For definitions and the distribution of anal yst ratings, and other disclosures, please refer to pages 30 - 31 of this report. ® October 26, 2011 Celsion Corporation (CLSN) INITIATING COVERAGE LIFE SCIENCES Market Outperform / Speculative Risk Reni Benjamin, Ph.D. 212-430-1743 [email protected]CLSN: OFF TO THE RACES – THERMODOX TURNS UP THE HEAT IN HCC MARKET DATA 10/25/2011 Price $2.75 Exchange NASDAQ Target Price $6.00 52 Wk Hi - Low $4.37 - $1.98 Market Cap(MM) $72.3 EV(MM) $67.5 Shares Out (MM) 26.3 Avg. Daily Vol 512,187 Short Interest 1,716,960 BALANCE SHEET METRICS Cash (MM) $25.0 LTD (MM) $0.1 Debt/Capital NA Cash/Share $0.12 Book Value(MM) NA Book Value/Share $0.03 Cash (MM): Pro formaEARNINGS DATA ($) FY - Dec 2010A 2011E 2012E Q1 (Mar) (0.50) (0.28)A (0.26) Q2 (Jun) (0.22) (0.42)A (0.19) Q3 (Sep) (0.38) (0.25) (0.19) Q4 (Dec) (0.43) (0.26) (0.33) Full Year EPS (1.52) (1.14) (0.97) Revenue (MM) 0.0 2,000.0 0.0 VALUATION METRICS Price/Earnings NM NM NM EV/Revenue 0.0x Y/Y EPS Growth NM NM EV/Sales INDICES DJIA 11,706.6 SP-500 1,229.0 NASDAQ 2,335.9 NBI 1,000.0 Q3 Q1 Q2 Q3 0 1 2 3 4 5 2011 2012 1 Year Price History Created by BlueMatrix 0 1 2 3 INVESTMENT OPINION We are initiating coverage of Celsion with a Market Outperform / Speculative Risk rating and a target price of $6, based on a discounted revenues and earni ngs per share valuati on metho dology . The compa ny’s novel platfo rm techno logy utilizes heat specif ic labile phospholipids which can release chemotherap eutics upon activ ation by a heat source. Celsion’s late-s tage asset, ThermoDox, has completed enrollment in a >600 patient world-wide liver cancer trial with the potential to report final results by year end 2012. The product is currently seeking to address the >$1 B hepatocellular carcinoma (HCC) market, but can be rapidly expanded to address multiple billion dollarmar kets . Cel sion has established relationships with Pharma and has already forged a commercial partnership with Yakult Honsha to market ThermoDox in Japan. With approximately $25 MM in cash pro forma, and an enterprise value of $47 MM, we believe Celsion represents an undiscovered, and undervalued company with multiple near-term drivers poised to create shareholder value in 2012. A TROJAN HORSE WAITING TO CONQUER CANCER Celsion’s most advanced pr oduc t is Ther moDox, a liposomal encapsul at ion of dox orubicin, which is acti vated upon exp osure to mild hyperthermia. The company has completed enrollment of over 600 patients in the pivotal Phase 3 HEAT Study ev alu ating ThermoDox in conjunct ion wi th radiofrequency ablation (RFA), the standard of care in Stage A/B HCC. The >600 patient trial is expected to report interim results in 4Q11 with final progression free survival results expected as early as 4Q12. With a projec ted 80% gros s mar gin on sal es, we are for ecasti ng peak risk adjusted world-wide revenues of approximately $400 MM by 2019. HOT TO TROT IN EMERGI NG MARKETS The company’s ongoin g HEAT Study is being conducted in over 11 countries including China, and is under a Special Protocol Assessment (SPA) with the FDA. Given the world-wide incidence of HCC and the dearth of therapeutic options, we believe Asia, in particular China, represents a key market whereby significant sales can be recorded. The company has also formed a joint research agreement with Philips Healthcare to evaluate the Philips’ high intensity focused ultrasound (HIFU) with ThermoDox® in a broad range of cancers. PHYSICIAN’S CORNER We consulted with Dr. Riccardo Lencioni, Dr. Thanjavur Ravikumar, and Dr. Steven Libutti as part of our due diligence for ThermoDox. All three physicians have experience with the drug in HCC patients. All three commented favorably regarding the chance forsuccess in the ongoing Phase 3 trial, as well as the significant market adoption that could take place, if the trial is successful and approved formarketing.

Transcript

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 1/31For definitions and the distribution of analyst ratings, and other disclosures, please refer to pages 30 - 31 of this repor

CLSN: OFF TO THE RACES – THERMODOX TURNS UP THE HEAT IN HCC

MARKET DATA 10/25/2011Price $2.75

Exchange NASDAQ

Target Price $6.00

52 Wk Hi - Low $4.37 - $1.98

Market Cap(MM) $72.3

EV(MM) $67.5

Shares Out (MM) 26.3

Avg. Daily Vol 512,187

Short Interest 1,716,960

BALANCE SHEET METRICS

Cash (MM) $25.0

LTD (MM) $0.1

Debt/Capital NA

Cash/Share $0.12

Book Value(MM) NA

Book Value/Share $0.03

Cash (MM): Pro forma

EARNINGS DATA ($)

FY - Dec 2010A 2011E 2012E

Q1 (Mar) (0.50) (0.28)A (0.26)

Q2 (Jun) (0.22) (0.42)A (0.19)

Q3 (Sep) (0.38) (0.25) (0.19)

Q4 (Dec) (0.43) (0.26) (0.33)

Full Year EPS (1.52) (1.14) (0.97)

Revenue (MM) 0.0 2,000.0 0.0

VALUATION METRICSPrice/Earnings NM NM NM

EV/Revenue 0.0x

Y/Y EPS Growth NM NM

EV/Sales

INDICES

DJIA 11,706.6

SP-500 1,229.0

NASDAQ 2,335.9

NBI 1,000.0

Q3 Q1 Q2 Q30

1

2

3

4

5

2011 2012

1 Year Price History

Created by BlueMatrix

0

1

2

3

INVESTMENT OPINION We are initiating coverage of Celsion with Market Outperform / Speculative Risk rating and a target price of $6based on a discounted revenues and earnings per share valuatiomethodology. The company’s novel platform technology utilizes heaspecific labile phospholipids which can release chemotherapeutics upoactivation by a heat source. Celsion’s late-stage asset, ThermoDox, hacompleted enrollment in a >600 patient world-wide liver cancer trial witthe potential to report final results by year end 2012. The product currently seeking to address the >$1 B hepatocellular carcinoma (HCCmarket, but can be rapidly expanded to address multiple billion dollamarkets. Celsion has established relationships with Pharma and haalready forged a commercial partnership with Yakult Honsha to markeThermoDox in Japan. With approximately $25 MM in cash pro formaand an enterprise value of $47 MM, we believe Celsion represents a

undiscovered, and undervalued company with multiple near-term driverpoised to create shareholder value in 2012.

A TROJAN HORSE WAITING TO CONQUER CANCER Celsion’s mosadvanced product is ThermoDox, a liposomal encapsulation odoxorubicin, which is activated upon exposure to mild hyperthermia. Thcompany has completed enrollment of over 600 patients in the pivotaPhase 3 HEAT Study evaluating ThermoDox in conjunction witradiofrequency ablation (RFA), the standard of care in Stage A/B HCCThe >600 patient trial is expected to report interim results in 4Q11 witfinal progression free survival results expected as early as 4Q12. Withprojected 80% gross margin on sales, we are forecasting peak risadjusted world-wide revenues of approximately $400 MM by 2019.

HOT TO TROT IN EMERGING MARKETS The company’s ongoinHEAT Study is being conducted in over 11 countries including Chinaand is under a Special Protocol Assessment (SPA) with the FDA. Givethe world-wide incidence of HCC and the dearth of therapeutic optionwe believe Asia, in particular China, represents a key market wherebsignificant sales can be recorded. The company has also formed a joinresearch agreement with Philips Healthcare to evaluate the Philips’ higintensity focused ultrasound (HIFU) with ThermoDox® in a broad rangof cancers.

PHYSICIAN’S CORNER We consulted with Dr. Riccardo Lencioni, DrThanjavur Ravikumar, and Dr. Steven Libutti as part of our due diligencefor ThermoDox. All three physicians have experience with the drug iHCC patients. All three commented favorably regarding the chance fosuccess in the ongoing Phase 3 trial, as well as the significant markeadoption that could take place, if the trial is successful and approved fomarketing.

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 2/31

RODMAN & RENSHAW EQUITY RESEARCH

INVESTMENT SUMMARY

Celsion, based in Lawrenceville, NJ focuses on the in-licensing, development and commercialization of targetedchemotherapeutic treatments based on a proprietary heat-activated liposomal delivery technology. The liposomadelivery technology allows for the release of encapsulated chemotherapeutic agents at specific tumor sites upontargeted activation by heat. Celsion’s core compound is ThermoDox, a proprietary liposomal doxorubicin complex thais currently being evaluated in combination with Radiofrequency Ablation (RFA) in a Phase 3 trial for the treatment ofHepatocellular Carcinoma (HCC). The Phase 3 trial, known as the HEAT Study, completed enrollment of 600 patients inAugust 2011 and is under a Special Protocol Assessment (SPA) with FDA Fast Track Designation. Interim results areexpected in 4Q11. Celsion has elected to continue enrollment to 700 patients in order to accelerate time whenendpoints will be achieved and to ensure at least 200 patients will be enrolled in China. The company also receivedorphan drug designation in both the US, and Europe for ThermoDox to treat HCC. Importantly, the HEAT Study issupported by Phase 1 data which showcase a clinically significant dose response in those patients treated withThermoDox + RFA at increasing dose levels. Specifically, the median time to progression (TTP) more than doubled inpatients treated at the maximal tolerated dose (MTD) compared to those patients at lesser doses. ThermoDox is alsobeing used in combination with hyperthermia for the treatment of Recurrent Chest Wall (RCW) breast cancer in anongoing Phase 1/2 trial, known as the DIGNITY Study. Celsion recently completed the Phase 1 portion of the DIGNITYStudy and plans to move into the Phase 2 portion of the trial following complete review of the Phase 1 data.Additionally, Celsion has launched a Phase 2 trial of ThermoDox in combination with RFA for the treatment of colorectalliver metastasis in September, 2011, and Celsion has developed a Phase 2 protocol (under FDA review) for the use ofThermoDox in combination with High Intensity Focused Ultrasound (HIFU) for the treatment of painful bone metastases.

