26

CommBank Legal Market Pulse Conducted by Beaton Research + Consulting Quarter 3 FY15

CommBank Legal Market PulseConducted by Beaton Research + Consulting

Quarter 3 FY15

1

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Contents

Foreword 2

Economic outlook 3

Snapshot of report findings 4

Firm StructureOffice locations 7

Primary practice areas 7

Business conditionsPerceived performance of the Australian economy 8

Perception of business conditions - present to 2017 8

Perception of business conditions - by area 9

FY15 financial performanceTotal revenue change FY14 to FY15 10

FY15 budgeted and actual revenue results 10

FY15 budgeted and actual expenses results 11

Revenue predictionsChange in revenue over the next 6 months - by location 12

Change in revenue over the next 6 months - by practice area 13

Realised rates and fee structureExpected changes in realised rates - next 6 and 12 months 15

Expense and profitability predictionsChange in expenses over the next 6 months 16

Change in staffing over the next 6 months 17

Change in operating margins over the next 6 months 18

Managing people, staff and talentCore staff turnover between 1 July & 31 December 2014 19

Expected change in core staff turnover in FY15 19

Expected change in core staff remuneration in FY15 20

Contract staff headcount 20

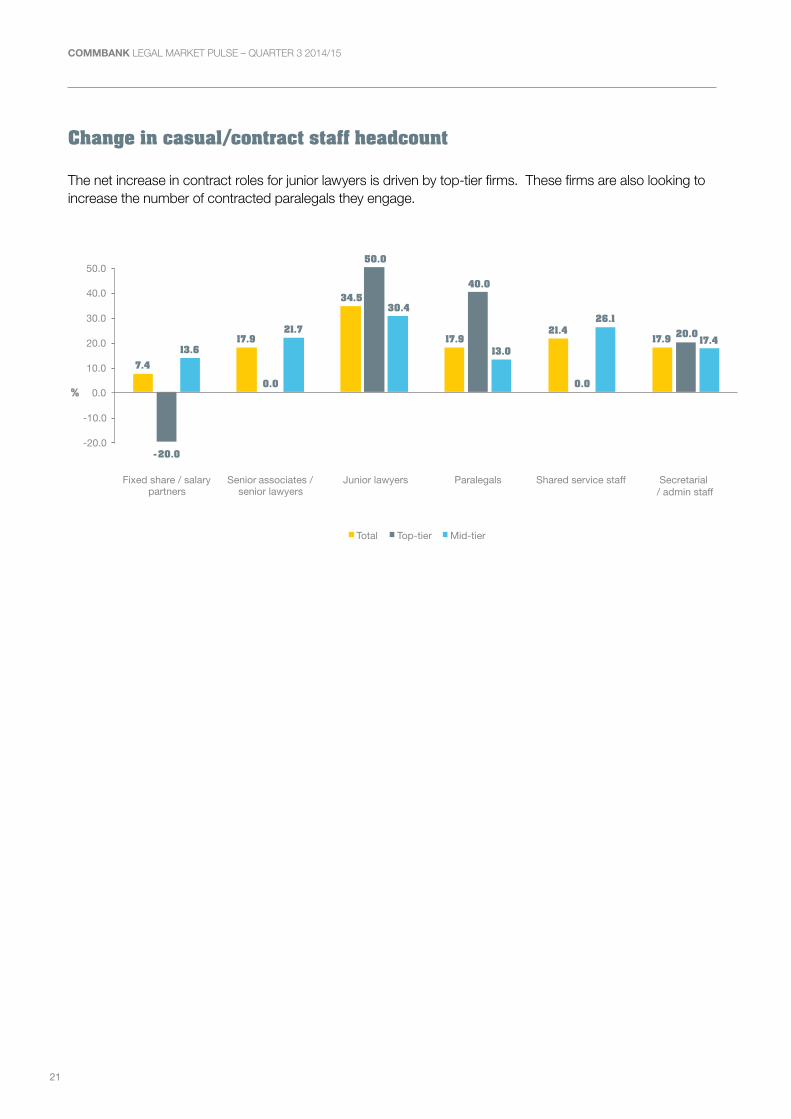

Change in casual/contract staff headcount 21

Sourcing and outsourcingUse of LPOs - next 12 months 22

Client driven LPO usage 22

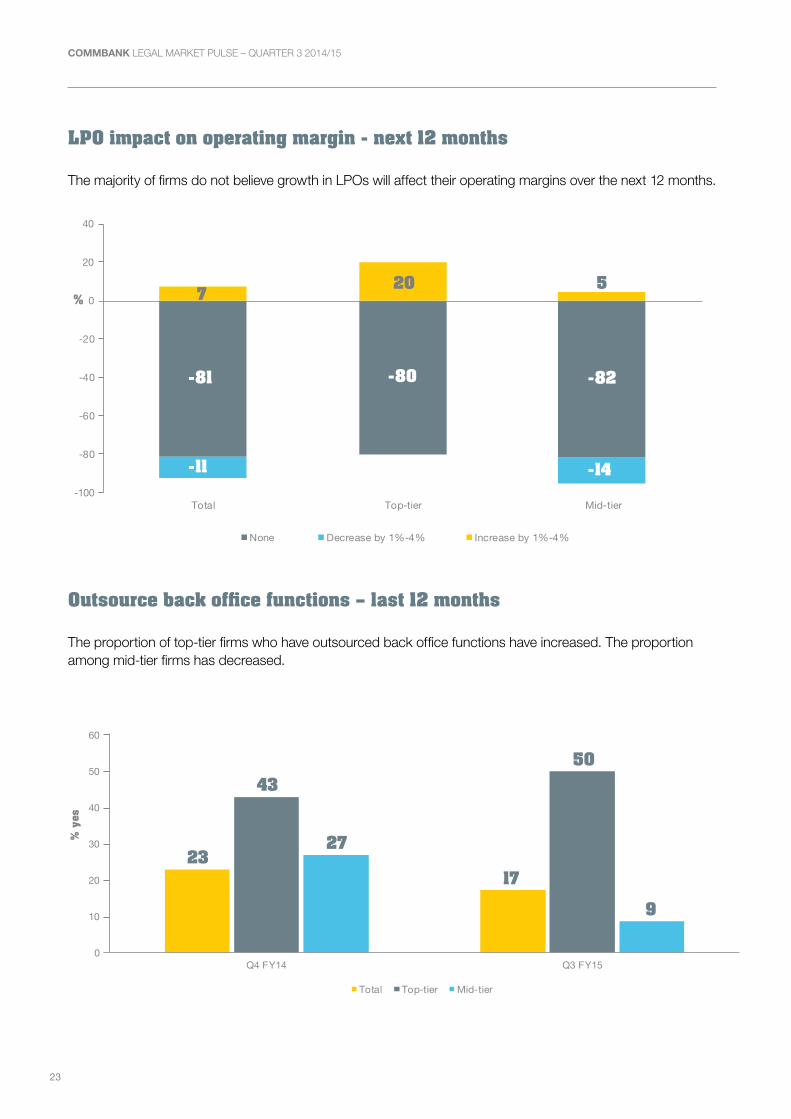

LPO impact on operating margin - next 12 months 23

Outsourcing back office functions - last 12 months 23

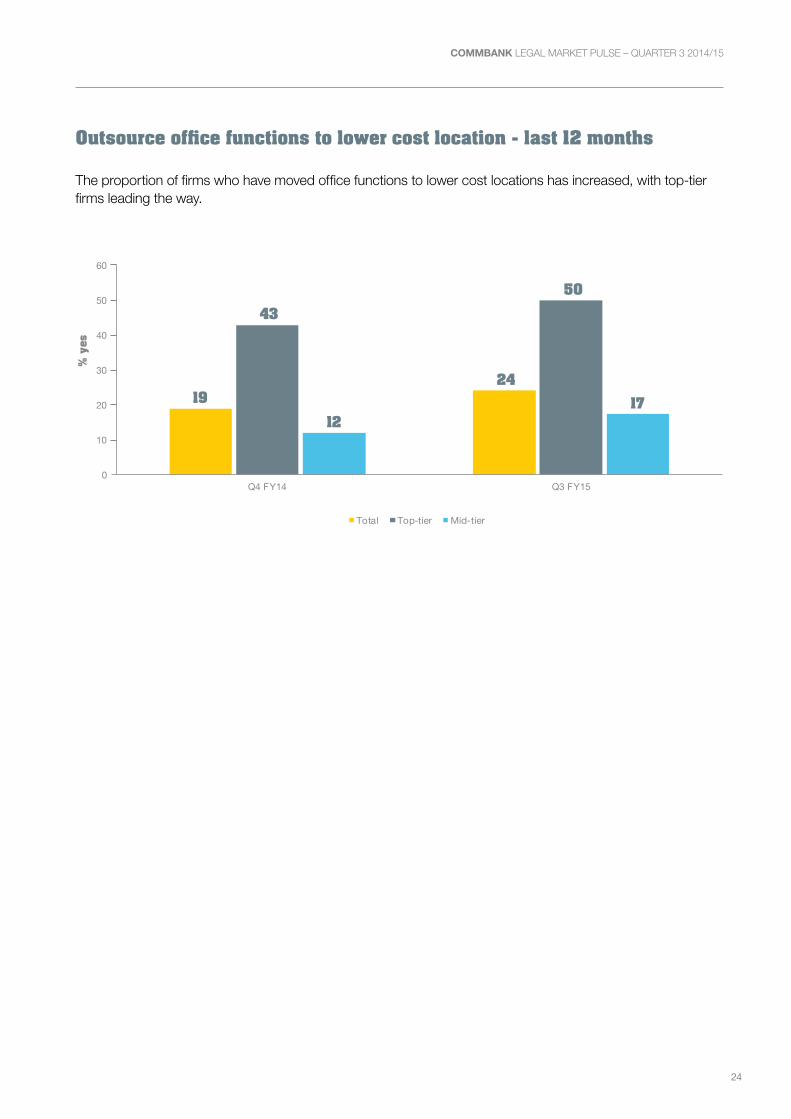

Outsource office functions to lower cost locations - last 12 months 24

2

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Marc Totaro National Manager, Professional Services Commonwealth Bank

Welcome to the third quarter edition of the CommBank Legal Market Pulse for the 2015 financial year.

It’s good to see confidence is rising among Australia’s top-tier law firms, with the vast majority expecting business conditions to improve over the next two years.Our latest report shows long-term optimism returning to the industry, fuelled by expectations of revenue growth, low interest rates and an improved economy. Every top-tier firm surveyed forecast higher revenues over the next six months in Europe, Asia and Sydney, with most also anticipating growth in Brisbane and Canberra.

But while sentiment has improved markedly among the top-tier, mid-tier firms are less positive. With comparatively little exposure to global economic growth and large transactions, these firms are less optimistic about revenue growth and are generally more subdued about conditions over the next 12 months, although most still expect an improvement by 2017.

Asked which practice areas were likely to outperform, firms nominated employment, insurance and property law as the most likely sources of increased revenues. However, government work looks set to decline as reduced state and federal spending take their toll, while revenue across construction, IT, telecommunications and media are also forecast to fall.

Investments in marketing and business development are expected to rise, as firms aggressively pursue revenue growth. Yet many are also looking to rein in non-essential expenses before the end of financial year, with spending on IT and staff training set to tighten.

The intensely competitive market is also reflected in the lateral hiring of partners and lawyers, which has continued apace over the last quarter. Firms continue to poach lawyers and partners from their rivals, while a growing number of junior staff has switched employers in search of greener pastures.

