41

Sandpiper Bay – Florida October 21, 2011 Club Med Americas Sandpiper Bay

Sandpiper Bay – Florida

October 21, 2011Club Med AmericasSandpiper Bay

2

Agenda

North AmericaFrom Defense to Offense

MICHEL WOLFOVSKI

Chairman and Chief Executive Officer

Executive Vice President and Chief Financial Officer

AmericasStrategic overview

HENRI GISCARD D’ESTAING

Chief Executive Officer – North AmericaXAVIER MUFRAGGI

Chief Executive Officer – Latin AmericaJANYCK DAUDET

South AmericaOverview

3

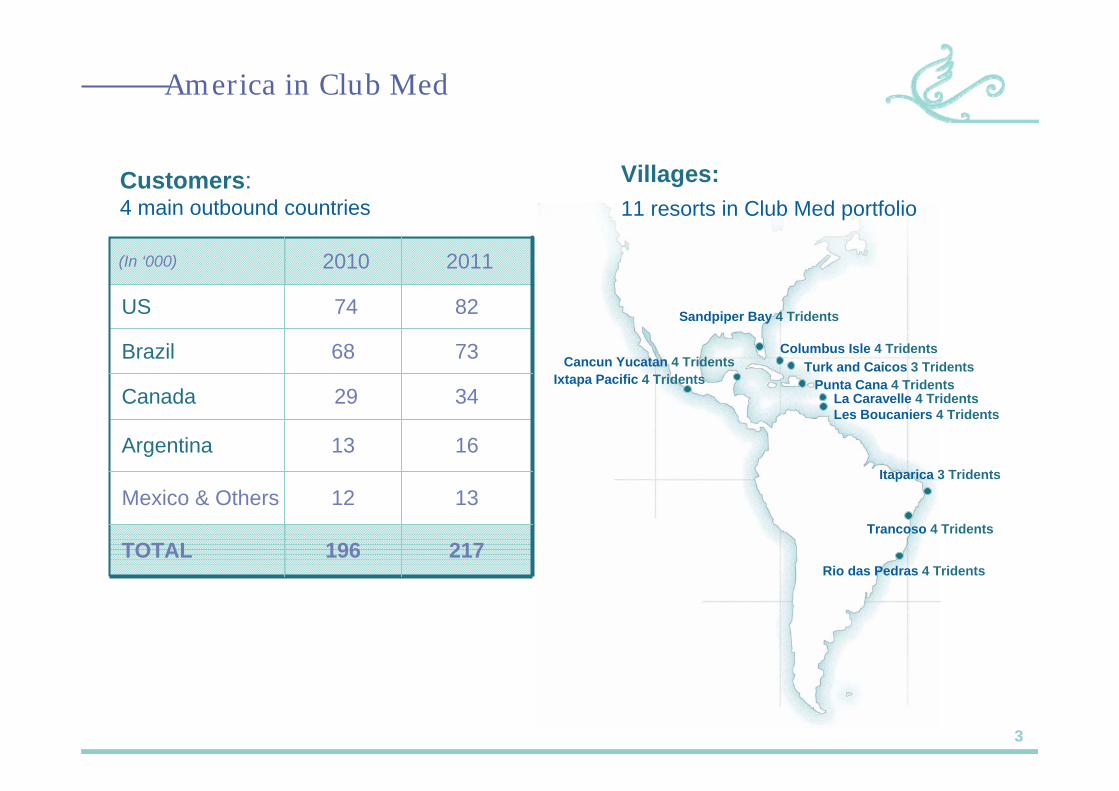

America in Club Med

217 196 TOTAL

13 12Mexico & Others

16 13 Argentina

7368Brazil

20112010(In ‘000)

34

82 74US

29Canada

Customers:4 main outbound countries

Villages: 11 resorts in Club Med portfolio

Turk and Caicos 3 TridentsColumbus Isle 4 Tridents

Punta Cana 4 TridentsLa Caravelle 4 TridentsLes Boucaniers 4 Tridents

Sandpiper Bay 4 Tridents

Ixtapa Pacific 4 Tridents

Rio das Pedras 4 Tridents

Itaparica 3 Tridents

Trancoso 4 Tridents

Cancun Yucatan 4 Tridents

4

SurviveStop the losses

Change the model

Status post 2001

(34)

317

20%

284

27%

19

2001

27%o/w Customers 4 & 5 Tridents

26%Capacity 4 Tridents

14Number of Villages

233Customers (In ‘000)

(41)Operating Income (In €m)

220Revenues (In €m)

2002

5

Product positioning not clear enough:

For couples, Fun? Families?

Villages not upscale enough

Disparity of products

Not suitable with American standards

Fierce copying from competitionCopy of the Club Med Concept:Super Clubs, Sandals etc…

Going one step further with the all-inclusive

A huge potential market in all inclusive upscale family segment: USA/Brazil/Canada

Club Med offer fits with American customers

Worldwide Geographical spread with international customers filling up villages in unique locations

Unique experience in kids Clubs: best family experience

Strategic decision: Is there a room for Club Med in the Americas ?

