COLORADO CHARITABLE SOLICITATIONS ACT INSTRUCTIONS ONLINE CHARITABLE SOLICITATIONS REGISTRATION SYSTEM (Rev. June 1, 2011) INTRODUCTION GETTING ORIENTED GETTING STARTED REGISTRATION STATEMENT – CHARITABLE ORGANIZATIONS FINANCIAL REPORT – CHARITABLE ORGANIZATIONS

Transcript

COLORADO CHARITABLE SOLICITATIONS ACT

INSTRUCTIONS

ONLINE CHARITABLE SOLICITATIONS REGISTRATION SYSTEM

(Rev. June 1, 2011)

INTRODUCTION

GETTING ORIENTED

GETTING STARTED

REGISTRATION STATEMENT – CHARITABLE ORGANIZATIONS

FINANCIAL REPORT – CHARITABLE ORGANIZATIONS

Registration Instructions for Charities (Rev. June 1, 2011) Page 2 of 21

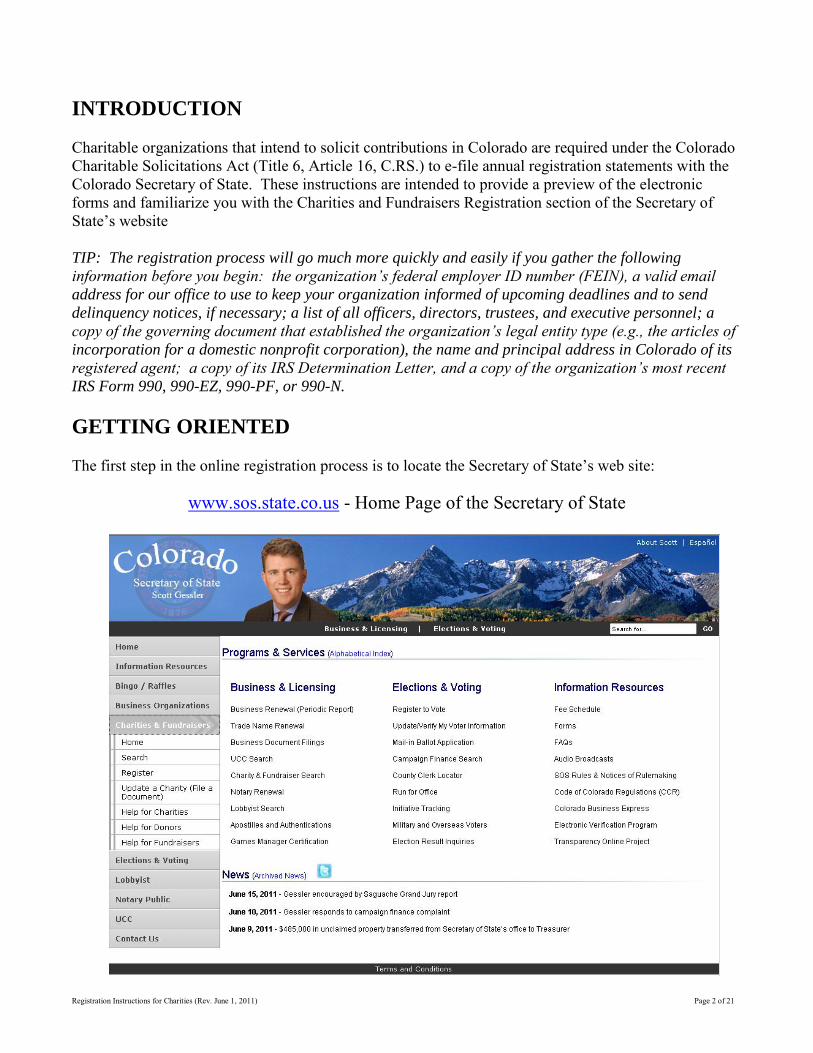

INTRODUCTION Charitable organizations that intend to solicit contributions in Colorado are required under the Colorado Charitable Solicitations Act (Title 6, Article 16, C.RS.) to e-file annual registration statements with the Colorado Secretary of State. These instructions are intended to provide a preview of the electronic forms and familiarize you with the Charities and Fundraisers Registration section of the Secretary of State’s website TIP: The registration process will go much more quickly and easily if you gather the following

information before you begin: the organization’s federal employer ID number (FEIN), a valid email

address for our office to use to keep your organization informed of upcoming deadlines and to send

delinquency notices, if necessary; a list of all officers, directors, trustees, and executive personnel; a

copy of the governing document that established the organization’s legal entity type (e.g., the articles of

incorporation for a domestic nonprofit corporation), the name and principal address in Colorado of its

registered agent; a copy of its IRS Determination Letter, and a copy of the organization’s most recent

IRS Form 990, 990-EZ, 990-PF, or 990-N.

GETTING ORIENTED The first step in the online registration process is to locate the Secretary of State’s web site:

