71

1 Compensation A Multi-Dimensional Analysis

| Date post: | 05-Jun-2018 |

| Category: |

Documents |

| Upload: | truonglien |

| View: | 214 times |

| Download: | 0 times |

1

Compensation

A Multi-Dimensional Analysis

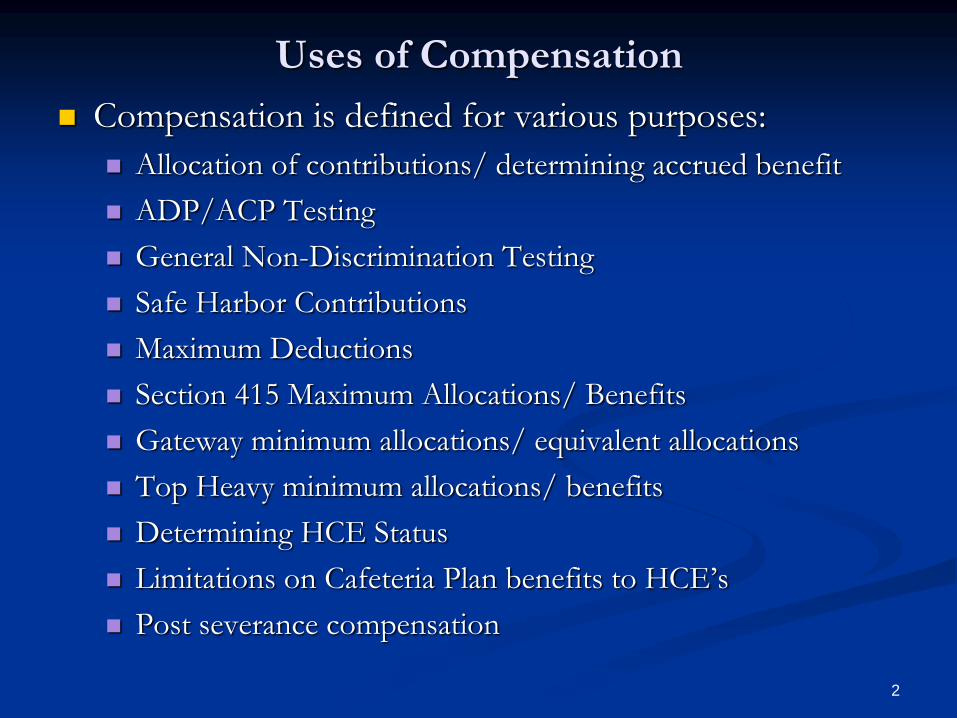

2

Uses of Compensation

Compensation is defined for various purposes:

Allocation of contributions/ determining accrued benefit

ADP/ACP Testing

General Non-Discrimination Testing

Safe Harbor Contributions

Maximum Deductions

Section 415 Maximum Allocations/ Benefits

Gateway minimum allocations/ equivalent allocations

Top Heavy minimum allocations/ benefits

Determining HCE Status

Limitations on Cafeteria Plan benefits to HCE’s

Post severance compensation

3

Defining Compensation

Section 415 contains the central definition

See Reg §1.415(c)-2

Applies to

§415 maximum allocations/ benefits- 100% rule

Top heavy minimum allocations/ benefits

Maximum deductions (§404(a)(12))

Determination of HCE’s

Implicitly-determine from what compensation participants

can make salary deferrals and can receive allocations of

contributions/ accruals of benefits

4

Defining Compensation

What’s included?

Wages and all other cash compensation for personal services performed for the employer maintaining the plan

Non-Cash compensation relating to these services

Specifically- Salary, commissions, tips, bonuses, share of profits, etc.

Compensation must be earned as an employee

Amounts that would have been included in income except it was deferred under §§401(k), 403(b), 457(b), 125, 132(f)(4) (bus tokens)

5

Defining Compensation

What’s included?

Taxable fringe benefits

Include the taxable portion of health and disability insurance

Specialty Items

Moving expense reimbursement that is taxable

Taxable non-statutory stock options in the year granted

Deferred compensation taxable under §409A

6

Defining Compensation

What’s Included?

Amounts constructively received (also amounts

included under §83(b))

What’s Excluded?

Non-taxable contributions/ value of benefits under

qualified or non-qualified deferred compensation

plans

Distributions from qualified or non-qualified

deferred compensation plans

Taxable amounts from exercise of non-statutory

options

7

Defining Compensation

What’s Excluded?