Club Med Threats in America post 2001

Club Med Strengths

BUT

6

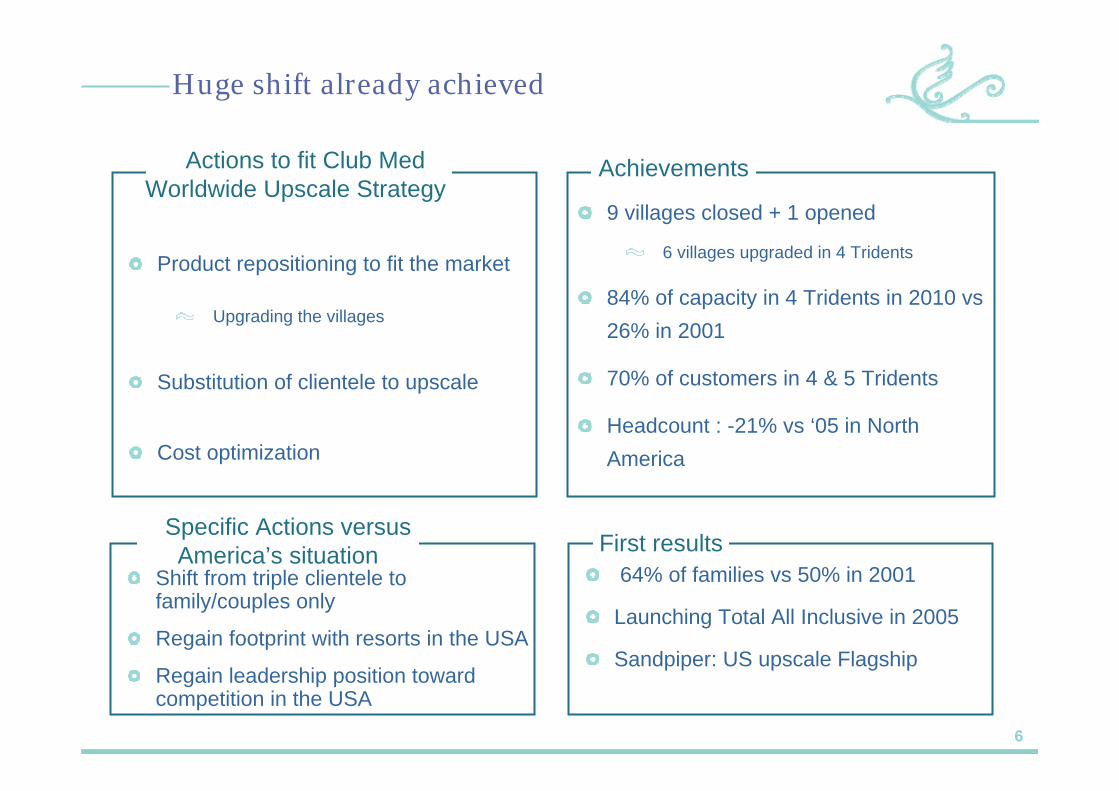

Product repositioning to fit the market

Upgrading the villages

Substitution of clientele to upscale

Cost optimization

9 villages closed + 1 opened

6 villages upgraded in 4 Tridents

84% of capacity in 4 Tridents in 2010 vs26% in 2001

70% of customers in 4 & 5 Tridents

Headcount : -21% vs ‘05 in North America

Huge shift already achieved

Actions to fit Club Med Worldwide Upscale Strategy

Achievements

Specific Actions versus America’s situation

Shift from triple clientele to family/couples only

Regain footprint with resorts in the USA

Regain leadership position toward competition in the USA

First results64% of families vs 50% in 2001

Launching Total All Inclusive in 2005

Sandpiper: US upscale Flagship

7

Portfolio post 2001 & actions

Closed in 2003YESYESYESVaradero 4T

Renovation started in 2010+ extension to come YESYESYESRio das Pedras 4T

fits to strategy – renovation/extension projectNOYESNOColombus Isle 4T

Room lifting in 2003NOYESYESTurkoise 3T

fits to strategyYESYESYESItaparica 3T

21 M€ to upgrade from 3 to 4 Tridents in 2010-2012YESNOYESSandpiper 3T

28 M€ to upgrade from 3 to 4 Tridents in 2007-2009YESNOYESPunta Cana 3T

19 M€ to upgrade from 3 to 4 Tridents in 2007-2008YESNOYESIxtapa 3T

20 M€ to upgrade from 3 to 4 Tridents in 2005-2006 + extension to come NONONOCaravelle 3T

24 M€ to upgrade from 3 to 4 Tridents in 2006 -2007+ product repositioning : from single to family segmentYESNOYESCancun 3T

48 M€ to upgrade from 2 to 4 Tridents in 2005-2006+ product repositioning : from single to family segmentNONONOBuccaneer s Creek 2T

Closed in 2008NONOYESMexican Villas

Closed in 2001YESNONOSonora Bay 3T

Closed in 2001NONOYESSainte Lucie 3T

Closed in 2001: only opened in winterNONONOPlaya Blanca 3T

Closed in 2004NONOYESParadise 4T

Closed in 2001YESNONOHuatulco 3T

Closed in 2006: only opened in winterNOYESNOCrested Butte 4T

Closed in 2002: only opened in winterNONONOCopper Mountain 3T

Villages in 2001 Permanent Premium Criticalsize Actions

CLO

SED

UPG

RA

DED

REN

OVA

TED

8

Where are we today ?

