sponsored by Asset Finance Pricing Review Taking the guesswork out of Total Cost of Ownership Colin Tourick analyses the current boom in UK fleet sizes Experteye spots RV variation across Europe Fleet leasing in Germany powers ahead

Transcript

1

Asset financepricing review

Pricing action plan for improved profits

Best practices for setting residual values

Kwik Fit’s fast fit,service excellence and

savings

sponsored by

Car WarsBryan Marcus reconciles divergentpricing perspectives between salesdirector and CFO

Volume, market share or profit. What’s your primary pricing priority?

Asset FinancePricing Review

Taking the guesswork out of Total Cost

of Ownership

Colin Tourick analyses the current boom in

UK fleet sizes

Experteye spots RV variation across Europe

Fleet leasing in Germany powers ahead

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

2

IntroductionWelcome to the latest edition of our Asset Finance Pricing Review, published in association with Asset Finance International.

We start by taking a close look at what’s driving fleet markets to new heights in the UK. We also spotlight fleet leasing in Germany and total cost of ownership in fleets. Our aim, as always, is to shine a light in the otherwise dark corners of vehicle asset finance pricing.

Early autumn has witnessed unprecedented upheaval in the motor industry, following the VW emissions scandal. We have yet to see what the long-term implications will be for the sector, but suffice to say consumers and fleet vehicle purchasers are likely to be sceptical towards manufacturers’ efficiency claims, which will make it harder for lessors and OEMs to charge a premium for fuel-efficient products. You’ll find more on this in the news section starting on page 19.

But we begin this issue with automotive sector expert Professor Colin Tourick and the BVRLA (British Vehicle Rental and Leasing Association) revealing details of their latest research findings on the UK market. Interestingly, many of the factors driving economic austerity appear to be aiding and abetting UK growth in the vehicle leasing and rental sectors.

Starting on page 7, our own operations director Owen Goschen talks about total cost of ownership in fleet, and how technology can provide valuable information where and when it’s needed to enable managers to make better cost cutting decisions.

Fleet leasing in Germany is currently experiencing growth and innovation and Asset Finance International’s author of country reports Nigel Carn takes us through the country’s story to date, starting on page 10. Vehicle market trends, the importance of the fleet sector to Germany, developments in mobility and innovation are all covered.

A round-up of key news stories, including VW, used car sales, BVRLA’s new-look fraud fighting system and the European new car market is found starting on page 19,along with details of telematics specialist Motrak’s introduction of in-vehicle CCTV.

We end as usual with ExpertEye’s forecasts for residual values across Europe.

We hope you’ll agree that we’ve crammed a lot into this issue, with a great deal of valuable insight from industry experts on offer and, as ever, we welcome your feedback.

Gary JefferiesSales and Marketing Director, Bynx

Introduction

Welcome to the sixth edition of Asset Finance Pricing Review, published incollaboration with Asset Finance International and Professor Colin Tourick.

As in all previous issues, we again put forward a host of articles from industryinsiders that serve to illuminate the more challenging aspects of asset financepricing. The purpose is to bring you valuable insights, knowledge and examples.

In any company, there are different stakeholders involved in pricing policy andexpecting sales and finance to see eye-to-eye on every issue is the stuff of fantasy.This is especially true for businesses that operate internationally and have to takeinto account the cultural, political, financial and regulatory differences within thosemarkets. In Car Wars – reconciling divergent views on manufacturer auto financepricing (pages 3-5), Bryan Marcus, regional director of VWFS Latin America,Canada and Northern Europe, offers an interesting perspective on resolving pricingdisputes – and one that doesn’t involve leather gloves and a boxing ring!

There are many ‘levers to profit’ in every asset finance business but the one thatwill have the greatest impact on the bottom line is changing your pricing policy.This is the advice of Professor Colin Tourick, management consultant and editor ofAsset Finance Pricing Review, in The pricing action plan for profit (pages 6 and 7).

There’s only one topic (other than pricing policy) that can claim joint ownership ofthe most-difficult-aspect-to-get-right-in-asset-finance title and that is settingResidual Values (RVs). But it’s not just a matter for vehicle leasing and daily rentalcompanies, states Dean Bowkett, technical director and chief editor atEurotaxGlass’s. In his article Setting Residual Values (pages 8-10), he examines thepitfalls and best practices and offers a unique perspective on how it matters forOEMs too.

Page 11 presents the results of our last Pricing Survey, which posed questionsaround how to pitch pricing at a level that delivers the most new business andhighest margins. As ever, the results surprised us. They may surprise you too orperhaps confirm your prior thinking. Either way, get in touch and give us yourperspective.

Take part in our next survey

We’re very grateful to everyone who takes part in our surveys (you can do soanonymously if you like) because they always provide us with valuableunderstanding and ideas. This time we’re asking: What is the primary considerationwhen your asset finance business sets its prices/issues a quote? You can take parthere: http://bit.ly/bynxpr5.

