36

Kathrine Fog, SVP Corporate Strategy & Analyses Market Outlook

Kathrine Fog, SVP Corporate Strategy & Analyses

Market Outlook

Macro and downstream

67

Improving macro environment evident in aluminium demand

68

Semis demand at or above GDP in key regions

Source: Thomson Reuters, Republished under license from CRU International Ltd

Semis demand annual growth, key regions(%)

0%

2%

4%

6%

8%

10%

China North America Western Europe World ex. China

2016 2017

40

45

50

55

60

65S

ep-1

1

Apr-1

2

Nov

-12

Jun-

13

Jan-

14

Aug

-14

Mar

-15

Oct

-15

May

-16

Dec

-16

Jul-1

7USA ISM Eurozone China NBS China Caixin

Increasing production

Contractingproduction

Manufacturing PMI’s

Substitution trend in automotive progressing

69

US semis demand in automotive remains positive although car sales have overall moderated in 2017

Source: Thomson Reuters, Republished under license from CRU International Ltd

Semis demand in transport, annual growth(%)

0%

2%

4%

6%

8%

10%

US Western Europe

2016 2017 E 2018 E

50

60

70

80

90

100

110

120

130

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

US light vehicle sales Eurozone car registration

US and European automotive indicators(Index, Jan. 2008=100)

Automotive demand for aluminium supporting several semis productsCar makers utilizing aluminium to reduce weight and increase fuel-efficiency

70

Source: Hydro analysis, Republished under license from CRU International Ltd*Other includes e.g wire

0

5

10

15

20

25

30

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Castings Extrusions Other* Rolled products

7 %

7 %

4 %

Global semis demand for transport sector by product form(Mill t)

CAGR 2016-20

Level ofsubstitution

High-growth automotive segment with substantial further potential due to aluminium’s superior inherent properties

New segments and applications supporting aluminium demand

71

Marine / Offshore applications Zero-emission electrical car ferries in 100% aluminium for light-weighting

Industrial applications, ex. furnitures

B&C, ex. Supertall buildings

Middle and high voltage cables, wireand cables for electrical applications

Transportation, truck & trailer applications

Automotive, stong drive towards EV Aluminium in solar panels

Rolled products demand driven by transport segment

72

Transport share increasing in total rolled products demand

General rolled products demand, selected regions • Continued substitution trend in transport main

demand driver• Growth in packaging driven by can stock and

foil in emerging markets

0%

2%

4%

6%

2014 2015 2016 2017 E 2018 E

North America Europe*

Source: Hydro Analysis, Republished under license from CRU International Ltd*Total EU27+EFTA

YoY-growth

Expected market development

50%

17%

14%

8%

5%4% 2%

PackagingTransportConstructionMachinery & EquipmentConsumer durablesElectricalOther

Global segment composition, rolled products(2017)

Extrusion market supported by continued momentum in B&C market and improving demand in transport

73

Source: Thomson Reuters, Hydro Analysis, Republished under license from CRU International Ltd

62%14%

12%

5%4%

3%

Construction TransportMachinery & equipment ElectricalConsumer durables Other

Global segment composition, extrusion(2017)