(6)

203

32%

268

29%

14

2004

(2)

196

29%

222

32%

12

2006

(6)

181

47%

211

58%

12

2008

(34)

317

20%

284

27%

19

2001

(41)

220

27%

233

26%

14

2002

86%68%Clients 4 & 5 Tridents

84%77%Capacity 4 Tridents

profit

196

217

11

2011

11Number of Villages

196Clients (In ‘000)

(3)Op. Income – Villages (In €m)

176

2010

Revenues (In €m)

Moving to a profitable & sustainable modelHuge shift already achieved

Profitable in 2011

Worldwide main events 9/11 Gulf War Global financialcrisis

H1N1 Virus

9

Developing Club Med Business Offer

Launching new concept : Golf and Tennis Academies

Increasing number of Europeans clients 1/3 of hotel days

2011-2015 drivers: Working on Seasonality issue

Seasonality in profitability Areas for improvement in Summer

12

(20)

15

(18)

23

W09 S09 W10 S10 W11

Operating Income VillagesReported figures in €m

10

Villages capacity Opening of a 4th village in Buzios (Brazil)

• Inbound customers (Brazil/Argentina)• International customers

Sandpiper Bay – Phase 2• Fully renovated as of Dec. 22, 2011 (Winter 12)

Capacity Optimization • Columbus renovation + 60 new Deluxe Condos (Winter 13) • Ixtapa/Cancun 14 Villas or condos• Sandpiper phase 3: 30 new deluxe rooms• Boucaneers : capacity increase of 60 deluxe rooms• Caravelle: capacity increase of 36 deluxe rooms• Rio das Pedras: capacity increase of 22 rooms and renovation

Market and pricingMarket potential

• Brazil growing market• Canada: A mature country to reach 60% sales contribution in 2015

Pricing initiatives• Structural: coming from new upscale capacity and room reclassification• Pricing project: reassess pricing practices to improve BV STS

Mid TermAdditional villages : opening of a mountain bi-seasonal village (managed)

• Europeans in summer • Easy access

2011-2015 Key drivers

11

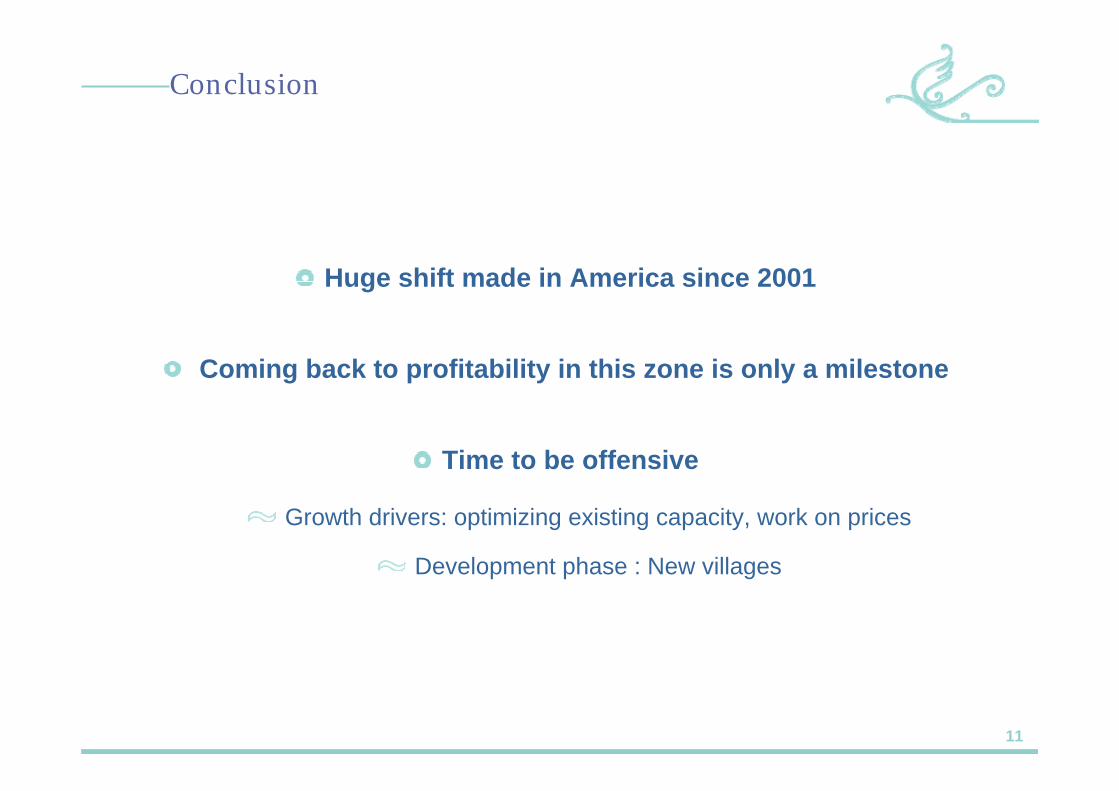

Huge shift made in America since 2001

Coming back to profitability in this zone is only a milestone

Time to be offensive

Growth drivers: optimizing existing capacity, work on prices

Development phase : New villages

Conclusion

Sandpiper Bay – Florida

October 21, 2011South America overview

13

Potential Market Latin America

Brazil´s population: 190 millionClub Med´s clients: 73 thousand

Potential clients: 2.18 million of people

Mexico

Social Classes: A+, A, B+ and B

ArgentinaBrazil

Mexico´s population: 113 millionClub Med´s clients: 11 thousand

Potential clients: 1.76 million of people

Argentina´s population: 40 millionClub Med´s clients: 16 thousand

Potential clients: 1.20 million of people

14

Sales Distribution 2010 - 2011

Mexico2010 201169% 72% (direct sales)31% 28% (indirect sales)