www.sos.state.co.us - Home Page of the Secretary of State

Registration Instructions for Charities (Rev. June 1, 2011) Page 3 of 21

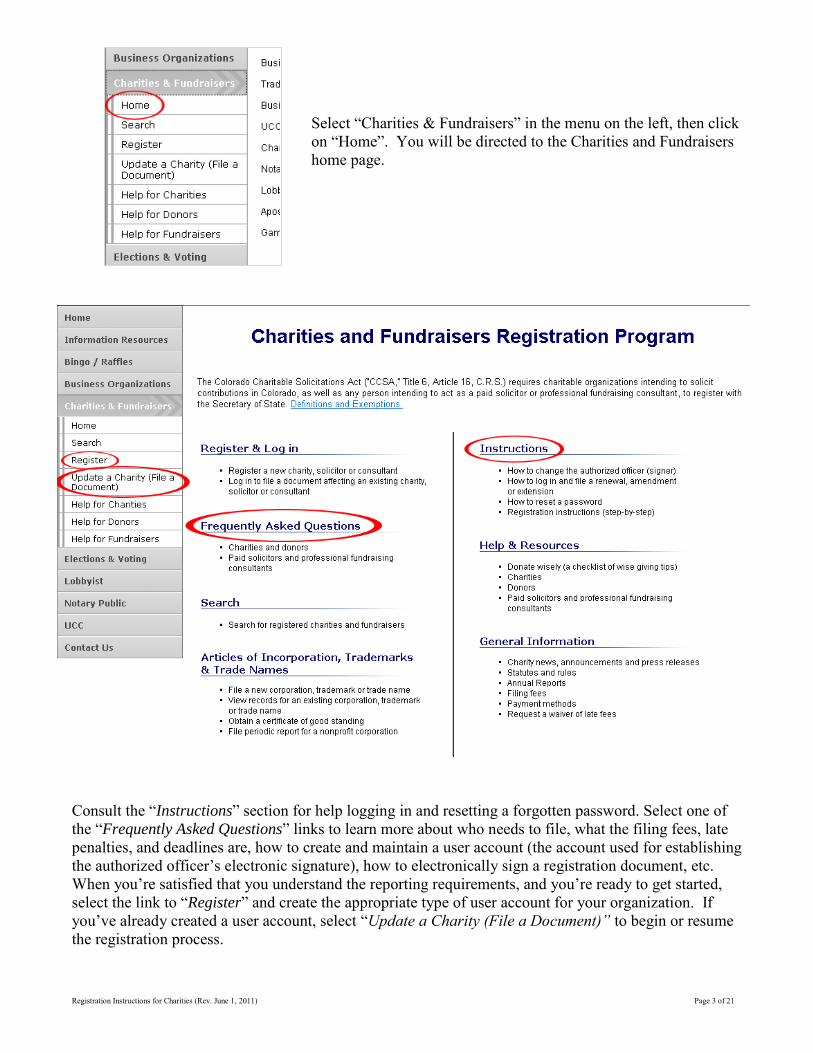

Select “Charities & Fundraisers” in the menu on the left, then click on “Home”. You will be directed to the Charities and Fundraisers home page.

Consult the “Instructions” section for help logging in and resetting a forgotten password. Select one of the “Frequently Asked Questions” links to learn more about who needs to file, what the filing fees, late penalties, and deadlines are, how to create and maintain a user account (the account used for establishing the authorized officer’s electronic signature), how to electronically sign a registration document, etc. When you’re satisfied that you understand the reporting requirements, and you’re ready to get started, select the link to “Register” and create the appropriate type of user account for your organization. If you’ve already created a user account, select “Update a Charity (File a Document)” to begin or resume the registration process.

Registration Instructions for Charities (Rev. June 1, 2011) Page 4 of 21

OVERVIEW OF THE REGISTRATION PROCESS

1. Create a New Account. Select the Register a New Charity, Solicitor or Consultant link to begin. On this first step, you will create a user account that ties together your organization’s filing history over time. Enter the organization’s FEIN, the name of an authorized officer1 who will electronically “sign” your forms, a daytime telephone number, and an email address for our office to use to contact the group regarding its filings. The registration e-file software will send all re-set passwords, receipts for payments, confirmations of approved filings, reminders of upcoming deadlines, and delinquency notices to this email address. Once the account is created, the e-file software will create a user ID and password that will constitute the authorized officer’s electronic signature and send the login information to the email address provided.

PLEASE NOTE:

o If you have been issued a user ID and password previously, you will need to select the Login

link rather than the Create New Account link to access the organization’s record and select registration documents.

o The e-file software permits only one user account per organization. If you receive an error message stating that the FEIN already exists or is already taken, it means that someone set up an account for your organization already, so you will need to contact program staff at (303) 894-2200 ext. 6487 or [email protected] to change the authorized officer’s name, telephone number, or email address.

o If you have forgotten your password, you can re-set it and receive a temporary password valid for four hours by selecting the Login link, and then the Forgot Password? link. You will need to know the organization’s FEIN and the email address used by the current authorized officer in order to re-set the password. If you don’t have both pieces of information, you may contact program staff at (303) 894-2200 ext. 6487 or [email protected] for assistance.

2. Log in. After creating an account, you can login to …

o Access and sign electronic registration forms o Review the status of pending filings o Electronically sign a solicitation notice or campaign financial report prepared by a paid

solicitor o Review your filing history o Pay filing fees and late fees o Change the organization’s fiscal year o File an extension

1 As stated in 8 CCR 1505-9, Rule 1.3, “Authorized Officer” means the officer designated by the filing entity to electronically sign any forms on behalf of the organization pursuant to the CCSA. This person shall be an officer of a nonprofit corporation, a trustee of a charitable trust, or a senior manager member of any other type of entity subject to the filing requirements of the CCSA.

Registration Instructions for Charities (Rev. June 1, 2011) Page 5 of 21

3. Summary Page. If the group is already registered and has no incomplete forms open on the system, you will be directed to the Summary Page upon login, where you will find links to file a document (amendments, renewals, extensions, etc.), a history of the organization’s filings and statuses, a link to archived Form 990s, and an option to print a registration certificate. The e-file software cannot accommodate more than one incomplete form at a time, so until one form is completed, signed, and the fee is paid, or else the form is cancelled, you will land directly in the incomplete form rather than the Summary Page when you login.

4. Registering Online. You will file everything online. This includes the Initial Registration,

Amendments, Renewals, Extension Requests, and Fiscal Year Changes. When the Initial Registration is approved, a registration number will be issued to the organization. The registration must then be renewed annually, which consists of providing updated financial information from the most recent fiscal year and making any other necessary changes, such as changes to the board of directors, changes to addresses, and so forth. Initial Registration Statement. If an Initial Registration is filed using estimated financial information, it will need to be updated via an Amendment by the 15th day of the fifth month following the close of the organization’s fiscal year. If the organization is unable to provide the actual financial figures from the most recent fiscal year by that time, it must file online for an extension of the deadline to remain in “Good” status and avoid late fees. “Renewing” a registration means updating the information on file with the Secretary of State after the organization’s fiscal year has concluded. This is done once per year, and is due at the same time as when the Form 990 is due to the IRS (the 15th day of the fifth month after the organization’s fiscal year has concluded). A Renewal automatically advances the reporting period one year and must include a financial report. If financial information for the most recent fiscal year is not available by the renewal deadline, the organization must file online for an extension of the deadline to remain in “Good” status and avoid late fees. “Amending” a registration is different. You file an Amendment if you need to correct an error or omission to same reporting period listed on your Initial Registration or Renewal (whichever was filed most recently), or if you need to update estimated financial information on an Initial Registration with actual financial figures. When an “Amendment” is selected, the reporting period is not advanced to the next year, because the information applies to the same reporting period listed on the organization’s last registration or renewal.

5. Signing Documents Prepared by Paid Solicitors (if applicable). If the organization has

contracted with an outside paid solicitor, the paid solicitor will prepare solicitation notices and solicitation campaign financial reports using the e-file software, and charities can login to their own records to view and sign those documents. Once it has signed a solicitation notice or campaign financial report, the charity should notify the paid solicitor that the document is ready to be filed with the Secretary of State, so the paid solicitor can pay the filing fee and submit the document for examination and approval by program staff.

