1 Climate change-related corporate governance information: an explanation of the difference between the supply of and demand for such information by: Shamima Haque, Craig Deegan and Robert Inglis School of Accounting, RMIT University, GPO Box 2476V, Melbourne, Victoria, Australia, 3001 [email protected][email protected][email protected]Abstract This study investigates the gap between the climate change-related corporate governance information being disclosed by companies, and the information sought by stakeholders. To accomplish this objective we utilised previous research on stakeholder demand for information, and we conducted in-depth interviews with six corporate representatives from major Australian emission-intensive companies. Having gained and documented a rich insight into the potential factors responsible for the current gap in disclosure we find that the existence of an expectations gap; the perceived cost of providing commercially sensitive information; the limited accountability being accepted by the corporate managers; and, a lack of stakeholder pressure together contribute to the lack of disclosure. In highlighting the gap in disclosure, this study suggests strategies to reduce the gap in climate change-related corporate governance disclosures. Keywords: Climate change; corporate governance; climate change-related disclosure; expectations gap, cost-benefit, accountability, stakeholder power.

Transcript

1

Climate change-related corporate governance information: an explanation of the difference between

the supply of and demand for such information

by:

Shamima Haque, Craig Deegan and Robert Inglis

School of Accounting, RMIT University, GPO Box 2476V, Melbourne, Victoria, Australia, 3001

Abstract This study investigates the gap between the climate change-related corporate governance information being disclosed by companies, and the information sought by stakeholders. To accomplish this objective we utilised previous research on stakeholder demand for information, and we conducted in-depth interviews with six corporate representatives from major Australian emission-intensive companies. Having gained and documented a rich insight into the potential factors responsible for the current gap in disclosure we find that the existence of an expectations gap; the perceived cost of providing commercially sensitive information; the limited accountability being accepted by the corporate managers; and, a lack of stakeholder pressure together contribute to the lack of disclosure. In highlighting the gap in disclosure, this study suggests strategies to reduce the gap in climate change-related corporate governance disclosures. Keywords: Climate change; corporate governance; climate change-related disclosure; expectations gap, cost-benefit, accountability, stakeholder power.

2

Climate change-related corporate governance information: an explanation of the difference between

the supply of and demand for such information Abstract This study investigates the gap between the climate change-related corporate governance information being disclosed by companies, and the information sought by stakeholders. To accomplish this objective we utilised previous research on stakeholder demand for information, and we conducted in-depth interviews with six corporate representatives from major Australian emission-intensive companies. Having gained and documented a rich insight into the potential factors responsible for the current gap in disclosure we find that the existence of an expectations gap; the perceived cost of providing commercially sensitive information; the limited accountability being accepted by the corporate managers; and, a lack of stakeholder pressure together contribute to the lack of disclosure. In highlighting the gap in disclosure, this study suggests strategies to reduce the gap in climate change-related corporate governance disclosures. Keywords: Climate change; corporate governance; climate change-related disclosure; expectations gap, cost-benefit, accountability, stakeholder power. 1. Introduction This paper is a part of a broader study consisting of three parts. The first part investigated the climate change-related corporate governance disclosure practices of five major Australian energy-intensive companies over a 16 years period (Haque and Deegan, 2010). In doing so, the paper developed a disclosure index consisting of 25 specific climate change-related corporate governance issues under eight general categories. The index was developed on the basis of six expert guides provided by various research organisations and non-governmental organisations (NGOs) in respect of what elements should be included within a corporate governance system that properly addresses climate change. The paper argued that reports that provide information about the existence, or non-existence, of most of the 25 governance practices would provide useful (high quality) insights to report users whereas reports that provide little information would not be useful in assessing the companies’ response to climate change risks and opportunities. Looking at the disclosure levels the study concluded that although there was an increasing disclosure trend over the years, there was minimal reporting by major Australian companies in relation to climate change-related corporate governance practices. The results from the first part of the study (Haque and Deegan, 2010 as described above) lead to the following question: is this lack of climate change-related corporate governance disclosure a matter of concern? If nobody actually sought or used information about a company’s climate change-related corporate governance practices, then perhaps not (although from a sustainability perspective we might be concerned that people did not demand such information). With this issue in mind Haque, Deegan and Inglis (2010) investigated whether various groups in society demand climate change-related corporate governance information. They investigated