Celsion has licensed exclusive world-wide rights to the proprietary lipid technology from Duke University and has IPprotection until 2018. Additionally, the orphan drug designation provides Celsion with 7 years of exclusivity in the U.Sand 10 years of exclusivity in Europe. Celsion also completed an out-licensing agreement with Yakult Honsha in 2008which gives Yakult the exclusive right to commercialize and market ThermoDox in Japan. The Yakult agreement entitlesCelsion to receive at least $10 MM in milestone payments following the marketing approval of ThermoDox in Japan, aswell as double digit royalties on ThermoDox sales in Japan.

EXPECTED NEWSWORTHY EVENTS/MILESTONES FOR 2011-2012Hepatocellular Carcinoma

- Potential for blinded interim efficacy and futility analysis of data from the HEAT Study (4Q11)

- Potential for complete data readout from the HEAT Study (4Q12)

Recurrent Chest Wall Breast Cancer

- Potential to proceed with Phase 2 portion of the DIGNITY Study (1Q12)

Colorectal Liver Metastasis Trial

- Expecting first patient to be randomized in a Phase 2 trial of ThermoDox in combination with RFA for the

treatment of the colorectal liver metastasis in 4Q11

Bone Metastasis Trial

- Potential to begin enrollment in the Phase 2 trial of ThermoDox in combination with HIFU for the treatment o

painful bone metastases (4Q12)

INVESTMENT OPINION

We are initiating coverage of Celsion with a Market Outperform / Speculative Risk rating and a target price of $6, basedon a discounted revenues and earnings per share valuation methodology. Celsion’s late-stage asset, ThermoDox, hascompleted enrollment in a >600 patient world-wide liver cancer trial with the potential to report final results by year end2012. The product is currently seeking to address the >$1 B hepatocellular carcinoma (HCC) market, but can be rapidlyexpanded to address multiple billion dollar markets. Celsion has already forged a commercial partnership with YakulHonsha to market ThermoDox in Japan with the potential for a commercial launch in 2015. With approximately $25 MMin cash and cash equivalents, Celsion represents an undervalued opportunity with multiple near-term drivers poised tocreate shareholder value in 2012.

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 3/31

RODMAN & RENSHAW EQUITY RESEARCH

INVESTMENT HIGHLIGHTS

THERMODOX

ThermoDox is a heat sensitive liposomal encapsulation of doxorubicin which can be activated to release thechemotherapeutic agent in regions of localized mild hyperthermia. The release from the liposome, facilitated bystandard of care devices, including radiofrequency probes as well as ultrasound devices, should enable highconcentrations of doxorubicin to be deposited preferentially in the region of the tumor target. Celsion has completed a

Phase 1 liver cancer study demonstrating a dose dependent improvement in time to tumor progression (TTP) in patientsthat have undergone RFA to treat their cancer. Importantly, in a sub-group analysis of patients treated at the MTD of 50mg/m2 or greater, a statistically significant quadrupling of time to treatment failure was observed. Celsion’s leadproduct, ThermoDox®, is being evaluated under a SPA in a 700 patient Phase 3 study in primary liver cancer evaluatingThermoDox+RFA versus RFA alone, as well as in a Phase 1/2 study in recurrent chest wall (RCW) breast cancer. Thefinal results from the Phase 3 pivotal study are expected as early as 4Q12.

ThermoDox has Distinct Advantages:

ThermoDox achieves maximal plasma concentrations within 30 minutes of injection and maintains a high serumconcentration for about 6 hours, allowing for a convenient window for complete tumor ablation.

ThermoDox is systemically administered, but concentrates in the liver with site specific locations achieving 10Xthe peri-tumoral dosage levels as compared to conventional or “free” doxorubicin.

ThermoDox preferentially releases doxorubicin upon activation by an increase in thermal temperature, whichhappens to be a by-product of RFA. The ThermoDox benefit is achieved when high levels of doxorubicin aredeposited at or around the residual tumor resulting in increased killing of peripheral zone cancer cells, which areknown to cause recurrence.

ThermoDox possesses a relatively similar safety profile as doxorubicin.

FIGURE 1: TARGETED RELEASE OF CHEMOTHERAPY

Source: Celsion Presentation

Phase 1 Trial Sets Stage for Registrational Study

Celsion completed a Phase 1 dose escalation study consisting of 9 patients with primary HCC and 15 patientswith liver tumors that had metastasized from other organs. Patients were treated with a single 30-min IVinfusion of ThermoDox at 20, 30, 40, 50, or 60 mg/m

2before undergoing an RFA procedure. A maximum

tolerated dose (MTD) of ThermoDox was determined to be 50 mg/m2, with the most common grade 3+ events

being abnormal liver enzyme levels. In the Phase 1 study, the median time to treatment failure for patientsreceiving at least 50 mg/m

2was 374 days, whereas patients receiving less than the MTD of 50 mg /m

2had an

80 day median time to treatment failure (p= 0.038). A sub-group analysis of the 9 HCC patients in the Phase 1study indicate that the “time to progression” increased from 156 days at doses ≤ 40 mg/m

2to 337 days at doses

≥ 50 mg/m2

days. Taken together, the Phase 1 data indicate that RFA combined with ThermoDox is wetolerated and produces a significant and compelling dose response effect in liver tumors.

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 4/31

RODMAN & RENSHAW EQUITY RESEARCH

Phase 3 Study (HEAT) Represents Key Value Driver for Shareholders

An ongoing Phase 3 study is one of the largest, controlled trials to be run in HCC. The Phase 3 trial, known asthe HEAT Study, is a randomized, double-blind, controlled study comparing RFA + ThermoDox to RFA alone fothe treatment of unresectable HCC. The HEAT Study involves 76 clinical sites in 11 countries. The pre-planned600 patient enrollment objective of the study was achieved in early August 2011. The company is also workingdiligently to support registration in multiple Asian countries by enrolling enough patients from each respectivegeography. For example, approximately 200 patients will be from China; 90 patients from South Korea; and 70patients from Taiwan. By way of comparison, the Nexavar study conducted by Bayer and Onyxx enrolled 602

patients (526 from Europe and Australia, 56 from North America, and 20 from Central and South America). ThePhase 3 HCC Sutent study by Pfizer planned to enroll 1200 patients; however, enrollment was halted after 1074patients had been enrolled due to serious adverse advents in the Sutent arm of the study.

The Heat Study is 80% powered to detect a 33% improvement in the rate of recurrence. Given the historicacontrol rate for median PFS of 12 months, the study will be a success if the ThermoDox + RFA arm cangenerate a median PFS of 16 months.

The study calls for an independent Data Monitoring Committee interim efficacy analysis following completion oenrollment and after approximately 190 PFS events have been confirmed. The interim analysis is expected in4Q11. The analysis is blinded with both futility and efficacy hurdles built in to the design. The three possibleoutcomes from upcoming analysis are: 1) stop and unblind the study due to overwhelming efficacy (we estimatea p value of 0.001); 2) stop and unblind the study due to futility; 3) continue the study until final analysis. In ouropinion, the most likely scenario involves the continuation of the study until the final analysis is triggered upon

380 PFS events. We expect these events to occur as early as 4Q12.

Existing Japanese Partner in Yakult Honsha Suggests Others Waiting on the Sidelines

Celsion completed a licensing deal with Yakult Honsha Co., Ltd. (Tokyo: 2267) for the commercialization oThermoDox in Japan in 2008. Under the terms of the original agreement, Celsion received a $2.5 MM upfronpayment, which is to be followed by an $18 MM milestone payment upon the approval of ThermoDox by theJapanese Ministry of Health. Upon ThermoDox approval in Japan, Celsion is also eligible for sales milestonepayments, double digit sales royalties, and $7 MM in shared development costs. In January 2011, Celsionamended the Yakult Agreement which provided for an early $2 MM accelerated payment by Yakult in exchangefor a reduction of the original approval milestone payment to Celsion. The amendment also allows for anadditional $2 MM accelerated payment by Yakult upon resumption of enrollment in Japan for a Phase 3 study ofThermoDox. Taking into account both of the Yakult payments set forth by the January 2011 amendment and

the partial reduction in milestones, the original ThermoDox approval milestone will be reduced by approximately40%, or $7.2 MM.

Physician’s Corner:

Dr. Riccardo Lencioni is Associate Professor of Radiology and Head of Diagnostic Imaging and Intervention inthe Department of Liver Transplantation, Hepatology and Infectious Diseases of the University of Pisa. He haspublished seminal papers regarding RFA and was involved in the first randomized study to treat HCC with RFA.He is currently participating in the ongoing HEAT Study. Dr. Lencioni highlighted that RFA is the standard ocare in patients with nodes > 3cm, and that the majority of HCC patients present with tumors ranging from 3-7cm. If the tumor is completely eradicated, Dr. Lencioni believes that 60-70% of patients can be alive at 5 yearsHowever, current imaging techniques greatly under-estimate the amount of residual disease, leading to higherates of recurrence. In his estimation, 5-10% get no treatment; 5-10% of patients proceed to transplant; 5-10%are resection eligible; and an overwhelming 75% get some form of intervention, including RFA or chemo

embolization.

