Slide 1 Click to edit Master title style Click to edit Master text styles Second level ― Third level • Fourth level Midwest Fractionation Overview Platts NGLs Conference| September 24, 2013 President & CEO Bill McAdam

Transcript

Slide 1

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Midwest Fractionation Overview Platts NGLs Conference| September 24, 2013

President & CEO

Bill McAdam

Slide 2

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 2

Outline

1. Basics of Gathering, Processing, Fractionation, Storage

2. Overview of North American NGL Supply/Demand

3. What drove building of Midwest fractionation facilities?

4. What will drive expansion of Midwest fractionation?

5. Summary

Slide 3

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 3

Natural Gas and NGL Value Chain

Slide 4

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 4

Key Drivers to locate/build Facilities

1. Location of Raw Gas Production

2. Access to “salt” underground storage

3. Quality/Quantity of the Raw Gas

4. Natural Gas specs to transport processed Gas

5. Proximity to NGL mix takeaway systems

Truck, Rail, Pipeline

6. Proximity to NGL spec product customers

Fractionation primarily built close to end-user demand

Producers are faced with three primary decisions with regards to how best

to handle their Raw (NGL rich) Gas:

1. Extract NGL Mix in field and transport to Fractionate in selected Market.

2. Extract NGLs, Fractionate in the field and distribute to local Markets.

3. Transport NGL rich gas to Market, Extract/Fractionate in this Market.

Slide 5

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 5

Typical NGL Schematic

Slide 6

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 6

C2 C3 C4s C5+ Total

Supply (mmbpd) Gas Plants 1.2 0.8 0.5 0.4 2.9

Refineries - 0.6 0.1 0.0 0.7

Total Supply 1.2 1.4 0.6 0.4 3.6

Demand (mmbpd) Chemical feedstock 1.2 0.6 0.2 - 2.0

Heating/Commercial/Ind’l - 0.7 - - 0.7

Refinery (Gasoline Blending) - - 0.3 0.1 0.4

Heavy Oil Diluent - - - 0.2 0.2

Other, Net Exports - 0.1 0.1 0.1 0.3

Total Demand 1.2 1.4 0.6 0.4 3.6

Source: EIA, NEB, Petral, IHS

North American NGL Supply/Demand Snapshot: 2012

Slide 7

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 7

Alliance Pipeline

Aux Sable

Rich Gas Shales will be Developed and

Add to NGL Supply

Slide 8

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 8

C2 C3 C4s C5+

Supply Direction

Gas Plants UP UP UP UP

Refineries - flat- flat- flat-

Demand Direction

Petrochemical Feedstock UP balance up up?

Heating/Commercial/Ind’l - flat/down - -

Refinery (Gasoline Blending) - - down down

Heavy Oil Diluent - - up UP

Dehydro (PDH/BDH), MTBE - UP ? -

Net Exports - UP up -

Key Trends

1. NGL production up from Gas Plants (“oily” gas focus in shales)

2. Ethane balanced by increased Petchem feedstock demand

3. Propane balanced by increased exports, PDH

4. Butanes balanced by increased exports, MTBE

North American NGL Supply/Demand Trends

2013 - 2020

Slide 9

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 9

Mont Belvieu

Conway

Sarnia (2.6 B lbs/Yr)

Fort

Saskatchewan

(2.6 B lbs/Yr)

Chicago

ENTERPRISE

ONEOK

COCHIN

ENBRIDGE

ALLIANCE

PTC Empress

Salt Storage

ENTERPRISE

Cochrane

AEGS

North American Ethylene Plants

Extraction Facilities

Ethylene Plant

Joffre (6.0 B lbs/Yr)

USGC (55 B lbs/Yr)

Clinton (1.1 B lbs/Yr)

Morris (1.3 B

lbs/Yr)

Calvert City (0.4 B lbs/yr)

Slide 10

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 10

North American NGL Infrastructure…in transition

Slide 11

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 11

Key Midwest Areas

Conventional (historic):

Conway area (Conway/Bushton/Hutchinson/Medford)