It’s always interesting to read how suppliers work successfully with leasingcompanies and Kwik Fit GB is no exception. In an article, Kwik Fit GB fast fitsdeliver service excellence and financial savings (pages 12 and 13) Peter Lambert,fleet director, talks us through how the fast fits concept is delivering tangible resultsfor leasing companies.

We end this Pricing Review with the latest figures on changes in residual valueforecasts, SMR costs and lease rental rates across Europe (to January 2014) frombenchmarking and research specialist Experteye.

And don’t forget to share your feedback with us and tell us what you’d like to seein future Pricing Reviews.

Gary JefferiesSales and Marketing Director, Bynx

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

3

BVRLA member fleets drive UK market to new highs Fleet sizes are increasing at an impressive rate, with leasing numbers hitting all time records, suggesting that careful pricing and a sound understanding of the market are reaping rewards in both the corporate and personal sectors

By the time you read this it is quite likely that BVRLA (British Vehicle Rental and Leasing Association) member fleets will exceed 4.25 million vehicles for the first time ever. If this rate of growth continues, the total fleet could reach five million in the next 18 months or so which is double the number in 2008. This remarkable success story no doubt owes a lot to the recovery in th UK economy since the financial crisis, and to the ability of BVRLA members to both stimulate demand and to meet that demand. This article will explore the figures in more detail and try to provide some lessons for other fleet markets.The BVRLA carries out its most detailed survey of member fleets once a year and asks members for trends in the interim. At the end of last year BVRLA members funded and managed 3,856,747 vehicles, from cars to heavy commercial vehicles and for consumers, SMEs and large fleets across the UK.The breakdown is as follows:

Vehicle type Type Fleet size 2014 Membership trends 2015Car Corporate leasing 1,820,828 Growing same rateCar Personal leasing 1,078,208 Rapid growth slowingCar Short term rental 245,730 Growing fasterCommercial vehicle Corporate leasing 70,217 Growing same rateCommercial vehicle Personal leasing 742Commercial vehicle Short term rental 44,826 Growing fasterLight commercial vehicle Corporate leasing 456,034 Growth slowingLight commercial vehicle Personal leasing 18,921 Rapid growth slowingLight commercial vehicle Short term rental 121,241 Growing fasterTOTAL 3,856,747

Source: BVRLA

Space does not allow discussion of each section of the market so we will just look at a few of these categories. The biggest category of course is cars leased to businesses. Of the 1,820,828 total at the end of 2014, volumes for both cars funded on contract purchase and cars purchased on finance leases remained largely unchanged over the previous year, confirming their relative unpopularity amongst corporate clients.

