COMMONWEALTH ASSOCIATION FOR CORPORATE GOVERNANCE DRAFT (2) CACG GUIDELINES Corporate Governance in Government Companies BEST PRACTICE GUIDE NO. 3 - June 2002 Sponsored by: Commonwealth Secretariat Shell International Institute of Chartered Secretaries and Administrators

Transcript

COMMONWEALTH ASSOCIATION FOR

CORPORATE GOVERNANCE

DRAFT (2)

CACG GUIDELINES

Corporate Governance in

Government Companies

BEST PRACTICE GUIDE NO. 3 - June 2002

Sponsored by:

Commonwealth Secretariat Shell International

Institute of Chartered Secretaries and Administrators

Commonwealth Association for Corporate Governance

President

Dato Mohammed Azlan Hashim

Chair

Ms Jyoti Munsiff

Chief Executive

Lt Col Geoffrey Bowes MNZM

Council Members

John Ainsworth (United Kingdom) Philip Armstrong (South Africa) Winston Cox (Deputy Secretary General Commonwealth Secretariat) Marcelo Mackinlay (Canada) Richard Nottage (New Zealand) Gamini Wijeyesinghe (Sri Lanka)

Honorary Secretary

Ms Caroline Phillips

Executive Assistant

Gillian Edwards

CACG is a non-profit organisation incorporated under the Incorporated Societies Act, 1908 of New Zealand.

The CACG is extremely grateful for the contributions of Professor Y.R.K. Reddy of India, The Crown Company Monitoring Advisory Unit in New Zealand, Ron Hamilton and the Australian National Audit Office for the generous permission to use, and reproduce, their extensive material on the monitoring of boards and directors of Government Companies. Readers are reminded of the copyright restrictions which vest in the contributors of the material which have been reproduced, with permission, in this latest series of Best Practice Guides issued by the CACG.

Sponsors

Shell International New Zealand Government – Ministry of Foreign Affairs and Trade

Institute of Chartered Secretaries and Administrators – United Kingdom

Members

Caroline Philips, United Kingdom Davis Global Advisors Inc, United States of America

Duntroon Associates, New Zealand Gillian Edwards, New Zealand

Growth International, United Kingdom Huria Associates, New Zealand

Justice Awuku –Sao, Ghana Maswill Limited, United Kingdom

Mervyn King, South Africa Philip Armstrong, South Africa Priam (Pty) Limited, Australia

Research Institute of Investment Analysis, Malaysia Ron Hamilton, New Zealand

Securicor plc, United Kingdom South African Reinsurance Limited

Stephen Tiley, South Africa Sunderland Business School, United Kingdom

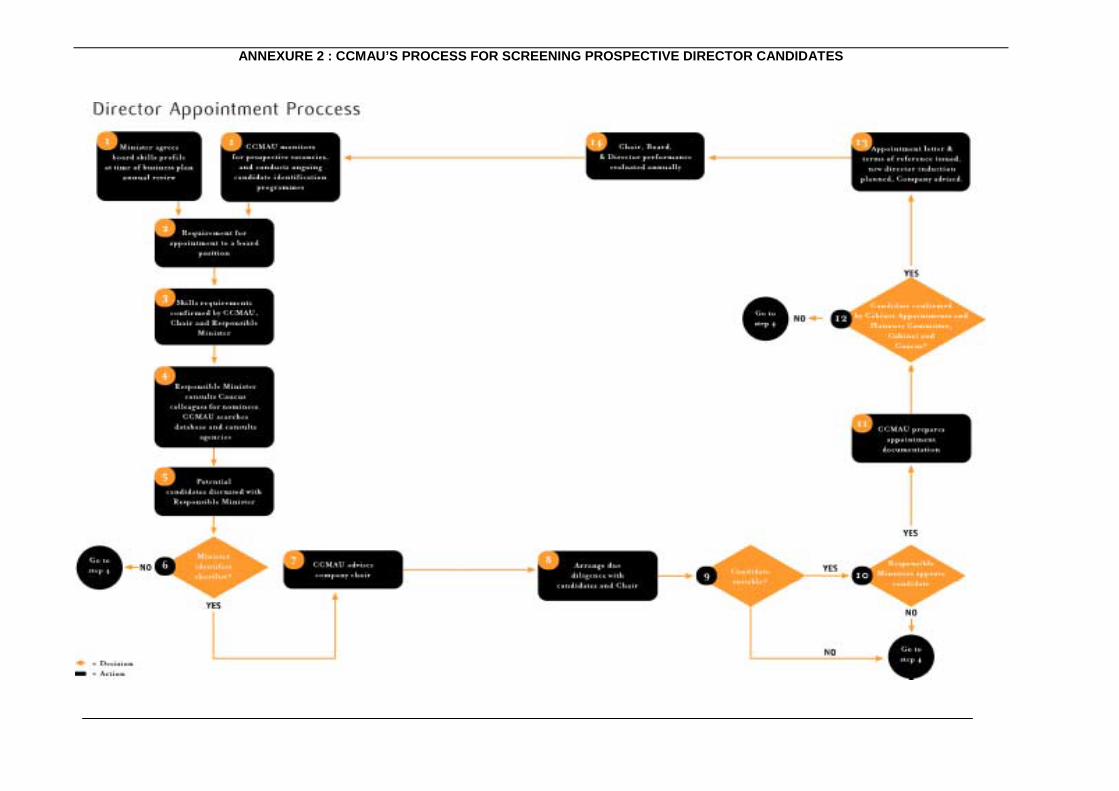

Times Media Limited, South Africa Vishnu Ramlogan, Spain Prof. Y.R.K. Reddy, India

Affiliates

Academy of Corporate Governance - India Australian Institute of Company Directors

Caribbean Management Development Association, Barbados Chartered Institute of Company Secretaries in Australia

Chartered Institute of Corporate Management, New Zealand Fiji Institute of Directors

Global Corporate Governance Research Center, United States of America Institute of Chartered Secretaries and Administrators, United Kingdom

Institute of Chartered Secretaries and Administrators in Zimbabwe Institute of Corporate Governance of Uganda

Institute of Directors in New Zealand Institute of Directors in Southern Africa

Institute of Directors in Zimbabwe Institute of Directors of Zambia

Institute of Directors, Ghana Institute of Directors, United Kingdom

Institute of Company Directors, Papua New Guinea Institute for Southern Africa Development

Investor Responsibility Research Center, United States of America Lusaka Stock Exchange, Zambia

Malaysian Association of the Institute of Chartered Secretaries and Administrators Malaysian Institute of Corporate Governance

National Association for Corporate Directors, United States of America Private Sector Corporate Governance Trust, Kenya

Private Sector Organisation of Jamaica Securities and Exchange Commission of Zambia

Strategic Management Centre, Nigeria The Centre for Tomorrow’s Company, United Kingdom