Edmonton/Fort Saskatchewan

Sarnia

Channahon

New Areas driven by Shale Plays:

Bakken (ND) other

Marcellus/Utica (PA/OH/WV)

Montney/Duvernay (AB/BC)

Slide 12

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 12

Conway Area

Location of Supply: KS, CO, WY, UT, ND

Supply Logistics: Primarily gathering pipelines from field

extraction plants NGL mix (C2+)

Local Markets: Refiners

Regional Markets: a. C2 Crackers in IA, IL

b. Refiners in IL, IN

c. Propane markets in WI, IL, IN, MI

d. EP, NGL product markets in USGC (MB)

Facilities: no adjacent Extraction Capacity

515 kbd Fractionation Capacity (+)

5 kbd Isomerization Capacity

Storage: ~50 mmbbls

Slide 13

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 13

Conway Area

Slide 14

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 14

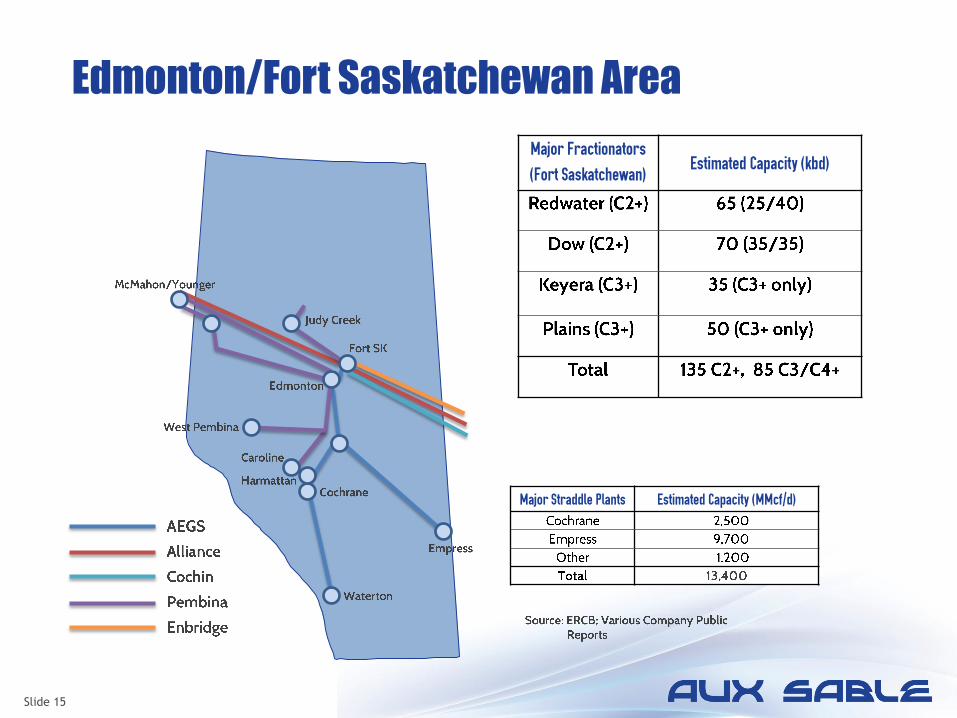

Edmonton/Fort Saskatchewan Area

Location of Supply: AB, BC

Transport Source: Pipelines NGL mix (C2+, C3+) via Pembina,

Plains, Keyera

Local Markets: Refiners in Edmonton, Petchems in

FSK/Joffre,

Regional Markets: Refiners (SK, MT)

Propane markets in AB, BC, SK, US upper

Midwest

Heavy oil blending

Facilities: 275 kbd Fractionation Capacity (+)

Storage: ~40 mmbbls

Slide 15

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 15

Edmonton/Fort Saskatchewan Area

Major Straddle Plants Estimated Capacity (MMcf/d)

Major Fractionators

(Fort Saskatchewan) Estimated Capacity (kbd)

Slide 16

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 16

Sarnia Area

Location of Supply: AB, BC

Transport Source: Pipeline NGL mix (C3+) via Enbridge

(note: Cochin is essentially zero)