3

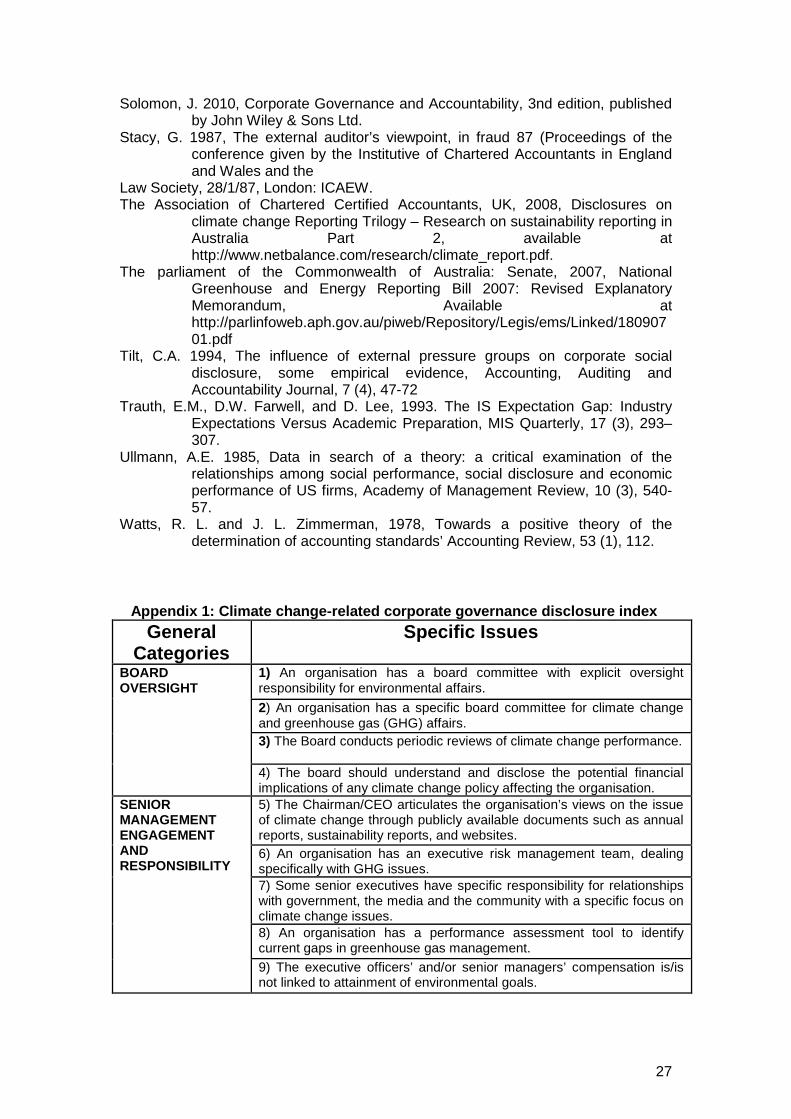

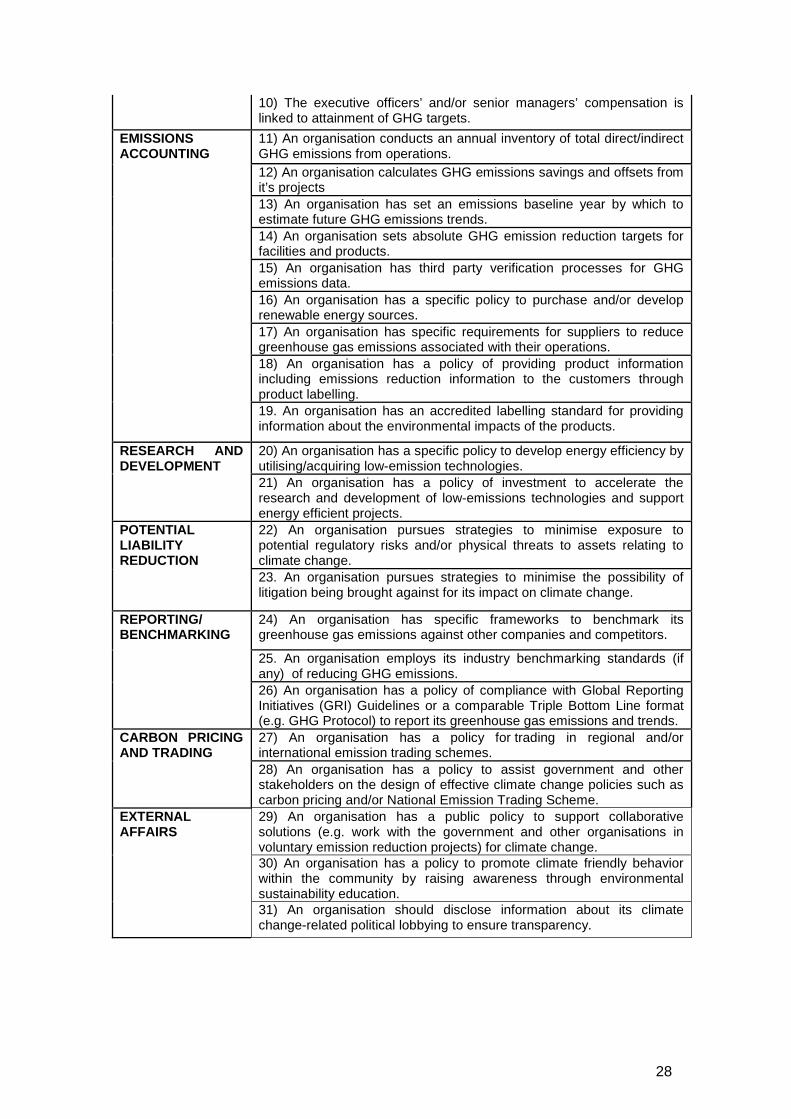

what types of information different groups of stakeholders believe that companies should disclose in relation to climate change-related corporate governance practices. Based on an online survey instrument the study asked a group of experts within different stakeholder groups (including institutional investors, government bodies, environmental NGOs, environmental consultancies, researchers, and accounting professionals) to rank the 25 specific climate change-related corporate governance disclosure issues developed in the previous research by Haque and Deegan (2010) in terms of their importance in assessing a company’s performance and risk exposure with respect to climate change. The results of their study highlighted that the expert respondents unanimously considered the issues in the index, developed in phase one of the research (that is, in Haque and Deegan, 2010), to be at least ‘important’ in assessing organisations’ climate change-related corporate governance practises. The study also found six additional issues recommended by the respondents leading to a final index of 31 disclosure issues under eight general categories. Thus the second part of the study effectively utilised the disclosure index developed in phase one to build a ‘best practice disclosure index’ by using experts’ opinions. Appendix 1 presents the climate change-related corporate governance disclosure index developed by Haque, Deegan & Inglis (2010). The corporate governance disclosure index identified various items of information that stakeholders believe important in assessing the risks of an organisation in relation to climate change. The basis of the disclosures is that in assessing the future risks and opportunities that climate change poses to an organisation it is necessary to know the governance policies that have been put in place to address climate change. Taken together, the results of the previous two phases of the research project indicate that there appears to be differences between what companies are disclosing (supply) and what different groups of stakeholders are expecting companies to disclose (demand) in relation to climate change-related corporate governance practices. The experts within different stakeholder groups identified 31 specific climate change-related information items as important and expected companies to disclose such information (Haque, Deegan & Inglis, 2010). But the current climate change-related corporate governance disclosure practices suggest that current disclosure practices fail to meet the information needs of the stakeholders (Haque and Deegan, 2010). Other recent studies on companies’ climate change-related disclosure practices have also suggested that the current disclosure practice is typically deficient and not of a standard to satisfy the information needs of various stakeholder groups (Calvert and CERES, 2007; Carbon Disclosure Project, 2007; Friends of the Earth, 2006; GRI and KPMG, 2007; Kolk, Levy and Pinkse, 2008; The Association of Chartered Certified Accountants, UK, 2008). With this low level of disclosures, it would be very difficult for stakeholders to make an assessment of the potential climate change-related risks1 companies are facing (Haque and Deegan, 2010). The question examined in this current paper is why is there an apparent difference between the climate change-related corporate governance information provided by the companies and the information expected by the stakeholders? By interviewing senior executives of some Australian companies, this paper investigates the reasons for the difference between the climate change-related corporate governance

1 Included within these risks were regulatory risks (e.g. regulation aimed at emissions trading; emissions reductions and increased energy efficiency; regulatory uncertainty and duplication; increased costs and growing compliance costs; mandatory greenhouse and energy reporting), physical risks (e.g. extreme weather events; rising sea levels and water shortages; infrastructure damage and associated costs; availability of water and other resources; increased insurance costs; business disruptions either directly or via the supply chain), and other risks (e.g. change in consumer attitudes and demand; damage to reputation; difficulty in attaining investment) (Labatt and White, 2007; Carbon Disclosure Project, 2008) .

4

information provided by the companies and the information that is sought by the stakeholders. This paper will progress as follows. In the next section we will consider the potential reasons for the low level of corporate disclosure (which in itself falls short of what stakeholders demand). In explaining why disclosures seem to be lower than stakeholders desire reference will be made to the notion of an expectations gap, the costs and benefits associated with reporting, the notion of accountability, and the concept of stakeholder power as outlined in social and environmental accounting literature. The paper will then describe the research methods employed before presenting the results of the study. The paper concludes by providing a discussion of the implications of the research. 2. Possible explanations for the difference between the climate change-related corporate governance information provided by the companies and the information sought by stakeholders Comparing the previous two studies (Haque and Deegan, 2010 and Haque, Deegan & Inglis, 2010) we identified a gap between the supply of, and demand for, information with respect to climate change-related corporate governance practices. In this section we discuss the possible reasons for such a gap. While not all-inclusive, this will serve as a starting point for explaining the reasons for the low level of corporate disclosure relative to stakeholder demands. 2.1 The notion of expectations gap Research into the existence of an expectations gap began in 1970s. Liggio (1974) first defined an expectations gap as ‘a factor of levels of expected performance as envisioned both by the independent accountant and by the user of financial statements’ (p. 27). Deegan and Rankin (1999) used the term ‘expectations gap’ to explain ‘the situation whereby a difference in expectations exists between a group with a certain expertise, and a group which relies upon that expertise’ (p. 316). Apart from the accounting literature, the notion of an expectations gap has also been used in other research areas, such as to explore the perceptions of the information systems industry in relation to the academic preparation of graduates (Trauth et al, 1993), difference in expectations of advertising agencies and their clients in relation to campaign values (Murphy and Maynard, 1996), and variation in performance standards across demographic groups due to different proficiency standards (Reed, 2009). Extant research in accounting literature regarding expectations gap falls into two categories: one being the audit expectations gap and the other being an expectations gap relating to financial statements (Higson, 2003). The audit expectations gap literature has investigated differing perceptions between auditors’ understanding of their function, and public expectations of the audit process (Porter, 1991; Humphrey et al, 1993; Monroe and Woodliff, 1993; Epstein and Geiger, 1994; Koh and Woo, 2001; Dewing and Russell, 2002; Adams and Evans, 2004). Research concerning the existence of an audit expectations gap can be classified into three categories: differences in perceptions between auditors and financial statement users regarding what auditors’ should do (Lowe and Pany, 1993; Monroe and Woodliff, 1993; Porter, 1993; Epstein and Geiger, 1994); differences in perceptions between auditors and financial statement users regarding what auditors’ are able to accomplish (Libby,

