26

Company Overview Larraín Vial 6 th Annual Andean Conference March 19 th – 20 th , 2012

Company Overview

Larraín Vial 6th Annual Andean Conference March 19th – 20th, 2012

Agenda

2

Business

Divisions

Financial

Review Company

Overview 3 9 19

3

CMPC is one of the most important players in the P&P industry

CMPC participates in many segments of the

P&P business; producing pulp, paper and

other forest products.

One of the highest rated credits in the industry

(BBB+) by S&P and Fitch.

Market capitalization of US$9.7 billion as of

February 29th, 2012, among he highest of the

P&P industry.

Controlled by the Matte Family, one of Chile’s

leading economic groups.

Figures for 2011 (MUS$):

• Sales: 4,797

• EBITDA: 1,078

• Net Income: 494

• Assets 13,294

• Net Debt: 2,451

P&P companies by market cap (BUS$)*

Shareholders’ Structure*

*As of February 29th, 2012. Source: Bloomberg

*As of December 31st, 2011. Source: CMPC

Local Investors

24,2%

Matte Group55,4%

Foreign Investors

8,9%

Chilean Pension

Funds11,4%

15,4

12,6

9,7

6,2

4,2

2,2

IP SCA CMPC Stora Enso Fibria Suzano

4

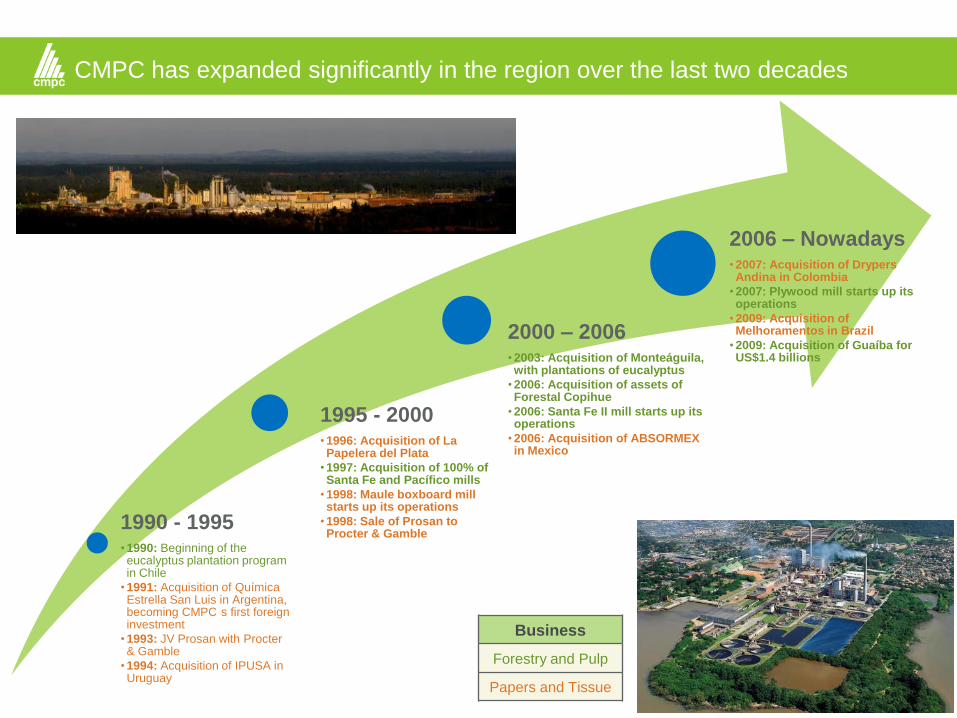

1990 - 1995 • 1990: Beginning of the eucalyptus plantation program in Chile

• 1991: Acquisition of Química Estrella San Luis in Argentina, becoming CMPC s first foreign investment

