Commercial Payments in Asia-Pacific: Is this the New Opportunity? Asia-Pacific Commercial Cards and Payments Summit, Singapore 14-15 May 2015 Presentation CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited

Transcript

Commercial Payments in Asia-Pacific: Is this the New Opportunity?

Asia-Pacific Commercial Cards and Payments Summit, Singapore

14-15 May 2015

Presentation

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

McKinsey & Company | 1

Commercial Payments in Asia-Pacific: Is this the New Opportunity?

▪ Overview of Commercial Payments in Asia-Pacific

▪ Roadblocks to success

▪ Changes impacting Commercial Payments landscape

▪ Way forward

Contents

McKinsey & Company | 2

Global payments revenues have resumed a healthy growth rate after the crisis; Asia Pacific will account for 56% of overall growth

SOURCE: McKinsey Global Payments Map, McKinsey Global Banking Pools

+8% p.a.

+8% p.a.-12% p.a.

2018

2.3

2013

1.6

2009

1.2

2008

1.3

Share of total banking, %

39 4334 41

US$ trillion

Payments revenue growth decomposition 2013-2018

100% =

13%

15%

APAC

EMEA

2013-2018 growth

NorthAmerica

Latin America

755

56%

16%

10%

5%

5%

11%

CAGR2013-18

Global payments revenue

Percentage (100% = US$ billion)

McKinsey & Company | 333

6

13

42

14

EMEA

Credit card issuing

Commercial CA

Transactions

309

12

1

28

5

12

167

61

22

64

Merchant Acquiring

Transactions

Credit card issuing

Consumer CA

Latin America

44

35

9

31

9

33

28

North America

323

6

10

15

27

APAC

539

81

Percent of total revenue pool within geography, 2013, USD Billion

Already today APAC shows the biggest payment revenue pools, mostly coming from Commercial Accounts

SOURCE: McKinsey Global Payments Map

Co

nsu

mer

Co

mm

erc

ial

1 Includes Cash, Cheques, Transfers, Direct debits, Debit cards, Prepaid cards2 Includes Current Account and Overdrafts

McKinsey & Company | 4

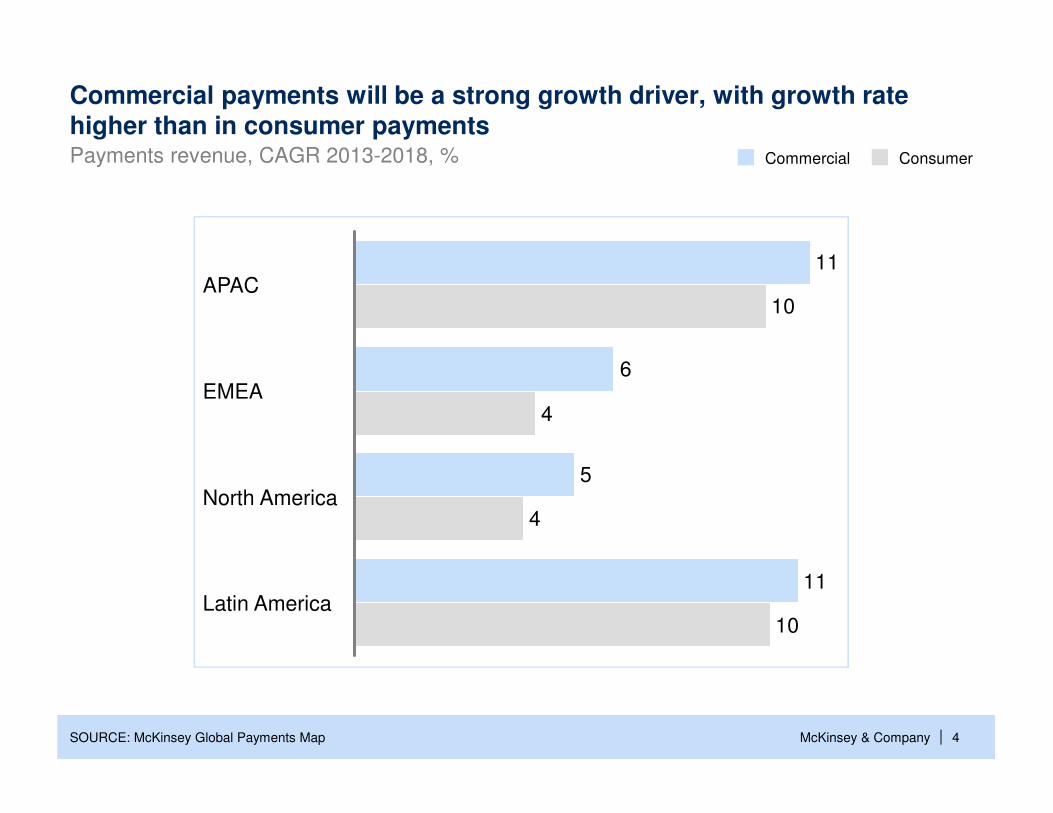

Commercial payments will be a strong growth driver, with growth rate higher than in consumer paymentsPayments revenue, CAGR 2013-2018, %