Professor Colin Tourick

Forecast Car ResidualsRise as Optimism Returns

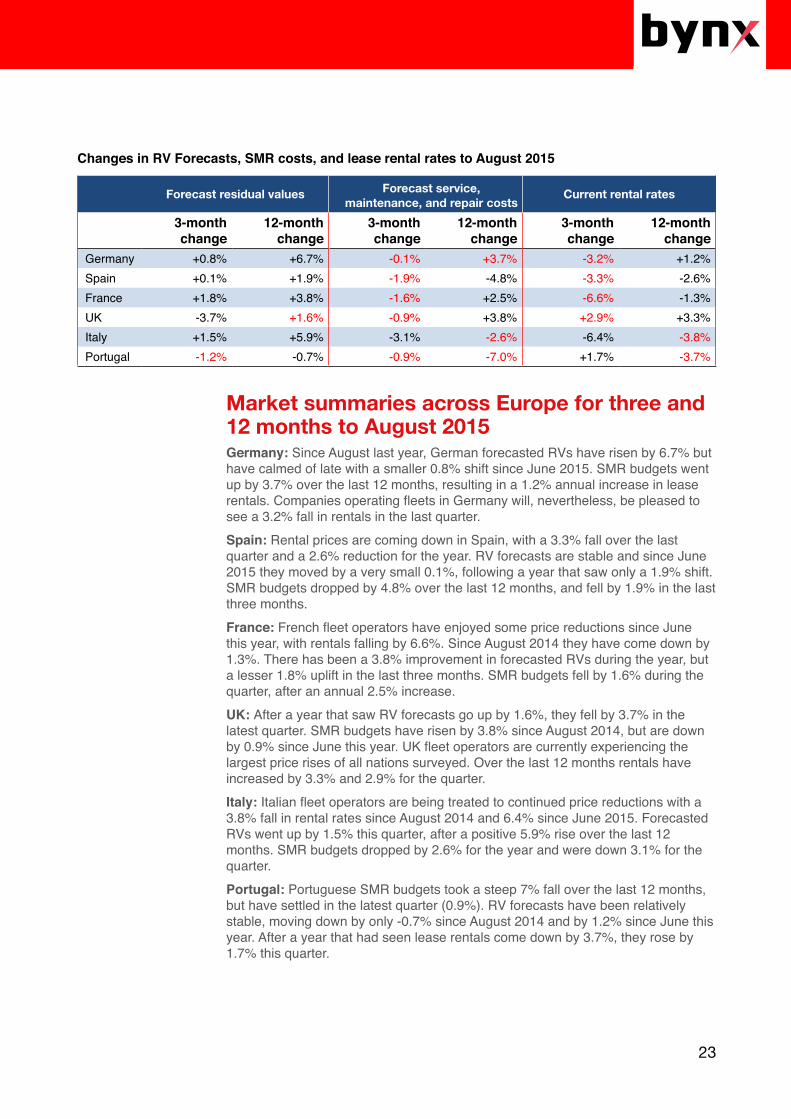

Changes in residual value (RV) forecasts, SMR costs and lease rental rates to January 2014Forecast residual values Forecast service, Current rental rates

It appears that fleet lessors across Europe arebecoming increasingly optimistic about futureresidual values. To end, January we sawlessors increase their forecast RVs by 2.8% inthe UK, 1.1% in Italy, 0.9% in Germany, 0.7%in Portugal and 0.2% in France. Spain reportedthe only reduction and this was by just 0.1%).

These figures are collated by Experteye’sEuropean Leasing index survey which tracksforecasted residual values (RV), servicing,maintenance and repair (SMR) costs and rentalrates in six European countries using datasupplied by major leasing companies.

Looking over the past 12 months we can seethat at one extreme forecast RVs rose by 7.3%in the UK, and at the other extreme they fell by2.6% in Portugal.

Forecast SMR costs have also stabilisedsomewhat over the last three months, havingsuffered significant falls in Spain, Portugal, Italyand Germany in the previous nine months.

Rentals seem to have stabilised somewhat tooin the last three months, having been quitevolatile in the UK, Portugal and Germany inparticular in the previous nine months.

Professor Colin Tourick is a management consultant, former MD of Citibank's fleet leasingbusiness and a 34 year leasing industry veteran

• The comparisons are for vehicles with a contractduration of 36 months / 90,000 KM• Twelve month comparisons show change sinceFebruary 2013• Three month comparisons show change sinceNovember 2013. • Rental rate changes compare the rates in effect atthe time of the survey with those in effect three ortwelve months ago.

• RV and SMR changes show the change inparticipating leasing companies' forecasts of residualvalues and maintenance costs over the period.The Experteye European Leasing Index reports ontrends in leasing company forecasts, plus currentrental rate movements, covering representativeversions of up to 250 vehicles in the six markets.

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

4

Outsourcing wins fansIn contrast, contract hire growth hit record levels, which shows the enduring strength of this product, and probably says something about clients realising that with contract hire they get all of the benefits of outsourcing in a relatively straightforward product that allows them to get on and run their core business without the need to become experts on the automotive industry. The BVRLA statistics also show that its members managed increasing numbers of cars under fleet management contracts, which have been rising steadily. No doubt the reason for the success of this product was the same as for contract hire: the continued growth in businesses recognising the power of outsourcing.In the most recent survey carried out this year, BVRLA members reported that contract hire had continued to grow at the same speed as in 2014, which suggests that by the end of this year there will be more than 1.6 million contract hire vehicles in the UK. These figures offers great ammunition to fire back at those who say “the company car is dead”. Contract hire is popular because it appeals to so many different parts of the market – from public sector and the biggest corporate right down to the SME – and also because it delivers real cost benefits to most clients compared with outright purchase. A client that wants to do a quick evaluation of the benefits – comparing the rental costs over three years against the depreciation if they buy outright and maintain the car themselves – will usually find that contract hire is cheapest. And if they decide to do a more detailed evaluation – taking into account every cash flow likely to arise over the course of three or four years should they opt to lease or buy, including the VAT and tax cash flows – they will generally find that contract hire emerges as the winner here too.

Personal leasing popularThe second most popular form of car finance is personal leasing. The growth in demand for this product in the UK in recent years has been astonishing and this growth has continued during 2015, albeit at a slower pace. It is interesting to look for reasons why this product should have become so sought after. Paradoxically, the major reason probably owes a lot to UK house prices. These have become so unaffordable – out of step with average earnings – that people in their late teens and early twenties have come to realise that a house purchase is something they will need to put off for some years because they cannot afford either the deposit or the repayments. They have become the “stay with parents” generation, leaving home perhaps a decade later than would have been the case in the 1960s, and even then deciding first to rent rather than buy because of the problem of raising a deposit. Whilst low mortgage interest rates have encouraged some young people to step onto the housing ladder, others have remained concerned that interest rate rises will leave them financially stretched. In much the same way as this generation don’t value house ownership, it seems they don’t value car ownership either, and they are happy to rent a car or belong to a car club if they have the occasional need for a car, rather than buying one. The trend for young people to move to cities has encouraged this phenomenon: a car can be a liability in a city centre. And when they do decide to have their own car,

