24

© 2017 Linh Vo COMM 294 FINAL REVIEW SESSION –ANSWER KEY BY LINH VO

| Date post: | 19-May-2018 |

| Category: |

Documents |

| Upload: | hoangduong |

| View: | 214 times |

| Download: | 1 times |

©2017LinhVo

COMM294FINALREVIEWSESSION–ANSWERKEY

BYLINHVO

©2017LinhVo

TABLEOFCONTENT

I. IntroductionII. Budgeting(Chap.9)III. StandardCosting,OperationalPerformance

Measure(Chap.10)--------------BREAK--------------

IV. Reportingforcontrol:SegmentedReporting(Chap.11)

V. DecisionMaking:RelevantCostsandBenefits(Chap.12)

VI. GeneralTipsandTricks

©2017LinhVo

I. INTRODUCTIONLinhVo

4thyearAccounting

SauderJDCWestCompetitor,2017

PwCTaxSummerAssociate,2016

©2017LinhVo

II. BUDGETING1. SalesBudget2. ExpectedCashCollections

AccountReceivable/DueintheMonthfromprevioussale+ AccountPayable/Duenowfromthispurchase= ExpectedCashDisbursement

3. ProductionBudget

BudgetedSales+ DesiredEndingInventory= TotalNeed- BeginningInventory= RequiredProduction

4. DirectMaterialBudget

RequiredProduction x Materialperunit = DMforproductionneed + DesiredEndingDM = TotalDMneed - BeginningDM

= DMneedtobepurchased

©2017LinhVo

5. DirectLabourBudget

Unitofproduction(productionbudget)x DLhour/unit= DLRequired

6. ManufacturingOHbudgeted

BudgetedDLHx VariableOHrate= VariableMOH+ FixedMOH= TotalMOH- Non-cashcost(depreciation)= CashdisbursementforMOH

