43

CLERK & TREASURER: WORKING TOGETHER Presenters: Cindy Davis & Jim Beelen Member Information Services Michigan Townships Association 1

| Date post: | 26-Mar-2018 |

| Category: |

Documents |

| Upload: | phunghuong |

| View: | 213 times |

| Download: | 0 times |

CLERK & TREASURER:WORKING TOGETHER

Presenters:Cindy Davis& Jim Beelen Member Information Services Michigan Townships Association

1

Who Do You Work With?

This?2

Who Do You Work With?

Or this?3

Who Do You Work With?

Or this?4

Why Two Offices?

The state’s Accounting Procedures Manualrequires that townships have financial internal controls.

The two separate offices (clerk and treasurer) involved in township financial transactions provides a level of internal control.

5

6

APM

Department of Treasury Accounting Procedures Manual for Local Units of Government

7

Financial Policies

Although the APM provides guidance, financial policies help provide clear direction and good internal controls. They include, but are not limited to: Investment/depository Credit card ACH (Automatic Clearing House) Purchasing Post audit Travel and expense

See the MTA publication Policy Matters for samples of these policies and more.

8

Handling Public Funds

The township board must adopt a depository and investment policy Designates the financial institutions in which the

treasurer may place public money Designates the investment tools the treasurer

may use

9

Handling Public Funds

The treasurer can permit others to accept money on his or her behalf Develop a policy The person receiving the money provides a receipt to

the payer Periodically the money is given to the treasurer using

a transmittal advice The treasurer prepares a receipt The treasurer deposits the funds

10

Uniform Accounting and Procedures Manual Sample11

Bank Accounts

All cash and investments are under the control of the treasurer No additional approval required to open accounts or

move money Deposits must be made intact – cash and checks

received correspond to numerically sequenced receipt group (no dime store receipt books)

Deposits must be made timely Bank accounts ending date should be the end of

the month A timing issue for financial reports to the township

board

12

Financial Reports

The local unit's legislative body must be provided periodic financial reports from the treasurer and the clerk. Required Detailed financial report Investment report

Best practice Balance sheet Cash activity by fund

Required Financial ReportsFrom the Accounting Procedures Manual

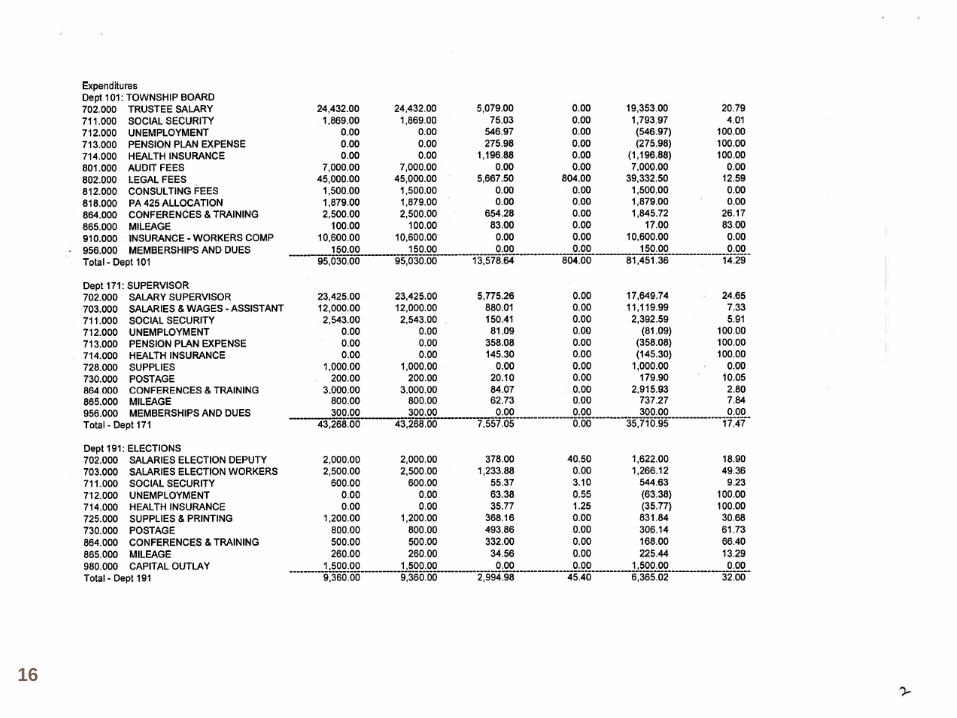

Detailed financial report including:• Account number• Description• Amended budget• Current period• Year to date• Budget balance

• Provided monthly by the clerk• Information comes from the general ledger

14

Revenues and Expenditures

15

16

Investment report including: Name of the financial institution Type of investment Anticipated yield Date of maturity Provided quarterly by the treasurer