SOURCE: McKinsey Global Payments Map

11

4

10

5

6

11

4

10

Latin America

North America

EMEA

APAC

ConsumerCommercial

McKinsey & Company | 5

Accounts and transactions likely to be the main source of payments growth in APAC Commercial

World payments revenue growth 13-18

60

29

67

106

28

13Transactions

Accounts

Credit cardsissuing

Merchant acquiring

5

USD billions

SOURCE: McKinsey Global Payments Map

154

22

59

3

9

19

15

67

Consumer Commercial

APAC RoW

McKinsey & Company | 6

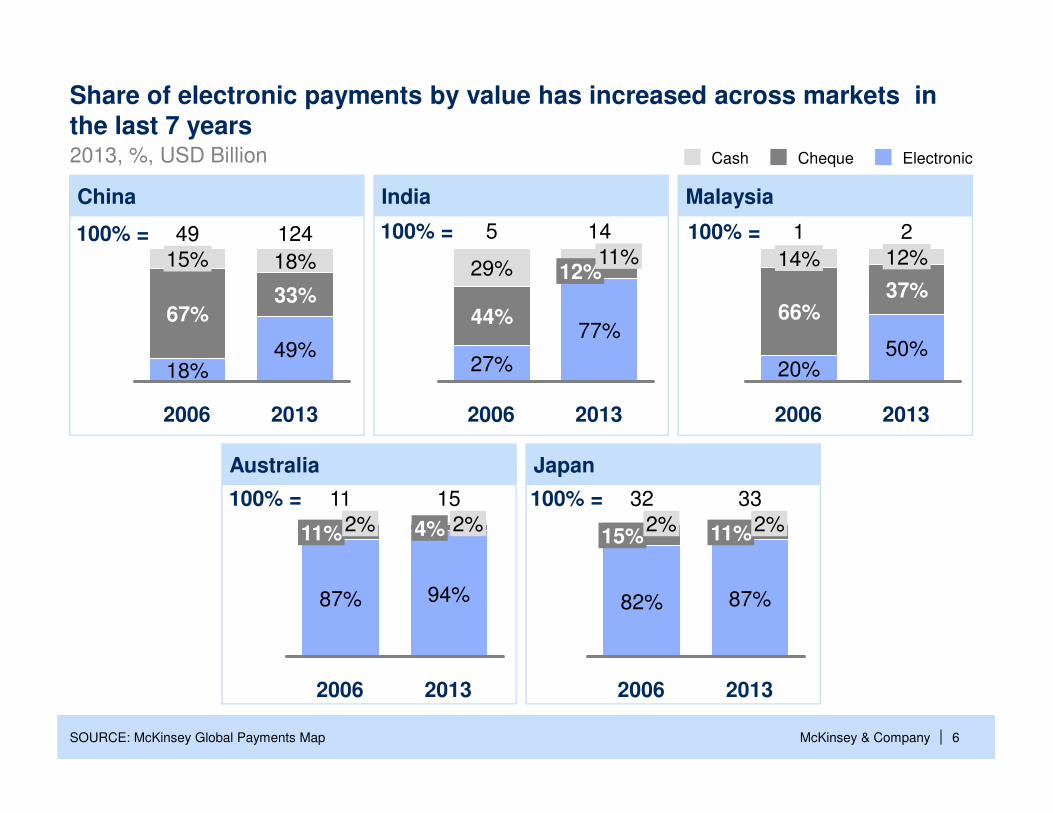

Share of electronic payments by value has increased across markets in the last 7 years