Local Markets: Refiners, Petchems in Sarnia

Regional Markets: a. Refiners in Ontario

b. Propane markets in ON, PQ, MI, US NE

Facilities: 150 kbd Fractionation Capacity (flat)

Storage: ~25 mmbbls

Slide 17

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 17

Sarnia Area

Slide 18

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 18

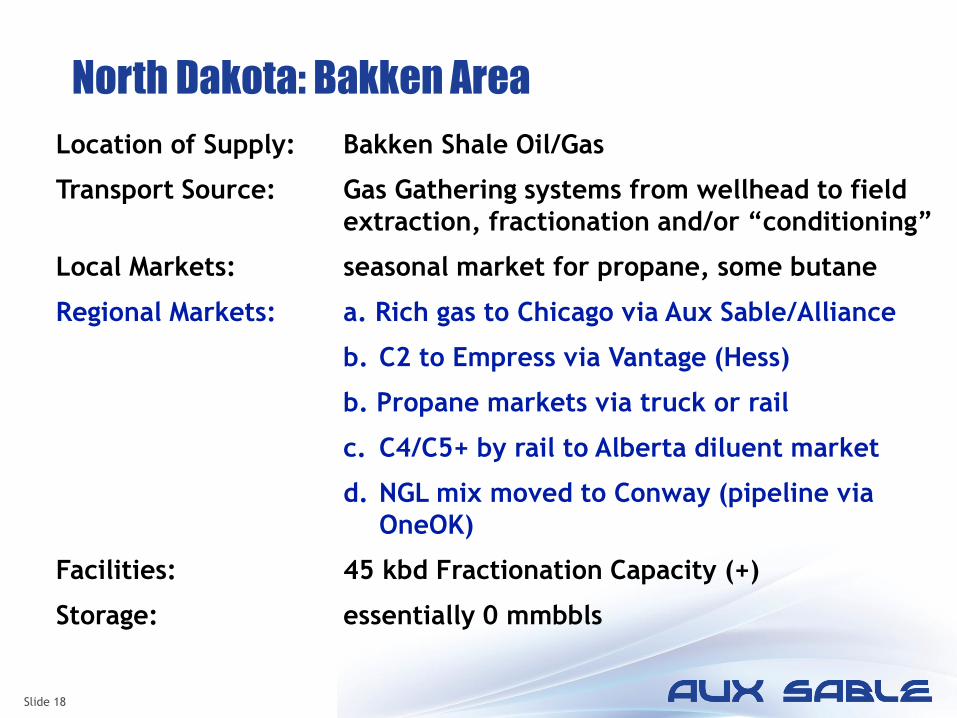

North Dakota: Bakken Area

Location of Supply: Bakken Shale Oil/Gas

Transport Source: Gas Gathering systems from wellhead to field

extraction, fractionation and/or “conditioning”

Local Markets: seasonal market for propane, some butane

Regional Markets: a. Rich gas to Chicago via Aux Sable/Alliance

b. C2 to Empress via Vantage (Hess)

b. Propane markets via truck or rail

c. C4/C5+ by rail to Alberta diluent market

d. NGL mix moved to Conway (pipeline via

OneOK)

Facilities: 45 kbd Fractionation Capacity (+)

Storage: essentially 0 mmbbls

Slide 19

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 19

North Dakota: Bakken Area

Palermo Conditioning Plant Prairie Rose Pipeline

Alliance Pipeline

Conditioning Plant

Slide 20

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 20

Marcellus/Utica Area

Location of Supply: Marcellus/Utica Shale gas

Transport Source: Gas gathering, local extraction and

fractionation (focused on C3 and C4+)

Local Markets: PA, OH, WV propane markets, Refiners

Regional Markets: a. Pipeline C2 to Sarnia via Mariner West

b. Pipeline C2/EP to USGC (being developed)

c. Pipeline C2+ to USGC (being developed)

Facilities: 100 kbd Fractionation Capacity (+++)

Storage: ~ 3 mmbbls (C3/C4 underground)