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

5

leasing provides the ideal solution: renting rather than owning, but just for a longer period. Brokers have also played a part in the growth of personal leasing. Many broker websites offer lease cars at remarkably affordable prices, which they are able to do either because of special deals direct with manufacturers or because they are particularly adept at identifying and promoting the best deals on offer from the leasing companies. Personal contracts currently account for 33% of the fleet of cars placed by brokers with contract hire companies in the UK, probably because brokers tend to do a high percentage of business with SMEs where the business is operated as a sole trader or partnership rather than a company.

Source: Data to 2014 BVLRA; 2015 projection University of Buckingham

Vans move into the fast laneThe final category of note is the leasing of light commercial vehicles (LCVs) to corporate businesses. This has been a real success story for leasing companies, and there are currently twice as many leased vans than in 2009. Unlike with cars, where the VAT rules normally help make a strong financial case for leasing rather than outright purchase, with LCVs there is often little difference when a financial analysis is carried out on whether to lease or buy a van. Success in this segment of the UK market has therefore come from a combination of factors. These include the trend for leasing companies to build specialist teams

2008 2009 2010 2011 2012 2013 2014 2015 (proj)

BVRLA member fleet

Car corporate leasing

Car personal leasing

LCV corporate leasing

Car short term rental

CV corporate leasing

LCV short term rental

CV short term rental

2,000,000

1,800,000

1,600,000

1,400,000

1,200,000

1,000,000

800,000

600,000

400,000

200,000

–

Vehi

cles

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

6

of LCV experts who better understand the needs of customers in this sector. In addition, customers are becoming more enamoured with the idea that they can offload the residual value risk if they lease rather than buy. Also, it is quite likely that the strength of the UK economy has made companies more relaxed about entering into a fixed term commitment and handing back the vehicle at the end, rather than buying outright and retaining the flexibility about how long to hold on to it. Taken overall, the figures reported by the BVRLA show how very strongly the industry has bounced back since the recession, suggesting that it is now powering ahead and with few obstacles in sight. This revved up performance is no accident, however. Rather, it is the result of careful analysis of what customers want, shrewd pricing strategies, and a willingness to invest time and money in delivering innovative new solutions. The UK fleet market thus provides lessons from which some European leasing companies can learn a lot.

Colin Tourick, Grant Thornton Professor of Automotive Management at the University of Buckingham. Colin is a management consultant, 35-year leasing industry veteran and the former MD of Citibank’s fleet leasing business.

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

7

Total Cost of Ownership in fleet management – how technology is replacing guess workOwen Goschen, operations director, Bynx looks at how technology can support fleet managers by providing the data they need to keep costs to a minimum

There are many cost elements within a fleet business that contribute to the total cost of ownership (TCO) of vehicle assets. While some, such as depreciation, fuel consumption and service, maintenance and repair (SMR), are more obvious than others, in such complex businesses it’s almost impossible to know through pure guesswork which initiatives will have the greatest impact on TCO over the long-term. Hypothesis, however, has been the most widespread option for too long. Until recently, the limitations of technology have prevented adequate data gathering and without relevant and realtime intelligence, it’s impossible to make informed decisions. That’s now changing as technology - and fleet management systems in particular - are playing a pivotal role in reducing TCO.There are many ways to reduce fleet costs: decreasing fleet size, better monitoring of driver territories, downsizing vehicles, retraining drivers and so on, but each in itself carries a cost. Knowing where investment will make the biggest impact is hard and time consuming without the aid of technology to bring all the data on all the factors together.

Popular ways of reducing TCOBuying vehicles more cheaply reduces capital outlay at the beginning. But the question is whether this approach will deliver as many long-term benefits as looking at all the core costs of running the fleet put together: depreciation, interest payments, SMR, fuel consumption, insurance, tax and fees, combined.It’s not just fleet policy or vehicle choice that influence TCO, there are indirect costs too: employee productivity, driver and vehicle downtime, time spent on administration and fleet management processes, buildings and facilities, computer systems, utilities, tools and so on. All of them have a bearing on TCO - even if only in a small way.

Reducing fleet sizeReducing fleet size is often viewed as one of the best ways of decreasing TCO, or at least the one with the obvious potential to yield the biggest savings. It can cost between €2,800 and €5,500 per year to run one fleet vehicle, so reducing larger fleets by just 100 vehicles can bring significant savings. However, this will have an impact on the operating costs of the remaining fleet. If business volume increases

Owen Goschen

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

8

and more vehicles are required, operating costs will go up through having to either outsource to third parties or rent additional capacity.