Argentina2010 201129% 32% (direct sales)71% 68% (indirect sales)

Brazil2010 201140% 49% (direct Sales)60% 51% (indirect sales)

Definition: Club Med Corners inside tourism agenciesObjective: Strengthen the brand / direct link with customers / increase sales2 opened Club Med Corners : Belo Horizonte (MG) ; São Paulo (SP)4 future projects: Campinas (SP) ; Porto Alegre (RS); Curitiba (PR); Buenos Aires (Argentina);

Shop in Shop: Club Med Corners

Belo Horizonte, BH

15

Brazil: Macroeconomic indicators

Inflation Rate GDP

5,45,9

0

5

10

15

20

25

4,2

7,5

-2

0

2

4

6

8

10

Brazil is in a very favorable economic time, with prevision of growth rate of 4%. The inflation rate is under control. The outlook for the future continues to be favorable, with high growth economy.

16

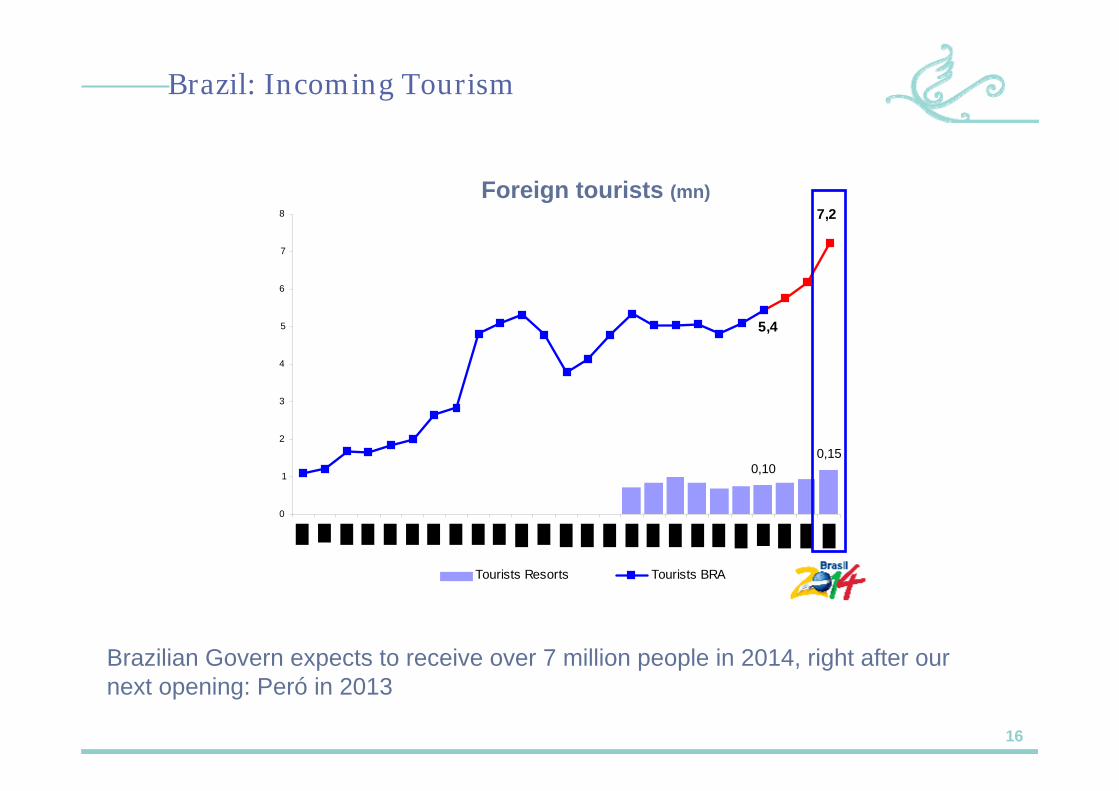

Brazil: Incoming Tourism

0,150,10

5,4

7,2

0

1

2

3

4

5

6

7

8

Tourists Resorts Tourists BRA

Foreign tourists (mn)

Brazilian Govern expects to receive over 7 million people in 2014, right after our next opening: Peró in 2013

