32

INVESTMENT SUMMARY Colonial BancGroup, Inc.

| Date post: | 15-Apr-2017 |

| Category: |

Investor Relations |

| Upload: | offtherunideas |

| View: | 435 times |

| Download: | 0 times |

INVESTMENT SUMMARY

Colonial BancGroup, Inc.

Colonial BancGroup, Inc.

Colonial BancGroup, Inc. is one of the last remaining bank holding company litigation plays and its outstanding preferred stock (CBCPQ) and subordinated notes (CBCDQ) offer extraordinary deep value.

Colonial Bank (the “Bank”) was seized by Alabama State Banking Department on August 14, 2009 and the FDIC was appointed receiver

Colonial BancGroup (“Colonial”) filed for bankruptcy in the Bankruptcy Court for the Middle District of Alabama on August 25, 2009

Chapter 11 plan of liquidation has been confirmed, and Colonial’s activities are focused on litigating valuable causes of action against the Bank’s receivership and other parties

Rulings have been delayed for the last two years by the imminent retirement of the local District Court judge

Colonial’s Trust Preferred Securities (“TruPS”) (ticker: CBCPQ), and subordinated notes (ticker: CBCDQ), trade over the counter at $1 - $2 per share, or 4 – 8% of face value

2

CBCPQ and CBCDQ represent the unsecured claims in Colonial’s bankruptcy estate.

Chapter 11 Plan of Liquidation went effective on June 3, 2011

Plan was structured provide for the litigation of causes of action Colonial retained for recovery of certain assets

Post-confirmation, Colonial obtained funding to pursue litigation in the form of a term loan and a participation interest in certain of the litigation claims

* Certain allowed claims (not shown here) have been settled since confirmation

COLONIAL BANCGROUP, INC. Al l owed Mark etPro Forma Al lowed Claims Cl a i ms Val ue

Litigation Funding Term Loan ($7.5M + Accrued Interest) $11,574,761PBGC Claims $30,000,000SUBTOTAL: ADMINISTRATIVE & PRIORITY CLAIMS $41,574,761 $41,574,761

8.875% Subordinated Notes (Ticker: CBCDQ) $250,000,0007.875% TruPS (Ticker: CBCPQ) $100,000,000FRN Jr. Debentures (subordinated) $5,155,000SUBTOTAL: UNSECURED CLAIMS $355,155,000 $14,206,200

TOTAL ALLOWED CLAIMS $396,729,761 $55,780,961

Chapter 11 Bankruptcy

3

Chapter 11 Bankruptcy

Potential Assets

Colonial’s primary remaining assets are valuable causes of action related to the ownership or recovery of $1.5 billion in assets.

COLONIAL BANCGROUP, INC. Potenti a l Pro Forma Bankruptcy Assets Val ue

Tax Refunds $260,000,000Florida REIT Preferred Stock $300,000,000Fidelity Bond Proceeds $30,000,000Deposit Accounts $28,000,000SUBTOTAL "DISPUTED ASSETS" $618,000,000

2007 Avoidable Transfers $216,281,6272008 Avoidable Transfers $375,000,0002009 Avoidable Transfers $308,586,159SUBTOTAL "AVOIDANCE ACTIONS" $899,867,786

AUDITOR LIABILITY Unknown

MISC. UNDISPUTED ASSETS $1,800,000

TOTAL ASSETS $1,519,667,786

“Unlike many, or perhaps most, chapter 11 debtors, where the debtor is an operating concern with a stream of income, the instant debtor is not reorganizing but liquidating in chapter 11. Though the debtor has some hard assets, the overwhelming bulk of its assets exist in the form of causes of action. Therefore, from its inception, the primary thrust of this case has been the prosecution of claims -- claims such as malpractice claims against the debtor's accountants, substantial tax refund claims, claims against the FDIC-Receiver, preference claims against prior attorneys, fraudulent conveyance claims, and more. The debtor values these claims in the hundreds of millions of dollars.”

~ Hon. Dwight H. Williams

(In re: The Colonial BancGroup, Inc., Doc. No. 1650 at 4-5)

4

Chapter 11 Bankruptcy

Active Litigation

General Description Case Title, No. Description of Issue

1. Receivership Claim The Colonial BancGroup, Inc. v. FDIC, Case No. 2:10-cv-00198 (M.D. Ala.)

Enforcing Colonial BancGroup’s claim in Colonial Bank’s receivership for ~$1.5 billion in assets.