The Hong Kong Institute of Directors Limited

Affiliates Continued

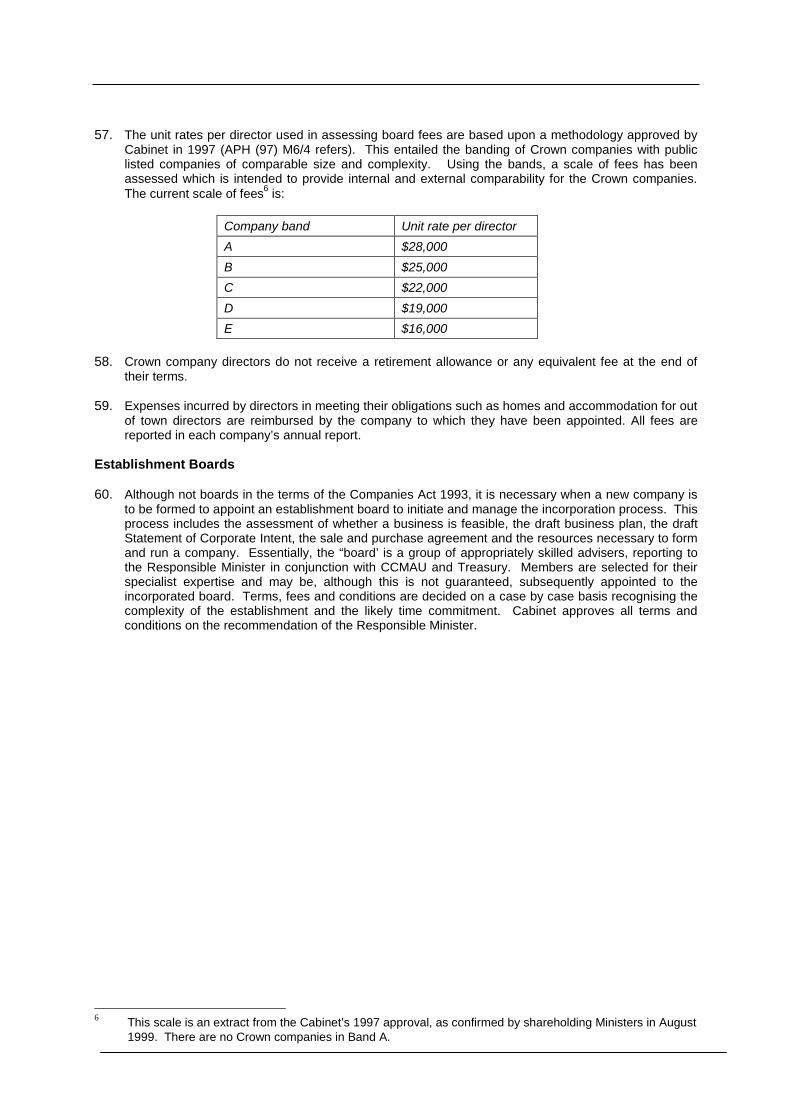

The Institute of Chartered Secretaries and Administrators in Sri Lanka

The Institute of Corporate Directors, Canada The Singapore Association of the Institute of Chartered Secretaries and Administrators

The Southern African Institute of Chartered Secretaries and Administrators The Society of Accountants in Malawi

Interested Party

The Commonwealth Secretariat

Monitoring of Boards and Directors in Government Companies

Table of Contents

Preface

Conceptual Framework of Primary Principles

The First Principles of Corporate Governance for Public Enterprises in India

Annexure

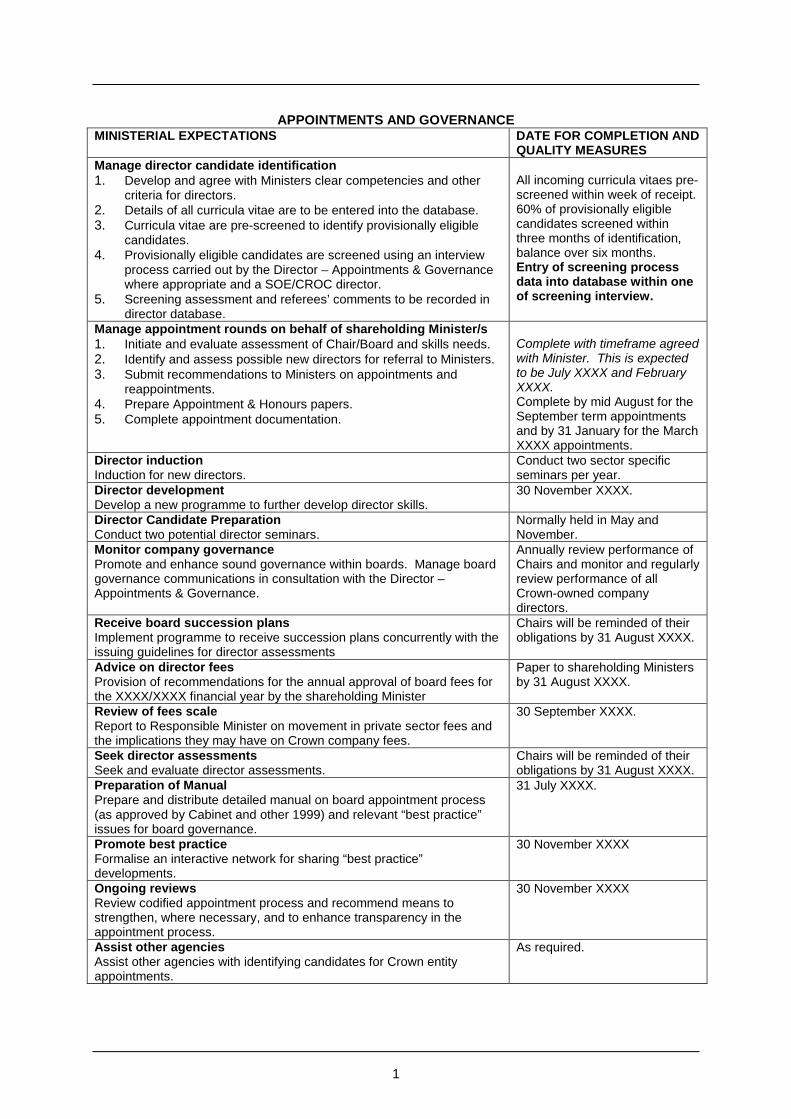

The Crown Company Board Appointment Process, New Zealand

Annex 1 - Codification of the Appointment Process

Annex 2 - Process of Screening Prospective Director Candidates

Annex 3 - Conflict of Interest Letters

Monitoring Government Companies

Annex 1 - Monitoring Vehicles

Annex 2 - Purchase Agreement

Principles and Better Practices for Corporate Governance in Commonwealth Authorities and Companies, Australia

i

Preface Introduction The relentless advance of globalisation of economies has forced formerly protected industries to compete with the most efficient companies in the world. Globalisation has put pressure on state-owned enterprises to restructure along more business-like lines and adopt international standards of good corporate governance in order to compete for scarce investment capital. State-owned enterprises are now expected to make profits and private companies are increasingly conscious of their social responsibilities. Multi-lateral lenders like the International Monetary Fund, as well as international institutional shareholders, take good corporate governance into account when making investment or lending decisions. This is one of the reasons good governance is a business issue which has to have the support of government. Weak governance is generally associated with slow and sometimes regressive, economic development; while improved governance promotes development success, and is a precursor to the possibility of international capital investment especially in the course of privatisation initiatives. In the 21st Century, state-owned enterprises which encourage market incentives will result in an improvement in the quantity and quality of services provided to communities. The process of change is always difficult, particularly when it involves a change in culture. The bureaucracy of government and the legacy of a culture driven by traditional business values make the principles of corporate governance difficult to implement. However, transparency, disclosure and accountability are even more important in the public sector because government holds a position of trust in these enterprises and is accountable to taxpayers and its citizens for the proper and efficient use of their money and utilisation of national assets. State Enterprises and Corporate Governance State enterprises must operate within the overall policy framework set by government. However, this requires difficult choices because government’s political objectives may be different from the commercial interest of the state enterprise. As a shareholder, the state has a responsibility to enhance the value of its assets. This may conflict with a need to provide services to the poor. Accordingly, the objectives of both government and state enterprises needs to be very definite to ensure that the most appropriate trade-offs are made. The roles and objectives of boards must also be clearly articulated and aligned with government’s objectives and to separate the operational and fiduciary responsibilities of the board. A particular problem of state enterprises is that government often delegates its responsibilities to one Minister. One individual acting as the interface between the shareholder and the board then wields an enormous amount of power. This can result in the relationship between the responsible Minister and the board being personality driven and vulnerable to political agendas which may not be in the best commercial interests of the state enterprise. Many governments view privatising as a means of realising capital for the economy and generating greater commercial by placing state assets in the hands of the private sector. Government still retains a minority share in industries which would not be able to survive without a government subsidy, or in order to maintain a level of control to ensure that the social objectives of such entities are not entirely compromised. This in itself presents difficulties or conflicts that need to be carefully managed. One way to achieve this, is to ensure that recognised practices and procedures of good governance are established in the enterprise, which encourage the required levels of accountability and responsibility in attaining the policy objectives of government and commercial imperatives of an efficiently utilised asset. Best Practice in Government Owned Companies and Authorities This Best Practice Guide contains case studies of the problems, processes and recommended practices in state enterprises in India, New Zealand and Australia. The intention is that these examples will be both thought provoking and helpful to Commonwealth countries. It is recommended that these case studies be read in conjunction with the CACG Guidelines on Boards and Directors, Best Practice Guide No 2 of August

ii

2000, as the corporate governance issues in that document apply equally to the private sector and state-owned enterprises. The intention is to provide Commonwealth countries with the opportunity to take the best corporate governance practices available and adapt them to their own needs and circumstances Geoffrey T. Bowes MNZM Philip A. Armstrong Chief Executive Special Advisor to the CACG

