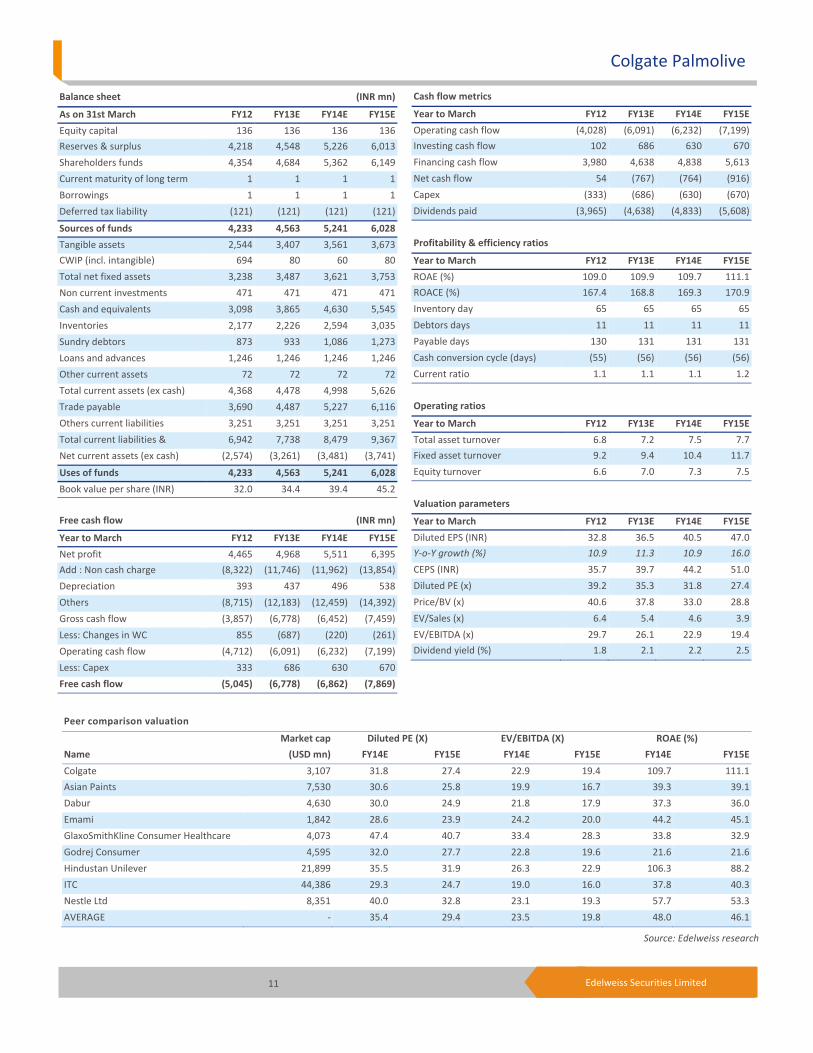

Edelweiss Research is also available on www.edelresearch.com, Bloomberg EDEL <GO>, Thomson First Call, Reuters and Factset. Edelweiss Securities Limited We recently met Ms. Prabha Parameswaran, Managing Director, Colgate‐ Palmolive India (Colgate). She reiterated that there is no slowdown in growth, except for some impact in the mouthwash segment. Management expects sales growth momentum (16% CAGR over FY08‐13) to remain robust riding rise in both penetration (rural stands at only 63% against 91% in urban) and per capita consumption (India half of China; pushing “brushing twice”). We believe the company is well equipped to counter competition from P&G’s impending entry in the toothpaste market. However, we expect ad spends in the toothpaste category to accelerate (will aid broadcasters like ZEE, Sun TV). Maintain ‘HOLD’. Premiumisation, penetration, consumption: Growth mantra Colgate will focus on increasing rural penetration and per capita consumption. Premiumisation will aid gross margin (globally, Colgate’s margins are 5‐7% higher than in India). Premium segment now contributes 10% to sales versus negligible earlier. Our view: Well equipped to tackle fresh competition In our view, P&G’s impending entry seems ill‐timed. Since the entry has been anticipated for years, existing players are well prepared—Colgate, HUL and Dabur have stepped up aggression in distribution, innovation and promotion; GSK is well entrenched in the premium segment. It will thus be a difficult and expensive affair for P&G. The toothpaste market, in our view, is the toughest nut in the Indian consumer space to crack as it is strongly dominated by Colgate, armed with an increasing and highest‐ever market share. Also, as P&G sharpens focus on the toothpaste category, its focus on shampoos, skin cream and detergents is likely to wane, benefiting HUL, Dabur etc. Thus, we expect P&G’s entry to be gradual and selective. Outlook and valuations: Robust; maintain ‘HOLD’ We continue to like Colgate’s strong distribution, generic brand, customer activations and innovation. Currently, the stock is trading at 31.8x and 27.4x FY14E and FY15E EPS, respectively. We maintain ‘HOLD’ and rate the stock ‘Sector Performer’. VISIT NOTE COLGATE PALMOLIVE Fore warned is fore armed EDELWEISS 4D RATINGS Absolute Rating HOLD Rating Relative