Registration Instructions for Charities (Rev. June 1, 2011) Page 6 of 21

6. Paying Fees. VISA, MasterCard and American Express are accepted. Checks or money orders

drawn from a foreign financial institution will not be accepted as a form of payment for transactions with the Department of State; any document submitted with such a payment will be rejected and returned to the filing party. Only checks or money orders that are drawn from a United States financial institution will be accepted. Prepaid accounts can be established by paper application (available for printing on the website) with an initial deposit of a minimum of $500. Thereafter, future deposits to maintain the Prepaid Account must be a minimum of $500 each. Beginning with the first month upon opening a Prepaid Account, and for each month thereafter, the Department will assess a monthly service fee of $25 to cover costs associated with managing the account activity. No filing is officially submitted until it has been signed by all required parties and any applicable fee has been paid, including late fees. Once the fee is paid, the filing is submitted for approval. The secretary of state has up to ten days in which to approve or reject the filing. Filers will receive confirmation by email once a filing has bee approved. NOTE: A filing that is pending approval cannot be accessed by the filer for changes, until after it has been approved or rejected by program staff. If you have a filing awaiting approval, you cannot open or file any additional registration documents. Please allow time for your filing to be reviewed, before logging in again and attempting to file anything else from the Charities and Fundraisers section of the website.

7. Searching the Charities and Fundraisers Database. This is the public search capability that

lets consumers check the registration status of a charitable organization, paid solicitor, or professional fundraising consultant and inspect an organization’s filings and reports.

Registration Instructions for Charities (Rev. June 1, 2011) Page 7 of 21

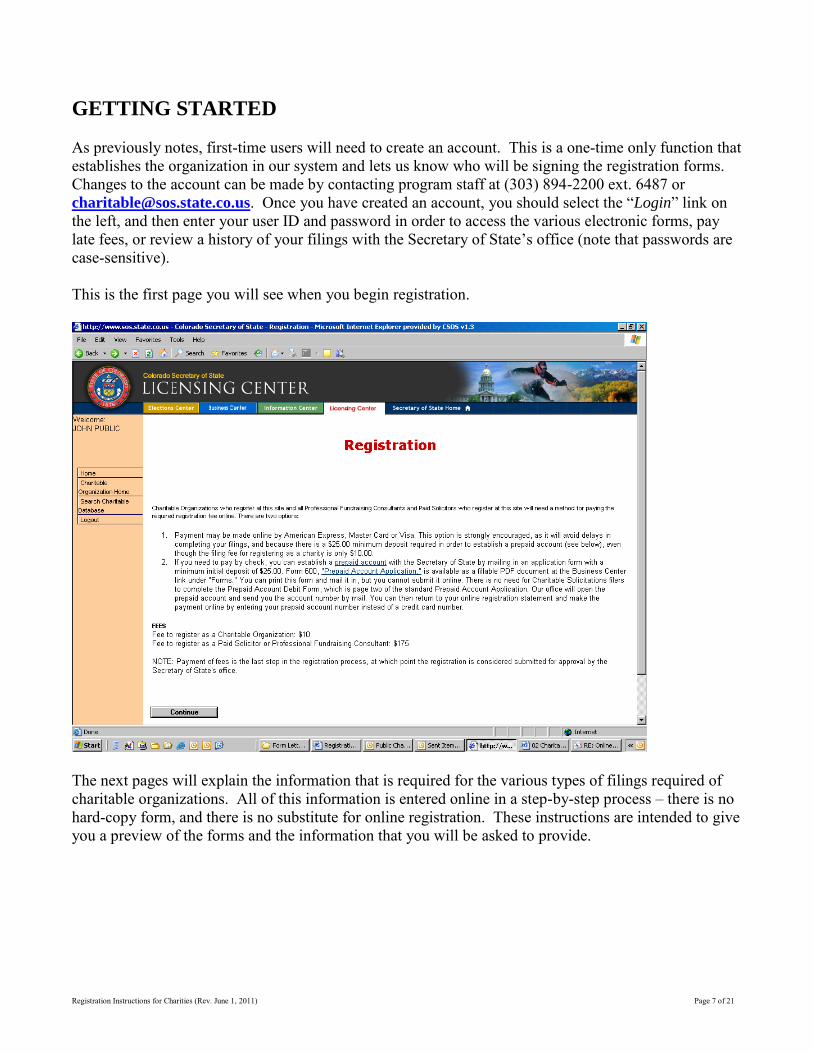

GETTING STARTED As previously notes, first-time users will need to create an account. This is a one-time only function that establishes the organization in our system and lets us know who will be signing the registration forms. Changes to the account can be made by contacting program staff at (303) 894-2200 ext. 6487 or [email protected]. Once you have created an account, you should select the “Login” link on the left, and then enter your user ID and password in order to access the various electronic forms, pay late fees, or review a history of your filings with the Secretary of State’s office (note that passwords are case-sensitive). This is the first page you will see when you begin registration.

The next pages will explain the information that is required for the various types of filings required of charitable organizations. All of this information is entered online in a step-by-step process – there is no hard-copy form, and there is no substitute for online registration. These instructions are intended to give you a preview of the forms and the information that you will be asked to provide.

Registration Instructions for Charities (Rev. June 1, 2011) Page 8 of 21

THE REGISTRATION STATEMENT

(CHARITABLE ORGANIZATIONS)

Every charitable organization -- except those listed in 6-16-104(6) C.R.S. -- that intends to solicit contributions, have contributions solicited on its behalf in Colorado, or participate in a charitable sales promotion must register with the Secretary of State prior to engaging in any of these activities. This registration requirement applies to all means of solicitation. Registration must be renewed annually and includes the filing of a financial report for the most recent fiscal year, which must be filed on or before the 15th day of the fifth calendar month after the close of each fiscal year in which the charity solicited funds in Colorado. In some cases, a parent organization may need to file a consolidated registration statement for itself and any of its chapters, branches, or affiliates that are also required to register in Colorado. Organizations that have been issued a group exemption letter by the Internal Revenue Service are eligible for this option, as are any organizations that are not required to file a Form 990 and prepare instead a single, consolidated financial statement on behalf of its subordinate organizations according to Generally Accepted Accounting Principles (GAAP). The main factor in deciding whether to file a consolidated registration statement is whether or not you can file a single financial statement that reflects the operations of the parent organization and all of its subordinate organizations. Registration Information Requested: 1) Name, address, telephone number, fax number (optional), email address (optional), web

address (optional) of the charitable organization. Please list the principal place of the business2 at a minimum. If this is not possible due to concerns about the safety of employees, volunteer, or the beneficiaries or the organization’s charitable services, please contact program staff at (303) 894-2200 ext. 6487 or [email protected] to discuss alternatives.