Dr. Thanjavur Ravikumar is a board certified surgeon at the Henry Cancer Center Geissinger Medical Center.He is medical director at the NCI Community Cancer Care Centers Program, and Director at the Center forSurgical Innovation. Dr. Ravikumar commented that in the US, the gold standard for HCC is resectionHowever, in cases where there are multiple nodes, or nodes >3 cm, RFA is the gold standard. In fact, in hisestimation, tumors <2 cm have a local recurrence rate which is negligible, where as tumors > 3 cm have localrecurrence rate of >45% within 12 months. Key concerns regarding the ongoing HEAT Study include interinvestigator variability as well as the fact that HCC is globally heterogeneous tumor. However, Dr. Ravikumadid explain away such concerns given the size of the trial, as well as the fact that it is randomized andcontrolled. In the future, he believes that a minimally invasive and safe procedure, followed by systemicadministration of chemotherapy will likely become the standard of care.

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 5/31

RODMAN & RENSHAW EQUITY RESEARCH

Dr. Steven Libutti is a board certified surgeon and Director at the Montefiore-Einstein Center for Cancer Care

Dr. Libutti expressed his support regarding the design and conduct of the Phase 3 trial and also felt that therationale for the initiation of a Phase 3 trial based on the 24 patients involved in the Phase 1/2 trial made soundscientific sense. In his opinion, conducting a larger Phase 2 trial would not significantly change the Phase 3 triadesign or the assumptions behind the statistical considerations. Given that RFA + ThermoDox is being testedagainst RFA + placebo, Dr. Libutti believes that the odds for a successful trial are stacked in Celsion’s favor.

Market Potential: The market potential for ThermoDox in HCC alone exceeds $1 B. Given a HCC population of approximately

9,800 in the US, 15,000 in the EU, and approximately 200,000 in China, the addressable total worldwidepopulation could be greater than 225,000 patients. Assuming that 50% of HCC patients are eligible for nonsurgical invasive therapy, such as RFA, approximately 112,000 patients worldwide would be eligible foThermoDox. Assuming an annual cost of treatment for ThermoDox of $25,000 in the US, $15,000 in the EUand $12,500 in China, we estimate the market potential of ThermoDox could be closer to $1.5 billion.

Our model assumes FDA approval of ThermoDox and launch in the US in 2013. Marketing approvals in the EUand China are expected in 2014 and 2015, respectively. Given a modest ramp achieving peak sales within 5years of launch, we project 2018 risk-adjusted revenues in the US, EU, and China of approximately $30.7 MM,$37.3 MM, and $302.6 MM, respectively.

Phase 2 Recurrent chest wall breast cancer Celsion

Phase 2(planned)

Colorectal liver metastasis Celsion

Phase 2(planned)

Painful bone metastasis Celsion

Source: Celsion Presentation

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 6/31

RODMAN & RENSHAW EQUITY RESEARCH

INVESTMENT PROS AND CONS

The major investment pros and cons, as we see them, are summarized in the following table:

POSITIVES NEGATIVES

ThermoDox has the potential to address largeunmet medical needs in HCC

Competition in the HCC field is intense and rangesfrom advancements in current treatments protocols

to the development of novel chemotherapeutic

agents in Phase 3 trials

ThermoDox HCC treatment increases theeffectiveness of a proven treatment for HCC (RFA)

New treatment regimens (ex. Nexavar) combinedwith preexisting techniques (TACE) may impact the

HCC market and / or provide a less invasivetreatment options

Large worldwide market for ThermoDoxCelsion will need to partner to develop ThermoDox

outside the US

ThermoDox can be used to treat additional cancerindications

Company will require additional financing todevelop ThermoDox for other indications

ThermoDox US method of use patent extends to

2021

Platform technology relies on the heat activatedrelease of the chemotherapeutic agent to the target

tissue, and therefore treatment indications arelimited to tissues which can be directly stimulated

by an external heat source

Celsion’s platform technology is expandable toother chemotherapeutics

Source: Rodman & Renshaw Research, Celsion

SCIENTIFIC BACKGROUND

THE CLINICAL CHALLENGE OF HEPATOCELLULAR CARCINOMA

Hepatocellular carcinoma (HCC) is the most prevalent subtype of primary liver cancer liver1. HCCs are often described

as complex heterogeneous tumors which respond poorly to traditional chemotherapeutic agents2. In addition, given the

lack of clinical biomarkers available for diagnosis, greater than 70% of patients present with advanced disease. Giventhat curative treatment options for patients with late stage clinical presentation are limited, the advanced HCC populationrepresents a significant unmet medical need and robust area of development for novel treatment options

3.

Incidence, Prevalence & Survival Statistics

HCC is the third most common cause of cancer worldwide, and is responsible for over 700,000 deaths each year4

Approximately 75% of HCC cases occur in patients with chronic liver disease, which may result from chronic hepatitisinfection, including both hepatitis B (hep B) or hepatitis C (hep C) infection

5.

The incidence of HCC varies throughout the world by geographic location, but in general, the incidence rates are lowerin developed countries than developing countries (Figure 2). For example, the 1975 U.S. incidence of HCC per 100,000people was 2.6 for men, and 0.8 for women. By 2005, the U.S. incidence of HCC per 100,000 people increased to 7.9

for men and 2.3 for women

6

. Although the rate of HCC is increasing in the U.S., the incidence rates in other parts of theworld are substantially higher. South-Eastern Asia has one of the highest HCC incidence rates in the world. Foexample, in China, the incidence of liver cancer is 35.2/100,000 for males and 13.3/100,000 for females

7.

1 Zhang Y, Wang S, Li D., Zhnag J, Gu D, Zhu Y, & He F (2011). A sys tems biology-based classifier for hepatocellular carcinoma diagnosis. PLoS One. 2011;6(7):e22426. Epub 2011 Jul 28.2

Simonetti RG, Liberati A, Angiolini C, Pagliaro L. Treatment of hepatocellular carcinoma: a systematic review of randomized controlled trials. Ann Oncol. 1997 Feb;8(2):117-36.3

Thomas MB, et al. Hepatocellular carcinoma: consensus recommendations of the National Cancer Institute Clinical Trials Planning Meeting. J Clin Oncol. 2010 Sep 1;28(25):3994-4005. Epub 2010Aug 2.4

Parkin DM, Bray F, Ferlay J, Pisani P. Global cancer statistics, 2002. CA Cancer J Clin. 2005 Mar-Apr;55(2):74-108.5

Perz JF, Armstrong GL, Farrington LA, Hutin YJ, Bell BP. The contributions of hepatitis B virus and hepatitis C virus infections to cirrhosis and primary liver cancer worldwide. J Hepatol. 2006Oct;45(4):529-38. Epub 2006 Jun 23.6

Altekruse SF, McGlynn KA, Reichman ME. Hepatocellular carcinoma incidence, mortality, and survival trends in the United Stat es from 1975 to 2005. J Clin Oncol. 2009 Mar 20;27(9):1485-91. Epub2009 Feb 17.7 http://www.cancer.org/Research/CancerFactsFigures/GlobalCancerFactsFigures/index

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 7/31

RODMAN & RENSHAW EQUITY RESEARCH

Although the HCC incidence is high, in south-eastern Asia, declines in the incidence rate of HCC have been reported foregions of China and Japan, which are thought to be due primarily to public health-related measures. It is alsonoteworthy that a Hepatitis C vaccination program, which began in Taiwan during the 1980’s, has led to a significanreduction in HCC rates of children from 0.70/100,000 to 0.36/100,000

8.

Figure 2: Annual Incidence and Mortality of Liver Cancer Throughout the World

*Note that HCC accounts for 70-90% of Liver Cancer Source: GLOBOCAN

In terms of survival, the statistics appear to be improving as well. For example, in 1992, the United States 5-yea

survival rate was 8%9

, and by 2010, the 5-year survival rate increased to approximately 20% (Figure 3). Despite modesincreases in survival over the past 20 years, the overall 5-year survival rate of HCC remains below 15% throughout theworld

10, highlighting the need for more effective treatment options.

Source: American Cancer Society (ref: http://www.cancer.org/Cancer/LiverCancer/DetailedGuide/liver-cancer-survival-rates)

Tumor Staging

HCC staging is an important factor used for prognosis and planning the course of patient management. One stagingsystem that has gained wide acceptance is the Barcelona-Clinic Liver Cancer (BCLC) staging, which aims to classifypatients by tumor stage, liver function, physical status, and cancer related symptoms

11. The BCLC classification system

was also designed to incorporate prognosis estimation and potential treatment advancements (Figure 4).

8Röcken C, Carl-McGrath S. Pathology and pathogenesis of hepatocellular carcinoma. Dig Dis. 2001;19(4):269-78.

9 Altekruse SF, McGlynn KA, Reichman ME. Hepatocellular carcinoma incidence, mortality, and survival trends in the United States from 1975 to 2005. J Clin Oncol. 2009 Mar 20;27(9):1485-91. Epub2009 Feb 17.10 http://www.cancer.org/Research/CancerFactsFigures/GlobalCancerFactsFigures/index11 Pons F, Varela M, Llovet JM. Staging systems in hepatocellular carcinoma. HPB (Oxford). 2005;7(1):35-41.