7. ExpectedCashDisbursementfortheMonth

AccountPayable/DueintheMonthfrompreviouspurchase

+ AccountPayable/Duenowfromthispurchase= ExpectedCashDisbursement

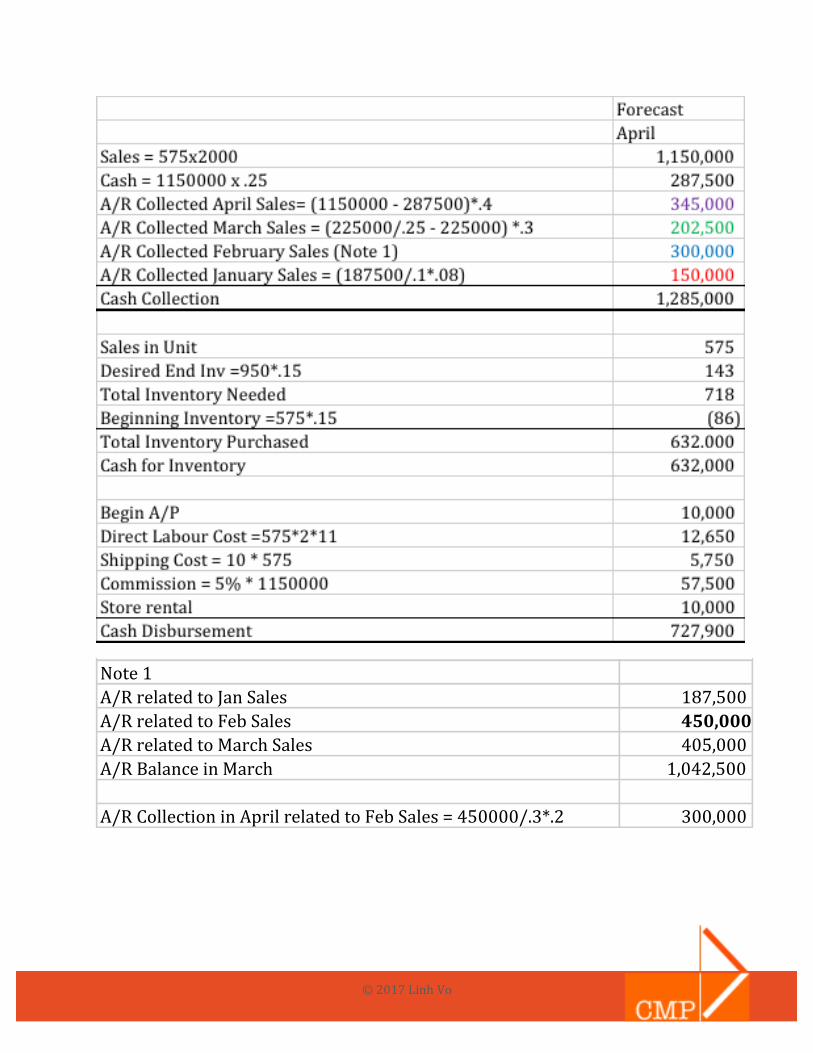

Question1:CMPLtd.sellselectronicstoraisefundforfinalreviewsessions.CMPLtd.sellsoncreditandforcash.Roy,thedirector,wantsyoutoforecasttheAprilcashcollectionanddisbursement.Cecillia,hisVPFinance,givesyouthebelowinformation:

©2017LinhVo

ForecastSaleUnitforApril 575ForecastSalesUnitforMay 950CashSalesinMarch 225,000A/REndingBalanceinMarch 1,042,500A/REndingBalanceinMarchrelatedtoJanSales 187,500EndingA/PMarch 10,000

M0 M1 M2 M3SalesinCash 25%CollectionofA/R 40% 30% 20% 8% 2%

DLH/unitSellingpriceWageCommissionStorerental/monthShippingcost/unitInventorycost/unit

15%

2 2,000 11 5%

10,000

Uncollectible

M0=MonthofSalesM1=OnemonthafterSalesM2=TwomonthsafterSalesM3=ThreemonthsafterSales

dollarsdollarsdollars

ofnextmonthforecastedsaleDesiredlevelofEndInventory

hoursdollarsdollarsonSalesdollars

10 1,000

Pleaseshowyourwork.

©2017LinhVo

Note1A/RrelatedtoJanSales 187,500 A/RrelatedtoFebSales 450,000 A/RrelatedtoMarchSales 405,000 A/RBalanceinMarch 1,042,500

A/RCollectioninAprilrelatedtoFebSales=450000/.3*.2 300,000

©2017LinhVo

III. STANDARDCOSTINGActualcosts–Standardcosts,if:Actualcosts>Standardcosts=Unfavourable(+)Actualcosts<Standardcosts=Favourable(-)

AQ=ActualQuantity SQ=StandardQuantityAP=ActualPrice SP=StandardPrice

(AQxAP)–(AQxSP)=

AQx(AP–SP)

(AQxSP)–(SQxSP)=

SPx(AQ–SQ)