February 2002

The CACG Guidelines may be found on the following websites: http://www.cacg-inc.com http://www.cbc.to, http://www.combinet.net,

General Government Companies are any entities that are owned either partly or wholly by the government of the country. They may well be called Public Enterprises, Government Companies, State Owned Enterprises or Parastatils etc., so long as they are registered under the Companies Act or some similar Act. This document applies to all such entities. Governance of a government company is no different from that of a private sector company in terms of executing the duties of director, individually or collectively. For this reason, the Principles laid out in “CACG Guidelines – Principles for Corporate Governance in the Commonwealth”, should be read and adapted in conjunction with that laid out hereunder. The major difference between the private and public sector company lies in the relationship and covenants between the shareholders, usually Ministers, and the board. Where these are obscure and or obtuse, then it is highly probable that the government company will not maximise its potential and/or not provide an adequate return to the country. It is recommended that in drafting a Code of Best Practice for Government Companies those doing so first look to the “CACG Guidelines – Principles for Corporate Governance in the Commonwealth” and also consider the principles laid out hereunder. Tenet 1 – DUTY It should be clearly stated where the director’s prime duty lies. In the private sector, the law in most countries states that the first duty of any director is to the company. In government companies it may well be to the Minister(s) who in turn are accountable to Parliament. It can be argued that Parliament is but a fiduciary for the citizens of the country and that the assets of such companies are not the Government’s assets but rather the assets of the people. Hence, any diminution of these assets by politicians could lead to legal action by the citizens. No matter what applies, the first or primary duty should be clearly stated and supported by legislation. Tenet 2 – LAW It should be clearly stated as to what the relevant laws are that apply to directors germane to the governance of government companies. Government companies have tended to be established under a number of Acts. CACG recommends, if this is possible, that one Act covers all matters related to the governance of Government Companies. This should include the local Companies Act. Tenet 3 – MONITORING There should be a clear statement as to what agency(ies) will be responsible for monitoring the performance of the government companies on behalf of the shareholder(s), complete with its (their) Terms of Reference. In government companies the shareholder is usually a Minister(s) of the Government and they will require and indeed should get advice on the performance and governance of their companies. CACG recommends one centralised Monitoring Unit, which is suitably staffed by officials or contractors, who have the required experience and background to provide all the necessary advice to the Shareholding Minister(s). Experience has shown that such a Unit should be independent of any other branches of the government. In the statement on Monitoring mention should also be made of any other monitoring that could be in place – e.g. Select Committees. Tenet 4 – CONTRACT There should be a clear statement as to how contracts, between the Shareholder(s) and the Boards of Directors are negotiated and signed off regarding the objectives and outcomes that the company is to deliver. Any uneconomic arrangements in such contracts should be declared and transparent. CACG recommends that contracts and Statements of Corporate Intent (sanitised public document) should be negotiated annually, initially with the Monitoring Unit and then with the Shareholder(s) and that they

2

clearly lay out what is expected to be delivered by the company in the following year. Once this is done the Board should be left to implement the expected delivery. In the event that Shareholder(s) want to make variations to such agreements, then these variations should be subject to negotiation and an amended Statement of Corporate Intent be produced and signed off. Tenet 5 – APPOINTMENTS There should be a statement on how the appointments process for directors will operate in government companies. CACG recommends that advice to the shareholder(s) should be given by the Monitoring Unit, and that the process is transparent and ensures that appointments are made on merit, not for political reasons. Such appointees will be independent directors, not have conflicts of interest and not be allowed to appoint alternates. Appointments should be for a specific term but the Shareholder(s) should have enshrined rights on termination for lack of performance and this should all be contained in a letter of appointment. Where a replacement director is being sought the Chairman of that company should be consulted. CACG believes that there is merit in having a Commissioner of Appointments who can comment, if necessary, on all such appointments in public. Tenet 6 – REPORTING Any Code should contain details on what reporting is required and to who, by the Board. CACG recommends that such reporting should be through the Monitoring Unit and that such reports allow for a full evaluation of the performance of the company against agreed objectives. It is suggested that this should be done monthly. Tenet 7 – EVALUATION There should be a clear statement as to how the directors, collectively and individually, will be evaluated on their performance germane to directing the company. CACG recommends that this should be a peer review for individuals and be undertaken annually. For review of the Board as a whole collective, there may be merit in using an external facilitator. The objective all such evaluations is to improve performance. Where performance needs to be improved, the board should be proactive in providing education and information. The Chairman must be included in this review. Tenet 8 – REMUNERATION Remuneration is always a contentious issue and hence the Code should contain a statement on how remuneration of directors is set. CACG recommends that it should be done by the Shareholder(s) based on advice from the Monitoring Unit, who will in turn have consulted the board and cross referenced the fees with similar entities in the private sector. Tenet 9 – CHAIRMEN * A clear statement should be made as to how Chairmen are appointed and for what period. CACG recommends that Chairmen should annually be required to seek a vote of confidence from their fellow board members. The Chairman is the leader of the board, the conduit to the Shareholder(s) and Monitoring Unit, accountable to the Shareholder(s) and the spokesperson for the Company on matters that impact on the Shareholder(s) or the future direction of the Company. * either gender. Tenet 10 – CHIEF EXECUTIVE The Chief Executive must be appointed by and responsible to the board only for the duties that the board has delegated to him or her. Experience has shown that where the Chief Executive has responsibilities or direct access to either the politicians or bureaucrats there can be major problems. This must be clearly stated in any Code.

The First Principles of Corporate Governance for Public Enterprises in India

by

Prof. Y. R. K. Reddy

Reprinted with kind permission of Prof. Y.R.K Reddy

Preface 2 PART I 1. Background 3 2. The State and State Controlled Enterprises 5 PART II 3. Board Structure and Control Dynamics – A Factual Position of

Central Public Sector Undertakings 8

PART III 4. The First Principles 11 Annexure Recommendations of 1997 Report on

“Corporate Governance and PSUs” 15

2

Preface India’s progress in public enterprise reform has been admittedly modest. The familiar issues of multiple roles of the Government, the agency problem, contractual incompleteness, and information asymmetry continue to affect adversely the potential of this sector. Yet the public enterprises will continue to dominate the economy for several years to come. It is inappropriate to believe that the argument of public vs. private has been settled conclusively so as to imply the gradual disappearance of the state owned enterprise. Despite the notable fatigue and cynicism that has set in, the reality is that Indian public enterprises need reform both in policy conditions and the internal structures and processes. The popular codes and principles on Corporate Governance are, in most parts, relevant to public enterprises. At the same time, they appear incomplete, as they have not addressed the special features of governmental control systems, which impinge on the quality of governance. I had occasion to raise the critical diversities in the governance systems of the widely held private firms and the state owned enterprises in the Commonwealth and the need to develop a more relevant set of principles for the latter. The SCOPE had commissioned a study in 1997 on this issue and had suggested in October 2000 that we prepare a document afresh for wider discussion. This report is the outcome of the initiative of the then Secretary-General of SCOPE and the subsequent support lent by the Forum for Policy Promotion, Hyderabad. The report uses a wide framework for the definition of public enterprises covering state level and central level companies; statutory bodies; Government trusts; departmental undertakings and state controlled co-operatives. The objective of the report is however, limited to: “Developing an approach and the first principles for improving the conditions for good corporate governance in public enterprises in India”. I recognize the difficulty in implementation of several of the first principles. This is indeed the case with any type of principles. Yet, there is need to build consensus on the non-negotiability of a few foundations on which the edifice of good governance in PEs can be built. The report discusses in Part – I the special features of the state controlled enterprises. In Part - II, the central public sector undertakings have been paid closer attention by debating the typical structure of the board, the process of decision-making and dynamics of control in them. This will help in assessing the major infirmities in policy and legal conditions, that affect the quality of corporate governance in the most visible and sizeable segment of public enterprises, which are in competition with private sector players. Part - III contains the First Principles with brief annotations. I have benefited greatly from interactions with international specialists and several documents of the Commonwealth Association for Corporate Governance. I also acknowledge with gratitude the comments and helpful suggestions on an earlier draft, from several friends, policy makers and academics. October 2001 Y.R.K. Reddy

3

PART – I

1. BACKGROUND

1.1. Corporate Governance has reached centre-stage in the global agenda. The principles and codes that have evolved in several countries have furthered the cause of efficiency, transparency and equity particularly in the interest of the shareholders. Sustainable shareholder value has become the mantra for corporate immortality translating into the welfare of the society.