Stage

5-year

Relative

Survival Rate

Localized 21%

Regional (Turmors in multple lobes) 6%

Distant (Metastasis) 2%

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 8/31

RODMAN & RENSHAW EQUITY RESEARCH

Under the BCLC staging system, stage 0 and stage A patients are diagnosed as having early stage disease and areeligible for tumor resection, a curative treatment. Patients with stage A disease may also qualify for RadiofrequencyAblation (RFA; see below for description). Patients with multiple nodule non-invasive tumors are considered tumostage B. Patients with tumors that have vascular involvement or with metastasis outside the liver are considered tumostage C, and may be eligible for chemotherapy or participation in novel clinical trials. Finally, patients with significantumor burden and impaired physical status are considered stage D and receive palliative care

12. It is noteworthy that the

BCLC incorporates the Child-Pugh score, a system that ranks liver disease severity on the basis of results from liver

function tests. Child-Pugh scores are grouped into three categories: class A, B, and C. Child Pugh class-A correlateswith early stage HCC whereas a Child Pugh class-B correlates with Intermediate to advanced HCC, and Child Pughclass-C correlates with end stage HCC. The Child Pugh scores are calculated on five clinical parameters of livefunction, and the scores range from more liver function and longer survival (Child Pugh class-A) to less liver function andlower overall survival (Child Pugh class-C)

1314.

Figure 4: Barcelona Clinic Liver Cancer Staging Classification and Treatment Schedule

Source 1516

THERAPEUTIC OPTIONS

Liver transplantation can significantly improve patient survival, however, transplantation is limited to patients with earlystage HCC and is restricted by the availability of donor tissue. Surgical resection is the preferred form of HCCtreatment, however only 10-30% of patients are eligible for complete resection. Several factors determine eligibility foresection including, the health of the liver, the location of the tumor within the liver, and the total number of tumorsthroughout the liver. If complete resection is not practical then partial resection may be combined with additionatherapy. Early, intermediate, and advanced tumors, not suitable for surgical resection or transplant, may be eligible folocalized treatment (Figure 5).

12 Llovet JM, Fuster J, Bruix J; Barcelona-Clínic Liver Cancer Group. The Barcelona approach: diagnosis, staging, and treatment of hepatocellular carcinoma. Liver Transpl. 2004 Feb;10(2 Suppl1):S115-20.13

Pugh RN, Murray-Lyon IM, Dawson JL, Pietroni MC, Williams R. Transection of the oesophagus for bleeding oesophageal varices. Br J Surg. 1973 Aug;60(8):646-9.14 Schepke M, Roth F, Fimmers R, Brensing KA, Sudhop T, Schild HH, Sauerbruch T. Comparison of MELD, Child-Pugh, and Emory model for the prediction of survival in patients undergoingtransjugular intrahepatic portosystemic shunting. Am J Gastroenterol. 2003 May;98(5):1167-74. 15 Zhang ZM, Guo JX, Zhang ZC, Jiang N, Zhang ZY, Pan LJ. Therapeutic options for intermediate-advanced hepatocellular carcinoma. World J Gastroenterol. 2011 Apr 7;17(13):1685-9.16 Llovet JM, et al. Design and endpoints of clinical trials in hepatocellular carcinoma. J Natl Cancer Inst. 2008 May 21;100(10):698-711. Epub 2008 May 13.

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 9/31

RODMAN & RENSHAW EQUITY RESEARCH

Figure 5: Therapeutic Options for Hepatocellular Carcinoma

Source: 17

Liver Transplantation and Resection

Liver transplantation is an effective treatment for HCC as it allows for the removal of the tumor tissue and it alsoreplaces the non-cancerous diseased liver with healthy tissue. Liver transplantation is a high-risk procedure reservedfor early stage HCC patients, and is limited by the availability of donor organs.

An alternative to transplantation is resection. As discussed above, resection is an effective treatment for HCC andinvolves the radical removal of the portion of liver that contains the tumor. The goal of the radical resection is to removethe main tumor as well as any nearby marginal tumor cells that may not be detected. With later stage disease radicaresection may not be possible and palliative resection may be performed. Palliative resection is used in intermediate toadvanced disease as a means to surgically remove as many HCC nodules as possible while still preserving liverfunction. Palliative resection may be used in combination with therapies such as RFA, or may be followed bychemotherapy.

Cryosurgical Ablation

Cryosurgical ablation is a technique that involves freezing-thawing of tumor tissue. Needles are inserted into the tumor

argon-helium gas is then passed through the needles to freeze the tumor tissue (<-140°C). The freezing process resultsin the rapid formation of ice crystals inside and outside of the cells, after which the tumor tissue is thawed. The overalfreeze-thaw process disrupts the structural integrity of the HCC cells and results in tissue necrosis. Cryosurgicaablation is indicated for HCC tumors with <3 nodules and < 5cm in diameter. Alternatively, it may also be used to treaone HCC nodule that is >5cm in diameter.

Embolization

Transcatheter arterial chemoembolization (TACE) involves delivery of a chemotherapeutic agent directly to the hepaticartery. TACE takes advantage of the unique nature of blood supply to the liver and to HCC tumors. The liver receivesapproximately 70% of its blood supply from the portal vein and 30% of its blood supply from the hepatic artery.However, in HCC, the tumor is thought to derive 90% of its blood supply from the hepatic artery and 10% from the portavein. As a result, the injection of chemotherapy into the hepatic artery results in a higher accumulation of thechemotherapy in the tumor. Following the chemotherapy injection, the artery closed off (embolized), through theinjection of an artery blocking agent, which prevents the chemotherapy from being rapidly cleared from the area of thetumor. TACE is indicated for intermediate to advanced HCC, but it is not considered a curative procedure

18.

17Zhang ZM, Guo JX, Zhang ZC, Jiang N, Zhang ZY, Pan LJ. Therapeutic options for intermediate-advanced hepatocellular carcinoma. World J Gastroenterol. 2011 Apr 7;17(13):1685-9.

18 Sergio A, et al. Transcatheter arterial chemoembolization (TACE) in hepatocellular carcinoma (HCC): the role of angiogenesis and invasiveness. Am J Gastroenterol. 2008 Apr;103(4):914-21. Epub2008 Jan 2.

Type of Treatment Indication

Liver TransplantationSingle tumor ≤ 5 cm or 2-3 tumors ≤ 3 cm and no macrovascular invasion

no extrahepatic spread

Radical ResectionHCC with a Single large HCC nodule or multiple HCC with 3 or less nodule

in one lobe of the liver

Palliative ResectionHCC with 3-5 tumor nodules, multiple HCC with nodules localized in 2-3

adjacent segments of the liver, or invaded organs around the liver

Cryosurgical AblationHCC with nodule ≤ 3 nodules < 5 cm in diameter or a nodule > 5 cm with

irregular margins

Transcatheter Arterial Chemoebolization

(TACE)Intermediate to advanced HCC that is considered inoperable

Portal Vein EmbolizationIntermediate to advanced HCC prior to surgical resection or in comination

with TACE

Sorafenib / Nexavar®Oral medication for the treatment of advanced unresectable HCC; FDA

Approved

Radiofrequency AblationHCC with ≤ 5 nodules each < 3cm in diameter, and can be used along wit

surgical resection

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 10/31

RODMAN & RENSHAW EQUITY RESEARCH

Portal vein embolization (PVE) is also used for patients with HCC. During the PVE procedure, a catheter is used todeliver particles that close off portal veins in the liver. PVE can also be used in a pre-surgical setting, prior to resectionin an attempt to increase the volume and function of the liver. In the pre-surgical setting, blocking of a portal vein leadsto increased hepatocyte proliferation, which leads to an increase in normal tissue. Alternatively, PVE can also be usedin combination with TACE to block the blood supply in the tumor and prevent the chemotherapy from rapidly exiting thetumor.

Sorafenib

Sorafenib is a FDA approved chemotherapeutic agent, currently being marketed by Bayer (BAY; Not Rated) and Onyxx(ONXX; Not Rated) for the systemic treatment of unresectable HCC. Sorafenib is a kinase inhibitor that has activityagainst multiple kinases that are responsible for cell proliferation and survival, including B-RAF, C-RAF, and VEGFR-2Although sorafenib has activity against multiple targets, the exact target that is responsible for its clinical activity is stilunknown. Despite the uncertainty regarding the drugs exact molecular mechanism of action, a Phase 3 trial of sorafenibrevealed that the drug provided a delay in radiological progression of HCC compared to placebo (5.5 months vs. 2.8months; p<0.001). Additionally, overall survival was significantly increased in the sorafenib treated patients compared tothe placebo group (10.7 months vs. 7.9 months; p<0.001)

19.

