22

Company Presentation Mensch und Maschine Software SE August 2008

CompanyPresentation

Mensch und Maschine Software SE

August 2008

Business model

Mensch und Maschine Software SEis one of the leading vendors of CAD/CAM solutions in Europe(CAD/CAM = Computer Aided Design/Manufacturing)

Well balanced business model within the CAD/CAM market in three respects:

Geographical markets Customers and industry segments Product portfolio

Business model Geographical markets:

Market access in 16 European countries

New since February 2008: Romania

Additional sales offices in the USA, APAC and Japan

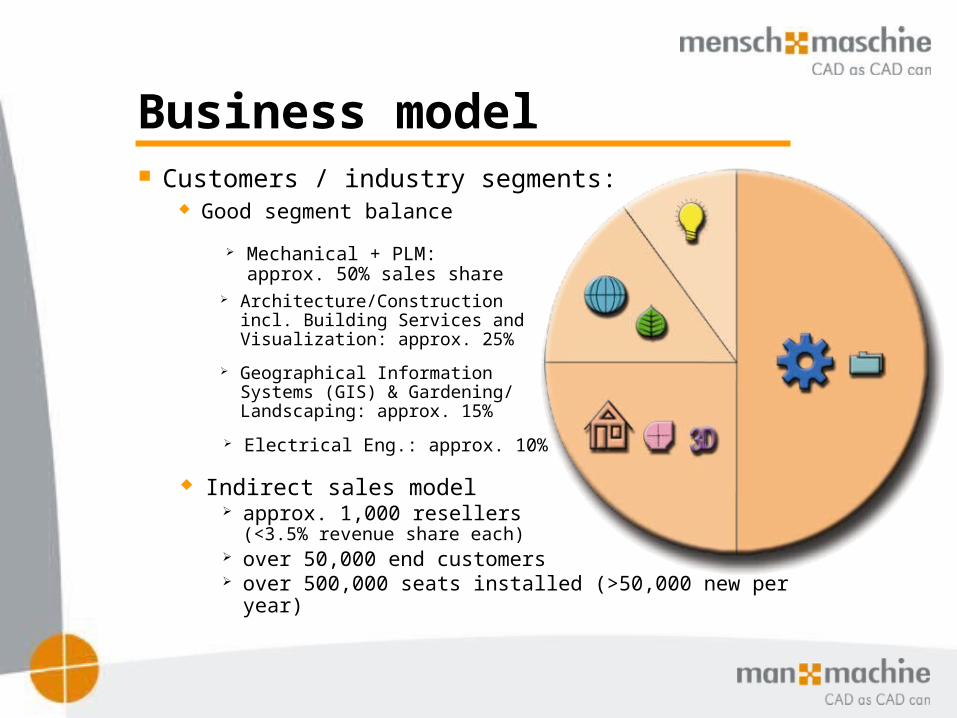

Business model Customers / industry segments:

Good segment balance Mechanical + PLM:

approx. 50% sales share Architecture/Construction

incl. Building Services and Visualization: approx. 25%

Geographical Information Systems (GIS) & Gardening/ Landscaping: approx. 15%

Electrical Eng.: approx. 10%

Indirect sales model approx. 1,000 resellers

(<3.5% revenue share each) over 50,000 end customers over 500,000 seats installed (>50,000 new per year)

Business model Product portfolio: Software development/distribution balance

M+M Software development (M+M Technology) Concentration on applications in addition to CAD standards High gross margin ~90%, 2007 EBIT margin 16.6% (potential 20-25%) Important for differentiation and profile in the CAD/CAM market

Value-Added Software Distribution (Trading products) Concentration on CAD market leader Autodesk High sales, gross margin ~16%, 2007 EBIT margin 3.2% (potential 4-5%) Important for market position

Gross margin mix: ~44% M+M software / ~56% Distribution

Approx. 2/3 sales new business + 1/3 recurring business

Wide price/performance range: Software from 100 Euro to more than 100,000 Euro per seat

Target market

Market volume CAD/CAM Software&Services: Worldwide > 10 bln EUR

(Sources: Daratech, Dressler-Verlag, own research)

Europe: > 3 bln EUR Market share M+M in Europe:

directly approx. 7% indirectly approx. 15% (end customer sales by resellers)