SOURCE: McKinsey Global Payments Map

2013, %, USD Billion

MalaysiaIndia

Australia

China

Japan

100% =

2013

15

94%

4% 2%

2006

11

87%

11%2%100% =

2013

33

87%

11%2%

2006

32

82%

15%2%

100% =

2013

124

49%

33%

18%

2006

49

18%

67%

15%

100% =

2013

14

77%

12%11%

2006

5

27%

44%

29%

100% =

2013

2

50%

37%

12%

2006

1

20%

66%

14%

Cash ElectronicCheque

McKinsey & Company | 7

MalaysiaIndia

Australia

China

Japan

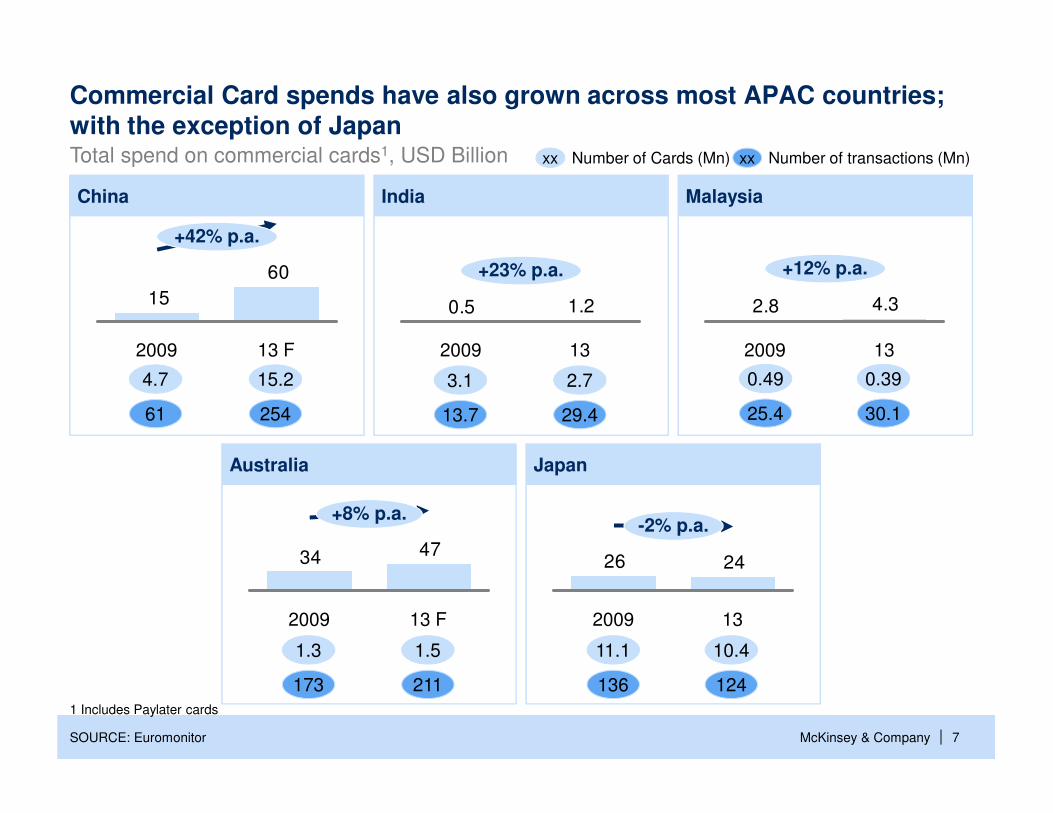

1.3 1.5

173 211

0.49 0.39

25.4 30.1

4.7

61

15.2

254

3.1 2.7

13.7 29.4

11.1 10.4

136 124

Commercial Card spends have also grown across most APAC countries; with the exception of Japan

SOURCE: Euromonitor

Number of Cards (Mn)xx xx Number of transactions (Mn)

4734

+8% p.a.

13 F2009

2426

-2% p.a.

132009

60

15

2009

+42% p.a.

13 F

1.20.5

+23% p.a.

132009

4.32.8

+12% p.a.

132009

Total spend on commercial cards1, USD Billion

1 Includes Paylater cards

McKinsey & Company | 8

1 Includes prepaid cards

Number of payments transactions Value of payments transactions

However, still significant opportunity to electronify payments, including Commercial