Taxable amounts from sale of stock received under a

statutory option

Implicitly, amounts not taxable pursuant to the exercise of

a statutory option

Untaxed fringe benefits that are employer paid (such

as group term life)

Compensation in excess of §401(a)(17) limit is

disregarded. See Reg §1.415(c)-2(f).

Apply 401(a)(17) limit to each year involved

Pre-EGTRRA years (up through 2001) can use $200K if

elected in plan

8

Defining Compensation

What’s Excluded?

Severance Pay

Not permitted to be counted

Distinguish from regular pay, bonuses, commissions

that would have been paid if employment had

continued

9

Defining Compensation

What can the plan choose to exclude?

Amounts received under a non-qualified, unfunded

deferred compensation plan, in the year received

What can the plan choose to include?

Payment of unused sick leave and vacation pay

subject to timing rules

Hypothetical compensation for disabled participant

10

Earned Income

Self-Employed Persons

Proprietorships

Partnerships

Limited Liability Companies

Receive no wages

“Earned income” from performance of services

11

Earned Income

Self-Employed Persons

“Earned income” from performance of services

Refer to Schedule SE of Form 1040

What about Shareholders of S Corps

They should receive wages

Dividend income reported in Form K1

What if some K1 income transferred to Schedule SE

Is this permissible?

Reserve only for damage control

12

Earned Income

Self-Employed Persons

Rules for “Traders”

Stocks and bonds

Ordinarily short term capital gain

Can make election to be treated as a dealer

Then earned income

Full recognition of losses

Commodities and Index Futures

Blended short and long term CG rates

Ordinarily not earned income

Can make election to be treated as a dealer

Must have use of an exchange membership

Do not need to trade “on the floor”

Earned income applies for retirement plan

13

Defining Compensation

Safe Harbor Definitions- Reg §1.415(c)-2(d)

Alternatives to general definition

Must be provided in plan document

Include all cash and non-cash compensation, but exclude

Health and disability insurance contributions paid by employer and taxable

Moving expense

Taxable non-qualified deferred compensation

Non-statutory stock option

Section 83(b) amounts

14

Defining Compensation

Safe Harbor Definitions- Reg §1.415(c)-2(d)

Section 3401 wages

Wages subject to withholding

Include salary deferral amounts

These safe harbors omit items that are harder to measure

Period for measuring §415 Comp

Limitation year for §415 purposes

Calendar year

Plan year

15

Defining Compensation

Period for measuring §415 Comp

Limitation year for §415 purposes

Calendar year

Plan year

16

Defining Compensation

Period for measuring §415 Comp

Limitation year

Calendar year ending within plan year

Plan year

Minor timing differences

Paid in the first few weeks of next year

All participants treated the same

No double counting

Eg. Weekly payroll that staggers the calendar year

17

Defining Compensation

Period for measuring §415 Comp

Payment after severance of employment

Later of: end of limitation year or 2 ½ months after severance

Must count-

All pay, commissions, bonuses, etc. that would have been paid had employment continued

May count (see plan provision-amendment)

Accrued sick, vacation pay

Payments under non-qualified unfunded deferred compensation plan that would have been paid anyways

18

Defining Compensation

Period for measuring §415 Comp May not count severance pay

Some pretend compensation can count

Disabled participants

Total disability

Impute compensation based on prior rate of pay

NHCE’s only or all employees who are totally disabled

will receive contributions for a fixed period

Optional provision

Back pay is compensation for the period to which it

applies

19

Defining Compensation

Participants in active military service

USERRA (§414(u)(8)) and HEART (§414(u)(9)) See Rev Notice 2010-15

Differential wage payments

Can use this as compensation from which deferrals can be made

Optionally, count as compensation for profit sharing allocations

Participants considered “in service” so top heavy minimum applies to top heavy plans and is not optional

For soldiers who die or are disabled in active duty: Match may be contributed based on imputed salary deferrals using previous rate of deferrals

20

Example

“Retiring” president of a small bank leaves at the end of May

He receives a bonus in June and another in January of the following year

He normally receives an end of year bonus

Bank stock is publicly traded

Declaration of bonus is posted on SEC web site

Language makes it clear the payment is in the nature of a severance payment

Payment is being made to “settle” the contract with former president

21

Example- Analysis

Was the payment being made for services performed?

Would the payment have been made anyways had employment continued?