Market growth / market development: Solid market growth 5-10% p.a. M+M well positioned in growth segments e.g.:

Indirect sales / mid price systems CAM (highly innovative 5 axis milling)

History & Culture

M+M was founded in 1984 by Adi Drotleff 24 years of market experience / developed market position Public since 1997 / Listing in Prime standard

Developed Corporate Culture Employees in the M+M group are „Co-Entrepreneurs“

(profit oriented remuneration, options, decision making processes)

Low fluctuation & sickness rate

Experienced Management Team Most members are >10 years in the company Strong 2nd/3rd management level

M+M is European SE Since 12/2006, MuM is SE (Societas Europaea)

Seated in seven EU states, M+M already has the target SE structure – simple conversion was possible (Art 2 (4) EU-D. 2157)

Monistic board system Ideal board structure for entrepreneurial public company with a

shareholders‘ meeting majority held by management board Administrative Board: Adi Drotleff, Norbert Kopp, Thomas Becker Managing Directors: Adi Drotleff (CEO), Werner Schwenkert

(CTO), Peter Schützenberger (CFO), Michael Endres (Marketing), Jens Jansen (CIO)

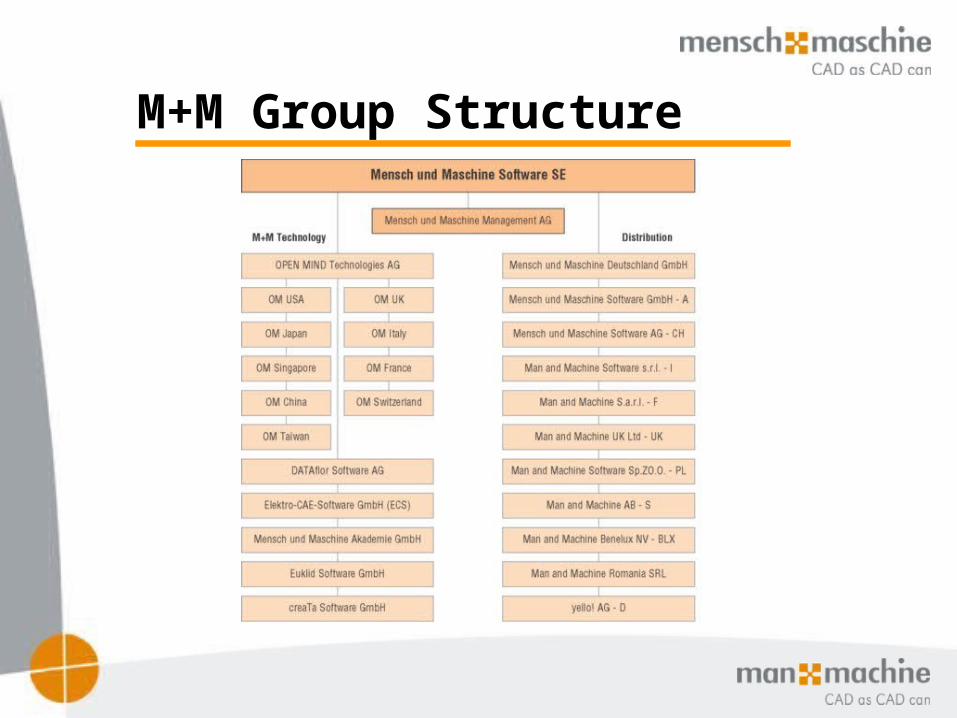

M+M SE is pure group holding Operating business through subsidiaries

M+M Group Structure

Marketing Instruments Strong presence at trade shows:

2007: 47 shows in 14 countries

Live presentations via Internet 2007: ~600 presentations with

approx. 3,000 attendees Rapidly growing trend

Prospects database / CRM approx. 150,000 addresses Lead qualification (Telemarketing) Highly developed lead management dealers/endusers

approx. 10,000 qualified leads per yearpassed on to authorized dealers

IT / Web / Back office Nearly all M+M group members

using SAP R/3 as ERP system Integrated CRM system

(Customer Relationship Management)

Fully integrated online shop: >60% online order entry Direct SAP access for

M+M’s authorized dealers

SCM (Supply Chain Management) Automatic order processing with suppliers and customers Target: driving online order entry quota towards 100% High cost- & time savings, error reduction