• 1993: JV Prosan with Procter & Gamble

• 1994: Acquisition of IPUSA in Uruguay

1995 - 2000 • 1996: Acquisition of La Papelera del Plata

• 1997: Acquisition of 100% of Santa Fe and Pacífico mills

• 1998: Maule boxboard mill starts up its operations

• 1998: Sale of Prosan to Procter & Gamble

2000 – 2006 • 2003: Acquisition of Monteáguila, with plantations of eucalyptus

• 2006: Acquisition of assets of Forestal Copihue

• 2006: Santa Fe II mill starts up its operations

• 2006: Acquisition of ABSORMEX in Mexico

2006 – Nowadays • 2007: Acquisition of Drypers Andina in Colombia

• 2007: Plywood mill starts up its operations

• 2009: Acquisition of Melhoramentos in Brazil

• 2009: Acquisition of Guaíba for US$1.4 billions

CMPC has expanded significantly in the region over the last two decades

Business

Forestry and Pulp

Papers and Tissue

5

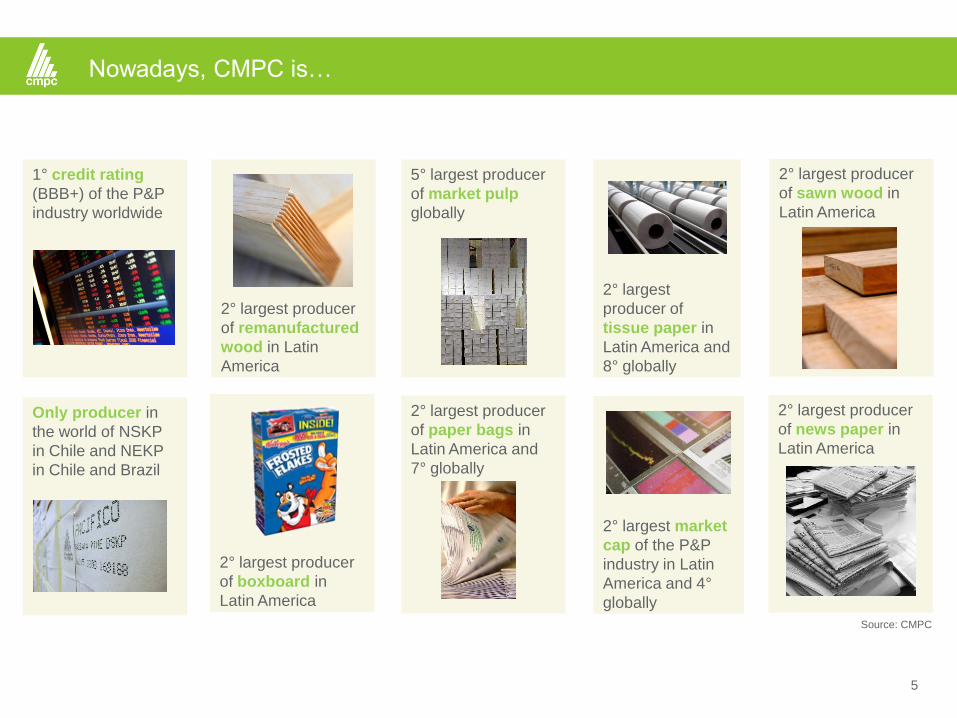

Nowadays, CMPC is…

2° largest producer

of sawn wood in

Latin America

2° largest producer

of remanufactured

wood in Latin

America

5° largest producer

of market pulp

globally

2° largest

producer of

tissue paper in

Latin America and

8° globally

2° largest producer

of news paper in

Latin America

2° largest producer

of boxboard in

Latin America

2° largest producer

of paper bags in

Latin America and

7° globally

1° credit rating

(BBB+) of the P&P

industry worldwide

2° largest market

cap of the P&P

industry in Latin

America and 4°

globally

Only producer in

the world of NSKP

in Chile and NEKP

in Chile and Brazil

Source: CMPC

6

Plywood

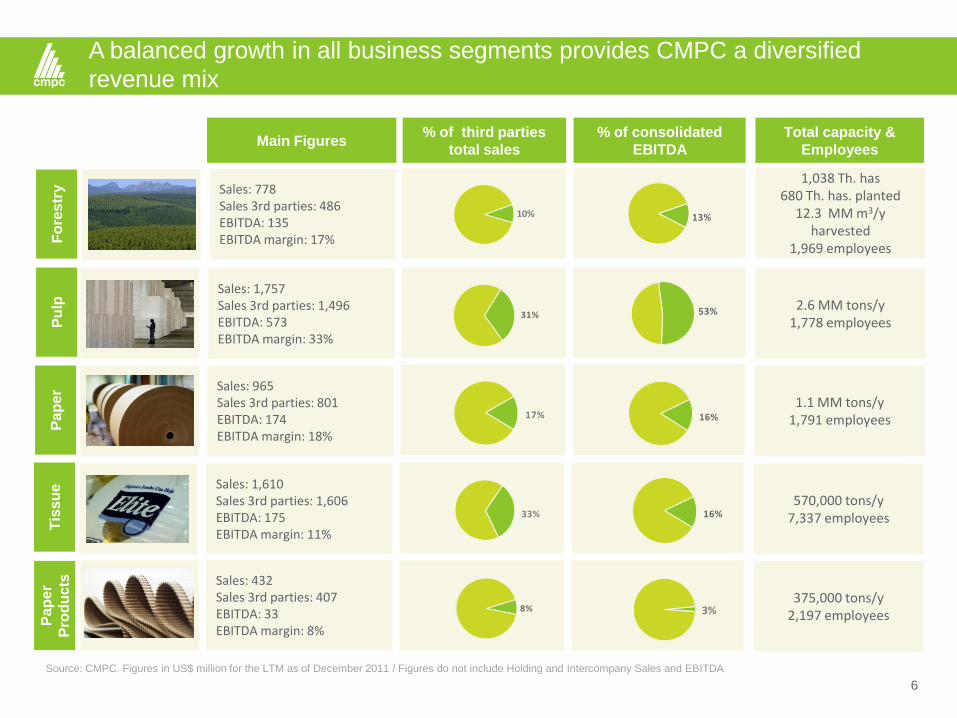

A balanced growth in all business segments provides CMPC a diversified

revenue mix

10%

31%

17%

33%

8%

Source: CMPC. Figures in US$ million for the LTM as of December 2011 / Figures do not include Holding and Intercompany Sales and EBITDA

1.1 MM tons/y

500,000 tons/y

Main Figures % of third parties

total sales

% of consolidated

EBITDA

Total capacity &

Employees

Fo

res

try

Pu

lp

Pap

er

Tis

su

e

Pa

pe

r

Pro

du

cts

Sales: 778 Sales 3rd parties: 486 EBITDA: 135 EBITDA margin: 17%

1,038 Th. has 680 Th. has. planted

12.3 MM m3/y harvested

1,969 employees

Sales: 1,757 Sales 3rd parties: 1,496 EBITDA: 573 EBITDA margin: 33%

2.6 MM tons/y 1,778 employees

Sales: 965 Sales 3rd parties: 801 EBITDA: 174 EBITDA margin: 18%

1.1 MM tons/y 1,791 employees

Sales: 1,610 Sales 3rd parties: 1,606 EBITDA: 175 EBITDA margin: 11%

570,000 tons/y 7,337 employees