5

1979; Bailey, 1981; Nair and Rittenberg, 1987; Porter, 1993); and differences in the actual knowledge levels of both auditors and financial statement users regarding the audit situation (Hatherly et al, 1991; Porter, 1993). The objectives of these studies was to set out in more detail the auditors’ work and responsibilities, and thus help tackle the audit expectations gap (Higson, 2003). Previous studies investigating the expectations gap relating to financial statements described the difference between the expectations of users and preparers of financial reports (AAA, 1990; Accountancy, 1993: 1; ASCPA and ICAA, 1994; Deegan and Rankin, 1999; the Financial Reporting Commission, 1992: 53; Liggio, 1974; Stacy, 1987: 94; Independent Audit Limited, 2006). For example, ASCPA and ICAA (1994) considered the term expectations gap to describe the difference between the expectations of financial report users and the accounting profession with respect to the perceived quality of financial reporting and auditing services. Another report provided by Independent Audit Limited and the ACCA found that there is a substantial expectations gap between the financial information provided by companies and the information sought by users and interested parties (Independent Audit Limited, 2006). However, compared to the recognition given to the financial statement expectations gap, the possibility of a non-financial statements expectations gap has almost been ignored. A notable exception was the research undertaken by Deegan and Rankin (1999) who found the existence of an expectations gap between the users and preparers of annual reports in relation to corporate environmental information. They observed that an expectation gap existed between the users and preparers of annual reports where users perceived environmental information to be more important relative to the preparers’ perspective of its importance to report users’ decision making processes. Deegan and Rankin (1999) argued that an expectations gap is considered to exist when there is a difference between the expectations users have in relation to corporate environmental information and the expectations preparers believe users have in regard to that information. Consistent with the notion of an expectations gap, and for the purposes of the focus of this paper, there may be a gap between the expectations stakeholders have with regard to the importance of climate change-related corporate governance information and the expectations companies believe stakeholders have in relation to that information. Although stakeholders identified a growing demand for climate change-related corporate governance disclosures, corporate managers might be unaware of the demand. Thus, perhaps it is not clear to preparers what is expected by the stakeholders in relation to climate change-related corporate governance information. The existence of an expectations gap might explain, at least in part, why the demand for climate change-related corporate governance information is not currently being satisfied. 2.2 Cost-benefit analysis In the absence of any regulatory requirements in relation to climate change-related corporate governance disclosure practices it is important to understand the managerial motivations for reporting or hiding information. Deegan and Rankin (1999) argued that an important consideration in the companies’ ‘decision to disclose environmental information within the annual report is the cost of gathering and presenting such information, when compared to the perceived benefits of doing so’ (p. 320). Corporate environmental information tends to be provided free of charge to

6

the users of such information, with companies bearing the full cost of disclosure (Solomon, 2000; Solomon, 2010). The insights from previous studies on cost-benefit analysis indicated that information costs influence the levels of corporate disclosure (Chandra and Greenball, 1977; Gray and Roberts, 1989; Entwistle, 1997). Gray et al (1990, p. 617) found that voluntary disclosures depend largely upon the ‘outcome of an assessment of the economic consequences of the proposed’ disclosure items. Adams (2002) argued that companies’ perceptions about the benefits of reporting influence the extent and nature of corporate social reporting. Thus, the decision to provide information to the users would depend on determining the costs and benefits associated with such reporting. There is currently no nationally consistent approach or regulatory requirement for reporting of climate change-related corporate governance information in Australia. Higher levels of climate change-related data integrity and accuracy increase the reporting costs for individual entities (Department of Climate Change, 2009). There might be also a commercial impact of potential energy consumption and production which suggests a cost associated with disclosure of energy emissions that subsequently leads to commercial disadvantage (EPA Victoria, 2006). A high level of data accuracy is also required. Other costs could include the possibility that various stakeholders will use information provided by the company to take actions, including legal actions, against the company due to the perceived shortcomings in its environmental performance (Deegan and Rankin, 1999). There might also be some potential reputation cost from negative press such as costs associated with countering any negative publicity as a result of disclosure (EPA Victoria, 2006). The benefits to business of disclosing climate change-related information may include an improvement in the management of the organisation’s processes, and GREATER regulatory certainty (Deegan and Rankin, 1999; EPA Victoria, 2006). In addition, providing information helps to build credibility and trust within the community, along with increased investor support for the companies i.e. boosting ‘good reputation’ among investors ((EPA Victoria, 2006; Solomon, 2010). Comparing the perceived costs and benefits associated with reporting is an important exercise for company managers. Therefore, deciding not to disclose particular information might be deemed better for the value of the company. In our current research context, perhaps cost-benefit assessments associated with reporting determines companies’ decisions about what climate change-related corporate governance information should be disclosed, or not disclosed. 2.3 The notion of Accountability The cost-benefit rationale discussed in the previous section has come from the positive accounting theory perspective (Watts and Zimmerman, 1978; Cormier and Magnan, 1999; Hope, 2003) where managers are portrayed as rational actors who calculate the net benefits of voluntary disclosure in order to decide whether to report or not. This idea of assessing costs and benefits of disclosure is counter to the notion of accountability which emphasises ‘the duty to provide an account or reckoning of those actions for which one is held responsible’ (Gray, Owen, and Adams, 1996, p. 38). Gray, Owen and Maunders (1991) applied the notion of accountability to corporate social reporting and argue that the role of corporate social reporting is to inform society about the extent to which the organisation meets the responsibilities imposed upon it. The notion of accountability explains that provision of voluntary

7

reporting has net benefits in that stakeholders’ information needs are met and accountability requirements are discharged. Corporate social reporting is therefore, assumed to be responsibility-driven rather than demand or survival-driven which implies that people in society have a right to be informed about certain aspects of an organisation’s operations (Deegan, 2009). Deegan (2009) suggests that the rights to information grounded in an accountability perspective as outlined by Gray et al. (1991; 1996) is consistent with the normative branch of stakeholder theory2. Based on ethical principles, normative stakeholder theory focuses on how managers should act. This approach provides the moral basis for stakeholder theory by stating, “Do (Don’t do) this because it is the right (wrong) thing to do” (Donaldson and Preston, 1995, p.72). Normative stakeholder theory investigates whether managers should meet the demands of the stakeholders other than shareholders and, if so, on what grounds these various stakeholders have justifiable claims over the firm (Margolis and Walsh, 2003). It attempts to lay the ethical foundation for the suggestion that an organisation has an obligation to recognise the demands of all appropriate stakeholders. Given that management is ultimately responsible for their companies’ contribution to global climate change, and therefore implicitly accountable for implementing climate change-related corporate governance practices, the accountability perspective would argue that companies should account for their actions or inactions in some form of report provided to the stakeholders. However, the current climate change-related corporate governance reporting practices made by Australian companies offers little evidence to demonstrate such a normative duty towards stakeholders. Therefore, perhaps one reason for the relatively low level of disclosure is that managers consider they have limited accountability in relation to the governance policies they have in place to address climate change. 2.4 Stakeholder power While the normative branch of stakeholder theory (on which the notion of ‘accountability’ is based) emphasises that all stakeholders have the right to be treated fairly by an organisation, it does not consider issues of stakeholder power (Deegan, 2009). A counter view is that organisations will respond to the expectations of those stakeholders with the most power over the organisation (Deegan and Blomquist, 2006; Deegan, 2009). These stakeholder groups control resources necessary to the organisation’s operations and would withdraw support from the organisation if important social responsibilities were unattended (Freeman, 1984; Ulmann, 1985; Deegan and Blomquist, 2006). This notion comes from the managerial branch of stakeholder theory which predicts that management is more likely to focus on meeting the expectations of powerful stakeholders, who have the greatest potential to influence organisations’ ability to generate maximum financial returns. The power of a particular stakeholder to influence corporate management depends on the extent the stakeholder has control over the resources required by the organisation (Ullman, 1985). Mitchell et al (1997) maintain that stakeholders can be identified based on three criteria: power, urgency, and legitimacy. According to their theory, the level of stakeholder salience is determined by how many of the criteria the

2 Deegan (2002) suggests that stakeholder theory has an ethical (normative) and a managerial (positive) branch. While the ethical branch provides theoretical prescriptions about who an organisation’s stakeholder ought to be and how they should be treated, the managerial branch (stakeholder management) is more concerned with managing the stakeholders.