17

Next Resort in Brazil – Buzios, Peró

Club Med Pero – P&L 20134th Resort in Brazil

Localization: Peró Beach (Cabo Frio, RJ) next to Buzios

Beach 5 Km longer, larger than Copacabana

Situaded in a natural reserve

4T Resort with a 5T Luxury Space

Family Resort

400 apartments

Opening: End of 2013

Sandpiper Bay – Florida

October 21, 2011North America from Defense to Offense

19

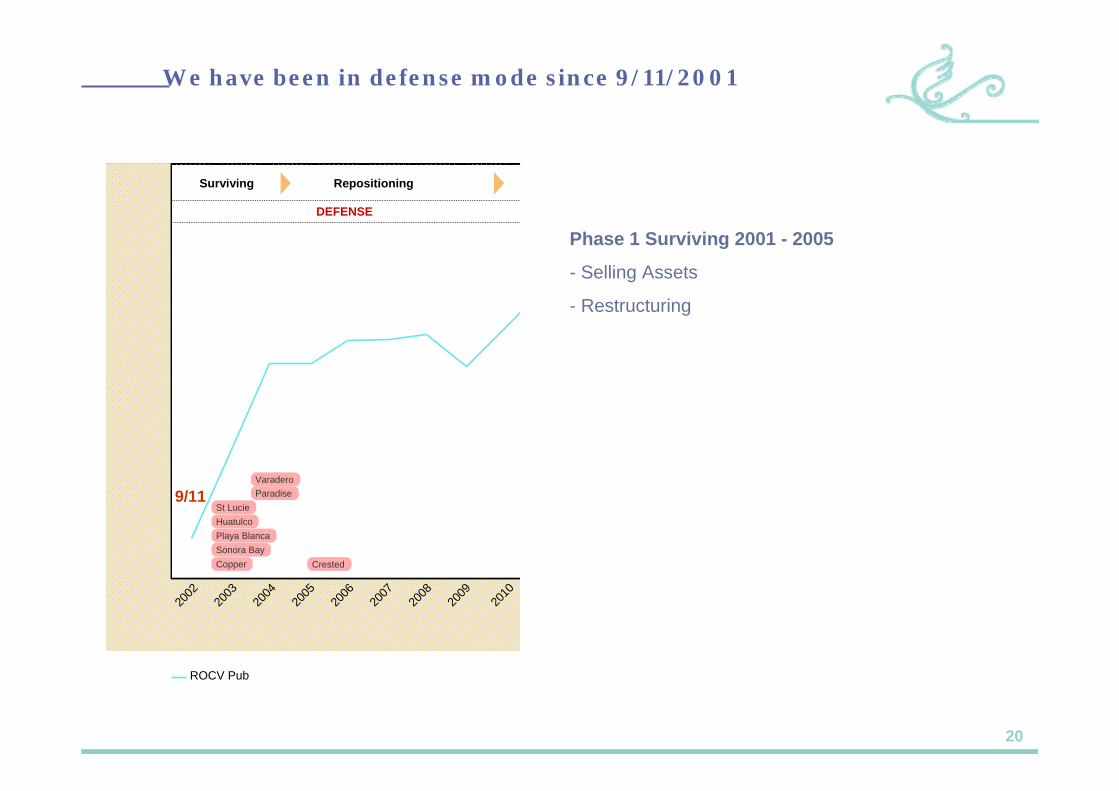

We have been in defense mode since 9/11/2001

2002

2003

2004

2005

2006

2007

ROCV Pub

2008

2009

2010

2011

2012

Plan 20

13

9.6%

Surviving Repositioning Growth

DEFENSE OFFENSE

Columbus

Turkoise

+14.6M

9/11

20

We have been in defense mode since 9/11/2001

2002

2003

2004

2005

2006

2007

ROCV Pub

2008

2009

2010

2011

2012

9.6%

Surviving Repositioning Growth

DEFENSE OFFENSE

St LucieHuatulcoPlaya BlancaSonora BayCopper

VaraderoParadise

Crested Columbus

9/11

Phase 1 Surviving 2001 - 2005

- Selling Assets

- Restructuring

21

We have been in defense mode since 9/11/2001

2002

2003

2004

2005

2006

2007

ROCV Pub

2008

2009

2010

2011

2012

Plan 20

13

Surviving Repositioning

DEFENSE

St LucieHuatulcoPlaya BlancaSonora BayCopper

VaraderoParadise

Crested

BuccaneersCaravelleCancun

IxtapaPunta

Sandpiper Bay

Columbus

Turkoise

9/11

Phase 1 Surviving 2001 - 2005

- Selling Assets

- Restructuring

Phase 2 Repositioning Upscale Family 2005 - 2010

- Resorts Portfolio Renovation

- New Marketing/Sales strategy

Sandpiper Bay – Florida

October 21, 20112005 – 2010: A defensive strategy to become sustainable

23

KEY DRIVER #1: renovate our Resorts to give a financial step change…

$6.6m

$97

319 days

$135

232

728 988652Average # of beds

$11.0m

$83

365 days

$137

361

$1.9m

$77

295 days

$115

192

GOP *

REVPAB

Duration of the season

Average price (per hotel nights)

Capacity (in ‘000s)

3 4

* Gross Operating Profit

BEFORE (2009) AFTER (2013)

New Club Med model

Source: Hyperion Planning

CURRENT (2011)

4

GOP B-Case planned for Y13 should be closed to

be achieved in Y12

28.9 M$ invested in Sandpiper renovation

+ 17%

X 3.5

24

… and deliver a consistent Premium Promise

Ixtapa 4.5/5

Cancun 4.5/5

Sandpiper 4/5

Punta Cana 4.5/5

Turkoise 4/5

Columbus 4.5/5

TripAdvisor rating in September 2011

Customer Satisfaction and « Word of Mouth » effect are the heart of our Resort Renovation Strategy