1.2. The debate and effort in the arena of corporate governance has been tilted mostly in favour

of publicly listed and widely held companies. It is possible that three factors have determined this inclination in the debate on corporate governance so far. First was the study of Berle and Means, which referred to the shifting of control when a company’s ownership is dispersed. The idea underscored the need to create and activate structures and processes by which the owners can ensure appropriate governance and management. The problem identified was not of efficiency of capital in itself or of ownership, but the possible divergence of interests between management and the dispersed owner (or some ownership vis-à-vis the rest). The influence of this study on subsequent principles and codes is evident from the arguments for separation of the position of the Chairman from that of the Chief Executive and for induction of independent directors.

1.3. The second factor is the Cadbury Committee’s report, which has been widely acclaimed

and emulated despite its limited set of terms of reference. The London Stock Exchange constituted the committee. The report dealt with the financial issues of the publicly listed companies in the London Stock Exchange. The Cadbury code addressed the prominent concerns of corporate failures and became the mother of all codes in several ways. Most other capital markets and their regulators adopted similar recommendations, albeit, given by locally appointed committees and commissions. The effort, in sum, appears to be towards more efficient regulation through amendments to listing agreements and company laws as well as updated standards of accounting, reporting and disclosures. A comprehensive solution to the Berle and Means propositions appears to have been found through changes in board structures, processes, shareholder rights, reporting, disclosure standards and legal remedies.

1.4. The third factor has been the hope of market efficiency as an ultimate solution to corporate

conduct and performance. This implied the creation of a market for control of the company and freely entering and exiting owners who made their decisions on the basis of returns. This factor, which has been experiencing a long and bullish run, implies aggressive corporatisation, privatisation and undiluted focus on shareholder value.

1.5. These three factors have influenced the environment for good corporate governance in the

developed world where capital markets are vibrant. The codes and principles derived from this experience appear to be influencing developing countries in terms of sensitisation to the need for good governance. This is particularly so in countries where capital markets are expanding quickly. In the process, however, major business/commercial segments of the economies in the developing world are not covered by a corporate governance regulatory net or have found the principles less rewarding in practice. These are agencies, which carry out commercial activities, but operate under the control of government and are as such, incorporated public enterprises. In these economies, public enterprises, listed and unlisted, dominate over the private sector listed companies in terms of contribution to GDP, capital employed, income, employee strength, social impact and possibly, as is being asserted lately, in profitability.

1.6. The Standing Conference of Public Enterprises (SCOPE), New Delhi, recognised in 1996,

the need to examine the corporate governance issues relevant to the public sector undertakings in India i.e. those companies in which central government has equity of 51% and above. It was recognised that the codes, which were referred to (Cadbury’s and the Confederation of Indian Industry’s at that time), were most appropriate to the private sector and that the infirmities in the public enterprise governance needed a devoted attention. An attempt was made to address the special conditions of the central public sector undertakings, which are also publicly listed and traded on the stock exchanges and Yaga

4

Consulting prepared a report titled “Corporate Governance and the Public Sector Undertaking” in October, 1997 (see Annexure).

1.7. The report, derived from the perspectives of several industry leaders and academicians,

highlighted a multitude of issues and recommendations to improve the quality of corporate governance. It was made prior to the Kumar Mangalam Birla Committee report and the changes effected by the Securities and Exchange Board of India in its listing agreements. The Kumar Mangalam Birla Committee report, like the Cadbury Committee, had limited its perspective to the typical private sector company – the composition of the committee reflects the tilt to this sector. Subsequent developments also affirm this limitation. (For instance, the dangers were not noted of separation of the positions of Chairman and Chief Executive in the case of public enterprises. Such a separation has proved to be an incentive for political leaders to get nominated by the Government as independent Chairmen. Further, in the interpretation of independence, the Securities and Exchange Board of India preferred to treat, by a separate clarification, nominees of Financial Institutions/Foreign Institutional Investors as independent even though they are equity holders. However, the civil servants who are government nominees in public enterprises by virtue of government’s ownership are not considered on the same footing.)

1.8. Besides the central public undertakings, there are several other entities – the state level

public enterprises, state controlled co-operatives, organisations created by special statutes, joint ventures of state and central governments, departmental undertakings, companies promoted by developmental financial institutions of the government and the like, which are currently in commercial activities or are pursuing potentially commercial objectives. All these public enterprises have a greater potential impact on society than the private sector due to the higher degree of ripple effect. In the developing world, the returns from good corporate governance in these enterprises should exceed those in the private fold. Obviously, there is a strong interface between good governance and corporate governance in the context of public enterprises as the latter are often used and perceived as instruments of public policy.

1.9. It is against this backdrop that the need for a special perspective was recognised and a

request made by the then Secretary General, Standing Conference of Public Enterprises, New Delhi, to Yaga Consulting to prepare a note with the objective of:

“Developing an approach and the first principles for improving the conditions for good corporate governance in public enterprises in India”.

The term “Public Enterprise” here has the broad international meaning covering various types of state owned/controlled enterprises. The listed and the unlisted government companies, the central and the state level corporations, public sector banks, insurance and Fls, co-operatives and department undertakings are included in the term. The principles, if accepted, will obviously imply several operational difficulties, pulls, pressures and dilemmas. However, the attempt is to identify and gain consensus on the pillars for good corporate governance without being daunted by potential controversies or operational barriers. Though this report is specific to India, the principles may be of relevance to several developing countries. These would also reflect and reinforce the Commonwealth Association on Corporate Governance Guidelines, which adopted an inclusive approach, relevant to the developing world and the OECD principles, which mirror the long-term vision of active, transparent, accountable and efficient markets.

1.10. The report discusses in Part - I the special features of the state-controlled enterprises. In

Part - II, the central public sector undertakings have been highlighted for closer attention by debating the typical structure of the board, the process of decision-making and the dynamics of control. This will help in assessing the major infirmities in external conditions that impinge on the quality of corporate governance in one of the most visible and sizeable segments of public enterprises, which are in competition with private sector players. Part - III contains the First Principles with brief annotations.

5

2. THE STATE AND THE STATE CONTROLLED ENTERPRISES

2.1. There has been an universal belief that the government must restructure its activities and create market-related incentives and discipline for the enterprises in its control. Thus, corporatisation of state undertakings and privatisation have emerged as the most important methods of improving the efficiency of both the State and the corporate entities. Consequently, governments have been announcing the sale of several companies, reducing their stake in the existing public enterprises and restructuring Government Departments to become companies. In the case of co-operatives, the Indian government has sought to amend the law to enable them to become companies. Further, international bodies have been advising / pressurising governments to gradually eliminate subsidies, remove administered price mechanisms and reduce such other controls/support which contribute to false/artificial pricing and costs. The alternative, it is asserted, would perpetuate a moral hazard for the government - inefficiency in operations and management and a weak monitoring system. There is increasing convergence of thinking world-wide that:

! Commercial activities should be undertaken by the State;

! There should be a clear set of commercial/financially sustainable objectives without

cluttering social objectives; and

! Market related incentives and discipline including the market for corporate control would be necessary for sustainable economic management and development.

2.2. The framework for the principles of corporate governance has emanated from such a

“world-view” and with the objective of creating efficient and transparent markets with widely held private ownership. Understandably, codes and principles in different countries have tended to support the view that all enterprises will be of one variety only despite the caution that “one size doesn’t fit all”. Thus, public enterprises have been treated in the same manner as the private, either with the assumption that what is good for one is good for the other, or on the premise that eventually all enterprises should be free of dominant ownership by the government.

2.3. The assumption of free markets with widely held private enterprises could be insufficient at

present for four reasons:

! During the process of economic reform, several government departments will need to be corporatised and yet be under government control, at least in the initial stages. This process will be a continuous one as a State may declare one of its activities as detachable enough from the sovereign function to merit corporatisation. (For example: the Department of Telecommunications, which has been corporatised as Bharat Sanchar Nigam Limited). Until this process stops, we will continue to have State-owned enterprises which may not necessarily have the ideal market related incentives and disincentives, at least in the short term. Concurrently, there will be several statutory organisations, which might be considered as strategic/sensitive and hence not meant for privatisation at all for some years. (Ordinance factories, Nuclear Fuel Complex, Universities, Port Trusts).