8

stakeholders meet. Should a stakeholder have a legitimate claim on the organisation, but lack power and urgency3, Mitchell et al argue that it would have little salience in the eyes of management. Of the three criteria, a stakeholder’s power to affect the organisation is prioritised. The organisation may affect stakeholders but it will consider the effects of its actions on stakeholders mainly if the stakeholders can in turn influence their operations. Therefore, organisations will respond to those stakeholders who are considered as powerful (Buhr, 2002; Baily et al, 2000). A successful organisation is therefore, considered to be one that satisfies the needs of the various powerful stakeholder groups (Islam and Deegan, 2008). If managers perceive particular stakeholders to be both powerful and to be demanding information about the policies and procedures that the company has in place to address climate change then it would disclose information to conform to such demands. Another related theoretical perspective, overlapping with stakeholder theory, is institutional theory which posits that organisational structures and practices are shaped by pressures from stakeholders who expect to see particular practices in place. According to Scott (1987, p. 498) ‘Organizations conform [to institutional pressures for change] because they are rewarded for doing so through increased legitimacy, resources, and survival capabilities’. Institutional theory has been used to explain why there is often a degree of correspondence between the institutional practices used within different organisations. According to DiMaggio and Powell (1983), the greater the dependence of an organisation on another organisation, the more similar it will become to that organisation in structure, climate, and behavioural focus. Such a process is referred to as coercive isomorphism4. Coercive isomorphism is closely associated with the managerial branch of stakeholder theory (Deegan, 2009). It is more related to the concept of power, as it arises where organisations change their institutional practices because of pressure from those stakeholders upon which organisations are dependent (DiMaggio and Powell, 1983). The company is therefore coerced by its powerful stakeholders into adopting particular voluntary reporting practices. The apparent adoption of such practices is deemed to provide an organisation with a level of legitimacy that would not otherwise be available if it was to deviate from ‘accepted’ organisational forms or policies (DiMaggio and Powell, 1983). From the above discussion it is argued that what is important is the power that a stakeholder has over the organisation and its objectives. How much power the stakeholder can exert will reflect the extent to which the organisation relies on the stakeholder, and the extent the stakeholder can disrupt and cause uncertainty in organisations operations. Meeting the powerful stakeholders’ expectations will help ensure them the scarce and essential resources necessary to the achievement of the objectives. Therefore, how organisations operate and report will be influenced and shaped by the powerful stakeholders’ expectations for particular practices, including disclosure practices (Dowling and Pfeffer, 1975; Gray et al. 1995; Deegan, 2009).

3 Urgency is the extent to which stakeholder efforts call for immediate attention by a firm (Mitchell et al, 1997). 4 The other two categories of isomorphism are normative isomorphism and mimetic isomorphism that provides limited insight to understand the direct pressures of powerful stakeholder groups and how such pressures directly influence organisational practices including disclosure related practices. Further, it is difficult to identify that one form of isomorphism, above the others, is the driver for the adoption of particular organisational structures. As Carpenter and Feroz (2001, p. 573) state, ‘two or more isomorphic pressures may be operating simultaneously making it nearly impossible to determine which form of institutional pressure was more potent in all cases’.

9

However, in our current research context, the disclosure levels of the companies are not consistent with the expectations of the stakeholders in relation to climate change-related corporate governance practices. This suggests that meeting the information needs of the stakeholder groups are not the primary objectives of report preparers. Managers tend to identify relevant stakeholders as being those who are able to exert the most influence over the company’s operations (Owen, Shaw and Cooper, 2005; Deegan and Blomquist, 2006). Therefore, it is argued that the difference between the information provided by the companies and the information sought by the stakeholders is perhaps because stakeholders’ power is not perceived to be great enough to motivate the companies to report (or those with power do not want the information). To sum up this section, we have provided a number of potential reasons why stakeholder demand for information is not being satisfied. These reasons were linked to an expectations gap, the cost-benefit rationale, the notion of accountability, and the concept of stakeholder power. We attempt to consider these potential explanations as far as possible by interviewing corporate managers across a number of companies. The following section describes the research method employed. 3. Research Method The aim of this study is to investigate why there is a difference between the climate change-related corporate governance information provided by the companies and the information expected by the stakeholders. To achieve this objective, this study provides qualitative data from in-depth interviews about the perceptions of corporate managers. Interview questions were open-ended and were primarily derived from the research objective. The discussion in the literature review section above provides possible explanations about why such a difference might exist. It should be noted that these possible reasons were used only as a guide for our interviews to remain flexible so as to allow for other possible factors that might emerge from the interview data. Appendix 2 provides the interview guide for accomplishing the research objective. Interviewee selection Because of the access and time considerations associated with the collection of interview data, the number of companies and participants chosen from each company was limited. We selected participants from the companies identified in the first phase of the broader study which investigated climate change-related corporate governance disclosure practices. These companies were BHP Billiton (manufacturing/mining), Caltex (oil refinery), Origin Energy (oil, Gas, Electricity), Rio Tinto (manufacturing/mining), and Santos Limited (oil and gas). As indicated in the first study, the selection of the companies was based on the criteria that the company would be in an industry that would be likely to be highly exposed to risks and opportunities associated with climate change, and be listed on the Australian Securities Exchange (ASX)5. We also know that these selected companies were shown to provide fairly low levels of disclosure (Haque and Deegan, 2010).

5 In a report by Citigroup researchers claims that among the Australian Stock exchange (ASX) top-100 listed companies those who are most at risk from the impact of climate change are involved in emissions-intensive industries such as Rio Tinto, BHP Billiton, Caltex Limited, Santos Limited and those who will gain from climate change include alternative energy such as Origin Energy (Rolph and Prior, 2006).