Housing market indicatorsIndex, Jan 2010=100

80

100

120

140

160

180

200

220

240

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

Jan-

17Ju

l-17

US Building permitsUS Housing startsEU construction order book

US truck and trailer marketMonthly shipments, annual growth

-50%

-30%

-10%

10%

30%

50%

70%

90%

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

Jan-

17Ju

l-17

Light trucks Heavy duty trucks

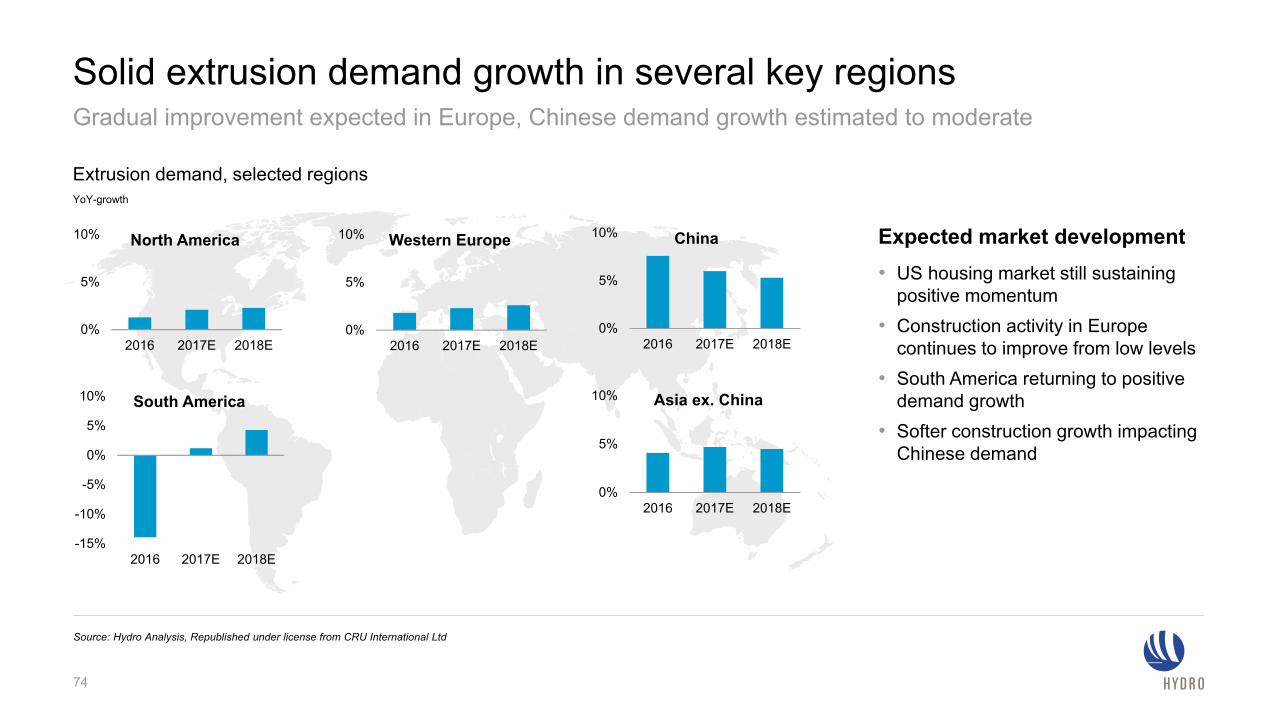

Solid extrusion demand growth in several key regions

74

Gradual improvement expected in Europe, Chinese demand growth estimated to moderate

Source: Hydro Analysis, Republished under license from CRU International Ltd

• US housing market still sustaining positive momentum

• Construction activity in Europe continues to improve from low levels

• South America returning to positive demand growth

• Softer construction growth impactingChinese demand

Expected market development

0%

5%

10%

2016 2017E 2018E

Asia ex. China

Extrusion demand, selected regionsYoY-growth

0%

5%

10%

2016 2017E 2018E

Western Europe

-15%

-10%

-5%

0%

5%

10%

2016 2017E 2018E

South America

0%

5%

10%

2016 2017E 2018E

China

0%

5%

10%

2016 2017E 2018E

North America

0%

2%

4%

6%

8%

10%

12%

0

50

100

150

200

250

300

350

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Foil Sheet & strip Extrusions* Net semis exports as share of semis production (RHS)

Largely stable Chinese semis exports last yearLimited extrusion exports to Europe and North America, extrusion stocks transferred from Mexico to Vietnam

Source: CRU, Antaike, Hydro Analysis*Mainly extrusions, but also including some smaller semis categories such as wire**US extrusion duties imposed in 2010, impacting volumes from 2011

Monthly Chinese net semis exports (12-month moving average)Thousand tonnes

0

200

400

600

800

1000

1200

1400

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Asia North America Europe Oceania Latin America Middle East Africa

Annual Chinese extrusion exports, by regionThousand tonnes

**

75

Source: Hydro Analysis, Antaike

Trade flows partly impacted by trade measures

76

Chinese semis exports by destination – Asia key region

(2016)

AsiaAfricaNorth AmericaEuropeMiddle EastLatin AmericaOceania

US• Import duties

on semis• Dumping cases• Signals on

more protection

Europe• Import duties

on semis• Dumping cases

44%

9%

15%

11%

10%

8%3%

Asia• Some import

duties• India introducing

duties

Primary metal market

77

Recap CMD 2016: Global primary market expected to be largely balanced also in 2017

78

Source: CRU, Hydro Analysis

30 000

35 000

40 000

45 000

50 000

55 000

60 000

65 000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

Supply Demand

Global (’000 mt)

Supply influences 2017

Chinese restarts

Chinese curtailments

Key regions in China adding capacity

Indian projects

Demand influences 2017

Momentum in Chinese construction and transport sector

Continued strong transport segment

Steady development US and Eurozone

Global growth expectations 2017

Demand: 3-5 %Supply: 4-6 %

Global primary market for 2017 in small deficit

79

Both supply and demand higher than expected

Source: CRU, Hydro Analysis

30 000

35 000

40 000

45 000

50 000

55 000

60 000

65 000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

Supply Demand

Global (’000 mt)

Supply influences 2017

Chinese restarts

Chinese curtailments

Key regions in China adding capacity

Indian projects

Demand influences 2017

Momentum in Chinese construction and transport sector

Continued strong transport segment

Steady development US and Eurozone

Global growth 2017Demand: ~6.0 %Supply: ~7.0 %

Happened to a limited extent Happened to a large extent

Global primary market expected to be largely balanced in 2018

80

Primary supply and demand growth expected to be largely similar

Source: CRU, Hydro Analysis

30 000

35 000

40 000

45 000

50 000

55 000

60 000

65 000

70 000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Supply Demand

Global (’000 mt)