100%

96%

76%

82%

90%

59%

57%

100%

15%

8%

46%

34%

36%

13% 39%

9%

G2G 0

G2B 07%

G2C 47%

B2G 0

B2B 186

B2C 15

C2G 4

C2B 1,618

C2C 457 19%

36%

25%

100%

13%

14%

8%

29%

67%

37%

56%

88%

55%

9%

89%

99%

8%

10%

83%

14%

G2G 1

G2B 4

G2C 34%

B2G 5

B2B 192

B2C 5

C2G 15%

C2B 164%

C2C 7

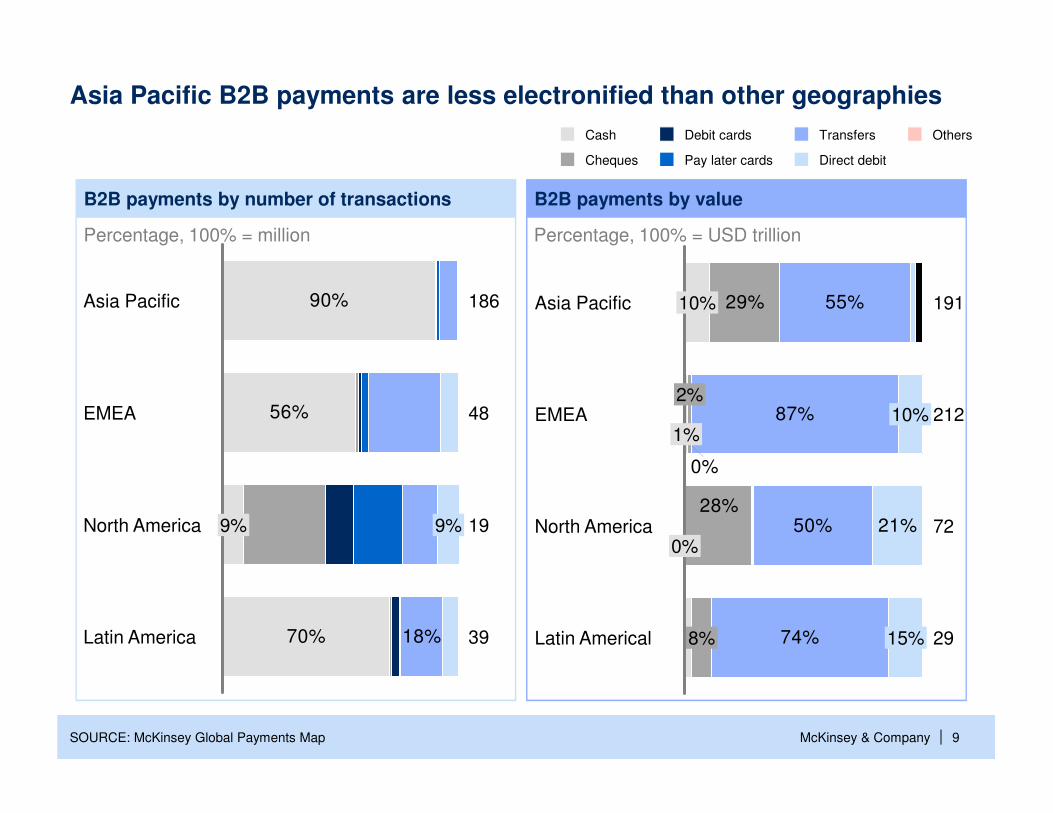

APAC, 2013OthersTransfers

Direct debitPay later cards

Debit cards1

Cheques

Cash

SOURCE: McKinsey Global Payments Map

Percentage, 100% = million Percentage, 100% = USD trillion

McKinsey & Company | 9

B2B payments by number of transactions B2B payments by value

Asia Pacific B2B payments are less electronified than other geographies

90%

56%

70% 18%Latin America 39

North America 199% 9%

EMEA 48

Asia Pacific 186 29% 55%

87%

50%

74%

28%

0%

21%

15%

10%

Latin Americal 298%

North America 720%

EMEA 2121%

2%

Asia Pacific 19110%

OthersTransfers

Direct debitPay later cards

Debit cards

Cheques

Cash

SOURCE: McKinsey Global Payments Map

Percentage, 100% = million Percentage, 100% = USD trillion

McKinsey & Company | 10

Commercial Payments in Asia-Pacific: Is this the New Opportunity?