Slide 21

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 21

Marcellus/Utica Area

Slide 22

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 22

Chicago Area

Location of Supply: AB, BC, ND

Transport Source: High pressure rich gas via Alliance Pipeline

Local Markets: Chicago Refiners (iC4 for Alkylation, nC4 for

winter gasoline), Lyondell Morris (C2),

Regional Markets: a. Lyondell Clinton (C2)

b. Propane markets IL,WI,IN,MI,OH,PADD IA&B

c. Diluent Market in Alberta (C5+)

Facilities: 102 kbd Fractionation Capacity (+)

10 kbd Isomerization Capacity

Storage: 0.5 mmbbls

Slide 23

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 23

Chicago Area

Aux Sable NGL Extraction

and Fractionation Facilities

Alliance Pipeline

Slide 24

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 24

Aux Sable Operations

Slide 25

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 25

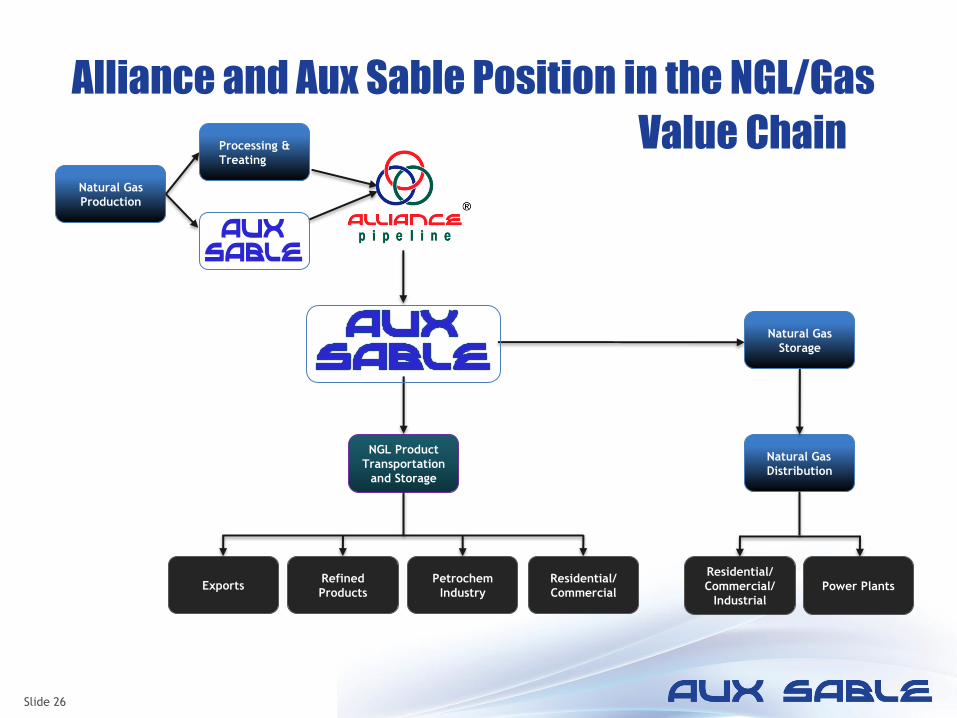

Alliance Pipeline and Aux Sable

Alliance

Owns and operates a 450 mile gathering system in NE BC and NW Alberta with 52 receipt points starting at Highway, BC

Owns and operates a 1850 mile, 1.6 bcf/d, high pressure, rich gas transportation pipeline to Chicago, IL with 7 primary delivery points (Nicor, NGPL,, Integrys, MW, Vector, ANR, ASLP)

Two receipt points in ND (Bantry (operating) and Tioga (under construction))

Aux Sable

Owns Septimus Gas Plants (60 mmcfd) & Septimus Pipeline (operated by Crew)

Owns and operates the Palermo Conditioning Plant (80 mmcfd) and the Prairie Rose Pipeline (110 mmcfd) in ND

Owns and operates a 2.1 bcf/d world scale extraction/fractionation plant at terminus of Alliance (Channahon, IL)

Developed NGL access to end-use markets in US north-east, US mid-west and USGC via pipelines, rail and truck

Developed capability to offload NGL mixes via railcar from shale plays

“Gathering and Processing System”

