Combined Scheme Information Document SMS INVEST to 56767 Toll free: 1800 200 2434 Visit: www.assetmanagement.hsbc.com/in The particulars of the Scheme(s) have been prepared in accordance with the Securities and Exchange Board of India (Mutual Funds) Regulations 1996, as amended till date, and filed with Securities and Exchange Board of India (SEBI), along with a Due Diligence Certificate from the AMC. The units being offered for public subscription have not been approved or recommended by SEBI nor has SEBI certified the accuracy or adequacy of the Combined Scheme Information Document. The Combined Scheme Information Document sets forth concisely the information about the scheme(s) that a prospective investor ought to know before investing. Before investing, investors should also ascertain about any further changes to this Combined Scheme Information Document after the date of this Document from the Mutual Fund / Investor Service Centres / Website / Distributors or Brokers. Investors in the Scheme(s) are not being offered any guaranteed / assured returns. Investors are advised to consult their Legal /Tax and other Professional Advisors in regard to tax/legal implications relating to their investments in the Scheme(s) before making decision to invest in or redeem the Units. The investors are advised to refer to the Statement of Additional Information (SAI) for details of HSBC Mutual Fund, Tax and Legal issues and general information on www.assetmanagement.hsbc.com/in. SAI is incorporated by reference (is legally a part of the Combined Scheme Information Document. For a free copy of the current SAI, please contact your nearest Investor Service Centre or log on to www.assetmanagement.hsbc.com/in. The Combined Scheme Information Document should be read in conjunction with the SAI and not in isolation. This Combined Scheme Information Document is dated October 10, 2016. Continuous offer of Units of the Scheme(s) at NAV based prices Sponsor: HSBC Securities and Capital Markets (India) Private Limited Regd. Office: 52/60, Mahatma Gandhi Road, Fort, Mumbai 400 001, India. Trustee: Board of Trustees 16, V. N. Road, Fort, Mumbai 400 001, India Asset Management Company: HSBC Asset Management (India) Private Limited Regd. & Corp. Office: 16, V. N. Road, Fort, Mumbai 400 001, India Refer next page for Product Labelling

The particulars of the Scheme(s) have been prepared in accordance with the Securities and Exchange Board of India (Mutual Funds)

Regulations 1996, as amended till date, and fi led with Securities and Exchange Board of India (SEBI), along with a Due Diligence

Certifi cate from the AMC. The units being offered for public subscription have not been approved or recommended by SEBI nor

has SEBI certifi ed the accuracy or adequacy of the Combined Scheme Information Document.

The Combined Scheme Information Document sets forth concisely the information about the scheme(s) that a prospective investor ought to know before investing. Before investing, investors should also ascertain about any further changes to this Combined Scheme Information Document after the date of this Document from the Mutual Fund / Investor Service Centres / Website / Distributors or Brokers. Investors in the Scheme(s) are not being offered any guaranteed / assured returns. Investors are advised to consult their Legal /Tax and other Professional Advisors in regard to tax/legal implications relating to their investments in the Scheme(s) before making decision to invest in or redeem the Units.

The investors are advised to refer to the Statement of Additional Information (SAI) for details of HSBC Mutual Fund, Tax and

Legal issues and general information on www.assetmanagement.hsbc.com/in.

SAI is incorporated by reference (is legally a part of the Combined Scheme Information Document. For a free copy of the current

SAI, please contact your nearest Investor Service Centre or log on to www.assetmanagement.hsbc.com/in.

The Combined Scheme Information Document should be read in conjunction with the SAI and not in isolation.

This Combined Scheme Information Document is dated October 10, 2016.

Continuous offer of Units of the Scheme(s) at NAV based prices

Sponsor:

HSBC Securities and Capital Markets (India) Private LimitedRegd. Offi ce: 52/60, Mahatma Gandhi Road,Fort, Mumbai 400 001, India.

Trustee:

Board of Trustees16, V. N. Road, Fort,Mumbai 400 001, India

Asset Management Company:

HSBC Asset Management (India) Private LimitedRegd. & Corp. Offi ce: 16, V. N. Road, Fort,Mumbai 400 001, India

Refer next page for Product Labelling �

2 Combined Scheme Information Document (SID)

PRODUCT LABELING:To provide investors an easy understanding of the kind of product / scheme they are investing in and its suitability to them, the product labeling for the following schemes is as under:

Scheme Name Riskometer

HSBC Equity Fund (HEF)(An open-ended diversifi ed Equity Scheme)This product is suitable for investors who are seeking*:

To create wealth over long term Investment in equity and equity related securities

Investors understand that their principal will be at Moderately High risk

HSBC India Opportunities Fund (HIOF)(An open-ended fl exi-cap Equity Scheme)This product is suitable for investors who are seeking*:

To create wealth over long term Investment in equity and equity related securities across market capitalizations Investors understand that their principal will be at Moderately High risk

HSBC Midcap Equity Fund (HMEF)(An open-ended diversifi ed Equity Scheme)This product is suitable for investors who are seeking*:

To create wealth over long term Investment in predominantly mid cap equity and equity related securities Investors understand that their principal will be at Moderately High risk

HSBC Infrastructure Equity Fund (HIEF)(An open-ended Equity Scheme)This product is suitable for investors who are seeking*:

To create wealth over long term Investment in equity and equity related securities, primarily in themes that play an important role in India’s economic development Investors understand that their principal will be at High risk

HSBC Dynamic Fund (HDF)(An open-ended Scheme)This product is suitable for investors who are seeking*:

To create wealth over long term Investment in equity and equity related securities and in debt instruments when view on equity markets is negative Investors understand that their principal will be at Moderately High risk

HSBC Emerging Markets Fund (HEMF)An open-ended SchemeThis product is suitable for investors who are seeking*:

To create wealth over long term Investment in equity and equity related securities of Emerging economies Investors understand that their principal will be at High risk

HSBC Tax Saver Equity Fund (HTSF)(An open-ended Equity Linked Savings Scheme (ELSS))This product is suitable for investors who are seeking*:

To create wealth over long term Investment in equity and equity related securities with no capitalisation bias. Investors understand that their principal will be at Moderately High risk

HSBC Dividend Yield Equity Fund (HDYEF)(An open-ended Equity Scheme)This product is suitable for investors who are seeking*:

To create wealth over long term Investment in equity and equity related securities

Investors understand that their principal will be at Moderately High risk

HSBC Asia Pacifi c (Ex Japan) Dividend Yield Fund (HAPDF) (An open ended fund of funds scheme)This product is suitable for investors who are seeking*:

To create wealth over long-term Investment in equity and equity related securities of Asia Pacifi c countries (excluding Japan) through fund of funds route Investors understand that their principal will be at High risk

HSBC Brazil Fund (HBF) (An open-ended Fund of Funds Scheme)This product is suitable for investors who are seeking*:

To create wealth over long term Investment in equity and equity related securities through feeder route in Brazilian markets Investors understand that their principal will be at High risk

HSBC Monthly Income Plan (HMIP) (An open-ended Fund) Monthly Income is not assured and is subject to the availability of distributable surplusThis product is suitable for investors who are seeking*:

Regular income over medium term Investment in fi xed income (debt and money market instruments) as well as equity and equity related securities

Investors understand that their principal will be at Moderately High risk

* Investors should consult their fi nancial advisers if in doubt about whether the product is suitable for them.

HSBC Mutual Fund 3

Scheme Name Riskometer

HSBC Ultra Short Term Bond Fund (HUSBF)(An open-ended Debt Scheme)This product is suitable for investors who are seeking*:

Liquidity over short term Investment in Debt / Money Market Instruments

Investors understand that their principal will be at Moderately Low risk

HSBC Flexi Debt Fund (HFDF)(An open-ended Debt Scheme)This product is suitable for investors who are seeking*:

Regular income over long term Investment in Debt / Money Market Instruments

Investors understand that their principal will be at Moderate risk

HSBC Global Consumer Opportunities Fund– Benefi ting from China’s Growing Consumption Power(An open-ended Fund of Funds Scheme)This product is suitable for investors who are seeking*:

To create wealth over the long-term. Investment in equity and equity related securities around the world focusing on growing consumer behaviour of China through feeder route.