Sales: 432 Sales 3rd parties: 407 EBITDA: 33 EBITDA margin: 8%

375,000 tons/y 2,197 employees

13%

16%

53%

16%

3%

7

Plywood

Product and geographic diversification provides flexibility

Source: CMPC. Figures in US$ million for the LTM as of December 2011.

Agenda

8

Business

Divisions

Financial

Review Company

Overview 3 9 19

9

Plywood

Forestry Division: the root of CMPC’s competitive advantage

Forestry

Chile:

730,335 has.

504,406 planted has.

Brazil:

213,104 has.

112,689 planted has.

Argentina:

94,283 has.

62,821 planted has.

Chile:

3 Sawmills:

Bucalemu,

Mulchén and

Nacimiento

Total capacity:

1,0 MM m3/y

Strategically located high quality timber assets and state of

the art facilities

Sawn wood

Chile:

2 Remanufacturing

plants:

Coronel and Los

Ángeles

Total capacity:

190 Th. m3/y

Ramanufactured

wood

Chile: • 1 Plywood mill:

Mininco

Total capacity:

240 Th. m3/y

Plywood

Source: CMPC

10

5,4 5,7 5,2 5,26,6

3,1 3,33,2

6,0

5,7

2007 2008 2009 2010 2011

Pine Eucaliptus

Forestry Division: the root of CMPC’s competitive advantage

What’s ahead…

• Chile and Brazil: acquisition of land, to increase CMPC’s forestry

base.

• New 240,000 m3/yr plywood line in Mininco, starting in 2013.

Key facts

• 100% planted and certified forests.

• Genetic and silvicultural practices / forest management to

enhance yield.

• Faster growth cycle .

• Proximity of forests to industrial facilities and ports.

• Young and growing forestry base

— Average age of CMPC’s Pine Forests: 13.4 years

— Average age of CMPC’s Eucalyptus Forests: 4.7 years

— Average ratio Planting / Harvesting: 1.4 times

Harvesting (million m3)

1.4x

Harvesting vs. Planting

21 2018

2528

3229

26

3735

2007 2008 2009 2010 2011

Harvest Plantations

Source: CMPC

Source: CMPC

11

BSKP1 Supply Curve (US$/ton)

Pulp Division: CMPC has one of the lowest cash costs of the pulp industry

Key facts

• First class assets.

• Strategic locations (mills near to forests and ports).

• One of the world’s lowest cost producer .

• Sales diversification.

• ISO, OHSAS certifications.

What’s ahead…

• Chile: revamping of Laja mill (110,000 tons of additional BSKP

capacity), starting in 2Q12.

• Debottlenecking of the Santa Fe II mill (200,000 tons of

additional BEKP capacity), starting in 1Q12.

• New turbo generators at the Laja and Santa Fe II mills.

• Brazil: Guaíba II line (1.3 million tons of additional BEKP

capacity), to be approved by the board.

