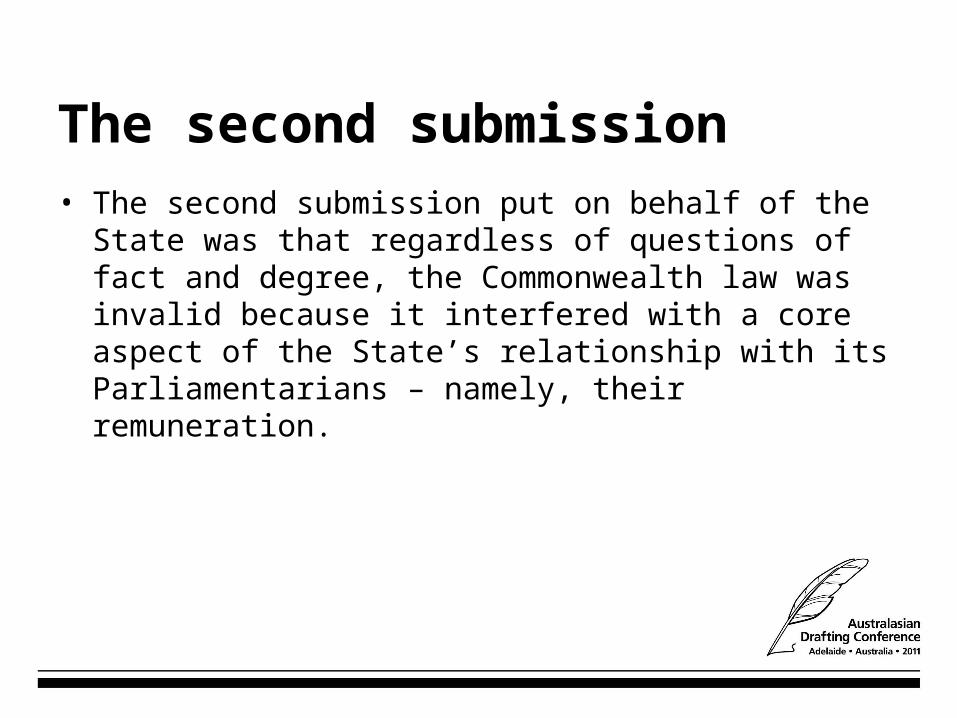

The second submission• The second submission put on behalf of the State was

that regardless of questions of fact and degree, the Commonwealth law was invalid because it interfered with a core aspect of the State’s relationship with its Parliamentarians – namely, their remuneration.

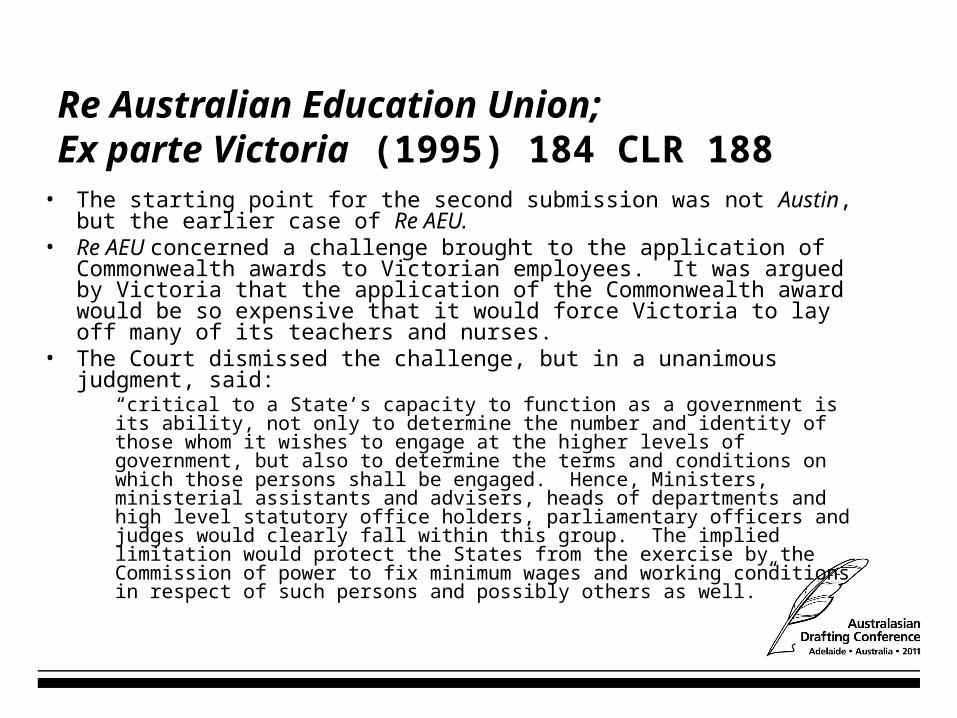

Re Australian Education Union; Ex parte Victoria (1995) 184 CLR 188

• The starting point for the second submission was not Austin, but the earlier case of Re AEU.