June payment was timely

January payment in following year was not timely regardless of the reason

Posting on SEC web site made it clear this was a severance payment

Former president was not permitted to make salary deferrals from either payment

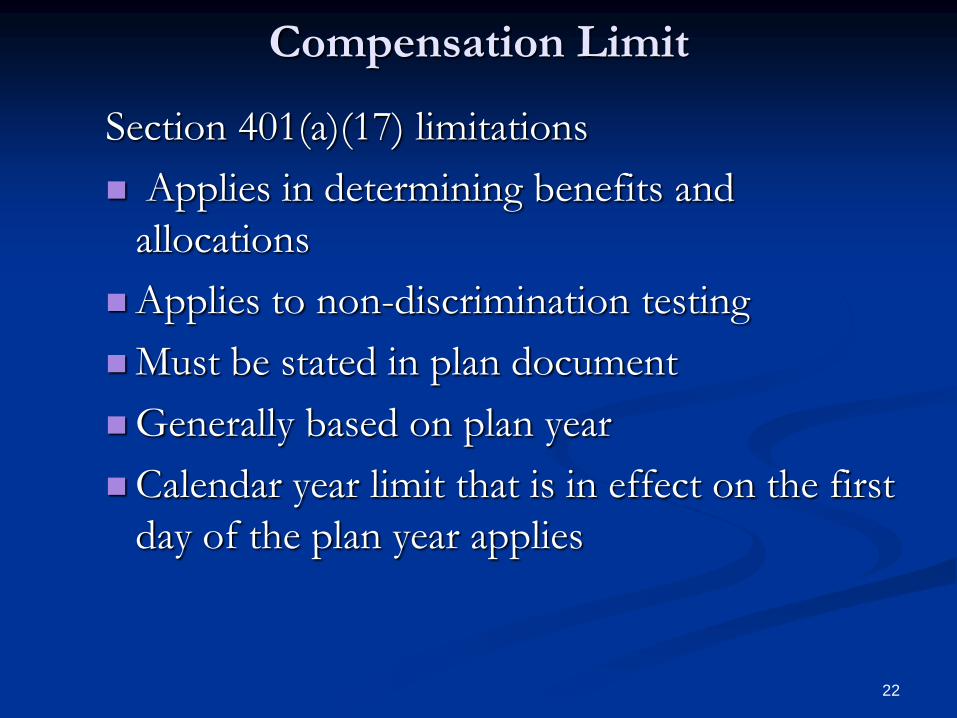

22

Compensation Limit

Section 401(a)(17) limitations

Applies in determining benefits and

allocations

Applies to non-discrimination testing

Must be stated in plan document

Generally based on plan year

Calendar year limit that is in effect on the first

day of the plan year applies

23

Compensation Limit

Section 401(a)(17) limitations

Section 401(a)(17) limits are prorated for

short plan year. Reg §1.401(a)(17)-

1(b)(3)(iii)(A).

Section 401(a)(17) limits are not prorated for

participation for a partial plan year. Reg

§1.401(a)(17)-1(b)(3)(iii)(B).

Applies per employer in a multi-employer

plan

24

Compensation Limit

Section 401(a)(17) limitations

Special EGTRRA Rule

Must be in plan

Allows use of $200K limit for years prior to 2002

(Rev Notice 2001-57 and EGTRRA §611(c))

VCP Correction (Rev Proc 2008-50)

Reduce account balance of violating HCE

Increase account balance of all others

25

Defining Compensation

Effect of Section 414(s)

Applies to

All non-discrimination testing

See special definition under Reg §1.401(a)(4)-12 (plan year compensation)

Gateway minimum allocations/ minimum equivalent allocations

Safe harbor contributions

Compensation for allocations and benefits need not meet a §414(s) definition (Reg §1.414(s)-1(a)(2) also see Reg §1.401(a)(4)-3(e)(1)).

26

Defining Compensation

Effect of Section 414(s)

Start with §415 definition

May exclude salary deferrals under §§401(k), 403(b), 408(p), 125, and 457

May exclude taxable fringe benefits, expense reimbursements, deferred compensation

May exclude pre-participation compensation

Non-discrimination testing

“Safe harbor” allocations under §1.401(a)(4)-2

May exclude other items if the exclusion is a category of compensation and the exclusion passes non-discrimination testing

27

Defining Compensation

Effect of Section 414(s)

May exclude other items from NHCE

compensation if the exclusion is a category of

compensation and the exclusion passes non-

discrimination testing

Bonuses

Overtime

Commissions

Etc.