Investors understand that their principal will be at High risk

HSBC Managed Solutions (HMS)(An open ended Fund of Funds Scheme)

Managed Solutions India – GrowthThis product is suitable for investors who are seeking*:

To create wealth over the long-term. Investing predominantly in units of equity mutual funds as well as in a basket of debt mutual funds, gold & exchange traded funds, offshore mutual funds and money market instruments;

Investors understand that their principal will be at

Moderately High risk

HSBC Managed Solutions (HMS)(An open ended Fund of Funds Scheme)

Managed Solutions India – ModerateThis product is suitable for investors who are seeking*:

To create wealth and provide income over the long-term; Investments in a basket of debt mutual funds, equity mutual funds, gold & exchange traded funds, offshore mutual funds and money market instruments;

Investors understand that their principal will be at

Moderately High risk

HSBC Managed Solutions (HMS)(An open ended Fund of Funds Scheme)

Managed Solutions India – ConservativeThis product is suitable for investors who are seeking*:

To provide income over the long-term; Investing predominantly in units of debt mutual funds as well as in a basket of equity mutual funds, gold & other exchange traded funds and money market instruments;

Investors understand that their principal will be at Moderate risk

HSBC Income Fund (HIF) - Investment Plan

(An open-ended Income Scheme)This product is suitable for investors who are seeking*:

Regular income over long term Investment in diversifi ed portfolio of fi xed income securities

Investors understand that their principal will be at Moderate risk

HSBC Income Fund (HIF) - Short Term Plan

(An open-ended Income Scheme)This product is suitable for investors who are seeking*:

Regular income over medium term Investment in diversifi ed portfolio of fi xed income securities

Investors understand that their principal will be at Moderately Low risk

HSBC Cash Fund (HCF)(An open-ended Liquid Scheme)HSBC Income Fund Short Term PlanThis product is suitable for investors who are seeking*:

Overnight liquidity over short term Investment in Money Market Instruments Investors understand that their principal will be at Low risk

* Investors should consult their fi nancial advisers if in doubt about whether the product is suitable for them.

4 Combined Scheme Information Document (SID)

Highlights / Summary of the Schemes .............................. 4

Due Diligence Certifi cate .................................................... 28

SECTION II

Information about the Schemes ......................................... 29

A. Type of the Scheme ........................................................ 29

B. Investment Objective ..................................................... 29

C. Asset Allocation of the Scheme ..................................... 29

D. Where will the Scheme Invest? ...................................... 29

E. Change in Investment Pattern ........................................ 42

F. Investment Strategies ..................................................... 49

F. Product Differentiation .................................................. 63

G. Fundamental Attributes .................................................. 67

H. Benchmark Index ........................................................... 67

I. Fund Manager(s) ............................................................ 69

J. Investment Restrictions .................................................. 71

K. Schemes Performance .................................................... 73

L. Scheme Portfolio Holdings ............................................ 77

M. Portfolio Turnover ......................................................... 81

N. Investment by Directors, Fund Managers and Key Managerial Personnel of the AMC in Schemes of HSBC Mutual Fund ...................................................... 81

SECTION III

Units and Offer .................................................................... 82

Deduction of Transaction Charge for Investments through Distributors / Agents ....................................... 102

Procedure for Direct Applications ................................. 102

SECTION V

Unitholders’ Rights ............................................................. 103

SECTION VI

Penalties and Pending Litigations ................................. 103

TABLE OF CONTENTS

Page No. Page No.

HSBC Mutual Fund 5

HIGHLIGHTS / SUMMARY OF THE SCHEMES

Name of the Scheme HSBC EQUITY FUND (HEF) HSBC INDIA OPPORTUNITIES FUND (HIOF)

Type of Scheme An open-ended diversifi ed equity Scheme An open-ended fl exi-cap equity Scheme

Investment Objective To generate long-term capital growth from an actively managed portfolio of equity and equity related securities.

To seek long term capital growth through investments across all market capitalisations, including small, mid and large cap stocks. The fund aims to be predominantly invested in equity and equity related securities. However, it could move a signifi cant portion of its assets towards fi xed income securities if the fund manager becomes negative on equity markets.

Liquidity Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to despatch redemption proceeds within 3 Business Days.

Benchmark Index S&P BSE 200 S&P BSE 500

Transparency / NAV Disclosure

The AMC will calculate and disclose the NAVs of the Scheme at the close of every Business Day. NAV of the Scheme / Option(s) shall be made available at all Investor Service Centres of the AMC. The AMC shall have the NAV published in two daily newspapers. The AMC shall update the NAVs on the website of the Fund www.assetmanagement.hsbc.com/in and of the Association of Mutual Funds in India - AMFI (www.amfi india.com) by 9.00 p.m. on every Business Day. In case of any delay, the reasons for such delay would be explained to AMFI in writing. If the NAVs are not available before commencement of Business Hours on the following day due to any reason, the Fund shall issue a press release giving reasons and explaining when the Fund would be able to publish the NAVs. The NAV of the Scheme will be determined on every Business Day, except under special circumstances specifi ed in this Combined SID.

As presently required by the SEBI (MF) Regulations, the AMC will disclose the monthly portfolio of the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. Also a complete statement of the Scheme’s portfolio would be available on the Fund’s website, and published by the Mutual Fund as an advertisement in one English daily circulating in the whole of India and in a newspaper published in the language of the region where the head offi ce of the mutual fund is situated, within 1 month from the close of each half year (i.e. 31 March and 30 September) or mailed to the Unitholders.

Loads (including SIP / STP where applicable)

Entry Load and Exit Load : NIL;

Minimum Application Amount(Lumpsum)

Rs. 10,000/- per application and in multiples of Re. 1/- thereafter

Minimum Additional investment

Rs 1,000/- per application and in multiples of Re. 1/- thereafter

Minimum Application Amount (SIP)

Minimum Investment Amount - Rs. 1000 (monthly) or Rs. 3000 (quarterly);Minimum no. of installments - 12 (monthly) or 4 (quarterly);Minimum aggregate investment - Rs. 12,000.

Minimum Redemption Amount

Rs 1000/- and in multiples of Re. 1/- thereafter

Plan / Options Options : i) Growth ii) DividendA Direct Plan (with the above Options) is also available for investors who subscribe to Units directly with the Fund.Plans and Options thereunder will have a common portfolio.

Sub Options Dividend Payout Option and Dividend Reinvestment Option

Dividend Declaration of dividend and its frequency will inter alia depend upon the distributable surplus. Dividend may be declared from time to time at the discretion of the Trustees.

Name of the Scheme HSBC MIDCAP EQUITY FUND (HMEF) HSBC INFRASTRUCTURE EQUITY FUND (HIEF)

Type of Scheme An open-ended diversifi ed equity Scheme An open-ended equity Scheme

Investment Objective To generate long term capital growth from an actively managed portfolio of equity and equity related securities primarily being Midcap stocks. However, it could move a portion of its assets towards fi xed income securities if the fund manager becomes negative on the Indian equity markets.

To generate long term capital appreciation from an actively managed portfolio of equity and equity related securities by investing predominantly in equity and equity related securities of companies engaged in or expected to benefi t from growth and development of Infrastructure in India.

6 Combined Scheme Information Document (SID)

Name of the Scheme HSBC MIDCAP EQUITY FUND (HMEF) HSBC INFRASTRUCTURE EQUITY FUND (HIEF)

Liquidity Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to despatch redemption proceeds within 3 Business Days.

Benchmark Index S&P BSE MidCap Index S&P BSE 200

Transparency / NAV Disclosure

The AMC will calculate and disclose the NAVs of the Scheme at the close of every Business Day. NAV of the Scheme / Option(s) shall be made available at all Investor Service Centres of the AMC. The AMC shall have the NAV published in two daily newspapers. The AMC shall update the NAVs on the website of the Fund www.assetmanagement.hsbc.com/in and of the Association of Mutual Funds in India - AMFI (www.amfi india.com) by 9.00 p.m. on every Business Day. In case of any delay, the reasons for such delay would be explained to AMFI in writing. If the NAVs are not available before commencement of Business Hours on the following day due to any reason, the Fund shall issue a press release giving reasons and explaining when the Fund would be able to publish the NAVs. The NAV of the Scheme will be determined on every Business Day, except under special circumstances specifi ed in this Combined SID.

As presently required by the SEBI (MF) Regulations, the AMC will disclose the monthly portfolio of the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. Also a complete statement of the Scheme portfolio would be available on the Fund’s website, and published by the Mutual Fund as an advertisement in one English daily circulating in the whole of India and in a newspaper published in the language of the region where the head offi ce of the mutual fund is situated, within 1 month from the close of each half year (i.e. 31 March and 30 September) or mailed to the Unitholders.

Loads (including SIP / STP where applicable)

Entry Load and Exit Load: NIL

Minimum Application Amount(Lumpsum)

Rs. 10,000/- per application and in multiples of Re. 1/- thereafter

Minimum Additional Investment

Rs. 1,000/- per application and in multiples of Re. 1/- thereafter

Minimum no. of installments - 12 (monthly) or 4 (quarterly);

Minimum aggregate investment - Rs. 12,000.

Minimum Redemption Amount

Rs 1000/- and in multiples of Re. 1/- thereafter

Plan / Options Options : i) Growth ii) Dividend

A Direct Plan (with the above Options) is also available for investors who subscribe to Units directly with the Fund.

Plans and Options thereunder will have a common portfolio.

