21

| Date post: | 12-Feb-2017 |

| Category: |

Technology |

| Upload: | decisive |

| View: | 238 times |

| Download: | 1 times |

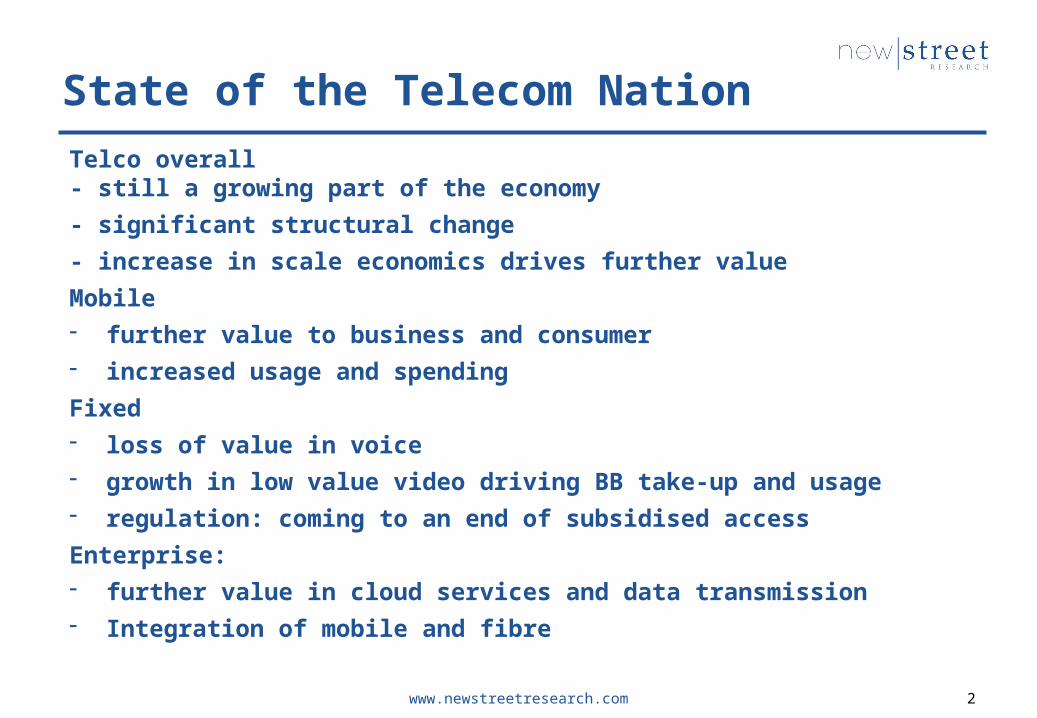

State of the Telecom NationTelco overall- still a growing part of the economy- significant structural change- increase in scale economics drives further valueMobile- further value to business and consumer- increased usage and spendingFixed- loss of value in voice- growth in low value video driving BB take-up and usage- regulation: coming to an end of subsidised accessEnterprise:- further value in cloud services and data transmission- Integration of mobile and fibre