Supply influences 2018Winter shutdowns

SOE projects in China

Limited growth for privatecompanies in China

US restarts

Indian projects

Demand influences 2018

Gradual slowdown in Chinese construction and transport sector

Continued strong transport segment

European and US growth continues

Global growth expectations 2018

Supply and demand: 4-5 %

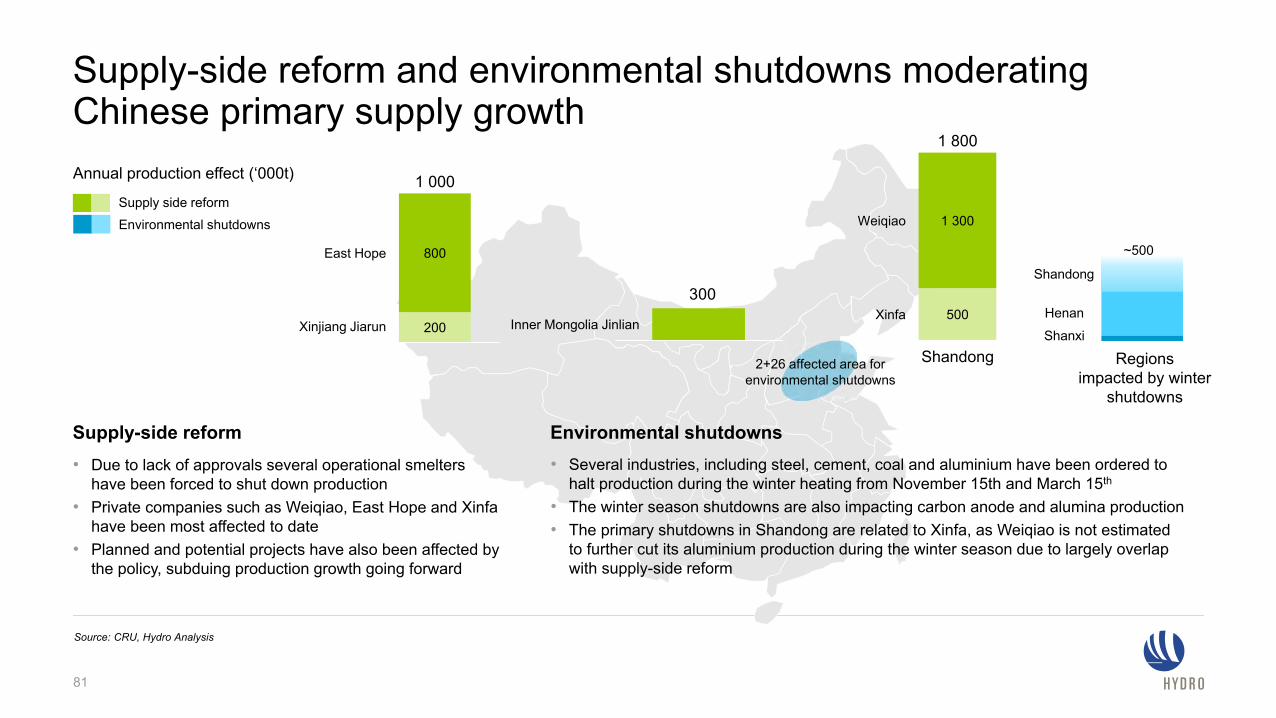

Supply-side reform and environmental shutdowns moderating Chinese primary supply growth

81

Xinfa

Weiqiao

500

1 300

1 800

2+26 affected area for environmental shutdowns

Xinjiang Jiarun 200

1 000

East Hope 800

300

Inner Mongolia Jinlian

• Several industries, including steel, cement, coal and aluminium have been ordered to halt production during the winter heating from November 15th and March 15th

• The winter season shutdowns are also impacting carbon anode and alumina production• The primary shutdowns in Shandong are related to Xinfa, as Weiqiao is not estimated

to further cut its aluminium production during the winter season due to largely overlap with supply-side reform

• Due to lack of approvals several operational smelters have been forced to shut down production

• Private companies such as Weiqiao, East Hope and Xinfahave been most affected to date

• Planned and potential projects have also been affected by the policy, subduing production growth going forward

Supply side reformEnvironmental shutdowns

Supply-side reform Environmental shutdowns

Annual production effect (‘000t)

Shandong Regions impacted by winter

shutdowns

Henan

Shanxi

Shandong

Source: CRU, Hydro Analysis

~500

Key drivers for China’s aluminium expansion losing momentum

82

PastDrivers for aluminium capacity

Demand growth

Lack of environmental restrictions

Energy availability

Access to financing

Raw material access

• Continued strong growth short-term, but expected to slow longer term• Export market impacted by trade restrictions