2. Denial of FDIC Claim In re: The Colonial BancGroup, Inc., Case No. 2:10-cv-00409 (M.D. Ala.)

Denying FDIC’s claim for the same ~1.5 billion in assets in Colonial BancGroup’s bankruptcy.

3. Section 541 Claim The Colonial BancGroup, Inc. v. FDIC, Case No. 2:10-cv-00410 (M.D. Ala.)

Further litigation over the same assets based on section 541 of the Bankruptcy Code.

4. FDIC “Capital Maintenance Claim” FDIC v. The Colonial BancGroup, Inc. (In re: The Colonial BancGroup, Inc.),Case No. 2:10-cv-00877 (M.D. Ala.)

FDIC’s claim for alleged capital maintenance obligations under section 365(o) of the Bankruptcy Code.

5. CNB Capital Maintenance Countersuit

The Colonial BancGroup, Inc. v. FDIC, Case No. 2:10-cv-00411 (M.D. Ala.)

Countersuit against FDIC’s alleged capital maintenance claim under section 365(o) of the Bankruptcy Code.

6. BB&T Deposits FDIC v. The Colonial BancGroup, Inc. (In re: The Colonial BancGroup, Inc.),Case No. 2:11-cv-00133 (M.D. Ala.)

FDIC’s claim for setoff rights against $28 million in deposits held by Colonial BancGroup at Colonial Bank at the time of seizure.

7. REIT Preferred The Colonial BancGroup, Inc. v. Branch Banking and Trust Company, et al., CaseNo. 2:11-cv-00824 (M.D. Ala.)

Litigation to enforce Colonial BancGroup’s ownership of $300 million of REIT preferred shares.

8. Professionals Suits The Colonial BancGroup, Inc., et al., v. PricewaterhouseCoopers LLP, et al., CaseNo. 2:11-cv-00746 (M.D. Ala.)

Colonial BancGroup suing for recovery of over $500 million damages from fraud undetected by PwC, its auditor.

5

Litigation Funding

Colonial obtained a commitment for up to $15 million in litigation financing on September 13, 2012 from certain investors/lenders, provided in exchange for a share of any recoveries from litigation and a term loan.

“Investment Facility”: $7.5 million in funding in exchange for a 33.3% share of any recoveries from all of the active litigation EXCEPT the Professional Suits against the auditors

“Term Loan Facility”: $7.5 million in funding in exchange for a three year term loan bearing interest at 7.5%, payable semiannually, secured by remaining 66.7% of any recoveries from the active litigation EXCEPT 100% of any recoveries from the Professional Suits

“[Colonial] has received, and continues to receive, funding under the Funding Transactions.” (6/30/14 3rd Post-Confirmation Report, Doc. 2087)

6

Chapter 11 Bankruptcy

Tax Refund Dispute

In 2010, Colonial filed a consolidated tax return claiming $260 million in refunds as a result of net operating losses incurred by the Bank in the 2009 taxable year.

The Bank’s losses in 2009 were “carried back” to offset previous years’ taxable income and generated a refund

IRS has paid the 2009 tax refund in full, but into escrow pending the outcome of a dispute over ownership

Calendar Period 2004 - 2007 2008 2009Taxable Income / Loss ($M) $1,340.0 -$473.9 -$3,800.0Tax refunds ($M) immaterial $166.0 $260.0

Status of refund Paid to BancGroup June 2009

Paid to escrow June 2012

7

Chapter 11 Bankruptcy

Tax Refund Dispute

Colonial and the Bank were party to a Tax Allocation Agreement (“TAA”) that governed the settlement of the Bank’s share of the group tax payment/refund.

30 day terms for any intercompany remittances for tax liability or benefit

No limitation on use of funds during the 30 days

Colonial

Bank

IRS

TAA provides 30 days for intercompany remittances

Note: With a consolidated filing, the IRS only faces the parent company Colonial, not the Bank.

Group Payment/Refund (time = t)

Individual Payment/Refund (due time = t+30)

Tax Refund Dispute

8

Chapter 11 Bankruptcy

Tax Refund Dispute

Colonial and the FDIC have each claimed ownership of the $260 million tax refund currently held in escrow.

