Page 1

H E A L T H W E A L T H C A R E E R

C O M P E N S A T I O NP L A N N I N G F O R 2 0 1 6E M E A F O R E C A S T SA N D T R E N D S

OCTOBER 28 2015

Alyson Callin, UKNuno-Filipe dos Santos Gomes, UAENicol Mullins, South AfricaDavid Wreford, UK

Page 2

© MERCER 2015 1

T O D AY ’ S S P E A K E R S

ALYSON CALLINLondon, UK

NUNO GOMESDubai, UAE

NICOL MULLINSSouth Africa

DAVID WREFORDLondon, UK

Page 3

© MERCER 2015 2

Context forPlanning

MercerSurveyInsights

Trends for2016 andBeyond

Call toAction

A G E N D A F O R O U R S E S S I O N T O D AY

Page 4

© MERCER 2015 3© MERCER 2015 3

CONTEXT FORPLANNING

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

Page 5

© MERCER 2015 4

E U R O P EE C O N O M I C C O N T E X T 2 0 1 5

-5%

0%

5%

10%

15%

20%

25%

30%

35%U

nite

dSt

ates

Bra

zil

Chi

na

Indi

a

Irela

nd

Switz

erla

nd

Gre

ece

Spai

n

Den

mar

k

Fran

ce

Italy

Ger

man

y

UK

Lith

uani

a

Slov

enia

Hun

gary

Pola

nd

Rom

ania

Serb

ia

Turk

ey

Rus

sia

Ukr

aine

Kaz

akhs

tan

Salary increases Inflation GDP Unemployment

Source: Global Compensation Planning Report, July 2015

Page 6

© MERCER 2015 5

E U R O P EE C O N O M I C A N D M A R K E T C O N T E X T

5

1. Stabilised economies and low inflation2. Sustained war for the best talent3. Diversity and inclusion agenda driving need for:

• Fairer rewards• Flexible rewards

4. Post-recession emphasis on maintaining good governance• From cost control to targeted investments• Distributed responsibility and function effectiveness

5. Increased transparency• Better educated managers• More informed employees

Page 7

© MERCER 2015 6

M I D D L E E A S TE C O N O M I C A N D M A R K E T C O N T E X T

Page 8

© MERCER 2015 7

A F R I C AE C O N O M I C A N D M A R K E T C O N T E X T

• 55 recognised African States

• Tough economic conditions– Legislation changes

• Tougher infrastructure challenges– Lack of dependable infrastructure

• Developed markets turning to emerging markets

• Africa is one of the earmarked growth regions globally

Page 9

© MERCER 2015 8© MERCER 2015 8

MERCER SURVEYINSIGHTS

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

Page 10

© MERCER 2015 9

4,823 PARTICIPANTS

S A L A R Y M O V E M E N T S N A P S H O T S U R V E YP A R T I C I P A N T P R O F I L E – S E P T E M B E R 2 0 1 5

79MARKETS

Source: Mercer EMEA SMS September 2015

376 UNIQUEORGANISATIONS

Page 11

© MERCER 2015 10

S A L A R Y M O V E M E N T S N A P S H O TP A R T I C I P A N T P R O F I L E

16%

4%

13%

7%

10%

12% 5%7%

14%

ENERGYHIGH TECHCONSUMER GOODS LIFE SCIENCESOTHER DURABLEGOODS MANUFG

SERVICES FINANCIAL SERVICES

11%

RETAIL & WHOLESALEOTHEROTHER NON-DURABLEMANUFACTURING

Page 12

© MERCER 2015 11

To what extent do your employees understand the basis upon whichtheir pay and incentives are determined?