2) Address and telephone number of any other offices in Colorado. “Other offices” usually share a

parent organization's Federal Employer Identification Number (FEIN) and are distinct from "chapters, branches, affiliates, subordinate offices, locals, or posts," which have their own FEINs.

3) Address and telephone number of all chapters, branches, or affiliates in Colorado. Applicable in the event you wish to file a consolidated statement on behalf of one or more subordinate organizations -- also known as "chapters, branches, or affiliates." Subordinate organizations are related to parent organizations, but have separate FEINs and should not be confused with “other offices” of the same parent organization. In order to file a consolidated registration statement, your organization must have been issued a group exemption letter by the IRS, or if it does not file a Form 990, it must file a single, consolidated financial statement according to Generally Accepted Accounting Principles (GAAP).

2 According to 8 CCR 1505-9, Rule 1.12, “Principal Place of Business” means the bona fide physical street address of the organization or sole proprietor. This does not include a post office box or private mailbox.

Registration Instructions for Charities (Rev. June 1, 2011) Page 9 of 21

4) Charitable purposes and programs of the organization. Describe the organization’s exempt purpose and any major program services in a clear and concise manner.

5) Federal Employer Identification Number (FEIN). This space will be pre-populated with the

FEIN you provided when you set up your user account. Please be sure the number is correct. If the number is incorrect, please stop and contact our office at 303 894-2200 x6487 or [email protected] for further instructions.

6) Has the organization applied for or been granted IRS tax exempt status? Y/N.

a) If yes, date of application letter OR date of determination letter. Enter the date of the IRS determination letter, if one has been issued. Otherwise, enter the date of your tax-exempt application to the IRS.

7) Select up to three NTEE code(s) that best describe(s) your organization. NTEE codes are a generally accepted coding system to describe a charitable organization’s program and activities. You may select three of the highest-level codes, e.g., Arts, Culture, and Humanities (“A” in the NTEE classification system), or Educational Institutions (corresponds to the NTEE code “B”).

8) Organization’s tax-exempt status. If the organization is exempt from federal taxes under the Internal Revenue Code, choose the appropriate number to identify the IRS subsection type of the organization. This information is listed on your IRS determination letter, if applicable. For example, public charities are 501(c)(3)s, but civic leagues, social welfare organizations, and local associations of employees are 501(c)(4)s. If the organization has not yet been issued a determination letter by the IRS, select N/A or To Be Determined.

9) Name of Registration Service Provider (optional) – Enter the name of any registration services provider used by the organization, and the name and e-mail address of a contact person at that firm who maintains the charity’s registration filings with state charity offices. While these providers are often legal firms, the question is not intended to gather the name of the organization’s general legal counsel, unless state registration is one service the law firm provides the charity.

10) Registered Agent (Name, Address and E-mail). All registrants will be asked to provide the name and address of a registered agent with a Colorado address. Domestic nonprofit corporations can refer to their most recent periodic report or articles of incorporation for this information. Please note that a foreign nonprofit (i.e. incorporated in a state other than Colorado) is considered to be transacting business or conducting activities in Colorado, if it is subject to registration under the Colorado Charitable Solicitations Act, so these types of entities should already have filed a Statement of Foreign Entity Authority with the commercial side of the Business & Licensing Division, and consequently they should already have a registered agent with a Colorado address.

11) All other names under which organization solicits contributions. List any trade names “DBAs”

or special programs under which the group is commonly known and/or solicits contributions. Donor-advised funds, or other distinct funds that reach out to potential donors using a name other than a registered charitable organization’s primary name (e.g. the name of the community foundation that maintains the donor-advised fund) should be listed, unless the registered charitable organization’s name is clearly referenced in all solicitation materials.

Registration Instructions for Charities (Rev. June 1, 2011) Page 10 of 21

12) Name and physical street address of the chair of the board of directors, List the name of the person who is the formal head of the board of directors and presides at their meetings, whether that person’s actual title is the Chair, Chairman, Chairperson, President, Founder, etc.

13) Name and physical (street) address of the person with custody of financial records. Please

enter a bona fide physical street address for this person.

14) Names and addresses of the officers, directors, trustees, and executive personnel of the

organization. List each person who was an officer, director, trustee, or executive of the organization at any time during the year. The entire board of directors should be listed. When you renew your registration in subsequent years, you will only need to enter new names and delete old names; you will not need to re-enter all of this information.

15) Ending month of the organization’s fiscal (reporting) year. An organization operating on the

calendar year should enter December, while an organization with a fiscal year ending on June 30 should enter June.

16) Place and date (MM/DD/YYYY) the charitable organization was legally incorporated. Most

public charities are incorporated as nonprofit corporations or, in some states, as public benefit corporations. If the organization is not incorporated, enter the legal entity type of the organization (e.g. unincorporated nonprofit association, LLC, charitable trust, cooperative association) in the spaces provided, along with the date and state where it was legally established. Do not enter terms such “charity,” “charitable,” “charitable non-profit,” “foundation,” or “501(c)(3)” as a “Type of Organization;” enter the legal form of the organization under state law.

17) Are contributions to the organization tax deductible? Y/N. Please refer to the Internal Revenue

Service rules for organizations of your type if no IRS Determination Letter has been received. You may need to answer “no” initially, until a Determination Letter has been received. If the IRS later determines that contributions to your organization are tax-deductible, then the organization can amend its initial registration to change this answer to “yes.” Similarly, if the IRS revokes the tax-exempt status of the organization, the organization must amend its most recent registration filing to change this answer to “no.”