! The second reason arises from the possibility of transitional control by the

government until a new set of active owners emerges. Such control by the government may be a fall back option in case of inefficient new owners or because the capital markets have not become mature enough to generate active shareholder monitoring, which would make a positive impact on managerial efficiency. The “golden share” approach adopted in some countries as an interim mechanism signifies the existence of a transitory position for the company before the ideal market conditions emerge.

The process of privatisation may ensure transferring property rights to new owners who may be from the general public, employees, other institutions and corporate entities. However, mere transfer of property rights does not ensure that the goals of privatisation have been attained. Sound corporate governance structures and processes need to be established and sustained during the transition period. In the

6

absence of a better governance system and process, including more active and vigilant shareholders, the goals of privatisation would not be met. Thus the government may have to continue a direct control or indirect monitoring of those companies which are in the process of privatisation till conditions emerge requiring withdrawal of direct and other contingent controls and contractual obligations. (The recent penal action against the Sterlite Group by the SEBI after the government concluded the sale of its equity in Bharat Aluminium Company Limited, has raised an important issue – that of discovery of “corporate turpitude” or criminality before and after the sale of public stake to a private firm and the role of the government in such situations. There are possibilities now of contingent controls that were not envisaged earlier).

! Thirdly, and relatedly, it has been observed that in several countries, the privatisation

process resulted in transferring the property rights to parties, which are less efficient and/or less honest than the government’s previous “agents”. Such new owners may have failed in meeting the long-term goals of divestment/dis-investment/sale and may have created conditions that force governments to re-nationalise or take control. (Jute industry in Bangladesh is reportedly an example).

! Fourthly, there could be a realignment of the equity structure over a period of time in

joint ventures between public and private enterprises whereby the public enterprise gains control over the management. Such a change in capital structure may be rare and not a prospect that government prefers. (For example: the reported move of the public enterprise Hindustan Petroleum Corporation Limited to purchase the equity of the house of Birlas in the joint venture Mangalore Refineries and Petrochemicals Limited and take control of the management as the Birlas are unable to invest further monies required). Similarly, a public enterprise may acquire a private firm or another public enterprise or a government-controlled co-operative.

2.4. Thus, despite the idealism and merit of free market economy, with appropriate incentive

and disincentive mechanisms, there is a prospect of continued presence of public enterprises in India, in a large measure and for several years to come. The “Third Way”, between the unfashionable socialism and the romantic market fundamentalism may rest on such a prospect.

2.5. The range of public enterprises is vast and government’s control varies depending on

whether the entity is a departmental undertaking (like the Railways in the central government); a state enterprise (e.g. Hyderabad Allwyn); a central public sector undertaking (like the Indian Oil Corporation or BHEL); a statutory body at the central or state level (e.g. Unit Trust of India and the State Finance Corporations); a public sector bank (e.g. the State Bank of India which was created by law and in which the regulator also has ownership); a government controlled co-operative where the de-jure position is countered by the de-facto control (e.g. Indian Farmers Fertilisers Co-operative Sugar Factories).

2.6. The departmental undertakings are government and in competition directly or otherwise for

market share. The railways, post & telegraph and telecommunications are a case in point. To the extent that they are businesses and have the characteristics to be separated and made corporations under the company law, these may be deemed as public enterprise to which the general principles of corporate governance apply. In the case of statutory bodies, it is evident that several provisions of special authorities, accountabilities and Board structures are inconsistent with principles of corporate governance. The incongruence becomes glaring where public holds some part of the equity of such corporations. Similar is the context of the central public sector undertakings and the Banks where the special rights and privileges for one owner, even if it is Government, agitate against the tenets of equitable shareholder rights, under the principles of corporate governance. The co-operative sector which is expected to thrive on the basis of voluntarism reflects yet another spectre of government exercising de-facto control, thus eroding the right of self-governance to the members.

2.7. The government’s control system reflects, inter alia, the inherent conflict of roles of the

State – as a regulator, owner, adjudicator and executive – and the divergence in applying the principles of corporate governance amongst the different entities and at different levels

7

of ownership. The multiplicity and ambiguity of roles has helped the State in using public enterprises as agents of political interest rather than public policy. Subsidy to consumers or targeted sections at the cost of the public enterprise, special grants and bail-out packages, have offered reasons, even if misplaced, for continued special controls and rights.

2.8. The infirmities in governance architecture in the case of public enterprises appears to arise

mainly from:

! The current powers to create, develop, renew and restructure the governing board and its members and their variance with the typical widely held public corporation.

! The powers specially created or exercised by the government, which are not in

agreement with the transparency ideal and other generally accepted principles of good corporate governance.

! The lack of logic for the continuation of these powers in the interest of independence

in the governing board, its integrity, accountability and transparency.

2.9. A close examination (as evident from the analysis pertaining to the central public sector undertakings in Part - II) reveals that the government has a massive task before it to create the enabling conditions that would improve the quality of corporate governance across the public enterprise system and for its transition to becoming market orientated.

2.10. Good corporate governance in public enterprises implies attention to issues larger than

those of law and stock exchanges. They need to address the principles of government and public enterprise relationships and create the fundamental pillars on which the governing board can be based on to become effective. The principles, codes and best practices for boards will become far more attractive and effective once these fundamentals are agreed upon and instituted. These have been termed as the First Principles and stated in Part - III.

8

PART – II

3. BOARD STRUCTURE AND CONTROL DYNAMICS – A FACTUAL POSITION OF CENTRAL PUBLIC SECTOR UNDERTAKINGS

3.1. The Board of Directors of public sector undertakings normally comprises of:

! Full time functional directors or executive directors

! Nominees of the Administrative Ministry

! “Non official part time directors” (independent directors) and, at times

! Special representatives (e.g. Worker representatives).

3.2. The chief executive and functional directors are recruited, selected/promoted by the Public

Enterprises Selection Board. Each appointment is normally for a term of three years but renewable till the age of superannuating.

3.3. The appointments of board members have to be cleared by the Appointments Committee of

the Cabinet consisting of ministers. The recommendations of the Public Enterprises Selection Board are considered by the committee but not necessarily accepted. A Maximum of two nominees for the Administrative Ministry are selected by the concerned minister – they are usually the Additional Secretary and the Joint Secretary of the relevant department. They operate on a non-rotational basis but the individuals keep changing, as transfers are frequent in most ministries. All appointments are subject to due diligence and clearance by the Central Vigilance Commissioner.

3.4. The Department of Public Enterprises, which has been issuing guidelines, has not expressed a view on whether the Chairman ought to be independent or have executive responsibilities. Almost all the central public sector undertakings have Executive Chairman with the designation Chairman & Managing Director. (This has closed the option to Government of nominating political leaders as Chairmen, which is not the case in the majority of the state level enterprises.) By a specific decision of the government, Members of Parliament are excluded from being appointed to the boards of the central public sector undertakings. The guidelines also recommend that full time functional directors should not exceed 50% of the board, government nominee directors should not exceed one sixth of the actual strength and in no case should the number exceed two.

Department of Public Enterprises

Administrative (Responsible)

Ministry -Officials and

Ministers

Board

Management

• Parliament and Parliamentary Committees

• Cabinet/Appointments Committee of the cabinet

• Finance Ministry/Special Committees of secretaries

• Planning Commission • Comptroller & Auditor

General of India • Central Bureau of

Investigation • Central Vigilance

Commission • Writ Jurisdiction of High

Court & Supreme Court • Public Enterprises Selection

Board

9

3.5. Part time non-official directors should make up at least one-third of the board. The responsibility for filling vacancies has been vested with the Administrative Ministries, the Department of Public Enterprises and the Public Enterprises Selection Board – the board itself has little power in board appointments, renewal or succession planning. The compensation for full time directors and the Executive Chairman are as per the guidelines issued by the Department of Public Enterprises while the non-official part time directors are allowed a sitting fee per meeting, which is a nominal amount.