www.newstreetresearch.com 2

State of the Telecom Nation

www.newstreetresearch.com 3

-

5,000

10,000

15,000

20,000

25,000

30,000

Telstra Optus TPG VOC NBN

Est Revenue FY16F

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

Telstra Optus TPG VOC NBN

Est EBITDA FY16F

-

1,000

2,000

3,000

4,000

5,000

6,000

Telstra Optus TPG VOC NBN

Est Capex FY16F

-25.0%-20.0%-15.0%-10.0%-5.0%0.0%5.0%

10.0%15.0%20.0%25.0%

Telstra Optus TPG VOC NBN

ROIC FY15

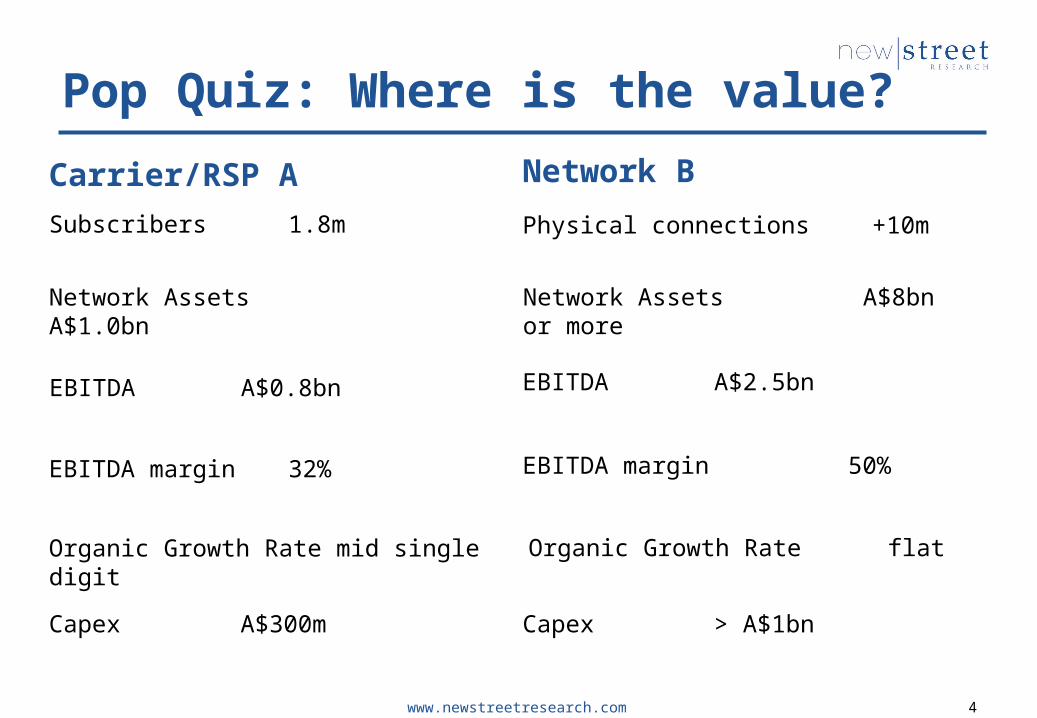

Pop Quiz: Where is the value?Carrier/RSP A

www.newstreetresearch.com 4

Network BSubscribers 1.8m Physical connections +10m

Network Assets A$1.0bn Network Assets A$8bn or more

EBITDA A$0.8bn EBITDA A$2.5bn

EBITDA margin 32% EBITDA margin 50%

Organic Growth Rate mid single digit Organic Growth Rate flat

Capex A$300m Capex > A$1bn

Mobile – Does 5G imply a two carrier mobile market?

www.newstreetresearch.com 5Source: NSR estimates, Company report

1H14 2H14 1H15 2H15 1H16 2H16FTelstra 51.6% 52.9% 53.8% 53.8% 53.3% 53.4%Optus 29.6% 29.5% 29.5% 29.7% 29.7% 29.6%Vodafone 18.8% 17.6% 16.7% 16.6% 16.9% 17.0%

