HIGHLIGHTS NORTH AMERICA WWW.COLLIERS.COM Q1 2012 | INDUSTRIAL K.C. CONWAY EMD | Market Analytics U.S. Industrial Trends • A U.S. manufacturing renaissance combined with growing agriculture and energy exports fuels demand for industrial real estate. • Proximity to intermodal infrastructure, ports and resources influence investor demand for indus- trial space. • High vacancy rates in some markets are propped up by functionally obsolete warehouses with low clear heights or lack of rail access, which mask the need for new bulk warehouse construction. • East Coast industrial is poised for demand growth, with port traffic growing faster than the Gulf or West Coast, and a Panama Canal expansion just around the corner. • Investor demand in non-core industrial is growing, as demonstrated by the recent $770 million DEXUS Property Group portfolio sale. Colliers International continues to believe that modern industrial property is an attractive asset class MARKET INDICATORS Relative to prior period U.S. INDUSTRIAL MARKET SUMMARY STATISTICS, Q1 2012 Industrial Real Estate Remains the Little Engine that Could Q1 2012 Q2 2012* VACANCY NET ABSORPTION CONSTRUCTION RENTAL RATE *Projected, relative to prior period Vacancy Rate: 9.66% Change from Q4 2011: –0.12% Absorption: 22.7 Million Square Feet New Construction: 6.6 Million Square Feet Under Construction: 36.4 Million Square Feet Asking Rents Per Square Foot Average Warehouse/ Distribution Center: $4.72 Change from Q4 2010: 0.21% Sq. Ft. By Region 2.000000 1.000000 2.000000 Total_OffSF-Vacant_OffSF Vacant_OffSF Absorption Per Market Q4 '11 - Q1 '12 2,300,000 230,000 -230,000 -1,200,000 4 million 2 million 400,000 Occupied Sq. Ft. Vacant Sq. Ft. 8.5% vac. 9.7% vac. 10.4% vac. 10.1% vac. 4.6% vac. NORTH AMERICAN INDUSTRIAL VACANCY, INVENTORY AND ABSORPTION—Q1 2012

Transcript

HIGHLIGHTSNORTH AMERICA

WWW.COLLIERS.COM

Q1 2012 | INDUSTRIAL

K.C. CONWAY EMD | Market Analytics

U.S. Industrial Trends•A U.S. manufacturing renaissance combined with growing agriculture and energy exports fuels

demand for industrial real estate.•Proximity to intermodal infrastructure, ports and resources influence investor demand for indus-

trial space.•High vacancy rates in some markets are propped up by functionally obsolete warehouses with low

clear heights or lack of rail access, which mask the need for new bulk warehouse construction.•East Coast industrial is poised for demand growth, with port traffic growing faster than the Gulf or

West Coast, and a Panama Canal expansion just around the corner. •Investor demand in non-core industrial is growing, as demonstrated by the recent $770 million

DEXUS Property Group portfolio sale.

Colliers International continues to believe that modern industrial property is an attractive asset class

MARKET INDICATORSRelative to prior period

U.S. INDUSTRIAL MARKETSUMMARY STATISTICS, Q1 2012

Industrial Real Estate Remains the Little Engine that Could

Q1 2012

Q2 2012*

VACANCY

NET ABSORPTION

CONSTRUCTION

RENTAL RATE

*Projected, relative to prior period

Vacancy Rate: 9.66% Change from Q4 2011: –0.12%

Absorption: 22.7 Million Square Feet

New Construction: 6.6 Million Square Feet

Under Construction: 36.4 Million Square Feet

Asking Rents Per Square Foot Average Warehouse/ Distribution Center: $4.72 Change from Q4 2010: 0.21%

Sq. Ft. By Region

2.00000000e+009

1.00000000e+009

2.00000000e+008

Total_O�SF-Vacant_O�SFVacant_O�SF

Absorption Per MarketQ4 '11 - Q1 '12

2,300,000

230,000

-230,000

-1,200,000

4 million

2 million

400,000

Occupied Sq. Ft.

Vacant Sq. Ft.

8.5% vac.

9.7% vac.

10.4% vac.

10.1% vac.

4.6% vac.

NORTH AMERICAN INDUSTRIAL VACANCY, INVENTORY AND ABSORPTION—Q1 2012

P. 2 | COLLIERS INTERNATIONAL

HIGHLIGHTS | Q1 2012 | INDUSTRIAL | NORTH AMERICA

Manufacturing Is Leading the U.S. Recovery The growth in manufactur-ing industry is not just a good thing for manufacturing property demand: When goods are manufactured, they are also transported and stored be-fore they are sold. In fact, manufacturing growth has an eventual spillover effect to all property types, starting with warehouse and distribution properties.

Specialized Manufacturing Drives Regional Demand As modern manu-facturers become more specialized, they are often anchored to a certain region by the specialized resources they require. These resources might include the skilled labor found in cities with clusters of institutions of higher education; needed inputs such as rare-earth minerals, water and energy; and robust intermodal networks with accessible ports. The find-ings of a recent study by the Brookings Institute, “Locating American Manufacturing – Trends in the Geography of Production” highlight this trend.

•Since 1980, U.S. metropolitan areas have seen increasing specialization in manufacturing, but the specialties of each metro can vary greatly.

•There are six industry concentrations which gravitate to different met-ros: computers and electronics, transportation equipment, low-wage manufacturing, chemicals, machinery, and food production.