AQxAP AQxSP SQxSP

PriceVarianceLabourRateVarianceVOHRateVariance

QuantityVarianceLabourEfficiencyVarianceVOHEfficiencyVariance

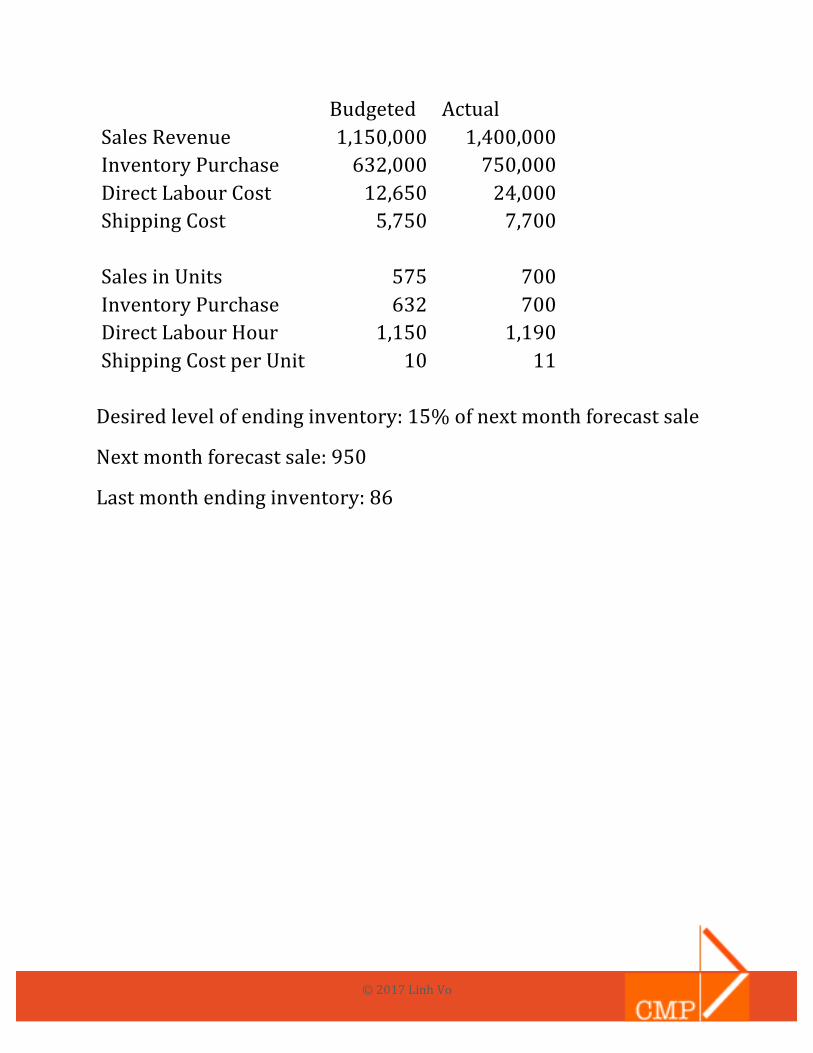

Question2:It’snowMay.Roy,thedirectorofCMPLtd.,wantstoknowwhotopraiseandwhotopunish.Heasksyoutocomputetheinventory,labour,andshippingvariances,andprovidesomereasonstowhyit’sunfavourableorfavourable.Cecillia,theVPFinance,alsoprovidesyouwiththeseinformation:

©2017LinhVo

Budgeted ActualSalesRevenue 1,150,000 1,400,000InventoryPurchase 632,000 750,000DirectLabourCost 12,650 24,000ShippingCost 5,750 7,700

SalesinUnits 575 700InventoryPurchase 632 700DirectLabourHour 1,150 1,190ShippingCostperUnit 10 11 Desiredlevelofendinginventory:15%ofnextmonthforecastsale

Nextmonthforecastsale:950

Lastmonthendinginventory:86

©2017LinhVo

Solutions

©2017LinhVo

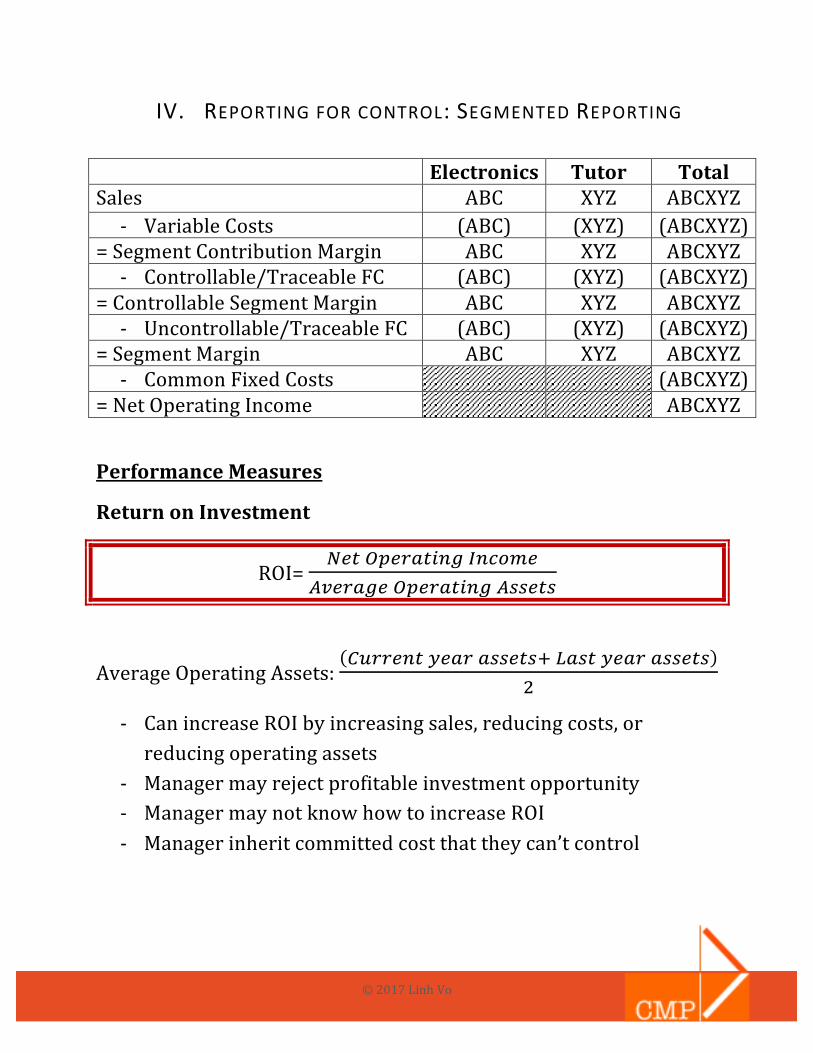

IV. REPORTINGFORCONTROL:SEGMENTEDREPORTING

Electronics Tutor TotalSales ABC XYZ ABCXYZ- VariableCosts (ABC) (XYZ) (ABCXYZ)