10

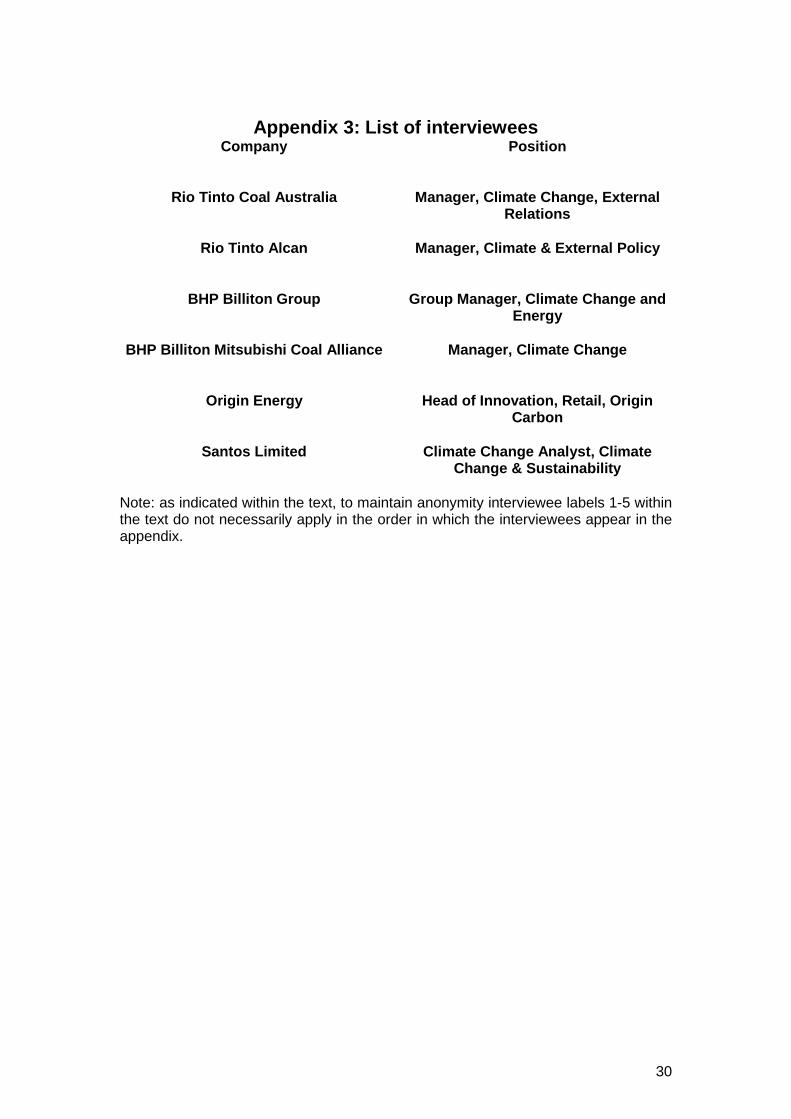

To identify relevant managers able to comment on the climate change-related corporate governance policies and related reporting practices, we conducted an analysis of the websites of the selected companies. The details of these interviewees appear in Appendix 3. The positions of the interviewees indicate their expertise and competency to evaluate the respective company’s climate change-related corporate governance practices and related disclosure practices. Confidentiality was assured and the interviewees are referred in this paper by a coded number, the order of which does not necessarily reflect the order in which they appear in the Appendix. Data collection and analysis Six in-depth interviews with the representatives of the selected companies were undertaken over a two month period from September 2010 to October 20106. Unfortunately it was not possible to interview a representative from Caltex7. Whilst our sample size is relatively small we believe that the views provided by the managers of the sample companies (all of which are very large organisations with major exposure to risk and opportunities associated with climate change) nevertheless provides valuable insights into climate change-related reporting practices. Those who were invited to participate in interview received an email invitation, explaining the purposes and nature of the research study, along with a sample interview guide so that participants might be familiar with the issues to be explored. The interviews ranged between 40 to 60 minutes. While we utilised an interview guide, interview questions were open-ended. Before each interview we explained our project to each interviewee. The interviews took place at a time and location of the participant’s choosing, with four of the six interviews conducted by telephone. All interviews were tape-recorded with the consent of interviewees and were subsequently transcribed almost verbatim. Transcriptions were carefully scrutinised against the tape recordings and amendments made where necessary. After transcription, the coding of the interview data was performed. The main issues around which the coding took place were the managerial motivations to disclose or not to disclose information. In order to provide information about what the interviewees have said we have elected to provide detailed replication of quotes which allows readers to consider not only the potential explanation the researcher has suggested, but also alternative explanations (Ferreira and Merchant, 1992). As indicated by Deegan and Blomquist (2006, p. 355), the reproduction of a number of direct quotes helps ‘guard, at least to some extent, against the authors providing their own, potentially biased, perspective of what interviewees were saying’. The quotes we have replicated were those quotes that represent the typical view of the interviewees. Details of any view provided by an interviewee that is in contrast to the other participants are provided. 4. Interview responses Our research objective was to investigate the reasons for the difference between the information provided by the companies, and the information sought by the stakeholders in relation to climate change-related corporate governance practices. To accomplish this research objective, we talked to six corporate representatives to

6 The companies were BHP Billiton, Origin Energy, Santos Limited, and Rio Tinto. Both BHP Billiton and Rio Tinto are divided into a number of international businesses differentiated by product type. For this study interviews have been taken place with BHP Billiton Groups and BHP Billiton Mitsubishi Coal Alliance, and Rio Tinto Coal Australia and Rio Tinto Alcan. 7 Various attempts to reach corporate representative from Caltex Limited were made including reminder e-mails and few telephone calls.

11

understand managerial motivations to disclose or not to disclose information. Thus, the main issues that we were particularly interested in investigating included— 1. Motivations for the companies to disclose climate change-related corporate governance information 2. Motivations for the companies not to disclose climate change-related corporate governance information 4.1 Motivations for disclosing climate change-related corporate governance information To investigate why companies do not disclose information, it would be useful to understand first what actually motivates them to disclose information. Our participant companies were identified in the first phase of the broader study that investigated current climate change-related corporate governance disclosure practices of some Australian companies through their annual and sustainability reports. In that study Haque and Deegan (2010) found that there is an increasing trend in companies’ climate change-related corporate governance disclosure practices over the years. In relation to the changing nature of the disclosure practices, the interviewees were therefore asked to identify the rationale for developing climate change-related corporate governance practices and related disclosure practices. Respondents unanimously indicated that their reporting practices were motivated by stakeholders’ interest for climate change-related corporate governance information. Reflective of the change in perceived expectation of the stakeholders, it was stated that—

…certainly interests from stakeholders. If you get back in early 2000s, you know back then when I started we did not receive many investors’ surveys. We did not receive that many questions from the community. Employees were not even interested. But certainly the last ten years have seen an increase in stakeholders’ interest, not just about what our carbon emissions are, but what governance policies we use internally to manage climate change. So there is a lot more interest from the stakeholders about how we are managing our climate change liabilities and those sorts of things. (Interviewee #5)

I think we are seeing an increase in requests from the stakeholders for disclosure about how much GHG we emit, how would we reduce the carbon intensity of our product, and how we manage our GHG emissions. I think what you have probably found in our annual and sustainability reports is that the change in reporting is derived by the increasing request for information about our performances and targets. (Interviewee #4)

The above quotes emphasise managers’ perceptions about the changing expectations of stakeholder groups for information. The quotes also reveal a perceived change in stakeholder’s interest that has moved from information about general carbon emissions to information about how companies manage climate change via their governance policies. Corporate representatives were then asked to identify the stakeholder groups who want information from the respective companies. Responses included:

There are many interested stakeholders. I suppose the obvious one to come to mind is government who has an interest in how we run our business through regulations. Our community is obviously another significant stakeholder. All the community around our operations are very interested in everything we do around climate change. Employees are another group interested to know what we are doing, broadly around sustainability not just climate change. (Interviewee #1)

There are interests from various stakeholders for information. For example, investors who are looking at companies to see how well they are managing this climate change issue. And there is also interest from external groups like NGOs. NGOs are following

12

companies’ statements and performance on reducing GHG emissions and monitoring whether companies are doing a good job or not or need to do more. (Interviewee #3)

We have four stakeholders. Number one is our shareholders. Number two is our customers. Number three is the community that we operate in, and number four is our employees. Then there are NGOs. I probably would say that our reporting is mostly aimed at our community and our shareholders. Our company has a responsibility to show how we respond and how we deal with climate change (Interviewee# 4)

The above quotes suggest that government, investors, NGOs, customers, employees, and the community in general were among the stakeholder groups who are perceived as wanting information. Companies’ reporting practices were aimed at the information needs of these stakeholder groups. The responses of the corporate representatives also indicate companies are being strategic in nature when responding to stakeholders’ interest for information with a motivating factor being competitive advantage:

There are interests from stakeholders for information, most recently, from the managers of the ethical investment funds. We believe that responding to them can eventually create a competitive advantage in the context of a future carbon-constrained environment. Our company is doing what is necessary to accurately collect information on our emissions in a comprehensive way. And then reporting this information is an important part of the company equipping itself to stay competitive in the future carbon constrained world. (Interviewee 6)

Again, the strategic nature of the companies’ disclosure policies is emphasised to gain benefits, and reporting is considered as a strategic policy that for the companies:

What I sort of look at it is that for the energy industry, as it goes through transition from very carbon intensive to low carbon, climate change will add value to the companies that are smart enough to adapt with it. That is why we are moving towards renewable sources of energy as a transition which plays very much into our strategic positioning. Reporting is one such area that would add value to our company. We think that there is value in there for our customer brand. We can differentiate ourselves a little more from our competitors by reporting more information which indicates that we are trying to do the right thing to our environment, to the community and to our customers’ life. (Interviewee #4)

In summarising companies’ motivations for reporting climate change-related corporate governance information, it appears that there were interests from stakeholder groups for more information and this had acted as a motivating factor behind companies changing their reporting practices. Disclosing information also is perceived to provide them competitive advantage over their business counterparts. Stakeholder groups identified by our participants included government, investors, NGOs, customers, employees, and community in general. However, question remains whether companies were fully aware of the expectations of these stakeholders in relation to various issues associated with climate change-related corporate disclosure practices. Later in the paper we report whether these stakeholder groups were perceived to be powerful enough to drive companies’ disclosure practices. At this stage of the interviews we advised our participants about the survey conducted in Haque, Deegan and Inglis (2010) that investigated different groups of stakeholders’ perceptions about what companies should disclose in relation to