This increase in specialized manufacturing has translated into increased demand for industrial space. In Q1 2012, there was net positive absorption

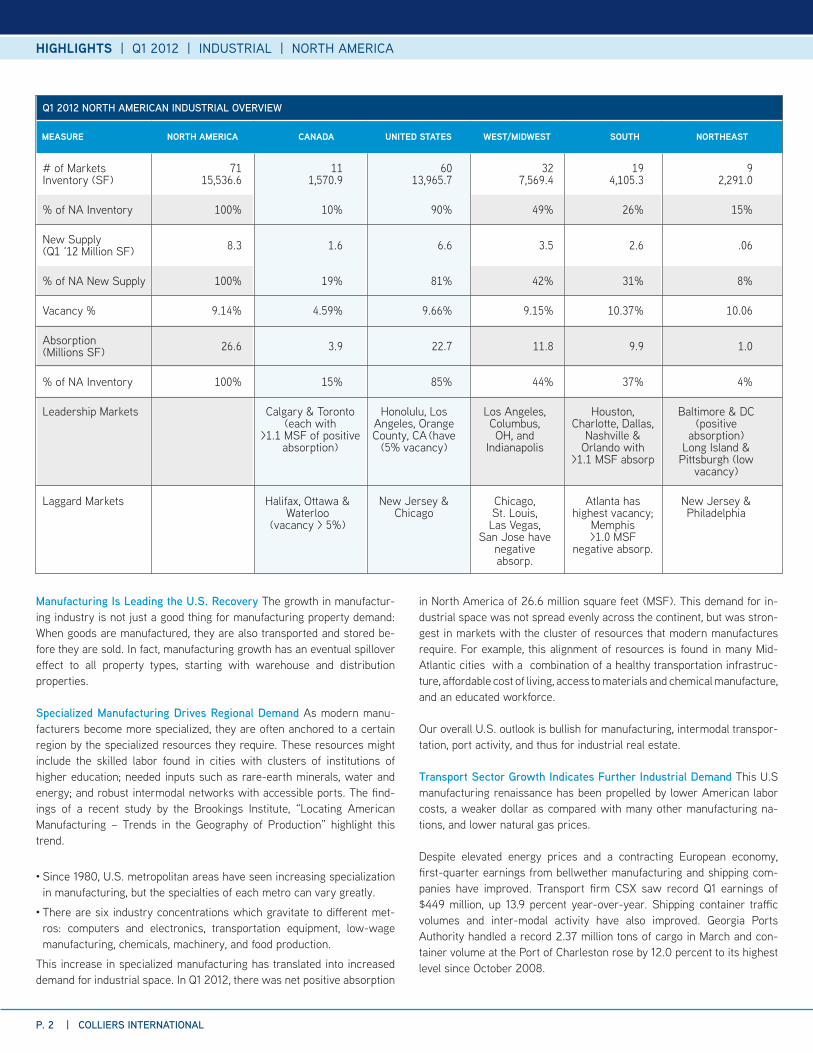

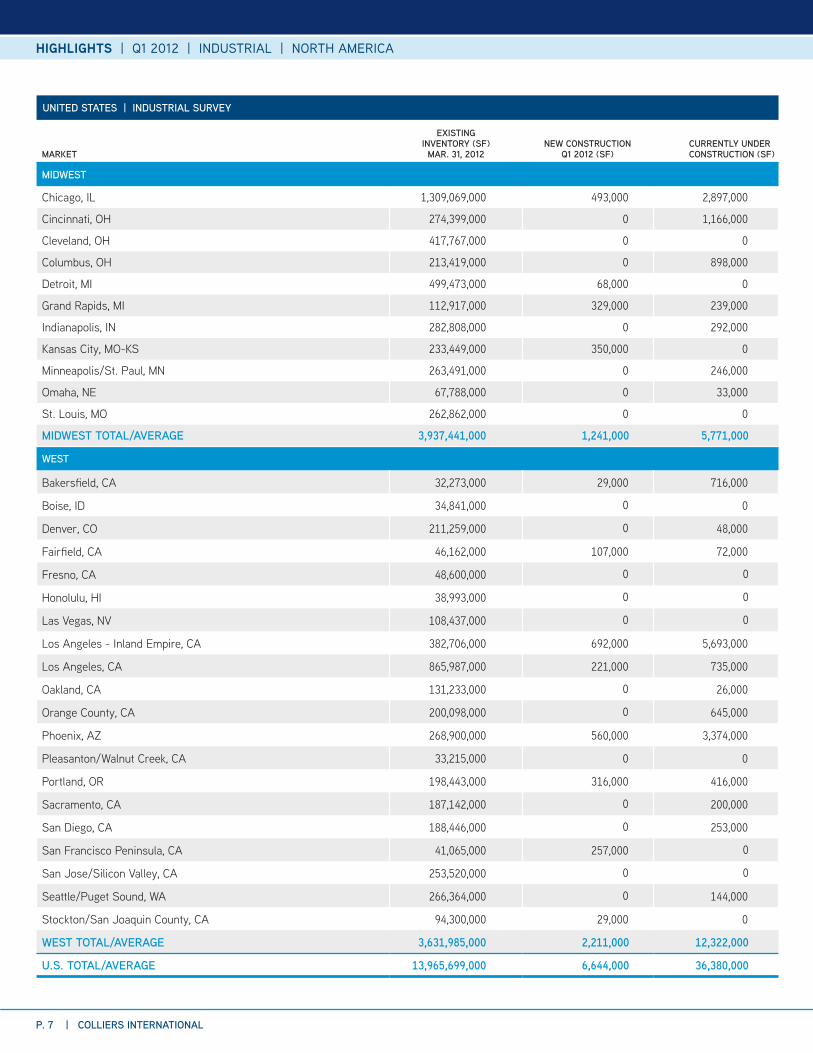

Q1 2012 NORTH AMERICAN INDUSTRIAL OVERVIEW

MEASURE NORTH AMERICA CANADA UNITED STATES WEST/MIDWEST SOUTH NORTHEAST

# of MarketsInventory (SF)

7115,536.6

11 1,570.9

6013,965.7

327,569.4

194,105.3

92,291.0

% of NA Inventory 100% 10% 90% 49% 26% 15%

New Supply (Q1 ‘12 Million SF) 8.3 1.6 6.6 3.5 2.6 .06

in North America of 26.6 million square feet (MSF). This demand for in-dustrial space was not spread evenly across the continent, but was stron-gest in markets with the cluster of resources that modern manufactures require. For example, this alignment of resources is found in many Mid-Atlantic cities with a combination of a healthy transportation infrastruc-ture, affordable cost of living, access to materials and chemical manufacture, and an educated workforce.

Our overall U.S. outlook is bullish for manufacturing, intermodal transpor-tation, port activity, and thus for industrial real estate.

Transport Sector Growth Indicates Further Industrial Demand This U.S manufacturing renaissance has been propelled by lower American labor costs, a weaker dollar as compared with many other manufacturing na-tions, and lower natural gas prices.