Global Customer Satisfaction in North American Villages

+2pts vs last 3 years

Customer Feedback measurement

25Source: Enterprise Guide

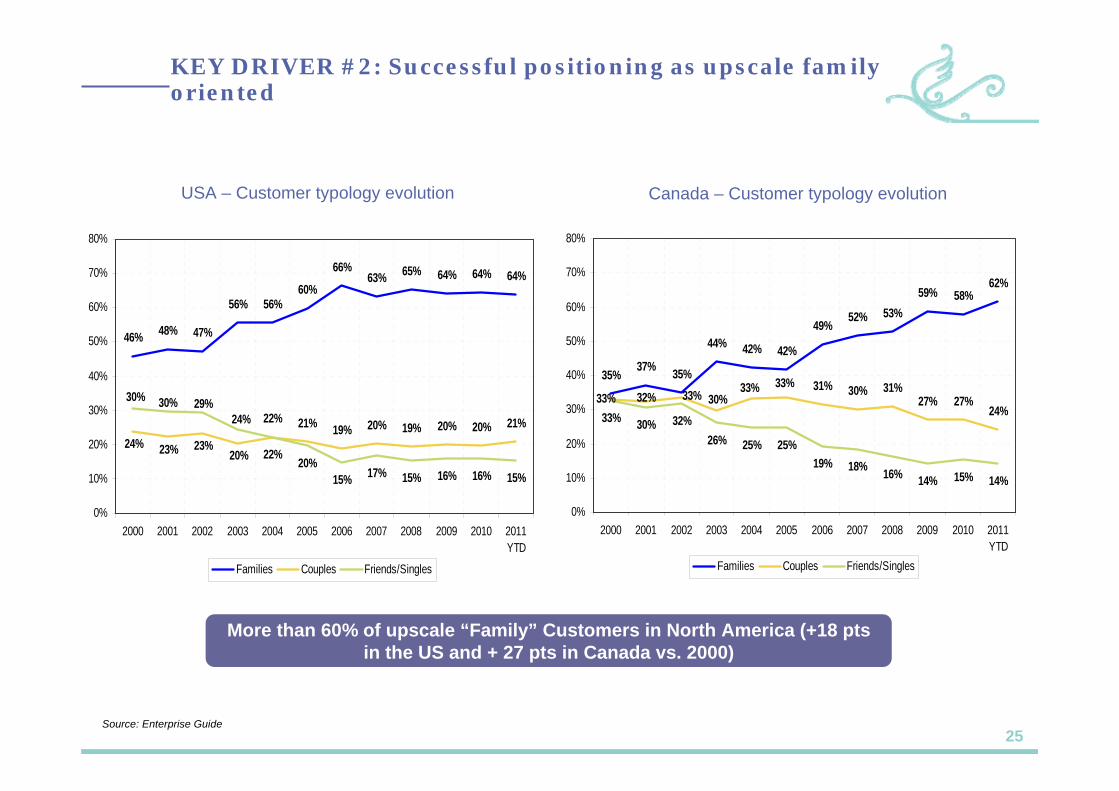

KEY DRIVER #2: Successful positioning as upscale family oriented

USA – Customer typology evolution Canada – Customer typology evolution

46% 48% 47%

56% 56%60%

66%63% 65% 64% 64% 64%

22% 21% 19% 20% 19% 20% 20% 21%

22% 20%15% 17% 15% 16% 16% 15%

20%23%23%24%

24%29%30%30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011YTD

Families Couples Friends/Singles

35% 37% 35%

44% 42% 42%

49%52% 53%

59% 58%62%

31% 30% 31%27% 27%

24%

25% 25%19% 18% 16% 14% 15% 14%

33% 32% 33% 30%33% 33%

33% 30% 32%26%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011YTD

Families Couples Friends/Singles

More than 60% of upscale “Family” Customers in North America (+18 pts in the US and + 27 pts in Canada vs. 2000)

26Source: Enterprise Guide

KEY DRIVER #3: Strong shift of distribution towards direct sales and targeted Travel Agents…

USA CANADA

36% from Internet

18% from Internet

64% direct sales in the US vs. 47% in 2004, from 13% to 35% of direct sales in Canada in 5 years

53%50%

48%44%

41% 40%36% 36%

56%59% 60%

64% 64%

52%50%

47%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 Forecast11

Total Indirect Total Direct87% 88% 87%

83%80%

76%

70%

65%

17%20%

24%

30%

35%

13% 12%

13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 Forecast11

Total Indirect Total Direct

27

A cost optimization thanks to our new distribution…

- 5.5 M$ in Sales commissions between 2005 and

2010

…and a main shift in our Marketing strategy…

- 6.6 M$ in Marketing budget between

2005 and 2010

…with a strong reallocation in digital

spending

From 0 to 60% of media spending online

between 2005 and 2010

1 2

3

… which permits a main commission sales decrease and foster our Marketing Strategy digitalization

Sandpiper Bay – Florida

October 21, 20112011-2015: Moving To Offense

29

The North American equation for Club Med in the next few years

A Strategic Market

AMN #1 market in the World (Around

$16MM*) for All Inclusive vacations…

… with a strong competition in the

Caribbean

*Source: PhoCusWright Travel Agency Distribution Landscape

30

The North American equation for Club Med in the next few years

BRAND: Still not known for what it has become

SHARE OF VOICE: too low to reverse the trend and demonstrate our difference

A new Customer Behavior

The Club Med challenges

DISTRIBUTION: Low/no visibility inTA, OTA, TO

PRICE: over market competition with aggressive promotions policy

Premium all inclusive resorts an enormous market but that has become a commodity

SEARCHED by clients through OTA / websearch

BOOKED by Clients still a lot from TO after checking “Word Of Mouth” and Tripadvisor