Both top and mid-tier firms are planning to decrease secretarial and shared service staff, with almost a quarter of all firms having outsourced office functions to lower cost locations. A key driver behind this trend is that half of all firms believe there is growing pressure from clients to use legal process outsourcing.

I hope you find this issue useful and informative. We look forward to continuing to monitor the legal industry’s sentiment and performance, and sharing these insights with you.

Email: [email protected] Tel: +61 2 9303 1940

Confidence set to rise over long-term, driven by optimism among top-tier firms

3

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Diana Mousina Associate Director Economics Commonwealth Bank

The latest growth figures have confirmed the Australian economy has expanded by a below-trend 2.7 percent over 2014. The story is really a tale of two halves, with annualised growth in the first half of 2014 tracking at 3.4 percent while growth in the second half was 1.7 percent. Below-trend growth is evidenced through soft readings across the business surveys. The latest CommBank Legal Market Pulse indicates a negative short-term outlook of business conditions across the legal industry. Perceptions of business conditions have increased marginally from last quarter but still remain weak.

The long-term outlook continues to remain positive. And top-tier firms are continuously more optimistic about future business conditions compared to mid-tier firms. Income growth in the economy is running at exceptionally weak levels. The significant decline in commodity prices over 2014 is the main reason behind this weakness. A lack of income has pushed consumers to defer spending and increase savings, businesses to defer or cancel capital spending and labour hiring and governments to tighten the fiscal screws. This income weakness is reflected in consumer and business surveys.

New sources of income are needed as the economy transitions from mining to non-mining led growth. Parts of this growth transition are on track. Resource exports are surging and will be a significant new source of income growth over the next two years. The residential construction upturn is also firmly entrenched. The labour-intensive nature of this sector will be positive for jobs growth. Mining related job losses are currently being more than offset with jobs related to rising dwelling investment.

Legal leaders surveyed in the CommBank Legal Market Pulse have mixed forecasts for staff numbers. Expectations for total staff numbers are relatively unchanged from last quarter however across the headline number there are variations across the different groups. Partner numbers are expected to decline, along with paralegals, secretarial and administrative staff. Graduate numbers are still expected to grow.

One part of the growth transition faltering is non-mining business capex. Recent data shows commercial lending growth, one of the funding sources for non-mining capex, has dropped after solid growth over 2014. This part of the transition needs to be stronger over 2015 for reasonable growth outcomes to be met. Business confidence and conditions will need to improve to drive non-mining capex higher.

The RBA downgraded their growth and inflation forecasts in early 2015 and were a key reason for their decision to cut the cash rate to 2.25 percent in February. The RBA’s rate cut is at odds with the central bank’s rhetoric regarding strong dwelling price growth in parts of Australia (particularly Sydney and Melbourne). The RBA expects macroprudential tools announced by the Australian Prudential Regulator in late 2014 will cool dwelling price growth this year. The RBA’s desire to influence consumption and investment patterns means that one standalone rate cut is unlikely. In an environment of low inflation, a rising unemployment rate and an uncertain growth transition, we and the market see another rate cut in the second quarter of this year, most probably in May.

