16

KILIFI TEACHERS SACCO SOCIETY LTD. DELEGA TES SEMINAR TEMPLE POINT RESORT, WATAMU 16 TH – 17 TH JUNE 2011 Satisfaction within our means

| Date post: | 07-Apr-2018 |

| Category: |

Documents |

| Upload: | daniel-masha |

| View: | 220 times |

| Download: | 0 times |

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 1/16

KILIFI TEACHERS SACCO

SOCIETY LTD.

DELEGATES SEMINARTEMPLE POINT RESORT, WATAMU

16TH – 17TH JUNE 2011

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 2/16

Areas to be covered

I. Introduction

☞ Definitions ☞How Saccos differ from other financial institutions

☞ Need for finance

II. Co-operative Finance☞ Sources ☞ Applications

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 3/16

Areas to be covered

(CONT

III. Why Saccos experience

difficulties in raising adequatefinance

IV. Suggested way forward

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 4/16

introduction DEFINITIONS

CO-OPERATIVE

DEF I:is a business organization owned and operatedby a group of individuals for their mutual benefit

DEF II: [ICA’S DEFINITION STATEMENT (PRURAL)]

As autonomous associations of persons united

voluntarily to meet their common economic, social, andcultural needs and aspirations through jointly ownedand democratically controlled enterprises

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 5/16

DEF III: as a business owned and controlled

equally by the people who use its services

● SACCO/CREDIT UNION [SACCO – acronym for Savings

and Credit Co-operatives]: is a co-operative financialinstitution that is owned and controlled by itsmembers and operated for the purpose of promoting thrift, providing credit at competitiverates, and providing other financial services to itsmembers.

● FINANCE

In general terms, it is the task of providing thefunds for business activities.

INTRODUCTION (CON’T)

- DEFINITIONS

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 6/16

INTRODUCTION (CON’T)

HOW SACCOS DIFFER FROM OTHER FINANCIALINSTITUTIONS

■Saccos represent people centered organizations,

as opposed to capital centered commercialcompanies.

■In a Sacco, customers are also its owners . Inother firms, customers and owners are separated

■In a Sacco, Price of share is fixed – not traded inan open market

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 7/16

■In a Sacco, objective is to benefitmember/customer by offering high qualitymember service. In other firms, primary

objective is to benefit owners by maximizingprofits

In a Co-op/Sacco, profit/surplus

generation is secondary: ought to be theresult of efficient operations

INTRODUCTION (CON’T) [how saccos differ]

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 8/16

NEED FOR FINANCE

■Start-up capital for acquisition of fixed assets:buildings, furniture, equipment etc

■Funds for operations to meet operating expenses

e.g stationery, rent, water, electricity, salaries etc■Funds for Investments in core business: lendingin the case of Saccos and other profitablesecurities

■Funds for Growth and Expansion in acquisition of

new fixed assets e.g additional branches,modernization of processes (ICT improvement)

■Business continuity: Retained earnings, reserves,inst capital

INTRODUCTION (CON’T) [need for finance]