to Sector Performer Risk Rating Relative to Sector Medium Sector Relative to Market Overweight MARKET DATA (R: COLG.BO, B: CLGT IN) CMP : INR 1,288 Target Price : INR 1,411 52‐week range (INR) : 1,580 / 1,097 Share in issue (mn) : 136.0 M cap (INR bn/USD mn) : 182/ 3,107 Avg. Daily Vol.BSE/NSE(‘000) : 108.3 SHARE HOLDING PATTERN (%) Current Q3FY13 Q2FY13 Promoters * 51.0 51.0 51.0 MF's, FI's & BK’s 5.2 5.4 6.0 FII's 21.6 21.6 20.9 Others 22.2 22.1 22.1 * Promoters pledged shares (% of share in issue) : NIL PRICE PERFORMANCE (%) Stock Nifty EW Consumer Goods Index 1 month (9.6) (5.9) 9.2 3 months 0.3 1.3 16.8 12 months 21.2 14.1 40.8 Abneesh Roy +91 22 6620 3141 [email protected]Pooja Lath +91 22 6620 3075 [email protected]India Equity Research| Consumer Goods June 24, 2013 Financials Year to March FY12 FY13 FY14E FY15E Revenues (INR mn) 26,932 31,638 36,860 43,168 Rev. growth (%) 17.8 17.5 16.5 17.1 EBITDA (INR mn) 5,785 6,568 7,444 8,751 Net profit (INR mn) 4,465 4,968 5,511 6,395 Shares outstanding (mn) 136 136 136 136 Diluted EPS (INR) 32.8 36.5 40.5 47.0 EPS growth (%) 10.9 11.3 10.9 16.0 Diluted P/E (x) 39.2 35.3 31.8 27.4 EV/EBITDA (x) 29.7 26.1 22.9 19.4 ROAE (%) 109.0 109.9 109.7 111.1

Transcript

Edelweiss Research is also available on www.edelresearch.com, Bloomberg EDEL <GO>, Thomson First Call, Reuters and Factset. Edelweiss Securities Limited

We recently met Ms. Prabha Parameswaran, Managing Director, Colgate‐Palmolive India (Colgate). She reiterated that there is no slowdown in growth, except for some impact in the mouthwash segment. Management expects sales growth momentum (16% CAGR over FY08‐13) to remain robust riding rise in both penetration (rural stands at only 63% against 91% in urban) and per capita consumption (India half of China; pushing “brushing twice”). We believe the company is well equipped to counter competition from P&G’s impending entry in the toothpaste market. However, we expect ad spends in the toothpaste category to accelerate (will aid broadcasters like ZEE, Sun TV). Maintain ‘HOLD’.

Premiumisation, penetration, consumption: Growth mantra Colgate will focus on increasing rural penetration and per capita consumption. Premiumisation will aid gross margin (globally, Colgate’s margins are 5‐7% higher than in India). Premium segment now contributes 10% to sales versus negligible earlier.