Driver behaviourAnother potentially high-yielding strategy but one that’s more contentious, is driver behaviour. It is estimated that the way in which a person drives can impact fuel efficiency by as much as 30%. Hard acceleration or breaking, idling, inconsistent speeds, excessive use of air conditioning can all have a bearing. But that’s not all: monitoring driver territories better, enforcing personal use policies and directly relating mileage and time to the number of sales or service calls can also slash costs. This is one area in which technology is having the greatest impact right now. Telematics systems give fleet managers less obtrusive ways of making sure “someone’s watching” the way in which vehicles are being driven and where. People are generally less careful when no one’s looking and more careful when they’re being monitored.

Mitigating risk and downsizingSafety management and risk assessment programmes can help reduce accidents, which in turn will reduce insurance premiums and the costs associated with accident management. Telematics systems play a role here too, by gathering data from the vehicle and feeding it back into the fleet management system where it can be recoded and analysed.Downsizing (reducing the size and weight of vehicles) will reduce fuel costs. Newer vehicles offer greater fuel economy but the capital cost of buying or leasing them (even smaller ones) may outweigh fuel efficiencies. Smaller vehicles can also depreciate quicker than larger ones.

Longer lifeIn some markets a lack of capital funding has resulted in fleets holding on to vehicles for longer, thus increasing the lifetime of the asset and therefore lifecycle costs. However, older vehicles can cost more in maintenance, they consume more fuel because their efficiency is lower than newer models and their utilisation may decrease because they spend longer in the workshop. Understanding the optimum time for vehicles replacement in fleet management is another issue that demands better knowledge and data about how to plan replacement cycles. As well as keeping running costs to a minimum, maintaining vehicles in the best condition possible will undoubtedly preserve resale values.

A single source of the truth All of these requirements demand technology that can provide a completely accurate source of the truth: detailed, up to date information about how much vehicles are costing to buy and operate, how they are being used and what they are delivering in return, both during their contract lifetime and at the end of it.

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

9

With so much data coming in from so many different sources it can be hard to see the complete picture and to make those crucial TCO decisions quickly. The knowledge and expertise of fleet managers can never be underestimated but they need support, not only from higher up the management scale but from the information systems they use on a daily basis. It’s no good if they are only given half the picture and have to guess the rest - that’s still speculation.They need information at their fingertips in order to make the right decisions at the right time. The right information presented in the right way can assist fleet managers via alerts; add value via benchmarking; and help manage by exception. This kind of “dashboard” provides the tools to drive down TCO. The establishment of KPIs (key performance indicators) enables fleet managers to see where and how trends are evolving over time and management information compiled from reliable and smart data is what’s required. Implementing the right technology platform to underpin business will give fleet managers the information they need to fully evaluate financial decisions. Vehicle procurement, administration, operation and fleet processes can be made quicker, more cost-effective and efficient by a software system with fleet-specific applications built in. Quotation requests and acceptances can be automated, for example, rather than having to be done manually. The system can track agreements with suppliers, including discounts, bonuses and delivery costs. A solution that supports and integrates with tracking and telematics systems and that can pull data in from other areas of the business (operations and financial management, for instance) will allow fleet managers to monitor those aspects of the business such as driver behaviour and vehicle utilisation that have the greatest controllable influence over TCO. Armed with information, fleet managers can implement changes that help rather than restrict drivers and other stakeholders in the cost reduction process. It will also greatly assist safety and risk matters. Being more efficient overall is the key to cutting fleet administration and management. Providing employees with a system that is functional, intuitive and easy to use will boost productivity and morale. More than anything, however, knowing exactly what and where the costs lie within the business, being able to access that data, extrapolate and analyse it, pull off management reports and maintain accurate financial records will offer the best chance of seeing the big picture of fleet TCO, making informed decisions and achieving the best results.

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

10

Fleet leasing in Germany – strong growth and innovationNigel Carn, author of Asset Finance International’s country reports, takes a look at the finance and pricing challenges facing the vehicle leasing and fleet markets in Germany

Germany has considerably the largest vehicle production industry in Europe, with total production of all vehicle types approaching six million units in 2014, representing 35% of total EU production. Germany also has the greatest number of new vehicle registrations, with over three million new passenger car registrations in 2014 representing nearly a quarter of the EU total (source: European Automobile Manufacturers’ Association − ACEA). This market is in good health: according to the ACEA, in the first half of 2015 new passenger car registrations in Germany increased 5.2% compared to the same period a year earlier, to reach 1.62 million units. Automotive advisory services firm IHS predicts full-year registrations of 3.14 million units, a rise of 3.5% on 2014. However, take-up of alternatively-fuelled vehicles has been slow, with only around 3% of the national market share in 2014. Average emissions, although reducing, are the highest in the EU outside eastern Europe.