A Strategic Market

*Source: PhoCusWright Travel Agency Distribution Landscape

AMN #1 market in the World (Around

$16MM*) for All Inclusive vacations…

… with a strong competition in the

Caribbean

31

…but the structural basis are solid and opportunities exist

* 4% of the richest Households of the country

GLO

BA

LTR

END

SU

PSC

ALE

ST

RA

TEG

YR

ECR

UIT

MEN

TLO

YALT

Y

Club Med North America is in a positive dynamic growth in Customer & BV

In 2012, Club Med North America will completely achieve its upscale strategy in terms of Customers 87% of Customer will book a 4-5T Resort whereas they were 68%

in 2010 (and 30% of TOP4* Customers)

Within 2015, recruitment will remain key to aliment Customer Stock and ensure business with more than 60% of New Customers expected every year…

…but Customer repurchase rate has increased during the last 3 years and is a key opportunity to leverage the top-line and to optimize occupancy rate

32

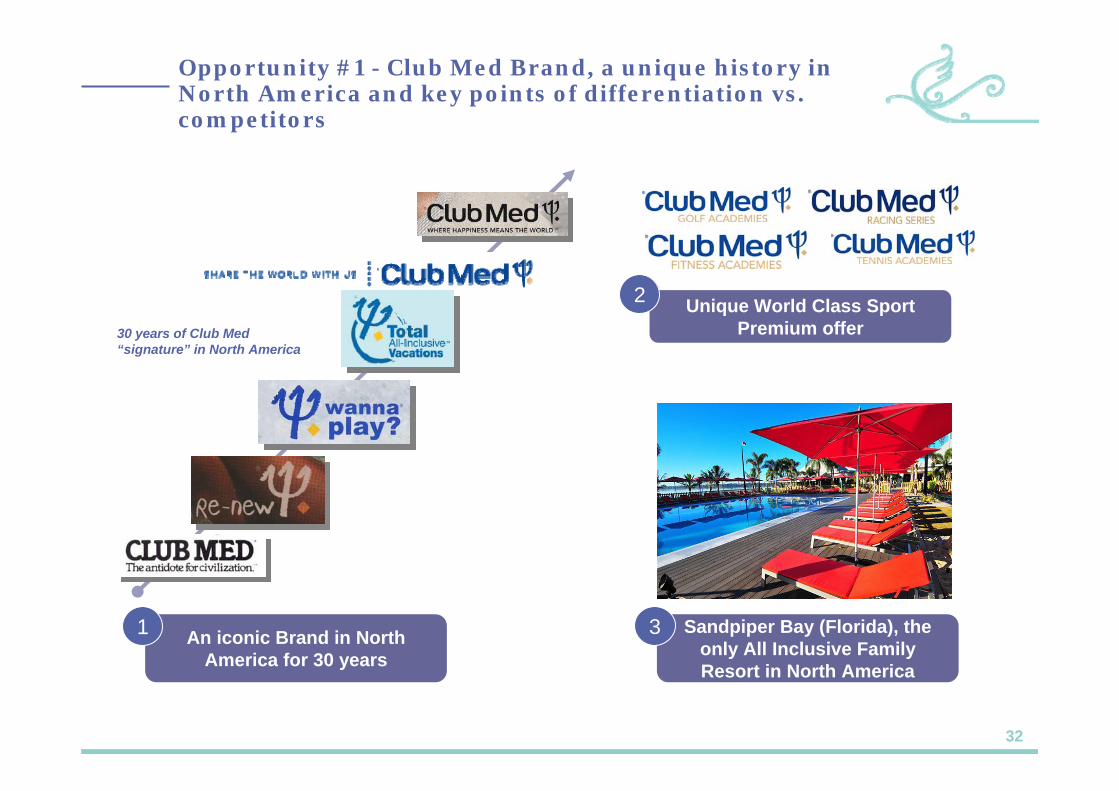

Opportunity #1 - Club Med Brand, a unique history in North America and key points of differentiation vs. competitors

Unique World Class Sport Premium offer

Sandpiper Bay (Florida), the only All Inclusive Family Resort in North America

An iconic Brand in North America for 30 years

1

2

3

30 years of Club Med “signature” in North America

33

Opportunity #2 - The new world of travel marketing & distribution, a key axis to develop our Share of Voice

The “Digital revolution” (OTA role, Social Network development) represents a strong opportunity to maximize our visibility