L I V E P O L LQ U E S T I O N 1

A – Not at all

B – To a slight extent

C – To a moderate extent

D – To a great extent

E – To a very great extent

0% 20% 40% 60%

To a very great extent

To a great extent

To a moderate extent

To a slight extent

Not at all

Results

Based on 183 responses

Page 13

© MERCER 2015 12© MERCER 2015 12

MERCER SURVEYINSIGHTSAFRICA

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

Page 14

© MERCER 2015 13

S A L A R Y I N C R E A S E F O R E C A S T S F O R 2 0 1 6A F R I C A – A L L R E S P O N S E S

Source: Mercer EMEA SMS September 2015 (Median)

Country Increase Country IncreaseMalawi 14.0% Algeria 6.9%Ghana 12.0% Uganda 6.9%Egypt 10.0% Tunisia 6.3%Ethiopia 9.9% Mauritius 5.5%Nigeria 9.9% Mozambique 5.5%Kenya 8.0% DRC 4.8%Zambia 7.7% Morocco 4.5%Tanzania 7.1% Ivory Coast 4.1%Angola 7.0% Senegal 4.0%South Africa 7.0% Gabon 3.1%

Page 15

© MERCER 2015 14© MERCER 2015 14

TRENDS FOR 2016 ANDBEYONDAFRICA

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

Page 16

© MERCER 2015 15

2 0 1 5 E C O N O M I C F R E E D O M H E A T M A PW O R L D AV E R A G E 6 0 . 4

Source: The Heritage Foundation, 2015 Economic Freedom Heat Map, http://www.heritage.org/index/heatmap

Page 17

© MERCER 2015 16

• AFRICA is VUCA– Volatile– Uncertain– Complex– Ambiguous

• 3 Main Regions in Africa– Anglophone– Francophone– Lusophone

• Currency Volatility & Depreciation– Angola– Ghana– Nigeria– South Africa

T R E N D S F O R 2 0 1 6 A N D B E Y O N DA F R I C A

Page 18

© MERCER 2015 17

T R E N D S F O R 2 0 1 6 A N D B E Y O N DA F R I C A

- 2 5 %

0 %

2 5 %

5 0 %

7 5 %

1 2 5 %

J A N 1 , 2 0 1 4 J U L 1 , 2 0 1 4 J U L 1 , 2 0 1 5J A N 1 , 2 0 1 5

1 0 0 %

U S $ /Z A R3 9 . 5 2 %

U S $ /RUB1 0 3 . 8 2 %

U S $ /A O A3 8 , 6 4 %

U S $ /N G N2 4 . 2 2 %

AV E R A G E B I D R AT E F O R T H E W E E K O F M O ND AY, S E P 2 8 , 2 0 1 5 TO SUNDAY,O C T 4 , 2 0 1 5 @ +/ - 0 %

U S $ /GHS7 2 . 8 5 %

Page 19

© MERCER 2015 18

• Sustained high inflation– IMF latest projections as October

- slow down in CPI- small growth in GDP

• Sustained high market increases– Real wage increases

• Sustained high levels of compensation

• Focus is on cash and benefits– Base salary not relevant benchmark

• Skill scarcity– High demand low supply– Most companies buy skills – very few build

• Opportunities bountiful – but for the brave …

T R E N D S F O R 2 0 1 6 A N D B E Y O N DA F R I C A

Page 20

© MERCER 2015 19

To what extent do you proactively adapt your compensation policiesto address your talent issues?

L I V E P O L LQ U E S T I O N 2

A – Not at all

B – To a slight extent

C – To a moderate extent

D – To a great extent

E – To a very great extent

Results

Based on 160 responses

0% 10% 20% 30% 40% 50%

To a very great extent

To a great extent

To a moderate extent

To a slight extent

Not at all

Page 21

© MERCER 2015 20© MERCER 2015 20

MERCER SURVEYINSIGHTS

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

MIDDLE EAST

Page 22

© MERCER 2015 21

S A L A R Y I N C R E A S E F O R E C A S T S F O R 2 0 1 6M I D D L E E A S T / A S I A – A L L R E S P O N S E S

Source: Mercer EMEA SMS September 2015 (Median)

Country Increase Country IncreaseIran 20.0% Iraq 5.5%Pakistan 11.6% Bahrain 5.0%Yemen 9.0% Kuwait 5.0%Uzbekistan 9.0% Oman 5.0%Kazakhstan 8.6% Qatar 5.0%Azerbaijan 8.0% Saudi Arabia 5.0%Syria 8.0% UAE 5.0%Lebanon 5.9% Israel 3.1%Jordan 5.7%

Page 23

© MERCER 2015 22© MERCER 2015 22

TRENDS FOR 2016 ANDBEYONDMIDDLE EAST

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

Page 24

© MERCER 2015 23

T R E N D S F O R 2 0 1 6 A N D B E Y O N DM I D D L E E A S T

SIMPLIFICATION OF COMPENSATION

FOCUS ON BENEFITS – STRONGER RETENTION

MANAGING WORKFORCE AND MARKET DIVERSITY

Page 25

© MERCER 2015 24

T R E N D S F O R 2 0 1 6 A N D B E Y O N DM I D D L E E A S T

IS THE CONCEPT OF TOTAL REWARDS FINALLY RESONATING IN THE MIDDLE EAST?