Our view: Well equipped to tackle fresh competition In our view, P&G’s impending entry seems ill‐timed. Since the entry has been anticipated for years, existing players are well prepared—Colgate, HUL and Dabur have stepped up aggression in distribution, innovation and promotion; GSK is well entrenched in the premium segment. It will thus be a difficult and expensive affair for P&G. The toothpaste market, in our view, is the toughest nut in the Indian consumer space to crack as it is strongly dominated by Colgate, armed with an increasing and highest‐ever market share. Also, as P&G sharpens focus on the toothpaste category, its focus on shampoos, skin cream and detergents is likely to wane, benefiting HUL, Dabur etc. Thus, we expect P&G’s entry to be gradual and selective.

Outlook and valuations: Robust; maintain ‘HOLD’ We continue to like Colgate’s strong distribution, generic brand, customer activations and innovation. Currently, the stock is trading at 31.8x and 27.4x FY14E and FY15E EPS, respectively. We maintain ‘HOLD’ and rate the stock ‘Sector Performer’.

VISIT NOTE

COLGATE PALMOLIVEFore warned is fore armed

EDELWEISS 4D RATINGS

Absolute Rating HOLD

Rating Relative to Sector Performer

Risk Rating Relative to Sector Medium

Sector Relative to Market Overweight

MARKET DATA (R: COLG.BO, B: CLGT IN)

CMP : INR 1,288

Target Price : INR 1,411

52‐week range (INR) : 1,580 / 1,097

Share in issue (mn) : 136.0

M cap (INR bn/USD mn) : 182/ 3,107

Avg. Daily Vol.BSE/NSE(‘000) : 108.3

SHARE HOLDING PATTERN (%)

Current Q3FY13 Q2FY13

Promoters *

51.0 51.0 51.0

MF's, FI's & BK’s 5.2 5.4 6.0

FII's 21.6 21.6 20.9

Others 22.2 22.1 22.1 * Promoters pledged shares (% of share in issue)

Meeting with Ms. Prabha Parameswaran | Key takeaways No slowdown in the toothpaste category: Despite some top‐end personal care categories facing slowdown, demand for Colgate continues to be robust in toothpaste. However, mouthwash growth has slackened (currently growing at 10‐12% YoY as against 25‐30% two years back). Premiumisation: The discretionary slowdown has also failed to impact premiumisation as higher disposable incomes in hands of consumers is leading to up‐trading to higher price packs, brands. Over the past two years, premiumisation growth has been dramatic, which is evident from the premium segment now contributing ~ 10% to sales versus negligible a few years ago. Globally, Colgate Total as percentage of sales is equivalent to contribution from Colgate Dental Cream in India; Brazil’s toothpaste market 10 years ago is where the Indian toothpaste market currently stands. This provides ample evidence of likely consumer up‐trading as the economy evolves. Gross margin is likely to expand as product mix improves (globally Colgate’s gross margins are 5‐7% higher than in India, due to higher sales from Colgate Total, sensitive and other premium products). Growth opportunity: Colgate has posted 16% CAGR over FY08‐13 and is confident of growing strongly in the coming years. Growth opportunity stems from: (i) toothpaste category’s rural penetration at 63% (up from 42% in 2006) against 91% in urban areas; and (ii) India’s per capita consumption being lowest in the world (at 137g). Rural opportunity remains bright: Good monsoons, higher support prices for crops and NREGA scheme will ensure higher disposable incomes coupled with adequate product availability (due to enhanced rural reach) which will help boost rural penetration. Strategy to increase consumption: India’s per capita consumption (PCC) is at 137g/year, half of that in China (277g) and one‐fifth of US and Brazil. If the consumption reaches even that of China, the toothpaste market will double. PCC has grown from 125g three years ago to the current primarily due to new users (converted significant number of non‐users and infrequent users to frequent users) and not so much due to habitual change (brushing twice) which provides huge headroom for growth. Colgate is working towards this goal by promoting night brushing which needs bringing about a change in the socio‐cultural behaviour. Government support in many other countries like Brazil, Sri Lanka plays a key role in imbibing “brushing twice” as a habit through school programmes. In India, the company has a drive “Bright Smiles Bright Futures”, which involves free dental check‐ups and teaching oral hygiene in schools; Colgate has touched ~100mn children through this drive till now. Market share: In the toothpaste category, Colgate’s volume market share increased to 55.4% in Q4FY13 (up 130bps YoY). The next two competitors have a market share of 23.5% and 13.2%, respectively. Toothbrush volume market share increased sharply to 41.5% in Q4FY13 (up 380bps YoY). The next two competitors have a market share of 19.0% and 7.8%, respectively. Colgate’s volume market share in the mouthwash category stood at 26.5% in Q4FY13 (up 30bps YoY).