May exclude any portion of HCE compensation

28

Defining Compensation

Effect of Section 414(s) Special non-discrimination testing

For each participant calculate a ratio

Numerator is the compensation included

Denominator is total compensation using a §414(s) definition- safe harbor

If some HCE’s have some compensation excluded, then the exclusion must be applied for those HCE’s. However, if all HCE’s have some excluded compensation, then the exclusion can be disregarded.

Separate HCE’s and NHCE’s

Average the ratios for each group

29

Defining Compensation

Effect of Section 414(s)

Discrepancy between inclusion rates cannot favor

HCE’s by more than a minimal amount

Other reasonable methods can be used

Suggest applying to IRS for review

30

Defining Compensation

Effect of Section 414(s)

Might be able to use aggregate compensation of

all employees in a group rather than ratio of

individual averages

This method does give greater weight to higher

earners

Minimal discrepancy is based on facts and

circumstances and can take prior results into

account

31

Defining Compensation

Effect of Section 414(s)

Section 401(a)(4)-12 plan year compensation

Refers to §414(s)

Pre-participation compensation

Can be excluded

Lack of year to year consistency cannot be strategic

Where plan year and compensation year do not

coincide, then special rule for new participants

32

Example

Total

Comp

Partcpt

Comp

Equiv

Ben

EBAR

Gross

EBAR

Partcpt

Topaz 150000 150000 800 0.53% 0.53%

Asher 60000 32000 175 0.29% 0.55%

Huey 70000 70000 180 0.26% 0.26%

Roger 40000 22000 118 0.30% 0.54%

Harry 30000 30000 100 0.33% 0.33%

33

Example- Analysis

Cross-Tested profit sharing plan

Using total plan year compensation lone HCE has greater EBAR than all NHCE’s

For new entrants, compensation earned as a participant is applied for testing only

Now 2 NHCE’s have a higher EBAR than the HCE and the plan passes

Plan definition of compensation may use total compensation for determining allocations

34

Defining Compensation

Effect of Section 414(s)

Self-employed participants

Need to adjust income based on inclusion ratio of

NHCE’s if “safe harbor” is not used

Rate of Compensation Rules

Cannot be used for ADP

Testing definition must parallel definition for

allocations

Must use inclusion ratio test under 414(s)

35

Defining Compensation

Effect of Section 414(s)

Pretend Compensation

Imputed compensation

Prior employer compensation

Only applies for DB plans

Must be used to determine benefits and for testing

Subject to non-discrimination testing

Legitimate business purpose

Consistency requirement

Imputed compensation under §415 still counts

36

Defining Compensation

Other Compensation Measurements

These tend to be rigid so as not to allow for variance in application

Deductions under §404

25% of compensation

Use §415(c)(3) definition (§404(a)(12))

This means total compensation including salary deferrals

HCE determination under §414(q)

Use §415(c)(3) definition (§414(q)(4))

This means total compensation including salary deferrals

37

Compensation Impact

Other Compensation Measurements

HCE Determination cont.

Definition used for applying threshold compensation in

prior year and for ranking of compensation in

determining top paid group

Top heavy minimum allocations/ accruals

Use §415(c)(3) definition (§416(i)(1)(D))

This means total compensation including salary deferrals

Must be based on plan year or calendar year ending within

plan year

Same definition must apply for all top heavy purposes,

such as determining officers and $150K

38

Compensation Period

Measuring period for compensation

Section 415- limitation year

Can be plan year

Calendar year

Some other 12 month period

Section 414(s)- testing, gateway, etc.

Plan year or

Calendar year ending within plan year

Other 12 month periods may be allowed

Compensation as a participant

Top heavy minimum- plan year only

39

Compensation Period

Measuring period for compensation

For 401(k)/(m) safe harbors under Reg

§1.401(k)-3(c)(5)(ii):

Allows for periodic matching

Pay period

Payroll periods within a month

Payroll periods within a quarter

Calculate compensation based on those periods

Must be paid by end of following quarter

Reg 1.401(k)-3(c)(5)(ii)