=SegmentContributionMargin ABC XYZ ABCXYZ- Controllable/TraceableFC (ABC) (XYZ) (ABCXYZ)

=ControllableSegmentMargin ABC XYZ ABCXYZ- Uncontrollable/TraceableFC (ABC) (XYZ) (ABCXYZ)

=SegmentMargin ABC XYZ ABCXYZ- CommonFixedCosts (ABCXYZ)

=NetOperatingIncome ABCXYZ

PerformanceMeasures

ReturnonInvestment

ROI=!"#%&"'(#)*+,*-./"

01"'(+"%&"'(#)*+022"#2

AverageOperatingAssets:34''"*#5"('(22"#267(2#5"('(22"#2

8

- CanincreaseROIbyincreasingsales,reducingcosts,orreducingoperatingassets

- Managermayrejectprofitableinvestmentopportunity- ManagermaynotknowhowtoincreaseROI- Managerinheritcommittedcostthattheycan’tcontrol

©2017LinhVo

ResidualIncome

OperatingIncome–(AverageAssetsxMinimumRequiredRateofReturn)

- ResidualIncomeencouragesmanagerstoinvestinprofitableprojectsthatwouldberejectedunderROI.

- Evaluatebasedonhistoricalaccountingdatawhichcanleadtopoorevaluation

- Needtobecomparedwithexternalbenchmarktoseewhatearningsshouldbe

- RequireadjustmentstoGAAPtocalculateRIwhichincreasesthecostofpreparinginformation

- Doesnotincorporatenon-financialfactors- Cannotbeusedtocompareperformanceofdifferent-sizeddivisions