Mouthwash: The category is in infancy and is bound to grow rapidly in larger cities in the coming years. Colgate is encouraging category growth with regular promotions in smaller SKU (60ml priced at INR40) to induce repeat purchase due to eventual habit formation. We believe uni‐dosage is a growth opportunity in the mouthwash space which will help rapid category expansion. New launches: Colgate launched whitening toothpaste Colgate Visible White offering whiter teeth (improvement by one shade) in just one week; priced at INR79 for 100g and INR40 for 50g. Colgate has roped in Sonam Kapoor as the brand ambassador for this product. Portfolio gap with parent: The company has brought in several products from the global portfolio to India, the latest being Colgate Visible White. It will continue this depending on the development of the Indian toothpaste market and probability of acceptance by the Indian consumer. Colgate’s Indian portfolio will thus never be complete due to the dynamic nature of the market where lifestyle changes provide opportunity for newer solutions (new toothpaste offerings) to be introduced. Handwash segment: Colgate remains open to the handwash category (which is a stronghold in many other markets) when the category evolves from the current positioning of markets on anti‐bacterial products to more premium and differentiated offerings like moisturizing and fragrance oriented products gaining centre‐stage (which is the company’s forte). R&D centre: Colgate has an Indian R&D centre dedicated to local research which reports to the global research centre. This helps address local needs with global technological support. Active salt and toothpowder were designed specifically to cater to the Indian cultural needs. Though localisation focused innovation is of prime importance currently, as people’s exposure to global environment increases, replicating the global portfolio will become more relevant. Pricing strategy: Colgate uses analytics to measure price sensitivity and accordingly takes pricing action to ensure minimum impact on volume growth. For instance, pricing action is less aggressive in categories like the INR5 price point and the 50g pack where users are price sensitive. Raw material also plays a vital role in determining pricing action. Sensitive toothpaste category: Rising awareness among consumers has rendered the sensitive toothpaste category a highly attractive segment to operate in. The segment has been growing at a higher clip (over a low base) and also at the cost of toothpastes positioned as herbal and medical. Currently, ~17% of population is a potential customer of this category; hence, it is likely to be significantly large category of the total toothpaste market in the next three to five years. Competition in the category has helped expand size which is likely to help Colgate. Mouthwash: The INR1bn category has been growing at a strong 30% YoY. However, being a discretionary product, some slowdown is likely in the near term. Colgate’s main competitors across the globe include Johnson & Johnson, GSK and P&G. Tax rate: Tax rate is expected to inch up 150bps each for FY14E and FY15E as the Baddi manufacturing facility moves out of tax exemption.