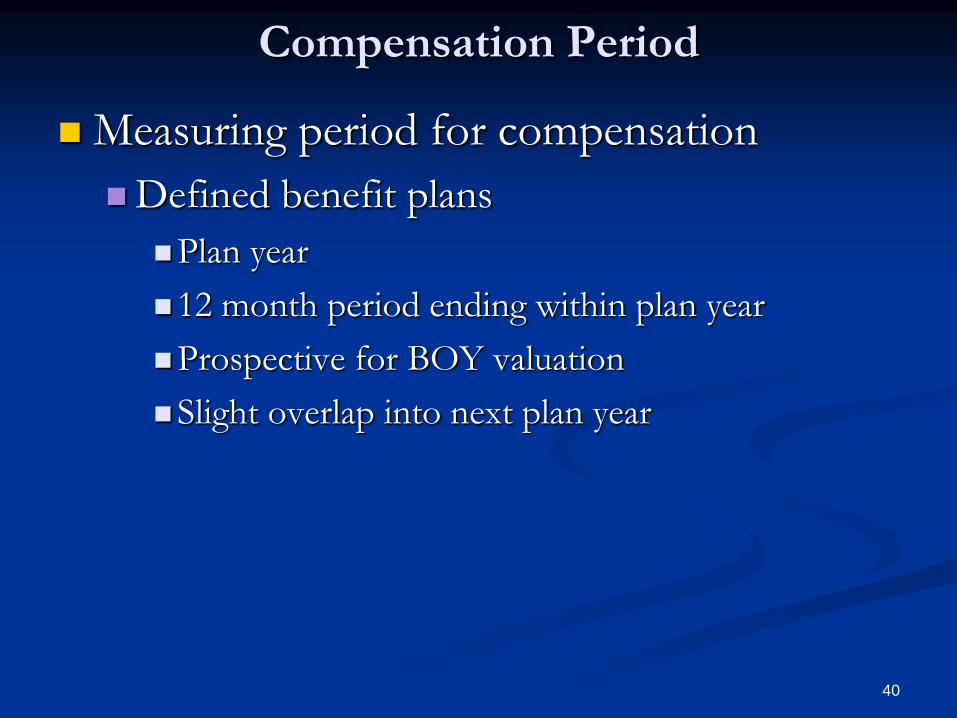

40

Compensation Period

Measuring period for compensation

Defined benefit plans

Plan year

12 month period ending within plan year

Prospective for BOY valuation

Slight overlap into next plan year

41

Compensation Period

Measuring period for compensation

Average compensation

Section 415 for DB plans uses 3 years of service for

100% of avg comp limit (§1.415(b)-1(a)(5))

Service versus participation

Less years are permitted if period of service is less than 3

years

Must be at least one year

Fractional years (at least one) are used

Periods during a severance of employment disregarded

Implied not all breaks in service disregarded

Section 416 uses 5 year avg (416(c))(1)(D))

42

Compensation Period

Measuring period for compensation

Average compensation

General testing/ cross-testing

Benefits under safe harbor DB formula

See Reg §1.401(a)(4)-3(e)(2)