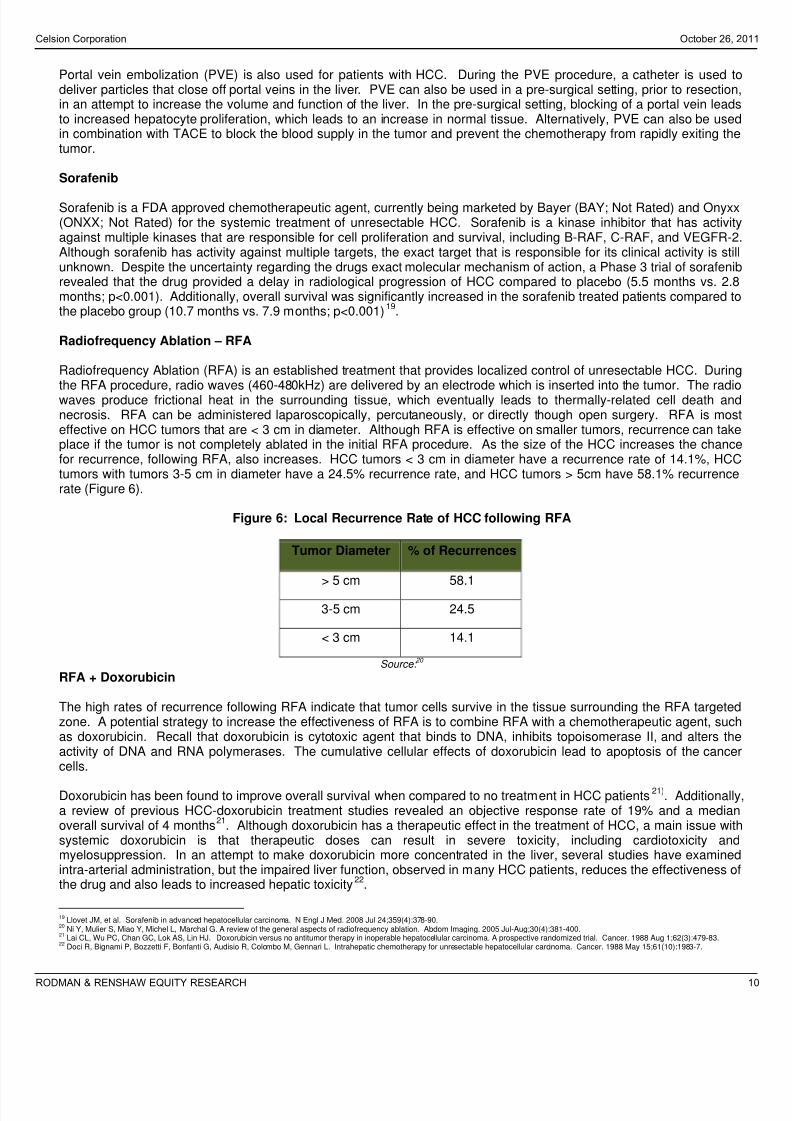

Radiofrequency Ablation – RFA

Radiofrequency Ablation (RFA) is an established treatment that provides localized control of unresectable HCC. Duringthe RFA procedure, radio waves (460-480kHz) are delivered by an electrode which is inserted into the tumor. The radiowaves produce frictional heat in the surrounding tissue, which eventually leads to thermally-related cell death andnecrosis. RFA can be administered laparoscopically, percutaneously, or directly though open surgery. RFA is moseffective on HCC tumors that are < 3 cm in diameter. Although RFA is effective on smaller tumors, recurrence can takeplace if the tumor is not completely ablated in the initial RFA procedure. As the size of the HCC increases the chancefor recurrence, following RFA, also increases. HCC tumors < 3 cm in diameter have a recurrence rate of 14.1%, HCCtumors with tumors 3-5 cm in diameter have a 24.5% recurrence rate, and HCC tumors > 5cm have 58.1% recurrencerate (Figure 6).

Figure 6: Local Recurrence Rate of HCC following RFA

Tumor Diameter % of Recurrences

> 5 cm 58.1

3-5 cm 24.5

< 3 cm 14.1

Source: 20

RFA + Doxorubicin

The high rates of recurrence following RFA indicate that tumor cells survive in the tissue surrounding the RFA targetedzone. A potential strategy to increase the effectiveness of RFA is to combine RFA with a chemotherapeutic agent, suchas doxorubicin. Recall that doxorubicin is cytotoxic agent that binds to DNA, inhibits topoisomerase II, and alters theactivity of DNA and RNA polymerases. The cumulative cellular effects of doxorubicin lead to apoptosis of the cancecells.

Doxorubicin has been found to improve overall survival when compared to no treatment in HCC patients21)

. Additionallya review of previous HCC-doxorubicin treatment studies revealed an objective response rate of 19% and a medianoverall survival of 4 months

21. Although doxorubicin has a therapeutic effect in the treatment of HCC, a main issue with

systemic doxorubicin is that therapeutic doses can result in severe toxicity, including cardiotoxicity andmyelosuppression. In an attempt to make doxorubicin more concentrated in the liver, several studies have examinedintra-arterial administration, but the impaired liver function, observed in many HCC patients, reduces the effectiveness othe drug and also leads to increased hepatic toxicity

22.

19 Llovet JM, et al. Sorafenib in advanced hepatocellular carcinoma. N Engl J Med. 2008 Jul 24;359(4):378-90.20

Ni Y, Mulier S, Miao Y, Michel L, Marchal G. A review of the general aspects of radiofrequency ablation. Abdom Imaging. 2005 Jul-Aug;30(4):381-400. 21 Lai CL, Wu PC, Chan GC, Lok AS, Lin HJ. Doxorubicin versus no antitumor therapy in inoperable hepatocellular carcinoma. A prospective randomized trial. Cancer. 1988 Aug 1;62(3):479-83.22 Doci R, Bignami P, Bozzetti F, Bonfanti G, Audisio R, Colombo M, Gennari L. Intrahepatic chemotherapy for unresectable hepatocellular carcinoma. Cancer. 1988 May 15;61(10):1983-7.

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 11/31

RODMAN & RENSHAW EQUITY RESEARCH

One strategy to limit the toxicity of doxorubicin is to encapsulate the compound into liposomes, thereby preventing thedoxorubicin from being systemically released throughout the body. Following intravenous injection, the liposomes couldpass through the circulatory system and get filtered by the liver where they should passively accumulate

23. High loca

concentrations of liposomal doxorubicin have previously been shown to sensitize liver tissue to thermal necrosis andpotentially increase the size of the RFA ablation zone. Although liposomes provide a system to deliver the drugs to aspecific tissue, one potential limitation with traditional liposomes is that the cytotoxic effect of the drug may be limited bythe slow release of the drug from the liposome. To circumvent the issue of slow drug release from traditional liposomes

Celsion has created a heat-sensitive liposome / doxorubicin complex known as ThermoDox.

ThermoDox

ThermoDox is a complex of doxorubicin combined with heat sensitive (lyso-thermosensitive) liposomes. The liposomesconsist of three synthetic phospholipids: DPPC (1,2-dipalmitoyl-sn-glycero-3-phosphocholine): MPPC (1-palmitoyl-2-hydroxy-sn-glycero-3-phosphocholine): DSPE-PEG-2000 (1,2-distearoyl-sn-glycero-3-phosphoethanol-amine-Npolyethylene glycol 2000)

24. The ratio of the specific phospholipids has been optimized to ensure that ThermoDox

rapidly releases doxorubicin upon exposure to temperatures ≥39.5 C (Figure 7). ThermoDox is injected intravenouslyand as a result of the liposome size, the ThermoDox passively accumulates into the liver. Following the ThermoDoxinfusion, the liver is then subjected to the RFA procedure, which heats the target tissue and leads to the release of thedoxorubicin from the ThermoDox complex.

Recall that RFA creates an ablation zone of necrosis. Following RFA, in the presence of ThermoDox, the doxorubicin isreleased and subsequently forms a concentration gradient in the margin surrounding the ablation zone, known as thethermal zone. The release of doxorubicin into the thermal zone kills tumor cells in the region, and as a result, effectivelyexpands the treatment area when compared to RFA alone (Figure 8). The expansion of the treatment zone should beclinically significant as it provides the opportunity to kill small populations of tumor cells that would have been untreatedwith traditional RFA, and could serve as sites for tumor recurrence.

Figure 7: ThermoDox: Heat Opens the Liposomal Membrane Borders and Releases Drug Directly to the Tumor

Source: Celsion Presentation

Figure 8: ThermoDox and RFA May Reduce the Potential for Recurrence at the Treatment Site

Source: Celsion Presentation

23 Ponce AM, Vujaskovic Z, Yuan F, Needham D, Dewhirst MW. Hyperthermia mediated liposomal drug delivery. Int J Hyperthermia. 2006 May;22(3):205-13.24 Poon RT, Borys N. Lyso-thermosensitive liposomal doxorubicin: an adjuvant to increase the cure rate of radiofrequency ablation in liver cancer. Future Oncol. 2011 Aug;7(8):937-45.

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 12/31

RODMAN & RENSHAW EQUITY RESEARCH

EARLY STAGE DEVELOPMENT OF THERMODOX

Preclinical studies examined ThermoDox in combination with microwave induced hyperthermia in canines with sarcomaor carcinoma. ThermoDox was given for three treatments and each treatment was separated by three weeks. In thestudy, the most serious side effects were Grade 4 neutropenia, and one animal died due to liver failure, which may havebeen due to the treatment. At the end of the study, 30% of the canines had a partial response to the drug and 60% othe canines had stable disease

25. Based on the results in treatment of canine tumors, ThermoDox was evaluated in

humans.

Phase 1 Trial of ThermoDox

In 2007, Celsion began a Phase 1 dose escalation trial in which patients with HCC or metastatic liver cancer weretreated with RFA and ThermoDox. The Phase 1 trial consisted of 24 patients, 9 patients with primary HCC and 15patients with liver tumors that had metastasized to and from other organs. Fifteen minutes prior to the RFA, patientswere treated with a single 30-min IV infusion of ThermoDox at 20, 30, 40, 50, or 60 mg/m

2. At 60 mg/m

2, two dose

limiting toxicities were observed: grade 3 alanine aminotransferase increase (a sign of liver damage), and grade 4neutropenia (loss of neutrophils), and as a result, the maximum tolerated dose (MTD) of ThermoDox was determined tobe 50 mg/m

2. In terms of safety, the most common grade 3+ events were abnormalities in the levels of the live

enzymes aspartate aminotransferase (40%) and alanine aminotransferase (32.7%), neutropenia (29.1%), leucopenia(12.7%), and lymphopenia (9.1%)

26.