Australian economic outlook

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Summary of Q1 FY2015 findingsSnapshot of survey findings

Perception of business conditions Perceived performance of the Australian economy over next 12 months

Net % (positive-negative)

-35% -31%

All firms

-17%

Top-tier firms Mid-tier firms

Net % (positive-negative)

Budgeted vs actual results

Revenue -1.3%

Expenses -3.2%

Total firms

Revenue 1.6%

Expenses -4.7%

Top-tier firms

Revenue -1.9%

Expenses -2.9%

Mid-tier firms

Mean %

-26% -24%

10% 29% 55% 10%

Q2 FY15 Q3 FY15 Q2 FY15 Q3 FY15 Q2 FY15 Q3 FY15

At the moment In 12 months In 24 months

Revenue expectations by state Highest revenue growth expectations – by practice area

Top-tier firms

Employment, workplace and OH&S

Net % (positive-negative)

IT, telecoms and media

Taxation

Insurance

Construction, engineering and major infrastructure

Employment, workplace and OH&S

67%

67%

50%

60%

50%

47%

Mid-tier firms

4

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Expected changes in realised rates

-0.5% -1.5%

Next 6 months

Next 12 months

Top-tier firms +0.4% +1.0%

Next 6 months

Next 12 months

Mid-tier firms

Operating margins

Top-tier firms

Mid-tier firms

67%

13%

Net % increase

Changes in staff numbers

Turnover of core workforce

Junior lawyers

Fixed share / salary partners Equity partners Senior lawyers Secretarial / admin staff Shared service staff Paralegals

Top-tier firms

Junior lawyers Fixed share / salary partners Senior lawyers Paralegals

Secretarial / admin staff Shared service staff

Mid-tier firms

Equity partners

Secretarial / admin

staff

9.7%

Junior lawyers

9.7%

Shared service

staff

8.1%

Senior lawyers

7.7%

Paralegals

7.5%

Fixed share / salary

partners

3.9%

Equity partners

2.8%

Expected change in staff turnover

21 14

28

7

-7 3

Senior lawyers

Fixed share / salary

partnersParalegals Secretarial /

admin staff

10

Junior lawyers Equity

partnersShared

service staffMean %

Mean %

Snapshot of survey findings

5

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Expected changes in realised rates

-0.5% -1.5%

Next 6 months

Next 12 months

Top-tier firms +0.4% +1.0%

Next 6 months

Next 12 months

Mid-tier firms

Operating margins

Top-tier firms

Mid-tier firms

67%

13%

Net % increase

Changes in staff numbers

Turnover of core workforce

Junior lawyers

Fixed share / salary partners Equity partners Senior lawyers Secretarial / admin staff Shared service staff Paralegals

Top-tier firms

Junior lawyers Fixed share / salary partners Senior lawyers Paralegals

Secretarial / admin staff Shared service staff

Mid-tier firms

Equity partners

Secretarial / admin

staff

9.7%

Junior lawyers

9.7%

Shared service

staff

8.1%

Senior lawyers

7.7%

Paralegals

7.5%

Fixed share / salary

partners

3.9%

Equity partners

2.8%

Expected change in staff turnover

21 14

28

7

-7 3

Senior lawyers

Fixed share / salary

partnersParalegals Secretarial /

admin staff

10

Junior lawyers Equity

partnersShared

service staffMean %

Mean %

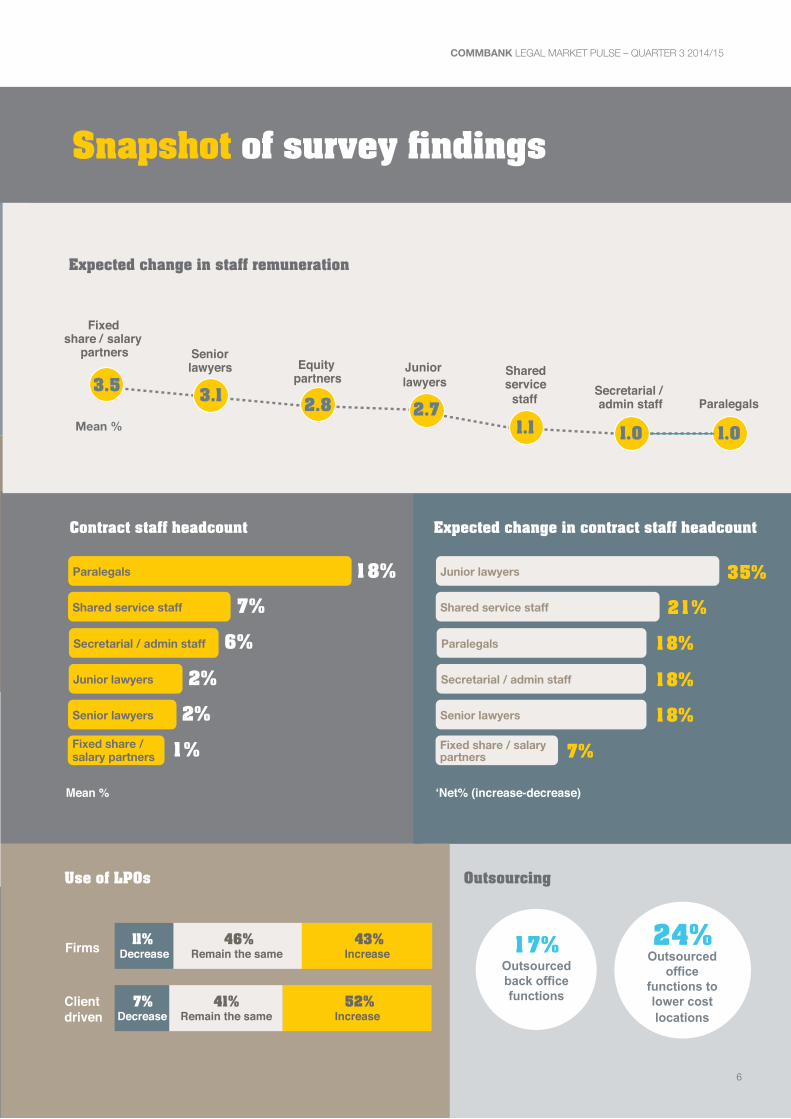

Contract staff headcount

Paralegals

Shared service staff

Secretarial / admin staff

Junior lawyers

Senior lawyers

Fixed share / salary partners

18%

7%

6%

2%

2%

1%

Expected change in contract staff headcount

Junior lawyers

Shared service staff

Paralegals

Secretarial / admin staff

Senior lawyers

Fixed share / salary partners

35%

21%

18%

18%

18%

7%

Mean % ‘Net% (increase-decrease)

Use of LPOs

46% Remain the same

43% Increase Firms

7% Decrease

41% Remain the same

52% Increase

Client driven

11% Decrease

Outsourcing

17% Outsourced back office functions

24% Outsourced

office functions to lower cost locations

Expected change in staff remuneration

3.1 2.8 3.5

1.1 1.0 1.0

Fixed share / salary

partners Senior lawyers Equity

partnersJunior lawyers

2.7

Shared service

staff Secretarial / admin staff Paralegals

Mean %

Snapshot of survey findings

6

7

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Firm structure

Office locations

76 72

69

41

28 24 24

21 21

0

20

40

60

80

Sydney Melbourne Brisbane Perth Asia Other Adelaide UK / Europe Canberra

%

Primary practice areas

55

62

66

69

69

69

76

76

79

79

83

86

86

93

97

0 20 40 60 80 100

Other general commercial work

Insurance

Taxation

Government

IT, telecoms and media

Energy and resources

Construction, engineering and major infrastructure (including project finance)

Competition, consumer law and trade practices

Intellectual property (including PTA and IP disputes)

Banking and finance (including funds management)