13

climate changerelated corporate governance practices8. In that survey study Haque, Deegan and Inglis developed a disclosure index, comprising 31 specific climate change-related corporate governance items of information (see Appendix 1), based on the expectations of a group of stakeholders including government bodies, institutional investors, environmental NGOs, and consumer associations – all of which were among the stakeholder groups perceived as having an interest in climate changerelated information. We provided the interviewees with the index containing the list of information items considered as important by the stakeholders in assessing an organisation’s climate change-related corporate governance practises. Our intention was to find out what the respective company representatives perceived about the expectations stakeholders had regarding climate change-related corporate governance information. The respondents were advised that despite the expectations of the stakeholders, much of the information was found missing in the respective companies’ annual and sustainability reports (that is, within their company’s own reports). The responses of the corporate representatives are provided below. Four out of six respondents indicated that there is some information that they specifically elect not to disclose. For example:

I am not trying to say we answer every question that everyone wants to know. I am sure there are some gaps. But I believe any gaps are not that significant. (Interviewee #3)

I know there is some information missing. But it does not mean that we will not consider it in the process. (Interviewee #4)

Consistent with the current research context, it does appear that despite the expectations of the stakeholders, companies are not disclosing all the climate change-related corporate governance information sought by stakeholders. 4.2 Motivations for not disclosing climate change-related corporate governance information Existence of an expectations gap Building upon the responses of the corporate representatives that there is a gap in current climate change-related corporate governance disclosure practices, they were asked to explain why some information is not being disclosed. A typical response to this question was that respondents believed that stakeholders were not interested in so much information.

I don’t think that people are interested so much in the absolute number of what we are reporting. People mean government, our employees, local communities which we operate in—are interested in, as a significant emitter whether we are improving our performance, and how we are improving our performance. Then they might be looking at what else we would be doing to try to improve our climate change-related corporate performance. So,

8 Solomon and Lewis (2002) argued that the user groups may consist of two sub-groups, namely a normative (environmental consultants, academics, professional organisations, trade and industry associations and government organisations) and an interested party group (environmental pressure groups, independent financial advisors, fund managers, researchers, political and professional bodies, banks, institutional investors and the media), where the normative party ‘may not actually use CED, they are likely to have strong views about what is required by users’; on the other hand, the interested party group ‘is intended to represent the users themselves’ (p. 160). Similarly, the stakeholder groups (accounting professionals, environmental NGOs, environmental consultancies, government bodies, institutional investors, researchers, consumer associations, and media) in Haque, Deegan and Inglis (2010) were considered as users of climate change-related corporate governance information as well as having expertise in relation to what is required by the users.

14

we always report on our performance which I believe is enough to satisfy stakeholders’ interests. (Interviewee #1)

Look, the information need [of the stakeholders] should also be realistic. Some of them [information items], I believe, are neither important nor what our stakeholders are really interested in. If we try to deal with all the information then we will probably overload people with information. Certainly that’s not what we want. (Interviewee #5)

Three of the six respondents emphasised that their level of disclosure is greater than what most people expect them to disclose.

The level of reporting that we provide is much greater level than what most people are interested in. I can’t see that there would be a lot of issues people would want to know. Most people don’t want to know all the specific climate change-related corporate governance issues you mentioned. Rather I guess they are more interested in broader climate change issues. (Interviewee# 2)

In relation to the above responses, respondents were asked to explain why they believed that stakeholders are not interested in some information. One respondent argued that if stakeholders were interested to know certain information, those issues must have been raised by them during companies’ engagement with stakeholders.

I think our people and investors’ relation team would get feedback of what they are expecting and what we are not doing. Thus, we continually assess whether or not we are meeting expectations. If there is certain information that they want us to disclose but we are not disclosing then clearly they will let us know. As we are not getting any such feedback I am not sure whether they are really interested to know so many things. With government we assess whether we are not meeting their expectations, mostly through compliance. So we have interaction with them. In terms of our community and employees, I think certainly our sustainability development reports meet their needs. We do talk with community to assess how to meet their needs, what they see that we are not seeing, and then we negotiate that back in. (Interviewee #2)

This above statement suggests that although there is a demand for information by the stakeholders (Haque, Deegan and Inglis, 2010), the information are not perceived as being raised with the companies. There is insufficient response from stakeholders which also implies a lack of pressure being exercised by stakeholder groups. This point is further discussed subsequently within the section ‘lack of stakeholder power’. Deegan and Rankin (1999) found that an environmental reporting expectations gap arises when the users considered environmental information as more important for their decisions than is perceived by the preparers. Likewise, our respondents argued that stakeholders are not interested as they believed that not all information is important for users’ decision making. A typical response was:

I don’t think all this information is necessarily important for stakeholders’ decision making. For example, regarding separate board committee, we thought about it. But at the same time thought what a separate board is going to do? Because carbon emissions are intrinsically linked to the whole operations. I would particularly argue that you need some kind of board where some of the difficult decisions are getting the right feasibility that would drive your organisation forward. Ifyou look at an organisation like us, carbon is such an important business driver for us, both on the opportunities and the risks that it is an inherent part of what we do and the decisions we make and the way we think. So it is like for us business as usual. So that’s why we do not have a separate board to look at these decisions. It is sort of part of our normal business. (Interviewee #4)

15

At the same time three respondents emphasised the less importance of annual and sustainability reports as means of communication, as well as the importance of keeping annual and sustainability reports as short and concise as possible.

There are many ways of providing such information. Annual reports etc are the lowest means of communication when it comes to meeting information needs. When we have a specific information requirement from the stakeholders, we try to meet that request in the most efficient and effective way possible. So you know if you only look at one element of our communication, annual reports are pretty blunt instrument really. And we do not seek to make our sustainability reports a fully comprehensive document that would meet the need of every potential stakeholder, because it would be 1000 pages and therefore it would be less useful because there would be too much information. (Interviewee #1)

For some of the information, particularly within the annual and sustainability reports, we always get the battle to try to keep them as short and concise as possible. We have been going through award processes and certainly try to look at how our sustainability report ranks against others. And the general feedback we are always getting is that the shorter the better. So sometimes it’s not possible to include all information in annual or sustainability reports. (Interviewee #5)

One of our aims in this research was to provide evidence to determine whether an expectations gap exists between stakeholders (users) and company managers (preparers) in relation to climate change-related corporate governance information in annual and sustainability reports. The results provided in this study indicate that such a gap does appear to exist. From the above responses it appears that corporate representatives believed that stakeholders were not interested in all the issues associated with climate change-related corporate governance practices. Respondents tended to disagree with a view that all the climate change-related corporate governance information items were important for users’ decision making. Respondents also tended to downplay the importance of annual and sustainability reports as a means of communication that are considered as important to the users. Based on the notion of expectations gap, it was posited that an expectations gap exists when there is a gap between the expectations stakeholders have and the expectations companies believe stakeholders have in relation to the importance of various issues associated with climate change-related corporate governance practices. In considering the answers provided by the corporate representatives, it does appear that the notion of an ‘expectations gap’ is able to offer an explanation of the current gap in disclosure. Cost-benefit consideration vs. notion of accountability With respect to the question ‘why some information is not being disclosed’, it emerged from the responses that companies did not believe that stakeholders were particularly interested in a broad range of issues. Respondents were then asked to explain whether they would disclose information if they were aware that stakeholders wanted to know additional information about climate change-related corporate governance processes. In response to this question there was an overwhelming consensus among the respondents about some information being commercially sensitive, therefore meaning it was not viable for them to disclose such information. Responses indicated that managers a constraint on disclosure would be the extent to which the information is deemed commercially sensitive. As indicated by one respondent:

We understand that there is a need on behalf of our stakeholders to disclose that information [items in the index]. We have lots of stakeholders all around the world. So you know our reporting is obviously in response to the needs of our stakeholders. The reason