Despite elevated energy prices and a contracting European economy, first-quarter earnings from bellwether manufacturing and shipping com-panies have improved. Transport firm CSX saw record Q1 earnings of $449 million, up 13.9 percent year-over-year. Shipping container traffic volumes and inter-modal activity have also improved. Georgia Ports Authority handled a record 2.37 million tons of cargo in March and con-tainer volume at the Port of Charleston rose by 12.0 percent to its highest level since October 2008.

HIGHLIGHTS | Q1 2012 | INDUSTRIAL | NORTH AMERICA

COLLIERS INTERNATIONAL | P. 3

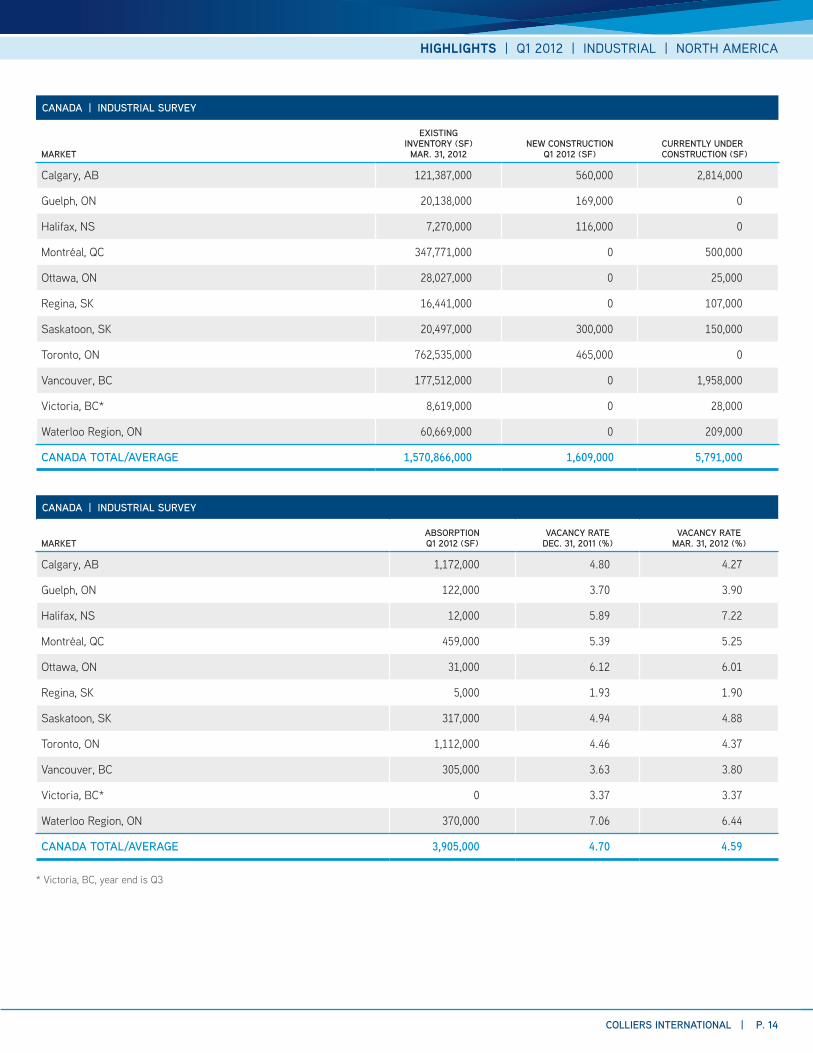

Toronto and Calgary Drive Canada’s Absorption In Canada, a combination of limited new supply and strong demand from the energy and bulk mate-rials sectors has set the stage for low vacancy rates and strong absorp-tion. 3.9 MSF of Canadian industrial space was absorbed by occupiers. Together, Toronto and Calgary, which reported more than 1.1 MSF of net absorption each, provided more than half of the net absorption in the country. This is an especially noteworthy feat for Calgary, which makes up only eight percent of the nation’s inventory, yet contributed thirty percent to the national absorption.