Insolvency and restructuring

Employment, workplace and OH&S

M&A and corporate advisory (including capital markets)

Property, environment and planning

Litigation and dispute resolution

%

8

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

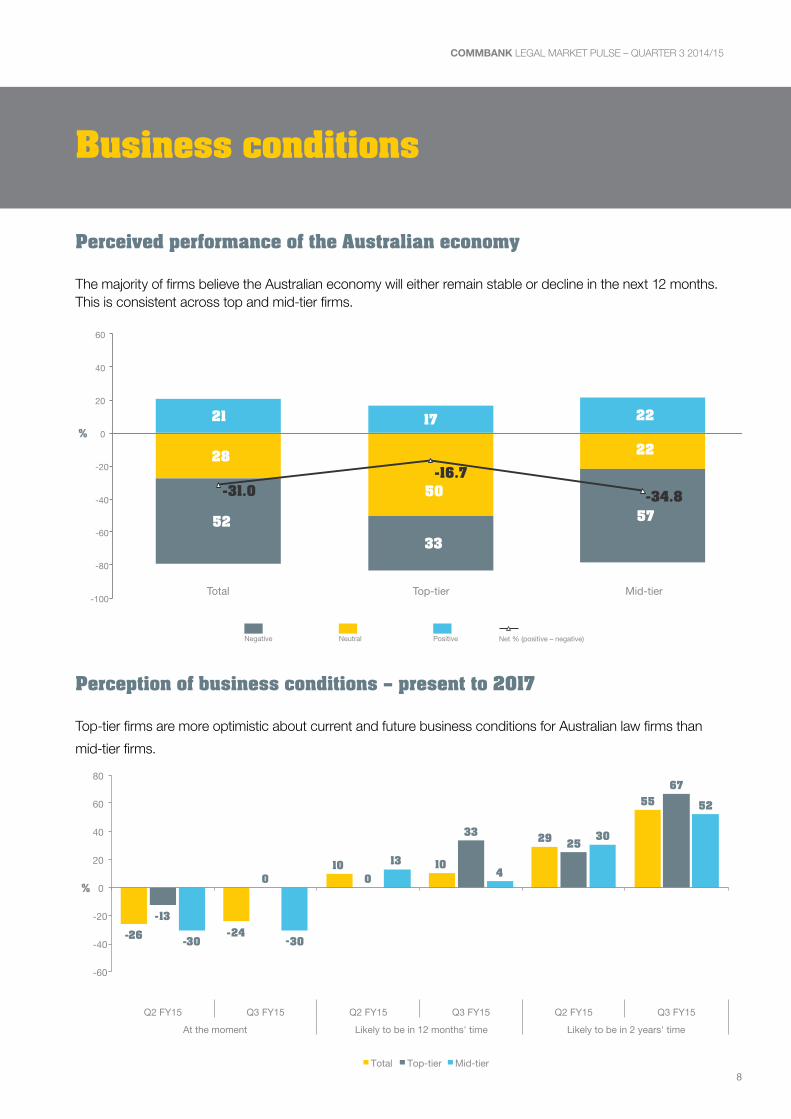

Business conditions

Perceived performance of the Australian economy

The majority of firms believe the Australian economy will either remain stable or decline in the next 12 months. This is consistent across top and mid-tier firms.

Positive Negative Neutral

32

18

21

39

18

29

Net % (positive – negative)

28

50

22

52 33

57

21 17 22

- 31.0 - 16.7

- 34.8

-100

-80

-60

-40

-20

0

20

40

60

Total Top-tier Mid-tier

%

Perception of business conditions – present to 2017

Top-tier firms are more optimistic about current and future business conditions for Australian law firms than

mid-tier firms.

- 26 - 24

10 10 29

55

- 13

0 0

33 25

67

- 30 - 30

13 4

30

52

-60

-40

-20

0

20

40

60

80

Q2 FY15 Q3 FY15 Q2 FY15 Q3 FY15 Q2 FY15 Q3 FY15 At the moment Likely to be in 12 months' time Likely to be in 2 years' time

%

Total Top-tier Mid-tier

9

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Perception of business conditions - by area

Mid-tier firms are finding it harder to collect invoices, find quality staff and keep expenses under control compared to the top-tier law firms.

39 55

- 13 - 3

- 42

- 28

50 50

- 13

0

- 25

0

35

57

- 13 - 4

- 48 - 35

-60 -40 -20

0 20 40 60

Q2 FY15 Q3 FY15 Q2 FY15 Q3 FY15 Q2 FY15 Q3 FY15 Accessing capital Keeping quality staff

- 26 - 14

- 23 - 17 - 13

0

- 13

0

- 30 - 17

- 26 - 22

Q2 FY15 Q3 FY15 Q2 FY15 Q3 FY15 Keeping expenses under

control Finding quality staff Collecting invoices

%

Total Top-tier Mid-tier

-100

-80

-60

-40

-20

0

20

40

60

- 55

- 41 - 50

- 33

- 57

- 43

Q2 FY15 Q3 FY15

Competing with other firms

- 55 - 48

- 75

- 50 - 48 - 48

Q2 FY15 Q3 FY15

Winning new business

- 45 - 55

- 50 - 50 - 43

- 57

Q2 FY15 Q3 FY15

Keeping staff fully utilised

- 81

- 66

- 88

- 67 - 78

- 65

Q2 FY15 Q3 FY15 Negotiating price with clients

%

Total Top-tier Mid-tier

10

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

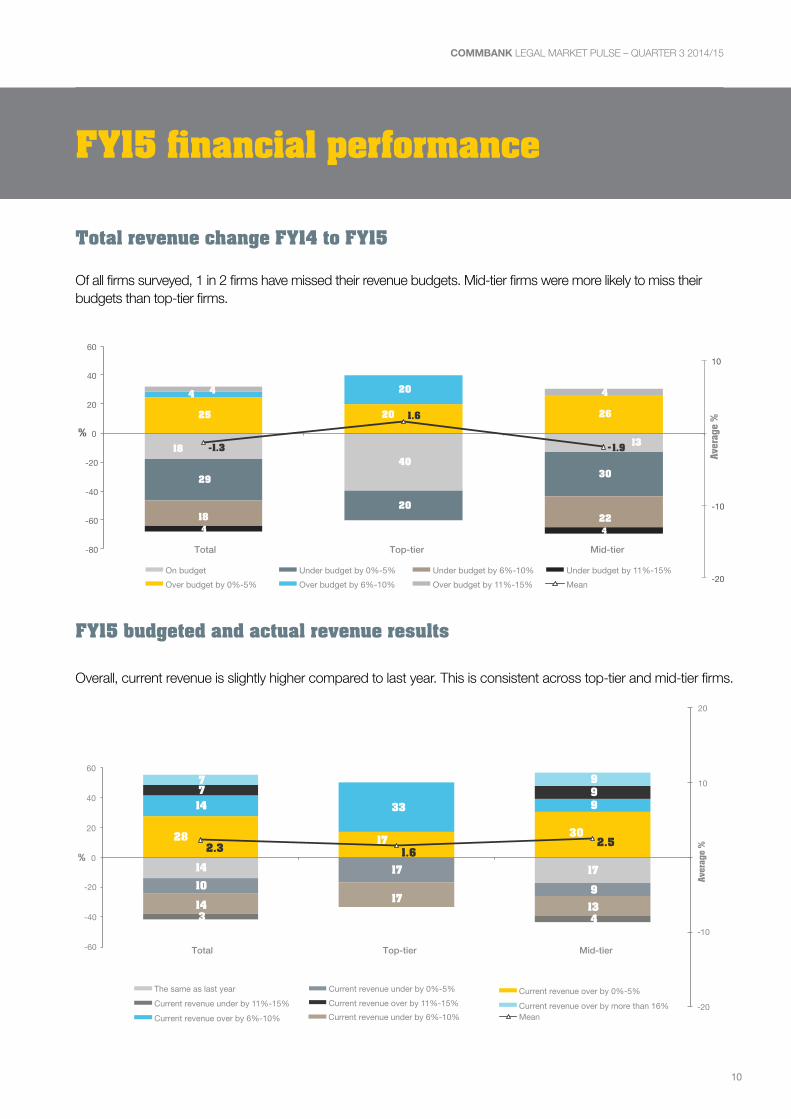

FY15 financial performance

Total revenue change FY14 to FY15

Of all firms surveyed, 1 in 2 firms have missed their revenue budgets. Mid-tier firms were more likely to miss their budgets than top-tier firms.