Sub Options i) Dividend Payout ii) Dividend Reinvestment

Dividend Declaration of dividend and its frequency will inter alia depend upon the distributable surplus. Dividend may be declared from time to time at the discretion of the Trustees.

Name of the Scheme HSBC DYNAMIC FUND (HDF) HSBC EMERGING MARKETS FUND (HEMF)

Type of Scheme An open-ended Scheme An open-ended Scheme

Investment Objective To provide long term capital appreciation by allocating funds in equity and equity related instruments. It also has the fl exibility to move, entirely if required, into debt instruments in times that the view on equity markets seems negative.

To provide long term capital appreciation by investing in India and in the emerging markets, in equity and equity related instruments, share classes and units/securities issued by overseas mutual funds or unit trusts. The fund may also invest a limited proportion in debt and money market instruments.

Liquidity Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to despatch redemption proceeds within 3 Business Days.

Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to despatch redemption proceeds within 7 Business Days.

Benchmark Index S&P BSE 200 MSCI Emerging Market Index

HSBC Mutual Fund 7

Name of the Scheme HSBC DYNAMIC FUND (HDF) HSBC EMERGING MARKETS FUND (HEMF)

Transparency / NAV Disclosure

The AMC will calculate and disclose the NAVs of the Scheme at the close of every Business Day. NAV of the Scheme/ Option(s) shall be made available at all Investor Service Centres of the AMC. The AMC shall have the NAV published in two daily newspapers. The AMC shall update the NAVs on the website of the Fund www.assetmanagement.hsbc.com/in and of the Association of Mutual Funds in India - AMFI (www.amfi india.com) by 9.00 p.m. on every Business Day. In case of any delay, the reasons for such delay would be explained to AMFI in writing. If the NAVs are not available before commencement of Business Hours on the following day due to any reason, the Fund shall issue a press release giving reasons and explaining when the Fund would be able to publish the NAVs. The NAV of the Scheme will be determined on every Business Day, except under special circumstances specifi ed in this Combined SID.

As presently required by the SEBI (MF) Regulations, the AMC will disclose the monthly portfolio of the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. Also a complete statement of the Scheme portfolio would be available on the Fund’s website, and published by the Mutual Fund as an advertisement in one English daily circulating in the whole of India and in a newspaper published in the language of the region where the head offi ce of the mutual fund is situated, within 1 month from the close of each half year (i.e. 31 March and 30 September) or mailed to the Unitholders.

The AMC will calculate and disclose the NAVs of the Scheme at the close of every Business Day. NAV of the Scheme / Option(s) shall be made available at all Investor Service Centres of the AMC. The AMC shall have the NAV published in two daily newspapers. The AMC shall update the NAVs on the website of the Fund www.assetmanagement.hsbc.com/in and of the Association of Mutual Funds in India - AMFI (www.amfi india.com) latest by 10.00 am on the next Business Day. In case of any delay, the reasons for such delay would be explained to AMFI in writing. If the NAVs are not available before commencement of Business Hours on the following day due to any reason, the Fund shall issue a press release giving reasons and explaining when the Fund would be able to publish the NAVs. The NAV of the Scheme will be determined on every Business Day, except under special circumstances specifi ed in this Combined SID.

As presently required by the SEBI (MF) Regulations, the AMC will disclose the monthly portfolio of the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. Also a complete statement of the Scheme portfolio would be available on the Fund’s website, and published by the Mutual Fund as an advertisement in one English daily circulating in the whole of India and in a newspaper published in the language of the region where the head offi ce of the mutual fund is situated, within 1 month from the close of each half year (i.e. 31 March and 30 September) or mailed to the Unitholders.

Loads (Including SIP / STP where applicable)

Entry Load and Exit Load: NIL

Minimum Application Amount(Lumpsum)

Rs. 10,000/- per application and in multiples of Re. 1/- thereafter

Minimum Additional Investment

Rs 1,000/- and in multiples of Re. 1/- thereafter

Minimum Application Amount (SIP)

Minimum Investment Amount - Rs. 1,000 (monthly) or Rs. 3,000 (quarterly);Minimum no. of installments - 12 (monthly) or 4 (quarterly);Minimum aggregate investment - Rs. 12,000.

Minimum Redemption Amount

Rs 1000/- and in multiples of Re. 1/- thereafter

Plan / Options Options : i) Growth ii) DividendA Direct Plan (with the above Options) is also available for investors who subscribe to Units directly with the Fund.Plans and Options thereunder will have a common portfolio.

Sub Options i) Dividend Payout ii) Dividend Reinvestment

Dividend Declaration of dividend and its frequency will inter alia depend upon the distributable surplus. Dividend may be declared from time to time at the discretion of the Trustees.

Name of the Scheme HSBC TAX SAVER EQUITY FUND (HTSF)HSBC DIVIDEND YIELD EQUITY

FUND (HDYEF)

Type of Scheme An open-ended Equity Linked Savings Scheme (ELSS) An open ended equity Scheme

Investment Objective To provide long term capital appreciation by investing in a diversifi ed portfolio of equity & equity related instruments of companies across various sectors and industries, with no capitalization bias. The Fund may also invest in fi xed income securities

The Scheme aims to generate dividend yield and capital appreciation by primarily investing into equities and equity related securities of domestic Indian companies.

8 Combined Scheme Information Document (SID)

Name of the Scheme HSBC TAX SAVER EQUITY FUND (HTSF)HSBC DIVIDEND YIELD EQUITY

FUND (HDYEF)

Liquidity Being an open ended Scheme, Units may be purchased or redeemed (after a lock in period of 3 years from the date of allotment) on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to despatch redemption proceeds within 3 Business Days. The Units purchased under the Scheme shall have a lock in period of three years from the date of allotment of Units. Accordingly, the Units can be redeemed (i.e. sold back to the Fund) on every Business Day, at the Applicable NAV (hereinafter defi ned), on expiry of lock in period of three years from the date of allotment. Redemption requests can be made for an amount of Rs. 500 or more. Subject to the lock in period stated above, Redemption could also be made for the total number of units standing to the credit of investor at the time of closure of account. It may, however, be noted that in the event of death of the Unitholder, the legal heir, subject to production of requisite documentary evidence, will be able to redeem the investment only after the completion of one year or anytime thereafter, from the date of allotment of Units to the deceased Unitholder.

Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to despatch redemption proceeds within 3 Business Days.

Benchmark Index S&P BSE 200 S&P BSE 200

Transparency / NAV Disclosure

The AMC will calculate and disclose the NAVs of the Scheme at the close of every Business Day. NAV of the Scheme / Option(s) shall be made available at all Investor Service Centres of the AMC. The AMC shall have the NAV published in two daily newspapers. The AMC shall update the NAVs on the website of the Fund www.assetmanagement.hsbc.com/in and of the Association of Mutual Funds in India - AMFI (www.amfi india.com) by 9.00 p.m. on every Business Day. In case of any delay, the reasons for such delay would be explained to AMFI in writing. If the NAVs are not available before commencement of Business Hours on the following day due to any reason, the Fund shall issue a press release giving reasons and explaining when the Fund would be able to publish the NAVs. The NAV of the Scheme will be determined on every Business Day, except under special circumstances specifi ed in this Combined SID.As presently required by the SEBI (MF) Regulations, the AMC will disclose the monthly portfolio of the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. Also a complete statement of the Scheme portfolio would be available on the Fund’s website, and published by the Mutual Fund as an advertisement in one English daily circulating in the whole of India and in a newspaper published in the language of the region where the head offi ce of the mutual fund is situated, within 1 month from the close of each half year (i.e. 31 March and 30 September) or mailed to the Unitholders.

Loads (Including SIP / STP where applicable)

Entry Load and Exit Load : NIL Entry Load and Exit Load: NIL

Minimum Application Amount (Lumpsum)

Rs. 500/- per application Rs. 10,000/- per application and in multiples of Re. 1/- thereafter

Minimum Additional Investment

Rs. 500/- per application and in multiples of Rs. 500/- thereafter

Rs. 1,000/- per application and in multiples of Re. 1/- thereafter

Minimum Application Amount (SIP)

Minimum Investment Amount - Rs. 500 (monthly) or Rs. 1500 (quarterly);Minimum no. of installments - 12 (monthly) or 4 (quarterly);Minimum aggregate investment - Rs. 6,000.Units allotted therein shall be locked-in for a period of three years, from the date of allotment.

Minimum Investment Amount - Rs. 1,000 (monthly) or Rs. 3000 (quarterly);Minimum no. of installments - 12 (monthly) or 4 (quarterly);Minimum aggregate investment - Rs. 12,000.

Minimum Redemption Amount

Rs 500/- and in multiples of Re. 1/- thereafter Rs 1,000/- and in multiples of Re. 1/- thereafter

Plan / Options Options : i) Growth ii) DividendA Direct Plan (with the above Options) is also available for investors who subscribe to Units directly with the Fund.Plans and Options thereunder will have a common portfolio.