BHKP2 Supply Curve (US$/ton)

Source: CMPC and Hawkins Wright as of February 2012

(1) BSKP: Bleached Softwood Kraft Pulp

(2) BHKP: Bleached Hardwood Kraft Pulp

CMPC’s pulp facilities

CMPC’s pulp facilities

12

Plywood

Pulp Division: CMPC has one of the lowest cash costs of the pulp industry

Chile

2 mills:

Pacífico (Pine)

Laja (Pine)

Total Capacity : 780 Th. tons/y

(890 Th. tons/y after April

2012)

Production capacity and distance from mills to forests and

ports

Softwood

Chile

2 mills:

Santa Fe I (Eucalyptus)

Santa Fe II (Eucalyptus)

Brazil

1 mill:

Riograndense

(Eucalyptus)

Total Capacity: 1.8 M tons/y

Hardwood

Santa Fe

Laja

Pacífico 163 Km.

93 Km.

119 Km.

Pacífico

Laja

Riograndense 80 Km.

80 Km.

93 Km.

Santa Fe 99 Km.

Riograndense 260 Km.

(By train)

(By train)

(By train)

(By barges)

CMPC’s average distance from… to…

13

Plywood

1

On December 15th 2009, Fibria transferred CMPC the ownership of a group of assets known as the Riograndense Unit for a total price of US$1,370 million. The

Riograndense Unit includes:

Sizable entry to Brazil.

Strategic location, complementary to existing facilities, to serve customers worldwide.

Ability to reconfigure sales, delivery and increase customers.

Ability to easily increase production to 1.75 million tons of pulp in the near future.

Potential to replicate CMPC Chile in one of the largest and most dynamic economies in the world.

Substantial forestry base and sylvicultural know-how.

Opportunity to further improve CMPC’s low cost producer status.

The Riograndense acquisition: the biggest project in CMPC’s History

Pulp mill with annual

production capacity of approx

450,000 tons

Paper mill with annual

production capacity of approx

60,000 tons

Approximately 212,000

hectares of land of which

125,000 are plantable

Licenses and authorizations to

execute an expansion project for the

pulp mill and increase its annual

capacity to app 1.75 mm tons

2 3 4

Riograndense

14

Plywood

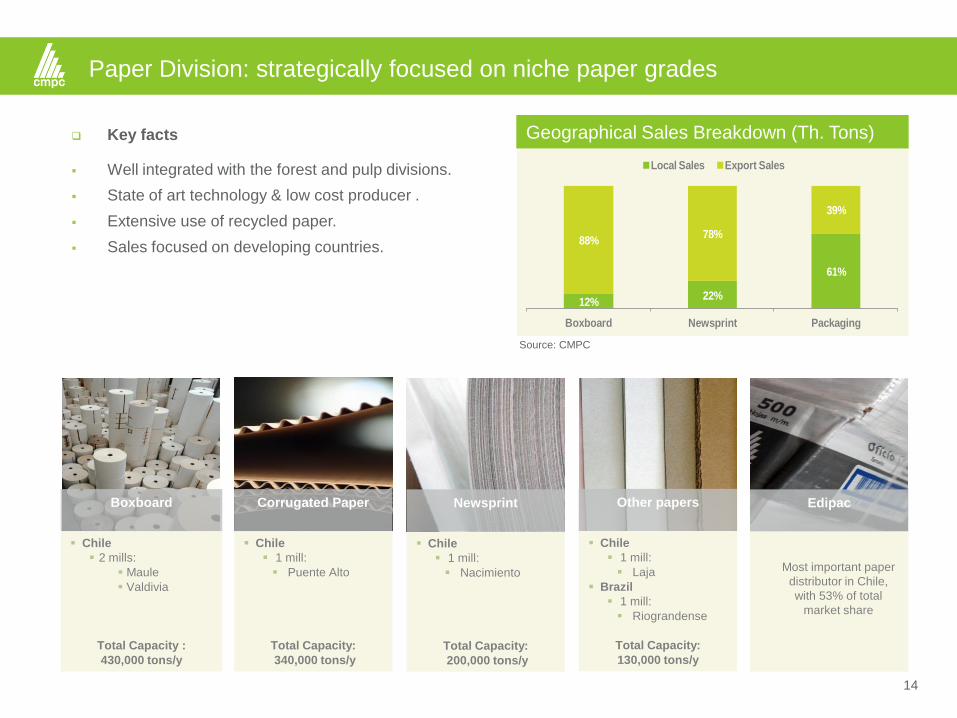

Paper Division: strategically focused on niche paper grades

Chile

2 mills:

Maule

Valdivia

Total Capacity :

430,000 tons/y

Boxboard

Chile

1 mill:

Puente Alto

Total Capacity:

340,000 tons/y

Corrugated Paper

Chile

1 mill:

Nacimiento

Total Capacity:

200,000 tons/y

Newsprint

Chile

1 mill:

Laja

Brazil

1 mill:

Riograndense

Total Capacity:

130,000 tons/y

Other papers

Most important paper

distributor in Chile,

with 53% of total

market share

Edipac

Key facts

Well integrated with the forest and pulp divisions.