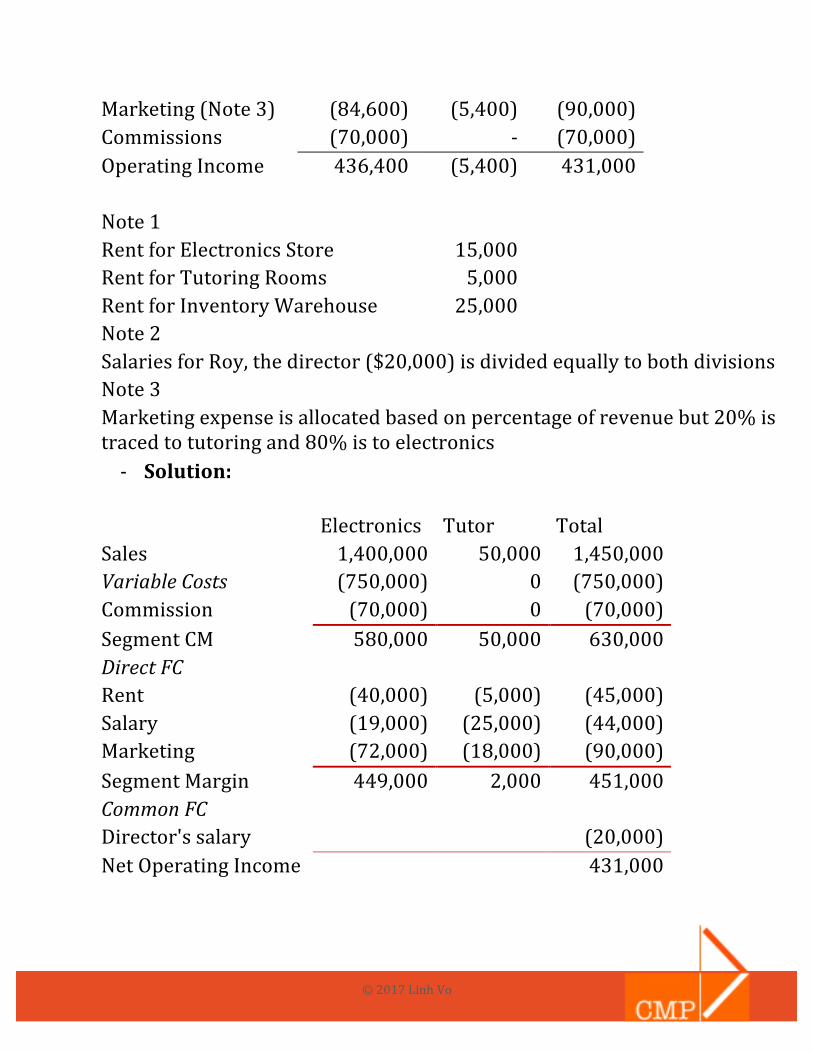

Question3:RoywantstoknowtheperformanceofdifferentdivisionsinMay.SinceTutorDivisionismakingaloss,Royconsidersdroppingthedivision.Cecilliaprovidesyouthebelowinformation.PleasehelpsavetheTutoringdivision.

Electronics Tutor Total Sales 1,400,000 50,000 1,450,000 COGS (750,000) - (750,000) GrossMargin 650,000 50,000 700,000 Rent(Note1) (30,000) (15,000) (45,000) Salaries(Note2) (29,000) (35,000) (64,000)

©2017LinhVo

Marketing(Note3) (84,600) (5,400) (90,000) Commissions (70,000) - (70,000) OperatingIncome 436,400 (5,400) 431,000

Note1 RentforElectronicsStore 15,000 RentforTutoringRooms 5,000 RentforInventoryWarehouse 25,000 Note2 SalariesforRoy,thedirector($20,000)isdividedequallytobothdivisionsNote3 Marketingexpenseisallocatedbasedonpercentageofrevenuebut20%istracedtotutoringand80%istoelectronics- Solution:

Electronics Tutor TotalSales 1,400,000 50,000 1,450,000VariableCosts (750,000) 0 (750,000)Commission (70,000) 0 (70,000)SegmentCM 580,000 50,000 630,000DirectFC Rent (40,000) (5,000) (45,000)Salary (19,000) (25,000) (44,000)Marketing (72,000) (18,000) (90,000)SegmentMargin 449,000 2,000 451,000CommonFC Director'ssalary (20,000)NetOperatingIncome 431,000

©2017LinhVo

TransferPricing

Transferpricingtransactionsbetweentwodivisionswillnotchangethecompany’soverallnetincome.

MinimumTransferPrice=SellingDivision’sLowestAcceptableTransferPrice

≥ UnitVC+RelevantFC+39:'./7.2#%4#2);"<(="2>.#(=?*)#>'(*2:"''";

MaximumTransferPrice=BuyingDivision’sHighestAcceptableTransferPrice

≤ Costofbuyingfromoutsidesuppliers IfMaxTP>MinTP,Transfer!IfMaxTP<MinTP,Don’tTransfer!