COMPENSATIONDirect monetary rewards provided in exchangefor employee time and performance.• Base Pay• Allowances• Short Term Incentive Plans• Long Term Incentive Plans

CAREERSRewards offered to improve employees’ skillsand advance their careers.• Performance Management• Promotion & Lateral Moves• Formal and Informal Training• Tuition Reimbursement

WORK-LIFERewards offered to enhance an employee’severyday work experience and contribute toquality of life.• Job Design and Flexibility• Recognition• Health & Well-Being• Dependent Care

BENEFITSRewards offered to protect the health and long-term financial security of the employee.• Health and Welfare• Paid Time Off• Retirement Plans• Perquisites and Other Benefits

Page 26

© MERCER 2015 25

PREVALENCE OF ALLOWANCES – UAE

T R E N D S F O R 2 0 1 6 A N D B E Y O N DM I D D L E E A S T

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Transportation Allowance

Housing Allowance

Meal Allowance

Shift Allowance

Furniture Allowance

Utilities Allowance

National Allowance

Other Guaranteed Allowance

Consolidated Allowance

2014 2015

19%

Source: Mercer 2015 UAE Total Remuneration Survey

Page 27

© MERCER 2015 26

To what extent do your pay and bonus programmes differentiate theemployee attributes you feel are important to drive business performance?

L I V E P O L LQ U E S T I O N 3

A – Not at all

B – To a slight extent

C – To a moderate extent

D – To a great extent

E – To a very great extent

Results

Based on 127 responses

0% 10% 20% 30% 40%

To a very great extent

To a great extent

To a moderate extent

To a slight extent

Not at all

Page 28

© MERCER 2015 27© MERCER 2015 27

MERCER SURVEYINSIGHTSEUROPE

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

Page 29

© MERCER 2015 28

S A L A R Y I N C R E A S E F O R E C A S T S F O R 2 0 1 6W E S T E R N E U R O P E – A L L R E S P O N S E S

Source: Mercer EMEA SMS September 2015 (Median)

Country Increase Country IncreaseGermany 3.0% France 2.3%Norway 3.0% Finland 2.2%UK 2.9% Ireland 2.2%Austria 2.7% Belgium 2.0%Denmark 2.5% Portugal 2.0%Italy 2.5% Spain 2.0%Luxembourg 2.5% Switzerland 2.0%Netherlands 2.5% Greece 1.7%Sweden 2.5%

Page 30

© MERCER 2015 29

S A L A R Y I N C R E A S E F O R E C A S T S F O R 2 0 1 6C E N T R A L / E A S T E R N E U R O P E – A L L R E S P O N S E S

Source: Mercer EMEA SMS September 2015

Country Increase Country IncreaseBelarus 12.0% Bosnia and Herzegovina 3.0%Ukraine 10.0% Estonia 3.0%Russia 8.0% Latvia 3.0%Turkey 7.8% Lithuania 3.0%Moldova 7.0% Montenegro 3.0%Georgia 6.9% Slovakia 3.0%Armenia 5.9% Albania 2.9%Serbia 5.4% Macedonia 2.9%Romania 4.5% Croatia 2.8%Bulgaria 4.0% Czech Republic 2.8%Hungary 3.5% Slovenia 2.8%Poland 3.1% Cyprus 1.5%