Vacancy rates remain low in the 11 primary Canadian markets, averaging less than 5 percent. The overall Canadian vacancy rate declined from 4.7 percent in Q4 2011 to 4.6 percent in Q1 2012. Only three markets (Halifax, Ottawa and Waterloo) have vacancy rates above 5 percent.

Southern Demand Rises Despite Elevated Vacancies The combined nine-teen southern U.S. markets show a vacancy rate of 10.37 percent, which is the highest among all regions in North America. Yet, the southern U.S. markets contributed the most positive absorption of any region in North America, thanks to growing port traffic and strengthening manufacturing. Recent announcements have bolstered our outlook for southern industrial markets. These include jumps in container volume in Charleston, record port tonnage in Georgia, a new airport intermodal facility in Charlotte, a new roll-on/roll-off South American shipping service in Port Everglades,

and the selection of Richmond as the last port of call by CKYH Alliance’s Asian service.

One reason for the high vacancy rate in the South is the fact that much of the standing warehouse space in markets like Atlanta, Columbia and Savannah is functionally obsolete. Perhaps as much as 40 percent of warehouse space is unusable by modern occupiers, with low ceiling heights, limited rail access, or inadequate power supply. IDI, one of North America’s largest industrial developers, acknowledged this fact with a recent announcement to develop speculative bulk warehouse properties

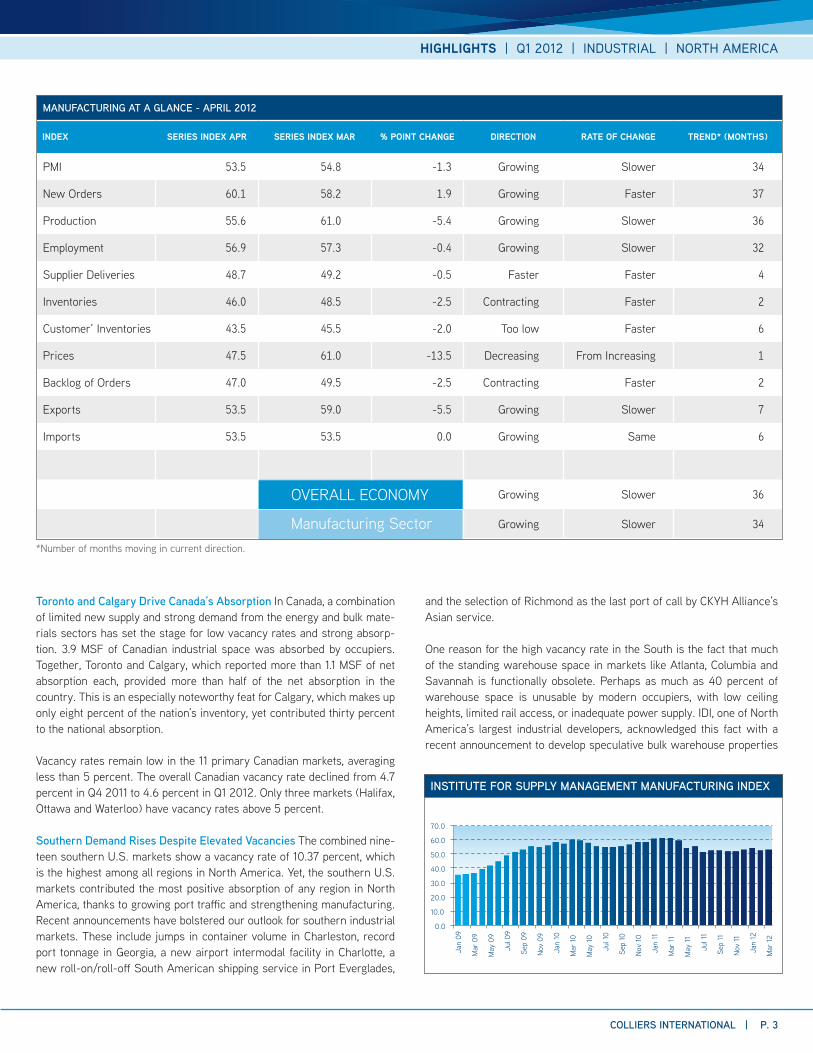

MANUFACTURING AT A GLANCE - APRIL 2012

INDEX SERIES INDEX APR SERIES INDEX MAR % POINT CHANGE DIRECTION RATE OF CHANGE TREND* (MONTHS)

Customer’ Inventories 43.5 45.5 -2.0 Too low Faster 6

Prices 47.5 61.0 -13.5 Decreasing From Increasing 1

Backlog of Orders 47.0 49.5 -2.5 Contracting Faster 2

Exports 53.5 59.0 -5.5 Growing Slower 7

Imports 53.5 53.5 0.0 Growing Same 6

Growing Slower 36

Growing Slower 34

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Jan

09

Mar

09

May

09

Jul 0

9

Sep

09

Nov

09

Jan

10

Mar

10

May

10

Jul 1

0

Sep

10

Nov

10

Jan

11

Mar

11

May

11

Jul 1

1

Sep

11

Nov

11

Jan

12

Mar

12

INSTITUTE FOR SUPPLY MANAGEMENT MANUFACTURING INDEX

OVERALL ECONOMY

Manufacturing Sector*Number of months moving in current direction.