Dispute arises from disagreement about the nature of the Bank’s relationship with Colonial with respect to the tax refunds

Colonial

BankFDIC: Colonial holds for 30 days as agent for the Bank -> Bank owns refund

Colonial: the Bank is a creditor with a 30 day receivable -> Bank has unsecured claim for refund

Issue Colonial’s Position FDIC’s Position

Ownership? Colonial Bank (receivership)

Intercompany relationship? Debtor-creditor Agent-principal

FDIC’s claim in Colonial’s bankruptcy? $260 million unsecured None, tax refund is property of the Bank

IRSGroup Payment/Refund (time = t)

TAA provides 30 days for intercompany remittancesIndividual Payment/Refund (due time = t+30)

Tax Refund Dispute

9

Chapter 11 Bankruptcy

Tax Refund Dispute

There is a substantial body of recent caselaw dealing with Tax Sharing / Allocation Agreements, all applying the same consistent logic in determining the nature of the relationship.

Only exception is IndyMac, where the language mentioning an agency language was particularly weak

Tax Refund Caselaw Summary

Case Title Ruling Date CourtTax Sharing Agreement?

Language indicating trust or

agency?

Language indicating debtor-

creditor Outcome of Decision

Bob Richards 1/18/1973 9th Cir. N N/A N/A Bank owns refundCapital Bancshares 4/3/1992 5th Cir. N N/A N/A Bank owns refundBankUnited 8/15/2013 11th Cir. N N/A N/A Bank owns refundBSD Bancorp 2/28/1995 SD CA Y Y Y Bank owns refundIntegrity (Lubin) 3/2/2011 ND GA Y Y Y Bank owns refundNetbank 9/10/2013 11th Cir. Y Y Y Bank owns refundIndymac (Siegel) 4/21/2014 9th Cir. Y Y Y Bank has unsecured claimTeam Financial 4/27/2010 Bk. KS Y N Y Bank has unsecured claimImperial 5/16/2013 SD CA Y N Y Bank has unsecured claimVineyard 3/28/2014 Bk. CD CA Y N Y Bank has unsecured claimDowney 1/26/2015 3rd Cir. Y N Y Bank has unsecured claimColonial BancGroup ?? MD AL Y N Y ??

Tax Refund Dispute

10

Chapter 11 Bankruptcy

Tax Refund Dispute

Colonial’s Tax Allocation Agreement is clearly of the type that the Courts have favored in previous cases.

Colonial and the Bank had a valid tax sharing / allocation agreement

The Tax Allocation Agreement contains no mention of a trust or agent-principal relationship

The Tax Allocation Agreement contains language consistent with a debtor-creditor relationship, including a due date / maturity and a lack of any limitations on use of funds

Colonial should be found to own the refunds, and the FDIC should have an unsecured claim for the same.

If there exists a tax sharing / allocation agreement…

… that unambiguously creates a debtor-creditor relationship, then the four corners of the agreement govern and the parent company owns the refunds.