In the Phase 1 study, the median time to treatment failure for patients receiving at least 50 mg/m 2 was 374 dayswhereas patients receiving less than the MTD of 50 mg /m

2had an 80 day median time to treatment failure (p= 0.038

Figure 9). A sub-group analysis of the 9 HCC patients in the Phase 1 study revealed that the “time to progressionincreased from 156 days at doses ≤ 40 mg/m

2to 337 days at doses ≥ 50 mg/m

2days (Figure 10). Taken together, the

Phase 1 data indicate that RFA combined with ThermoDox is safe and produces a significant dose response effect inliver tumors.

Figure 9: Phase 1 RFA / ThermoDox Time to Treatment Failure Correlates with Dose Level in Liver Cancer

Source: 26

Figure 10: Phase 1 Sub-Group Analysis of the Patients with HCC

Source: Celsion Presentation

25 Hauck ML et al. Phase I trial of doxorubicin-containing low temperature sensitive liposomes in spontaneous canine tumors. Clin Cancer Res. 2006 Jul 1;12(13):4004-10.26 Poon RT, Borys N. Lyso-thermosensitive liposomal doxorubicin: a novel approach to enhance efficacy of thermal ablation of liver cancer. Expert Opin Pharmacother. 2009 Feb;10(2):333-43.

Factor Failed Censored*Median Time To

Treatment Failurep-Value

ThermoDox Dose< 50 mg/m

215 0 80

≥ 50 mg/m2

5 4 3740.038

Days

ThermoDox

Dose

(mg/m2)

Tumor Size

(cm)

RFA Type:

P= Percutaneous

OS=Open Surgical

Time

(days)

Treatment

Failure

Median Time To

Treatment Failure

<40 mg/m2

Median Time To

Treatment Failure

>50 mg/m2

20 3.1 P 80 Y

30 1.7 OS 188 Y

30 2.9 OS 125 Y

40 1.7 OS 85 Y

40 2.1 OS 427 Y

40 3.1 OS 355 Y

50 6.5 P 374 Y

60 Not Reported P 122 N

60 2.5 OS 337 N

337

156

125

346

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 13/31

RODMAN & RENSHAW EQUITY RESEARCH

It is noteworthy that approximately 50% of the treated tumors were 3.8-6.5 cm in diameter, a size that would traditionallybe considered too large to treat with RFA (RFA is indicated for tumors < 3m in diameter). In fact, 4 patients from thePhase 1 trial had tumors > 5 cm. Two of these patients received a ThermoDox treatment of < 50 mg/m

2and two

patients received ThermoDox at ≥ 50 mg/m2. Of the two patients that received less than < 50 mg/m

2of ThermoDox, one

patient experienced treatment failure at day 29 and the other patient experienced treatment failure on day 93. Of thetwo patients treated with ≥ 50 mg/m

2, one patient experienced treatment failure at day 261 and the other patien

experienced treatment failure on day 374. Although no statistical conclusions can be drawn from data of the tumors >5

cm, the data suggest a relationship between ThermoDox dose and patient response in HCC tumors > 3 cm.

PHASE 3 CELSION TRIAL – HEAT STUDY

Based on the promising Phase 1 trial, Celsion was allowed to begin a Phase 3 trial for RFA in combination withThermoDox. The Phase 3 trial, known as the HEAT Study, is a randomized, double-blind, controlled study that wilcompare RFA + ThermoDox to RFA alone for the treatment of unresectable HCC. The HEAT Study is being carried ouunder an FDA Special Protocol Assessment, and the trial has been granted Fast Track Designation by the FDA. TheHEAT Study involved 76 clinical sites in 11 countries. The pre-planned enrollment objective of the study was 600patients (enrollment objective achieved in August 2011).

To be eligible for the trial, patients must have ≤ 4 HCC tumors, one tumor must be ≥ 3 cm, an d no tumor can be >7 cmin diameter. The selection of patients for this study is noteworthy as it requires that patients have at least 1 HCC tumothat is > 3cm. Recall that tumors > 3cm have a greater chance of recurrence than tumors < 3 cm following RFA alonePatients with Child-Pugh Class A or Class B status are eligible for the trial. Under the trial guidelines, the RFAprocedure can be performed percutaneously, laproscopically, or surgically. Patients are stratified according to RFAprocedure and tumor size (Figure 11).

The primary endpoint for the HEAT Study is progression free survival (PFS). The secondary endpoints for the trial areoverall survival, time to local recurrence, and safety. The experimental arm of the trial will receive ThermoDox (50mg/m

2) 15 minutes before the RFA procedure. The control arm of the study will receive a placebo infusion 15 minutes

prior to the RFA procedure. Following the RFA procedure, patients will be monitored with CT scans at 1, 3, 5, 7, 9, and12 months. After the initial 12 months, CT scans will be collected every three months until withdrawal from the study.

The study calls for an independent Data Monitoring Committee efficacy analysis following completion of enrollment andafter approximately 190 PFS events have been confirmed. For the primary endpoint, 380 PFS events will trigger theprimary endpoint analysis. Additionally, the secondary endpoint, overall survival, will be reached following 372 deaths.

Figure 11: Overview of the HEAT Study

Source: Celsion Presentation

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 14/31

RODMAN & RENSHAW EQUITY RESEARCH

Recurrent Chest Wall (RCW) Breast Cancer

Recurrent chest wall (RCW) breast cancer occurs in patients that have previously had a lumpectomy or a mastectomyfor breast cancer. Chest wall recurrence is difficult to treat and by many is considered a poor prognostic factor. RCWbreast cancer is defined as recurrence of breast cancer on or in the chest wall near the site of the lumpectomy ormastectomy, and the cancer is thought to develop from breast cancer cells that were not removed or killed following theoriginal treatment regimen. Management of the disease is difficult due to the lack of successful treatment options, andas a result, the 5-year survival rate of RCW breast cancer is approximately 30% to 50%

27.

Incidence, Prevalence & Survival Statistics

It is estimated that, annually in the U.S., 230,000 women will be diagnosed with breast cancer28

. Approximately 50% othese women will undergo a mastectomy as part of their treatment plan

29. The rate of locally recurrent breast cance

after mastectomy is estimated to be between 4% and 20%27

, which translates to approximately 5,200 to 26,000 cases oflocally recurrent breast cancer in the US alone. Due to the frequent appearance of metastasis the 5-year survival rate oRCW breast cancer is estimated to be 30% to 50%

27.

TRADITIONAL RCW TREATMENT

The World Health Organization (WHO) recommends the following treatment for local RCW breast cancer, surgicaresection, followed by radiation and subsequent systemic chemotherapy or hormone therapy. While this treatment plan

may be effective in select patients, the low 5-year survival of RCW breast cancer indicates that more effectivetreatments are required to manage this disease.

Surgery

Surgical treatment of RCW breast cancer will depend on the initial course of disease management. If a lumpectomywas performed during the initial treatment, then mastectomy is indicated for RCW breast cancer treatment. If amastectomy was performed during the initial treatment, then wide local excision of the tumor is recommended.Depending on the severity of the disease, the resection may involve the removal of rib bones as well as portions of thesternum. Treatment of RCW breast cancer with additional surgery alone provides limited control of the disease and theoverall 5-year local control rate following surgery alone is 33%

30.

Radiation

Following RCW breast cancer resection, the addition of radiation has demonstrated superior local control (48%)compared to surgery alone (34%), 5-years post treatment

31. If the RCW breast cancer is not suitable for resection then

radiation is recommend to control the disease. Although radiation provides a clinical benefit, the use of radiation canincrease safety concerns in patients that have been previously exposed to radiation treatments.

Hyperthermia

To increase the effectiveness of other therapeutic modalities, such as radiation, hyperthermia has been used in RCWbreast cancer treatment. In the RCW treatment setting, hyperthermia is defined as temperatures above normaphysiological conditions (40-45 ۟ C). In the case of radiation-based therapy, hyperthermia is thought to make the cancecells more susceptible to the harmful effects of the radiation. Hyperthermic conditions affect cell division and inhibispecific aspects of DNA repair, thereby affecting the ability of the cancer cells to recover from therapeutic damage. Infact, the combination of hyperthermia and radiation led to a 19% increase in the overall complete response ratecompared to patients receiving radiation alone32.

27Downey RJ, et al. Chest wall resection for locally recurrent breast cancer: is i t worthwhile? J Thorac Cardiovasc Surg. 2000 Mar;119(3):420-8.

28National Cancer Institute; http://www.cancer.gov/cancertopics/types/breast

29 Coombes RC, et al. N Engl J Med. 2004 Mar 11;350(11):1081-92.A randomized trial of exemestane after two to three years of tamoxifen therapy in postmenopausal women with primary breastcancer. N Engl J Med. 2004 Mar 11;350(11):1081-92. 30

Dahlstrøm KK, Andersson AP, Andersen M, Krag C. Wide local excision of recurrent breast cancer in the thoracic wall. Cancer. 1993 Aug 1;72(3):774-7.31 Schwaibold F, Fowble BL, Solin LJ, Schultz DJ, Goodman RL. The results of radiation therapy for isolated local regional recurrence after mastectomy. Int J Radiat Oncol Biol Phys. 1991Jul;21(2):299-310.32 Vernon CC, et al. Radiotherapy with or without hyperthermia in the treatment of superficial localized breast cancer: results from five randomized controlled trials. International CollaborativeHyperthermia Group. Int J Radiat Oncol Biol Phys. 1996 Jul 1;35(4):731-44.