P. 4 | COLLIERS INTERNATIONAL

HIGHLIGHTS | Q1 2012 | INDUSTRIAL | NORTH AMERICA

along I-20 West, Atlanta’s primary logistics corridor. Some initial observers doubted the need for such product in a market with a 13.3 percent vacancy rate. Yet, IDI’s decision was based on a careful analysis of the Atlanta market that showed a dearth of modern bulk warehouse space near this primary corridor.

East Coast Leads in Growing Port Traffic On both coasts the growing container traffic will sup-port new industrial property demand. According to PIERS, a leading shipping research firm, U.S. trade as measured in TEUs (Twenty-Foot Equivalent Units) was up 4.3 percent in 2011. The growth rate in container traffic among East Coast ports is now higher than the West Coast’s. East Coast ports posted a 5.5 percent year-over-year increase in container traffic in 2011, compared with a 3.0 percent increase in West Coast markets. In the East and Gulf coasts, growth opportu-nities lie in export trade: East Coast ports handle 48 percent of all U.S. export traffic. In contrast, the West Coast leads the nation in import trade with 54 percent of the import market share, with much of this traffic coming from Asia. Panama Canal Expansion Will Recalibrate U.S. Port Dynamics in 2014As the completion of the Panama Canal expansion project approaches in 2014, East Coast ports are making ready for the anticipated jump in traffic. In Savannah and Charleston, projects are underway to dredge deeper channels. Miami is working to upgrade its crane equipment. Florida ports are enhancing their roll-on, roll-off rail service. Right-to-work states from Virginia to Texas are automating port activities. Port authority directors along the East and Gulf coasts expect that warehouse demand will grow at double-digit rates in response to new larger vessels calling on their ports.

Northeast Region Most Exposed to European Woes The Northeast region is weak in comparison to the other regions, due in part to anemic trade flows inhibited by the European recession par-ticularly New York and Baltimore. As Europe wrestles with austerity measures and the United Kingdom endures a double-dip recession, warehouse demand growth will remain somewhat anemic in the Northeast.

The Northeast markets showed the least amount of net absorption in Q1 2012, with only 993,000 square feet. It was also the only region to not see a decline in warehouse vacancy. Overall va-cancy remained unchanged at 10.06 percent.

Two of the largest Northeast industrial markets, Central New Jersey and Philadelphia, each saw negative absorption in Q1 and have vacancy rates in excess of 10 percent. But the good news for this region is that there is little new supply being added to the market. Only 635,000 square feet of industrial property was delivered in Q1 2012. Central New Jersey and Philadelphia together saw only 150,000 square feet of new warehouse supply.

U.S. INDUSTRIAL MARKET Q1 2010 – Q1 2012

Mill

ion

Squa

reFe

et

Vaca

ncy

(%)

-30

-20

0

10

20

30

40

50

Q1Q4Q3Q2Q1Q4Q3Q2Q1

Absorption Completions Vacancy

2010 2011 2012

0

2

6

4

14

12

10

8

11.10 11.00 11.00 10.809.66

10.56 10.29 9.7710.01

48%46%

6%

Excluding renewals, of the leases signed this quarter in your CBD/downtown, did most tenants:

Contract Expand

Hold Steady

What was the trend for free rent (in months) o�ered by CBD landlords this quarter?

82%

12% 6%

Same

Less More

What was the trend for tenant improvement allowances ($ per SF) o�ered by landlords this quarter?

85%

12% 3%

Same

Less More

Excluding renewals, of the leases signed this quarter in your suburban o�ce market, did most tenants:

48%Expand 44%

Contract

8%Hold Steady

While Q1 demand for Industrial space moderated vs. Q4 2011, industrial vacancy fell to 9.66%—the sixth consecutive drop in vacancy since Q3 2010.