0%

10%

20%

30%

40%

50%

60%Mobile service revenue market share

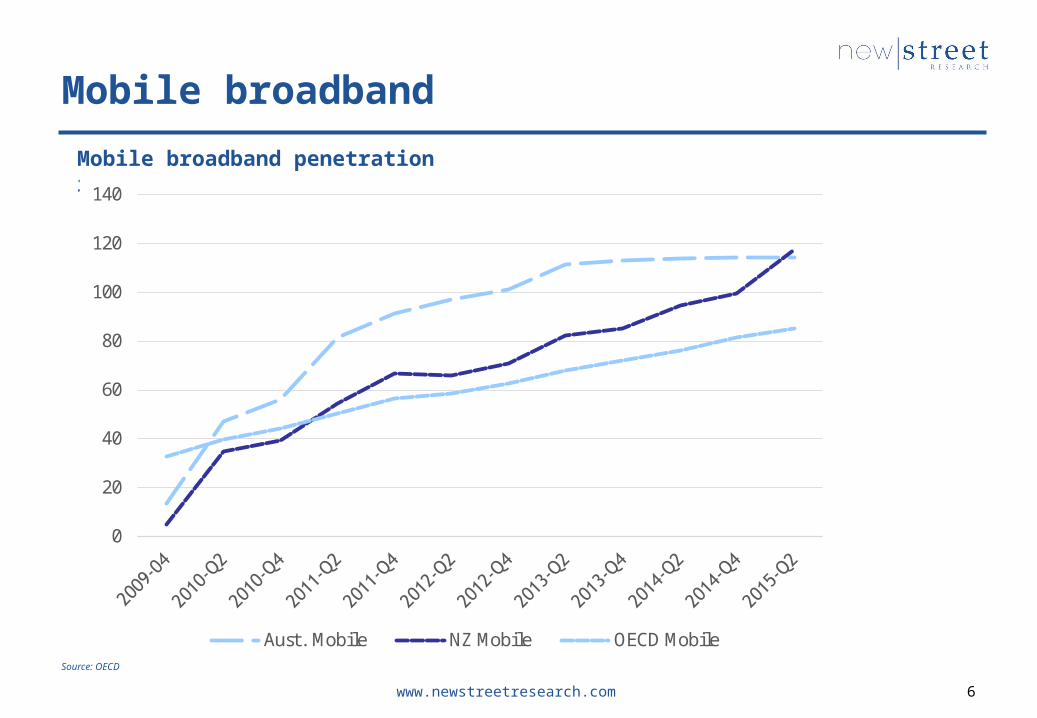

Mobile broadband

www.newstreetresearch.com 6

Mobile broadband penetration rates

Source: NSR, OECD Broadband Portal Feb 2016

0

20

40

60

80

100

120

140

Aust. Mobile NZ Mobile OECD MobileSource: OECD

Fixed broadband

www.newstreetresearch.com 7

Fixed broadband penetration rates

Source: NSR, OECD Broadband Portal Feb 20160

5

10

15

20