16

you report is because you believe that your stakeholders should know certain information. But again, there is always going to be an example of certain information a stakeholder group wants to know that we elect not to report. There is some information which is in confidence for commercial reasons, therefore it can not be shared publicly. So I suppose my response does not sound surprising. There are individual pieces of data that we do not report or have not reported that people would like to see. People would always want us to report everything. Clearly we cannot. (Interviewee #1)

This is supported by another respondent—

There is certain information that we can not disclose. There is some commercially sensitive information that does not project the company in the best possible way. If it is one such area then we would not disclose that information. Otherwise we certainly will never try to hide information. And sometimes we would be breaking ASX disclosure rules. (Interviewee #5)

The above responses suggests that even though managers are aware of the information needs of stakeholders, they would not disclose information if it is deemed commercially sensitive. Thus the concern over disclosing sensitive information seems to dominate the notion of expectations gap as a reason for non-disclosure. Corporate representatives also indicated a shareholder-oriented view by focusing on the commercial return of the companies. As stated by one respondent:

We have to balance commercial sensitivity. The company can only report what is in the best interest of the shareholders and we have commercial information that needs to be protected. Commercial profit is one aspect which is often forgotten when people ask for information. If stakeholders have all the information [in the index], and if they approach us with those needs, we would consider to respond accordingly and on most occasions, if it’s not commercially sensitive, then we simply provide this information. Transparency within the bound of commercial sensitivity is something that we value. (Interviewee #1)

Shareholders, especially institutional shareholders, want us to make commercially sensible decisions. You know we are not a philanthropic institution. A lot of decisions that we take are based on the business case. So when we make a decision to disclose information we have to make sure that shareholders interest are not compromised. We cannot disclose information that might have a negative impact on our commercial return. Disclosure of confidential and commercially sensitive information may not be necessarily beneficial for the shareholders. (Interviewee 4)

The above statements emphasise that the managers’ decision to disclose or not to disclose information is based on ‘economic’ rationales rather than on the basis of a duty of accountability towards a wider stakeholder audience. However, demands for transparency often relate to social and environmental matters as opposed to commercial issues (Crane and Matten, 2007). Avoiding the revelation of commercially sensitive information might protect the interests of the shareholders, but it is very difficult to envisage stakeholder accountability being established in a situation where managers have such a preoccupation with maximising shareholder value (Cooper and Owen, 2007). When asked what kind of information they considered as confidential, the typical responses were:

In the index you mentioned that stakeholders want us to disclose the potential financial implications of any climate change policy affecting the organisation. But we do not disclose this information for competitive reasons. We have discussed about this in our internal system and then decided not to disclose. We cannot disclose for example very specific information about the energy consumption by our specific operations because

17

that might be valuable to our competitor, how we are doing certain operations, how much energy it takes. So because of our competitive concern we cannot necessarily release information. (Interviewee #3)

I think that sometimes declaring certain information can get you into trouble because people can take that data and go do things with it. It might also be misinterpreted. Information about energy consumption and production can be particularly sensitive. (Interviewee# 2)

We might be doing some stuff that we do not want to talk about. This might relate to some strategic programs that we might develop in next few years. We do many things such as, electric vehicles, energy system management, fuel cells and that sort of thing. We probably don’t want to put them in reports if we think that it would bring us competitive disadvantage. We don’t want our competitors to know that we are doing this. There is also a risk of influencing the market value of the company [disclosing sensitive information publicly]. (Interviewee# 4)

The answers provided by the corporate representatives reveal that there is a cost associated with disclosing information around financial implications of climate change policies, energy consumption and production, and strategic policies that subsequently leads to competitive disadvantage. The quotes also display that companies’ fear misrepresentation of information (Solomon and Lewis, 2002). Regarding the cost of disclosures, one respondent indicated that there are some data collection and distribution costs associated with reporting. However, the respondent argued that this is not that material as it is a part of their ‘business as usual’ approach:

There are costs associated with reporting, for example, data collection and distribution costs. But would it be a significant cost in relation to all of our other costs? No, it would not be. Is it significant cost compared to the cost we pay for energy? No it is not. Clearly it’s a small proportion of our energy costs each year. However, there are some significant costs. As you know, it takes quite a lot of work and involves a lot of time and people within the organisation to make sure the information is appropriate and correct. But this cost would not be material, as well as it is certainly not insignificant. (Interviewee# 1)

Responses from the corporate representatives also indicated that because many of the benefits of reporting are internal (e.g. better data, identification of opportunities for improvement, boosting employee morale), and because these benefits are difficult to quantify (e.g. builds credibility and transparency within the community, and other stakeholders including shareholders), companies tend to underestimate their importance. In this paper we argued that the cost-benefit assessments associated with reporting determines companies’ decision to disclose information. The interview responses indicated that the most important cost limiting disclosure is competitive disadvantage (Gray et al, 1990), not the direct costs of disclosure which includes the costs of data collection, and dissemination. The most important consideration that influence companies disclosure practices was the competitive disadvantage in relation to disclosing commercially sensitive information. From the views expressed here, it seems reasonable to conclude that the companies’ interviewed did not feel ethically obliged to report certain information. Their positions imply that economic motive play a dominant role compared to embracing a broader level of accountability. Thus they are discharging limited accountability by not providing as fuller account as they could of their climate change-related corporate governance practices. The cost of reporting commercially sensitive information appears to dominate the notion of expectations

18

gap, as corporate representatives clearly stated that even though the stakeholders ask them for information, they would not disclose it if the information being requested is commercially sensitive. So the next question is whether the stakeholders’ power is perceived to be great enough to motivate companies to disclose information, including commercially sensitive information. Lack of stakeholder power Based on the complementary perspectives within the managerial branch of stakeholder theory and coercive isomorphism of institutional theory, it was argued that if the power of the stakeholder groups who want information is not perceived to be great enough then companies would not be motivated to disclose climate change-related corporate governance information. Therefore, the interviews held with the representatives of the companies sought to discover whether the pressure from the powerful stakeholder groups was great enough to drive companies’ climate change-related corporate governance disclosure practices. As identified earlier from the responses of the corporate representatives, there are several stakeholder groups who want information in relation to climate change-related corporate governance practices. The stakeholder groups identified by the respondents include investors, government, employees, NGOs, customers, and the community in general. Corporate respondents were, therefore, asked whether they perceived these stakeholder groups as powerful regarding their reporting issues. In response to this question, respondents argued that different stakeholders are powerful in different ways. Among them investors and government were considered as the most powerful stakeholders.

It’s hard to narrow down that one is more important than the others. There are all different and they have slightly different interests in what we are reporting. Certainly investors are one of the most important stakeholders. What is really important is that investors can understand that we are managing climate change adequately so that they will not feel unsafe with their investment (Interviewee #5)

If investors want to know any information we have to provide them that because we need funds from them. We need to demonstrate that we can manage our emissions and reduce our emissions as much as possible from the projects that they are investing in. We need to demonstrate that the projects are safe, so they are not going to lose their money. Otherwise they do not want to invest in our businesses. ((Interviewee #3)

The above responses indicated investors, as a fund provider, are the stakeholder considered as powerful. It indicates that if investors, as a supplier of resources, require companies to provide particular climate change-related corporate governance information then companies would provide this information to secure funding. But commercially sensitivity would still act as a barrier to reporting. Interview responses also suggested that investors are not perceived to be particularly interested in improving climate change-related practices of companies. Rather, they are more interested in the profitability aspect.