• Re AEU concerned a challenge brought to the application of Commonwealth awards to Victorian employees. It was argued by Victoria that the application of the Commonwealth award would be so expensive that it would force Victoria to lay off many of its teachers and nurses.

• The Court dismissed the challenge, but in a unanimous judgment, said:“critical to a State’s capacity to function as a government is its ability, not only to determine the number and identity of those whom it wishes to engage at the higher levels of government, but also to determine the terms and conditions on which those persons shall be engaged. Hence, Ministers, ministerial assistants and advisers, heads of departments and high level statutory office holders, parliamentary officers and judges would clearly fall within this group. The implied limitation would protect the States from the exercise by the Commission of power to fix minimum wages and working conditions in respect of such persons and possibly others as well.”

Analogy to Re AEUSouth Australia attempted to apply the high office holder exception recognised

in Re AEU to Clarke. The argument adopted the following steps:• It was an agreed fact that Ralph Clarke, as a member of the South

Australian Parliament, was a high office holder of state government.• In Austin it had been held that the concept of remuneration includes the

provision of superannuation and like benefits.• The Surcharge Laws impose tax liability upon the Appellant by reference to

his remuneration. • The Surcharge Laws thereby impaired the capacity of the State of South

Australia to determine the terms and conditions on which the Appellant was engaged.

• In other words, if the high office holder exception applies to the Commonwealth to prevent it dictating the terms and conditions of high office holders pursuant to the industrial relations power, then it should also apply to limit the Commonwealth’s capacity to impose a tax by reference to those terms and conditions.

The tax cases…Two precedents stood in our way:• Victoria v Commonwealth (1970) 122 CLR 353

(“Pay-roll Tax Case”). Victoria argued that all of its employees should be exempted from Commonwealth pay-roll tax. Failed.

• State Chamber of Commerce and Industry v Commonwealth (1987) 163 CLR 329 (“Second Fringe Benefits Tax Case”). A narrower argument was made that high ranking state officials should be exempt from Commonwealth fringe benefits tax. Failed.

Brennan J’s dissent in the Second Fringe Benefits Tax Case• Brennan J dissented. At 362ff he said that the Commonwealth

Parliament could:“not validly impose tax on a State in respect of so much of the fringe benefits provided in respect of the ‘employment’ of members of the State Parliament, Ministers of the Crown and judges of the State Supreme Court… The relevant principle, implied in the Constitution, is that a law of the Commonwealth cannot unduly impair the capacity of a State to perform its constitutional functions.”

• This looked very much like the high office holder exception which was held in Re AEU to limit the Commonwealth’s power to make industrial awards.

• South Australia argued that the statement in Re AEU constituted the ascendancy of Brennan J’s dissenting approach in the Second Fringe Benefits Tax Case. Therefore, the high office holder limitation recognised in Re AEU should now be taken to restrict the Commonwealth’s taxing power too.

The elephant in the room…

• The larger problem lying behind this submission was not pay-roll tax, fringe benefits tax or even the superannuation surcharge.

• If the Court accepted our submission that the Commonwealth cannot tax the remuneration of high office holders then income tax on high office holders would also be invalid.

• Although this was a large contention, the Solicitor-General did not shy away from it in oral argument.

The Court’s treatment of the second submission• Only judge to deal explicitly with the income tax

point was French CJ who said at [19] that:“State employees or what might broadly be described as ‘constitutional office holders’ do not enjoy … an immunity [from the taxation power of the Commonwealth]. The imposition of income tax on the salaries of members of Parliament, State Ministers, and judges does not infringe any implied prohibition.”

Ambiguity remains for another day

• Remains unclear whether the Melbourne Corporation doctrine operates as a bright line rule or operates as a matter of fact and degree.

• As a bright line rule is represents a stark deviation from the Engineers orthodoxy, because it creates a field of State immunity.

Bright line rule should prevail• It is consistent with authority (eg

Melbourne Corporation and Re AEU).• It respects not just the existence of

States, but their autonomy within narrowly defined fields to make a free choice as to how they order their affairs.

• It prevents the death to the states by a thousand cuts.