Autodesk to buy ecscad

Adhoc news August 20, 2008: Autodesk to buy ecscad technology from M+M

After Compass, C-Plan and RoCAD, ecscad is the fourth application technology Autodesk acquires from M+M

Only development and IP is sold to Autodesk, M+M continues to actively market and sell ecscad

– No material impact on future sales and earnings

Purchase price represents ~2.5x annual sales Estimated net cash inflow 2008 approx. EUR 2.5 mln

(after minority shares and escrow)

Estimated pretax disinvestment profit 2008 approx. EUR 2.0 mln

Closing scheduled for Q3/2008

Sales development Sales 2007: EUR 212.9 mln / +25%

CAGR 1997-2007: 15% p.a. Sales per share more than doubled:

1997: EUR 6.67 / 2007: EUR 16.64 International sales grew from

25% to 75% since 1997

0

25

50

75

100

125

150

175

200

225

97 98 99 00 01 02 03 04 05 06 07

Internat'lGermany

0

25

50

75

100

125

150

175

200

225

97 98 99 00 01 02 03 04 05 06 07

Internat'lGermany

+15%

p.a.

Quarterly seasonality 2007: Q1 with positive non-recurring effects Q4 slightly slower than normal

Sales 2008: Q1: EUR 67.0 mln / +4% Q2: EUR 52.6 mln / +15% 1-6: EUR 119.6 mln / +9% 0

25

50

75

Q1 Q2 Q3 Q4

200620072008

0

25

50

75

Q1 Q2 Q3 Q4

200620072008

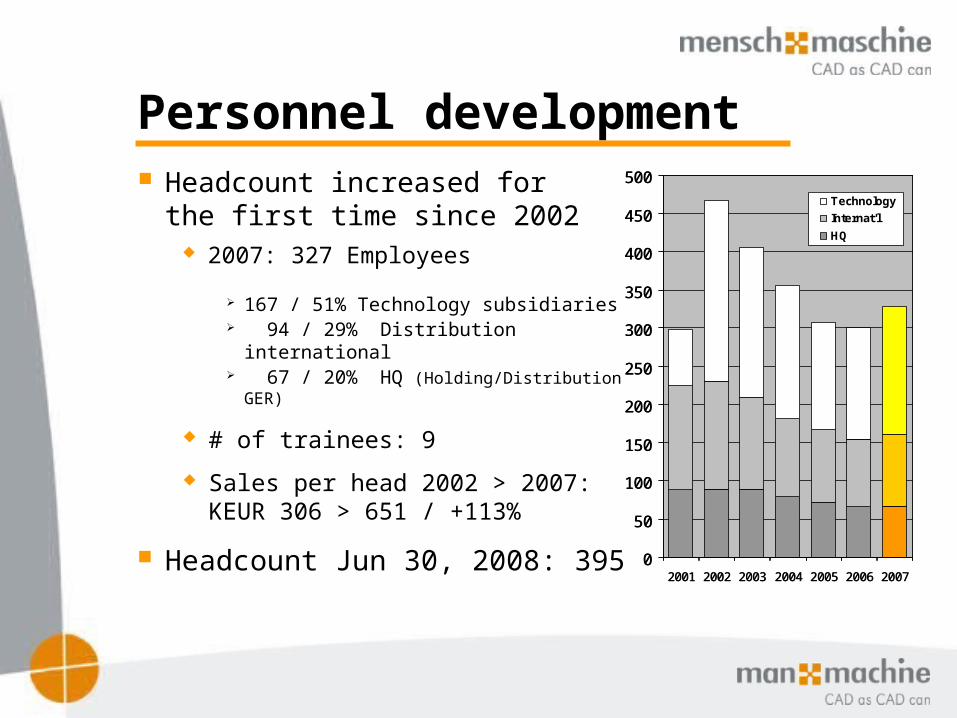

Personnel development Headcount increased for the

first time since 2002 2007: 327 Employees

167 / 51% Technology subsidiaries 94 / 29% Distribution international 67 / 20% HQ (Holding/Distribution GER)