25

30

35

Aust. Fixed NZ Fixed OECD FixedSource: OECD

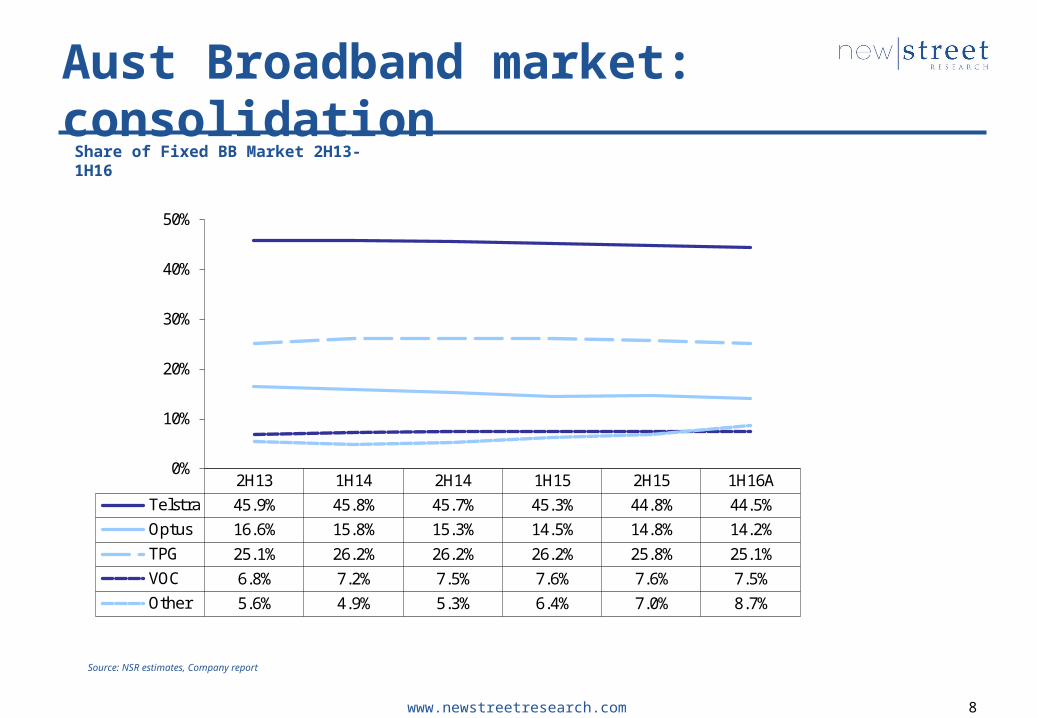

Aust Broadband market: consolidation

www.newstreetresearch.com 8

Share of Fixed BB Market 2H13-1H16

Source: NSR estimates, Company report

2H13 1H14 2H14 1H15 2H15 1H16ATelstra 45.9% 45.8% 45.7% 45.3% 44.8% 44.5%Optus 16.6% 15.8% 15.3% 14.5% 14.8% 14.2%TPG 25.1% 26.2% 26.2% 26.2% 25.8% 25.1%VOC 6.8% 7.2% 7.5% 7.6% 7.6% 7.5%Other 5.6% 4.9% 5.3% 6.4% 7.0% 8.7%