Page 31

© MERCER 2015 30© MERCER 2015 30

TRENDS FOR 2016 ANDBEYONDEUROPE

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

Page 32

© MERCER 2015 31

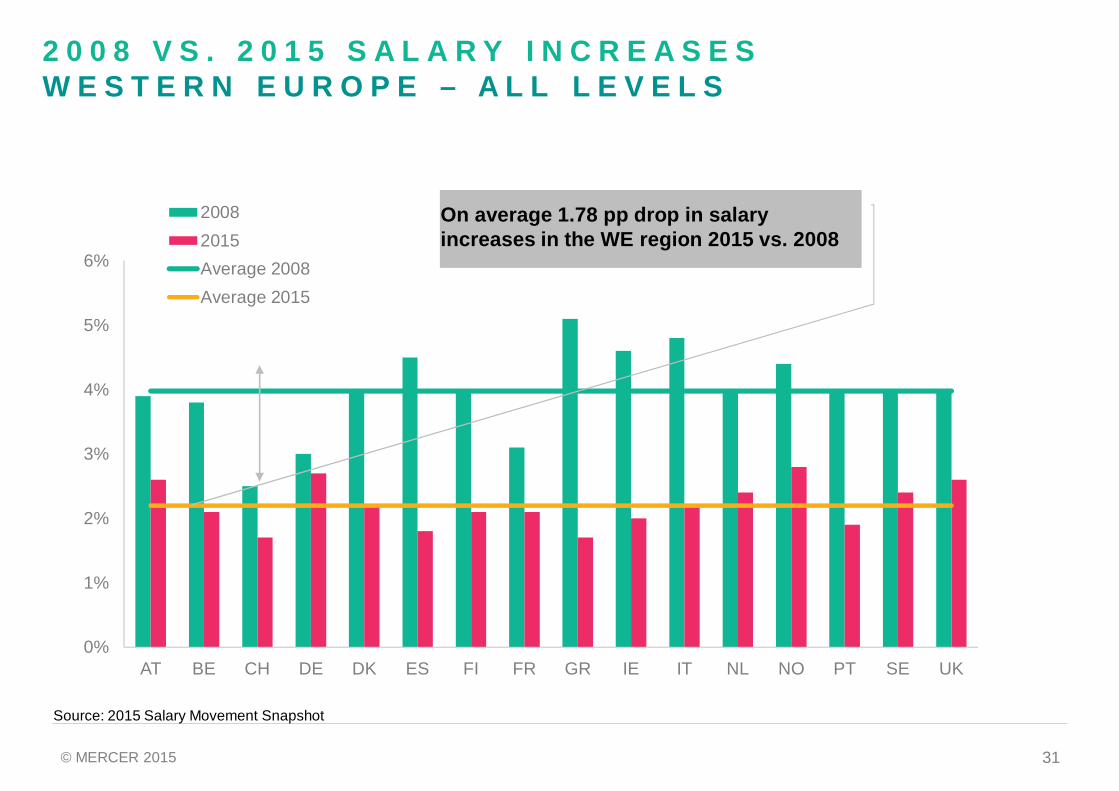

0%

1%

2%

3%

4%

5%

6%

AT BE CH DE DK ES FI FR GR IE IT NL NO PT SE UK

20082015Average 2008Average 2015

On average 1.78 pp drop in salaryincreases in the WE region 2015 vs. 2008

2 0 0 8 V S . 2 0 1 5 S A L A R Y I N C R E A S E SW E S T E R N E U R O P E – A L L L E V E L S

Source: 2015 Salary Movement Snapshot

Page 33

© MERCER 2015 32

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

BG CZ EE HR HU KZ LT LV PL RO RU RS SK SI TR UA

2008 2015 Average 2015 Average 2008

2 0 0 8 V S . 2 0 1 5 S A L A R Y I N C R E A S E SC & E E U R O P E – A L L L E V E L S

On average 5.84 pp drop in salaryincreases in the CEE region 2015 vs 2008

Source: 2015 Salary Movement Snapshot

Page 34

© MERCER 2015 33

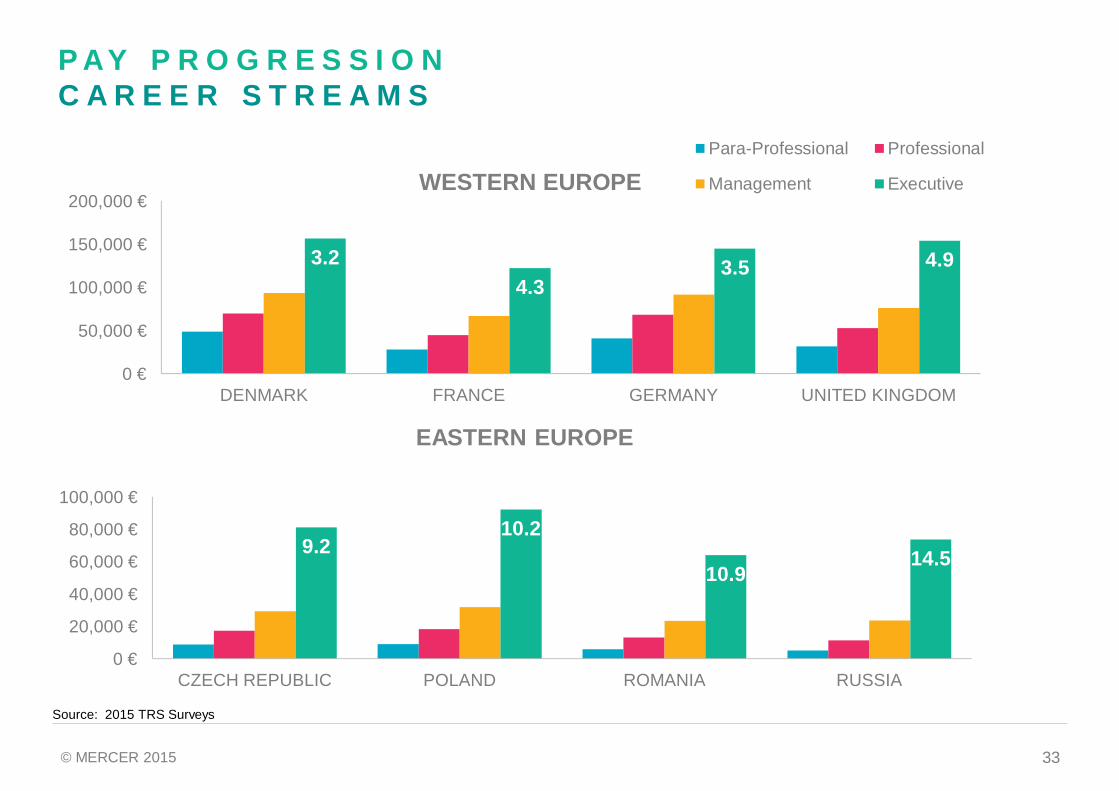

P AY P R O G R E S S I O NC A R E E R S T R E A M S

3.24.3

3.5 4.9

0 €

50,000 €

100,000 €

150,000 €

200,000 €

DENMARK FRANCE GERMANY UNITED KINGDOM

Para-Professional Professional

Management ExecutiveWESTERN EUROPE

9.210.2

10.914.5

0 €

20,000 €

40,000 €