Registration Instructions for Charities (Rev. June 1, 2011) Page 11 of 21

THE FINANCIAL REPORT The Financial Report includes a disclosure of the group’s revenue, expenses, assets and liabilities from the most recent reporting period. The period listed on this report should match the reporting period shown on the IRS Form 990, 990-EZ, 990-PF, or 990-N. When registering for the first time, organizations must supply financial information for the most recent fiscal year in which such information is available, even if they not able to provide financial information for the most recently concluded fiscal year. For example, if a calendar year organization wishes to begin soliciting in Colorado in February, 2011, and its 2010 Form 990 has not been prepared yet, it should file an Initial Registration for the 2009 reporting period using the actual financial information that is available for that period, and then it should immediately request an extension of time for filing the 2010 registration renewal. “Newly Formed Organizations”3 should check the “Estimated Financial Information” indicator box on the financial form and file a first year budget that includes projected, estimated figures. These estimated

amounts will need to be replaced with actual financial figures by the 15th

day of the fifth calendar

month after the close of the organization’s first fiscal year by filing an Amendment to the Initial

Registration. Recall that an Amendment permits changes to the same reporting period as the organization last filed with the Secretary of State, while a Renewal advances the reporting period one year. Existing groups that have just learned of the requirement to register and were subject to registration under the Colorado Charitable Solicitations Act in previous years should “file back” two years to establish a filing history for the period of time during which they should have been registered. Registrations must be renewed by the 15th day of the fifth calendar month after the close of each fiscal year in which a charitable organization solicits in Colorado. Requests for extensions of time to file the financial form are available by logging in and filing an extension on the Secretary of State’s website, and are granted under terms, conditions, and procedures applicable to obtaining an extension of time to file a Form 990 return from the Internal Revenue Service. It is not sufficient that the IRS granted the organization an extension for filing the Form 990, 990-EZ, 990-PF, or 990-N; the organization must file a separate extension on the Secretary of State’s website. Colorado’s financial form was designed to correspond as much as possible to line items on the IRS Form 990 or Form 990-EZ. Most of the language in the supplemental online instructions here can also be found in the IRS instructions for the Form 990 and Form 990-EZ (available under Forms and

Publications at http://www.irs.gov/). To enter negative numbers, use the negative sign rather than

parentheses. The e-file software does not recognize parentheses as denoting a negative number.

3 According to 8 CCR 1505-9, Rule 1.10, “Newly-Formed Charitable Organization” means an organization that has not completed its first fiscal year or has not reached the 15th day of the fifth month since the close of its first fiscal year.

Registration Instructions for Charities (Rev. June 1, 2011) Page 12 of 21

REVENUE (Amounts Received During the Year) CONTRIBUTIONS. Report cash and non-cash amounts received as voluntary contributions, gifts, grants, bequests, or other similar amounts from the general public, foundations, and other exempt organizations. The general public includes individuals, corporations, trusts, estates, and other entities. Include all funds raised by an outside professional fundraiser in the charity's name and not just the amount actually received by the charity. Include contributions and grants from public charities and other exempt organizations that are neither fundraising organizations nor affiliates of the filing organization. Voluntary contributions are payments, or the part of any payment, for which the payer (donor) does not receive full retail value (fair market value) from the recipient (donee) organization. Report contributions here regardless of whether they are deductible by the contributor. Report amounts contributed by a commercial co-venture as a contribution received directly from the public. These are amounts received by an organization (donee) for allowing an outside organization (donor) to use the donee's name in a sales promotion campaign. Include the total amount of contributions received from fundraising events, which includes, but is not limited to, gaming events, dinners, auctions, and other events conducted for the sole or primary purpose of raising funds for the organization’s exempt activities. Include the total amount of contributions received indirectly from the public through solicitations campaigns conducted by federated fundraising agencies and similar fundraising organizations (such as a United Way organization). Federated fundraising agencies normally conduct fundraising campaigns within a single metropolitan area or some part of a particular state, and allocate part of the net proceeds to each participating organization on the basis of the donors’ individual designations and other factors. Report membership dues and assessments that represent contributions from the public rather than payments for benefits received or payments from affiliated organizations. Membership dues that are not contributions because they compare favorably with available benefits are reported as Program Service

Revenue. Membership dues may consist of both contributions and payment for goods and services. In that case, the portion of the membership dues that is a payment for goods and services should be reported as Program Service Revenue. Report the portion that exceeds fair market value of the goods or services provided as a contribution. Report the amount of contributions received from related organizations that are closely associated with the reporting organization (including contributions received from a parent organization, subordinate, or another organization with the same parent). If the organization is a sponsoring organization that maintains one or more donor advised funds, include gross amounts of contributions, gifts, grants, and bequests received for all donor advised funds the organization maintains. Non-cash contributions are anything other than cash, checks, money orders, credit card charges, wire transfers, and other transfers and deposits to a cash account of the organization. Value noncash donated items, like cars and securities, as of the time of receipt, even if sold immediately after they were received. If this amount exceeds $25,000, the organization must answer “Yes” to Part IV, line 29 on the IRS Form 990 and complete and attach Schedule M (Form 990). The Secretary of State may request a copy of these federal forms to verify correct reporting of noncash contributions.

Registration Instructions for Charities (Rev. June 1, 2011) Page 13 of 21

Form 990: Corresponds to Part VIII, Line 1a + 1b + 1c + 1d + 1f ( or Line 1h minus Line 1e). Form

990-EZ: Corresponds to Part I, Line 1 + Line 3). Note: Make sure to subtract Government Grants that are treated as a grant equivalent to a

contribution from Contributions as shown on the Form 990 and Form 990-EZ. Government Grants

that can be treated as contributions are reported separately on the state financial form, as explained

in the next section. GOVERNMENT GRANTS. Report government grants if they represent contributions. Such grants represent contributions if they encourage an organization receiving the grant to carry on programs or activities that further its exempt purposes. Form 990: Corresponds to Part VIII, Line 1e. Form 990-EZ: There is no corresponding line for

Government Grants on the Form 990-EZ. 990-EZ filers should refer to their own financial records to

determine whether any amounts need to be reported here as revenue from Government Grants.

PROGRAM SERVICE REVENUE, INCLUDING GOVERNMENT FEES AND CONTRACTS.