18 40

13

29

20

30

18 22 4 4

25 20 26

4 20 4 4

- 1.3

1.6

- 1.9

-20

-10

10

-80

-60

-40

-20

0

20

40

60

Total Top-tier Mid-tier

Aver

age

%

%

On budget Under budget by 0%-5% Under budget by 6%-10% Under budget by 11%-15% Over budget by 0%-5% Over budget by 6%-10% Over budget by 11%-15% Mean

FY15 budgeted and actual revenue results

Overall, current revenue is slightly higher compared to last year. This is consistent across top-tier and mid-tier firms.

14 17 10

17

9 14 17

13 3 4

28 17 30

14 33 9 7 9 7 9

2.3 1.6 2.5

-20

-10

10

20

-60

-40

-20

0

20

40

60

Total Top-tier Mid-tier

Aver

age

%

%

The same as last year Current revenue under by 0%-5%

Current revenue under by 6%-10% Current revenue under by 11%-15%

Current revenue over by 0%-5%

Current revenue over by 6%-10% Current revenue over by 11%-15% Current revenue over by more than 16%

Mean

11

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

FY15 budgeted and actual expenses results

At this time of the financial year, 2 in 3 firms have managed to control their expenses and are tracking below budget.

25 20 26

43 60 39

14 17 7 20 4

11 13

- 3.2

- 4.7

- 2.9

- 20

-10

10

-100

-80

-60

-40

-20

0

20

40

Total Top-tier Mid-tier

Aver

age

%

%

On budget Under budget by 0%-5% Under budget by 6%-10% Under budget by 11%-15% Over budget by 0%-5% Mean

12

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

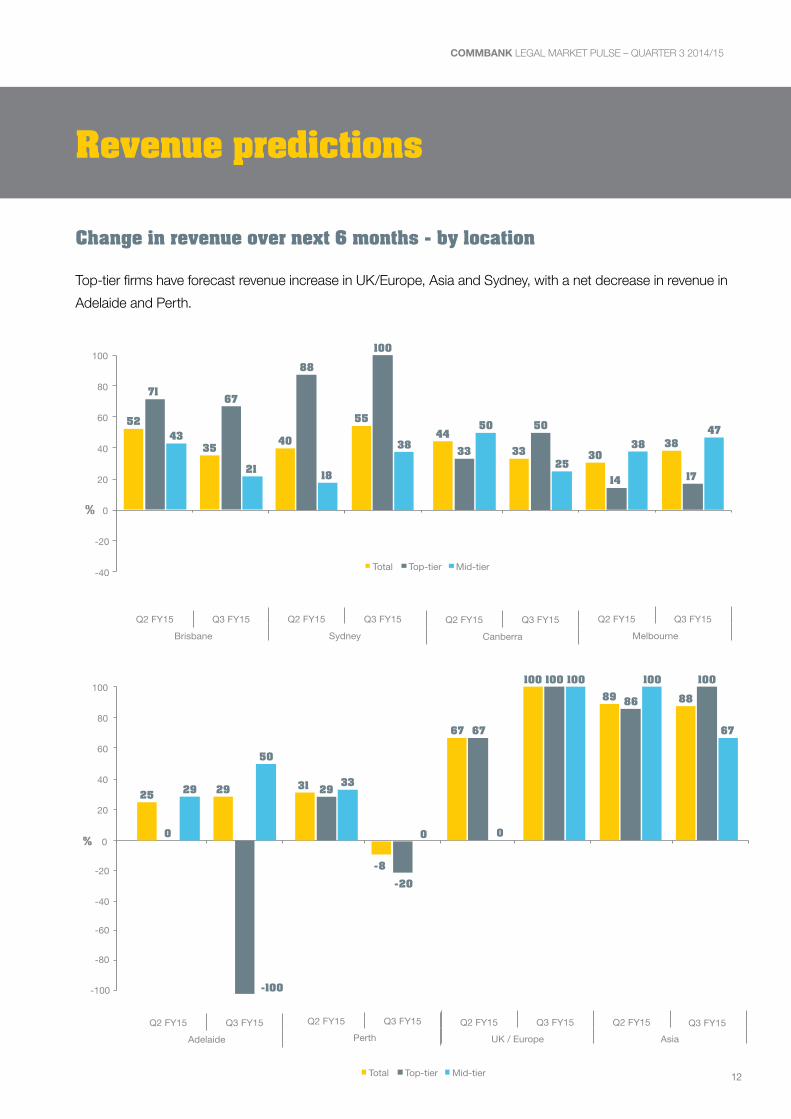

Revenue predictions

Change in revenue over next 6 months - by location

Top-tier firms have forecast revenue increase in UK/Europe, Asia and Sydney, with a net decrease in revenue in

Adelaide and Perth.