▪ Overview of Commercial Payments in Asia-Pacific

▪ Roadblocks to success

▪ Changes impacting Commercial Payments landscape

▪ Way forward

Contents

McKinsey & Company | 11

Substantial opportunity to create value from “e”-nablement of billing

SOURCE: Fidesic; Ariba, OP Bank Group; Gartner Research; Certipost

€ per bill

3.0

4.5

No printing and enveloping costsFewer exceptionsE-archiving

Automatic data encodingFewer exceptionsE-archiving

Theoretical savings potential

B2C: €7.5

Biller Receiver

McKinsey & Company | 12

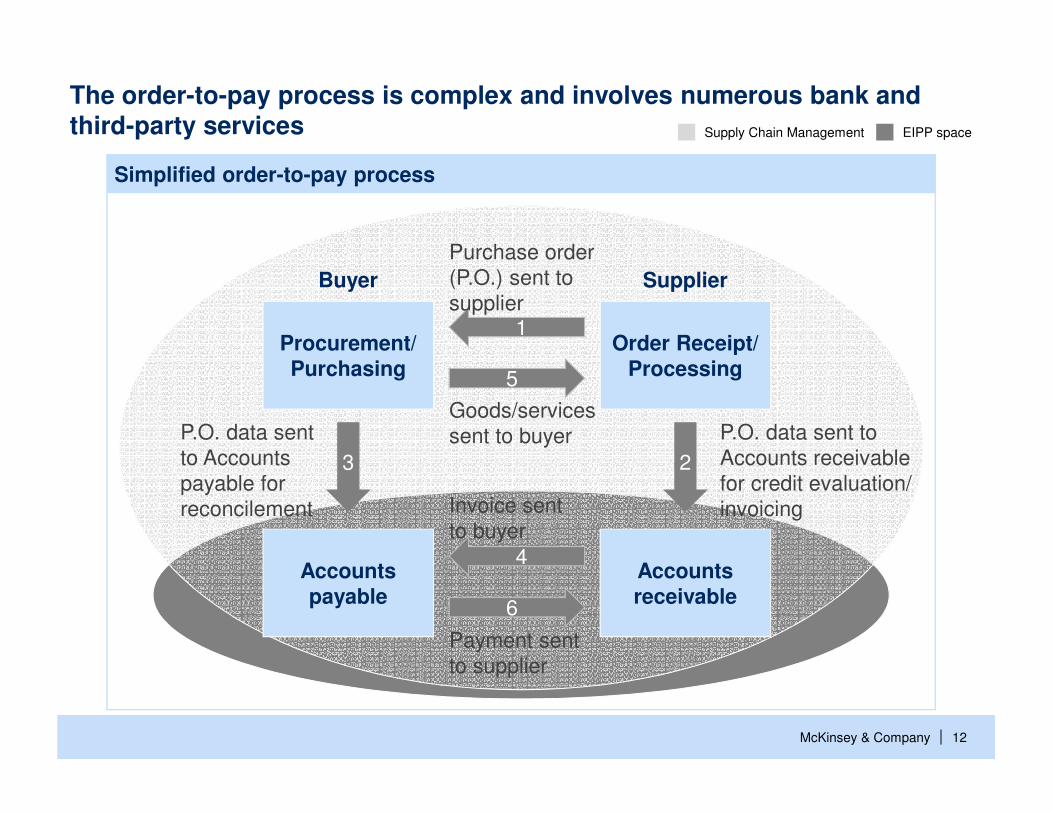

The order-to-pay process is complex and involves numerous bank and third-party services

Simplified order-to-pay process

Procurement/Purchasing

Accounts payable

Order Receipt/Processing

Accounts receivable

6

4

5

1

Buyer Supplier

3 2

Payment sent to supplier

Invoice sent to buyer

Goods/services sent to buyer

Purchase order (P.O.) sent to supplier

P.O. data sent to Accounts payable for reconcilement

P.O. data sent to Accounts receivable for credit evaluation/invoicing

Supply Chain Management EIPP space

McKinsey & Company | 13

… and client relationship life uplift of 30%

Transaction Banking continues to be very attractive for bankswith high relative returns and positive impact on client stickiness

5.3

2.3

CorporateBank

TransactionBank

9

7

With TB services

+29%

Credit onlyrelationship

Operating profit over RWA, % Years

2x higher relative returns on risk-weighted-assets…

McKinsey & Company | 14

5 key roadblocks in Commercial Payments

Lack of common standards and policy support to drive e-invoicing

1

Fragmented value chain for B2B automation2

Unclear revenue stream to replace loss of incumbent earnings

3

Significant informal SME economy4

Insufficient focus from leading players5

McKinsey & Company | 15

Commercial Payments in Asia-Pacific: Is this the New Opportunity?

▪ Overview of Commercial Payments in Asia-Pacific

▪ Roadblocks to success

▪ Changes impacting Commercial Payments landscape

▪ Way forward

Contents

McKinsey & Company | 16

We see 8 paradigm shifts that are impacting the Commercial Payments landscape

Improving customer willingness to use digital and alternative channels

1

Growth of Asia-linked trade and changing nature of businesses

2

Convergence of technologies, standards and 3rd

party platforms3

Digital @ the speed of thought – non-banking innovators are driving change

6

Increasing enablement by Governments8

Customers thinking ‘end-end’ – multi-platform, inter-operable and integrated solutions

4

Strengthened capabilities of local banks5

Adoption of big data & advanced analytics7

McKinsey & Company | 17SOURCE: World Bank, Strategy Analytics; IDC

In Emerging Asia, smartphone & internet penetration will exceed current bank account penetrations by 2018