Enter the total of program service revenue. Program services are primarily those that form the basis of an organization’s exemption from tax. Program services can also include the organization's unrelated

trade or business activities. For example, publishing a magazine is a program service even though the magazine contains both editorials and articles that further the organization's exempt purpose and advertising, the income from which is taxable as unrelated business income. Program service revenue includes income earned by the organization for providing a government agency with a service, facility, or product that benefited that government agency directly rather than benefiting the public as a whole. Program service revenue includes tuition received by a school, revenue from admissions to a concert or other performing arts event or to a museum; royalties received as author of an educational publication distributed by a commercial publisher, interest income on loans a credit union makes to its members; payments received by a section 501(c)(9) organization from participants or employers of participants for health and welfare benefits coverage; insurance premiums received by a fraternal beneficiary society; and registration fees received in connection with a meeting or convention. Include membership dues and assessments that are not contributions, i.e., that compare reasonably with membership benefits received. Examples of membership benefits include subscriptions to publications, newsletters (other than one about the organization's activities only), free or reduced-rate admissions to events the organization sponsors, the use of its facilities, and discounts on articles or services that both members and nonmembers can buy. In figuring the value of membership benefits, do not include intangible benefits, such as the right to attend meetings, vote or hold office in the organization, and the distinction of being a member of the organization. Program service revenue also includes income from program-related investments. These investments are made primarily to accomplish an exempt purpose of the investing organization rather than to produce income. Examples are scholarship loans and low interest loans to charitable organizations, indigents, or victims of a disaster.

Registration Instructions for Charities (Rev. June 1, 2011) Page 14 of 21

Form 990: Corresponds to Part I, Line 9 and Part VIII, line 2g. Form 990-EZ: Corresponds to Part I,

Line 2.

INVESTMENTS. Include interest on savings and temporary cash investments, dividends and interest income from equity and debt securities, net rental income or loss (gross rental - rental expenses), other investment income, and net gain or loss from the sale of assets other than inventory (assets such as securities, real estate, royalty interests, or partnership interests, as well as program-related investments and fixed assets used by the organization in its related and unrelated activities). Form 990: Corresponds to Part I, Line 10 or Part VIII, column (A), lines 3, 4, and 7d). Form 990-EZ:

Corresponds to Part I, Line 4.

SPECIAL EVENTS AND ACTIVITIES. Enter the gross revenue, expenses, and net income or loss from all special events and activities, such as dinners, concerts, sports events, dances, carnivals, raffles, bingo games, other gambling activities, and door-to-door sales of merchandise. Note: special events may generate both revenue and contributions; the amount entered here should represent revenue only. Fundraising events do not include sales or gifts of goods or services of only nominal value; raffles or lotteries in which prizes have only nominal value; and solicitation campaigns that generate only contributions. Proceeds from these activities are considered contributions. Fundraising events do not include events or activities that substantially further the organization’s exempt purpose even if the also raise funds. Revenue from such program service activities is reported as program service revenue. Form 990: Corresponds to Part VIII, Line 8c + Line 9c. Form 990-EZ: Corresponds to Part I, Line 6d. SALES OF INVENTORY. Report gross sales of inventory items, less returns and allowances and cost of goods sold. Sales of inventory items are sales of those items donated to the organization, that the organization makes to sell to others, or that it buys for resale. Report the sales revenue regardless of whether the sales activity is an exempt function of the organization or an unrelated trade or business. Sales of inventory do not include the sale of goods related to a fundraising event, which should be reported as Special Event Revenue. Do not report here sales of investments on which the organization expected to profit by appreciation and sale, which should be reported as Investments Revenue.

Form 990: Corresponds to Part VIII, Line 10c. Form 990-EZ, Corresponds to Part I, Line 7c.

OTHER REVENUE. Include all revenue not covered in any other category. Examples of other revenue include interest on notes receivable not held as investments or as program-related investments; interest on loans to officers, directors, trustees, key employees, and other employees, and royalties that are not investment income or program service revenue. Form 990: Corresponds to Part VIII, Line 5 + Line 6d + Line 11e. Form 990-EZ: Corresponds to Line

3 + Line 5c + Line 8.

Registration Instructions for Charities (Rev. June 1, 2011) Page 15 of 21

EXPENSES (Amounts Paid Out During the Year)

Tip for 990-EZ filers: Although the IRS changed Form 990-EZ to a new format, State of Colorado

reporting still requires expenses to be allocated across the three main functions, which are Program

Services, Management and General, and Fundraising.

You may be able to calculate reportable amounts using the following formula:

Program + Management and General + Fundraising = Total Expenses

Notice that Program Service Expenses (Part III, Line 32) and Total Expenses (Part I, Line 17) both

appear on Form 990-EZ. If you can determine the amount that your group spent on fundraising during

the reporting period, simply subtract program services expenses and fundraising expenses from your

total expenses to determine the figure to enter on the Colorado form for management and general

expenses.

PROGRAM SERVICES. Program services are mainly those activities that further the organization’s exempt purposes. A program service is a major (usually ongoing) objective of an organization, such as adoptions, recreation for the elderly, or rehabilitation. Program services can also include the organization's unrelated trade or business activities. For example, publishing a magazine is a program service even though the magazine contains both editorials and articles that further the organization's exempt purpose and advertising, the income from which is taxable as unrelated business income. Program services can include grants and other assistance that the organization, at its own discretion, gave to governmental units and other organizations in the United States; grants by a United Way or similar federated fundraising organization to member or participating agencies; any amount paid by the organization to individuals in the United States in the form of scholarships, fellowships, stipends, research grants, and similar payments and distributions; and any grants and other assistance paid to third party providers for the benefit of specified individuals; and the total amount of grants and other assistance made to foreign governments, foreign organizations, and foreign individuals outside the United States, and to U.S. individuals for foreign activity. Depending on the organization’s method of allocation (which must be reasonable, accurate, and documented in its records), any of the items listed in Part IX of the Form 990, Statement of Functional Expenses, except for Professional Fundraising Services (Part IX, Line 11e), can be allocated to program services. Professional Fundraising Services expenses should not be reported as program service expenses even though one of the organization’s purposes is to solicit contributions. Include lobbying expenses here if the lobbying is directly related to the organization’s exempt purposes.

Form 990: Corresponds to Part IX, Line 25, column B. Form 990-EZ: Corresponds to Part III, Line 32.

ADMINISTRATION - MANAGEMENT AND GENERAL. Report the organization's expenses for overall function and management, rather than to fundraising activities or program services. Overall management usually includes the salaries and expenses of the chief officer of the organization and that officer's staff. If part of their time is spent directly supervising program services and fundraising activities, their salaries and expenses should be allocated among those functions. Other expenses to report here include those for meetings of the board of directors or similar group; committee and staff meetings (unless held in connection with specific program services or fundraising activities); general

Registration Instructions for Charities (Rev. June 1, 2011) Page 16 of 21

legal services; accounting (including patient accounting and billing); general liability insurance; office management; auditing, personnel, and other centralized services; preparation, publication, and distribution of an annual report; and investment expenses. Include lobbying expenses, if they do not directly relate to the organization’s exempt purposes, and expenses incurred to manage investments. Do not use this field to report costs of special meetings or other activities that relate to fundraising or specific program services.