• From softer to harder constraints: strong enforcement of environmental shutdowns during winter shutdown

• Competitive advantage of coal-rich regions moderating, combined with rising coal prices

• Environmental issues will further challenge coal-based production

• Tighter financial liquidity perceived as constraint for potential capacity new-builds and restarts

• Supply-side reform limiting new projects, especially by private players

• Depleting domestic bauxite reserves, more dependent on imports• Carbon producers also impacted by environmental shutdowns

Present

Supportive of capacityexpansions

Moderating capacityexpansions

Chinese energy market reforms impacting aluminium smelter cost

-

100

200

300

400

500

600

700

800

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep

-15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep

-16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep

-17

Datong 5,500 NAR Qinhuangdao FOB price

Bohai-Rim steam-coal price index, 5,500 NAR

Source: IHS

Implement power pricing mechanisms

reflecting market fundamentals

Remove cross-subsidization

and regulate T&D tariffs at cost-plus levels

Promote direct power purchase and

power trading

Standardize andstrengthen supervisionof captive power plants

Chinese Power Market Reform:Key objectives

Chinese Steam Coal Price BandRMB/t

Reforms expected to even out power prices across the specter of Chinese aluminium producers

83

500

750

1 000

1 250

1 500

1 750

2 000

2 250

2 500

0 10 000 20 000 30 000 40 000 50 000 60 000

2016 Spot curve, Nov. 2017

Higher and steeper cost curve in 2017 compared to 2016

84

Higher end of the cost curve dominated by Chinese smelters

Source: Hydro analysis, IHS, Platts, Republished under license from CRU International Ltd

Cost pressure in 2017Higher coal prices

Higher alumina pricesHigher carbon costs

Business operating cost (BOC)USD/t

Index: Jan 2016 = 100

0

50

100

150

200

250

Q1-16 Q2-16 Q3-16 Q4-16 Q1-17 Q2-17 Q3-17 Q4-17

Chinese steam coal Alumina PAX Pet coke FOB US Gulf

Primary aluminium market to be largely balanced in 2018

85

Market balances largely similar compared to 2017

Source: CRU, Hydro analysis

~28.0 – 28.3

~30.1 – 30.4 ProductionDemand

~37.5 – 38.3

~35.7 – 36.4

ProductionDemand

3-4 %

3-4 %

4-6 %

4-6 %-3 000

-2 000

-1 000

0

1 000

2 000

China World ex. China Global

World ex. China 2018

China 2018

Primary market balance 2018(‘000t)

% Growth from 2017 to 2018

(mill t.)

(mill t.)