Sub Options Dividend Payout i) Dividend Payout ii) Dividend Reinvestment

Dividend Declaration of dividend and its frequency will inter alia depend upon the distributable surplus. Dividend may be declared from time to time at the discretion of the Trustees.

Declaration of dividend and its frequency will inter alia depend upon the distributable surplus. Dividend may be declared from time to time at the discretion of the Trustees.

HSBC Mutual Fund 9

Name of the Scheme HSBC MONTHLY INCOME

PLAN

HSBC INCOME FUND

INVESTMENT PLAN (HIF-IP) SHORT TERM PLAN (HIF-ST)

Type of Scheme An open ended Fund. Monthly income is not assured and is subject to the availability of distributable surplus.

An open-ended income Scheme

Investment Objective To seek generation of reasonable returns through investments in debt and money market Instruments. The secondary objective of the Scheme is to invest in equity and equity related instruments to seek capital appreciation.

To provide a reasonable income through a diversifi ed portfolio of fi xed income securities. The AMC's view of interest rate trends and the nature of the Plans will be refl ected in the type and maturities of securities in which the Short Term and Investment Plans are invested.

Liquidity Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to despatch redemption proceeds within 1 Business Day.

Benchmark Index CRISIL MIP Blended Index CRISIL Composite Bond Fund Index

CRISIL Short Term Bond Fund Index

Transparency / NAV Disclosure

The AMC will calculate and disclose the NAVs of the Scheme at the close of every Business Day. NAV of the Scheme / Option(s) shall be made available at all Investor Service Centres of the AMC. The AMC shall have the NAV published in two daily newspapers. The AMC shall update the NAVs on the website of the Fund www.assetmanagement.hsbc.com/in and of the Association of Mutual Funds in India - AMFI (www.amfi india.com) by 9.00 p.m. on every Business Day. In case of any delay, the reasons for such delay would be explained to AMFI in writing. If the NAVs are not available before commencement of Business Hours on the following day due to any reason, the Fund shall issue a press release giving reasons and explaining when the Fund would be able to publish the NAVs. The NAV of the Scheme will be determined on every Business Day, except under special circumstances specifi ed in this Combined SID.As presently required by the SEBI (MF) Regulations, the AMC will disclose the monthly portfolio of the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. Also a complete statement of the Scheme portfolio would be available on the Fund's website, and published by the Mutual Fund as an advertisement in one English daily circulating in the whole of India and in a newspaper published in the language of the region where the head offi ce of the mutual fund is situated, within 1 month from the close of each half year (i.e. 31 March and 30 September) or mailed to the Unitholders.

Loads (Including SIP / STP where applicable)

Entry Load and Exit Load: Nil Entry Load and Exit Load: Nil Entry Load and Exit Load: Nil

Minimum Application Amount (Lumpsum)

Growth Option : Rs. 10,000/- per application and in multiples of Re. 1/- thereafter.

Dividend Options :Monthly Dividend Option : Rs. 25,000/- per application and in multiples of Re. 1/- thereafter.

Quarterly Dividend Option : Rs. 10,000/- per application and in multiples of Re. 1/- thereafter.

Rs. 10,000/- per application and in multiples of Re. 1/- thereafter

Minimum Additional Investment

Rs. 1,000/- per application & in multiples of Re. 1/- thereafter

Rs. 1,000/- per application & in multiples of Re. 1/- thereafter

Minimum Application Amount (SIP)

Minimum Investment Amount - Rs. 1,000/- (monthly) or Rs. 3,000/- (quarterly);Minimum no. of installments - 12 (monthly) or 4 (quarterly);Minimum aggregate investment - Rs. 12,000.

Minimum Redemption Amount

Rs. 1,000 & in multiples of Re. 1/- thereafter

Plan / Options Options: i) Growth ii) DividendA Direct Plan is also available (with the above Options) for investors who subscribe to Units directly with the Fund. Plans and Options thereunder will have a common portfolio.

Options : i) Growth ii) DividendA Direct Plan (with the above Options) is also available for investors who subscribe to Units directly with the Fund. Plans and Options thereunder will have a common portfolio.

10 Combined Scheme Information Document (SID)

Name of the Scheme HSBC MONTHLY INCOME

PLAN

HSBC INCOME FUND

INVESTMENT PLAN (HIF-IP) SHORT TERM PLAN (HIF-ST)

Sub Options i) Monthly Dividend (Payout and Reinvestment)

Dividend Monthly, Quarterly or at such intervals as may be decided by the Trustees. An investor in Monthly, Quarterly Dividend can opt for payout / reinvestment.Declaration of dividend and its frequency will inter alia depend upon the distributable surplus.

Quarterly or at such intervals as may be decided by the Trustees. An investor in Quarterly Dividend can opt for payout / reinvestment.Declaration of dividend and its frequency will inter alia depend upon the distributable surplus.

Weekly, Monthly and Quarterly or at such intervals as may be decided by the Trustees. Weekly dividend will be reinvested whereas an investor in Monthly and Quarterly Dividend can opt for payout / reinvestment.Declaration of dividend and its frequency will inter alia depend upon the distributable surplus.

Name of the Scheme HSBC ULTRA SHORT TERM

BOND FUND (HUSBF)

HSBC CASH FUND (HCF)

Type of Scheme An open ended debt Scheme An open ended liquid Scheme

Investment Objective Seeks to provide liquidity and reasonable returns by investing primarily in a mix of short term debt and money market instruments.

Aims to provide reasonable returns, commensurate with low risk while providing a high level of liquidity, through a portfolio of money market and debt securities. However, there can be no assurance that the Scheme’s objective can be realized.

Liquidity Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to despatch redemption proceeds within 1 Business Day.

Benchmark Index CRISIL Liquid Fund Index - 90%CRISIL Short Term Bond Fund Index - 10%

CRISIL Liquid Fund Index

Transparency / NAV Disclosure

The AMC will calculate and disclose the NAVs of the Scheme at the close of every Business Day. NAV of the Scheme / Option(s) shall be made available at all Investor Service Centres of the AMC. The AMC shall have the NAV published in two daily newspapers. The AMC shall update the NAVs on the website of the Fund www.assetmanagement.hsbc.com/in and of the Association of Mutual Funds in India - AMFI (www.amfi india.com) by 9.00 p.m. on every Business Day. In case of any delay, the reasons for such delay would be explained to AMFI in writing. If the NAVs are not available before commencement of Business Hours on the following day due to any reason, the Fund shall issue a press release giving reasons and explaining when the Fund would be able to publish the NAVs. The NAV of the Scheme will be determined on every Business Day, except under special circumstances specifi ed in this Combined SID.As presently required by the SEBI (MF) Regulations, the AMC will disclose the monthly portfolio of the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. Also a complete statement of the Scheme portfolio would be available on the Fund’s website, and published by the Mutual Fund as an advertisement in one English daily circulating in the whole of India and in a newspaper published in the language of the region where the head offi ce of the mutual fund is situated, within 1 month from the close of each half year (i.e. 31 March and 30 September) or mailed to the Unitholders.

Loads (Including SIP / STP where applicable)

Entry Load and Exit Load - NIL Entry Load and Exit Load: Nil

Minimum Application Amount (lumpsum)

Rs. 10,000/- per application & in multiples of Re. 1/- thereafter

Minimum Application Amount (SIP)

Rs. 1,000/- (monthly) or Rs. 3,000/- (quarterly);Minimum no. of installments - 12 (monthly)or 4 (quarterly);

Minimum Investment Amount - Rs. 2,00,000 (daily), Rs. 1000/- (monthly) or Rs. 3,000/- (quarterly);Minimum no. of installments - 20 (daily), 12 (monthly) or 4 (quarterly);

Minimum Additional Investment

Rs 1,000/- per application & in multiples of Re. 1/- thereafter

Minimum Redemption Amount

Rs 1,000/- & in multiples of Re. 1/- thereafter

Plan / Options Options : i) Growth and ii) DividendA Direct Plan (with the above Options) is also available for investors who subscribe to Units directly with the Fund.Plans and Options thereunder will have a common portfolio.

Dividend Daily, Weekly, & Monthly Dividend or at such intervals as may be decided by the Trustees. Declaration of dividend and its frequency will inter alia depend upon the distributable surplus.

Daily, Weekly, & Monthly Dividend or at such intervals as may be decided by the Trustees. Declaration of dividend and its frequency will inter alia depend upon the distributable surplus.

Name of the Scheme HSBC FLEXI DEBT FUND (HFDF)HSBC ASIA PACIFIC (EX JAPAN)

DIVIDEND YIELD FUND (HAPDF)

Type of Scheme An open-ended debt Scheme An open ended fund of funds Scheme

Investment Objective To deliver returns in the form of interest income and capital gains, along with high liquidity, commensurate with the current view on the markets and the interest rate cycle, through active investment in debt and money market instruments.