0%

10%

20%

30%

40%

50%

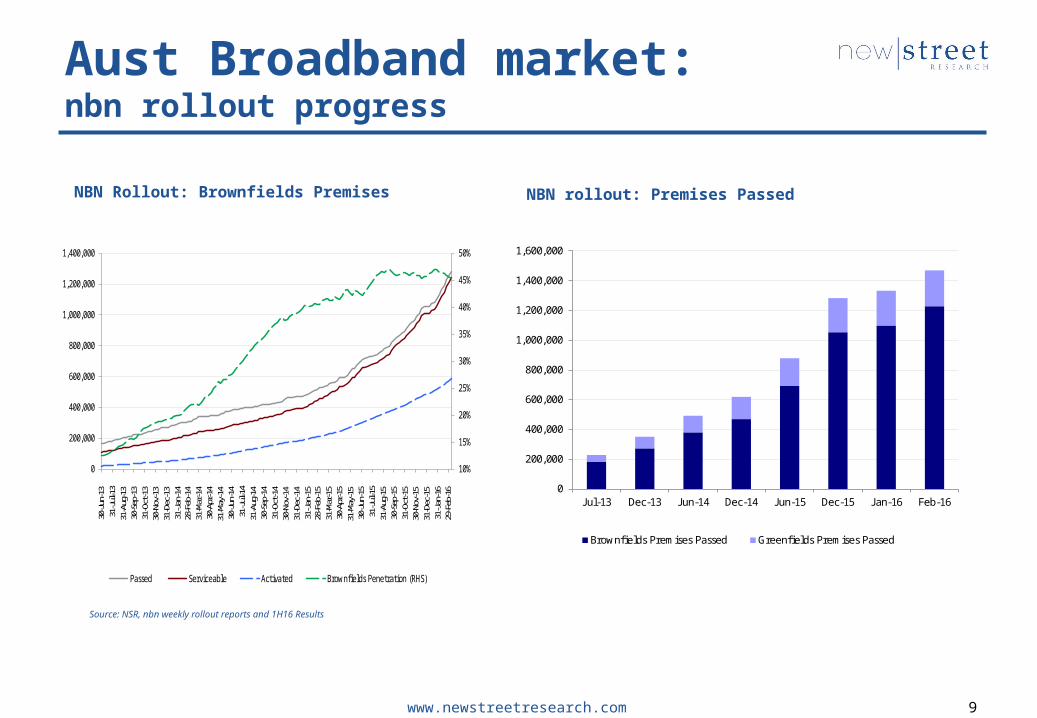

Aust Broadband market: nbn rollout progress

www.newstreetresearch.com 9

NBN Rollout: Brownfields Premises NBN rollout: Premises Passed

Source: NSR, nbn weekly rollout reports and 1H16 Results

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

30-Jun

-13

31-Jul-1

331

-Aug

-13

30-Sep

-13

31-O

ct-1

330

-Nov

-13

31-D

ec-1

331

-Jan

-14

28-F

eb-1

431

-Mar

-14

30-A

pr-1

431

-May

-14

30-Jun

-14

31-Jul-1

431

-Aug

-14

30-Sep

-14

31-O

ct-1

430

-Nov

-14

31-D

ec-1

431

-Jan

-15

28-F

eb-1

531

-Mar

-15

30-A

pr-1

531

-May

-15

30-Jun

-15

31-Jul-

1531

-Aug

-15

30-Sep

-15

31-O

ct-1

530

-Nov

-15

31-D

ec-1

531

-Jan

-16

29-F

eb-1

6

Passed Serviceable Activated Brownfields Penetration (RHS)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

J ul-13 Dec-13 J un-14 Dec-14 J un-15 Dec-15 J an-16 Feb-16

Brownfields Premises Passed Greenfields Premises Passed

Australian Broadband market: Impact of NBN now begins to take shape

www.newstreetresearch.com 10

Indicative NBN RSP Market Share: FY15A, 1H16A

Source: NSR estimates, Company Reports.

* TPG subscribers adjusted pro-rat to net adds to 30 June and 31 Dec. TPG nbn subs as at 31 Jan is 194k, indicative nbn share of 24.7% at 31 Jan

** M2 now included with Vocus, prior to 1H16 included in “Other RSP”

NBN Share FY15 1H16 FY15 1H16TLS 211 329 118 43.5% 44.7% 47.1%TPG* 122 183 61 25.1% 24.8% 24.3%Optus 54 88 34 11.1% 12.0% 13.6%VOC** n.a. 40 40 n.a. 5.5% n.a.Other RSP 99 96 n.a. 20.3% 13.0% n.a.NBN Premises Activated 486 736 250 100.0% 100.0% n.a.

Subscribers (k) Net Adds (k)