Consumer Goods

4 Edelweiss Securities Limited

Existing competition: In Q4FY13, Colgate’s strongest competitor in the toothpaste category, Hindustan Unilever (HUL), posted double digit growth (largely volume led) in its oral care portfolio. Also, the third largest player in the category, Dabur’s oral care portfolio grew 12.3% YoY. GSK Consumer launched new toothpaste from its global portfolio, Parodontax, in the gum care segment priced at INR100 for 80g; and a new variant of Sensodyne – Repair & Protect that repairs teeth enamel damaged due to sensitivity. Competition in the sensitive category: As per Nielsen, GSK Consumer (Sensodyne) has overtaken Colgate (Sensitive) in the sensitivity toothpaste segment with a market share of 26% against Colgate’s 25%. Figures are for March. We believe the market share gain by GSK is primarily due to stronger distribution of GSK Pharma in the chemist channel. Sensitive toothpaste market is 5% of toothpaste market, but has been growing at a fast rate due to premiumisation. The company aims to expand its pharmacy network to increase Sensitive sales. Colgate continues to be a mass focused brand. P&G’s impending entry in toothpaste: P&G has announced that it will soon be entering the Indian toothpaste market under the Oral‐B brand. Globally, Colgate has been able to maintain market share in most markets when P&G entered. Also Colgate with products spanning the entire price ladder is well poised to counter competition. In other markets like Mexico and Brazil, P&G had pitched Oral B against Colgate Total. However, Colgate will have to increase ad spends to maintain competitive intensity. We believe P&G’s entry is a logical step since it is already doing well in the toothbrush category, though the company has been late to enter the market. Past two years performance has been below expectation (in terms of profitability); the Indian toothpaste market is a tough nut to crack as it is strongly dominated by Colgate, which has sustained its leadership for decades owing to its robust distribution network, strong brand equity, over 75 years of presence in the category (which has made it a generic brand) and high level of consumer awareness programmes through continuous on ground events. Since P&G’s entry has been expected for a long time, competitors are well prepared for the onslaught; Colgate, HUL and Dabur have been aggressive on distribution, innovation (Colgate Whitening, Dabur’s Babool with salt; HUL’s Germ Protection) and promotion (“Fly to HongKong for a magical Disney Experience” in Pepsodent by HUL). It will thus be a difficult and expensive affair for P&G to gain a large market share in the Indian toothpaste market. We do expect ad and promotional expenses to step up with the heightened competitive intensity. It can potentially aid volumes for Colgate as increased noise in the space will help market growth, benefiting the leader the most (is always ahead of the curve with innovative and timely launches). Also, as P&G increases focus on the toothpaste category, its focus on shampoos, skin cream and detergents could likely reduce, benefiting HUL, Dabur etc. Thus, we expect P&G’s entry to be gradual and selective.

Status in other countries Through various innovative techniques and a strong distribution network, Colgate has been able to improve its global market share in both toothpaste and toothbrush categories over the past decade.

P&G is aggressively increasing visibility of Oral‐B brand

Colgate Palmolive

5 Edelweiss Securities Limited

With the entry of new players, the company has more or less retained market share while new players have gained market share from the No. 2 player. Currently, Colgate is well placed across the globe with over three times the market share of its nearest competitor. Brazil and China: In Brazil, Colgate has maintained its leadership and has managed to gain market share at the expense of the No. 2 player. Its leadership continues in China, whereas competitors have lost market share. The company continued its toothpaste leadership in Greater Asia, driven by market share gains in India, China, Thailand, the Philippines, Singapore and Vietnam. Successful new products including Colgate Optic White, Colgate Total Pro Gum Health, Darlie Enamel and Darlie Expert White toothpastes contributed to volume growth throughout the region. US: Unlike other US consumer companies, Colgate was strong in international markets and weak in the US, until it decided to focus on core oral care portfolio and take leading competitors (P&G and Unilever) head on in 1994. The company closed plants, reorganised supply chain, implemented SAP software and invested in neglected brands, including Colgate Toothpaste. In a stagnant US toothpaste market, Colgate's share climbed from 21.3% in 1994 to 26.2% in 1997 according to A.C. Nielsen. During the same period, P&G's market share fell from 31.6% to 25.3%.

Outlook and valuations: Fairly valued; maintain ‘HOLD’ We continue to like Colgate’s focus on activations, innovation, distribution expansion and building brand equity. We have cut our EPS marginally for FY14E and FY15E 1.9% and 1.4%, respectively (to INR40.5 and INR47.0) due to step up in ad costs due to entry by P&G. However, we believe P&G’s entry will lead to market expansion. We value Colgate at P/E of 30x FY15E (at a slight discount to HUL valued at 32x FY15E) arriving at a target price of INR1,411. We maintain ‘HOLD’ and rate the stock ‘Sector Performer’ on relative return basis.