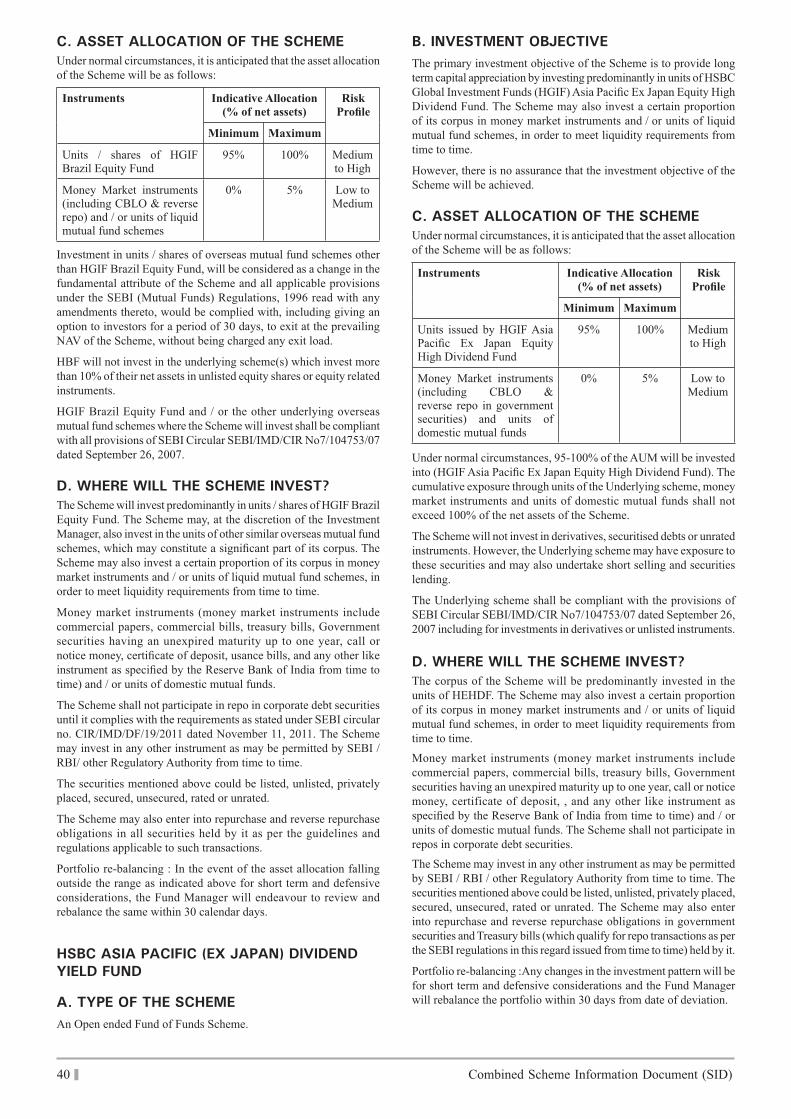

To provide long term capital appreciation by investing predominantly in units of HSBC Global Investment Funds (HGIF) Asia Pacifi c Ex Japan Equity High Dividend Fund (HEHDF). The Scheme may also invest a certain proportion of its corpus in money market instruments and / or units of liquid mutual fund schemes, in order to meet liquidity requirements from time to time. However, there is no assurance that the investment objective of the Scheme will be achieved.

Liquidity Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to despatch redemption proceeds within 1 Business Day.

Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, despatch redemption proceeds within 10 Business Days from date of acceptance of redemption request, while it will endeavour to dispatch the same within 7 business days.

Benchmark Index CRISIL Composite Bond Fund Index MSCI AC Asia Pacifi c ex-Japan The Fund reserves the right to change the benchmark for evaluation of the performance of the Scheme from time to time, subject to SEBI Regulations and other prevailing guidelines, if any.

Transparency / NAV Disclosure

The AMC will calculate and disclose the NAVs of the Scheme at the close of every Business Day. NAV of the Scheme / Option(s) shall be made available at all Investor Service Centres of the AMC. The AMC shall have the NAV published in two daily newspapers. The AMC shall update the NAVs on the website of the Fund www.assetmanagement.hsbc.com/in and of the Association of Mutual Funds in India - AMFI (www.amfi india.com) by 9.00 p.m. on every Business Day. In case of any delay, the reasons for such delay would be explained to AMFI in writing. If the NAVs are not available before commencement of Business Hours on the following day due to any reason, the Fund shall issue a press release giving reasons and explaining when the Fund would be able to publish the NAVs. The NAV of the Scheme will be determined on every Business Day, except under special circumstances specifi ed in this Combined SID. As presently required by the SEBI (MF) Regulations, the AMC will disclose the monthly portfolio of the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. Also a complete statement of the Scheme portfolio would be available on the Fund’s website, and published by the Mutual Fund as an advertisement in one English daily circulating in the whole of India and in a newspaper published in the language of the region where the head offi ce of the mutual fund is situated, within 1 month from the close of each half year (i.e. 31 March and 30 September) or mailed to the Unitholders.

Loads (Including SIP /STP where applicable)

Entry Load and Exit Load: Nil

Minimum Application Amount (Lumpsum)

Rs 10,000/- per application & in multiples of Re. 1/- thereafter

Minimum Application Amount (SIP)

Minimum Investment Amount - Rs. 1,000/- (monthly) or Rs. 3,000/- (quarterly);Minimum no. of installments - 12 (monthly) or 4 (quarterly);Minimum aggregate investment - Rs. 12,000.

Minimum additional investment

Rs 1,000/- per application & in multiples of Re. 1/- thereafter

Minimum Redemption Amount

Rs 1,000 & in multiples of Re. 1/- thereafter

Plan / Options Options: i) Growth ii) DividendA Direct Plan (with the above Options) is also available for investors who subscribe to Units directly with the Fund.Plans and Options thereunder will have a common portfolio.

12 Combined Scheme Information Document (SID)

Name of the Scheme HSBC FLEXI DEBT FUND (HFDF)HSBC ASIA PACIFIC (EX JAPAN)

DIVIDEND YIELD FUND (HAPDF)

Sub Options i) Fortnightly Dividend (Reinvestment)ii) Monthly (Payout & Reinvestment)iii) Quarterly (Payout & Reinvestment)iv) Half Yearly Dividend (Payout & Reinvestment)Fortnightly Dividend will be reinvested whereas investors in Monthly, Quarterly & Half Yearly Dividend can opt for Payout / Reinvestment.

i) Dividend Payoutii) Dividend Reinvestment

Dividend Fortnightly, Monthly, Quarterly & Half Yearly Dividend or at such intervals as may be decided by the Trustees.Declaration of dividend and its frequency will inter alia depend upon the distributable surplus.

Declaration of dividend and its frequency will inter alia depend upon the distributable surplus. Dividend may be declared from time to time at the discretion of the Trustees.

Name of the Scheme HSBC BRAZIL FUND (HBF)

HSBC GLOBAL CONSUMER OPPORTUNITIES FUND (HGCOF) –

Benefi ting from China’s Growing Consumption Power

Type of Scheme An open ended fund of funds Scheme An open ended Fund of Funds scheme

Investment Objective To provide long term capital appreciation by investing predominantly in units / shares of HSBC Global Investment Funds (HGIF) - Brazil Equity Fund. The Scheme may, at the discretion of the Investment Manager, also invest in the units of other similar overseas mutual fund schemes, which may constitute a signifi cant part of its corpus. The Scheme may also invest a certain proportion of its corpus in money market instruments and / or units of liquid mutual fund schemes, in order to meet liquidity requirements from time to time.

To provide long term capital appreciation by investing predominantly in units of HSBC Global Investment Funds (HGIF) China Consumer Opportunities Fund (Underlying scheme). The Scheme may also invest a certain proportion of its corpus in money market instruments and / or units of liquid mutual fund schemes, in order to meet liquidity requirements from time to time.

Liquidity Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will, under normal circumstances, endeavour to dispatch redemption proceeds within 7 Business Days.

Being an open ended Scheme, Units may be purchased or redeemed on every Business Day at NAV based prices, subject to provisions of exit load, if any. The Fund will dispatch redemption proceeds within 10 Business Days.