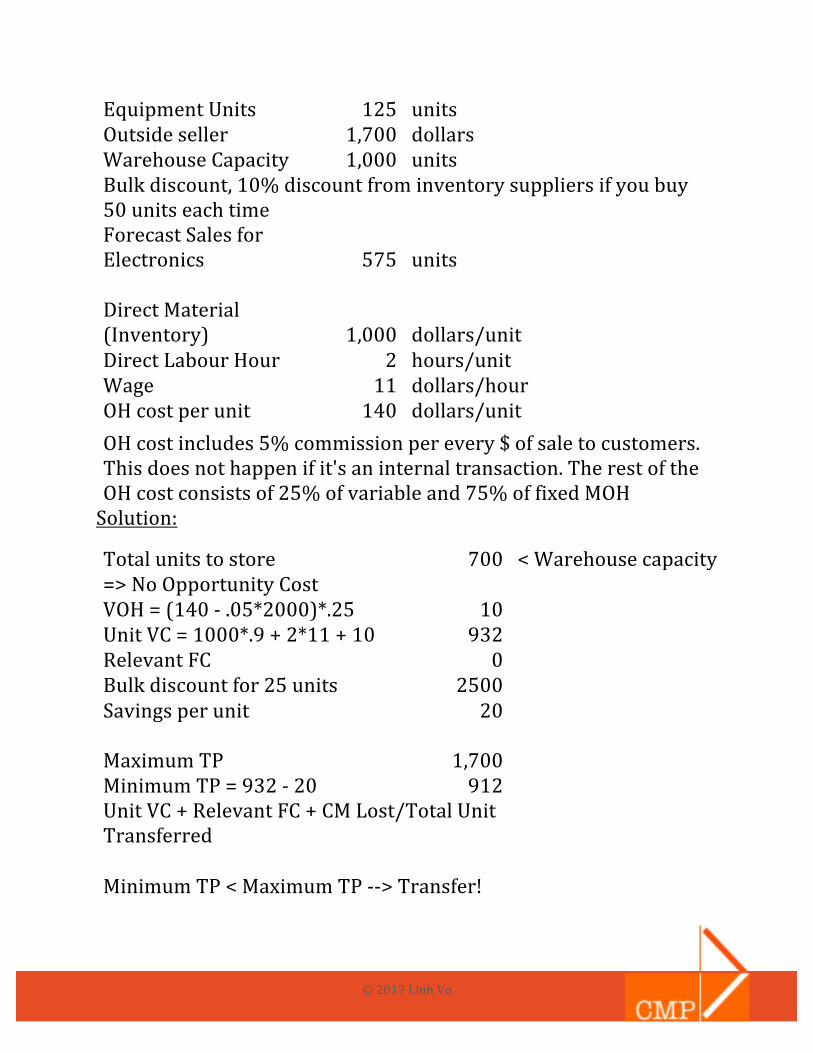

Question4:Tutoringdivisionwantstobuysomeoverheadprojectorsandcomputersforthereviewsessions,soNunu,themanagerofthedivision,isnegotiatingwithGalen,themanagerofElectronicsdivision.

Nunu:Icangettheequipmentelsewhereat$1,700eachsoIsuggestyougiveussomegooddeal.

Galen:Wecansellittocustomersfor$2,000.WhyshouldIsellittoyou?

*Bothstartfighting*soRoyasksyoutobethemediatorandsolvethis.YouturntoCecilliaforfurtherinformation:

©2017LinhVo

EquipmentUnits 125 units Outsideseller 1,700 dollars WarehouseCapacity 1,000 units Bulkdiscount,10%discountfrominventorysuppliersifyoubuy

50unitseachtimeForecastSalesforElectronics 575 units

DirectMaterial(Inventory) 1,000 dollars/unit

DirectLabourHour 2 hours/unit Wage 11 dollars/hour OHcostperunit 140 dollars/unit OHcostincludes5%commissionperevery$ofsaletocustomers.

Thisdoesnothappenifit'saninternaltransaction.TherestoftheOHcostconsistsof25%ofvariableand75%offixedMOHSolution:

Totalunitstostore 700 <Warehousecapacity=>NoOpportunityCost

VOH=(140-.05*2000)*.25 10 UnitVC=1000*.9+2*11+10 932 RelevantFC 0 Bulkdiscountfor25units 2500 Savingsperunit 20

MaximumTP

1,700 MinimumTP=932-20 912 UnitVC+RelevantFC+CMLost/TotalUnit

Transferred

MinimumTP<MaximumTP-->Transfer!

©2017LinhVo

V. DECISIONMAKING:RELEVANTCOSTSANDBENEFITS

Relevantcosts=coststhatdifferorcanbeavoidedbetweenalternatives

Acceptorrejectanorder

IncrementalCosts<IncrementalBenefits:AcceptIncrementalCosts>IncrementalBenefits:Reject

IncrementalCosts=VC+RelevantFC+OpportunityCostIncrementalBenefits=Orderprice,revenuereceivedfromorder

Question5:AsalepersoncomestoGalenandpresentsanofferfromacustomer.Sincethisisasaletocustomer,CMPstillneedstopaycommissiontothesalepersonandabonusof$1,000sinceit’sabigorder.Informationbelow:

#ofunitsinorder 500 units Proposedprice 1,800 dollars WarehouseCapacity 1,000 units

Bulkdiscount,10%discountfrominventorysuppliersifyoubuy50unitseachtimeForecastSalesforElectronics 575 units

DirectMaterial(Inventory) 1,000 dollars/unit DirectLabourHour 2 hours/unit Wage 11 dollars/hour

©2017LinhVo

OHcostperunit 140 dollars/unit OHcostincludes5%commissionperevery$ofsaletocustomers.Therest

oftheOHcostconsistsof25%ofvariableand75%offixedMOH

Solution:

VOH=(140-.05*2000)*.25+1800*.05 100 CMof75units 70,100 =25*(2000-1000-2*11-.05*2000-

10) +50*(2000-1000*.9-2*11-.05*2000-10) OrderRelevantCosts DM 450,000

DL 11,000 VOH 50,000 OpportunityCost 70,100

RelevantFC 1,000=bonusforsaleperson

582,100 OrderRelevantBenefit

Revenue 900,000 =500*1800

èYes,accepttheorder!