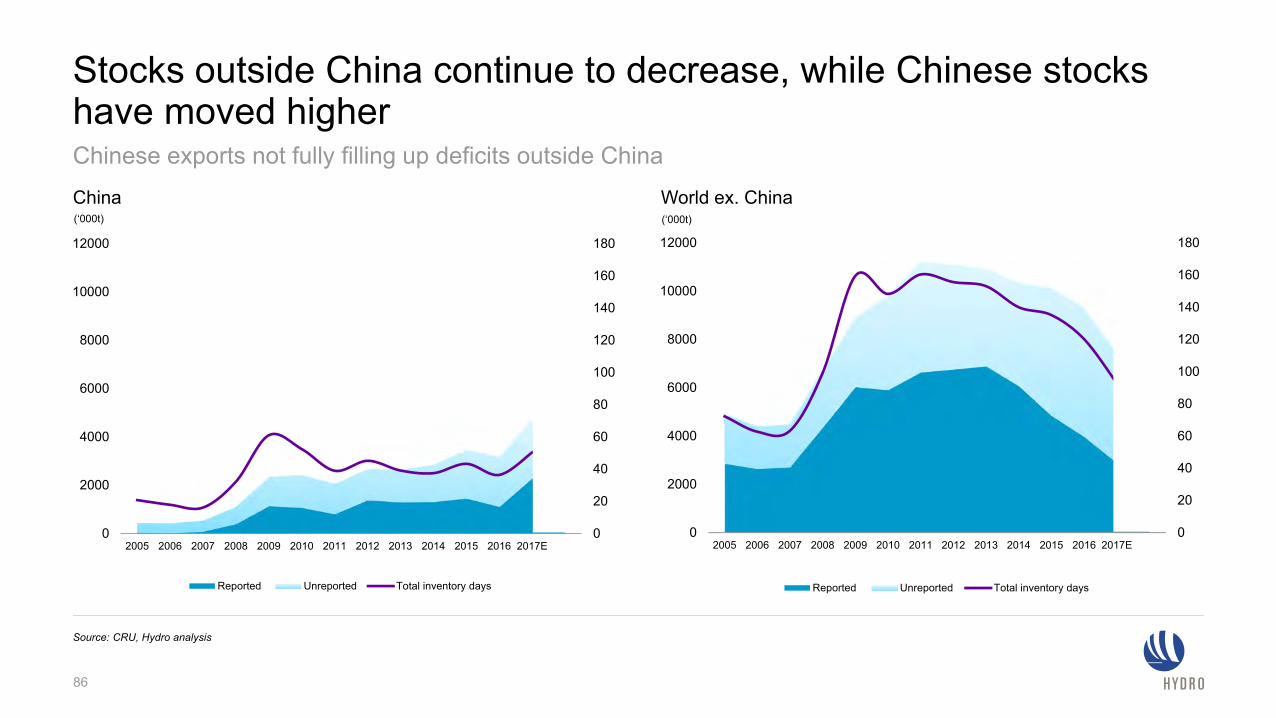

Stocks outside China continue to decrease, while Chinese stocks have moved higher

86

Chinese exports not fully filling up deficits outside China

Source: CRU, Hydro analysis

0

20

40

60

80

100

120

140

160

180

0

2000

4000

6000

8000

10000

12000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E

Reported Unreported Total inventory days

China

0

20

40

60

80

100

120

140

160

180

0

2000

4000

6000

8000

10000

12000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E

Reported Unreported Total inventory days

World ex. China(‘000t) (‘000t)

Inventory days approaching historically tight levels in world outside China in 2018

87

Chinese inventory days expected to increase, but not substantially

Source: CRU, Hydro analysis

0

20

40

60

80

100

120

140

160

180

0

2000

4000

6000

8000

10000

12000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E

Total stocks Total inventory days

0

20

40

60

80

100

120

140

160

180

0

2000

4000

6000

8000

10000

12000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E

Total stocks Total inventory days

China World ex. China(‘000t) (‘000t)

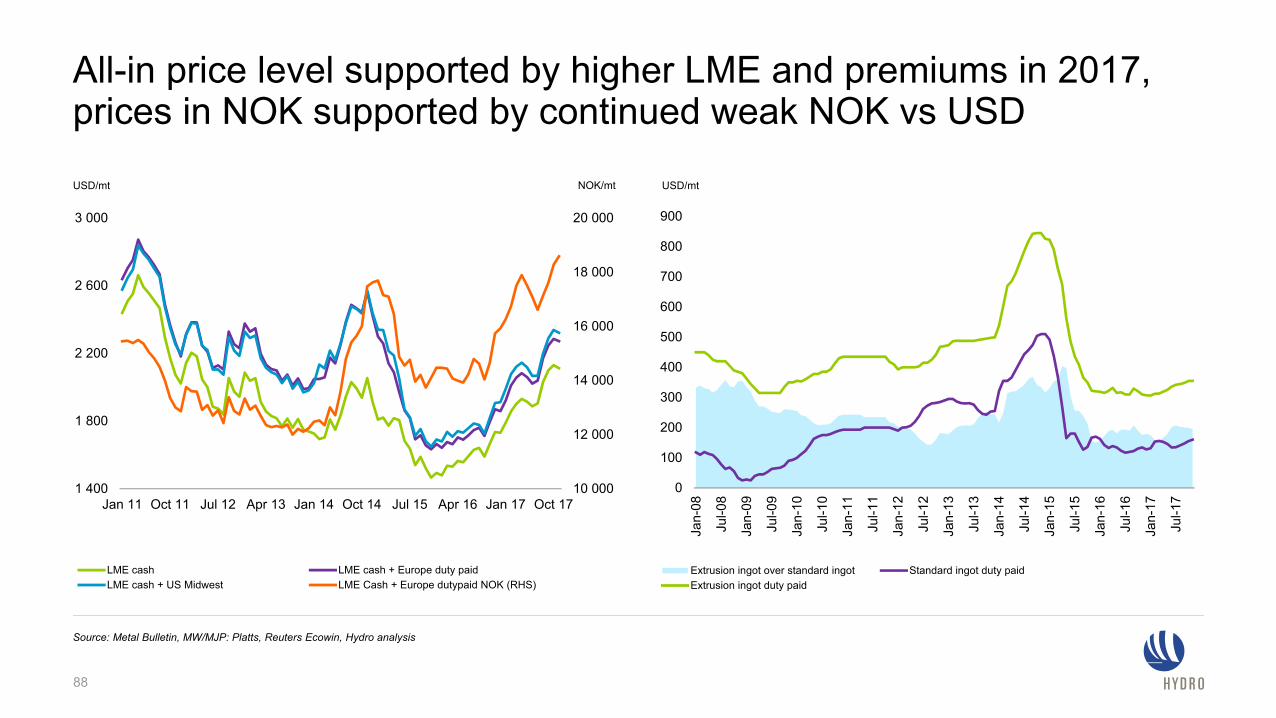

All-in price level supported by higher LME and premiums in 2017, prices in NOK supported by continued weak NOK vs USD