I think investors are certainly powerful stakeholders as they provide funds. If there is any specific query we are happy to provide that information. However in case of commercially sensitive information we cannot even disclose to our investors. I guess investors also understand that. They do not usually require any information that would be not be in the best interest of the company or the investors. I think they are more interested in commercial profitability of the business rather than social responsibility types of things. They are more concerned about the business risks we face from climate change, whether it’s going to cost our profit, or how we can utilise the opportunities to gain profit. (Interviewee #5)

19

We try to make sure that we consider the concerns of environmental NGOs, our employees, our customers, the community in general who are more interested in our climate change-related performances, as well as the concerns of our investors, who are more interested in our commercial return. So sometimes there might be some conflicts between which concerns you should prioritise. (Interviewee #4)

It was revealed by the respondents that there were a number of disclosure frameworks being used, such as the Carbon Disclosure Project (CDP) project. As indicated by one respondent:

We are providing information to our investors, particularly through the Carbon Disclosure Project (CDP). I think 2006 is the first year that Australian companies were invited to participate in CDP. We also report in other surveys that are more general in nature but have a climate change component in them. For example, we are participating in the Dow Jones Sustainability Index (DJSI). But the CDP project is more comprehensive with respect to climate change and it appears to have created a deal of interest with investors. (Interviewee #5)

The CDP has led to the institutionalisation of carbon reporting given that the majority of the 500 largest global companies are now using the CDP as a mechanism for carbon disclosure (Kolk et al, 2008). Kolk et al argued that the increasing response rate to the CDP suggests that investors’ pressure can have an impact on carbon reporting. However when asked whether they perceived any pressure to participate in the CDP, or any other similar reporting practices, one of the five respondents explained:

Rather than pressure it is probably useful in identifying our gaps and for focussing improvement. Particularly the CDP helps us to identify the gaps that we have. And the DJSI as well. (Interviewee #5)

What we have found from the responses was that although investors are powerful, they are perceived to be more interested in the profitability aspect of the business – that is, whether their return on investment is going to be affected. This concern for profitability versus concerns for environmental responsibility (Oliver, 1991) has an influence on corporations’ business practices, including reporting practices. . Another powerful stakeholder group with regards to reporting is government because of legal compliance. If it is a particular government requirement, then companies feel a need for compliance. Responses included:

Governments are obviously a very important stakeholder. All kinds of governments including state, federal and even local. If you have a legal obligation then government have power to make you report. If government wants any information we provide them that. (Interviewee #2)

However, the following response suggests that at present companies do not perceive a great deal of pressure from the government because of the lack of current regulatory requirements.

[Not exactly] I don’t see it [government] as providing much pressure. We have constant engagement with the government and it is more like an ongoing discussion around policy development, around mechanics of reporting in relation to climate change. I don’t think we feel any pressure. Government sometimes asks information like ‘do you have information on the emissions impact of your solar project, or do you have actual information around that’. But there is not that much pressure on the way we report. Our climate change-related reporting in annual and sustainability reports is totally voluntary.

20

There is no legal obligation for us to report on our climate change-related governance practices. But there might be government pressure brought upon us. We are now covered by National Greenhouse and Energy Reporting System (NGERS). So that’s the kind of reporting standard we are moving into. (Interviewee #4)

While companies do not perceive pressure from the government right now, there is a consensus about future regulatory environment in relation to climate change-related business practices. Respondents suggested that government regulation would be the biggest influence in future period for their climate change-related business practices:

I think given where government policies are heading there is potential for the government policies to have a big impact on businesses. Now we are operating in a more voluntary environment. And it will change as we move to a more regulated environment [such as price on carbon, taxes, and international trading on carbon]. (Interviewee #4)

Cowan and Deegan (2010) argued that although it is likely that the implementation of regulations like the NGER Act 2007 and the proposed CPRS may increase voluntary emissions disclosure in annual reports and other media, it is similarly likely that such disclosures will continue to be incomplete and inconsistent. When asked how respondents perceived that the future regulatory environment might affect company’s reporting practices, and the following perception emerged (which was reflective of the argument made by Cowan and Deegan, 2010):

I do not believe that our voluntary reporting practices would be changed much because of government regulation. We are already disclosing our emissions publicly, and doing compliance reporting as well. (Interviewee #5)

Other stakeholder groups considered as powerful included the ‘community’ in general, employees, customers, and NGOs. The following comment is reflective of this view:

Community is the one group who can stop us going ahead and expanded into new projects through the licence to grow, or license to operate. We also focus on employee engagement. Employees have certainly been taking a lot of interest in what we are doing. We have engagement programs to share our ideas, to make sure employees know what they are doing. Customers are probably the one we listen to more because at the end of the day they pay for everything. So we make sure to do what makes them happy. And that’s probably where we focus more and more to meet the customer needs. So I think they are all powerful but in different ways. We are in retail, so we are very close to the customers …and then there are NGO groups that are interested. We have received a lot of queries from environmental NGOs, especially when government policy got released. There is always a request for more information from NGOs for our strategic positioning towards climate change. But it’s hard to say one is really more important than the other. (Interviewee #4)

From the above responses by the corporate representatives, it appears that companies perceived that the community is a powerful stakeholder because without communities’ approval they cannot gain a ‘community license to operate’. Other powerful stakeholder groups are employees and customers who are interested in organisations’ climate change-related business practices. NGOs are another interested group. However when asked whether they feel any pressure from the groups they considered as powerful to disclose climate change-related corporate governance information, most of the interviewees indicated that they do not feel any pressure from the respective stakeholders. Typical responses included:

No, we don’t feel any real pressure. I don’t think their influence is great. I don’t think we set up our sustainability reports or other reports towards our stakeholders because they

21

are powerful. I think we report in a way that all of our stakeholders can read it and find it useful. There haven’t been any NGOs or any consumer groups or communities coming to us and complaining that we are not doing enough in terms of climate change policies and reporting. We have no pressure from our stakeholders that we need to do more on climate change. And that’s because we are very strong on our advocacy position and we are investing in cleaner technology etc. (Interviewee #4)

I will not necessarily say we feel pressure. We have never received any complaint that we are not working enough on climate change. But we do feel that they value information. There is value in us providing information. So I would say it’s more like a case of understanding that we can have better relations with our stakeholders and they will have a better view of our company if we make information available. (Interviewee #3)

Because of the concerns of others we never reported. We have given them the data and we believe that it is enough for them to make decisions. And we will continue to do that. We have been reporting voluntarily to the greenhouse challenge program for nearly 13 years now. So once you are into the culture of public disclosure I don’t think there is any issue that we don’t disclose. I would say in terms of our stakeholders such as environmental NGOs, or consumer groups, I am not aware that many of them actively seek out further information about our performance. So I wouldn’t say that we have got environmental NGOs coming to see us and say there is particular information they would like to know. We have already reported or are reporting everything necessary. And its not that we feel any pressure for this public disclosure. I think we are transparent on what we report. (Interviewee #2)

In considering the various answers provided by the corporate representatives it appears that the lack of stakeholder influence over companies’ disclosure practices offers an explanation of the current gap in disclosure. Stakeholder power stresses the power of stakeholders in influencing corporate practices. Prior literature found that because of the pressure from the powerful stakeholder groups such as investors, NGOs, and community in general, there was a change in companies reporting of some specific aspects of social and environmental performance (Deegan and Blomquist, 2006; Epstein and Freedman, 1994; Tilt, 1994). Thus the influence of the powerful stakeholder groups can bring change to organisation’s corporate practices. However, although considered as powerful, our corporate respondents had not perceived any great deal of pressure from the key stakeholders such as government, investors, NGOs, and the community in general in relation to climate change-related corporate governance information. Chang and Deegan (2010) found that because of a lack of pressure from the powerful stakeholder such as the government, environmental management accounting (EMA) would be less likely to be embraced by universities for the purpose of managing environmental costs and minimising environmental impacts. In this study, the interview responses indicated that powerful stakeholders have not been perceived to exercise pressure on companies to motivate them to disclose climate change-related corporate governance information. Although there is a demand for information from powerful groups, the level of pressure is not up to the level that drives companies to disclose more information. Due to a lack of exercise of stakeholder power, it is less likely that companies would be motivated to disclose the information sought by the stakeholders. Therefore, the lack of pressure from the powerful stakeholder groups contributes to explain the lack of climate change-related corporate governance information provided by Australian companies. 5. Discussion and conclusion This paper explores potential reasons for an apparent gap between the climate change-related corporate governance information being provided by companies, and the information being sought by stakeholders. Having now gained and documented

22