10

Cleared OTC FX Margin Methodology: HVAR Framework May 2012

Cleared OTC FX

Margin Methodology: HVAR Framework

May 2012

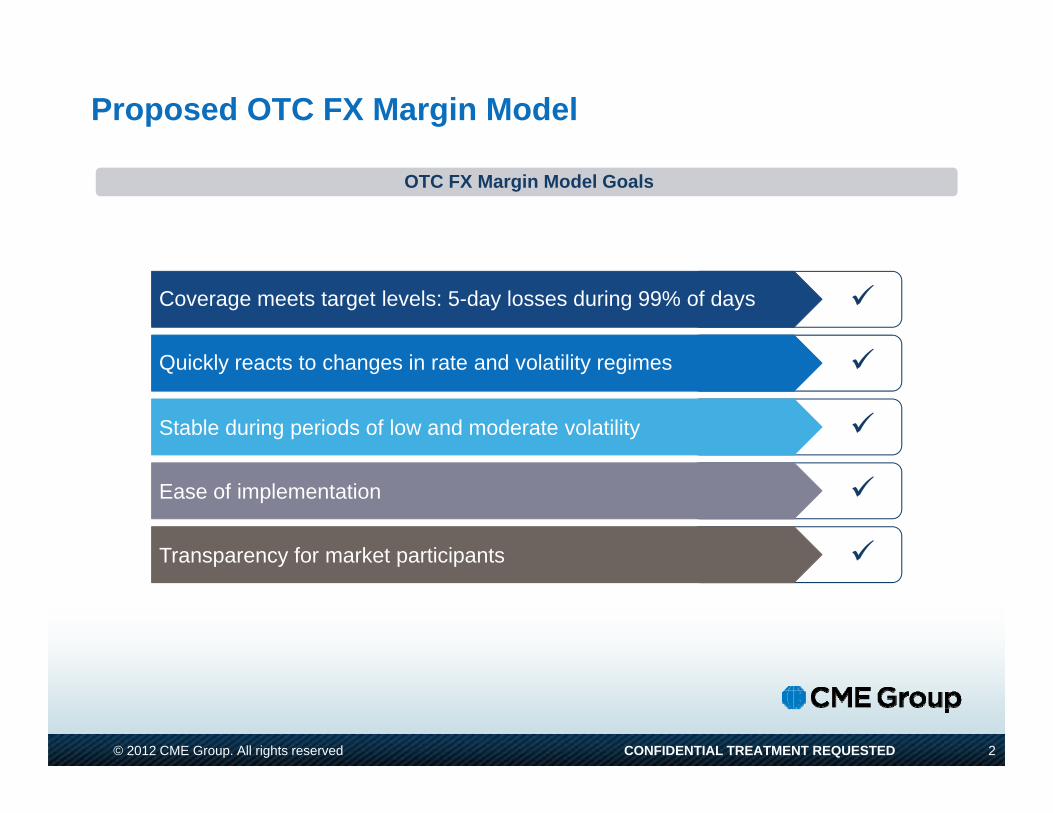

Proposed OTC FX Margin Model

OTC FX Margin Model Goals

Coverage meets target levels: 5-day losses during 99% of days

Q i kl t t h i t d l tilit iQuickly reacts to changes in rate and volatility regimes

Stable during periods of low and moderate volatility

Ease of implementation

Transparency for market participantsTransparency for market participants

© 2012 CME Group. All rights reserved CONFIDENTIAL TREATMENT REQUESTED 2

Proposed OTC FX Margin Model Historical VaRHistorical VaR

Introduction

• The margining model developed by CME Clearing is based on a Historical Value at Risk (HVaR) methodology with Exponentially Weighted Moving Average (EWMA) volatility re-scalinggy p y g g g ( ) y g– This methodology has been well researched over the years and is widely used in the industry

– The very same methodology has been applied by CME to the margining of IRS

– General acceptance by the Dealer Community as safe and sound risk management practice

• In the HVaR framework, past events are used for coming up with possible scenarios in the future– This approach implicitly assumes that historical data series provide a rich enough sample set of the possible

probability distribution of the relevant financial variables

• We found, however, that simple application of the past scenarios to current environment requires enhancement in order to correctly capture the proper volatility regimey p p p y g– To achieve that, our model scales historical returns by the ratio of the forecasted volatility to the realised volatility

from the time-period the shock was sampled

– This allows the model to retain a rich history of data/scenarios, but remain nimble enough to react to the current volatility regime

© 2012 CME Group. All rights reserved CONFIDENTIAL TREATMENT REQUESTED 3

Proposed OTC FX Margin Model Historical VaRHistorical VaR

Model Overview

• The HVaR model with volatility rescaling re-scales shocks obtained from historical price series to a level consistent with the current volatility regime to generate price change distributions which are used in the HVaR calculations.