88

Source: Metal Bulletin, MW/MJP: Platts, Reuters Ecowin, Hydro analysis

0

100

200

300

400

500

600

700

800

900

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

Jul-1

7

Extrusion ingot over standard ingot Standard ingot duty paidExtrusion ingot duty paid

USD/mt

10 000

12 000

14 000

16 000

18 000

20 000

1 400

1 800

2 200

2 600

3 000

Jan 11 Oct 11 Jul 12 Apr 13 Jan 14 Oct 14 Jul 15 Apr 16 Jan 17 Oct 17

LME cash LME cash + Europe duty paidLME cash + US Midwest LME Cash + Europe dutypaid NOK (RHS)

USD/mt NOK/mt

Bauxite and alumina market

89

Chinese primary production dependent on imported resources

90

Around 37% based on imported raw material (average 2013-2017)

Source: CRU, China customs, 2017 forecast Hydro analysis

0

10

20

30

40

50

60

70

80

90

100

Primary production Alumina Bauxite

100 % 93.7 %

6.3 %

63.3 %

30.4 %

% of Primary Production

Imported

Imported

Domestic

Domestic

2017f40%

Bauxite production in China to decline, triggering more imports

• Depleting resources not sufficient to sustain operations in key provinces:− inland refineries may convert to imported

bauxite or relocate to southern provinces

− new refinery capacity in coastal region, dependent on imported bauxite

− refinery capacity outside of China

• Bauxite (equivalent) imports could increase from ~70 Mtpy in 2017 to ~150 Mtpy in 2025

Chinese bauxite imports set to increase

91

Source: CM Group (ept 2017, $50/t cif bauxite scenario) * alumina imports as bauxite equivalent

Chinese bauxite production and importsMtpy

0

50

100

150

200

250

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

hist domestic production forecast domestic prod alumina import * imports

Guinea’s bauxite production is rising

• Committed capacity increasing to ~70 Mtpy by 2020

• Substantial bauxite resources available− 20+ billion mt within 150 km of coast

− Low reactive silica

• Chinese SOE bauxite and alumina projects more likely following USD20bn loan to Guinea

• Social instability could hamper investments − Higher HSE and community standards required

0

10

20

30

40

50

60

70

80

2015 2016 2017e 2018e 2019e 2020e

Guinea bauxite production (million mt)

CBG Kindia Dian-Dian SMB/WAP EGA (GAC) Alufer

92

Projects to add 25-30 Mtpa of bauxite export capacity, resource base could support additional volumes

Source: CRU, Hydro analysis

Altantic

Pacific

2013 2017

Chinese bauxite imports increasingly exposed to freight

93

Freight represents ~20 to 60% of the CIF price, freight rates increasing from low levels