HIGHLIGHTS | Q1 2012 | INDUSTRIAL | NORTH AMERICA

COLLIERS INTERNATIONAL | P. 5

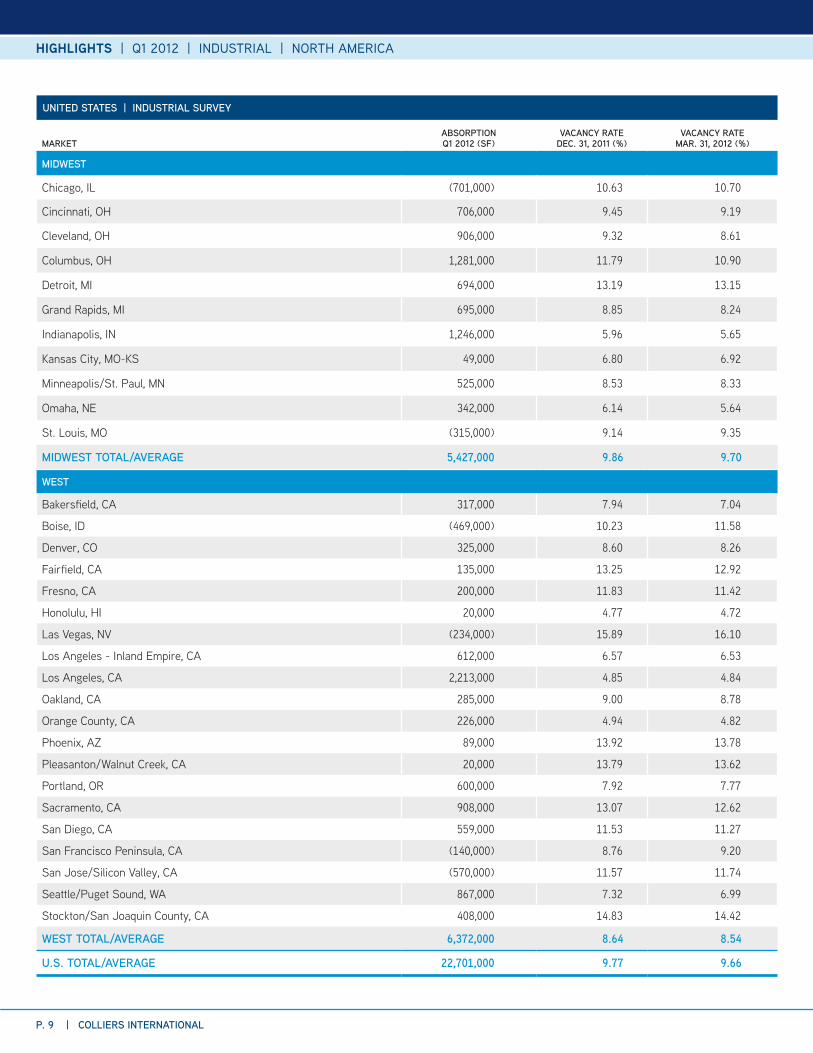

As Goes Western Industrial, So Goes the Nation The western industrial markets account for almost 50 percent of North American industrial space, and the two largest industrial markets—Los Angeles and Chicago—are in the two western regions. Thus, together the West and Midwest dictate much of the overall trend in North America.

Los Angeles, Columbus and Indianapolis each had in excess of 1 MSF of net absorption. Yet, half of the 12 North American markets with negative net absorption were also in the two western regions. Western markets which led in negative absorption were Chicago with -701,000 square feet, San Jose/Silicon Valley with -570,000 square feet, and Boise with -469,000 square feet. St. Louis, Las Vegas and San Francisco Peninsula also saw six-figure negative absorption.

Both the West and Midwest saw modest declines in vacancy in Q1 2012 and experienced positive net absorption. Together, they totaled 11.8 MSF of absorbed space, 44 percent of all absorption. Western regions, unlike the Northeast, have seen significant additions of new supply in recent quarters. To some degree, additions to supply are contributing to the ele-vated vacancy rate and absence of rent growth in the West and Midwest. More than half the total new warehouse supply added in the U.S. in Q1 2012 came from these two western regions, and half of that was in just three markets: Los Angeles, Phoenix and Chicago.

Blackstone Purchase Demonstrates Industrial’s Attraction Beyond Core Markets The demand for under-performing warehouse real estate in non-core markets is growing, as investors begin to chase yields in secondary markets. Global investment firm Blackstone Group LP cast a $770 million vote of confidence in secondary U.S. industrial markets with its purchase of 65 warehouse properties from DEXUS Property Group, an Australian property trust. The portfolio was sold with a cap rate of around 7 percent and contains mostly properties in the central U.S.

-2.0 -1.0 0.0 1.0 2.0

Savannah, GA

Chicago, IL

New Jersey - Central

Los Angeles - Inland Empire, CA

New Jersey - Northern

Detroit, MI

Atlanta, GA

Indianapolis, IN

Dallas-Ft. Worth, TX

Los Angeles, CA

3.0

Millions

ABSORPTION (SF) | SELECT MARKETS | Q1 2012

Other than warehouse, only multifamily properties have demonstrated this kind of transaction demand beyond core markets.

Disconcerting News for Maturing Debt The value of delinquent commer-cial mortgage-backed securities (CMBS) real estate loans is now at $58.1 billion, according to research firm TREPP. However, the mounting wave of maturing debt is less of a concern for industrial than other property types. Industrial properties make up the smallest percentage of outstanding dol-lars in maturing CMBS debt. The delinquency rate is also less concerning for industrial when one looks at the outstanding debt in absolute dollars. The delinquent industrial debt is skewed toward flex space, which has a higher percentage of office space and comparatively lower ceiling heights than bulk warehouse.