At least 3 high consecutive years

Any start date

Continuous

End in current year

Various adjustments

Plan year compensation OK for testing if accruals determined over current year

43

Audits

An error discovered on audit that the definition

of compensation in the plan was not followed

could result in

Additional employer contributions

A reallocation of contributions

Earnings adjustment if the error is discovered in a

later year

Plan disqualification

44

Audits

Accountant procedures require that the

compensation definition be reviewed and

compared to the actual contributions

They are likely to question any match that is not

consistent with the formula, or anything not

involving whole numbers

45

Audits

Employers have an obligation to maintain or have access to

records to demonstrate

An error has not occurred

The person changed contribution percentages during the

year

The person entered or left mid year

The person switched to or from a non-eligible status

46

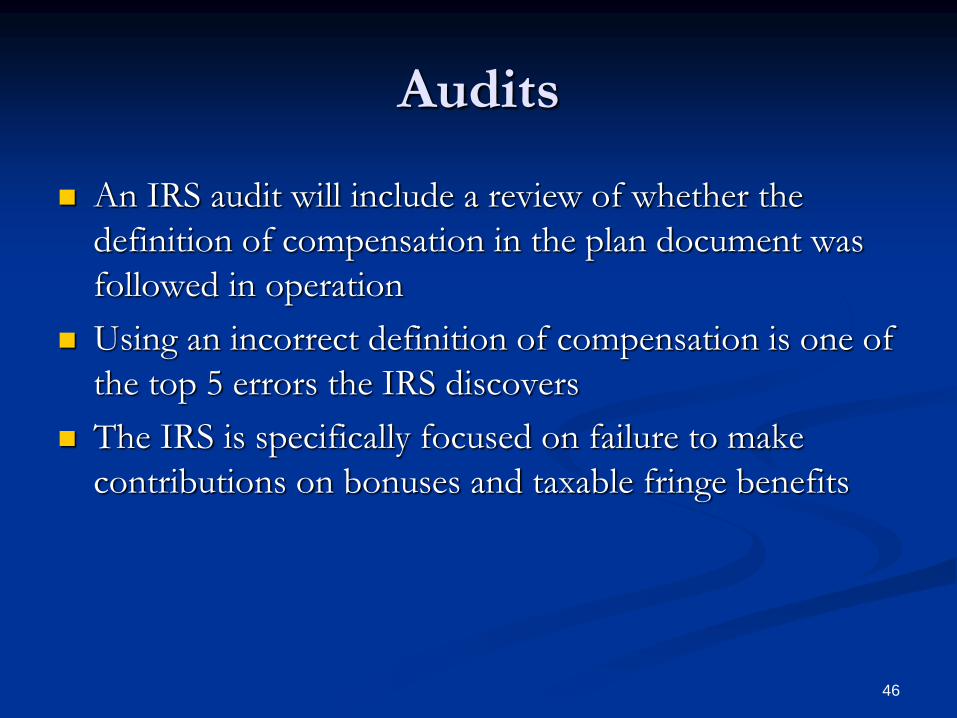

Audits

An IRS audit will include a review of whether the

definition of compensation in the plan document was

followed in operation

Using an incorrect definition of compensation is one of

the top 5 errors the IRS discovers

The IRS is specifically focused on failure to make

contributions on bonuses and taxable fringe benefits

47

Correction

Rev. Proc 2008-50 provides some guidance on

correcting an error in compensation

Acceptable correction methods

Additional employer contributions on any missed

compensation

Reallocation of contributions using the correct

definition

48

Planning Pointers

Practical Considerations- Plan Drafting

Compensation definition in plan

Applies to determination of allocations and benefit accruals

Applies to testing where plan defines a testing procedure

ADP testing

Can use a separate definition of compensation for ADP testing

Conversely, plan can use any 414(s) definition for non-discrimination testing that is not described in the plan

Generally year to year consistency not required

49

Planning Pointers

Practical Considerations- Plan Drafting

Compensation definition in plan

Best practice is not to define compensation for testing

Definition for allocation/accrual can be different than that used for testing

In general the definition for allocation or accrual need not be a 414(s) definition Reg §1.414(s)-1(a)(2)

§414(s) definition applies for ADP/ACP safe harbor contributions Reg § 1.401(k)-3(b)(2) and allocations intended to meet safe harbor formulas under Reg §1.401(a)(4)-12 (plan year compensation definition)

50

Planning Pointers

Practical Considerations- Plan Drafting

Compensation definition in plan

Ease of administration

Consider excluding taxable fringe benefits such as

taxable portion of health insurance and auto

allowance

If definition includes §125 deferrals, make sure

these are obtained

51

Planning Pointers

Practical Considerations- Plan Drafting

Compensation definition in plan

Avoid linking compensation definition to mechanics

of salary deferral elections

Avoid use of the term “compensation” in election

form

OK to refer to limits on deferrals as a % of

compensation in the plan document

The withholding process should be considered

administrative. Plan can acknowledge this.

52

Planning Pointers

Practical Considerations- Strategies

Plan amends definition of compensation to

exclude overtime pay

Only NHCE’s have overtime pay

Therefore, this definition will not pass the 414(s)

discrepancy test

Use total compensation under 414(s) to perform

testing

53

Planning Pointers

Practical Considerations- Strategies

Plan amends definition of compensation to

exclude overtime pay

Only NHCE’s have overtime pay

Therefore, this definition will not pass the 414(s)

discrepancy test

Use total compensation under 414(s) to perform

testing

54

Example

Base

Comp

Over-time ER

Alloc

Acc

Rate

Olio 200000 0 32500 6%

Lynn 75000 2000 6000 3%

Tracey 50000 0 3000 7%

Suzy 25000 3000 1500 8%

55

Example- Analysis

Use base compensation for determining

allocations

Use total compensation for testing

Specifically authorized under 414(s)