30 38

14 17

38 47

-40

-20

0

20

40

60

80

100

Q2 FY15 Q3 FY15 Melbourne

%

Total Top-tier Mid-tier

44 33 33

50 50

25

Q2 FY15 Q3 FY15 Canberra

52

35

71 67

43

21

Q2 FY15 Q3 FY15 Brisbane

40

55

88

100

18

38

Q2 FY15 Q3 FY15

Sydney

67

100 89 88

67 67

100

86

0

100 100 100

Q2 FY15 Q3 FY15 Q2 FY15 UK / Europe Asia

31

- 8

29

- 20

33

0

Q2 FY15 Q3 FY15 Perth

25 29

0

29

50

Q2 FY15 Q3 FY15 Adelaide

-100

-40

-60

-80

-100

-20

0

20

40

60

80

100

%

Q3 FY15

Total Top-tier Mid-tier

13

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

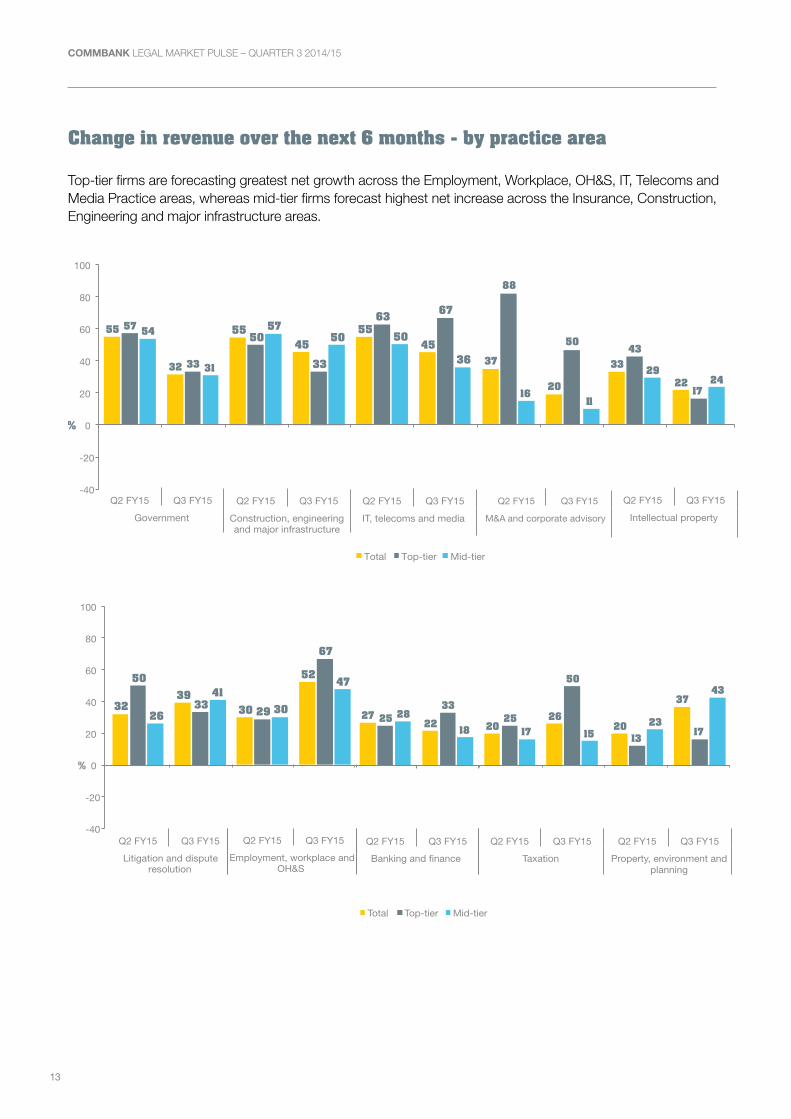

Change in revenue over the next 6 months - by practice area

Top-tier firms are forecasting greatest net growth across the Employment, Workplace, OH&S, IT, Telecoms and Media Practice areas, whereas mid-tier firms forecast highest net increase across the Insurance, Construction, Engineering and major infrastructure areas.

-40

-20

0

20

40

60

80

100

55 45

63 67

50

36

Q2 FY15 Q3 FY15 IT, telecoms and media

%

Total Top-tier Mid-tier

55

32

57

33

54

31

Q2 FY15 Q3 FY15 Government

55 45

50

33

57 50

Q2 FY15 Q3 FY15 Construction, engineering and major infrastructure

37

20

88

50

16 11

Q2 FY15 Q3 FY15 M&A and corporate advisory

33

22

43

17

29 24

Q2 FY15 Q3 FY15 Intellectual property

27 22 25

33 28

18

Q2 FY15 Q3 FY15 Banking and finance

20 26 25

50

17 15

Q2 FY15 Q3 FY15 Taxation

20

37

13 17

23

43

Q2 FY15 Q3 FY15 Property, environment and

planning

32 39

50

33 26

41

Q2 FY15 Q3 FY15 Litigation and dispute

resolution

30

52

29

67

30

47

Q2 FY15 Q3 FY15 Employment, workplace and

OH&S

-40

-20

0

20

40

60

80

100

%

Total Top-tier Mid-tier

14

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Change in revenue over the next 6 months - by practice area (continued)

17 14

63

50

- 6

0

Q2 FY15 Q3 FY15

Competition, consumer law and trade practices

15

50

- 25

0

25

60

Q2 FY15 Q3 FY15

Insurance

12 17 14

33

11 11

Q2 FY15 Q3 FY15

Insolvency and restructuring

5 6

- 20

50

12 0

Q2 FY15 Q3 FY15

Other general commercial work

- 30

- 15 - 25

50

- 33 - 43

Q2 FY15 Q3 FY15

Energy and resources

Total Top-tier Mid-tier

-40

-60

-20

0

20

40

60

80

100

%

15

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Realised rates and fee structure

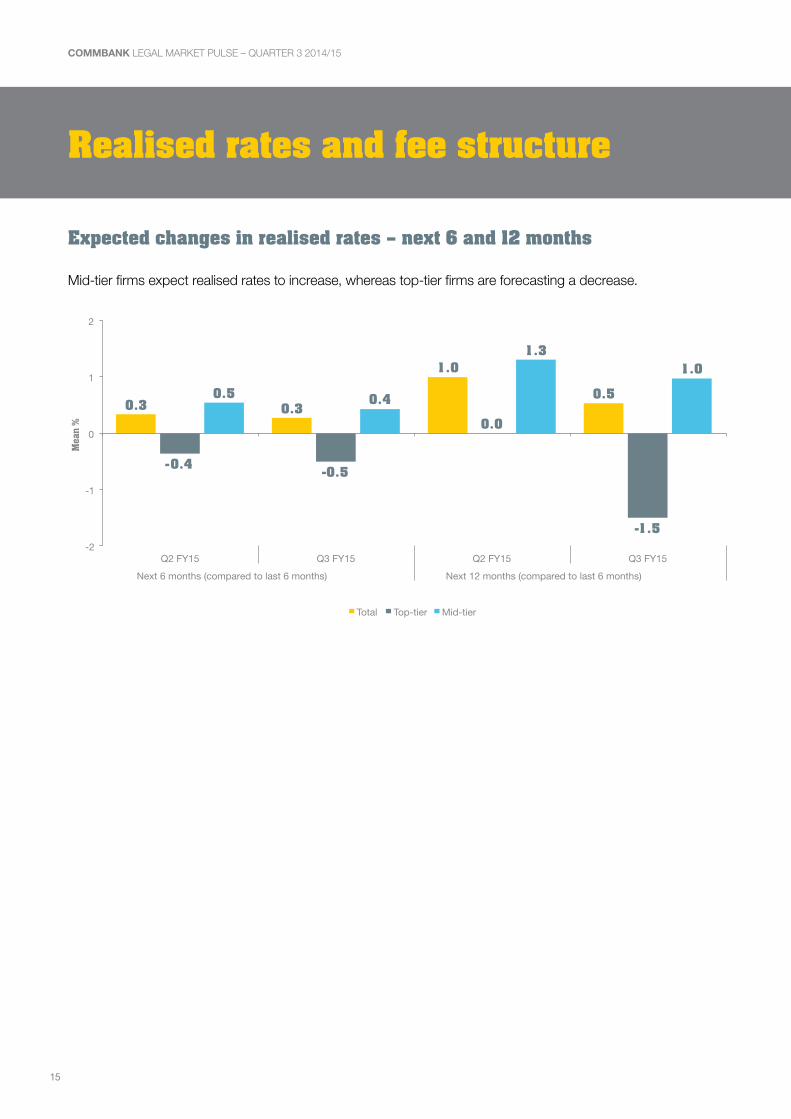

Expected changes in realised rates – next 6 and 12 months

Mid-tier firms expect realised rates to increase, whereas top-tier firms are forecasting a decrease.