Tax Refund Dispute

11

Chapter 11 Bankruptcy

Tax Refund Dispute

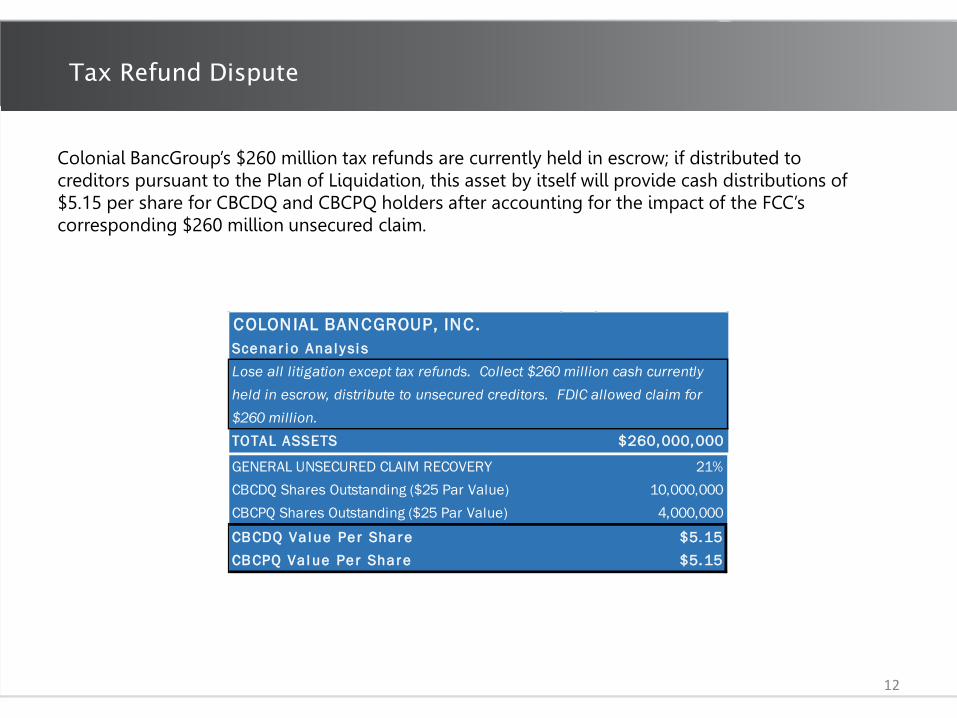

Colonial BancGroup’s $260 million tax refunds are currently held in escrow; if distributed to creditors pursuant to the Plan of Liquidation, this asset by itself will provide cash distributions of $5.15 per share for CBCDQ and CBCPQ holders after accounting for the impact of the FCC’s corresponding $260 million unsecured claim.

GENERAL UNSECURED CLAIM RECOVERY 21%CBCDQ Shares Outstanding ($25 Par Value) 10,000,000CBCPQ Shares Outstanding ($25 Par Value) 4,000,000

CBCDQ Val ue Per Share $5.15CBCPQ Val ue Per Share $5.15

COLONIAL BANCGROUP, INC. Scenar i o Anal y si s

TOTAL ASSETS $260,000,000

Lose all litigation except tax refunds. Collect $260 million cash currently held in escrow, distribute to unsecured creditors. FDIC allowed claim for $260 million.

Tax Refund Dispute

12

Chapter 11 Bankruptcy

REIT Preferred Stock

In 2009, Colonial received notice from the FDIC that the Bank was undercapitalized, triggering an exchange of $300 million in preferred shares issued by a REIT subsidiary of the Bank for $300 million of new Colonial preferred shares.

Effective automatically upon receipt of notice, Colonial issued $300 million of its own preferred stock to the former REIT holders in exchange for their REIT Preferred shares

Under the Exchange Agreement, Colonial was obligated to contribute those REIT Preferred shares to the Bank by updating the REIT’s share registry to reflect the Bank as new owner

Colonial

Bank

REIT Pfd Holders

“Downstream contribution”: equity capital contribution effectuated through a manual update to the share register

“Automatic exchange”: effectuated by operation of law upon receipt of notice from FDIC that Bank is undercapitalized

New Colonial Pfd & REIT Pfd

REIT Pfd & Bank Equity

REIT Preferred Stock

13

Chapter 11 Bankruptcy

REIT Preferred Stock

Colonial and the FDIC disagree on whether the “downstream contribution” actually occurred.

Dispute centers on the necessary steps for legal transfer of securities

Issue Colonial’s Position FDIC / Bank’s Position

“Downstream contribution” completed? Share register was not updated – shares were never transferred

Register update a formality, shares were “constructively delivered” to the Bank

Ownership of the shares? Colonial Bank (receivership)

FDIC’s claim in Colonial’s bankruptcy? Claim for the value of the shares ($300 million)

None – Bank holds the shares

Colonial

Bank

REIT Pfd Holders

“Downstream contribution”: equity capital contribution effectuated through a manual update to the share register

“Automatic exchange”: effectuated by operation of law upon receipt of notice from FDIC that Bank is undercapitalized

New Colonial Pfd & REIT Pfd

REIT Pfd & Bank Equity

Colonial: Share register was never updated, no contribution

FDIC: Shares were “constructively delivered” by intent and agreement

REIT Preferred Stock

14

Chapter 11 Bankruptcy

REIT Preferred Stock

Simple question of property transfer: courts have a well-established test for deciding this issue.

Shares were uncertificated following the conditional exchange (the existing certificates became New Colonial Preferred Shares)

Share registry was maintained by a direct subsidiary of the Bank

Share registry was never updated to reflect the Bank as the owner of the shares

Transfer could not have occurred.

If securities are uncertificated…

…and unless the share registry was outside of the parties’ control…

…the share registry must be updated by the company to effectuate a transfer of the shares.