Form 990: Corresponds to Part IX, Line 25, column C. Form 990-EZ: No corresponding entry; Refer to

the group’s financial records or Statement of Functional Expenses to determine this amount.

FUNDRAISING EXPENSES. Fundraising expenses are the total expenses incurred in soliciting contributions, gifts, and grants. Report as fundraising expenses all expenses, including allocable overhead costs, incurred in (a) publicizing and conducting fundraising campaigns, including any fees paid to outside fundraisers for solicitation campaigns they conducted or for consultation services connected with a solicitation of contributions by the organization itself; (b) soliciting bequests and grants from foundations or other organizations, or government grants; (c) participating in federated fundraising campaigns; (d) preparing and distributing fundraising manuals, instructions, and other materials; and (e) conducting special events that generate contributions in addition to revenue.

Form 990: Corresponds to Part IX, Line 25, column D. Form 990-EZ: No corresponding entry; Refer to

the group’s financial records or Statement of Functional Expenses to determine this amount.

Registration Instructions for Charities (Rev. June 1, 2011) Page 17 of 21

SUMMARY OF BALANCE SHEET AS OF FISCAL YEAR END

TOTAL ASSESTS, END OF YEAR. This should reflect the total of: (a) non-interest-bearing checking accounts, deposits in transit, change funds, petty cash funds, or any other non-interest-bearing accounts; (b) interest-bearing checking accounts, savings and temporary cash investments, such as money market funds, commercial paper, certificates of deposit, and U.S. Treasury bills or governmental obligations that mature in less than one year; (c) accounts receivable from the sale of goods and/or the performance of services; (d) pledges receivable; (e) grants receivable from governmental agencies, foundations, and other organizations; (f) receivables due from officers, directors, trustees, and key employees, and all secured and unsecured loans to such persons; (g) other notes and loans receivable; (h) materials, goods, and supplies purchased or manufactured by the organization and held for future sale or use (inventories for sale or use); (i) the amount of short-term and long-term prepayments of expenses attributable to one or more future accounting periods (i.e., "prepaid expenses and deferred charges" - examples include prepayments of rent, insurance, and pension costs, and expenses incurred for a solicitation campaign of a future accounting period; (j) the book value, which may be market value, of securities held as investments; (k) the book value (cost or other basis less accumulated depreciation) all land, buildings, and equipment held for investment purposes, such as rental properties; (l) all other investment holdings not accounted for elsewhere; (m) the book value (cost or other basis less accumulated depreciation) of all land, buildings, and equipment owned by the organization and not held for investment (includes any property plant, and equipment owned and used by the organization in conducting its exempt activities); and (n) the book value of each category of assets not accounted for elsewhere in this form (e.g., program-related investments, which are investments made primarily to accomplish an exempt purpose of the reporting organization rather than to produce income).

Form 990: Corresponds to Part X, Line 16, Column B. Form 990-EZ: Corresponds to Part II, Line 25,

Column B.

TOTAL LIABILITIES, END OF YEAR. This should reflect the total of: (a) accounts payable to suppliers and others and accrued expenses, such as salaries payable, accrued payroll taxes, and interest payable; (b) grants payable (the unpaid portion of grants and awards that the organization has made a commitment to pay other organizations or individuals, whether or not the commitments have been communicated to the grantees); (c) deferred revenue, i.e., revenue that the organization has received but not yet earned; (d) the unpaid balances of loans received from officers, directors, trustees, and key employees; (e) the amount of tax-exempt bonds (or other obligations) issued by the organization on behalf of a state or local governmental unit, or by a state or local governmental unit on behalf of the organization, and for which the organization has a direct or indirect liability (tax-exempt bond liabilities); (f) mortgages and other notes payable; and (g) other liabilities not reported elsewhere in this form.

Form 990: Corresponds to Part X, Line 26, Column B. Form 990-EZ: Corresponds to Part II, Line 26,

Column B.

NET ASSETS, END OF YEAR. The e-file software calculates this amount by subtracting Total Liabilities, end of year, from Total Assets, end of year.

Registration Instructions for Charities (Rev. June 1, 2011) Page 18 of 21

OPTIONAL. Certain types of organizations follow accounting standards outlined by the Financial Accounting Standards Board (FSAB) in FASB publication SFAS-117, Financial Statements of Not-for-Profit Organizations, now codified in FASB Accounting Standards Codification 958, Not-for-Profit Entities (ASC 958). Neither the IRS nor the State of Colorado requires that reports be prepared in accordance with SFAS-117 ASC 958. Classify and report net assets in three groups (unrestricted, temporarily restricted, and permanently restricted) based on the existence or absence of donor-imposed restrictions and the nature of those restrictions. NOTE: The total of these three categories must equal Net Assets, End of Year, as described above:

Form 990: Corresponds to Part X, Column B, Lines 27 through 29. Form 990-EZ: No corresponding

entry.

PAID SOLICITORS AND PROFESSIONAL FUNDRAISING CONSULTANTS 1) Outside Professional Fundraisers Fees. Enter the total amount the charitable organization paid to

outside fundraisers for solicitation campaigns or for consultation services connected with a solicitation of contributions by the organization itself.

Form 990: Most or all of this total should be taken from Part I, line 16a, Current Year. Form 990-

EZ: no corresponding entry.

2) Outside Fundraising Professionals. If the organization used or contracted to use outside fundraising professionals (such as “paid solicitors,” “professional fundraising counsel,” or “commercial co-venturers”) during the period covered by this report, list their names, addresses (street & mailing), telephone numbers, and location of offices used to perform work on behalf of your organization.

OTHER INFORMATION (similar to some of the questions asked on the Form 990, Parts IV and V.) 1) Is the organization related (other than by association with a statewide or nationwide

organization) through common membership, governing bodies, trustees, officers, etc., to any

other exempt or nonexempt organization? Answer “yes” if most (more than 50%) of the organization’s governing body, officers, directors, trustees, or membership are also officers, directors, trustees, employees or members of any other organization. Disregard any coincidental overlap of membership with another organization; that is, when membership in one organization is not a condition of membership in another organization. For example, assume that a majority of the members of a section 501(c)(4) civic organization also belong to a local chamber of commerce described in section 501(c)(6). The civic organization should answer “no” to this question if it does not require its members to belong to the chamber of commerce. Also disregard affiliation with any statewide or nationwide federation of similar organizations. A local labor union whose members are also members of a national labor organization would answer “no” to this question.