% e-Commerce penetration, 2018

% Population with bank account, 2011

% Smartphone penetration, 2018

% Internet penetration, 2018

Indonesia 20 44

India 35 21

96 84Japan

73 34Thailand

64 60China

66 74Malaysia

Higher penetra-tion enables mobile solutions

Higher penetra-tion increases likelihood to purchase online

730

829

6774

1744

4375

3043

1

Penetration: Share of population using

McKinsey & Company | 18

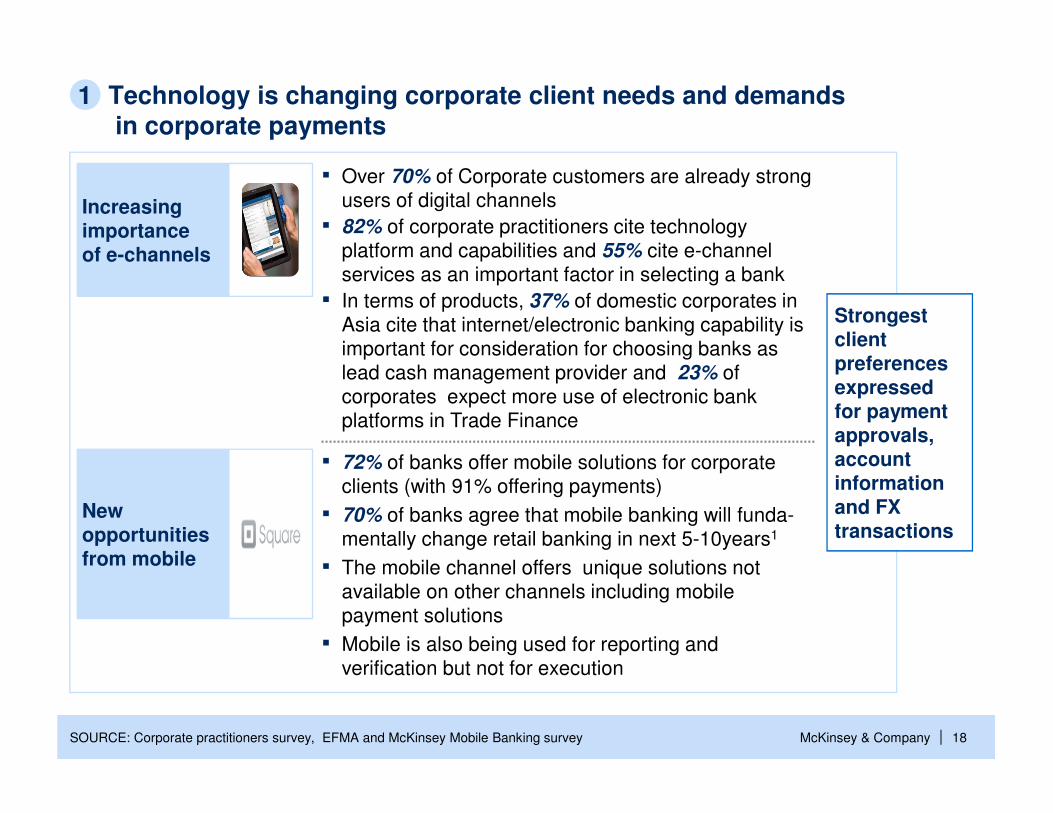

Technology is changing corporate client needs and demandsin corporate payments

SOURCE: Corporate practitioners survey, EFMA and McKinsey Mobile Banking survey

Increasing importance of e-channels

▪ Over 70% of Corporate customers are already strong users of digital channels

▪ 82% of corporate practitioners cite technology platform and capabilities and 55% cite e-channel services as an important factor in selecting a bank

▪ In terms of products, 37% of domestic corporates in Asia cite that internet/electronic banking capability is important for consideration for choosing banks as lead cash management provider and 23% of corporates expect more use of electronic bank platforms in Trade Finance

New opportunities from mobile

▪ 72% of banks offer mobile solutions for corporate clients (with 91% offering payments)

▪ 70% of banks agree that mobile banking will funda-mentally change retail banking in next 5-10years1

▪ The mobile channel offers unique solutions not available on other channels including mobile payment solutions

▪ Mobile is also being used for reporting and verification but not for execution

Strongest client preferences expressed for payment approvals, account information and FX transactions

1

McKinsey & Company | 19

SMEs are increasingly using digital channels and solutions

1 N = 750 SME customers in India; Interaction refers to any kind of contact with the bank, eg., doing transactions, gathering information, receiving advice, etc.

SOURCE: McKinsey BANCON survey 2013

2

8

8

9

17

21

Call Center

ATM

Mobile Banking

RM

Online Banking

Branch

Average number of interactions per customer per month across channels1

Digital Channels rapidly gaining in importance for SMEs

Accounting software penetration by segment , %

SMEs increasingly using ‘digital’ tools to facilitate business

80

60

25

Medium

Small

Micro

60-7015-20MYOB

Others

Sage

<55-10

AutoCount

▪ 25 touchpoints per month on digital channels▪ Branch & RMs remain important

▪ Roughly 200,000 SMEs are using Sage/UBS▪ Competition from small accounting software

such as Auto-Count and QnE is increasing

1

McKinsey & Company | 20

Incremental Asian cross-border trade likely to account for 57% of global growth over the next 5 yearsTotal cross-border trade flows (excl. services), growth 2013-2018F, US$ billions