Indicative NBN Share Indicative Share Net Adds

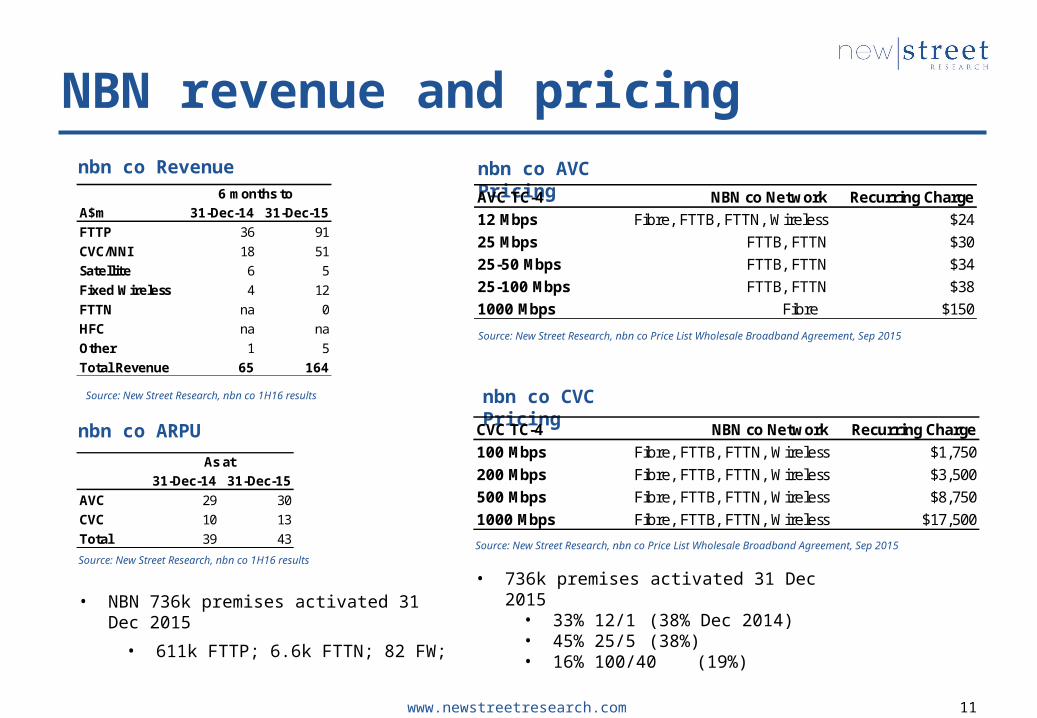

NBN revenue and pricing

www.newstreetresearch.com 11

Source: New Street Research, nbn co 1H16 results

nbn co Revenue

nbn co ARPU

Source: New Street Research, nbn co 1H16 results

nbn co AVC Pricing

Source: New Street Research, nbn co Price List Wholesale Broadband Agreement, Sep 2015

nbn co CVC Pricing

Source: New Street Research, nbn co Price List Wholesale Broadband Agreement, Sep 2015

A$m 31-Dec-14 31-Dec-15FTTP 36 91CVC/NNI 18 51Satellite 6 5Fixed Wireless 4 12FTTN na 0HFC na naOther 1 5Total Revenue 65 164

6 months to

31-Dec-14 31-Dec-15AVC 29 30CVC 10 13Total 39 43

As at

AVC TC-4 NBN co Network Recurring Charge12 Mbps Fibre, FTTB, FTTN, Wireless $2425 Mbps FTTB, FTTN $3025-50 Mbps FTTB, FTTN $3425-100 Mbps FTTB, FTTN $381000 Mbps Fibre $150

CVC TC-4 NBN co Network Recurring Charge100 Mbps Fibre, FTTB, FTTN, Wireless $1,750200 Mbps Fibre, FTTB, FTTN, Wireless $3,500500 Mbps Fibre, FTTB, FTTN, Wireless $8,7501000 Mbps Fibre, FTTB, FTTN, Wireless $17,500

• NBN 736k premises activated 31 Dec 2015

• 611k FTTP; 6.6k FTTN; 82 FW;

• 736k premises activated 31 Dec 2015• 33% 12/1 (38% Dec 2014)• 45% 25/5 (38%)• 16% 100/40 (19%)

NBN ICRA already at over A$6.0bn

www.newstreetresearch.com 12

2009 2010 2011 2012 2013 2014 20150

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Revenue ABBRR ICRA

Fixed Line: post Vertigan game changeTraditional network diseconomies of distance and population density