Benchmark Index MSCI Brazil 10/40 Index MSCI AC World Index

Transparency / NAV Disclosure

The AMC will calculate and disclose the NAVs of the Scheme at the close of every Business Day. NAV of the Scheme / Option(s) shall be made available at all Investor Service Centres of the AMC. The AMC shall have the NAV published in two daily newspapers. The AMC shall update the NAVs on the website of the Fund www.assetmanagement.hsbc.com/in and of the Association of Mutual Funds in India - AMFI (www.amfi india.com) latest by 10.00 a.m. on the next Business Day. In case of any delay, the reasons for such delay would be explained to AMFI in writing. If the NAVs are not available before commencement of Business Hours on the following day due to any reason, the Fund shall issue a press release giving reasons and explaining when the Fund would be able to publish the NAVs. The NAV of the Scheme will be determined on every Business Day, except under special circumstances specifi ed in this SID.As presently required by the SEBI (MF) Regulations, the AMC will disclose the monthly portfolio of the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. Also a complete statement of the Scheme portfolio would be published by the Fund as an advertisement in one English daily circulating in the whole of India and in a newspaper published in the language of the region where the Head Offi ce of the Fund is situated, within 1 month from the close of each half year (i.e. 31 March and 30 September) or mailed to the Unitholders.

The AMC will calculate and disclose the NAV at the close of every Business Day except in special circumstances described under ‘Suspension of Sale and Redemption of Units’ in the Statement of Additional Information (SAI). The NAVs will be released for publication in at least two daily newspapers having circulation all over India and updated on AMC’s website at www.assetmanagement.hsbc.com/in and on AMFI website at www.amfi india.com. The NAV of the Plans under the Scheme shall be made available at all Investor Service Centres of the AMC. The AMC will disclose the monthly portfolio (alongwith ISIN) of the each Plan under the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. The AMC shall disclose/publish the full portfolio of the Scheme on a half-yearly basis as per the SEBI Regulations. The AMC will issue an advertisement disclosing hosting of un-audited fi nancial results of the Plans under the Scheme on its website on a half yearly basis and shall disclose the annual results of the Plans under the Scheme on its website as per the SEBI Regulations.

Loads (Including SIP /STP where applicable)

Entry Load and Exit Load: Nil

HSBC Mutual Fund 13

Name of the Scheme HSBC BRAZIL FUND (HBF)

HSBC GLOBAL CONSUMER OPPORTUNITIES FUND (HGCOF) –

Benefi ting from China’s Growing Consumption Power

Minimum Application Amount (Lumpsum)

Rs 10,000/- per application & in multiples of Re. 1/- thereafter

Rs. 5,000/- per application & in multiples of Re. 1/- thereafter. Minimum application amount is applicable for switch-ins as well.

Minimum Application Amount (SIP)

Minimum Investment Amount - Rs. 1,000/- (monthly) or Rs. 3,000/- (quarterly);Minimum no. of installments - 12 (monthly) or 4 (quarterly);Minimum aggregate investment - Rs. 12,000.

Minimum additional investment

Rs 1,000/- per application & in multiples of Re. 1/- thereafter

Minimum Redemption Amount

Rs 1,000 & in multiples of Re. 1/- thereafter, or 100 units

A Direct Plan (with the above Options) is also available for investors who subscribe to Units directly with the Fund.Plans and Options thereunder will have a common portfolio.

Sub Options i) Dividend Payoutii) Dividend Reinvestment

–

Name of the Scheme: HSBC MANAGED SOLUTIONS

Name of the Plan Managed Solutions India – Growth Managed Solutions India – Moderate Managed Solutions India – Conservative

Type of Scheme An open-ended fund of funds Scheme

An open ended fund of funds scheme An open ended fund of funds Scheme

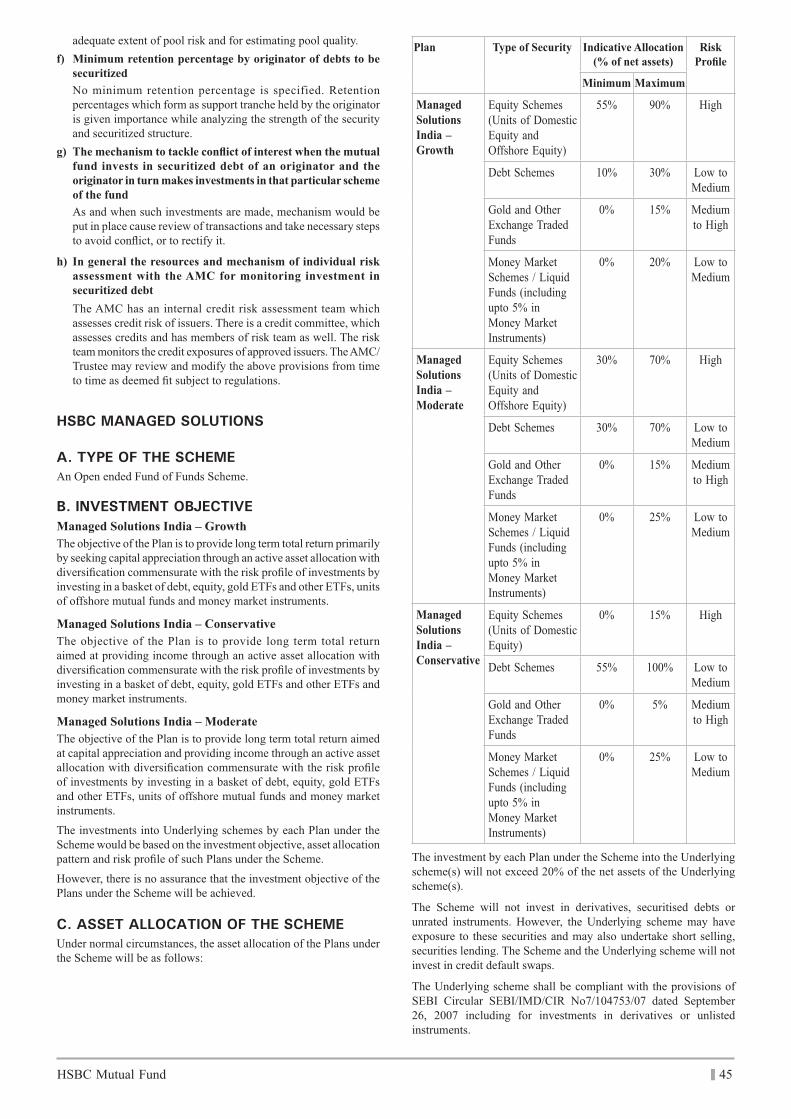

Investment Objective The objective of the Plan is to provide long term total return primarily by seeking capital appreciation through an active asset allocation with diversifi cation commensurate with the risk profi le of investments by investing in a basket of debt, equity, gold exchange traded funds (ETFs) and other ETFs, units of offshore mutual funds and money market instruments.

The objective of the fund is to provide long term total return aimed at capital appreciation and providing income through an active asset allocation with diversifi cation commensurate with the risk profi le of investments by investing in a basket of debt, equity, gold ETFs and other ETFs, units of offshore mutual funds and money market instruments.

The objective of the Plan is to provide long term total return aimed at providing income through an active asset allocation with diversifi cation commensurate with the risk profi le of investments by investing in a basket of debt, equity, gold ETFs and other ETFs and money market instruments.

The investments into Underlying schemes by each Plan under the Scheme would be based on the investment objective, asset allocation pattern and / risk profi le of such Plans under the Scheme. However, there is no assurance that the investment objective of the Plans under the Scheme will be achieved.

Liquidity The Plans under the Scheme will offer for purchase / switch-in and redemption / switch-out of units at NAV based prices on every Business Day on an ongoing basis. Under normal circumstances, the Mutual Fund shall dispatch the redemption proceeds within 10 business days from the date of acceptance of the redemption request.

Benchmark Index Composite Index constituting 80% of BSE 200 Index and 20% of CRISIL Composite Bond Index

CRISIL Balanced Fund Index Composite Index constituting of 90% into CRISIL Composite Bond Index and 10% of BSE 200 Index

The Fund reserves the right to change the benchmark for evaluation of the performance of the Plans under the Scheme from time to time, subject to SEBI Regulations and other prevailing guidelines if any.

Transparency / NAV Disclosure

The AMC will calculate and disclose the NAV at the close of every Business Day except in special circumstances described under ‘Suspension of Sale and Redemption of Units’ in the Statement of Additional Information (SAI). The NAVs will be released for publication in at least two daily newspapers having circulation all over India and updated on AMC’s website at www.assetmanagement.hsbc.com/in and on AMFI website at www.amfi india.com. The NAV of the Plans under the Scheme shall be made available at all Investor Service Centres of the AMC. The AMC will disclose the monthly portfolio (alongwith ISIN) of the each Plan under the Scheme as on the last day of the month on its website on or before the tenth day of the succeeding month. The AMC shall disclose / publish the full portfolio of the Scheme on a half-yearly basis as per the SEBI Regulations. The AMC will issue an advertisement disclosing hosting of un-audited fi nancial results of the Plans under the Scheme on its website on a half yearly basis and shall disclose the annual results of the Plans under the Scheme on its website as per the SEBI Regulations.