3.6. All listed public sector undertakings are required to follow the Securities Exchange Board of

India’s requirements of corporate governance including the constitution of the Audit Committee with a majority of independent directors with at least one director having accounting knowledge; disclosure of financial performance/results of the listed companies on their web-site or on the web-site of the stock exchange on which the company is listed; separation of the position of Chairman from the chief executive failing which a greater number of independent directors are to be inducted and provide a separate section on corporate governance with details on compliance, non-compliance (with reasons) of the mandatory requirements along with compliance certificate from the auditors in the Annual Report.

3.7. The courts have held that public sector undertakings are indeed part of government and

thus special privileges and rights are bestowed upon the employees, under Article 12 of the Constitution. Public sector undertakings also figure in Parliament debates and its committees by virtue of the majority holding by the government.

3.8. The Department of Public Enterprises issues guidelines on board appointments, the

appointment of other personnel, wages and salaries. The Central Vigilance Commissioner issues guidelines on conduct, disciplinary cases, investigations and the like. The central public sector undertakings are also subject to a special additional audit by the Comptroller and the Auditor General. The Central Bureau of Investigation assumes jurisdiction over the employees and the directors as they are regarded as “public servants”. The Planning Commission of the Government of India has a role in planning and project proposals of the public sector undertakings.

3.9. The ownership rights of the Government are exercised along with other controls by a

complex system primarily arising from the view that Public Sector Undertakings are indeed part of government and that the boards are needed only for compliance purposes. Though the public and the employees hold some stock, their role and voice appear even more subordinated than in a similar case of the private sector due to the additional controls that he Government exercises as an owner.

3.10. Several boards do not have the full complement of directors and several positions of

executive Chairman remain unfilled for long periods or are under additional / temporary charge. The ministry representatives on the Board often exercise, de facto, veto powers. The salaries and foreign travel of directors need ratification or approval from the ministry. Capital expenditure beyond a limit, long term purchase agreements, joint ventures and, technology agreements need a clearance by the ministry outside the board and the shareholder meetings, even in the case of the “Navratnas”.

3.11. The shareholder meetings are generally routine in nature and do not signal activism, except

occasionally by the employees. The expectations of employees and the general public of the boards also appear to be modest. The Department of Public Enterprises has conceived the functions of the boards as mostly relating to production management, materials management, financial management, construction management and general management. The illustrative checklist provided by the Department of Public Enterprises recommends several managerial functions for the boards and makes little reference to governance and strategic aspects. Case studies reveal that the Board processes and procedures reflect the dominance of compliance and operational bias rather than governance and strategy.

3.12. Control by the government is admittedly hampering the efficiency and competitiveness of

the public sector undertakings, which have represented the creation of a “level field” vis-à-vis the private sector. There is continued debate on the comparative efficiencies of the public sector and the private sector, with a recent survey by the Centre for Industrial and Economic Research revealing that the Indian public sector undertakings have better

10

performance ratings than those in the comparable private sector. There have been repeated public statements that autonomy, transparency and a governance structure akin to the one for the private sector would make public sector undertakings truly world class in their efficiency, growth and competitiveness.

11

PART – III

4. THE FIRST PRINCIPLES

4.1. The government should review the legal status of all organisations controlled by it so as to separate those which can carry out commercial activities as companies following the market discipline, and those that will continue as a sovereign function of the government.

Statutory bodies, Commisionerates, Directorates, Departmental Undertakings, Co-operatives and Trusts may be reviewed and given the opportunity of becoming companies under company law without any ambiguity regarding their character, purpose or legal status.

4.2. The government should draw up a consensus based comprehensive policy of

privatisation, of both companies and other entities delineating these, which will continue to be State-owned, the method of disengagement and the process of disengagement.

An approach has been attempted in a limited way by segregating “core and non-core” and “strategic” enterprises, though the criteria are not evident. The efforts of the Disinvestment Commission and the Department of Disinvestment in this direction are noteworthy. However, these need to be deepened and broadened so as to cover all issues pertaining to all the public enterprises and evolve a political consensus. The valuation methods, processes of valuation, choosing the method of disengagement, tendering/bidding and sale/selection of bidders have been contentious in most countries including India. These can be resolved through consensus and transparency and breaking away from the case-by-case approach.

4.3. The government should issue guidelines, policy or directives indicating the

contingent conditions alone under which a currently private sector activity will be brought under State-control.

This measure may limit the extent of moral hazard and the use of golden-share type of mechanisms. If a company/activity fails, there are numerous arguments and pressures to invoke the States’ support which obviously results in the foregoing of other socially advantageous opportunities. Room for such pressures need to be foreclosed to the extent feasible.

4.4. The continued ambiguity in the set of objectives of public enterprises should be

resolved by the government, highlighting the primacy of financial objectives within a framework of product – market targets and other values/social commitments.

Despite years of debate and directions, the ambiguity continues in both policy statements as well as actions. Consequently, public enterprises often have confusion concerning their market segments, value-delivery, levels and extent of social responsibility. A clear policy statement by the government will bring about the essential difference between the non-negotiable explicit financial objectives/priorities and the set of values and preferences inherent in the mission of the organisation, whether explicit or implicit.

4.5. The government should bring about greater transparency by fully accounting for

subsidies and price controls imposed on public enterprises, and by achieving the desired social and developmental objectives through government’s budgetary provisions and related mechanisms.

In the case of banks, such a measure would apply to directed social lending and in the case of insurance, the special schemes. In the case of electricity companies, it relates to free or concessional supplies to specified sectors and groups. These measures will ensure that true costs and prices are apparent in the books and transparent to all stakeholders. Social/human developmental objectives, which require investment must be met through direct budgeting, direct subsidies to the target group and long-term contracts between the government and the public enterprise. Such an approach will make the social objectives

12

more transparent, more efficient and also allow the public enterprises and governments to move towards global standards in fiscal transparency, accounting standards and public disclosure practices. This measure will also remove the confusion on the objectives of public enterprises.

4.6. The government should give up direct control over public enterprises by

restructuring/rationalising the role of departments overseeing these undertakings.

Government should arrange to exercise its superintendence through the Governing Board and the General Meetings. The current administrative control will become redundant if a special agency/body is used for exercising the ownership rights of the government, as recommended in 4.10 below. On the other hand, if there were any regulatory role for the ministry/department, the same would also need review in the context of the current perspectives on the independence of regulatory bodies from that of ownership. In either situation, redundant oversight may breed a false sense of legitimacy for inefficient control mechanisms and may also create special constituencies for drawing unjustifiable benefits.

4.7. The government must separate its ownership role and let public corporations be

governed by the same structure of controls as that of any other company. The laws giving special status to public enterprises or special controls over them must be amended / annulled.

In the case of central public sector undertakings, amendments would be required in the company law to remove the special status of a government company; revisiting the interpretation of the applicability of Article 12 of the Constitution to the employees of public enterprises; removal of the jurisdiction of Comptroller and Audit General, Central Vigilance Commission and the Central Bureau of Investigation. In the case of public sector banks, the role of the Reserve Bank of India must be restricted to being a regulator. In keeping with good principles of corporate governance and the several recommendations made already in this regard, the RBI must discontinue the practice of having its nominees on the boards of the banks it supervises and approving board appointments, and it must divest its equity stake in banks. Similar actions would be required in the case of ports, railways, electricity companies, government controlled co-operatives and a host of other public enterprises.

4.8. Parliamentary/Legislative Assembly control over public enterprises should be limited

to interaction with the body exercising the ownership rights of the government.

Currently, government ownership implies the right of Parliament over even the operating matters of PE’s. Managers in the PE’s regard this as a special control that the private sector does not suffer from. It is advisable that Parliament/Assembly deals with those exercising the ownership rights on behalf of the government (say, Trustees or members of a Commission, as the case may be).

4.9. The government should assess and re-capitalise public enterprises to ensure that

the cost of social burden on a historical basis is made good on a one-time basis after adjustments for special grants and concessions are given, if any.

This will help some of the public enterprises in mitigating the net burden or lagged effect of non-commercial objectives and directed activities and assist progress towards greater transparency and competitiveness.

4.10. Ownership rights of the government should be exercised by specialised bodies to be

created for that purpose.

These special bodies / agencies can be Trusts or Commissions, which alone should deal with the public enterprises as an owner. These may be both at the State and the Centre levels. The government should transfer all the shares / ownership rights to such special bodies. These special bodies should comprise of independent professionals with good experience of carrying out fiduciary responsibilities. These bodies may, as in the case of several countries, use special intermediaries (service providing companies) for actively monitoring, evaluating, contesting, and proxy voting on their behalf, if so required. Exercise of ownership rights may include disinvestments, privatisation, acquisition of equity,

13

reinvestment, portfolio management, JVs, M&As and the like which are typically associated with ownership rights that can be exercised through the Board and the shareholder meetings.