Vehicle leasing on a growth trackThe association covering all leasing market sectors is the Federal Association of German Leasing Companies (BDL). According to the BDL, total leasing new business volume (NBV) amounted to €48.6 billion in 2014, in which the auto sector is dominant, with passenger cars having 54% share and commercial vehicles (including trucks and buses) 16%. Both segments exhibited strong growth in 2014, with demand for passenger cars growing 9.9% and commercial vehicles up 11.7% on the previous year.Most leased vehicles are used for business purposes, with 65% of all new cars coming onto the roads in 2014 registered as “company” cars, and of these 82% were leased. In addition, in 2014, the increase in new company car registrations exceeded that of new private car registrations. The fleet market is understandably dominated by national automakers such as Volkswagen, Audi, BMW and Mercedes-Benz, although importers are making inroads. The fleet leasing sector is in turn dominated by manufacturers’ captives, such as VW Leasing and BMW subsidiary Alphabet, with other key players including ALD Automotive and LeasePlan. In addition to the BDL there is a separate umbrella organization for automotive financial services, the Association of Automobile Banks and Leasing Companies in Germany (AKA). This has 11 member firms representing the major auto manufacturers’ affiliated banks and leasing companies, which account for some two-thirds of the market for automotive financial services.

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

11

The AKA member firms are: Banque PSA Finance, BMW Group Financial Services, FCA Bank Deutschland, Ford Bank, Opel Bank, Honda Bank, Mercedes-Benz Bank, MKG Bank, RCI Banque, Toyota Financial Services and Volkswagen Financial Services.Leasing and other finance deals are used in relation to around 75% of all new car registrations in Germany, according to the AKA. The latest figures from the AKA reveal that member companies financed a total of 1.34 million new vehicles in 2014, with a value of €33.4 billion. This represents an increase of 9% in terms of units and 11% in value over the previous year, and also shows an encouraging turnaround after a disappointing performance in 2013. Captive banks continued to expand their share of the total volume of all new registrations in Germany, up by 2.5 percentage points to 45.9% in 2014. The portfolio of leasing and financing contracts grew 5% to a new record high of over €95 billion. Individual lease and financial contracts totalled around 595,000 in 2014, a rise of 7%, while commercial vehicle contracts bounced back after declining in 2013, with growth of 10% to just under 743,000 units. A further indicator of the relative health of the market is that bad debt ratios are currently at historically low levels of less than 1%.

German vehicle market key data

Vehicle market (AKA members) 2013 2014 Change (%)New registrations 2,838,606 2,914,570 3%Financing contracts, new business (units)

Private 557,950 594,954 7%

Commercial 672,954 742,953 10%

Total 1,230,904 1,337,907 9%

Financing penetration of new registrations (%) 43.40% 45.90%

Financing contracts, new business (value, € billion)

** Includes car insurance, credit insurance, warranty etc.Source: AKA

The main types of fleet lease contract are operational lease and full-service lease, which includes high-end services and cost guarantee products.The market conditions of continued low interest rates and the lack of attractive investment opportunities have tended to encourage cash purchases, so a prime plus point for auto finance providers has been the ongoing development of flexible financing solutions.

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

12

This has been notable in mobility services, additional auto-related financing and leasing services such as motor insurance, warranty and repair insurance, maintenance services, etc. The total number of such service contracts provided by AKA members exceeded 2.5 million in 2014, a rise of 7% on the year before, continuing an upward trend that indicates customers like to obtain these benefits from a single source.

Vehicle market trends, 2011−2014

Source: Asset Finance International, AKA

As mentioned above, the market turned down in 2013, but the year-on-year trends became increasingly positive in 2014.

Vehicle market, change on previous year (%)

Source: Asset Finance International, AKA

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

13

Fleet sector growing in importanceFigures from German fleet market research firm Dataforce show the fleet market grew by 8.6% in the first half of 2015 compared with the same period a year earlier. The number of registrations was the highest on record for the first half and increased the share of the overall market held by fleet customers.Commenting on the importance of the sector, Dr Heinz-Peter Renzel, general manager of the AKA, told Asset Finance International: “The company car market has proven to be the main growth driver over the last two years, while the private car market showed a stagnation of sales. It will remain the key pillar for some years to come.”He also noted the growing interest shown by company car lessors in energy-efficient vehicles such as e-vehicles and hybrids. “This makes the company car a main driver of innovation in environment-friendly mobility,” he said, adding: “Company cars not only have a high utilization rate but they are very likely to be leased, which means they will be exchanged in only a few years.”There are tax incentives applied to low carbon-emission vehicles, in addition to which vehicle lessors have introduced their own limitation on CO2 emission for company cars. “As a result,” Heinz-Peter Renzel observed, “CO2-efficient cars are much more common in the fleet market, and for top management personnel the days of gas-guzzlers and overly big status symbols are over.”These issues are of prime importance for vehicle lessors. CEO of Alphabet Germany, Ursula Wingfield, explained to Asset Finance International: “CO2 efficiency is an ever-more important factor for drivers and for companies when choosing a vehicle. This is demonstrated by the fact that our customers frequently use our CO2 limitation option. More than 80% of customers with a green policy used it to cap CO2 emissions.”An overview from the perspective of the BDL was provided by its managing director, Horst Fittler, who said: “Customers focus on optimizing costs and reducing fuel consumption and CO2 emissions. They increasingly ask for full service packages which leasing companies offer.”“Basically, the car world is changing,” he continued. “In mobility concepts of the future, company cars are only one of several options. Companies require a flexible travel management, which can provide mobility through various components.” He also noted that corporate car sharing is gaining in importance, which requires both individual and customized solutions, concluding: “Leasing companies are the right partners, due to their market knowledge and their asset expertise.”Ursula Wingfield also stressed the increasing cost-consciousness of customers: “There is growing interest in our Eco Driver courses to help lower fuel consumption and CO2 emissions, mainly because they promise long-term savings,” adding that “Fleets are even more environmentally-friendly when equipped with electric vehicles.”