REIT Preferred Stock

15

Chapter 11 Bankruptcy

REIT Preferred Stock

Colonial BancGroup should have $300 million in REIT preferred securities available to liquidate or distribute to creditors, providing distributable value of $5.85 per share to CBCDQ and CBCPQ holders after accounting for the FDIC’s $300 million unsecured claim for breach of contract.

COLONIAL BANCGROUP, INC. Scenar i o Anal y si s

TOTAL ASSETS $300,000,000

Lose all litigation except CBG Florida REIT Preferred. Gain title to $300 million REIT preferred shares, distribute to creditors. FDIC allowed claim for $300 million.

SUBTOTAL: ADMINISTRATIVE & PRIORITY CLAIMS $146,574,761

AVAILABLE F OR DISTRIBUTION TO UNSECUREDS $153,425,239

TOTAL CLAIMS $801,729,761

GENERAL UNSECURED CLAIM RECOVERY 23%CBCDQ Shares Outstanding ($25 Par Value) 10,000,000CBCPQ Shares Outstanding ($25 Par Value) 4,000,000

CBCDQ Val ue Per Share $5.85CBCPQ Val ue Per Share $5.85

REIT Preferred Stock

16

Chapter 11 Bankruptcy

Fidelity Bonds

Colonial’s fidelity bonds (insurance policies) have paid out $30 million to cover damages from a massive fraud perpetrated by key executives of the Bank.

Colonial incurred billions in losses from a massive mortgage warehousing fraud perpetrated by employees of the Bank and Taylor Bean & Whitaker.

Fidelity Bonds

17

Chapter 11 Bankruptcy

Fidelity Bonds

Colonial and the FDIC disagree about the beneficiary of Fidelity Bonds.

Simple question of contract interpretation

The $30 million has been placed in escrow pending a decision from the court

Issue Colonial’s Position FDIC / Bank’s Position

Beneficiary of the bonds? Colonial, as the “named assured” Bank (receivership), as the party suffering loss

Interpretation of the document? Four corners of the document are unambiguous

Court must look to external factors, primarily the source of the damages and intent of insurance

Fidelity Bonds

18

Chapter 11 Bankruptcy

Fidelity Bonds

A simple read shows that the four corners of the documents are clear – Colonial is the only beneficiary, and the source of the economic losses is utterly irrelevant.

-Colonial Bank “[shall not] have any direct beneficiary interest in or any right of action” under the any of the bonds.

~ Bond No. 81158390 DFI, pg. 7

Fidelity Bonds

19

Chapter 11 Bankruptcy

Fidelity Bonds

Colonial BancGroup should have an additional $30 million of cash from fidelity bonds for distribution to creditors, providing an incremental* $1.41 per share to CBCDQ and CBCPQ holders.

COLONIAL BANCGROUP, INC. Scenar i o Anal y si s

TOTAL ASSETS $30,000,000

Incremental impact from distribution of $30 million in fidelity bond proceeds directly to unsecureds (assumes other recoveries in excess of fixed priority claims).

SUBTOTAL: ADMINISTRATIVE & PRIORITY CLAIMS $10,000,000

AVAILABLE F OR DISTRIBUTION TO UNSECUREDS $20,000,000

TOTAL CLAIMS $365,155,000

GENERAL UNSECURED CLAIM RECOVERY 6%CBCDQ Shares Outstanding ($25 Par Value) 10,000,000CBCPQ Shares Outstanding ($25 Par Value) 4,000,000

CBCDQ Val ue Per Share $1.41CBCPQ Val ue Per Share $1.41

Fidelity Bonds

20

Chapter 11 Bankruptcy

BB&T Deposit Accounts

Colonial also has ~ $30 million in cash frozen in deposit accounts at BB&T, subject of an ongoing dispute over setoff between Colonial and the FDIC.

Originally deposit accounts of the Bank holding the operating , transferred as part of BB&T’s purchase of assets and assumption of liabilities

Cash frozen since the bankruptcy filing – FDIC has asserted a right to seize the cash to setoff against its claims in Colonial’s bankruptcy (of an amount TBD)

Setoff in bankruptcy requires mutual claims; Colonial and the FDIC disagree who is liable for the deposit accounts

Issue Colonial’s Position FDIC / Bank’s Position

FDIC’s right to setoff? None Should be allowed, contingent on the FDIC having claims in Colonial’s bankruptcy

Mutuality of liability? No, FDIC in its capacity as receiver is not liable for the accounts and FDIC-Corporate has no claim against Colonial

Yes, FDIC is ultimately liable for all deposits and has contingent claims against Colonial

Ultimate liability for deposit accounts?