14 Combined Scheme Information Document (SID)

Name of the Scheme: HSBC MANAGED SOLUTIONS

Name of the Plan Managed Solutions India – Growth Managed Solutions India – Moderate Managed Solutions India – Conservative

Loads (Including SIP / STP where applicable)

Entry Load and Exit Load: Nil

Minimum Application Amount (Lumpsum)

Rs. 5,000 per application & in multiples of Re. 1/- thereafter. Minimum application amount is applicable for switch-ins as well.

Minimum Application Amount (SIP)

Minimum Investment Amount – Rs. 1000 (monthly) or Rs. 3000 (quarterly);Minimum no. of installments – 12 (monthly) or 4 (quarterly);Minimum aggregate investment – Rs. 12,000.

Minimum additional investment

Rs 1,000 per application & in multiples of Re. 1/- thereafter

Minimum Redemption Amount

Rs 1,000 & in multiples of Re. 1/- thereafter, or 100 units

Plan / Options Options: i) Growth ii) Dividend Each of the Plans will also offer a Direct Plan (with the above Options) for investment applications which are not routed through a distributor. All the Scheme features of the Direct Plan will be the same as Regular Plan except for a lower expense ratio as detailed in Section IV: Fees and Expenses - B. Annual Scheme Recurring Expenses. Brokerage / Commission paid to distributors and distribution expenses will not be charged under the Direct Plan. Both the Regular and Direct Plans alongwith the Options thereunder will have a common portfolio.

Sub Options i) Dividend Payout and ii) Dividend Reinvestment

Dividend Declaration of dividend and its frequency will inter alia depend upon the distributable surplus. Dividend may be declared from time to time at the discretion of the Trustees.

Notes:1) Entry / Exit Load: In terms of SEBI circular no. SEBI/IMD/CIR No.4/ 168230/09 dated June 30, 2009, no entry load will be charged by the

schemes to investors effective August 1, 2009. Upfront commission shall be paid directly by the investor to the AMFI registered Distributors based on the investor’s assessment of various factors including the service rendered by the distributors. No exit load (if any) will be charged for units allotted under bonus / dividend reinvestment option.

2) Pursuant to SEBI circular no. CIR/IMD/DF/21/2012 dated September 13, 2012 and Gazette Notifi cation dated September 26, 2012, in order to comply with the single plan structure amongst all the Schemes, it has been decided to discontinue acceptance of fresh purchases / additional purchases /switch-ins under Regular & Institutional Plan of HCF, Regular & Institutional Plus Plan under HUSTBF, Regular Plan under HFDF, Institutional & Institutional Plus Plan under HIF - STP & Institutional Plan under HIF - IP effective from October 1, 2012. All the discontinued Plans will continue to exist till the existing investors remain invested in the Plan(s). Only redemptions and switch-outs will be permitted in the discontinued Plans. Any additional investments or switch-in requests received in the name of the discontinued Plans will be processed under the available single Plan.

3) HSBC Small Cap Fund has merged with HSBC Midcap Equity Fund & ceased to exist with effect from April 26, 2014. Kindly refer Notice dated March 14, 2014 on www.assetmanagement.hsbc.com/in for details on the merger. Hence, details of HSBC Small Cap Fund are not a part of this document.

4) HSBC Unique Opportunities Fund has been repositioned as HSBC Dividend Yield Equity Fund with effect from July 18, 2014. Kindly refer to Notice dated May 26, 2014 available on “http://www.assetmanagement.hsbc.com/in”

5) HSBC Progressive Themes Fund has been repositioned as HSBC Infrastructure Equity Fund with effect from October 14, 2015. Kindly refer to Notice-cum-Addendum dated August 6, 2015 and Corrigendum to Notice-cum-Addendum dated September 7, 2015 available on “http://www.assetmanagement.hsbc.com/in”

6) In accordance with SEBI circular dated February 25, 2016, HSBC Cash Fund has four separate plans for the limited purpose of deploying the unclaimed redemption and dividend amounts into this scheme. These plans are not available for regular investments / switches by investors. The investment objective, asset allocation pattern, investment strategy, risk factors and portfolio of these Plans will be same as other existing plans of HSBC Cash Fund. These plans will only have a growth option. Further, the Total Expense Ratio of these four plans will be capped at 50 bps and there will be no exit load charged, as required under the aforesaid circular. The list of names and address of Unitholders in whose folios there are unclaimed amounts along with the process of claiming such unclaimed amounts are available on our website http://www.assetmanagement.hsbc.com/in.

7) In accordance with SEBI circular no. Cir/ IMD/ DF/ 15 /2014 dated June 20, 2014 regarding minimum assets under management, HSBC Gilt Fund has been wound up with effect from December 1, 2015.

8) HSBC Floating Rate Fund - Long Term Plan has been merged with HSBC Ultra Short Term Bond Fund effective from May 25, 2016. Please refer to the Notice published on April 18, 2016 available on www.assetmanagement.hsbc.com/in for more details.

9) HSBC MIP - Regular Plan has been merged with HSBC MIP - Savings Plan (renamed as HSBC Monthly Income Plan) effective from October 8, 2016. Please refer to the Notice published on August 29, 2016 available on www.assetmanagement.hsbc.com/in for more details.

HSBC Mutual Fund 15

A. RISK FACTORS

Standard Risk Factors: � Mutual funds and securities investments are subject to market

risks and there is no assurance or guarantee that the objectives of the Scheme(s) will be achieved.

� Investment in Mutual Fund Units involves investment risks such as trading volumes, settlement risk, liquidity risk, default risk including the possible loss of principal

� As the price / value / interest rates of the securities in which the Scheme(s) invests fl uctuates, the value of your investment in the Schemes may go up or down depending on the various factors and forces affecting the capital markets and money markets.

� Past performance of the Sponsor / AMC / Mutual Fund does not guarantee future performance of the Schemes.

� HEF, HIOF, HMEF, HIEF, HMIP, HIF, HUSBF, HCF, HTSF, HDYEF, HDF, HFDF, HEMF, HBF, HAPDF, HGCOF and HMS are the name(s) of the Scheme(s) and do not in any manner indicate either the quality of the Scheme(s) or their future prospects and returns.

� The Sponsor is not responsible or liable for any loss resulting from the operation of the Scheme(s) beyond the initial contribution of Rs. 1,00,000/- (Rupees One Lakh only) made by it towards setting up the Fund. The associates of the Sponsor are not responsible or liable for any loss or shortfall resulting from the operation of the Scheme(s).

� The present Scheme(s) are not guaranteed or assured return scheme(s).

� Mutual funds being vehicles of securities investments are subject to market and other risks and there can be no guarantee against loss resulting from investing in the Scheme(s). The various factors which impact the value of the Schemes’ investments include, but are not limited to, fl uctuations in the bond markets, fl uctuations in interest rates, prevailing political and economic environment, changes in government policy, factors specifi c to the issuer of the securities, tax laws, liquidity of the underlying instruments, settlement periods, trading volumes etc.

� Investment decisions made by the AMC may not always be profi table.

Scheme Specifi c Risk Factors

Risk factors associated with investing in Equity or

Equity related Securities (applicable in case of HEF,

HIOF, HMEF, HIEF, HMIP, HDF, HTSF, HDYEF and

HEMF):

� Subject to the stated investment objective of the Scheme(s), the Scheme(s) propose to invest in equity and equity related securities. Equity instruments by nature are volatile and prone to price fl uctuations on a daily basis due to both macro and micro factors. Trading volumes, settlement periods and transfer procedures may restrict the liquidity of these investments. Different segments of fi nancial markets have different settlement periods and such periods may be extended signifi cantly by unforeseen circumstances. The inability of the Scheme(s) to make intended securities’ purchases due to settlement problems could cause the Scheme(s) to miss certain investment opportunities. In the view of the Fund Manager, investing in Mid and Small Cap stocks are riskier than investing in Large Cap Stocks.

� To the extent the assets of the Scheme are invested in overseas fi nancial assets, there may be risks associated with currency movements, restrictions on repatriation and transaction procedures in overseas market. Further, the repatriation of capital to India may also be hampered by changes in regulations or political circumstances as well as the application to it of other restrictions on investment. In addition, country risks would include events such as introduction of extraordinary exchange controls, economic

deterioration, bi-lateral confl ict leading to immobilization of the overseas fi nancial assets and the prevalent tax laws of the respective jurisdiction for execution of trades or otherwise.

� As the Fund will invest in securities which are denominated in foreign currencies (e.g. US Dollars), fl uctuations in the exchange rates of these foreign currencies may have an impact on the income and value of the fund. The investment manager in India may hedge the currency risk based on his view on the forex markets.

� As the portfolio will invest in stocks of different countries, the portfolio shall be exposed to the political, economic and social risks with respect to each country. However, the investment manager shall ensure that his exposure to each country is limited so that the portfolio is not exposed to one country. Investments in various economies will also diversify and reduce this risk.

� The fund will be exposed to settlement risk, as different countries have different settlement periods

� The Scheme(s) may also use various derivative products from time to time, as would be available and permitted by SEBI, in an attempt to protect the value of the portfolio and enhance Unitholders’ interest.