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

14

Developments in mobility solutionsIn Germany, there are various initiatives to promote eMobility. Ursula Wingfield commented: “Government-subsidized projects such as PREMIUM, ePowered Fleets Hamburg, and InitiativE Berlin-Brandenburg, with which Alphabet is a leasing partner, offer companies discounts when choosing an electric vehicle.”She continued: “Now more than ever, fleet management is mobility management. There is much more to it than simply financing a company car. Today, companies must address topics like changing work models and complex mobility needs, weighing the costs and profiling their company as an attractive employer amid the shortage of skilled personnel. Environmental and social responsibilities remain important aspects that will – alongside efficiency – be the main targets of future mobility innovations.” There is a shift towards vehicle sharing over vehicle ownership, and the need for greater flexibility and the aim of leasing firms such as Alphabet is to combine the advantages of eMobility – environment-friendliness and sustainability – with the efficiency and economic viability of corporate car sharing.On this topic, Ursula Wingfield stated: “We are certain that electric vehicles are the perfect addition to company fleets, as shown by the high demand for the BMW i3 among our customers. Yet a key part of successfully integrating eMobility into a company’s fleet is making the switch as easy as possible. This requires precisely analysing each client’s specific needs, which is why holistic consulting and analysing individual requirements are essential parts of our eMobility solution, AlphaElectric.”She added: “We will see major progress in the eMobility sector in the next couple of years, including the advancement of vehicles and infrastructure to make eMobility accessible to a greater population. Innovation will play a key role in eMobility’s ability to penetrate the market.”The AKA expects more solutions for shared fleets and corporate car sharing models in the near future. Heinz-Peter Renzel provided an example: “Daimler Fleet Management, a subsidiary of Mercedes-Benz Bank, has recently introduced corporate car sharing services, and as a result, companies can now better utilize their fleet capacity and reduce their total costs by up to 30%,” he said, adding that “the product was developed in cooperation with Daimler Mobility Services, which brought car2go to the streets.”

Innovation is keyCar2go is one of a number of innovative car sharing operations now active in Germany. Others include carzapp and Flinkster, and their rise is based on increasingly sophisticated technology, particularly smartphone apps, as well as the growing popularity of a car sharing culture. However, the attraction of car ownership remains powerful, including among the young. A recent mobility study by car parts firm Continental revealed that 86% of 18-30 year-olds prefer ownership, whilst just 10% stated a preference for “something else”, which includes leasing, renting and car sharing.Nonetheless, the motivation is there for fleets to adopt innovation in mobility. As Ursula Wingfield noted, with connectivity and intermodal mobility becoming

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

15

increasingly interesting for companies, there is innovation potential in this area for lessors. She elaborated: “Alphabet is already working on mobility products that significantly surpass the use of company cars. With our newly optimized app, AlphaGuide, we will extensively support users, not only with their vehicle but also in accordance with their overall mobility requirements.” She continued: “Fuel management is likewise a starting point for innovations that facilitate efficient and sustainable fleet management. We are currently working on a hybrid fuel and charging card, with which users can both traditionally refuel and charge at charging stations. Additionally, there is interesting potential for mobility cards equipped with credit card functions.” The scope for collaboration between finance providers and technology developers is expanding. The increasing digitalization of services and greater integration of offline and online resources are key to maintaining growth for vehicle leasing companies. Heinz-Peter Renzel concluded: “Many future business models will only be possible and successful if the industry is open to collaborate with new technology developers and partners from different sectors.”