©2017LinhVo

Adding/DroppingSegment

FixedCostSaving>LostSegmentContributionMargin,thendrop!

Question6:LookingattheperformanceofTutoringdivision,RoyisconsideringtoeliminatethedivisionandfocussolelyonElectronicssales.PleasehelpconvinceRoytokeeptheTutoringdivision.Cecilliaprovidesyouwiththefollowinginformation.

Tutor Revenue 50,000 COGS (10,000) GrossMargin 40,000 Rent(Note1) (20,000) Salaries(Note2) (35,000) Marketing(Note3) (20,000) Commissions(Note4) (1,000) OperatingIncome (36,000)

Note1 Allocationofheadofficerent 15,000 RentforTutoringRooms 5,000 Note2 50%ofsalariesforRoy,thedirector($20,000)isallocatedtoTutoringNote3 20%ofmarketingexpenseisallocatedtotutoringdivision.Cecilliasaysthatthemarketingmaterialforthisdivisiononlycosts$5000

©2017LinhVo

Solution:

Keep Drop DifferenceSales 50,000 - (50,000)VariableCosts (10,000) - 10,000Commission (1,000) - 1,000SegmentCM 39,000 - (39,000)DirectFC Rent (5,000) - 5,000Salary (25,000) - 25,000Marketing (5,000) - 5,000SegmentMargin 4,000 - (4,000)CommonFC HeadofficeRent (15,000) (15,000) -GeneralMarketing (100,000) (100,000) -Director'ssalary (20,000) (20,000) -NetOperatingIncome (131,000) (135,000) (4,000)