Required Financial ReportsFrom the Accounting Procedures Manual

17

18

Financial ReportsBest Practice

Balance sheet Each fund Provided monthly by the clerk Information comes from the general ledger

19

Fund Balance Definition

The net worth of a fund, measured by total assets minus total liabilities

20

Financial Reports Best Practice

Cash activity Summary of cash activity by:

Fund Bank account CD Investment account

Provided monthly by the treasurer

21

Reconciliation of Accounts

Cash balances of the various bank accounts shall be reconciled to the bank statements monthly The treasurer keeps track of total cash and

investments for each bank account and reconciles to the monthly statements from the bank

The treasurer provides a listing of all cash and investments along with a copy of the bank statements to the clerk each month

The clerk reconciles the cash and investments recorded in the general ledger to the bank statements

How does this really work?

23

Check Writing/Accounts Payable Township bank accounts

All bank accounts must be in the name of the local governmental unit and the local unit treasurer. Use of the local unit’s tax ID number should be strictly

controlled by the treasurer

Signing checks There is a difference between what statute

requires and what a bank may require Statute = clerk and treasurer Bank = treasurer

24

Check Writing/Accounts Payable Procedure - clerk

Clerk receives the bill Clerk prepares the accounts payable list The township board approves the accounts

payables The clerk prepares the warrant/voucher The clerk signs the warrant/voucher, attaches to

the original invoice and gives to treasurer

25

26

27

Check Writing/Accounts Payable Procedure - treasurer

The treasurer compares the warrant to the invoice, checking for accuracy

The treasurer makes certain there is enough money in the account to cover the checks

The treasurer signs the warrant (it now is a check and is negotiable)

The treasurer mails the payment to the vendor The check should never go back to the originator

(clerk)

28

Check Writing/Accounts Payable Who keeps copies of the invoices and checks?

Clerk? Treasurer? A central location?

29

ACH Payments

Automated Clearing House Before making ACH payments the township

board must adopt: an authorizing resolution and, a policy for ACH payments

30

ACH Policy

Treasurer Presents an ACH policy to the township board for

approval Prepares a list of vendors Following board approval of the expenditure-signs

the ACH warrant and initiates the electronic transaction

Retains ACH documents for audit purposes

31

ACH Policy

Clerk Signs the ACH invoice (an invoice from a list of

approved ACH vendors) Submits to the township board the ACH invoice

which is equivalent to a warrant Retains the ACH invoice for audit purposes

32

Tax Collection

Dual signatures are not required for the tax collection checking account.

Best practice may be that there is a second signature

33

Tax Collection

Internal control Treasurer provides the amount of the total tax

levy to the clerk The treasurer reports deposits and distribution

amounts (copies of checks) to the clerk, which the clerk records in the townships accounting system

The treasurer reports to the clerk the amount of tax returned delinquent

34

Tax Collection

Reporting sample Total levy $1,000,000 Total receipts $859,000 Total checks written $859,000 Total returned delinquent $141,000 Total checks written plus total delinquent equals

total levy $859,000 + $141,000 = $1,000,000

35

Billing/Accounts Receivable

Whose statutory responsibility is billing? No ones! Examples of accounts receivable with no elected

officer having statutory responsibility Cost recovery fees (e.g. fire run cost recovery

ordinance)Water/sewer use charges Recreation fees

36

Billing/Accounts Receivable

Exception – Special assessments

MCL 41.729 The township clerk shall thereupon deliver to the township treasurer such special assessment roll, to which he shall attach his warrant commanding the township treasurer to collect the assessments therein in accordance with the directions of the township board in respect thereto.

Tax collections MCL 211.44 Upon receipt of the tax roll, the township

treasurer or other collector shall proceed to collect the taxes.

37

Billing/Accounts Receivable

The township should create a policy Who is responsible for invoicing (cannot require

an elected official to do) The township should create a billing procedure

indicating: the frequency of the billing, the form and content of the bill and, the distribution of the bill (who gets copies)

38

Billing/Accounts Receivable

Internal control/segregation of duties for the billing procedure requires consideration of: who does the invoicing, who does the receipting, who applies the payment to the customer account

and, who makes non-cash adjustments to the

customers account.

39

Clerk in Review

Who is responsible for what? ClerkGeneral ledger for all funds Disbursements journal for all funds Reconciles accounts with the treasurer Records tax receipts and disbursements Prepares and signs the warrants for payment of bills

40

Treasurer in Review

Who is responsible for what? Treasurer Receipts township revenue Collects property taxes Reports tax collections and disbursements to clerkMaintains township bank accounts Invests surplus township funds Reconciles accounts with the clerk Signs the warrants and sends out payment

41

Record Keeping

Retention Schedules General Schedule #25 - Township Clerk Records General Schedule #29 - Township Treasurer

Records Local Government Financial Records (approved

4-7-2009)

42

Like Jim says…..

When we work together, two heads are better than one no matter how dumb they are.

43