4.11. The body exercising the voting rights should actively structure, create, develop and

renew the governing board ensuring the highest qualities of leadership, enterprise, integrity and judgement.

The body must be staffed with professionals who are well trained in law, finance and general management. The body should build data and knowledge of various standards, situations, board dynamics, the internal process of briefing, de-briefing, monitoring and evaluation. It should have sound mechanisms of managing the performance of its representatives/nominees.

4.12. Governments must ensure that persons who are or were members of parliament or

legislative assemblies be excluded from occupying the positions of Chairman or members of the governing board of a public enterprise, thus extending the spirit followed in the case of central public undertakings.

This is to ensure that public representation, which is a function of the practice of vote maximisation, and nurturing of constituencies, does not contradict the pursuit of transparent sustainable objectives of the enterprise.

4.13. The position profile and specifications of chairman, chief executive and members of

the governing boards should be approved by the governing board and shareholders in advance and through the expert advice of external bodies.

This will ensure that people do not chase board slots and jockey for a position. It will also help in debating and structuring the Board with the requisite competencies required to steer the organisation well into the future. Periodic amendments and exceptions may be needed. However, these amendments should pass through the board and the shareholders. Such a system will help in curtailing the scope for “cronyism”.

4.14. Listed public enterprises will have to follow the mandatory requirements of company

law and the stock exchange regulations. All other public enterprises should follow the relevant CACG or OECD principles that would foster independence, integrity, transparency and accountability of the governing board, protect the rights of shareholders and engage the stakeholders.

There is increased compulsion now for listed companies to induct independent directors, create an audit committee, have a separate section in the annual reports on corporate governance compliance, a section on management discussion and analysis, better disclosures and board practices. Public enterprises other than the listed corporates are not under any obligation to improve the quality of transparency and accountability. As a first step, they may adopt the international guidelines and list in their reports the current state and further steps contemplated vis-à-vis each of such principles/guidelines. These public enterprises may give a short report as to how the structure, systems and processes of the governing board will meet the principles/guidelines and the spirit behind them.

4.15. Each public enterprise should develop a best practice manual for board processes,

procedures and formats which may include, inter-alia, the profile of board positions; recruitment, selection, induction, training processes; conduct of board meetings; dealing with conflict of interests, disclosures, accounting and reporting requirements; evaluating board members; remuneration and renomination.

The best practice manual will be helpful in lessening the scope for poor governance and, progressing to meet international standards. There will be fewer omissions and, hopefully, there will be some control over commissions of unethical/inappropriate actions.

4.16. Public enterprises should ensure that individuals chosen for appointment as

directors are either properly accredited, when such facility is available, or be formally trained in corporate governance practice.

14

The major challenge in progressing quickly on good governance is the dearth of competence in directorial functioning. Most directors do not have the essential knowledge on relevant law; duties, responsibilities and liabilities; financial analysis; strategy; business ethics and effective decision-making. It is necessary to build capacity throughout the country by an accreditation process, training and development. Directorship must develop, eventually, as a profession with a sound body of knowledge. A director must be recognised because of such knowledge and the associated competence rather than the position itself. Several countries including the UK, Australia and New Zealand have set excellent examples for director training and accreditation.

15

ANNEXURE

RECOMMENDATIONS OF THE 1997 REPORT ON

“CORPORATE GOVERNANCE AND PSUs’

by Yaga Consulting Pvt. Ltd. A. Government & Public Sector Units:

A.1 It is indeed trite to repeat the several recommendations and the logic behind each one of them, from the 60’s onwards, exhorting the government to give greater autonomy to the Central Public Sector Units (PSUs). The several Committees on Public Undertakings have highlighted this aspect but there has hardly been any change. One of the major complaints of PSU’s has been that the minister and the officials in the ministry exercise authority frivolously through formal as well as informal communications. Concurrently, there is inadequate consultation and discussion during crucial decisions. Whereas, the ministry can easily conjure up reasons for all such communications and non-communications, there is unanimity that good governance will endure if communications systems and structures are rationalised. It is also a fact that several directors and chief executives often appear to be seeking undue interaction with the ministers and secretaries – such inclination is also rationalised giving reasons for the importance of managing this authoritarian stakeholder. Irrespective of who is to be blamed for this situation, it is recommended that the administrative ministry contact the PSUs only through its representatives on the Board and not otherwise. Even as its feasibility is discussed, the interim arrangement must be to list all such communication-events along with the subjects of discussion for circulation among members of the Board every three months (Recommendation 1).

A.2 The BPE (now the Department of Public Enterprise) was set-up with laudable objectives,

which appeared strategic at the time. Most objectives, even on reckoning the recommendations for strengthening the BPE’s role and the current process of re-engineering the circulars and guidelines, now appear incongruous. This is primarily because of the need for firm-specific approaches as against unitary designs and also the ineffectiveness of departmental governance. The command and control approach which had much validity in the early years after the Independence is no longer valid due to the induced as also the naturally evolving diversities and complexities in the nature of ownership, nature of differentiated competition in the market place and other related issues. Kathryn said the above paragraph does not make sense (highlighted) Thus, the Department of Public Enterprises must revisit its role. It is recommended that the Department of Public Enterprises recraft its mission and role to that of a competitive consultancy organisation offering value-added services to all varieties of PSU and in the process severe all of its traditional relationships with PSUs. (Recommendation 2). This would seem drastic but administrative reform which is connected with economic adjustments calls for, among others, restructuring and “institutionalising” / corporatisation of some services. Countries such as Australia and the U.K did this successfully years ago.

A.3 The performance contract system between the Government and the PSU`s has had a long

and unsatisfactory history in the world. By now, it is abundantly clear that the Memorandum of Understanding (MoU) is, as termed by an eminent academic, `more memoranda than understanding’ and has degenerated into a ritual. The system itself has no fit with the new dynamism required for a more competitive world. However, it is a necessary transition that an economy like ours had to go through rather than leapfrog into the totally unfamiliar. It is evident that no straight-jacket system such as the Memorandum Of Understanding will suit the needs of individual companies and their technology, products, markets, risk profiles, competitive conditions, cost structures and inherent disabilities. Importantly, the legality and ethical justification for such a contract with a part owner even if the largest, would soon become questionable. Consequently, it is recommended that the Memorandum of Understanding system is scrapped and in its

16

place, a firm-specific `Strategy Agreement’ is implemented. This new instrument will concentrate on a few crucial issues surrounding the profitability, survival, and sustainability issues under the most plausible scenario of competition, supply-demand-price dynamics and the changing profile of governmental support, direct and indirect. This Strategy Agreement System may be developed by specialists to a full-blown form and will enable a strategic approach and encourage commitment rather than rituals. This system may adopt a yearly cycle. In course of time, and on attaining reasonable diversity in ownership, it would be prudent to involve other important stockholders in this exercise. (Recommendation 3)

A.4 Several experts on PSU`s have criticised the role of Comptroller and Audit General (CAG)

as an additional burden. Whereas, the Comptroller and Audit General is an important instrument of public accountability, it works to the detriment of several normal rights of enterprises. It is recommended elsewhere that the Comptroller and Audit General must become involved through a different mechanism to ensure diligence in management and restructure the method required to advise on the appointment of chartered accountants, issue directions under section 619(3) of the Companies Act, to prepare special reports, affirm, or comment upon or supplement the audit report prepared by the Chartered Accountants as provided under section 619(4) of the Companies Act. PSUs have complained that this double check is not suffered by the private sector and also that the annual general meetings are delayed, among other reasons, on account of the Comptroller and Audit General audit. More importantly, despite the recent castigation of some auditing firms, a re-certification by the Comptroller and Audit General is considered as an affront to the chartered accountancy profession. It is recommended that the Companies Act be amended to remove the separate category of government companies and provide the necessary level-playing field for the PSU. In the interim, it is recommended that the Comptroller and Audit General carries itself as an instrument of public accountability through participation in the Audit Committee of the Boards and refrains from the traditional types of scrutiny to the extent legally permissible. Continuation of the existing approach in light of errant auditors is no justification for over-governance but is a fit case to be addressed by the profession itself. (Recommendation 4).