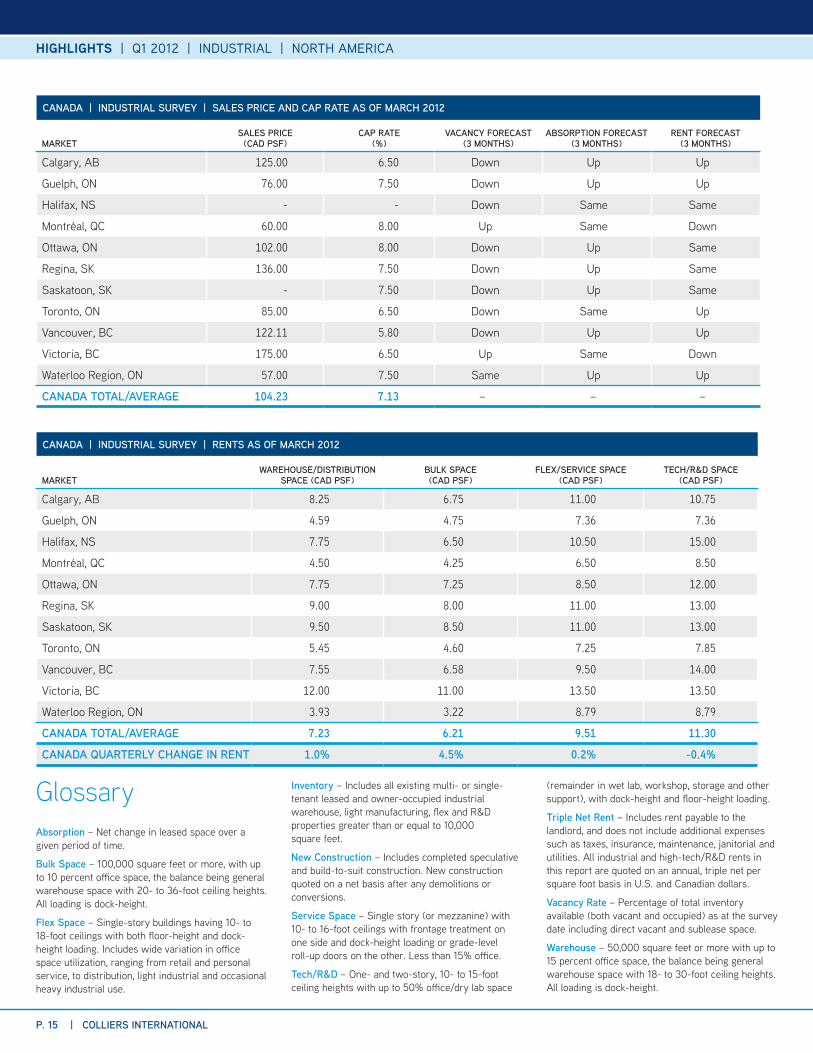

CANADA | INDUSTRIAL SURVEY | SALES PRICE AND CAP RATE AS OF MARCH 2012

MARKETSALES PRICE

(CAD PSF)CAP RATE

(%)VACANCY FORECAST

(3 MONTHS)ABSORPTION FORECAST

(3 MONTHS)RENT FORECAST

(3 MONTHS)

Calgary, AB 125.00 6.50 Down Up Up

Guelph, ON 76.00 7.50 Down Up Up

Halifax, NS - - Down Same Same

Montréal, QC 60.00 8.00 Up Same Down

Ottawa, ON 102.00 8.00 Down Up Same

Regina, SK 136.00 7.50 Down Up Same

Saskatoon, SK - 7.50 Down Up Same

Toronto, ON 85.00 6.50 Down Same Up

Vancouver, BC 122.11 5.80 Down Up Up

Victoria, BC 175.00 6.50 Up Same Down

Waterloo Region, ON 57.00 7.50 Same Up Up

CANADA TOTAL/AVERAGE 104.23 7.13 – – –

CANADA | INDUSTRIAL SURVEY | RENTS AS OF MARCH 2012

MARKETWAREHOUSE/DISTRIBUTION

SPACE (CAD PSF)BULK SPACE(CAD PSF)

FLEX/SERVICE SPACE (CAD PSF)

TECH/R&D SPACE (CAD PSF)

Calgary, AB 8.25 6.75 11.00 10.75

Guelph, ON 4.59 4.75 7.36 7.36

Halifax, NS 7.75 6.50 10.50 15.00

Montréal, QC 4.50 4.25 6.50 8.50

Ottawa, ON 7.75 7.25 8.50 12.00

Regina, SK 9.00 8.00 11.00 13.00

Saskatoon, SK 9.50 8.50 11.00 13.00

Toronto, ON 5.45 4.60 7.25 7.85

Vancouver, BC 7.55 6.58 9.50 14.00

Victoria, BC 12.00 11.00 13.50 13.50

Waterloo Region, ON 3.93 3.22 8.79 8.79

CANADA TOTAL/AVERAGE 7.23 6.21 9.51 11.30

CANADA QUARTERLY CHANGE IN RENT 1.0% 4.5% 0.2% -0.4%

GlossaryAbsorption – Net change in leased space over a given period of time.

Bulk Space – 100,000 square feet or more, with up to 10 percent office space, the balance being general warehouse space with 20- to 36-foot ceiling heights. All loading is dock-height.

Flex Space – Single-story buildings having 10- to 18-foot ceilings with both floor-height and dock-height loading. Includes wide variation in office space utilization, ranging from retail and personal service, to distribution, light industrial and occasional heavy industrial use.

Inventory – Includes all existing multi- or single- tenant leased and owner-occupied industrial warehouse, light manufacturing, flex and R&D properties greater than or equal to 10,000 square feet.

New Construction – Includes completed speculative and build-to-suit construction. New construction quoted on a net basis after any demolitions or conversions.

Service Space – Single story (or mezzanine) with 10- to 16-foot ceilings with frontage treatment on one side and dock-height loading or grade-level roll-up doors on the other. Less than 15% office.

Tech/R&D – One- and two-story, 10- to 15-foot ceiling heights with up to 50% office/dry lab space

(remainder in wet lab, workshop, storage and other support), with dock-height and floor-height loading.

Triple Net Rent – Includes rent payable to the landlord, and does not include additional expenses such as taxes, insurance, maintenance, janitorial and utilities. All industrial and high-tech/R&D rents in this report are quoted on an annual, triple net per square foot basis in U.S. and Canadian dollars.

Vacancy Rate – Percentage of total inventory available (both vacant and occupied) as at the survey date including direct vacant and sublease space.

Warehouse – 50,000 square feet or more with up to 15 percent office space, the balance being general warehouse space with 18- to 30-foot ceiling heights. All loading is dock-height.

HIGHLIGHTS | Q1 2012 | INDUSTRIAL | NORTH AMERICA

WWW.COLLIERS.COM

COLLIERS INTERNATIONAL

601 Union Street, Suite 4800Seattle, WA 98101TEL +1 206 695 4200

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

Accelerating success.