Keep in mind

Top heavy minimum allocation based on total

compensation for full year- 3% of comp

Gateway minimum can be based on compensation

earned as a participant and could exclude salary

deferrals- 5% of comp

56

Planning Pointers

Practical Considerations- Strategies

Exclude salary deferrals such as made under

401(k) and 125 plans

If HCE’s have compensation above 401(a)(17)

limit, then testing compensation for HCE’s may

remain at 401(a)(17) limit

Compensation for NHCE’s will reduce

Therefore allocation/ accrual rates for NHCE’s

will increase relative to those of HCE’s

57

Example

Status Total

Comp

Def $ Net

Comp

Gross

Def %

Net

Def %

Abe HCE 300K 16500 245K 6.73% 6.73%

Izzy NHCE 50K 2600 47400 5.20% 5.49%

Jake NHCE 40K 1600 38400 4.0% 4.17%

58

Example- Analysis Using gross compensation NHCE ADP is 4.6%

which is lower than the required 4.73% and a correction is needed

Using net compensation NHCE ADP is 4.83% and no correction is needed

Note 401(a)(17) caps compensation for HCE at $245,000 in both cases

Had the HCE have net compensation less than $245K, the result may have been worse

59

Planning Pointers

Practical Considerations- Strategies

Exclude categories of compensation for certain

non-owner HCE’s

For example, exclude commissions earned by

HCE’s in determining allocations

This will reduce allocation costs for those affected

Testing (if necessary) can be based on total

compensation, or adjusted compensation

60

Example

Base

Comp

Comm Total

Comp

Def SH

Match

Net

SH

Match

Gross

Dan 245K 0 245K 16500 9800 9800

Jon 245K 0 245K 16500 9800 9800

Ashley 50K 100K 150K 10000 2000 6000

Topley 100K 50K 150K 8000 4000 6000

61

Example- Analysis 414(s) allows exclusion of a category of income

Commissions are a category of income

If NHCE’s affected must test

Only HCE’s are affected- specifically authorized

Reduce match cost for non-owner HCE’s from

12K to 6K, a savings of 6K

62

Planning Pointers

Practical Considerations- Strategies

Use compensation for a subset of the year to

calculate and pay safe harbor matching

contributions

Does 415 limit apply to each pay period?

See Reg §1.401(a)(17)-1(b)(3)(iii)(A)

This technique avoids cost of paying and

calculating a “true-up” after year end

63

Example Plan has a safe harbor match

It is calculated and paid based on pay periods falling within the month

Participant receives compensation of $4,000 per month

Participant withholds $120 per month for 401(k)

Participant receives bonus of $2,000 in July and $5,000 in December

Participant withholds an additional $1,000 from each bonus

64

Example- Analysis

Total compensation for the year is $55,000

Total 401(k) deferrals for the year are $3,440

If full year compensation is used, then the match would

be 4% of compensation- $2,200

If match is calculated based on monthly compensation,

then

June compensation is $6,000 and deferrals are $1,120. Match

is $240

December compensation is $9,000 and deferrals are $1,120.

Match is $360

65

Example- Analysis

Compensation other 10 months is $4,000 per month

and deferrals are $120. Match is $120 each month

for a total of $1,200 for the year

Total match for the year is $1,800

Compare to $2,200 using the full year

Compensation must be measured each month (See

Reg §1.401(a)(17)-3(b)(iii))

Does this include taxable fringe benefits? Auto allowance?

Etc.

Are annual items of income pro-rated?

66

Cross Testing is Fun!

67

You Know You’re in Trouble

When… 10. DOL 408(b)(2) regulations authorize civil

penalties for Indecent Disclosure

9. The US military adopts the DOL’s electronic

5500 signing process as an acceptable method

of interrogation

8. ASPPA lobbies Congress to pass the Annual

Stimulus for Pension Professional Act (ASPPA),

requiring costly plan amendments each year

68

69

You Know You’re in Trouble

When… 7. You think a PTIN is something you find in an

outhouse

6. Caving in to client pressure, you held a 5500 signing party with open bar, this past Friday night

5. It figures that a Congressman from Texas would spend so much time thinking about cross-testing

4. You hire an ERPA to lead you on your next Himalayan expedition

70

You Know You’re in Trouble

When… 3. You think an AFTAP is something a

professional athlete does to a reporter, then gets in trouble

2. Rather than resort to the same old “double letter” protocol, the IRS devises a whole new alphabet for the sub-section following 414(z)

1. You’ve blown up more safe harbors this year than the Navy SEALS

71