Slide 26

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 26

Alliance and Aux Sable Position in the NGL/Gas

Natural Gas

Production

Processing &

Treating

NGL Product

Transportation

and Storage

Refined

Products

Petrochem

Industry

Residential/

Commercial

Natural Gas

Storage

Residential/

Commercial/

Industrial

Power Plants

Natural Gas

Distribution

Exports

Value Chain

Slide 27

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 27

Aux Sable Midstream Operations

Slide 28

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 28

Gathering Systems Connected to ASM’s Palermo

Conditioning Plant

Slide 29

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 29

Aux Sable Canada Operations

Slide 30

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 30

Simplified Process Flow Diagram

Slide 31

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 31

Aux Sable’s Channahon NGL Facility

Slide 32

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 32

What drove building of current Midwest

fractionation facilities?

1. Location of raw gas production

2. Proximity to salt storage

3. Local/regional need for one or more spec products

C2 in Alberta (Joffre/FSK), C2/EP for Equistar, C2 in Sarnia for

NovaChem/EssoChem

seasonal propane markets in populated areas

iC4 for Alkylation, nC4 for gasoline blending

4. Aggregate NGL mix via pipelines to obtain scale for fractionation facilities

5. “Straddle” gas to extract NGLs at high gas volume points

(Empress/Cochrane)

C2 to Joffre and C3+ mix moved to fractionation locations (FSK or Sarnia)

6. Aux Sable-Alliance rich gas system minimizes field extraction in production

region, reduces effective cost of gas transport and centralizes

extraction/fractionation in a demand location (Chicago)

Slide 33

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 33

Midwest Fractionation Capacity by Location

Fractionation

Location 2004 2012

Conway area 400 515

Edmonton/FSK 225 275

Sarnia 150 150

Channahon 85 102

Marcellus/Utica N/A 100

North Dakota 30 45

Total ~900 kbd ~1200 kbd

Source: PIRA, IHS, Various Company

All values shown in kbd.

Slide 34

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 34

What will drive expansion of Midwest

fractionation facilities?

1. Location of raw gas production

rich shale gas production has been the prime driver since 2005/2006 and will

continue to drive facility needs in the future

2. Local/regional need for one or more spec products

Up to the saturation point

Need to address seasonal demand versus ratable supply without access to cost

effective storage

Provide feedstock for “Midwest” petchems that want to expand on C2 feedstock

Isomerization facilities (new or expanded) may be harder to justify in face of flat

demand from refiners and increasing iC4 in raw gas production

3. Conversion of existing pipeline infrastructure to move NGL mix to USGC

fractionators will result when local markets are saturated

4. Leverage Aux Sable-Alliance rich gas system to minimize new field

extraction in production region, reduce cost of gas transport and

economically expand fractionation in Chicago

Slide 35

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 35

Midwest Fractionation Capacity by Location

Fractionation

Location 2004 2012

Estimated

Future Capacity

Conway area 400 515 575

Edmonton/FSK 225 275 325

Sarnia 150 150 150

Channahon 85 102 140

Marcellus/Utica N/A 100 475

North Dakota 30 45 60

Total ~900 kbd ~1200 kbd ~1,700 kbd

Source: PIRA, IHS, Various Company

All values shown in kbd.

Slide 36

Click to edit Master title style

Click to edit Master text styles

Second level

― Third level

• Fourth level

Slide 36

Summary

Midwest Fractionation facilities will be expanded by about 500 kbd,

driven by growth in end-user needs

Ethane demand to support petchem growth at existing or new sites

Overall Propane demand projected to be flat/declining in Midwest. Backing out

supply delivered into PADD 1A and 1B will continue.

Refinery demands for iC4/nC4 projected to be flat or perhaps decline with lower

overall demand and requirement to blend ethanol

C5+ demand for diluent in Alberta is growing

Midwest demand for spec NGLs is becoming saturated

Focus is now turning on delivering y-Grade to USGC facilities versus further

expanding facilities currently under construction

Industry now looking to access international markets for C3/C4s

Expansion of ethane petchem industry will grow modestly in the Midwest with