• A EWMA (Exponentially Weighted Moving Average) volatility model is used as the forecasting model to provide volatility forecasts ‘as if’ computed on each day in the time series. The percentage changes in these conditional volatility forecasts are used to adjust historical shocks to account for the change in the conditional volatility forecast between the date of the shock and ‘today’

– A simple way to understand this volatility scaling is to notice that if forecasted volatility increases, then the distribution of returns will have more dispersion than what is observed in the sampled historical period

– In a highly volatile environment the model appropriately scales up the returns that were obtained during periods of lower volatility

Th it f i l t– The opposite of course, is also true

© 2012 CME Group. All rights reserved CONFIDENTIAL TREATMENT REQUESTED 4

Proposed OTC FX Margin Model Historical VaRHistorical VaR

Methodology Overview

Generate Matrix of Historical Returns

Get historical forward rates for the prior 10 years including all available standard tenors on the forward curve.Calculate 5 days log returns

Adjust Historical Returns for Current Forecasted Volatility

Calculate EWMA forecast of conditional volatility for each day in the history of each currency pairf ( ) fGenerate a distribution of re‐scaled shocks (returns). The return for each day is rescaled using the

forecasted EWMA volatility for that day and the current forecasted EWMA volatility

Calculate Portfolio Margin

Calculate the portfolio gain/loss for each scenario (day) by matrix multiplication of portfolio position in each currency pair by the matrix of volatility‐adjusted price changes for each currency pairSelect the margin as a targeted loss percentile from the portfolio gain/loss distribution

© 2012 CME Group. All rights reserved CONFIDENTIAL TREATMENT REQUESTED 5

Proposed OTC FX Margin Model Historical VaRHistorical VaR

Model Parameters

Pegged Currency Pair Volatility Floor

• We margin each pegged currency separately

• Artificial shocks are applied to today’s forward curve to imply large parallel, slope and curvature moves

• Artificial shocks are periodically reviewed based on the recent market events

© 2012 CME Group. All rights reserved CONFIDENTIAL TREATMENT REQUESTED 6

OTC FX Margin Model Backtesting ResultsBacktesting Results

Portfolio: EUR / USD $100mm vs 91 Days Outright

lambda 94l bd 97lambda 97

© 2012 CME Group. All rights reserved CONFIDENTIAL TREATMENT REQUESTED 7

OTC FX Margin Model Backtesting ResultsBacktesting Results

Portfolio: AUD / USD 183 Days vs USD / JPY 183 Days Cross Pair

© 2012 CME Group. All rights reserved CONFIDENTIAL TREATMENT REQUESTED 8

OTC FX Margin Model Backtesting ResultsBacktesting Results

Portfolio: USD / BRL $100mm 91 Days Outright

© 2012 CME Group. All rights reserved CONFIDENTIAL TREATMENT REQUESTED 9

Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for a futures position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles. And only a portion of those funds should be devoted to any one trade because they cannot expect to profit on every trade.profit on every trade.

The Globe Logo, CME®, Chicago Mercantile Exchange®, and Globex® are trademarks of Chicago Mercantile Exchange Inc. CBOT® and the Chicago Board of Trade® are trademarks of the Board of Trade of the City of Chicago. NYMEX, New York Mercantile Exchange, and ClearPort are trademarks of New York Mercantile Exchange Inc COMEX is a trademark ofClearPort are trademarks of New York Mercantile Exchange, Inc. COMEX is a trademark of Commodity Exchange, Inc. CME Group is a trademark of CME Group Inc. All other trademarks are the property of their respective owners.

The information within this presentation has been compiled by CME Group for general purposes only CME Group assumes no responsibility for any errors or omissions Although every attemptonly. CME Group assumes no responsibility for any errors or omissions. Although every attempt has been made to ensure the accuracy of the information within this presentation, CME Group assumes no responsibility for any errors or omissions. Additionally, all examples in this presentation are hypothetical situations, used for explanation purposes only, and should not be considered investment advice or the results of actual market experience.

All matters pertaining to rules and specifications herein are made subject to and are superseded by official CME, CBOT, NYMEX and CME Group rules. Current rules should be consulted in all cases concerning contract specifications.

© 2012 CME Group. All rights reserved CONFIDENTIAL TREATMENT REQUESTED 10