State of art technology & low cost producer .

Extensive use of recycled paper.

Sales focused on developing countries.

Geographical Sales Breakdown (Th. Tons)

12%22%

61%

88%78%

39%

Boxboard Newsprint Packaging

Local Sales Export Sales

Source: CMPC

15

Plywood

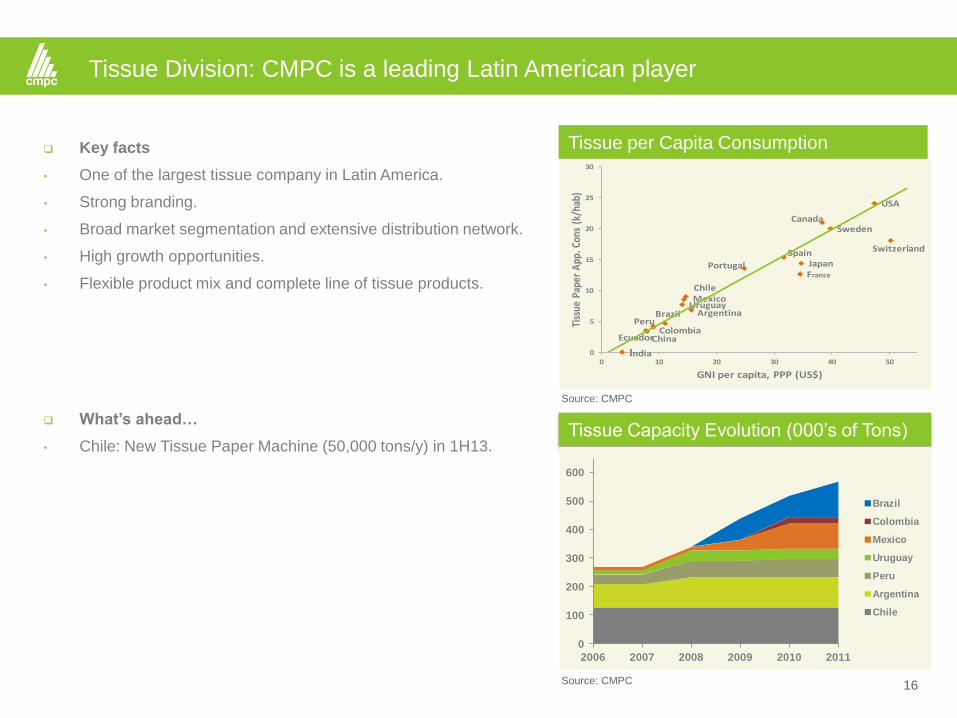

Tissue Division: CMPC is a leading Latin American player

Strong market share throughout the region

Market Share:

Capacity: 89,000 tons/yr

5%

Mexico (Since 2006)

Colombia (Since 2007)

Market Share:

Capacity: 125,000 tons/yr

11%

Brazil (Since 2009)

Market Share:

Capacity: 37,000 tons/yr 87%

Market Share:

Only Conversion Process

23%

Ecuador (Since 2009)

Market Share:

Capacity: 63,000 tons/yr

56%

Peru (Since 1996)

Market Share:

Capacity: 127,000 tons/yr

79%

Chile (since 1980)

Market Share:

Capacity: 106,000 tons/yr

48%

Argentina (Since 1991)

Market Share: 11%

Capacity: 22,000 tons/yr

Uruguay (Since 1994)

Tissue products

Baby & Adult

diapers

Feminine care

Away from

Home products

16

Tissue Division: CMPC is a leading Latin American player

Key facts

• One of the largest tissue company in Latin America.

• Strong branding.

• Broad market segmentation and extensive distribution network.

• High growth opportunities.

• Flexible product mix and complete line of tissue products.