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 9/16

co-operative finance

SOURCES AND APPLICATION OF FINANCEINTERRELATIONSHIP BETWEEN SAVINGS, CAPITAL AND INVESTMENT

SAVINGS INVESTMENT

INCOME

CONSUMPTION

CAPITAL

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 10/16

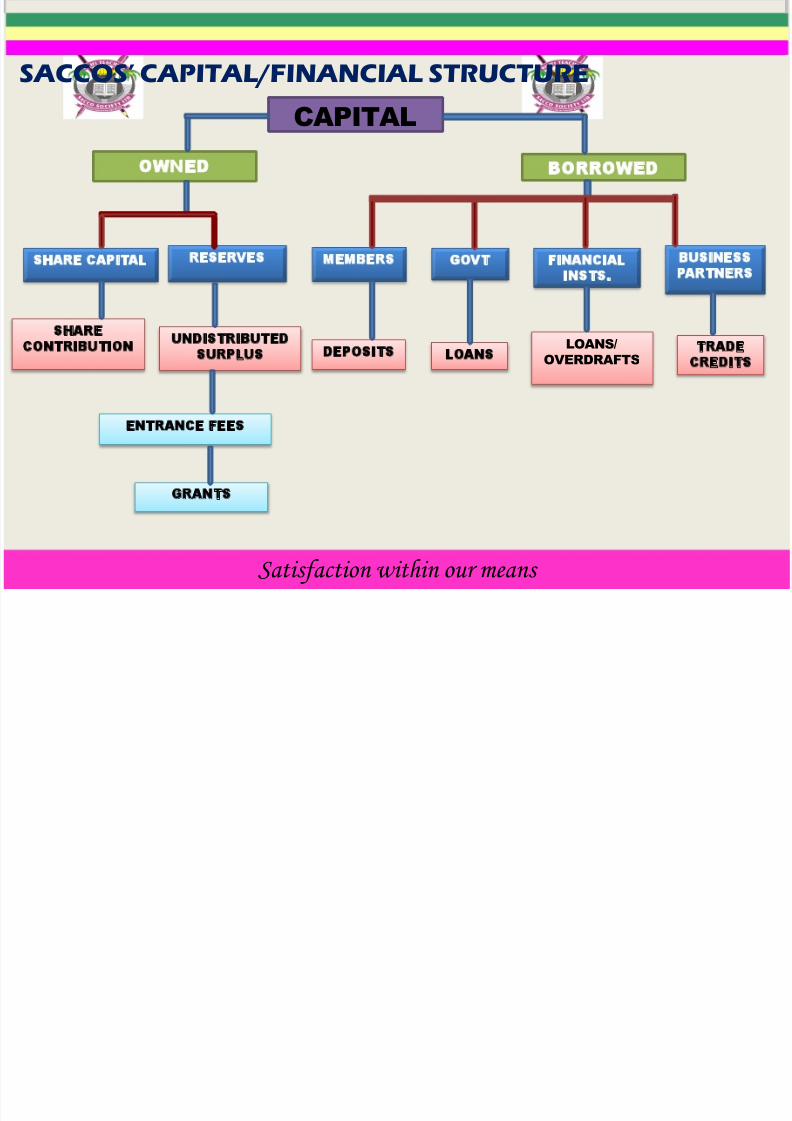

BORROWEDWNED

CAPITAL

SHARE CAPITAL RESERVES

SHARE

CONTRIBUTION UNDISTRIBUTED

SURPLUS

ENTRANCE FEES

GRANTS

MEMBERS GOVT FINANCIAL

INSTS.

BUSINESS

PARTNERS

DEPOSITS LOANS LOANS/

OVERDRAFTS

TRADE

CREDITS

SACCOS’ CAPITAL/FINANCIAL STRUCTURE

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 11/16Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 12/16

WHY SACCOS EXPERIENCE DIFFICULTIES IN RAISING

ADEQUATE FINANCE

LIMITED AREA OF

OPERATION/CLOSED MEMBERSHIP

POOR SAVINGS CULTURE: CONCEPT OF NET

BORROWERS VS NET SAVERS

POOR RESERVE RETENTION

AND CAPITAL BUILD UP

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 13/16

Poor image/branding

Poor pricing of products/low profitability

Distribution of dividends ignoringcapitalization concerns

WHY SACCOS EXPERIENCE DIFFICULTIES IN RAISING

ADEQUATE FINANCE

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 14/16

SUGGESTED WAY FORWARD

•Long term savings products

•Liquidity retentionPRODUCT

DIVERSIFICATION

•Children and Youth Savings

•Create incentives for Net Saversvs Net Borrowers

ENCOURAGE

SAVINGS

•Take advantage of the newregulatory environment tobuild confidence

REGULATORY

ENVIRONMENT

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 15/16

SUGGESTED WAY FORWARD (cont)

•Have a broader outlookof membership

•The larger themembership base, thelarger the capital base,ultimately the more thefinancial strength and

stability

AREA OF

OPERATION

Satisfaction within our means

8/6/2019 Co Op Finance

http://slidepdf.com/reader/full/co-op-finance 16/16

END

THANK YOU

JUNE 2011

BY Daniel S.G.Masha – Chief Executive Officer, Kilifi Teachers Sacco

Satisfaction within our means