40M Visitors/month

More than 600M of Members

9M Visitors/Day19M Visitors/Month

15M Visitors/Day

10.6M Visitors/Month

Around 100MM searches/month

10M Visitors/month

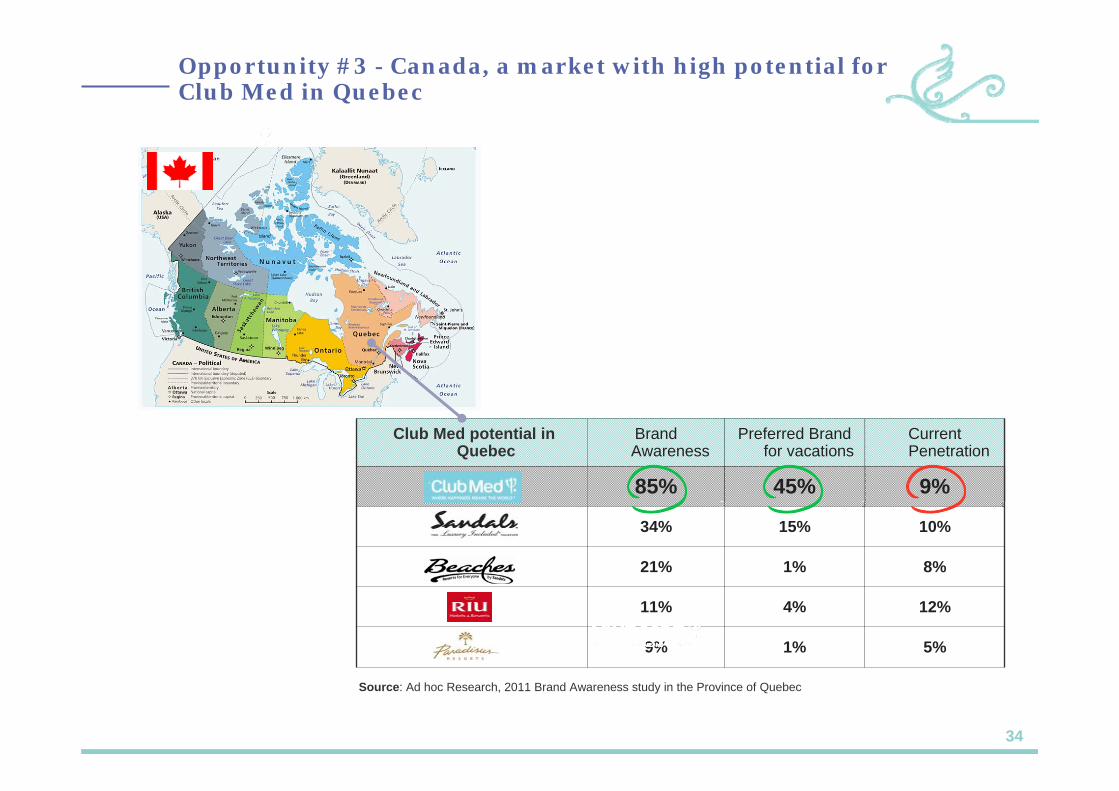

34

1%

4%

1%

15%

45%

Preferred Brand for vacations

12%11%

9%

21%

34%

85%

Brand Awareness

5%

8%

10%

9%

Current Penetration

Club Med potential in Quebec

Source: Ad hoc Research, 2011 Brand Awareness study in the Province of Quebec

Opportunity #3 - Canada, a market with high potential for Club Med in Quebec

35

Our 100K North American Customers are more loyal…

+ 2 pts of increase in repeat purchase rate

between 2008 and 2011

…on who we already have a great understanding thanks to our unique

Customer Database…

1 2

Opportunity #4 - Our Customer Database, an asset to exploit to maximize BV and Ambassadorship

…and we could benefit from a direct contact with the largest part of our

Customers to increase our Customer Knowledge…

3…including a new Social dimension

thanks to the digital revolution

4

More than 50% of direct distribution to

personalize our relationship at each contact point with Customers

Already 120 000 Facebook Fans in less than 6

months

36

Opportunity #5 - A new Premium Pricing Strategy to sustain growth by the Top Line

…to develop Business Volume

…to develop Business Volume

Create Saturation…

Create Saturation…

…Earlier in the season…

…Earlier in the season…

…in a clear communication

for the Customers…

…in a clear communication

for the Customers…

…in an international approach…

…in an international approach…

• A fair, transparent and understandable Price & Promotion strategy

• A fair, transparent and understandable Price & Promotion strategy

• Ascending price curveimplementation

(Pricing Premium virtuous circle)

• Ascending price curveimplementation

(Pricing Premium virtuous circle)

• Leverage a readable Promotion Strategy based on early booking reinforcement

• Leverage a readable Promotion Strategy based on early booking reinforcement

• New Pricing graphic identity

• New Pricing graphic identity

• Consistent Price harmonizationbetween North American Customers expectations and European demand

• Consistent Price harmonizationbetween North American Customers expectations and European demand

Sandpiper Bay – Florida

October 21, 2011Conclusion

38

And today we celebrate Sandpiper Bay renovation

39

$28.9M of investment…

A renovation in 2 phases (Phase 1 from Sept. to Dec. 2010 and Phase 2 from Sept. to Dec 2011)

+336 beds with the same number of rooms

21 Tennis courts in the Village

1 Golf on-site and 15 others ones at less than 20 mns

+$4.7M of GOP in 2011 vs 2010 (before renovation)

+6.4K Customers in 2011 vs 2010 (including 90% of New Customers)

Sandpiper renovation in 8 figures

40

The best of a 4 Trident Club Med Family Village…

…with a point of difference: Sport Academies

The only family all-inclusive destination in the USA, located in the Sunshine State

340 rooms, including Family and Couple Deluxe rooms

Children’s programs available for ages 4 months - 17 years

2 gourmet dining options

An endless array of sports and activities

3 swimming pools and a splash park for children

A new Spa featuring the latest treatments designed to renew the senses

World Class infrastructures• 21 Tennis Courts (clays and hard court)• 16 Golf courses 20 min with concierge• Fitness Center and L’Occitane Spa

Multicultural World Class Coaches specialized in kids and juniors

Program personalized for everyone• Kids to Seniors• Novice to Elite

Club Med Sandpiper Bay, first flagship of the “premium Sport” category

41

Last figure but not the least…

100% of those tennis players were coached by our Pro in the past