What’s ahead…

• Chile: New Tissue Paper Machine (50,000 tons/y) in 1H13. Tissue Capacity Evolution (000’s of Tons)

Tissue per Capita Consumption

India

ChinaEcuador

PeruColombia

BrazilUruguayMexicoChile

Argentina

Portugal

Spain

France

Japan

CanadaSweden

USA

Switzerland

0

5

10

15

20

25

30

0 10 20 30 40 50

Tiss

ue P

aper

App

. Con

s (k

/hab

)

GNI per capita, PPP (US$)

0

100

200

300

400

500

600

2006 2007 2008 2009 2010 2011

Brazil

Colombia

Mexico

Uruguay

Peru

Argentina

Chile

Source: CMPC

Source: CMPC

17

Plywood

Paper Products Division: Local sales mainly oriented to export industries

Chile

4 mills:

Buin

Quilicura

Til Til

Osorno

Total Capacity : 287,000

tons/y

Corrugated boxes

Chile

1 mill:

Chillán

Argentina

1 mill:

Hinojo

Peru

1 mill:

Lima

Mexico

1 mill:

Guadalajara

Total Capacity: 70,000

tons/y

Paper bags

Chile

1 mill:

Puente Alto

Total Capacity: 18,000

tons/y

Molded pulp trays

Key drivers

Market leader in corrugated boxes and

multiwall bags markets in Chile.

Well diversified sales among different

segments of the market in corrugated

boxes.

Manufacturing process benefits from

backward integration.

Although a significant fraction of the sales

of this business area are local, CMPC

Paper Products is also expanding its

exports.

What’s ahead…

Mexico: new 40,000 tons paper bags mill

in Guadalajara, starting 2013.

Agenda

18

Business

Divisions

Financial

Review Company

Overview 3 9 19

19

Plywood

Financial Summary

4Q10 2010 3Q11 4Q11 2011 QoQ% YoY%

Sales 1.150 4.219 1.228 1.129 4.797 -8% -2%

Operating Costs (706) (2.572) (794) (795) (3.120) 0% 13%

Other Operating Expenses (143) (509) (155) (154) (598) -1% 7%0

EBITDA 302 1.138 278 180 1.078 -35% -40%

Depreciation & Stumpage (106) (387) (104) (105) (413) 1% -1%

Change in Net Value of Biological Assets (11) 59 23 50 110 114% -564%0

Operating Income 184 810 198 125 775 -37% -32%0

Financial Costs (34) (135) (42) (42) (163) -1% 22%

Other Non Operational Items 32 (36) (46) (10) (118) -79% -130%0

Net Income 182 640 109 73 494 -33% -60%

EBITDA Margin 26% 27% 23% 16% 22% -7% -42%

Total Assets 12.876 12.876 13.181 13.181 13.181 0% 2%

Total Liabilities 5.055 5.055 5.377 5.377 5.377 0% 6%

Shareholder's Equity 7.822 7.822 7.804 7.804 7.804 0% 0%

4Q11

20

267

115

248

-

494 495

167

291

48

99

285

303

244 160

2012 2013 2014 2015 2016 2018 2019 2027 2030

Bonds Banks Revolving

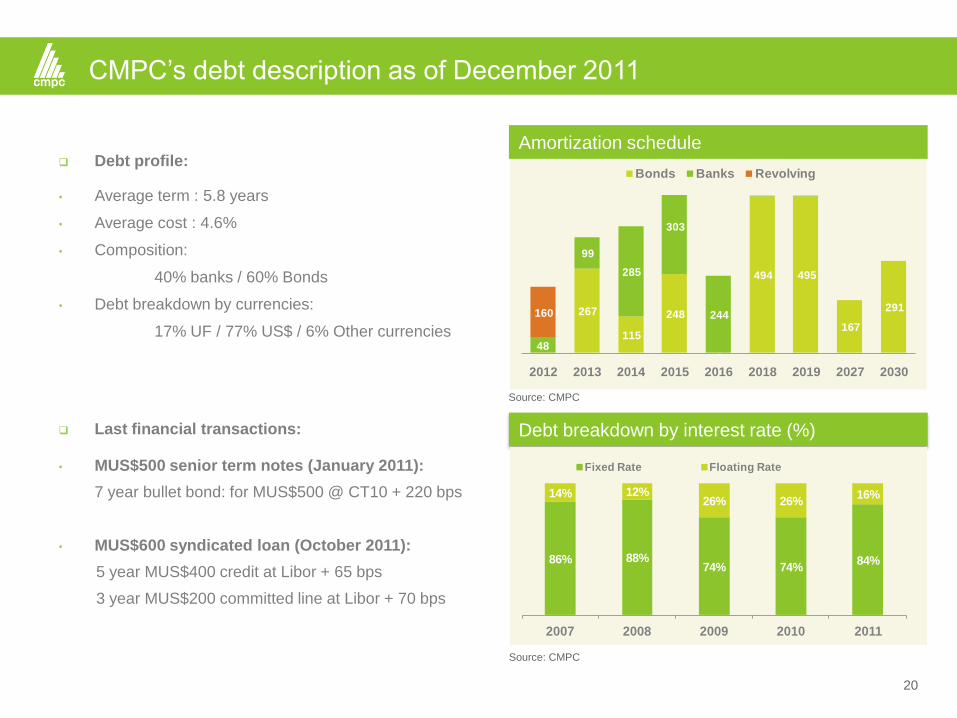

CMPC’s debt description as of December 2011

Last financial transactions:

• MUS$500 senior term notes (January 2011):

7 year bullet bond: for MUS$500 @ CT10 + 220 bps

• MUS$600 syndicated loan (October 2011):

5 year MUS$400 credit at Libor + 65 bps

3 year MUS$200 committed line at Libor + 70 bps

Debt profile:

• Average term : 5.8 years

• Average cost : 4.6%

• Composition:

40% banks / 60% Bonds

• Debt breakdown by currencies:

17% UF / 77% US$ / 6% Other currencies

Debt breakdown by interest rate (%)

Amortization schedule

86% 88%74% 74%

84%

14% 12%26% 26%

16%

2007 2008 2009 2010 2011

Fixed Rate Floating Rate

Source: CMPC

Source: CMPC

21

Plywood

Main financial metrics

*Figures as of 2007 and 2008 are under Chilean GAAPs. Figures for 2009, 2010 and 2011 are under the IFRS accounting standard.

Debt evolution (US$ million)*

1.362 1.3492.130 2.185 2.452

167 229

761 650822

2007 2008 2009 2010 2011

Net debt Cash

0,28x

0,33x

0,42x

0,37x

0,43x

2007 2008 2009 2010 2011

Net debt / EBITDA*

1,5x1,7x

3,3x

1,9x2,3x

2007 2008 2009 2010 2011

EBITDA / interest expenses*

11,9x

10,1x

6,3x

8,6x6,9x

2007 2008 2009 2010 2011

Financial debt / equity*

Source: CMPC

Source: CMPC Source: CMPC

Source: CMPC

22

Plywood

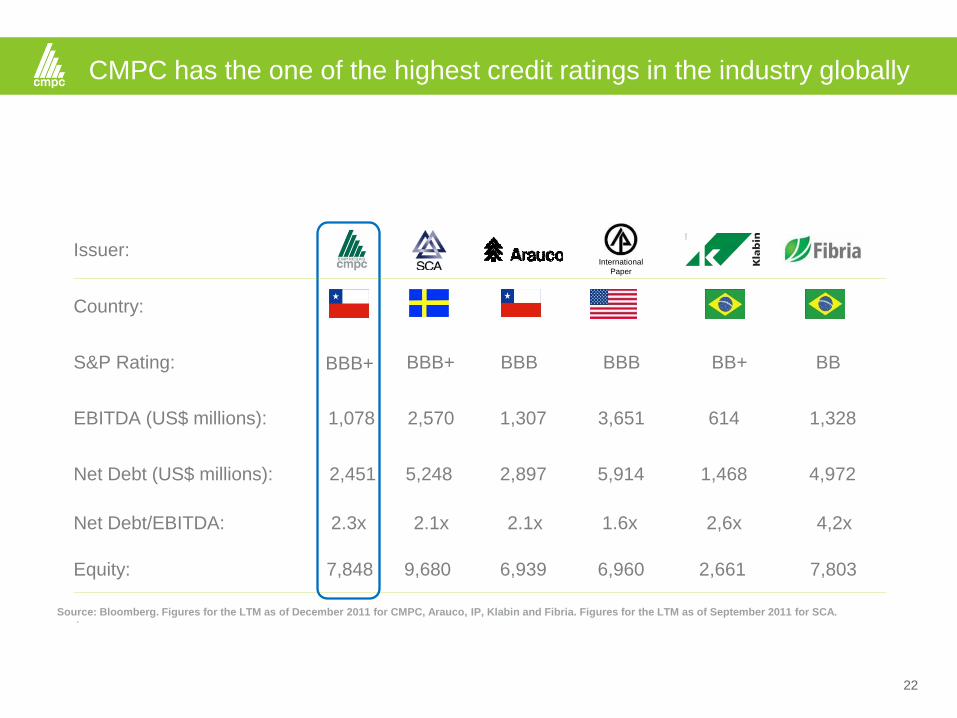

CMPC has the one of the highest credit ratings in the industry globally

Country:

S&P Rating: BBB+ BBB+ BBB BBB BB BB+

EBITDA (US$ millions): 1,078 2,570 1,307 3,651 1,328 614

Net Debt (US$ millions): 2,451 5,248 2,897 5,914 4,972 1,468

International

Paper

.

Issuer:

Net Debt/EBITDA: 2.3x 2.1x 2.1x 1.6x 4,2x 2,6x

Equity: 7,848 9,680 6,939 6,960 7,803 2,661

Source: Bloomberg. Figures for the LTM as of December 2011 for CMPC, Arauco, IP, Klabin and Fibria. Figures for the LTM as of September 2011 for SCA.