Consumer Goods

6 Edelweiss Securities Limited

Chart 1: Per capita consumption of toothpaste low in India

Chart 2: Comparison of rural vs urban penetration of toothpaste in India

Chart 3: Overall volume growth (%)

Source: Company, Edelweiss research

100

220

340

460

580

700

Brazil USA Philippines China India

(Gms/year)

20.0

35.8

51.6

67.4

83.2

99.0

2005 2006 2007 2008 2009 2010 2011 2012

(%)

Rural Urban

2.0

5.2

8.4

11.6

14.8

18.0

FY08 FY09 FY10 FY11 FY12 FY13

(%)

Colgate Palmolive

7 Edelweiss Securities Limited

Chart 4: Toothpaste volume growth (%)

Chart 5: Gross margin comparison with peers

Source: Company, Edelweiss research

Fig. 1: Colgate—Global leader in toothpaste and toothbrush categories

Colgate earns one of the highest margins in the Consumer space owing to its dominance in the category and strong brand equity. Margins could come under pressure as pricing power moderates due to P&G's foray into the Indian toothpaste space.

Consumer Goods

8 Edelweiss Securities Limited

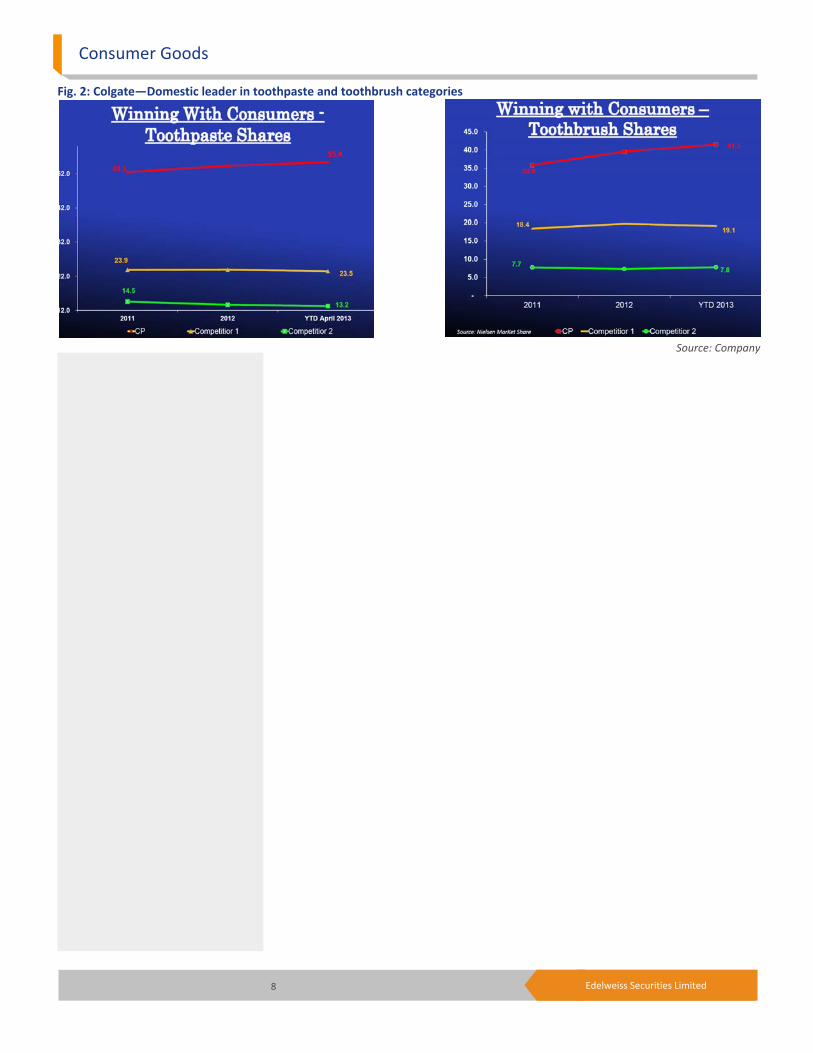

Fig. 2: Colgate—Domestic leader in toothpaste and toothbrush categories

Source: Company

Colgate Palmolive

9 Edelweiss Securities Limited

Company Description Colgate is India’s biggest oral care products company with more than 95% of its sales coming from this product category. The company has products across variants and price points in toothpaste, toothpowder, and toothbrushes, and is the leader in each of these categories.