60,000 €

80,000 €

100,000 €

CZECH REPUBLIC POLAND ROMANIA RUSSIA

EASTERN EUROPE

Source: 2015 TRS Surveys

Page 35

© MERCER 2015 34

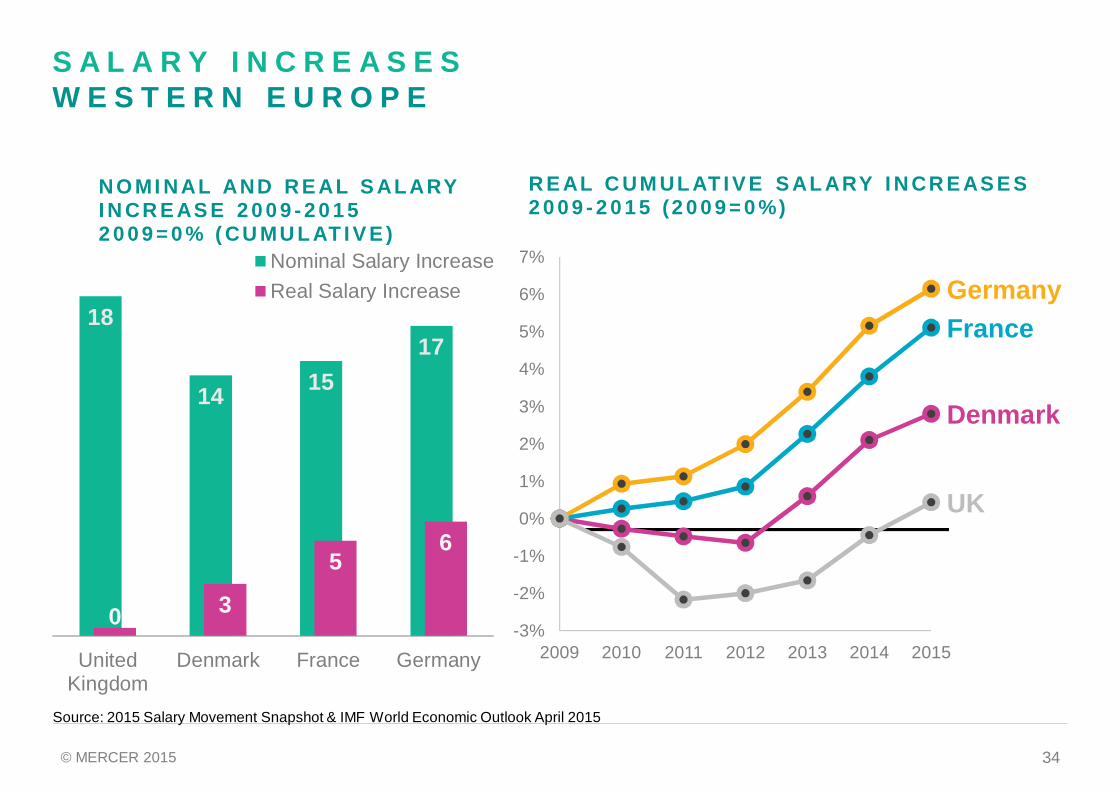

18

14 1517

0 3

56

UnitedKingdom

Denmark France Germany

NO MI NAL AND RE AL S ALARYI N CR E AS E 2 0 0 9 - 2 0 1 52 0 0 9 = 0 % ( CU MU L AT I V E )

Nominal Salary IncreaseReal Salary Increase

S A L A R Y I N C R E A S E SW E S T E R N E U R O P E

Denmark

FranceGermany

UK

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

2009 2010 2011 2012 2013 2014 2015

R E AL C UM UL AT I V E S AL ARY I N CR E AS E S2 0 0 9 - 2 0 1 5 (2 0 0 9 = 0 %)

Source: 2015 Salary Movement Snapshot & IMF World Economic Outlook April 2015

Page 36

© MERCER 2015 35

32

19

61

24

5 7 7 10

Romania CzechRepublic

Russia Poland

NO MI NAL AND RE AL S ALARYI N CR E AS E 2 0 0 9 - 2 0 1 52 0 0 9 = 0 % ( CU MU L AT I V E )

Nominal SalaryIncreaseReal SalaryIncrease

S A L A R Y I N C R E A S E SE A S T E R N E U R O P E

CzechRepublic

Poland

Romania

Russia

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2009 2010 2011 2012 2013 2014 2015

R E AL C UM UL AT I V E S AL ARY I N CR E AS E S2 0 0 9 - 2 0 1 5 (2 0 0 9 = 0 %)