www.newstreetresearch.com 13

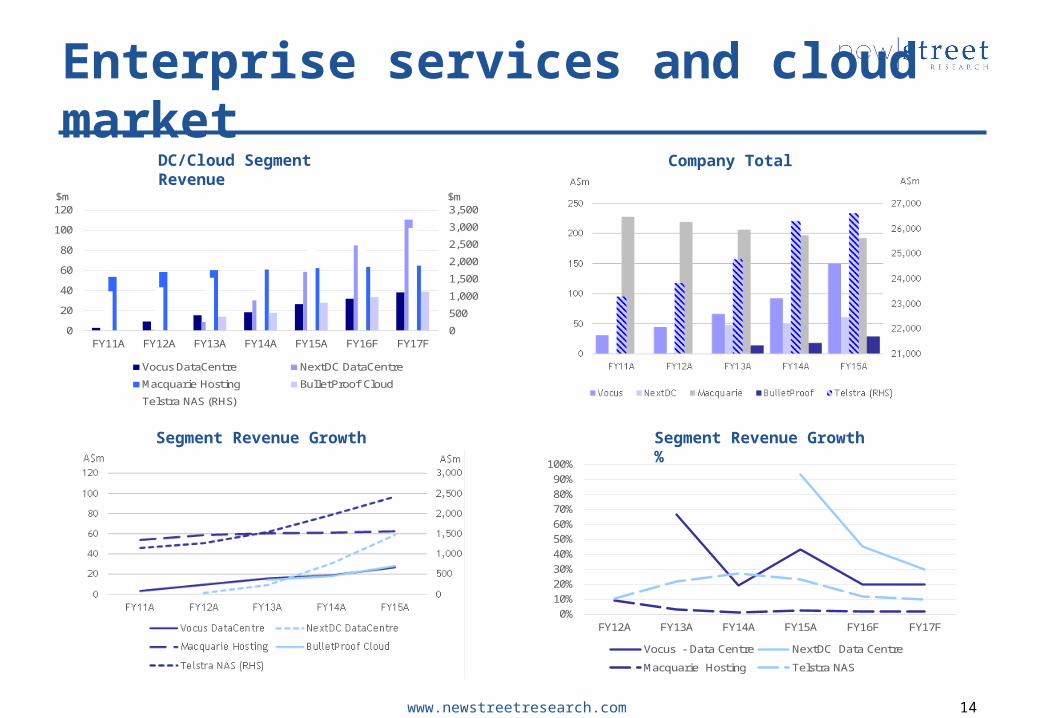

Enterprise services and cloud market

www.newstreetresearch.com 14

05001,0001,5002,0002,5003,0003,500

020406080

100120

FY11A FY12A FY13A FY14A FY15A FY16F FY17F

$m $m

Vocus DataCentre NextDC DataCentreMacquarie Hosting BulletProof CloudTelstra NAS (RHS)

DC/Cloud Segment Revenue

Company Total Revenue

0%10%20%30%40%50%60%70%80%90%

100%

FY12A FY13A FY14A FY15A FY16F FY17FVocus - Data Centre NextDC Data CentreMacquarie Hosting Telstra NAS

Segment Revenue Growth $

Segment Revenue Growth %

State of the Telecom NationTrend towards 2 or 3 full service playersand specialist (niche) RSPs

• Telstra: Ongoing leader in mobile, fixed and cloud/data• NBN: Value likely to be c50% of A$49bn-56bn spending • Optus: Maintaining position in mobile, losing ground in

fixed• Vodafone: Stopped the decline but lacks a case for next

stage• TPG: iiNet last big fixed line acquisition. Integration w VHA?

End of regulated subsidised access prices• Vocus: What role for a fourth player? Without mobile• Nextgen: What role for a fourth player? Without mobile• SpeedCast: Attractive satellite economics: growth by

acquisition• Small RSPs: Niche opportunities in mobile services and data

centrewww.newstreetresearch.com 15

Submarine Cable west coast routeDemand for new Australia-Asia subsea cable• Existing west coast cable is reaching end of design life: Sea-Me-We3 • Repairs, data transmission, latency, redundancy• Other Australian international cables all East Coast• Growth in data traffic and expected developments in demand for video

content

Three proposed west coast for the second west coast cable – Perth-Singapore…• APX West Cable System (APX), supported by SubPartners• Australia-Singapore Cable (ASC) NextGen and non-binding deal with

Vocus• Trident Sub-Sea Cable (TSC), private equity so far, has Indonesian

landing rights, looking for funding

…and one more proposal bypasses Asia to go straight to Middle East• Australia West Express (AWE) sponsored by GoTo Networkswww.newstreetresearch.com 16

Pop Quiz: Where is the value?Services or infrastructure?

Carrier/RSP A TPG

www.newstreetresearch.com 17

Network B TLS CANSubscribers 1.8m Physical connections +10m

Network Assets A$1.0bn Network Assets A$12bn

EBITDA A$775m EBITDA A$3.4bn

EBITDA margin 32% EBITDA margin 50%

Organic Growth Rate mid single digitOrganic Growth Rate mature

Capex A$300m Capex > A$1bn

Value A$9.4bn Value A$8.0bn

Telco is a capital intensive industryReflected in the access regime where there are three limbs of the LTIE• Competition• Capital efficiency• Any to any connectivity• Must give equal consideration to each: Federal Court 2006