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 15/31

RODMAN & RENSHAW EQUITY RESEARCH

Chemotherapy

Chemotherapy is recommended for breast cancer recurrence. Several systemic chemotherapeutic drugs are availablefor the treatment of breast cancer, including cyclophosphamide, methotrexate, 5-fluorouracil, doxorubicin, and othersDepending on the diagnosis, these drugs may be used, as single agents, or in combination with each other. However apotential problem with chemotherapy is that the toxicity of the drugs can limit their therapeutic potential. It is noteworthythat although systemic chemotherapy has been approved for breast cancer, no chemotherapeutic agents have beenspecifically approved for the treatment of RCW breast cancer. While studies have demonstrated the effectiveness o

RCW therapies, such as radiation and hyperthermia, more detailed studies are needed to identify chemotherapeuticagents that may benefit patients with RCW breast cancer. For example, a previous study examined the impact ohyperthermia and liposomal doxorubicin on patients with RCW breast cancer

33. Although the study population was

small, the combinatorial treatment with liposomal doxorubicin was well tolerated and the data was suggestive of apositive clinical outcome.

THERMODOX – HOPE FOR RCW BREAST CANCER TREATMENT

Given the low survival rate of patients with RCW breast cancer, Celsion is evaluating the company’s heat sensitiveliposomal doxorubicin complex, ThermoDox, in combination with hyperthermia for the treatment of patients with RCWbreast cancer. ThermoDox is relevant for the treatment of RCW breast cancer due to the fact that the active drugdoxorubicin, is approved for the treatment of breast cancer. Additionally, the ability to thermally control the release odoxorubicin allows for doxorubicin to be administered to the site of the breast tumor while minimizing the release of thedrug throughout the body.

For RCW breast cancer treatment, ThermoDox will be injected intravenously. The doxorubicin will be released when theThermoDox enters the hyperthermic chest wall tissue. The chest wall tissue is heated with an external hyperthermiadevice that is placed on the patient’s chest. It is important to note that the hyperthermia device heats the tissue to atemperature that is suitable to stimulate the release of ThermoDox, but the temperature is much lower (40-42 C) thanthe temperature required in the previously mentioned RFA studies.

Although doxorubicin is known as a potent chemotherapeutic agent, it is noteworthy that microwave hyperthermia hasalso been shown to kill breast cancer cells

34. Breast cancer cells are presumed to have greater water content than the

cells in the surrounding normal tissue, and as a result the tumor retains more heat, which ultimately leads to tumor cel

death. Heating cancer cells with a microwave device for 60 minutes at 43C has been found to kill tumor cells, andCelsion expects that the combination of microwave hyperthermia and ThermoDox will have a greater effect than othenon-heat activated liposome based drugs.

33Park J, Stauffer P, Diederich C, et al. Pegylated Liposomal Doxorubicin plus Hyperthermia for Metastatic Breast Cancer of the Chest Wall. Proceedings from the 23rd annual Chemotherapy

Foundation Symposium. November 2005. New York. Abstract #53.34 Celsion (CLSN)10-K 2010

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 16/31

RODMAN & RENSHAW EQUITY RESEARCH

Duke Phase 1 Trial of ThermoDox for RCW Breast Cancer

In April of 2006, Duke University began enrollment of a Phase 1 trial of ThermoDox in RCW Breast Cancer. The studyplanned to enroll 30 patients in the trial. The study was to enroll cohorts of 3-6 patients at escalating doses oThermoDox until an MTD Is determined. Duke has reported 16/16 patients had a clinical response of stable diseasepartial response, or complete response. Of note, at the 30 mg/m

2dose, 6 of 6 patients had a clinical response, and 2 of

the 6 patients had a complete response after 4 treatments with ThermoDox (Figure 12).

Figure 12: Duke Phase 1 Data: 30 mg/m2

Dose of ThermoDox Induces a Complete Response

Source: Celsion Presentation

DIGNITY: Phase 1/2 Study

In 2009, Celsion initiated a dose-escalating ThermoDox Phase 1/2 study, known as DIGNITY, for patients with RCWbreast cancer. The trial planned to enroll 109 patients at 10 sites throughout the U.S. The primary endpoint of the triais durable complete local response. A durable complete local response will be achieved if the initial chest wall tumor(sare no longer detected for at least three months following the initial treatment. In the Dignity Study, patients will be givenThermoDox intravenously over a 30 minute period followed by hyperthermia treatment (Figure 13).

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 17/31

RODMAN & RENSHAW EQUITY RESEARCH

Figure 13: Protocol for the DIGNITY Study

Source: Celsion Brochure

During the dose escalation part of the study, patients received up to 6 ThermoDox / hyperthermia treatments at 21-day

intervals. Dosing began at 40 mg/m2, a dose that produced clinical activity as well as a satisfactory safety profile. The

subsequent cohort of patients received 6 ThermoDox / hyperthermia treatments at 50 mg/m2

(MTD). Following

completion of the 50 mg/m2

cohort, a Drug Safety Monitoring Board (DSMB) recommended that the Phase 1/2 tria

advance to a Phase 2 trial at a dose of 50 mg/m2. Celsion is currently in process of planning the initiation of the Phase 2

portion of the trial in 1Q12 (Figure 14).

Figure 14: Overview of the DIGNITY Study

Source: Celsion Presentation

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 18/31

RODMAN & RENSHAW EQUITY RESEARCH

Next Clinical Study: Colorectal Liver Metastasis

Incidence, Prevalence & Survival Statistics

Colorectal cancer (CRC) is the fourth most common cancer, worldwide it accounts for an estimated 600,000 deathseach year

35. In the U.S. approximately 142,000 cases of CRC are diagnosed each year and 51,000 will die from the

disease. It is estimated that approximately 60% of CRC patients will develop liver metastasis throughout the course o

the disease 36

.

Treatment of CRC Liver Metastasis

Treatment of CRC liver metastasis may involve surgical resection, surgical alternatives (RFA; Radio FrequencyAblation), and chemotherapy. Liver resection is considered the primary choice of liver cancer treatment and it providesa 5-year survival rate of 20-50%

37. However, only 10-25% of the liver metastases can be removed surgically

3839

Chemotherapy plays a significant role in the management of CRC, as chemotherapeutic agents may shrink the tumorsize and make the tumors more amenable to surgical removal

40. In the case of inoperable CRC liver metastasis, the

primary role of chemotherapy is to provide palliative care and prolong life41 .

Although surgical resection is the preferred form of CRC liver metastasis treatment, RFA is used to treat patients withunresectable liver metastasis. RFA prolongs overall survival compared to chemotherapy alone in the treatment of CRCliver metastasis. RFA has also been shown to decrease metastatic tumor size, which subsequently allows for tumoresection42.

ThermoDox and RFA Offer Potential to Treat CRC Liver Metastasis – Phase 2 Trial (Ablate Study)

Celsion is evaluating the company’s heat sensitive liposomal doxorubicin complex, ThermoDox, in combination with

RFA for the treatment of metastatic CRC. The combination of ThermoDox and RFA is relevant for the treatment of CRC

due to the fact the treatment has been shown to be effective for the treatment of liver tumors. Additionally, a componen

of the treatment regimen, RFA, has previously been shown to be effective in prolonging the survival of patients with

metastatic CRC. The ability to thermally control the release of doxorubicin allows for doxorubicin to be administered to

metastatic liver tumor while minimizing the release of the drug throughout the body. It is also important to note that 24

metastatic liver cancer patients, from 9 primary sites, have been studied in two separate Phase 1 trials. These Phase 1

results revealed local disease control and they also suggested a dose-response relationship. Taken together, theprevious RFA and ThermoDox data indicate that further studies are needed to define the relationship between RFA and

ThermoDox for the treatment of patients with metastatic colorectal liver cancer.

Celsion has initiated plans for a Phase 2 study of ThermoDox in CRC liver cancer patients. The study will involve

multiple centers and consist of two arms; RFA alone and RFA in combination with ThermoDox. The FDA has agreed to

the Phase 2 protocol and Celsion predicts that the trial will begin enrolling patients in 4Q11.

35 World Health Organization Cancer Fact Sheet. February 2011. http://www.who.int/mediacentre/factsheets/fs297/en/ 36

Lin AY, et al. Comparative profiling of primary colorectal carcinomas and liver metastases identifies LEF1 as a prognostic biomarker. PLoS One. 2011 Feb 24;6(2):e16636.37

Kavlakoglu B, Ustun I, Oksuz O, Pekcici R, Ergocen S, Oral S. Surgical treatment of liver metastases from colorectal cancer: experience of a single institution. Arch Iran Med. 2011 Mar;14(2):120-5.38 Abdalla EK, Vauthey JN, Ellis LM, Ellis V, Pollock R, Broglio KR, Hess K, Curley SA. Recurrence and outcomes following hepatic resection, radiofrequency ablation, and combined resection/ablationfor colorectal liver metastases. Ann Surg. 2004 Jun;239(6):818-25; discussion 825-7.39

Kavlakoglu B, Ustun I, Oksuz O, Pekcici R, Ergocen S, Oral S. Surgical treatment of liver metastases from colorectal cancer: experience of a single institution. Arch Iran Med. 2011 Mar;14(2):120-5.40 Tsoulfas G, Pramateftakis MG, Kanellos I. Surgical treatment of hepatic metastases from colorectal cancer. World J Gastrointest Oncol. 2011 Jan 15;3(1):1-9.41

Goodwin RA, Asmis TR. Overview of systemic therapy for colorectal cancer. Clin Colon Rectal Surg. 2009 Nov;22(4):251-6.42 Stang A, Fischbach R, Teichmann W, Bokemeyer C, Braumann D. A systematic review on the clinical benefit and role of radiofrequency ablation as treatment of colorectal liver metastases. Eur JCancer. 2009 Jul;45(10):1748-56. Epub 2009 Apr 6.