23

Plywood

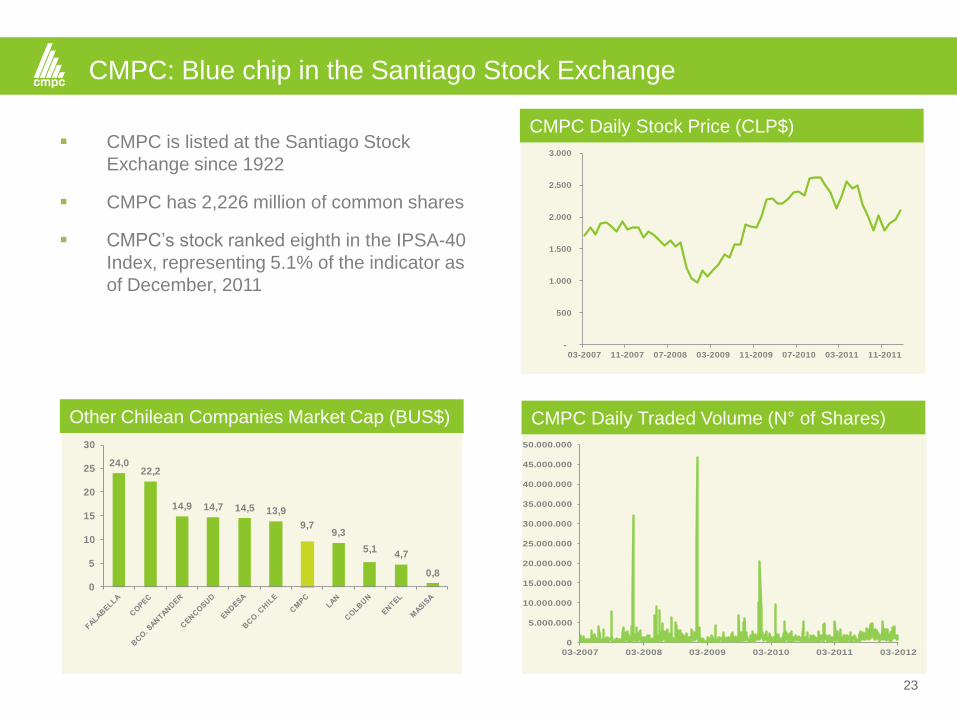

CMPC: Blue chip in the Santiago Stock Exchange

CMPC is listed at the Santiago Stock

Exchange since 1922

CMPC has 2,226 million of common shares

CMPC’s stock ranked eighth in the IPSA-40

Index, representing 5.1% of the indicator as

of December, 2011

CMPC Daily Stock Price (CLP$)

CMPC Daily Traded Volume (N° of Shares) Other Chilean Companies Market Cap (BUS$)

-

500

1.000

1.500

2.000

2.500

3.000

03-2007 11-2007 07-2008 03-2009 11-2009 07-2010 03-2011 11-2011

24,022,2

14,9 14,7 14,5 13,9

9,79,3

5,14,7

0,8

0

5

10

15

20

25

30

0

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

30.000.000

35.000.000

40.000.000

45.000.000

50.000.000

03-2007 03-2008 03-2009 03-2010 03-2011 03-2012

24

Investment Highlights

CMPC is:

World class company in the industry.

Low cost producer in most of our product lines.

Products and geographical diversification allows strong cash.

generation in spite of economic and price cycles.

One of the highest rated credits in the industry.

Committed to sustainable growth.

Strong balance sheet prepared for growth opportunities.

Experienced management and strong shareholders.

25

Disclaimer

The foregoing material is a presentation of general background information about CMPC’s activities as of the date of the presentation. It is

information given in a summary form and does not purport to be complete. It is not intended to be relied upon as advice to investors or

potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. These

should be considered, with or without professional advice, when deciding if an investment is appropriate.

Forward Looking Statements

This presentation contains statements that constitute “forward-looking statements” within the meaning of securities laws of applicable

jurisdictions. Examples of these forward-looking statements include, but are not limited to (i) statements regarding our future results of

operations and financial condition, (ii) statements of plans, objectives or goals, and (iii) statements of assumptions underlying those

statements. Words such as “may,” “will,” “expect,” “intend,” “plan,” “estimate,” “anticipate,” “believe,” continue”, “probability,” “risk,” and

other similar words are intended to identify forward-looking statements but are not the exclusive means of identifying those statements. By

their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that the

predictions, forecasts, projections and other forward-looking statements will not be achieved. We caution readers that a number of

important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions

expressed in such forward-looking statements.

Q & A

March 2012