FDIC – Corporate, as insurer of all depositors FDIC – Receiver, by virtue of right to reverse transfers to BB&T under the Purchase & Assumption Agreement governing the sale of the Bank’s operations to BB&T

BB&T Deposit Accounts

21

Chapter 11 Bankruptcy

BB&T Deposit Accounts

Colonial BancGroup may be able to distribute ~$30 million in cash currently held in deposit accounts.

The Bankruptcy Court denied the setoff in early 2011, but District Court overturned in January 2012, finding the FDIC ultimately liable for the deposit accounts

Colonial has appealed the District Court ruling with a request for a rehearing on the basis that the court failed to consider the FDIC’s dual capacities

The District Court has not yet decided on the rehearing request

Even assuming the District Court’s ruling is upheld, setoff means that the $30 million will dollar for dollar reduce the FDIC’s claims against Colonial, including unsecured claims arising from favorable (for Colonial) rulings on the tax refund and REIT Preferred Stock issues

BB&T Deposit Accounts

22

Chapter 11 Bankruptcy

Fraudulent Conveyances

Colonial transferred $900 million in value to the Bank in the months and years before its seizure, a time period in which Colonial and the Bank were likely insolvent.

Ongoing fraud perpetrated by Taylor Bean & Whitaker was a significant factor undiscovered until after the Bank’s seizure

The transfers are potentially reversible fraudulent conveyances under the bankruptcy code

Capital Contributions and Other Transfers From Colonial BancGroup to Colonial Bank

F rom 8/24/2007 1/1/2008 1/1/2009Through 12/31/2007 12/31/2008 8/24/2009

Cash (Financings) $375,000,000 $50,880,867 $425,880,867Citrus & Chemical Acquisition $216,281,627 $216,281,627Loans Contributed $70,664,037 $70,664,037Securities Contributed $21,041,255 $21,041,255Tax Refunds $166,000,000 $166,000,000

Tota l Transfers $216,281,627 $375,000,000 $308,586,159 $899,867,786

Insolvency? Likely >$1 billion in fraudulent …Reported $1.1 billion in …$268 million in lossesloans already 'bought' but as pretax losses, ending the in 1Q09 alone… Bankyet undiscovered… yr. severely undercapitalized was siezed 8/14 with a

even without fraud… ~$1 billion capital deficitthat later was found to be more than $4 billion.

Cumul ati ve

Fraudulent Conveyances

23

Chapter 11 Bankruptcy

Fraudulent Conveyances

Colonial believes that these transfers were all fraudulent conveyances and has asserted a claim in the Bank’s receivership for the full $900 million.

Fraudulent conveyance requires a transfer of an asset for less than reasonably equivalent value in the four years prior

Banking regulations prohibit reversal of fraudulent conveyances to a Bank if the depository institution is operating under a “written direction” from its regulators to increase capital

Issue Colonial’s Position FDIC / Bank’s Position

Did Colonial receive “reasonablyequivalent value” for the $900M in transfers?

No – Bank was insolvent and its equity accordingly worthless

Yes, Bank was solvent until FDIC directed it to increase its capital levels

Colonial insolvent at the time of transfers? Yes, Colonial was insolvent as early as December 2007

No, not until early 2009

The Bank subject to a “written direction” from regulators to increase its capitalization?

Not until the July 15, 2009 Cease & Desist Order from the FDIC, after all of the transfers took place

As of the December 15, 2008 MOU between the Bank and the FDIC

Fraudulent Conveyances

24

Chapter 11 Bankruptcy

BB&T Deposit Accounts

Colonial has a very strong case that at least the 2008 and 2009 transfers were reversible fraudulent conveyances.

December 15, 2008 memorandum of opinion was a voluntary agreement, not a “written direction”, to improve capitalization

2009 transfers were almost certainly for less than “reasonably equivalent value” – even the FDIC admits as much

2008 transfers likely meet this criteria as well

2007 transfer maybe

Colonial should have at least $300 million, likely more than $600 million in claims in the Bank’s receivership for fraudulent conveyances.