Source: 2015 Salary Movement Snapshot & IMF World Economic Outlook April 2015

Page 37

© MERCER 2015 36

2 0 1 5 A C T U A L S A L A R Y I N C R E A S E SP E R F O R M A N C E M A T R I X

0%1%2%3%4%5%

Denmark France Germany UK

Average actualsalary increase 2015

Top Performers

Standard Performers

Low Performers

Market Average

Source:September 2015 Salary Movement Snapshot

25%

65%

10%

0%1%2%3%4%5%

Denmark France Germany UK

Average forecastsalary increase 2016

Top Performers

Standard Performers

Low Performers

Market Average

25%

65%

10%

4.1%

3.7% 3.6%4.1%

3.5% 3.2%4.0%

4.3%

Page 38

© MERCER 2015 37

2 0 1 5 A C T U A L S A L A R Y I N C R E A S E SP E R F O R M A N C E M A T R I X

0%2%4%6%8%

10%

Czech Republic Poland Romania Russia

Average actualsalary increase 2015

Top Performers

Standard Performers

Low Performers

Market Average

Source: September 2015 Salary Movement Snapshot

25%

65%

10%

0%2%4%6%8%

10%

Czech Republic Poland Romania Russia

Average forecastsalary increase 2016

Top Performers

Standard Performers

Low Performers

Market Average

25%

65%

10%

10.5%

4.7%5.5%

8.3%

4.4%5.6%

6.8%

11.6%

Page 39

© MERCER 2015 38

To what extent are your employees consistently paid for the workthey do?