Regulating the industry as if it isn’t capital intensive is a form of ‘industry policy rather than mature and independent regulation• ACCC backflip on access prices in 2009• Failure to evaluate risk in FAD• Inconsistent use of fixed price principles and allocation of NBN impact• Habit of saying one thing prior to investment commitment, and doing a

different thing after investment commitment (eg pre and post T3) • Approach has been to share the benefit of network investment but not

the riskACCC approach to access regulation has more in common with the automobile industry of the 1960s and 1970s than independent regulation

www.newstreetresearch.com 18

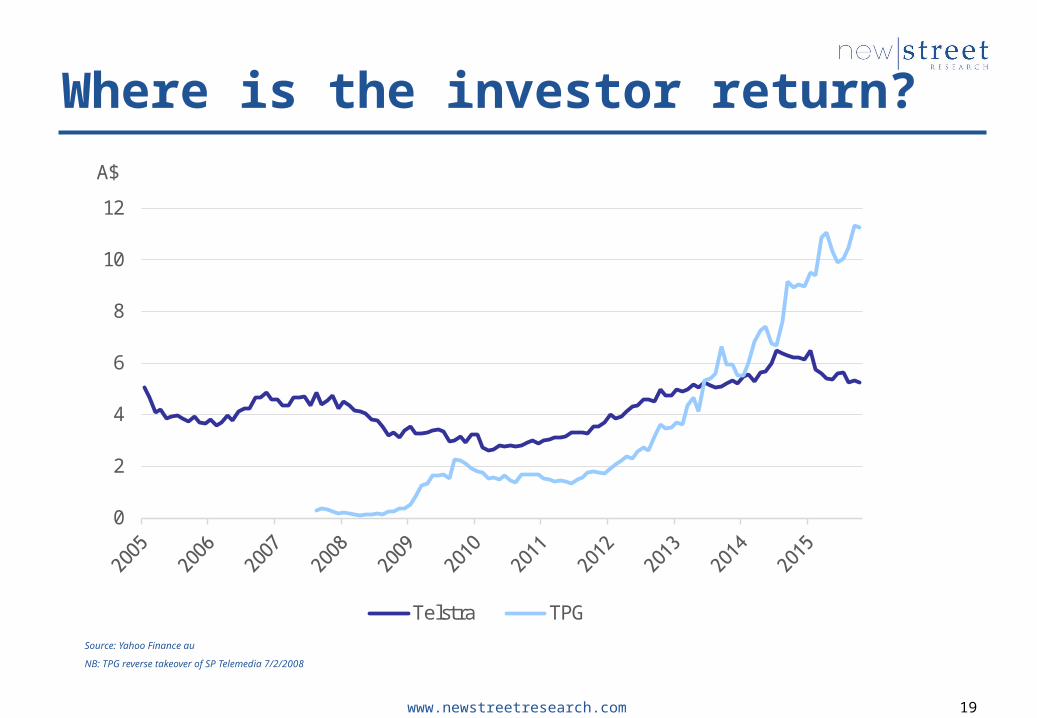

Where is the investor return?

www.newstreetresearch.com 19

Source: Yahoo Finance au

NB: TPG reverse takeover of SP Telemedia 7/2/2008

0

2

4

6

8

10

12A$

Telstra TPG

20

What might have been? AWA and mobile telephony, 1949

Source: AWA Annual Report 1949

Mobile wireless

www.newstreetresearch.com 21

This report was produced by New Street Research LLP. 11 Austin Friars, London EC2N 2HG

This document has been communicated to its clients by New Street Research LLP in accordance with its terms and conditions. This document is confidential and should not be communicated to persons other than the clients of New Street Research LLP.

The document is directed only to investment professionals, as defined in section 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001, and other persons to whom financial promotions may be lawfully communicated. The services provided by New Street Research LLP will only be provided to such persons. Persons who do not have professional experience in matters relating to investments should not rely on the contents of this document. New Street Research LLP is authorised and regulated in the conduct of its designated investment business in the United Kingdom by the Financial Services Authority. The contents of this document are subject to updating, completion, revision, further verification and amendment. The value of shares and other investments and the income derived from them may go down as well as up, and you may not get back the full amount you originally invested.

© 2016. New Street Research LLP.