A.5 The Parliament’s role in the governance of PSUs has received mixed reactions but

predominantly indicates that call attention motions and questions in the Parliament have not served the interest of the PSUs, save a very few policy discussions that took place in the case of Indian Airlines, Steel Authority of India Limited. Whereas, policy discussions should feature prominently in this forum, it is the dominant view that several questions are constituency based and interest related and hence avoidable. It is recommended that Parliament adopts an internal code to be enforced by the Speaker, through which all questions related to specific PSUs will be raised only in the Consultative Committee. The Committee can call the Chairman of the concerned PSU and also a representative of the ministry, if required, for clarification and discussion. It is also recommended that the discussions pertain to strategic matters only and not operational. Such a system will bring greater transparency apart from being more effective. To strengthen this system, the Consultative Committee and the Committee on Public Enterprises may be apportioned special budgets for engaging external consultants or commissioning special studies as in the case of the Senate Committee in the United States. (Recommendation 5). Though the practicality / acceptability of this best practice code may be doubted, it may be pointed out that it will have as much good effect as any other code and is non-competing with better alternatives that may emerge in the years to come.

A.6 The writ jurisdiction provided by Article 12 of the Constitution has come under severe

criticism. This provision has led to a flood of cases and a fear psychosis amongst management. At the same time, there are several employees who prefer the continuation of this coverage. Though this provision is not a part of corporate governance in itself, it seems to have an impact on building long term capabilities in competition with those in the private sector and also those where the government control falls below 51%. It is recommended that Article 12 of the Constitution be amended to exclude coverage of PSU`s and provide them with a level playing field. Meanwhile, it is noticed that the Supreme Court has also undergone changes in interpreting labour laws evidenced in some recent judgments. Keeping this in view an early opportunity may be made use of to test the applicability of Article 12 once again. (Recommendation 6).

17

A.7 Similarly, the jurisdiction and roles of the Central Bureau of Investigation and Central Vigilance Commission are seen as an anachronism. PSU employees may be treated no differently from other corporate employees - it would indeed be difficult to comprehend the need for differing systems for increasingly identical segments of employees. It is recommended that the Prevention of Corruption Act be amended to exclude the PSU employees from the definition of `public servant’. Further, it is recommended that the Central Vigilance Commission’s jurisdiction over PSUs is removed and the Board is allowed to appoint a Chief Vigilance Officer as deemed appropriate. (Recommendation 7).

A.8 It is realised that integration of employees, management and the Boards in the process of

increasing share-holders’ value and the value of the shares in the market is important for acquisition and long-term sustenance of competitive abilities. Employee Stock Option Plans are an important instrument not only for better strategic management of the enterprise but as an indirect mechanism of corporate governance in future. It is strongly recommended that PSU`s examine and devise valid Stock Option Models to achieve objectives of corporate governance as well as operational efficiency on a dynamic basis. (Recommendation 8).

B. The Board of Directors:

B.1 It is regrettable that several directives and recommendations regarding the composition of the Board have remained un-implemented. The more recent foray into this is the important circular of the Department Of Public Enterprises dated 16th March 1992. It is the general feeling that the stake-holders’ interests are being sacrificed significantly through slow action in professionalising and empowering the Boards on the one hand, and politically motivated decisions in the appointments of both CMDs (Chairman and Managing Directors) and Directors, full-time as well as part-time, on the other. It is, however, a happy augury that the `Navratnas’ are being given further powers and the boards being reconstituted. Similar move in the case of Miniratnas may also be noted with optimism. Reckoning all aspects and without labouring on the much discussed lacunae, our recommendations in respect of the Board of Directors is as follows.

B.1.1 It is recommended that the positions of Chairman and Managing Director continue

to be vested in one person, which goes against the popular view for the private sector. (Recommendation 9). This is to ensure that PSUs do not get into the same difficulties as several State level enterprises due to political appointees as non-executive Chairmen. The positions may be separated as and when the selection process of the non-executive Chairman becomes objective and not a political patronage. The situation in the private sector is the converse, as the balance of power needs to be distributed in the opposite direction as a check against run-away management.

B.1.2 It is recommended that each PSU Board has a minimum of 8 and a maximum of 15

directors at any point in time and 50% of this number be functional directors including the Chairman and Managing Director. (Recommendation 10). This implies a minimum of four functional directors including the Chairman and Managing Director.

B.1.3 If there is any vacancy due to the number of functional directors not adding up to

50%, then a representative from the employee and consumer segments must be co-opted in that priority to take up the position as a part-time Director. This recommendation is in the hope that undue delays are prevented in the process of appointing functional directors. (Recommendation 11).

B.1.4 One-quarter of the Board must be drawn from experts, academicians, professionals

and technocrats. (Recommendation 12).

B.2 The suggested structure would require a change in due course to provide for representation of financial institutions or similar significant shareholders in the making. Even if the government continues to hold more than 51% stock, it would be prudent to allow one or two financial institutions or mutual funds holding considerable shares, to take Board positions. This is in recognition of the general trends world-over towards proportionate representation.

18

B.3 Representatives from the administrative ministry and Ministry of Finance must be

represented at a senior a level as possible and not exceed two. (Recommendation 13). B.4 It is recommended that no director shall hold such a position in more than three

organisations concurrently. This may be adopted as a “Best Practice” norm as the Companies Act provides for twenty directorships. (Recommendation 14).

B.5 The tenure may be fixed at three years for the part-time directors and in respect of

Chairman and Managing Director and functional directors it may be five years or superannuation, whichever is earlier but not less than three years. (Recommendation 15).

B.6 Each Board must appoint from within them an Appointments Committee and standing Audit

Committee. Similarly, committees for Capital Expenditure and Compensation may also be created on a need-basis. In the Board managed situation capital expenditure decisions and compensation designs may be left to the Boards/AGM (Annual General Meeting). These committees may co-opt external specialists, representatives of ministries, PESB (Public Enterprises Selection Board), Comptroller and Auditor General as appropriate. (Recommendation 16).

B.7 The manner of appointing directors may be changed forthwith. The representatives of the

ministry may be nominated by the Secretary and in his own case, by the Minister concerned. The selection of functional directors as well as the Chairman and Managing Director must be done by the Appointments Committee of the existing board of the PSU with the assistance of the Public Enterprise Selection Board. The Public Enterprise Selection Board must take a supportive and advisory role without wielding any specific over-riding authority. It may be worthwhile for the Public Enterprise Selection Board to change its mission and role to that of a service provider to all PSUs, at a price. The logic for this suggestion will be found in the realm of administrative reform under economic adjustments, as already mentioned elsewhere. (Recommendation 17).

B.8 It is realised that several suggestions/nominations by the concerned PSU and/or the Public

Enterprise Selection Board have been turned down by the ministry/ACC (Appointments Committee of the Cabinet) concerned with little justification, making the entire process a futile exercise. It is sincerely hoped that the current efforts in respect of Navratnas and the others will be more objective and expeditious. While appreciating this effort, it is felt that some changes in the context of empowering the boards are still needed.

B.9 It is recommended that a unanimous decision by the Public Enterprise Selection Board and

the Appointments Committee of the Board be treated as automatic approval. The composition of the Appointments Committee may be made dynamic, in such a way as to exclude those who are candidates for the directorships. Where there is a difference of opinion, the same may be referred to the Appointments Committee of the Cabinet or to its delegated authority. In due course, however, these decisions may be taken at the Board level and Annual General Meeting without involving the Public Enterprise Selection Board. (Recommendation 18).

B.10 Appointments on the board must be so timed as to ensure that there is no large-scale

change amongst the directors and that there is always some mix of the earlier members and the fresh ones. In selecting the directors, the Appointments Committee of the Board must ab-initio describe the existing profile of the Board, the gaps in the expertise/skills and the specifications of the desired additions. (Recommendation 19).

B.11 It should be ensured that full-time directors are identified/appointed so as to be in place

and understudy the current incumbents for at least three months ahead of the completion of their term. (Recommendation 20).

B.12 In the case of a new PSU or the Joint Ventures/Subsidiaries of existing ones, it may be

ensured that the functional directors are in place before any strategic decisions such as those relative to locations, choice of technology and long-term contracts are made. (Recommendation 21).

19