L I V E P O L LQ U E S T I O N 4

A – Not at all

B – To a slight extent

C – To a moderate extent

D – To a great extent

E – To a very great extent

Results

Based on 136 responses

0% 10% 20% 30% 40% 50%

To a very great extent

To a great extent

To a moderate extent

To a slight extent

Not at all

Page 40

© MERCER 2015 39© MERCER 2015 39

CALL TO ACTION

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

Page 41

© MERCER 2015 40

I N D U S T R Y D A T A2 0 1 6 F O R E C A S T S

AFRICARetail/Wholesale

Consumer Goods

Life Sciences

High TechServicesEnergy

Mining & MetalsFinancial Services

TransportationEquipment

Ins/reinsurance

MIDDLE EASTLife Sciences

Consumer Goods

High Tech

TransportationEquipmentServices

Retail/WholesaleEnergy

Ins/reinsuranceMining & Metals

Financial Services

W EUROPERetail/Wholesale

High TechIns/reinsuranceLife SciencesTransportation

EquipmentMining & Metals

Consumer Goods

Services

FinancialServices

Energy

E EUROPEConsumer Goods

Life Sciences

Retail/Wholesale

TransportationEquipmentHigh TechServicesEnergy

Mining & MetalsIns/Reinsurance

Financial Services

ALL INDUSTRY

ABO

VEBE

LOW

Source: Mercer EMEA SMS September 2015 40

Page 42

© MERCER 2015 41

P A S T – P R E S E N T – F U T U R E S T A T E

41

One size fitsall

Segmentation&

differentiationPersonalisation

CompetitivePay Fair pay Responsible

pay

Fixedemployment

costs

Flexibleemployment

costs

Multiple fullyflexible

PA S T P R E S E N T F U T U R E

Page 43

© MERCER 2015 42

C A L L T O A C T I O NW H E R E T O F O C U S F O R 2 0 1 6

ü Clear alignment between organisational and workforce plans, EVP and rewardprogrammes (incl. analytics)

ü Integrated reward and talent programmes that support each other

ü Grading structures that clearly define career levels and expectations

ü Clear definition of drivers that define factors that determine and progress reward

ü Thoughtful segmentation and differentiation

ü Transfer of benefit risk, choice and cost to employees

ü Tighter governance of reward resulting in:§ Clear definition of function design and priorities§ greater cost control and can limit overspending and result in less

attraction/retention risk

ü Well managed and transparent reward structures, and managers who areconsistent advocates of rewards result in better employee perception ofinternal equity

ü Better understanding of rewards resulting in increased employee satisfactionand commitment to their employers

Page 44

© MERCER 2015 43© MERCER 2015 43

QUESTIONS

C O M P E N S A T I O N P L A N N I N G F O R 2 0 1 6

Page 45

© MERCER 2015 44

Q U E S T I O N S

QUESTIONSPlease type your questions in the Q&A section of the toolbarand we will do our best to answer as many questions as wehave time for.

To submit a question while in full screen mode, use the Q&Abutton, on the floating panel, on the top of your screen.

CLICK HERE TO ASK A QUESTIONTO “ALL PANELISTS”

FEEDBACKPlease take the time to fill out thefeedback form at the end of this webcastso we can continue to improve. Thefeedback form will pop-up in a newwindow when the session ends.

www.mercer.com/webcastsView past recordings and sign up forupcoming webcasts

ALYSON CALLIN NUNO GOMES DAVID WREFORDNICOL MULLINS

Page 46

© MERCER 2015 45

S A L A R Y M O V E M E N T S N A P S H O T ( S M S ) S U R V E Y

45

SALARY MOVEMENT SNAPSHOTRegister for our quarterly snapshot surveyproviding complimentary salary movementdata: www.imercer.com/sms

– Over 500 participating organizations– Available in 80+ EMEA markets– Updated quarterly– FREE for participants!

R E G I S T E R N O W !The next edition launches on 2 November