-->Keepthedivisionbecausethebenefitis39,000>FCof35,000

©2017LinhVo

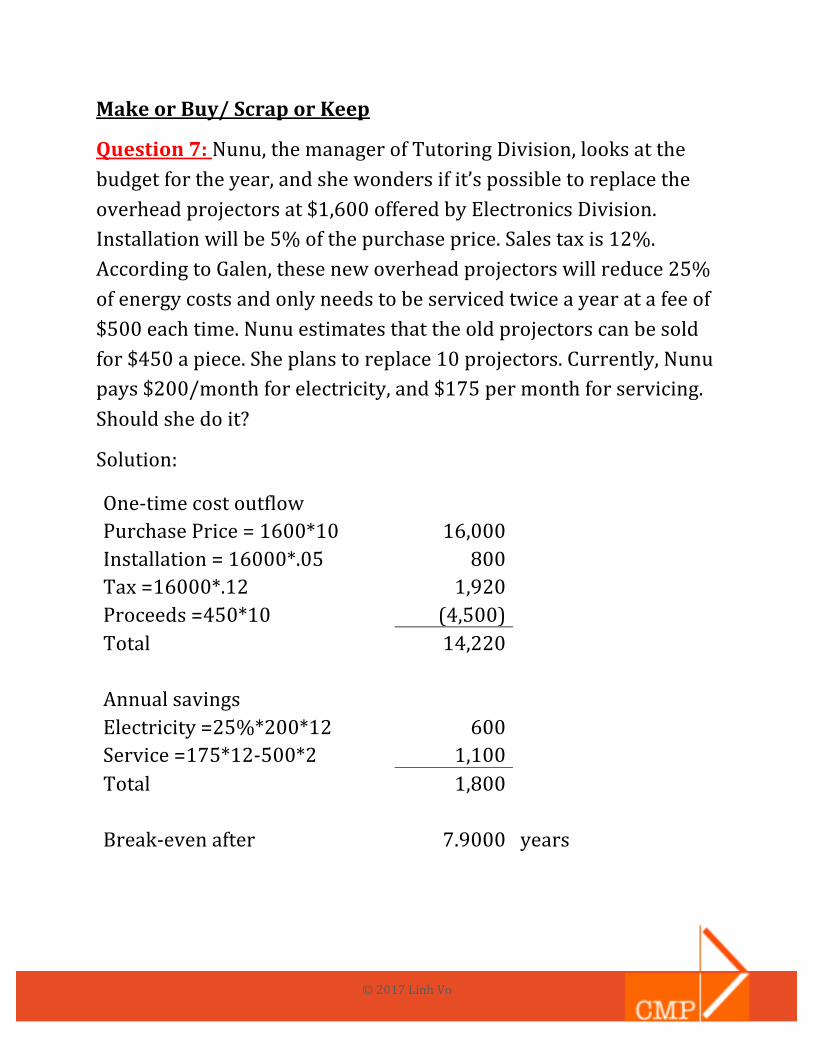

MakeorBuy/ScraporKeep

Question7:Nunu,themanagerofTutoringDivision,looksatthebudgetfortheyear,andshewondersifit’spossibletoreplacetheoverheadprojectorsat$1,600offeredbyElectronicsDivision.Installationwillbe5%ofthepurchaseprice.Salestaxis12%.AccordingtoGalen,thesenewoverheadprojectorswillreduce25%ofenergycostsandonlyneedstobeservicedtwiceayearatafeeof$500eachtime.Nunuestimatesthattheoldprojectorscanbesoldfor$450apiece.Sheplanstoreplace10projectors.Currently,Nunupays$200/monthforelectricity,and$175permonthforservicing.Shouldshedoit?

Solution:

One-timecostoutflow PurchasePrice=1600*10

16,000Installation=16000*.05

800

Tax=16000*.12

1,920Proceeds=450*10

(4,500)

Total

14,220

Annualsavings Electricity=25%*200*12

600Service=175*12-500*2

1,100

Total

1,800

Break-evenafter

7.9000 years

©2017LinhVo

Sell/ProcessFurther

ExtraCosts>ExtraRevenueàSellExtraCosts<ExtraRevenueàProcessFurther

IgnoreallcostsuptotheSplit-uppoint

Question8:AnothercustomercomestoCMPandmakesanoffer.HeislookingtobuycomputerswithpreloadedcoursematerialspreparedbyCMPtutors.Sinceit’sarushorder,CMPwillhavetopayanextramark-upof15%forthecomputers(pricedat$1000),andpaythetutorsanextra20%ontopofnormalwages($20/hour).Ittakesthetutor10hourstopreparecoursematerials.However,thecoursematerialscanbeusedbyCMPlaterforotherpurposes.Thecustomeroffers$5000fortwocomputerswithtwodifferentcoursematerials.Normalcomputersaresoldfor$2000/each.ShouldCMPaccept?

Solution:

ExtraCost:Totalextracost=$380

Computer=.15*1000*2=300

Wage=10*20*.2*2=80

ExtraRevenue:

$5000-$2000*2=$1000

ExtraCost<ExtraRevenueàAccepttheorder

©2017LinhVo

UtilizationofConstrainedResources

Maximizethetotalcontributionmarginoftheproduct/salemixFocusonContributionMarginperunitofConstrainedResourcesProducetheproductwithhighestCMperunitofconstrained

resourcesfirst,thenmovedownthelist.

Question9:Afterthepreviousorderofcomputerspreloadedwithstudymaterials,CMPexecutivesthinkthattheycanmakemoreprofitbydoingthat.Theybrainstorm,doresearch,andgiveyouthisinformation.Pleasehelpthemdecide.

TotalTutorHour 32 hoursOvertimehour* 8 hoursNormalwage 20 dollarsOvertimewage 25 dollarsComputersCost 1000 dollarsTechnicianTime 500 hoursTechnicianwage 25 Dollars

**

Material(hr)

Loading(hr)

#ofDemand SellingPrice

Econ101 8 4 100 2,200Econ102 9 3 90 2,200Comm291 11 6 95 2,400Comm294 12 6 30 2,500*Eachcourseisallocated8hoursofnormaltutorhour**Timeneededfortutortopreparematerial,andtimeneededfortechniciantoloadthecourseontothecomputer

©2017LinhVo

Productionplan #ofunitTotaltechtime

Econ101 57 228 Econ102 90 270 Comm291 0 0 Comm294 0 0

Course Econ101 Econ102 Comm291 Comm294Revenue 220,000 198,000 228,000 75,000Comp.Cost (100,000) (90,000) (95,000) (30,000)TutorCost (160) (160) (160) (160)TutorOT - (25) (75) (100)Techcost (10,000) (6,750) (14,250) (4,500)CM 109,840 101,065 118,515 40,240CMpertechhour 274.60 374.31 207.92 223.56

©2017LinhVo

VI. TIPSANDTRICKS

1) Practicemakesperfect!- Practicemidterms- Assignmentsandin-classquestions- Textbookexercises- 2016CMPReviewPackage:Question–Answer

2) Officehourandotherhelpavailable!- Professor’sreviewtutorial- Professor’sofficehour- CMPofficehour

3) Relax,eatwell,andgetenoughsleep!