Registration Instructions for Charities (Rev. June 1, 2011) Page 19 of 21

Form 990: corresponds to Part IV, Line 34. Form 990-EZ: no corresponding question.

a) If “Yes,” enter the name of the organization: (Form 990: see Schedule R, Part II ; Form 990-

EZ: no corresponding question.) i) Is this related organization an exempt or nonexempt organization? (Form 990: see Schedule

R, Part I, Column D; Form 990-EZ: no corresponding question) 2) Did the organization solicit any contributions or gifts that were not tax-deductible?

a) If “Yes,” did the organization include with every solicitation an express statement that such contributions or gifts were not tax deductible? (Part V, Line 6b of Form 990; not asked on Form

990-EZ) Form 990: corresponds to Part V, Line 6a; Form 990-EZ: no corresponding question.

3) List the States with which you are registered to conduct solicitations or from which you have

been granted an exemption. Please list all of the states with which the organization registered, regardless of whether or not the organization sent each state a 990 or 990-EZ in fulfillment of the state’s reporting obligations. You can select “United States” from the drop-down list if you are registered nationally, or you can select multiple states by holding down the control key and clicking your left mouse button. Form 990: Similar – but not identical – to part VI, Section C, Line 17; Form 990-EZ: similar to

question asked in Part V, Line 41.

Registration Instructions for Charities (Rev. June 1, 2011) Page 20 of 21

CHARITABLE ORGANIZATION EXTENSION REQUESTS

Requests for extensions of time to file a charity’s annual financial report are granted under terms and conditions applicable to obtaining an extension of time to file a Form 990 with the IRS, but they must be filed online at the Secretary of State’s website, even if the organization has already sent a Form 8868 to the Internal Revenue Service. Extension requests should be made before the original or extended deadline has passed if the organization wishes to remain in “Good” standing and avoid paying late fees. Organizations cannot apply for both the automatic three-month extension and the additional three-month extension at the same time. If both three-month extensions are needed, the group should file the first extension and then return to the File a Document menu, file the second extension, and provide a reason for the second extension. The following items appear on the extension request form: 1) Registration Number. This is the 11-digit registration number issued when the organization’s

initial registration for charitable solicitations was approved.

2) Federal FEIN. The organization’s 9-digit Federal Employer Identification Number. 3) Name of Organization.

4) Address of Principal Office.

5) Telephone and Fax Number.

6) E-mail Address.

7) Name of person making request.

8) Is this a Form 990-T corporation? The IRS Form 990-T is a tax return (rather than an information return) that must be filed by organizations that had unrelated trade or business income. The answer to this question is “No” for most organizations. a) If the answer is yes, then that means your organization is requesting an automatic 6-month

extension rather than the 3-month extension available to all other organizations. There is no second extension request required of organizations that file the Form 990-T.

Registration Instructions for Charities (Rev. June 1, 2011) Page 21 of 21

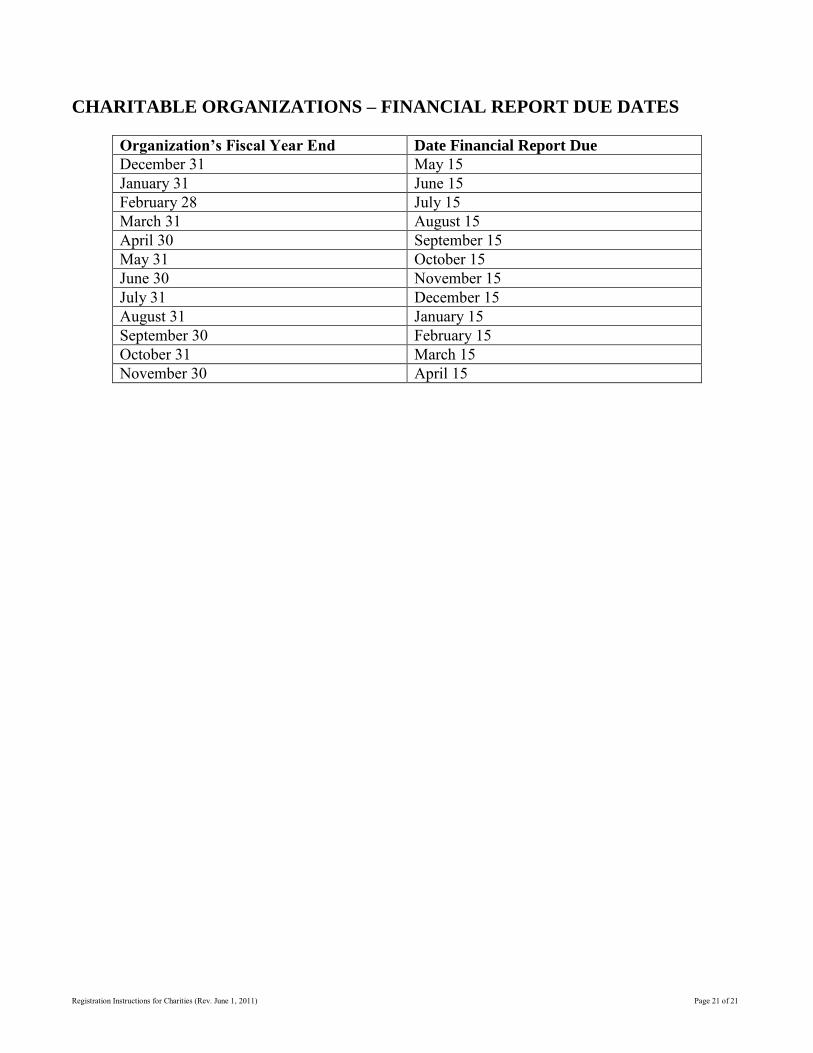

CHARITABLE ORGANIZATIONS – FINANCIAL REPORT DUE DATES

Organization’s Fiscal Year End Date Financial Report Due

December 31 May 15 January 31 June 15 February 28 July 15 March 31 August 15 April 30 September 15 May 31 October 15 June 30 November 15 July 31 December 15 August 31 January 15 September 30 February 15 October 31 March 15 November 30 April 15

![ICAPA Presentation.pptx [Read-Only] presentation.pdf · 10/12/2016 1 Office of the Attorney General Lawrence G. Wasden Idaho Charitable Solicitations Act, title 48, chapter 12, Idaho](https://static.documents.pub/doc/80x56/5f0b6c7c7e708231d43072ca/icapa-read-only-presentationpdf-10122016-1-office-of-the-attorney-general.jpg)