Source: China customs, Bloomberg, Hydro analysisNote: 2017 is Jan-Sep annualized

0

1000

2000

3000

Feb-

13

Jun-

13

Oct

-13

Feb-

14

Jun-

14

Oct

-14

Feb-

15

Jun-

15

Oct

-15

Feb-

16

Jun-

16

Oct

-16

Feb-

17

Jun-

17

Oct

-17

Origin of Chinese bauxite imports

Baltic Dry Index

20

30

40

50

60

70

80

90

Jul-09 Jul-10 Jul-11 Jul-12 Jul-13 Jul-14 Jul-15 Jul-16 Jul-17

Indonesia Australia India Brazil Guinea Malaysia

CIF China, USD/t

100

150

200

250

300

350

400

0 20 000 40 000 60 000 80 000 100 000 120 000 140 000

2016 Spot curve, Nov. 2017

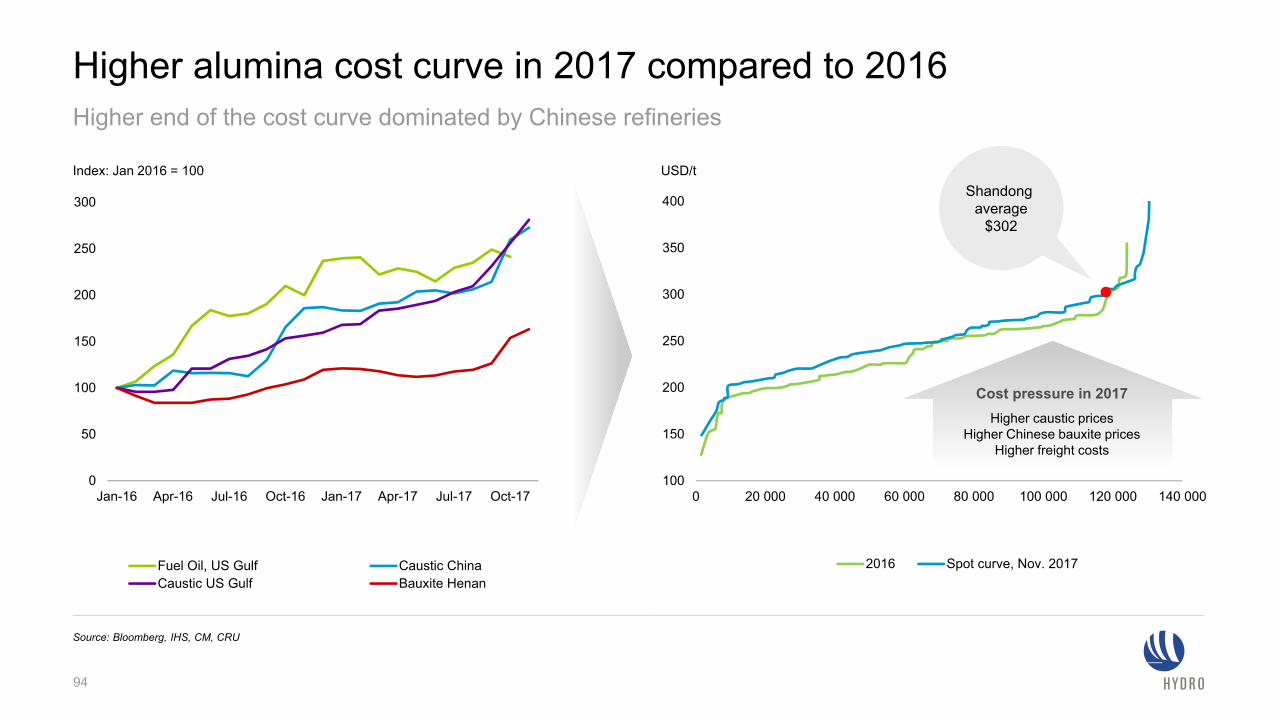

Higher alumina cost curve in 2017 compared to 2016

94

Higher end of the cost curve dominated by Chinese refineries

Source: Bloomberg, IHS, CM, CRU

USD/tShandong

average$302

Index: Jan 2016 = 100

0

50

100

150

200

250

300

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17

Fuel Oil, US Gulf Caustic ChinaCaustic US Gulf Bauxite Henan

Cost pressure in 2017Higher caustic prices

Higher Chinese bauxite pricesHigher freight costs

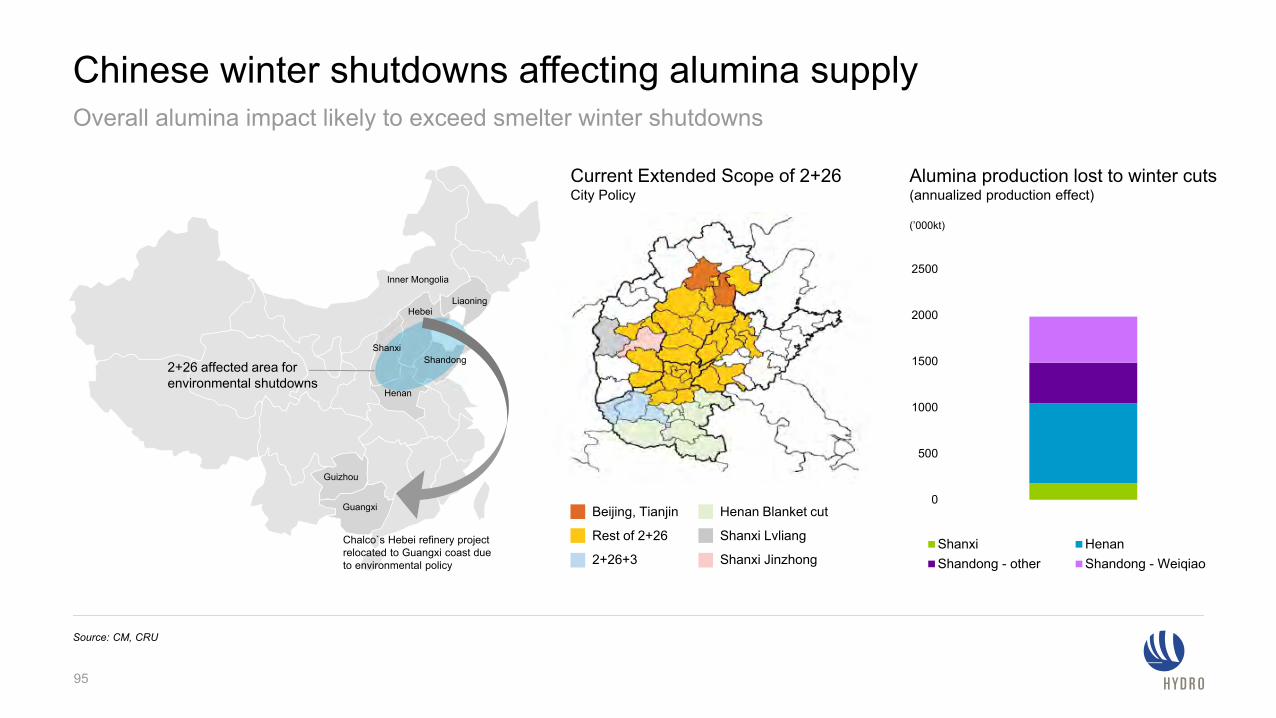

Chinese winter shutdowns affecting alumina supply Overall alumina impact likely to exceed smelter winter shutdowns