Risk factors applicable to HDYEF

Though the investments would be in companies having a track record of dividend payments, the performance of the Scheme would interalia depend on the ability of these companies to sustain dividends in future. Such stocks may be less liquid in terms of trading volumes in the stock markets and commensurately the liquidity risk could be higher. There could be time periods when securities of this nature may underperform relative to other stocks in the market. This could impact performance. The Scheme retains the fl exibility to hold from time to time relatively more concentrated investments in a few sectors as compared to plain diversifi ed equity funds. This may make the Scheme vulnerable to factors that may affect these sectors in specifi c and may be subject to a greater level of market risk leading to increased volatility in the Scheme’s NAV.

Risk factors applicable to HMEF

� Medium capitalisation stocks have the potential to experience greater volatility and may be less liquid than larger capitalisation stocks. Thus, relative to larger, more liquid stocks, investing in medium capitalization stocks, involves potentially greater volatility and risk. The biggest risk of equity investing is that returns can fl uctuate and investors can lose money.

� The Scheme seeks to generate returns by investing in stocks of Medium Cap Companies that have strong or improving fundamentals, high growth potential or are under-priced relative to their intrinsic value. This may or may not happen. However, as with all equity investing, there is the risk that a company will not achieve its expected earnings results, or that an unexpected change in the market or within the company will occur, both of which may adversely affect investment results.

Risk factors applicable to HBF

� The Scheme will be investing predominantly in units / shares of HGIF Brazil Equity Fund. Hence HBF’s performance may depend upon the performance of this underlying scheme. Any change in the investment policy or the fundamental attributes of the underlying scheme will affect the performance of HBF.

� Investments in HGIF Brazil Equity Fund, which is an equity fund, will have all the risks associated with investments in equity and the offshore markets.

� If HGIF Brazil Equity Fund declares any day as a non-business day, AMC will also declare that day as a non business day. However, if this information is received by the AMC from underlying scheme later in the day and HBF has already accepted transactions, such transactions will be processed on the next business day.

SECTION I - INTRODUCTION

16 Combined Scheme Information Document (SID)

� The portfolio disclosure of HBF will be largely limited to the investments made by the Scheme.

� Currency Risk: As the underlying scheme will invest in securities which are denominated in foreign currencies (e.g. US Dollars), fl uctuations in the exchange rates of these foreign currencies may have an impact on the income and value of the Scheme. The assets in which the underlying scheme is invested and the income from the assets will or may be quoted in currencies which are different from the underlying scheme’s base currency. The performance of the underlying scheme will therefore be affected by movements in the exchange rate between the currencies in which the assets are held and the underlying scheme’s base currency and hence there can be the prospect of additional loss or the prospect of additional gain to the investors greater than the usual risks of investment. The performance of the underlying scheme may also be affected by changes in exchange control regulations.

� Country Risk: As the portfolio will invest primarily in a well diversifi ed portfolio of investments in equity and equity equivalent securities of companies which have their registered offi ce in, and with an offi cial listing on a major stock exchange or other regulated Market of Brazil, as well as those companies which carry out a preponderant part of their business activities in Brazil, the portfolio shall be exposed to the political, economic and social risks with respect to Brazil.

� Hedging Risk : The investment manager to the underlying scheme is permitted, but not obliged, to use hedging techniques to attempt to offset market and currency risks. There is no guarantee that hedging techniques will achieve the desired result.

� Liquidity Risk: : Investors should be aware that the investments of the underlying scheme being primarily in the Brazilian market, its stocks may be negatively impacted by low liquidity, poor transparency and greater fi nancial risks. Investments in products relating to Brazilian market may also become illiquid which may constrain the ability of the investment manager to the underlying scheme to realize some or all of the portfolio. Securities, which are not quoted on the stock exchanges, are inherently illiquid in nature and carry a larger amount of liquidity risk, in comparison to securities that are listed on the exchanges.

� Settlement Risks: HBF will be exposed to settlement risk, as Brazil may have different settlement periods and the procedures may be different.

� Sector Concentration Risk: The portfolio may have a high concentration in natural resources sector. Because these investments are limited to narrow segment of the economy, the performance of HBF could be sensitive to movements in these sectors.

� Stock Risk: The underlying scheme is exposed to equity markets for all or part of its total assets. The value of these assets can therefore rise or fall and investors may not get back all of their investment.

� Emerging Market Risk: Brazil, being an emerging market, investors are advised to consider carefully the special risks of investing in emerging market securities. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Brokerage commissions, custodial services and other costs relating to investment in Emerging Markets generally are more expensive than those relating to investment in more developed markets. The risk also exists that an emergency situation may as a result of which trading of securities may cease or may be substantially curtailed and prices for a sub-fund’s securities in such markets may not be readily available.

� Swing Pricing Risk: There are trading and associated transaction costs involved when there are signifi cant infl ows into or signifi cant outfl ows from the underlying scheme. The dealing charges incurred as a result of such signifi cant fl ows fall not

only on those investors who have just transacted but on all the investors in the underlying scheme thereby diluting the value of their existing shareholders’ holding. Introduction of Swing Pricing aims to protect the interest of the existing investors from some of the performance dilution that they may suffer as a result of signifi cant infl ows and outfl ows from the underlying scheme. It is a process whereby the NAV of the underlying scheme is swung or adjusted when a predetermined net capital activity threshold (or swing threshold) is exceeded. Thus, if Net subscriptions (Total subscriptions - Total redemptions) are above the swing threshold, the NAV per share is swung up by the swing factor. Conversely, if Net redemptions (Total redemptions - Total subscriptions) are above the swing threshold, the NAV per share is swung down by the swing factor. The swing threshold has been set at a level by the underlying scheme which it believes best manages the objective of protecting their existing shareholders from NAV dilution by capturing a signifi cant percentage of the gross amount of deals on any fund whilst maintaining a reasonable level of fund volatility by not swinging the NAV all the time.

Adjusted NAV Calculation: Subscription Example -

� Using the following swing pricing criteria: � The swinging threshold is 0.5% of the underlying scheme’s

Net Assets � The swing factor on the offer (net subscriptions above the

threshold) is 1.0% � The swing factor on the bid (net redemptions below the

threshold) is 0.5% � Assume the following fund data :

Total net assets (US$)

Net subscriptions (US$)

No. of shares

US$ 100,000,000 US$ 600,000 1,000,000

� Net subscriptions = US$600,000 � The swinging threshold = Total Net Assets x 0.5% =

US$100,000,000 x 0.5% = US$500,000 � As the net infl ows exceed the swinging threshold, the NAV per

share has to be adjusted � Unadjusted NAV per share = Total Net Assets / No. of shares =

US$100,000,000/1,000,000 = US$100.00 � Adjusted NAV per share = NAV per share x (1 + swing factor) =

US$100.00 x (1+ 0.01) = US$101.00 � The NAV is adjusted upwards as net subscriptions have exceeded

the swinging threshold. � Therefore, all investors (including the local Scheme) redeeming

or subscribing into the underlying scheme will deal at the adjusted price of US$101.00 per share. Thus, investors of the underlying scheme (including the local scheme) may be positively or negatively impacted by application of the swing price factor by the underlying scheme, depending upon whether they are subscribing / redeeming on the date of application of swing price factor.

Risk factors applicable to HEMF

� The Scheme will be investing predominantly in units / shares of HSBC Global Investment Funds (HGIF) - Global Emerging Markets Equity Fund (HSBC GEM Fund). Hence HEMF’s performance may depend upon the performance of this underlying scheme. Any change in the investment policy or the fundamental attributes of the underlying scheme will affect the performance of HEMF.

� If HSBC GEM Fund declares any day as a non-business day, AMC will also declare that day as a non business day. However, if this information is received by the AMC from underlying scheme later in the day and HEMF has already accepted transactions, such transactions will be processed on the next business day.

HSBC Mutual Fund 17

� As the underlying scheme will invest in emerging markets, investors are advised to consider carefully the special risks of investing in emerging market securities. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Brokerage commissions, custodial services and other costs relating to investment in Emerging Markets generally are more expensive than those relating to investment in more developed markets. The risk also exists that an emergency situation may arise as a result of which trading of securities may cease or may be substantially curtailed and prices for the underlying scheme’s securities in such markets may not be readily available.

� Swing Pricing Risk: HEMF, HAPDF and Underlying schemes of HMS, being overseas investing schemes, are also exposed to ‘Swing Pricing Risk’ as stated above under section on ‘Risk factors applicable to HBF’.

Risk factors applicable to HAPDF & HGCOF

� Investments in the Underlying scheme, which also consist of equity funds, will have all the risks associated with investments in equity and the offshore markets.

� The portfolio disclosure of the Scheme will be largely limited to the investments made by the Scheme.