# of trainees: 9

Sales per head 2002 > 2007: KEUR 306 > 651 / +113%

Headcount Jun 30, 2008: 395 0

50

100

150

200

250

300

350

400

450

500

2001 2002 2003 2004 2005 2006 2007

Technology

Internat'l

HQ

0

50

100

150

200

250

300

350

400

450

500

2001 2002 2003 2004 2005 2006 2007

Technology

Internat'l

HQ

Development of expenses 2002-2005, operating expense base

was lowered by approx. EUR 10 mln

2007: Opex EUR 45.5 mln Sales&Marketing: EUR 28.1 mln / +7% General&Admin: EUR 10.1 mln / +12% Development: EUR 7.3 mln / +22%

Attention: R&D expenses only occur for software development segment, not for trading segment

No capitalization of development costs according to IAS 38.45

Software library including many hundred man years of invested development is a hidden reserve

1-6/2008: Opex +9%

S&M62%

G&A22%

R&D16%

0

10

20

30

40

50

60

01 02 03 04 05 06 07

R&DG&AS&M

0

10

20

30

40

50

60

01 02 03 04 05 06 07

R&DG&AS&M

Profit development Operating profit EBITA 2007

EUR 10.0 mln (PY: 6.8 / +47%) EBITA margin 4.7% (PY: 4.0%) Quarterly seasonality following sales EBITDA 2007: EUR 10.9 mln (PY: 7.7)

0

2

4

6

8

10

12

2005 2006 2007

EBITA

Netto

Net earnings 2007 nearly doubled:EUR 6.1 mln (PY: 3.2)

Per share: EUR 0.47 (PY: 0.24) Dividend (tax free): EUR 0.20 (PY: 0.15)

Results 1-6/2008: EBITA: EUR 6.04 mln / +4% (Q2: +30%) Net: EUR 3.71 mln / +7% (Q2: +29%) Best first half year in company history

0

2

4

6

8

10

12

2005 2006 2007

EBITA

Netto

0

2

4

6

8

10

12

2005 2006 2007

EBITA

Netto

0

1

2

3

4

5

Q1 Q2 Q3 Q4

200620072008

0

1

2

3

4

5

Q1 Q2 Q3 Q4

200620072008

0

10

20

30

40

2001 2002 2003 2004 2005 2006 2007

50

60

70

80

90

2001 2002 2003 2004 2005 2006 2007

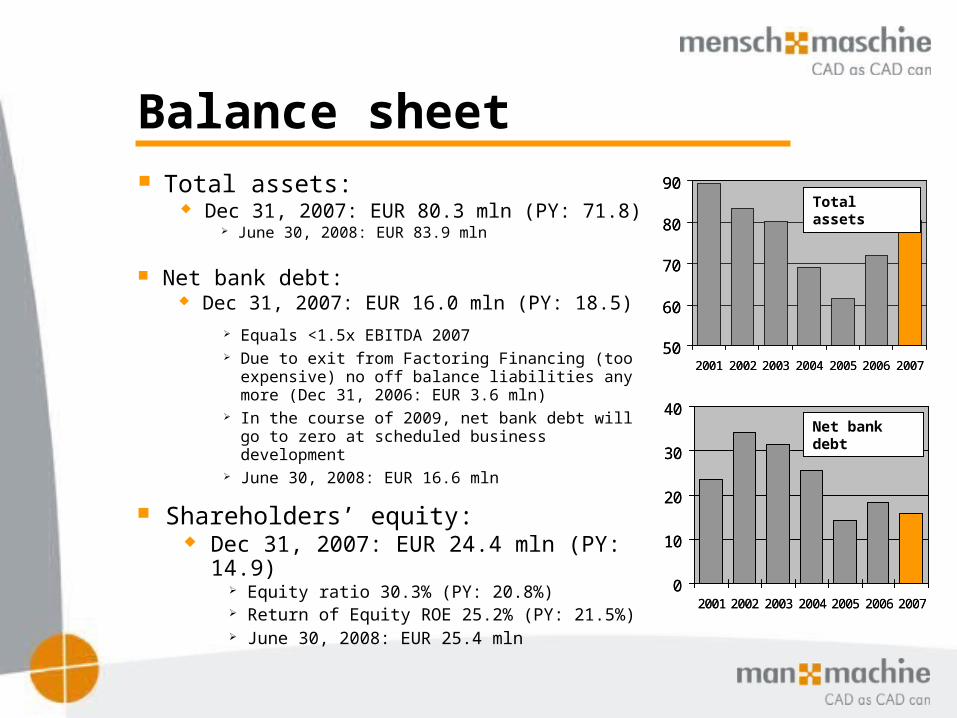

Balance sheet Total assets:

Dec 31, 2007: EUR 80.3 mln (PY: 71.8) June 30, 2008: EUR 83.9 mln

Net bank debt: Dec 31, 2007: EUR 16.0 mln (PY: 18.5)

Equals <1.5x EBITDA 2007 Due to exit from Factoring Financing (too

expensive) no off balance liabilities any more (Dec 31, 2006: EUR 3.6 mln)

In the course of 2009, net bank debt will go to zero at scheduled business development

June 30, 2008: EUR 16.6 mln

Shareholders’ equity: Dec 31, 2007: EUR 24.4 mln (PY: 14.9)

Equity ratio 30.3% (PY: 20.8%) Return of Equity ROE 25.2% (PY: 21.5%) June 30, 2008: EUR 25.4 mln

50

60

70

80

90

2001 2002 2003 2004 2005 2006 2007

0

10

20

30

40

2001 2002 2003 2004 2005 2006 2007

Total assets

Net bank debt

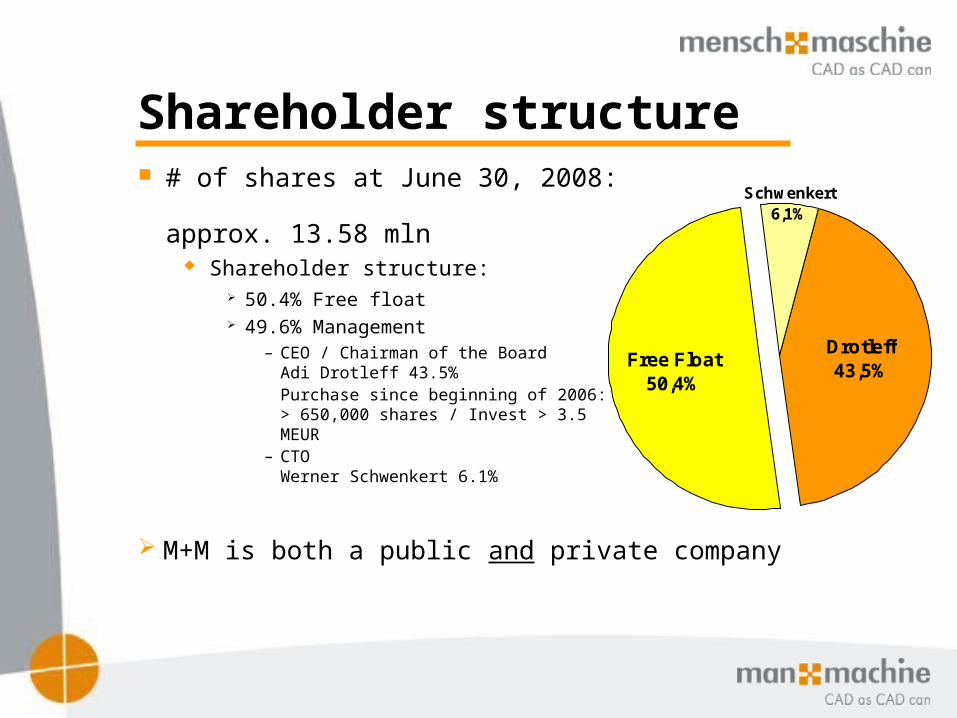

Shareholder structure # of shares at June 30, 2008:

approx. 13.58 mln Shareholder structure:

50.4% Free float 49.6% Management

– CEO / Chairman of the Board Adi Drotleff 43.5%Purchase since beginning of 2006:> 650,000 shares / Invest > 3.5 MEUR

– CTO Werner Schwenkert 6.1%

M+M is both a public and private company

Schwenkert6,1%

Free Float50,4%

Drotleff43,5%

Investor Relations Designated Sponsors:

LBBW, Stuttgart Close Seydler, Frankfurt

Analyst coverage: LBBW: „Buy“ - fair value EUR 7.60 Independent Research: „Buy“ - fair value EUR 7.70 SES Research: „Buy“ - fair value EUR 7.00 Performaxx: „Buy“ – fair value EUR 9.62 GSC Research: „Buy“ – fair value EUR 7.50

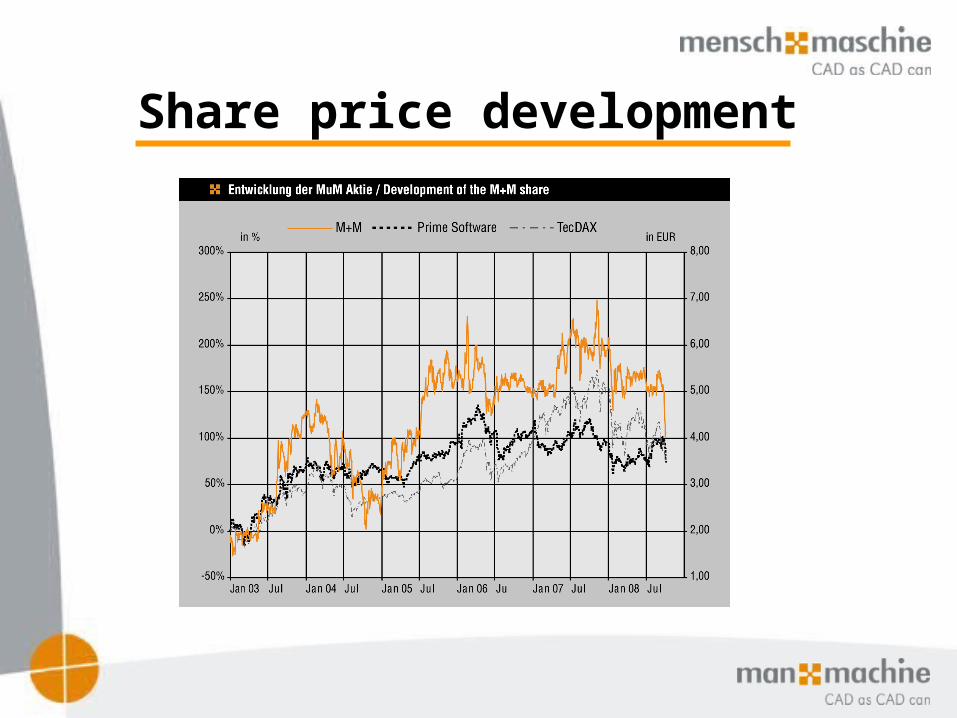

Share price development

Outlook Mid term goal: Moderate sales growth /

focus on improvement of profit margin Targets 2008:

Sales: EUR ~240 mln / ~+13% EBITA margin ~5.5% (2007: 4.7%)

EUR ~13 mln / ~+30% Net profit: EUR ~8.6 mln / ~+40%

approx. EUR 0.62 per share Dividend EUR 0.25 per share (tax free)

Targets 2009: Sales: EUR ~275 mln / ~+15% EBITA: EUR ~16.5 mln / margin ~6.0% Net profit: EUR ~11.6 mln / ~+35%

approx. EUR 0.84 per share Dividend EUR 0.30 per share (tax free)

0

50

100

150

200

250

300

2005 2006 2007 08E 09E

0

4

8

12

16

20

2005 2006 2007 08E 09E

EBITA

Netto

0

50

100

150

200

250

300

2005 2006 2007 08E 09E0

50

100

150

200

250

300

2005 2006 2007 08E 09E

0

4

8

12

16

20

2005 2006 2007 08E 09E

EBITA

Netto

0

4

8

12

16

20

2005 2006 2007 08E 09E

EBITA

Netto

0

4

8

12

16

20

2005 2006 2007 08E 09E

EBITA

Netto

0

4

8

12

16

20

2005 2006 2007 08E 09E

EBITA

Netto

Sales

Investment Highlights

Mensch und Maschine is: Established in the CAD/CAM market for 24 years Both a public and private company

Mensch und Maschine has: A good market position in a growth market A well balanced business model A consolidated growth story A profit margin potential for further improvement A conservative market valuation (P/S <0.4 / P/E08E <10) A good dividend yield (2008E: ~4.5-5.0% net)