0

500

1000

1500

2000

2500

Shanxi HenanShandong - other Shandong - Weiqiao

Source: CM, CRU

(’000kt)

Alumina production lost to winter cuts(annualized production effect)

Current Extended Scope of 2+26City Policy

Beijing, Tianjin

Rest of 2+26

2+26+3

Henan Blanket cut

Shanxi Lvliang

Shanxi Jinzhong

2+26 affected area for environmental shutdowns

Inner Mongolia

LiaoningHebei

Shanxi

Henan

Shandong

Guizhou

Guangxi

Chalco`s Hebei refinery project relocated to Guangxi coast due to environmental policy

95

Alumina market balancing, Chinese additions also outside China

96

Limited capacity increases outside China

Source: Hydro analysis

Curtailed 2015 - 16

Capacity additions ex. China

Bubble size represents capacity 1 Mt

Point Comfort (2.3)

Paranam (2.25)

Chinese additions

Chinese refineries outside China

Atlantic curtailments• Atlantic market rebalancing

through curtailments• Corpus Christi and Paranam

restarts unlikely

Capacity additions ex. China• Middle East and India adding

capacity to supply own value chain

• Friguia restart in Guinea

Ras Al Khair (1.8)Al Taweelah (2.0)

Chinese additons• Chinese companies increasing

alumina production in Jamaica and Indonesa

• Domestic capacity additions, of which half located coastal

Alpart (1.65)Nhan Co (0.65)

Kendawangan (1.0)

Chinese additions2018: ~4.0 Mt

Friguia (0.65)India (1.0)Corpus Christi (1.63)

Being dismantled

Alumina prices rise amid policy implementation uncertainty

97

Market tightness, high metal prices, and increasing costs support prices

Source: Platts, Bloomberg

Market balances• New smelter projects ramping up in China• Re-stocking ahead of winter• Tighter market balance in China, less volumes

available outside China

Cost inflation• Higher caustic soda costs• Higher transport costs in China (road & rail)• Higher Chinese domestic bauxite prices

Other factors• Environmental inspections, shut down of

unsafe and small bauxite mines• Uncertainty regarding upcoming winter

heating season cuts

Recent alumina price drivers Platts alumina index (PAX, to 22 Nov 2017))PercentUSD/t

12%

14%

16%

18%

20%

22%

24%

150

200

250

300

350

400

450

500

550

Aug

201

0

Jan

2011

Jun

2011

Nov

201

1

Apr

201

2

Aug

201

2

Jan

2013

June

201

3

Nov

201

3

Apr

201

4

Aug

201

4

Jan

2015

June

201

5

Nov

201

5

Mar

201

6

Aug

201

6

Jan

2017

June

201

7

Nov

201

7

PAX % of LME 3M

Long-term outlook and summary

98

Strong demand drivers in key aluminium segments

Strong growth drivers across segments providing solid demand outlook

99

Source: CRU, Hydro Analysis

UrbanizationCopper substitution

UrbanizationHousing market recovery in mature regionsEnergy neutral buildings

Improving industrial sentiment in mature regionsManufacturing activity and industrial growth in emerging countries

UrbanizationEnvironmentally-friendly solutions

Transport

Construction

Electrical

Machinery & equipment

Packaging& foil

Growth in automotive vehicle productionAluminium content in cars increasingGrowth in other transport modes, e.g. railway

3 – 4 %

2 – 3 %

2 – 3 %

3 – 4 %

2 – 3 %

2000-17Global semis demand per segment, CAGR

5.0 %

6.5 %

7.0 %

6.0 %

4.0 %

2017-27

Global semis demand(CAGR 00-17)

5.5 %

Global semis demand

(CAGR 17-27)

~3 %

China:14.7 %

ROW:2.3%

China and ROW:~3 %

Still encouraging demand outlook from strong base – converging demand China and outside China

Growth in global semis demand creates opportunities for both primary and recycled material

100

Solid growth for semis, primary and recycling

Source: CRU, Hydro Analysis* Post-consumer and fabrication scrap** Unallocated creep estimated at same level as unallocated disruptions

CAGR 2017 – 2027

Semis

~3 %Primary

2-3 %Recycling*

3-4 %

• Solid long-term demand outlook supported bystrong growth drivers across segments

• Chinese primary supply moderating due to policy reform

• Global primary market largely balanced this year and next

• Cost curve pressured upwards by rising alumina and coal prices, with regional differences

• Recycling growth accelerating with increased generation of post-consumer scrap

• Chinese bauxite import dependency continues to increase

• Alumina market impacted by cost push and tightermarket balances

101