Provided that the transferee was not a depository institution operating under a written direction from its regulator to improve its capital position….

… Transfers for “less than reasonably equivalent value” made while the transferor was insolvent are reversible under the bankruptcy code.

Fraudulent Conveyances

25

Chapter 11 Bankruptcy

BB&T Deposit Accounts

While economic recovery on such claims faces long odds, at the very least they provide for the basis of setoff against any claims held by the FDIC against Colonial BancGroup.

Establishes mutuality of claims assuming favorable (for Colonial) rulings on either the tax refund or REIT Preferred Stock litigation

SUBTOTAL: ADMINISTRATIVE & PRIORITY CLAIMS $133,241,428

AVAILABLE F OR DISTRIBUTION TO UNSECUREDS $126,758,572

TOTAL CLAIMS $488,396,428

GENERAL UNSECURED CLAIM RECOVERY 36%CBCDQ Shares Outstanding ($25 Par Value) 10,000,000CBCPQ Shares Outstanding ($25 Par Value) 4,000,000

CBCDQ Val ue Per Share $8.92CBCPQ Val ue Per Share $8.92

Tax Refund Win + Setoff of Fraudulent Conveyances

COLONIAL BANCGROUP, INC. Scenar i o Anal y si s

TOTAL ASSETS $260,000,000

Lose all litigation except tax refunds. Collect $260 million cash currently held in escrow, distribute to unsecured creditors. FDIC allowed claim for $260 million, but setoff with >$300 million in fraudulent conveyances.

COLONIAL BANCGROUP, INC. Scenar i o Anal y si s

TOTAL ASSETS $300,000,000

Lose all litigation except CBG Florida REIT Preferred. Gain title to $300 million REIT preferred shares, distribute to creditors. FDIC allowed claim for $300 million, but setoff with >$300 million in fraudulent conveyances.

REIT Preferred Win + Setoff of Fraudulent Conveyances

SUBTOTAL: ADMINISTRATIVE & PRIORITY CLAIMS $146,574,761

AVAILABLE F OR DISTRIBUTION TO UNSECUREDS $153,425,239

TOTAL CLAIMS $501,729,761

GENERAL UNSECURED CLAIM RECOVERY 43%CBCDQ Shares Outstanding ($25 Par Value) 10,000,000CBCPQ Shares Outstanding ($25 Par Value) 4,000,000

CBCDQ Val ue Per Share $10.80CBCPQ Val ue Per Share $10.80

Fraudulent Conveyances

26

Chapter 11 Bankruptcy

Auditor Negligence and Malpractice

Colonial is also suing its former auditors, PricewaterhouseCoopers and Crowe Horwath, as well as advisor Ernst & Young for damages in the multi-billion dollar Taylor Bean & Whitaker fraud scheme.

Dispute centers on accounting malpractice and professional negligence in discovering the sale of more than a billion dollars in nonexistent loans to Colonial Bank

Auditors overlooked the fraud for 7 years (2002-09), signing off on a clean audit each year while the cumulative damages to Colonial from the scheme grew from millions to billions of dollars

Auditor Negligence and Malpractice

27

Chapter 11 Bankruptcy

Auditor Negligence and Malpractice

Early indications for Colonial’s case are very positive.

In October 2014, District Court ruled in Colonial’s favor on the Auditors’ motion to dismiss, and case is now in discovery

District Court heavily favored Colonial in its recent ruling on the auditors’ motion to dismiss

Deloitte has already settled similar litigation, terms undisclosed

Every indication so far is positive for Colonial’s multi-billion dollar damages claim.

“The court does not… buy into PwC’s express and Crowe’s implied arguments[, which] fundamentally misstate the professional role of auditors in the banking business… [S]ome characteristics of the alleged facts and citations to case law were misleading and perilously close to constituting dishonesty towards the court.” (9/9/14 Order on Motion to Dismiss)

Auditor Negligence and Malpractice

28

Chapter 11 Bankruptcy

365(o) Claims

The FDIC has asserted priority claims for the deficit in the Bank’s receivership on the basis of Title 11 U.S.C Section 365(o); its claims were denied by the bankruptcy court and are now on appeal.

365(o) gives priority treatment to the FDIC’s claims arising from an agreement with the Bank’s parent company (here, Colonial) regarding maintenance of specified capital levels at the Bank

Bankruptcy court ruled in Colonial’s favor in August 2010, finding that none of the agreements contained a specific commitment to maintain capital

FDIC has appealed to the District Court, a ruling is pending

Issue Colonial’s Position FDIC’s Position

Did Colonial agree to maintain the Bank’s capital at a certain level?