0.3 0.3

1.0

0.5

- 0.4 - 0.5

0.0

- 1.5

0.5 0.4

1.3 1.0

-2

-1

0

1

2

Q2 FY15 Q3 FY15 Q2 FY15 Q3 FY15 Next 6 months (compared to last 6 months) Next 12 months (compared to last 6 months)

Mea

n %

Total Top-tier Mid-tier

16

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Expense and profitability predictions

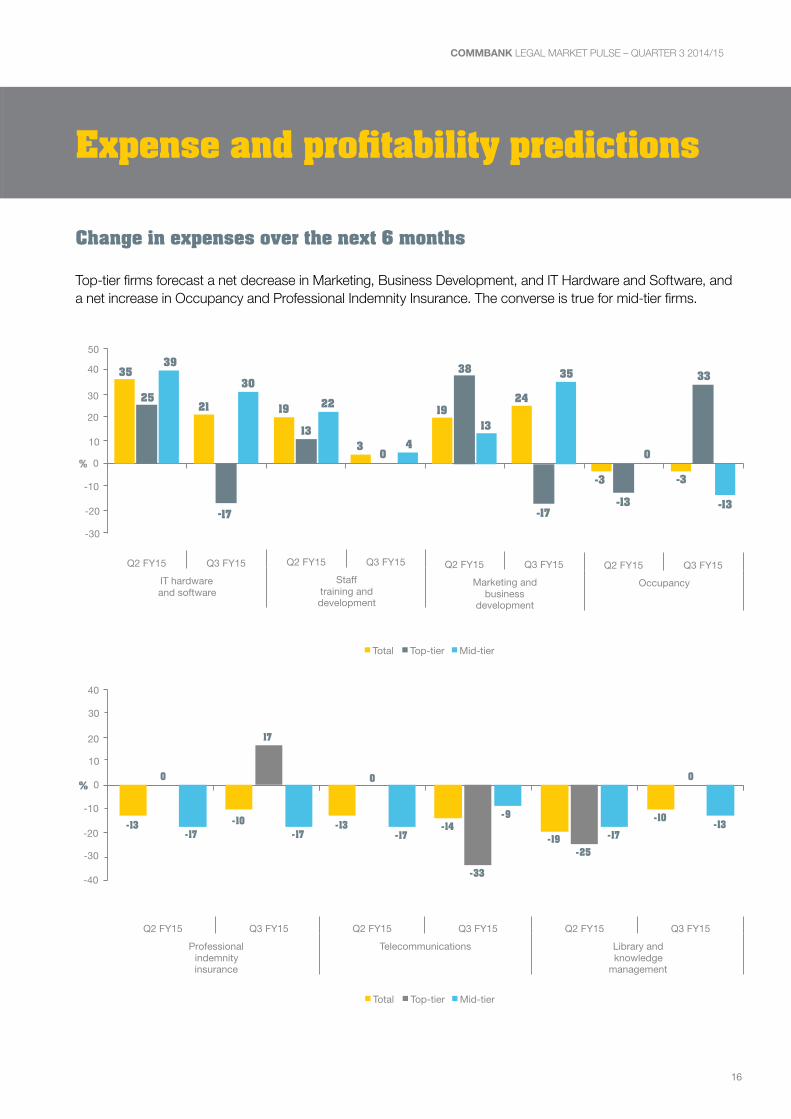

Change in expenses over the next 6 months

Top-tier firms forecast a net decrease in Marketing, Business Development, and IT Hardware and Software, and a net increase in Occupancy and Professional Indemnity Insurance. The converse is true for mid-tier firms.

-20

-10 0

20

10

40

50

19 24

38

- 17

13

35

Q2 FY15

Q3 FY15

Marketing and

business

development

19

3 13

0

22

4

Q2 FY15 Q3 FY15

Staff

training and

development

- 3

- 3

- 13

33

0

- 13

Q2 FY15

Q3 FY15

Occupancy

%

Total

Top-tier

Mid-tier

35

21 25

- 17

39 30

Q2 FY15

Q3 FY15

IT hardware

and software

-30

30

-40

-20

0

20

10

-10

-30

30

40

- 13 - 10

0

17

- 17 - 17

Q2 FY15

Q3 FY15

Professional

indemnity insurance

- 19 - 10

- 25

0

- 17 - 13

Q2 FY15

Q3 FY15

Library and knowledge

management

%

Total

Top-tier

Mid-tier

- 13 - 14

0

- 33

- 17 - 9

Q2 FY15 Q3 FY15

Telecommunications

17

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Change in staffing over the next 6 months

There is a forecasted decline in net proportion of partner numbers which is being driven by top-tier firms.

6

- 7

26 17 16 17

26 31

0

- 33

- 13

- 67

13

- 33

13 17 9

0

39 39

17 30 30

35

-60

-80

-40

-20

0

20

40

Q2 FY15 Q3 FY15

Q2 FY15 Q3 FY15

Q2 FY15 Q3 FY15

Q2 FY15 Q3 FY15

Equity partner numbers

Fixed share / salary partner

numbers

Senior associates / senior lawyers

(4th year+)

Junior lawyer numbers (Graduates

– 3rd year)

%

Total

Top-tier

Mid-tier

- 26 - 18

- 29 - 31

6 3

- 25 - 20 - 25 - 33

- 13 - 17 - 26

- 17 - 30 - 30

13 9

-40

-20

0

20

40

Q2 FY15 Q3 FY15

Q2 FY15

Q3 FY15

Q2 FY15 Q3 FY15

Shared service staff numbers

Secretarial / admin staff numbers

Paralegals

%

Total

Top-tier

Mid-tier

18

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Change in operating margins over the next 6 months

Top-tier firm leaders forecast a greater increase in operating margins, compared to their peers in mid-tier firms.

23 24

50 67

13 13

-40

-20

0

20

40

60

80

Q2 FY15 Q3 FY15

%

Total Top-tier Mid-tier

19

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Managing people, staff and talent

Core staff turnover between 1 July & 31 December 2014

Top-tier firms are experiencing the highest turnover in staff, predominantly with junior lawyers.

10.5

2.8 3.9

7.7 9.7

7.5 8.1 9.7 10.0

2.0 3.8

7.0 9.2

7.4 7.3 8.9

12.0

5.7 4.3

10.3 11.5

8.0

11.2 12.7

0.0

5.0

10.0

15.0

Total core workforce

Equity partners

Fixed share / salary

partners Senior

associates / senior

lawyers

Junior lawyers

Paralegals Shared service staff

Secretarial / admin staff

Mea

n %

Total Top-tier Mid-tier

Expected change in core staff turnover in FY15

There is a high net forecast turnover among salary partners, senior lawyers and paralegals, driven by top-tier firms.