SOURCE: IMF DOTS, McKinsey Global Payments Map

Trade > 5% of total/growth

Trade > 10% of total/growth Trade > 20% of total/growth

Trade < 5% of total/growth

Total cross-border trade flows (excl. services), growth 2013-2018F

… to

Africa

Oceania

Asia

Europe

Latin America

Middle East

North America

Africa Oceania Asia EuropeLatin America

Middle East

North America

2013 71 7 202 222 25 24 61

Growth 36 1 172 135 9 10 23

2013 6 21 224 20 4 12 16

Growth 2 5 118 11 2 3 3

2013 206 163 2,970 918 329 333 986

Growth 113 72 1,750 517 126 109 300

2013 215 58 883 4,713 193 343 522

Growth 66 8 501 2,037 64 132 64

2013 23 6 255 149 241 21 488

Growth 6 1 209 74 93 9 110

2013 59 10 734 209 16 125 127

Growth 29 1 584 102 7 77 34

2013 438 34 466 301 398 91 599

Growth 15 7 256 147 154 41 103

Trade flows from …

US$ billions

2

McKinsey & Company | 21

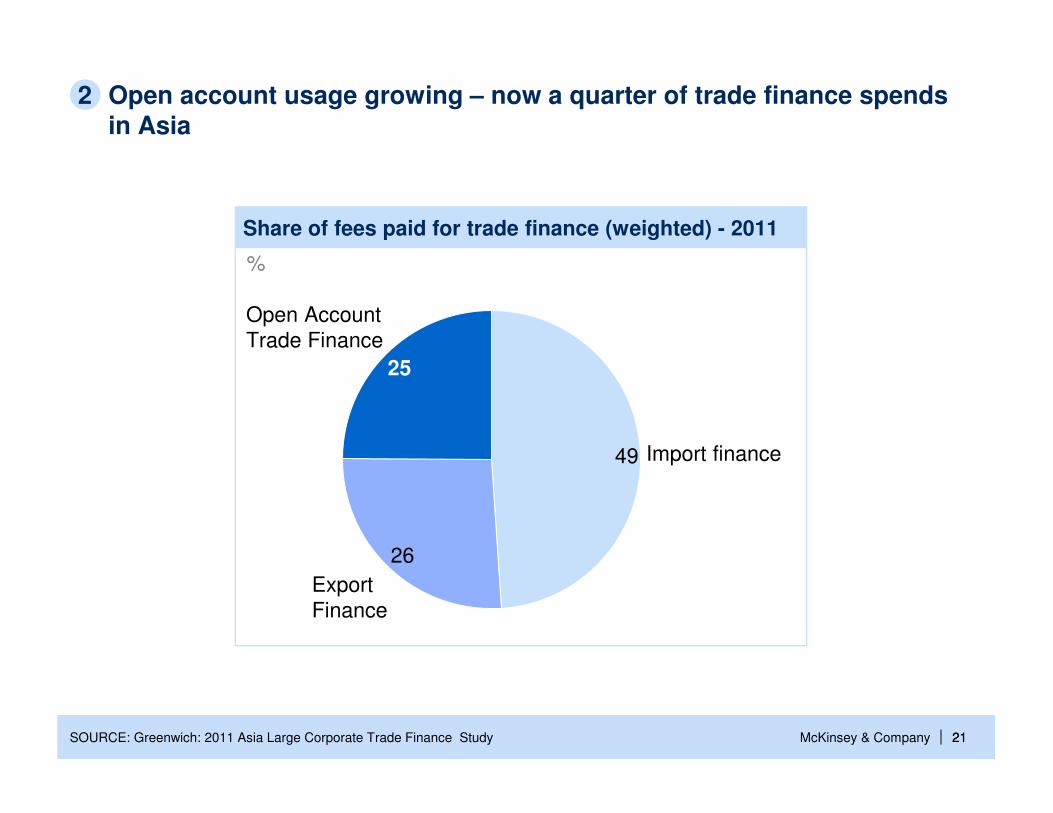

Open account usage growing – now a quarter of trade finance spends in Asia

SOURCE: Greenwich: 2011 Asia Large Corporate Trade Finance Study

Share of fees paid for trade finance (weighted) - 2011

%

Export Finance

Open AccountTrade Finance

25

26

Import finance49

21

2

McKinsey & Company | 22

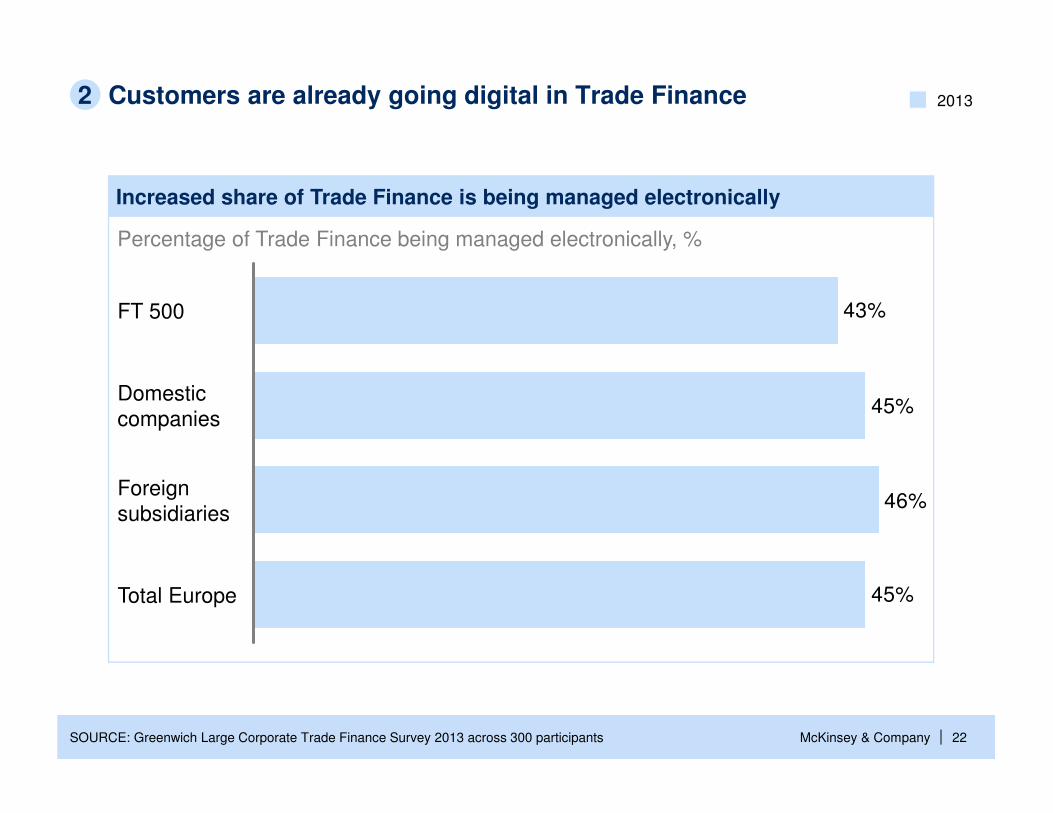

Customers are already going digital in Trade Finance

45%

45%

46%

43%FT 500

Domesticcompanies

Foreignsubsidiaries

Total Europe

Increased share of Trade Finance is being managed electronically