No, January and June agreements were broad statements not specificcommitments and

Yes, agreements Colonial entered into in January and the Cease & Desist Order entered against it in June 2009 indicated it would support the Bank

What is the legal requirement for a 365(o) claim?

Clear, specific capital metrics that must bemaintained – creating the obligation to contribute capital

General statements indicating standby support for the Bank

365(o) Claims

29

Chapter 11 Bankruptcy

365(o) Claims

Here again, precedent favors Colonial: courts have only found 365(o) obligations in those cases were a specific capitalization metric was required to be maintained at a certain level.

In all of the agreements, Colonial was simply required to “assist” the Bank in reaching regulatory compliance and generally act a “source of strength”.

Undisputed testimony from the Federal Reserve Bank and the Alabama State Banking Board and Colonial’s executives clearly shows that no one party to the agreements understood any part of them to be binding obligations.

The Bankruptcy Court ruling should upheld on appeal.

A “mere acknowledgement” of the holding company’s obligations to act as a “source of strength” is not sufficient basis for a 365(o) claim…

… And the regulators party to the agreement must have understood it to be a binding obligation of the holding company.

365(o) Claims

30

Chapter 11 Bankruptcy

Conclusion

Colonial BancGroup is a multi-faceted litigation play with enormous upside potential from the market-implied valuation.

Colonial BancGroup will likely recover in excess of $500 million in cash and other valuable assets, which will then be distributed to creditors including CBCDQ and CBCPQ holders

In a base case scenario where Colonial BancGroup obtains favorable rulings on tax refunds, REIT preferred securities, fidelity bond proceeds and some avoidance actions, CBCDQ and CBCPQ holders will receive over $24 per share

Success on even one single issue, such as the tax refund or REIT preferred stock, could provide substantial upside from today’s trading price

Multi-billion dollar case against auditors provides ‘bluebird’ potential

Conclusion

31

Chapter 11 Bankruptcy

Summary of Scenarios

COLONIAL BANCGROUP, INC. LITIGATION & CLAIMS SCENARIO ANALYSISSCENARIO: POTENTIAL BASE CASE REIT PF D TAX REF UNDSTax Refunds $260,000,000 $260,000,000 $0 $260,000,000Florida REIT Preferred Stock $300,000,000 $300,000,000 $300,000,000 $0Fidelity Bond Proceeds $30,000,000 $30,000,000 $0 $0Deposit Accounts $28,000,000 $0 $0 $0SUBTOTAL "DISPUTED ASSETS" $618,000,000 $590,000,000 $300,000,000 $260,000,000

2007 Avoidable Transfers $216,281,627 $0 $0 $02008 Avoidable Transfers $375,000,000 $0 $0 $02009 Avoidable Transfers $308,586,159 $0 $0 $0SUBTOTAL "AVOIDANCE ACTIONS" $899,867,786 $0 $0 $0

AUDITOR LIABILITY Unk, assm. $0 Unk, assm. $0 Unk, assm. $0 Unk, assm. $0

UNDISPUTED ASSETS $1,800,000 $1,800,000 $0 $0

TOTAL ASSETS $1,519,667,786 $591,800,000 $300,000,000 $260,000,000

SUBTOTAL: ADMINISTRATIVE & PRIORITY CLAIMS $252,574,761 $243,241,428 $146,574,761 $133,241,428

AVAILABLE F OR DISTRIBUTION TO UNSECUREDS $1,267,093,024 $348,558,572 $153,425,239 $126,758,572

SUBTOTAL: UNSECURED CLAIMS $915,155,000 $355,155,000 $655,155,000 $615,155,000

GENERAL UNSECURED CLAIM RECOVERY 138% 98% 23% 21%CBCDQ Shares Outstanding ($25 Par Value) 10,000,000 10,000,000 10,000,000 10,000,000CBCPQ Shares Outstanding ($25 Par Value) 4,000,000 4,000,000 4,000,000 4,000,000

CBCDQ Val ue Per Share $25.00 $24.54 $5.85 $5.15CBCPQ Val ue Per Share $25.00 $24.54 $5.85 $5.15

Summary of Scenarios

32