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 19/31

RODMAN & RENSHAW EQUITY RESEARCH

Planned Program: ThermoDox in combination with High Intensity Focused

Ultrasound (HIFU)

Bone metastasis occurs when tumor cells spread from a primary tumor, from a tissue outside of the bone, to any bone

throughout the body. Metastasis is common in many cancers (Figure 15), and it is estimated that 350,000 people die in

the U.S. as a result of bone metastasis each year43

. Bone metastasis is a complex multi-step process which results in

tumors from outside the bone migrating into the bone where they begin to grow and divide. The presence of tumor cellswithin the bone disrupts the normal function of the bone and can lead to bone marrow infiltration, hypercalcemia (too

much calcium in the blood), and bone fracture. For the patient, bone metastases can have a significant impact on

quality of life as the metastasis may lead to impaired mobility and severe pain. In terms of a clinical standpoint

metastasis represents a significant problem as treatment options are limited and survival rates are low. For example

breast cancer patients with bone metastases have a median survival of 2-4 years44

, and prostate cancer patients with

bone metastases have a median survival of 2-3 years45

.

Figure 15: Prevalence of Bone Metastases by Tumor Type

Source: 46

To address the treatment of bone metastasis, Celsion has partnered with Phillips HealthCare to combine ThermoDox

with High Focused Ultrasound (HIFU). The HIFU technology uses MRI guided ultrasound waves to heat a specific body

tissue. The ultrasound waves can be focused on an internal plane that lies beneath the surface of the skin, which allows

heating of internal tissue (Figure 16, Left Panel). In the case of a ThermoDox-based treatment, the HIFU could be used

to heat a target organ or tumor. Theoretically, ThermoDox will circulate through the bloodstream until it reaches the

heated tissue, whereby doxorubicin would be released into the target tissue. Results from a preclinical mode

demonstrate that HIFU can induce a statistically significant difference in the amount of tissue doxorubicin compared to

no HIFU exposure (Figure 16, right panel). Based on the preclinical data, HIFU data, as well as ThermoDox clinical tria

data, Celsion plans to initiate a Phase 2 trial in metastatic bone cancer. The protocol for this trial is currently pending

final FDA review. The trial will be conducted in collaboration with Phillips Healthcare.

43 Mundy GR. Metastasis to bone: causes, consequences and therapeutic opportunities. Nat Rev Cancer. 2002 Aug;2(8):584-93.44

Guise TA, Kozlow WM, Heras-Herzig A, Padalecki SS, Yin JJ, Chirgwin JM. Molecular mechanisms of breast cancer metastases to bone. Clin Breast Cancer. 2005 Feb;5 Suppl(2):S46-53.45 Saad F, Clarke N, Colombel M. Natural history and treatment of bone complications in prostate cancer. Eur Urol. 2006 Mar;49(3):429-40. Epub 2006 Jan 646 Coleman RE. Metastatic bone disease: clinical features, pathophysiology and treatment strategies. Cancer Treat Rev. 2001 Jun;27(3):165-76.

Tumor TypePrevelence of Bone

Metastases

Prostate cancer 65% to 75%Breast cancer 65% to 75%

Given that HCC is the third most common type of cancer worldwide, and given that the HCC does not respond well to

traditional chemotherapy, there is an effort by industry and academia to identify therapeutic modalities that can treat this

disease. Currently, sorafenib (Nexavar) is FDA approved for the treatment of unresectable advanced HCC. However, a

search of the NIH’s clinical trial website reveals that 26 Phase 3 trials across industry and academia are open to

recruitment or recently completed enrollment (Figure 17).

Figure 17: Distribution of Current Phase 3 Trials for the Treatment of Unresectable HCC in Industry andAcademia

Source: www.clinicaltrial.gov and Rodman & Renshaw Research

Therapeutic Treatment Industry Academic

Sorafinib (single agent or

combination)2 3

Novel HCC Agent or Delivery

system5 1

TACE 1 10

RFA 1 1

Radiation - 2

Total 9 17

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 21/31

RODMAN & RENSHAW EQUITY RESEARCH

While it is impractical to thoroughly discuss every agent in Phase 3 development for HCC, we note that sorafenib is

currently being investigated in both industry and academic sponsored trials. The only industry sponsored RFA study is

the ThermoDox trial being conducted by Celsion, in which final data for the primary outcome is expected in December

2012. The other RFA study is an academic trial comparing RFA vs. microwave ablation, and therefore not immediately

relevant to the ThermoDox HCC trial. When examining the competitive landscape for HCC it is important to note tha

certain treatment modalities are indicated for different stages of disease. For example, the TACE procedure and

sorafenib are used to treat patients with advanced HCC. Advanced HCC is defined as unresectable HCC with vascula

invasion or extrahepatic spread47

. RFA treatment is indicated for patients that do not have vascular involvement. It isimportant for investors to appreciate the difference between the patient populations in advanced HCC vs. the patien

population suitable for RFA. Recall that RFA-based treatment can potentially cure HCC48

, whereas more advanced

treatments are aimed at controlling/managing the disease with the goal of prolonging survival49

.

Of note, 5 industry-based trials are investigating drugs or drug delivery systems that are new to Phase 3 HCC treatment

Of the 5 trials, 3 of these trials are designed for patients with more advanced HCC than the ThermoDox HCC trial, the

other 2 trials enrolled patient populations that are similar to those enrolled in the HCC ThermoDox trial and will be

discussed in greater detail below. Despite other ongoing Phase 3 trials, it is important for investors to note the Celsion

trial has a unique feature that separates it from the other drugs and treatments. Particularly, the HCC ThermoDox tria

specifically includes patients with HCC tumors up to 7 cm in diameter. This is significant as traditional RFA is only used

to treat tumors up to approximately 3 cm in diameter.

Sorafenib

In 2007, sorafenib was approved in the US for advanced HCC. Sorafenib is a kinase inhibitor that has activity agains

multiple kinases that are responsible for cell proliferation and survival, including B-RAF, C-RAF, and VEGFR-2.

Sorafenib provides overall survival benefits to unresectable HCC, 10.7 months (sorafenib) vs. to 7.9 months (placebo).

The FDA has approved sorafenib for the treatment of “unresectable HCC”, a designation that has been cited as both

vague and broad50

. It is worthwhile for investors to note that sorafenib is also being evaluated at other stages of HCC

Several trials have examined the use of sorafenib in combination with local therapy; however the trials have been

criticized as being too small and premature50

. Although HCC is currently being investigated in additional advanced

HCC settings, it is also important for investors to remember that the ThermoDox HCC trial is focused on patients with an

intermediate stage disease.

ABT-869 (Linifanib)

Abbott is currently conducting a Phase 3 trial of ABT-869, an inhibitor of the vascular endothelial growth factor (VEGF)

and platelet-derived growth factor (PDGF) family of tyrosine kinases. The trial will enroll 900 patients, and the primary

end point of the study is overall survival. Phase 2 data revealed that ABT-869 provided patients with a 112 day median

time to progression and a median overall survival benefit of 295 days51

. The Phase 3 study is examining ABT-869

compared against sorafenib in subjects with advanced or metastatic HCC. While the patient population has more

advanced disease than the patients in the ThermoDox trial, the outcome of this trial could change treatment plans of

advanced HCC and may impact the future treatment of other stages of HCC. The estimated completion date of the

Phase 3 trial of ABT-869 trial is February 2012.

47Llovet JM, Brú C, Bruix J. Prognosis of hepatocellular carcinoma: the BCLC staging classification. Prognosis of hepatocellular carcinoma: the BCLC staging classification.

48 Poon RT. Radiofrequency ablation combined with resection enhances chance for curative treatment of hepatocellular carcinoma. Ann Surg Oncol. 2007 Dec;14(12):3299-300. Epub 2007 Sep 25.49

MD Anderson Cancer Center: OncoLog, May 2008, Vol. 53, No. 5. http://www2.mdanderson.org/depts/oncolog/articles/08/5-may/5-08-1.html50 Kim R, Byrne MT, Tan A, Aucejo F. What is the indication for sorafenib in hepatocellular carcinoma? A clinical challenge. Oncology (Williston Park). 2011 Mar;25(3):283-91, 295. 51 Toh H, Chen P, Carr BI, et al. A phase II study of ABT-869 in hepatocellular carcinoma (HCC): interim analysis. J Clin Oncol. 2009;27: 222s:abstr 4581

Celsion Corporation October 26, 2

8/3/2019 CLSN

http://slidepdf.com/reader/full/clsn 22/31

RODMAN & RENSHAW EQUITY RESEARCH

Talaporfin Sodium (Atipocine) and Interstitial Light Emitting Diodes

Talaporfin sodium is a light-activated drug that is currently in Phase 3 trials for HCC conducted by Light Sciences

Oncology. The treatment consists of talaporfin sodium and the Litx device, which is made up of light-emitting diodes

First, the Litx device is percutaneously placed at the tumor site, followed by intravenous injection of the talaporfin

sodium. The light produced by the Litx device causes the talaporfin molecule to produce a reactive oxygen molecule

that kills cells in the target tissue. A Phase 1/2 HCC trial of Litx/talaporfin demonstrated that the treatment was safe

however, the trial only involved 8 patients and no statistically significant efficacy claims could be drawn from the trial52

The Phase 3 trial enrolled 200 patients and results are expected in 2011. Investors should be aware that the Ligh

Sciences Oncology trial targets a similar population as the ThermoDox Phase 3 HCC trial. However, the ThermoDox

HCC trial enrolled 600 patients, and the ThermoDox trial builds upon a preexisting standard of care (RFA) and clinically-