Percentage of Trade Finance being managed electronically, %

SOURCE: Greenwich Large Corporate Trade Finance Survey 2013 across 300 participants

20132

McKinsey & Company | 23

Increasing globalisation of supply chains

SOURCE: WTO, Research

China

2030

Emerging Market ex China

Developed Markets

60

2012

40

1990

20

Percent

Import contribution to global exports1

1 Value of imports in the goods exported - global average

2

Supply chains across industries continue to become more globalised

McKinsey & Company | 24

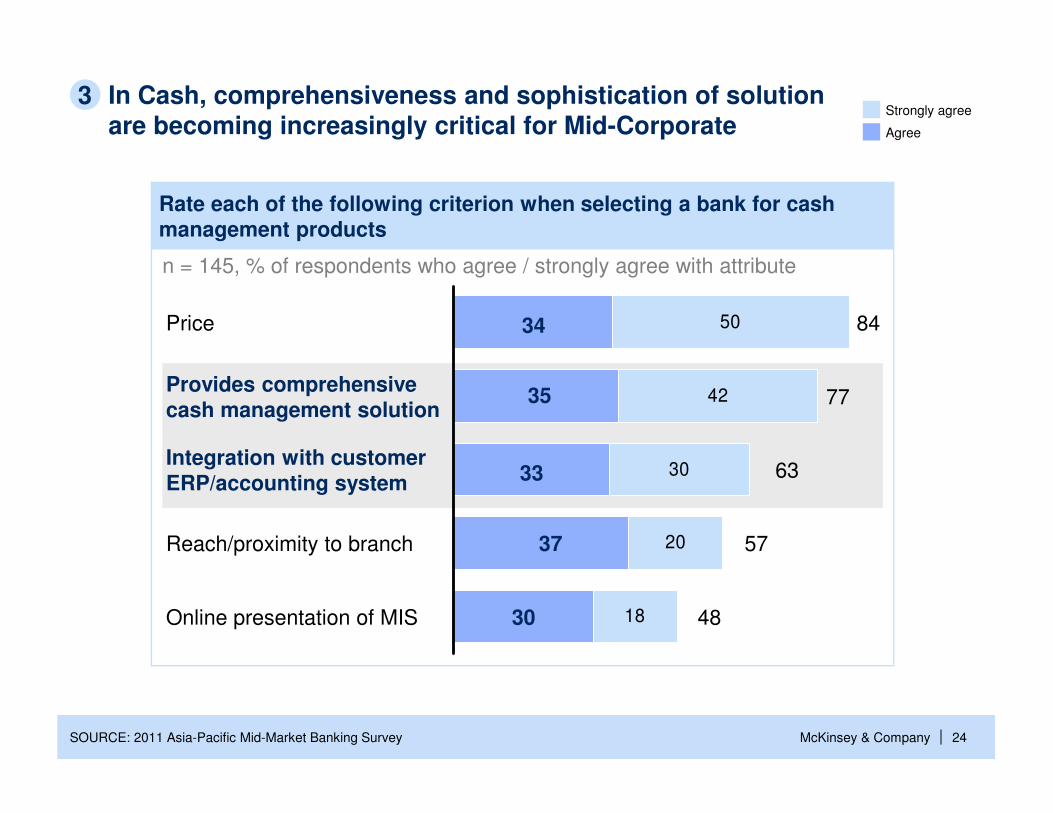

In Cash, comprehensiveness and sophistication of solutionare becoming increasingly critical for Mid-Corporate

n = 145, % of respondents who agree / strongly agree with attribute

![Contract Administration Activity 41: Administering ... · commercial financing [policy]. FAR 32.202-2 Types of payments for commercial item purchases. FAR 32.207 Administration and](https://static.documents.pub/doc/80x56/5fdcb5a9c2ff1d6b2e4c3fca/contract-administration-activity-41-administering-commercial-financing-policy.jpg)

![Pacific Commercial Advertiser. (Honolulu, HI) 1878-03-09 [p ]. · Haiku, Mali, February 23d, 1878. To the Editor of the Pacific Commercial Advertiser: Dear Sir: I bare tbe pleasure](https://static.documents.pub/doc/80x56/60be80193ef8237243479d1f/pacific-commercial-advertiser-honolulu-hi-1878-03-09-p-haiku-mali-february.jpg)