Investment Theme Colgate is market leader in oral care category with ~55.4% market share in toothpaste category and enjoys strong brand equity, built over the years through high investment on creating consumer awareness and brand recall. Volume growth would also remain robust riding rise in both penetration and per capita consumption. Also, new categories like sensitive toothpaste and mouthwash will further enhance growth and premiumisation. However, higher competition will induce Colgate to increase its brand spends, which could cap its margins.

Key Risks New entrants like P&G could hit the company hard. Further risks arise from down trading by consumers due to the delayed monsoon, gloomy macroeconomic environment and rising food inflation. Deficient rainfall could impact agricultural activity, which in turn could hit rural demand. Sharp rise in input prices or continued depreciation of the INR could increase cost of imported chemicals.

10 Edelweiss Securities Limited

Consumer Goods

Financial Statements

Income statement (INR mn)

Year to March FY12 FY13 FY14E FY15E

Net revenue 26,239 30,841 35,961 42,074

Other Operating Income 694 797 899 1,094

Total operating income 26,932 31,638 36,860 43,168

Oppenheimerfunds Incorporated 5.64 Arisaig Partners Asia Pte Ltd 3.53

Life Insurance Corp Ltd 3.53 Virtus Emerging Markets 1.24

Harris Trust & Savings Bank 1.24 Wasatch Advisors Inc 1.15

Vontobel Asset Management AG 0.80 Columbia Wanger Asset Management 0.75

Eastspring Investments Singapore 0.66 Vanguard Group Inc 0.53

*as per last available data

Insider Trades Reporting Data Acquired / Seller B/S Qty Traded No Data Available

*in last one year

Bulk Deals Data Acquired / Seller B/S Qty Traded Price No Data Available

*in last one year

Additional Data

Directors Data Mukul Deoras Chairman Mr. R. A. Shah Vice Chairman P.K. Ghosh Deputy Chairman Prabha Parameswaran Managing Director Paul Alton Whole‐time Finance Director Niket Ghate Whole‐time Director, Company SecretaryVikram Singh Mehta Executive Director J.K. Setna Non‐executive Director Indu Shahani Non‐executive Director

Buy appreciate more than 15% over a 12‐month period

Hold appreciate up to 15% over a 12‐month period

Reduce depreciate more than 5% over a 12‐month period

Rating Expected to

15 Edelweiss Securities Limited

Colgate Palmolive

DISCLAIMER General Disclaimer:

This report has been prepared by Edelweiss Securities Limited (Edelweiss). Edelweiss, its holding company and associate companies are a full service, integrated investment banking, portfolio management and brokerage group. Our research analysts and sales persons provide important input into our investment banking activities. This report does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The information contained herein is from publicly available data or other sources believed to be reliable, but we do not represent that it is accurate or complete and it should not be relied on as such. Edelweiss or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. This report is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this report should make such investigation as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this report (including the merits and risks involved), and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors. We and our affiliates, group companies, officers, directors, and employees may: (a) from time to time, have long or short positions in, and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as advisor or lender/borrower to such company (ies) or have other potential conflict of interest with respect to any recommendation and related information and opinions. This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Edelweiss and affiliates/ group companies to any registration or licensing requirements within such jurisdiction. The distribution of this report in certain jurisdictions may be restricted by law, and persons in whose possession this report comes, should inform themselves about and observe, any such restrictions. The information given in this report is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. Edelweiss reserves the right to make modifications and alterations to this statement as may be required from time to time. However, Edelweiss is under no obligation to update or keep the information current. Nevertheless, Edelweiss is committed to providing independent and transparent recommendation to its client and would be happy to provide any information in response to specific client queries. Neither Edelweiss nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Past performance is not necessarily a guide to future performance. The disclosures of interest statements incorporated in this report are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. Edelweiss Securities Limited generally prohibits its analysts, persons reporting to analysts and their dependents from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. The information provided in these reports remains, unless otherwise stated, the copyright of Edelweiss. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright Edelweiss and may not be used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders. Analyst Certification:

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. Analyst holding in the stock: No. Edelweiss shall not be liable for any delay or any other interruption which may occur in presenting the data due to any reason including network (Internet) reasons or snags in the system, break down of the system or any other equipment, server breakdown, maintenance shutdown, breakdown of communication services or inability of the Edelweiss to present the data. In no event shall the Edelweiss be liable for any damages, including without limitation direct or indirect, special, incidental, or consequential damages, losses or expenses arising in connection with the data presented by the Edelweiss through this presentation.

16 Edelweiss Securities Limited

Consumer Goods

Access the entire repository of Edelweiss Research on www.edelresearch.com

Disclaimer for U.S. Persons

This research report is a product of Edelweiss Securities Limited, which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker‐dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker‐dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by Edelweiss Securities Limited only to "Major Institutional Investors" as defined by Rule 15a‐6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor.

In reliance on the exemption from registration provided by Rule 15a‐6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, Edelweiss Securities Limited has entered into an agreement with a U.S. registered broker‐dealer, Enclave Capital, LLC ("Enclave").

Transactions in securities discussed in this research report should be effected through Enclave Capital, LLC.

Disclaimer for U.K. Persons

The contents of this research report have not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 ("FSMA").

In the United Kingdom, this research report is being distributed only to and is directed only at (a) persons who have professional experience in matters relating to investments falling within Article 19(5) of the FSMA (Financial Promotion) Order 2005 (the “Order”); (b) persons falling within Article 49(2)(a) to (d) of the Order (including high net worth companies and unincorporated associations); and (c) any other persons to whom it may otherwise lawfully be communicated (all such persons together being referred to as “relevant persons”).

This research report must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this research report relates is available only to relevant persons and will be engaged in only with relevant persons. Any person who is not a relevant person should not act or rely on this research report or any of its contents. This research report must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person.

Disclaimer for Canadian Persons

This research report is a product of Edelweiss Securities Limited ("ESL"), which is the employer of the research analysts who have prepared the research report. The research analysts preparing the research report are resident outside the Canada and are not associated persons of any Canadian registered adviser and/or dealer and, therefore, the analysts are not subject to supervision by a Canadian registered adviser and/or dealer, and are not required to satisfy the regulatory licensing requirements of the Ontario Securities Commission, other Canadian provincial securities regulators, the Investment Industry Regulatory Organization of Canada and are not required to otherwise comply with Canadian rules or regulations regarding, among other things, the research analysts' business or relationship with a subject company or trading of securities by a research analyst.

This report is intended for distribution by ESL only to "Permitted Clients" (as defined in National Instrument 31‐103 ("NI 31‐103")) who are resident in the Province of Ontario, Canada (an "Ontario Permitted Client"). If the recipient of this report is not an Ontario Permitted Client, as specified above, then the recipient should not act upon this report and should return the report to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any Canadian person.

ESL is relying on an exemption from the adviser and/or dealer registration requirements under NI 31‐103 available to certain international advisers and/or dealers. Please be advised that (i) ESL is not registered in the Province of Ontario to trade in securities nor is it registered in the Province of Ontario to provide advice with respect to securities; (ii) ESL's head office or principal place of business is located in India; (iii) all or substantially all of ESL's assets may be situated outside of Canada; (iv) there may be difficulty enforcing legal rights against ESL because of the above; and (v) the name and address of the ESL's agent for service of process in the Province of Ontario is: Bamac Services Inc., 181 Bay Street, Suite 2100, Toronto, Ontario M5J 2T3 Canada.

Copyright 2009 Edelweiss Research (Edelweiss Securities Ltd). All rights reserved