10 3

21 28

7 14

- 7

10 13

0

17 26

13 9

- 13

9 0

17

33 33

- 17

33

17 17

-20 -10

0 10 20 30 40

Total core workforce

Equity partners

Fixed share / salary

partners Senior

associates / senior

lawyers

Junior lawyers

Paralegals Shared service staff

Secretarial / admin staff

%

Total Top-tier Mid-tier

20

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

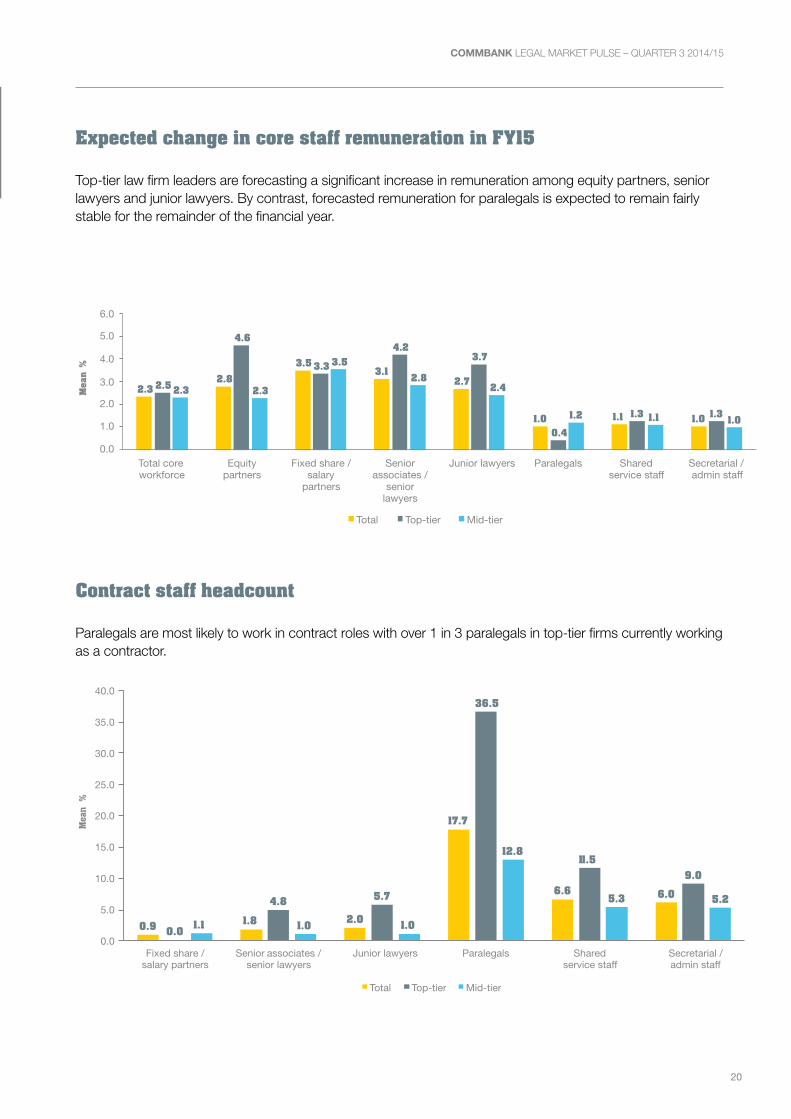

Expected change in core staff remuneration in FY15

Top-tier law firm leaders are forecasting a significant increase in remuneration among equity partners, senior lawyers and junior lawyers. By contrast, forecasted remuneration for paralegals is expected to remain fairly stable for the remainder of the financial year.

2.3 2.8

3.5 3.1

2.7

1.0 1.1 1.0

2.5

4.6

3.3

4.2 3.7

0.4 1.3 1.3

2.3 2.3

3.5 2.8

2.4

1.2 1.1 1.0

0.0

2.0

4.0

6.0

5.0

3.0

1.0

Total core workforce

Equity partners

Fixed share / salary

partners Senior

associates / senior

lawyers

Junior lawyers

Paralegals Shared service staff

Secretarial / admin staff

Mea

n %

Total Top-tier Mid-tier

Contract staff headcount

Paralegals are most likely to work in contract roles with over 1 in 3 paralegals in top-tier firms currently working as a contractor.

0.9 1.8 2.0

17.7

6.6 6.0

0.0

4.8 5.7

36.5

11.5 9.0

1.1 1.0 1.0

12.8

5.3 5.2

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Fixed share / salary partners

Senior associates / senior lawyers

Junior lawyers

Paralegals Shared service staff

Secretarial / admin staff

Mea

n %

Total Top-tier Mid-tier

21

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Change in casual/contract staff headcount

The net increase in contract roles for junior lawyers is driven by top-tier firms. These firms are also looking to increase the number of contracted paralegals they engage.

13.6 21.7

30.4

13.0

26.1 17.4

7.4 17.9

34.5

17.9 21.4 17.9

- 20.0

0.0

50.0 40.0

0.0

20.0

-20.0 -10.0

0.0 10.0 20.0 30.0 40.0 50.0

Fixed share / salary partners

Senior associates / senior lawyers

Junior lawyers Paralegals Shared service staff Secretarial / admin staff

%

Total Top-tier Mid-tier

22

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Sourcing and outsourcing

Use of LPOs - next 12 months

The majority of firms believe use of LPOs among firms and clients will either increase or remain the same over the next 12 months.

- 46 - 33 - 50 - 41 - 50 - 38

- 7 - 17

- 5 - 4 - 5

- 4 -

5 -

4

- 5

43 50 41 52 50 52

-60

-40

-20

0

20

40

60

Total Mid-tier Total Mid-tier Firm useTop-tier

Client useTop-tier

%

Remain the same Decrease Decrease significantly Increase

Client driven LPO usage

Of the firms surveyed, 1 in 2 top-tier firms believe there is growing pressure from their clients to use LPOs. This sentiment is less prevalent among mid-tier firms.

- 48 - 50 - 48

- 21

0

- 26

31 50 26 10.3

50.0

0.0

-80

-60

-40

-20

0

20

40

60

Total Top-tier Mid-tier

%

Neutral Disagree Agree Net % (agree-disagree)

23

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

LPO impact on operating margin - next 12 months

The majority of firms do not believe growth in LPOs will affect their operating margins over the next 12 months.

-81 -80 -82

-11 -14

7 20 5

-100

-80

-60

-40

-20

0

20

40

Total Top-tier Mid-tier

%

None Decrease by 1%-4% Increase by 1%-4%

Outsource back office functions – last 12 months

The proportion of top-tier firms who have outsourced back office functions have increased. The proportion among mid-tier firms has decreased.

4350

27

9

2317

0

10

20

30

40

50

60

Q4 FY14 Q3 FY15

% y

es

Total Top-tier Mid-tier

24

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Outsource office functions to lower cost location - last 12 months

The proportion of firms who have moved office functions to lower cost locations has increased, with top-tier firms leading the way.

1924

4350

1217

0

10

20

30

40

50

60

Q4 FY14 Q3 FY15

% y

es

Total Top-tier Mid-tier

25

COMMBANK LEGAL MARKET PULSE – QUARTER 3 2014/15

Further information

For further insights or information, please contact:

Marc Totaro, National Manager Professional Services

Mobile: 0477 739 315 Phone: +61 2 9303 1940 Email: [email protected] Web: commbank.com.au/legalmarketpulse

For media inquiries, please contact:

Sarah Gibbons, Public Relations Advisor Phone: +61 2 9118 1706 Email: [email protected]

About Beaton Research + Consulting

Beaton Research + Consulting is a full-service research firm which offers a full range of solutions for professional services firms, financial services firms and associations. Their expertise includes benchmarking, thought leadership, brand solutions, customised solutions and client satisfaction.

Things to know before you Can: This report is published solely for information purposes. As this report has been prepared without considering your objectives, financial situation or needs, you should before acting on the information in this report, consider its appropriateness to your circumstances and if necessary seek the appropriate professional advice. This quarterly report has been prepared independently by Beaton Research + Consulting and commissioned by Commonwealth Bank. The confidential on-line survey used to prepare this report was undertaken by Beaton Research + Consulting in February 2015. The report is based on the views of 31 legal firms across Australia and any opinions, conclusions or recommendations are reasonably held or made, based on the information available at the time of its compilation, but no representation or warranty, either expressed or implied, is made or provided as to the accuracy, reliability or completeness of any statement made in this report. The project was undertaken in compliance with the requirements of ISO 20252. Commonwealth Bank of Australia ABN 48 123 123 124.