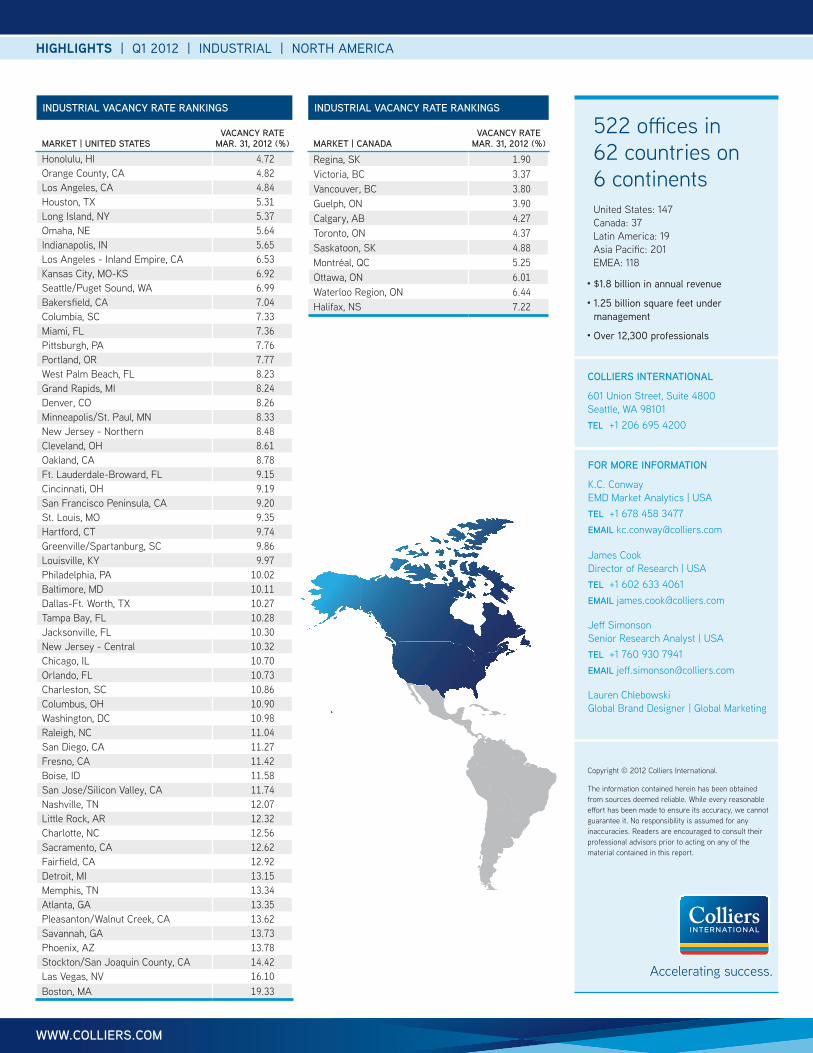

INDUSTRIAL VACANCY RATE RANKINGS

MARKET | UNITED STATESVACANCY RATE

MAR. 31, 2012 (%)

Honolulu, HI 4.72 Orange County, CA 4.82 Los Angeles, CA 4.84 Houston, TX 5.31 Long Island, NY 5.37 Omaha, NE 5.64 Indianapolis, IN 5.65 Los Angeles - Inland Empire, CA 6.53 Kansas City, MO-KS 6.92 Seattle/Puget Sound, WA 6.99 Bakersfield, CA 7.04 Columbia, SC 7.33 Miami, FL 7.36 Pittsburgh, PA 7.76 Portland, OR 7.77 West Palm Beach, FL 8.23 Grand Rapids, MI 8.24 Denver, CO 8.26 Minneapolis/St. Paul, MN 8.33 New Jersey - Northern 8.48 Cleveland, OH 8.61 Oakland, CA 8.78 Ft. Lauderdale-Broward, FL 9.15 Cincinnati, OH 9.19 San Francisco Peninsula, CA 9.20 St. Louis, MO 9.35 Hartford, CT 9.74 Greenville/Spartanburg, SC 9.86 Louisville, KY 9.97 Philadelphia, PA 10.02 Baltimore, MD 10.11 Dallas-Ft. Worth, TX 10.27 Tampa Bay, FL 10.28 Jacksonville, FL 10.30 New Jersey - Central 10.32 Chicago, IL 10.70 Orlando, FL 10.73 Charleston, SC 10.86 Columbus, OH 10.90 Washington, DC 10.98 Raleigh, NC 11.04 San Diego, CA 11.27 Fresno, CA 11.42 Boise, ID 11.58 San Jose/Silicon Valley, CA 11.74 Nashville, TN 12.07 Little Rock, AR 12.32 Charlotte, NC 12.56 Sacramento, CA 12.62 Fairfield, CA 12.92 Detroit, MI 13.15 Memphis, TN 13.34 Atlanta, GA 13.35 Pleasanton/Walnut Creek, CA 13.62 Savannah, GA 13.73 Phoenix, AZ 13.78 Stockton/San Joaquin County, CA 14.42 Las Vegas, NV 16.10 Boston, MA 19.33

INDUSTRIAL VACANCY RATE RANKINGS

MARKET | CANADAVACANCY RATE

MAR. 31, 2012 (%)

Regina, SK 1.90 Victoria, BC 3.37 Vancouver, BC 3.80 Guelph, ON 3.90 Calgary, AB 4.27 Toronto, ON 4.37 Saskatoon, SK 4.88 Montréal, QC 5.25 Ottawa, ON 6.01 Waterloo Region, ON 6.44 Halifax, NS 7.22