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

16

What’s driving fleet car pricing?A round up of some of the key auto finance industry stories in recent weeks

No tax hit from VW emissions scandal The UK government has made clear that fleets and drivers caught up in the ongoing Volkswagen emissions scandal will not face additional tax charges as a result of the German car maker’s use of so-called “defeat devices”’ to record incorrect levels of vehicle emissions. UK taxpayers will not incur higher Vehicle Excise Duty (VED) if their existing Volkswagen vehicles are found to be fitted with the illegal software that manipulates emissions tests, which would mean that the car might be re-categorised for tax purposes.Volkswagen has recalled almost 1.2 million diesel cars in the UK and halted the sale of 4,000 vehicles following the discovery that the manufacturer has routinely been using a defeat device so that official tests would show lower levels of emissions than was actually the case in everyday driving. In a statement, an HMRC (Her Majesty’s Revenue and Customs) spokesperson said: “Company car tax is based on the CO2 emission figures for the particular type of car, shown on either the UK approval certificate or the EU approval certificate. As the car benefit charge is calculated on the basis of the figures shown on the approval certificates, the tax position for Benefit-in-Kind purposes remains unchanged.” Patrick McLoughlin, transport secretary said: ‘Our priority is to protect the public and give them full confidence in diesel tests. The government expects Volkswagen to support owners of these vehicles already purchased in the UK and we are playing our part by ensuring no one will end up with higher tax costs as a result of this scandal.’

InvestigationThe government has already begun an investigation into the German car maker’s use of defeat devices in diesel cars, and is also looking at whether the illegal software used by Volkswagen is being used elsewhere. McLoughlin said: “We are starting our testing programme to get to the bottom of what the situation is for Volkswagen cars in the UK and understand the wider implications for other car types to give all consumers certainty.” “I have been pressing for action at an EU-level to improve emissions tests and will continue to do so. I have also called for a Europe-wide investigation into the use of defeat devices, in parallel to the work we are doing in the UK,” he added..The UK programme will involve re-testing diesel cars that Volkswagen group has confirmed contain defeat device software of Euro 5 category, in both a laboratory and real-world setting. These measurements will be used as a benchmark for further testing, with the final programme to be developed.

6

The pricing action plan for profitChanging your pricing policy may well be your most powerful lever forprofit. Make your action plan now!

So you want to improve your pre-taxprofits?

Well, you might decide to introduce a new ITsystem that would allow you to do morethings, introduce more products and be moreeffective than before - at a cost, of course. Oryou might introduce a new quality-management system or increase yoursalesforce or cut overheads or other costs.

These are the ‘levers of profit’, the aspects ofyour business that you can change togenerate more profit.

Generally speaking, if you pull one of theselevers it will have a modest effect on yourbottom line. You can often generate a muchbigger impact, with much less disruption tothe business, by changing your pricing policy.If you can implement a successful pricingchange you will improve your volumes andmargins simultaneously, with little disruptionand at little or no cost. Do it successfully andyou will enjoy the benefits immediately,without generating a negative response fromstaff or clients. Pricing is the most powerfullever of profit.

In previous Pricing Reviews we have looked

at the steps that asset finance companieshave taken to develop their businesses and inparticular how they have improved (or mightimprove) their pricing. In this article we willmove beyond that and set out an action planfor asset finance companies that want toimprove their pricing. The steps to follow are:diagnosis; decision; preparation; get buy-in;trial; implement and monitor.

1. Diagnosis

First, have a look at the way business ispriced at the moment. How are pricescalculated? Is it done centrally or byindividual salespeople? What insights aregained from the market to help guide pricing?Have a look at the range of prices quoted forthe same type of business to the same typeof customer; are they similar? If there is awide variation you have prima facie evidencethat something is going wrong.

Which customers get the lowest prices andwhy? What costs are incurred as a result ofdiscounting or other giveaways, e.g. givingaway costly contractual points during thenegotiation? Do the most valuable clients getthe biggest discounts? When pressed by a

17

Trade valuesTrade values of Volkswagen used cars have so far only been marginally affected by emissions scandal, according to data from Glass’s which has analysed more than 78,000 observations.The company says trade values of all Volkswagen used cars in the Glass’s database at the start of October were the same as they were at the beginning of September. However, the overall used car market has seen an increase of 2.1% during the same period - meaning that the value of the Volkswagens have effectively fallen by 2.1%.Looking at Volkswagen diesel used cars only, there was a 0.2% drop in values over the same period. However, the overall market in the same period has risen by 2.8%, meaning that the Volkswagens are trailing the market by 3%.Values of Golf diesels likely to be fitted with the Euro 5 engines affected by the scandal fell by 3.7% over the month, whereas the rest of its direct competition fell by 3.2%, meaning that these models are relatively speaking 0.5% lower than expected.However, Glass’s notes: “This is still a fluid situation and, we believe, will be very much affected on an ongoing basis by how Volkswagen deal with the problems facing them.“In our opinion, we may yet see further value changes as Volkswagen release more information. The way in which they do this, and the manner in which they support their dealer network and customers, will heavily impact on overall perception of the brand.”