100

Our way ahead Competence Competitiveness Continuity 2010 Annual Report

Our way aheadCompetence Competitiveness Continuity

2010 Annual Report

Our way aheadCompetence Competitiveness Continuity

2010 Annual Report

2

Contents

» 40 years of working together towards new goals 4

» Financial data 6 » Comer Industries at a glance 8 » 2010 highlights 10

1 Competence 12 » People: at the heart of change 14 » New development drivers from the green economy 16 » Cutting-edge engineering and technological solutions 17 » The future-oriented program of R&D 18

2 Competitiveness 20 » Comer Production System: the road to excellence 22 » The renewal of the ICT infrastructures 26 » The new industrial plan 28 » Growth, cornerstone of competitiveness 30 » Business development in China 31 » BRIC, emerging markets for growth 32

3 Continuity 34 » A solid financial base for development 36 » Committed to sustainability and safety 37 » Outlook for 2011 38

» Our first 40 years 40

» Extract from the report on operations accompanying the consolidated financial statements at December 31, 2010 42 » Extract from the consolidated financial statements

at December 31, 2010 52 » Auditors’ report 92 » Board of statutory auditors’ report 93

» Board of directors and management 94 » Contacts 95

3

Forty years of constant growth and inno-vation, financial stability and investments in the service of our customers. Forty years of competition and challenges overcome in all markets of the world. But, in particular, forty years whose value is based on the participation and enthu-siasm of the men and women who have built the history of Comer Industries.We began as four in 1970. Along with myself, there were my brothers Fabrizio and Oscar as well as my cousin Aimone; we were all driven by the core values of our business model: honesty, respect for one’s peers, perseverance and group spirit.These same values – which were also shared and nurtured by all of our staff over the past decades – represent the solid roots which have allowed us to realize the dream of a great industrial ven-ture and create, within Comer Industries, an expansive, cohesive and united com-munity that is enriched each day by the talent and skills of more than 1,200 peo-ple from Italy to China and from Europe to the United States.

Leaders in change: competent andmotivated individualsThe people in our company are, in fact, the creators of the new philosophy based on the principles of lean organization, continuous improvement, sustainability and widespread innovation, which has become part of our new corporate cul-ture.Thanks to this transformation, we have been more effective in tackling even the recent difficult global economic situation.The solid foundation of technical and managerial knowledge, as well as the interpersonal and human relations skills of our employees, has allowed us to

manage and effectively implement this change with a level of flexibility and re-sponsiveness that is greater than aver-age. In this manner, we have successfully adapted to new market needs as well as to critical factors within the world eco-nomic system.

2010: finally a recoveryStarting with ourselves, and our great corporate family, is truly the best way to celebrate our first forty years as a com-pany. A splendid achievement which, in 2010, we have hailed with the spirit of renewed optimism for our accomplish-ments and for our future prospects.As the year closed, our company had

grown 15%, with total revenues of 277 million euros. This occurred within an en-vironment of generalized recovery for our market sectors of reference.Within the industrial field, we reported im-proved levels of performance, particularly in the segments for compact construc-tion and road machinery. With regards to renewable energy, revenues from our ap-plications for wind generators increased further – this is particularly due to the excellent performance of the Chinese market.More comforting signs of recovery were also noted in the sector for agricultural applications; this was driven by wide-spread growth in demand following the

general increase in prices of agricultural commodities which occurred – even as a result of incidental factors – in the second half of 2010.

Stronger and more competitiveBesides growth in volumes, profitability index is also positive, and our consoli-dated financial position exhibits a signifi-cant indebtedness reduction: this is an extra advantage for us in the arena of international competition.In addition, we established the basis of the reorganization schedule for our manufacturing structures, planning a se-ries of investments which, starting from 2011, will involve all our production sites.

The main objective is to respond more effectively to the increasingly challenging demands of our global customers, with a strong sense of constructive partnership.

An efficient and sustainabledevelopment modelThe general picture provided by these factors leads us to believe that the worst, associated with the internation-al crisis, is now over, and that we can look to the future with more optimism. Uncertainty factors threatening the persistence of the recovery still remain – such as Chinese decisions regard-ing monetary policy, the rising costs of raw materials, the consequential infla-

40 years of working together towards new goals

The solid foundation of technical and managerial knowledge, as well as the interpersonal and human relations skills of our employees, has allowed us to manage and effectivelyimplement this change with a level of flexibility and responsiveness that is greater than average. In this manner,we have successfully adapted to new market needs as well as to critical factors within the global economic system.

4

tionary trends and an increased level of competition, a rebound in demand as a result of the inventory build-up and, equally important, social-political tensions in the North African region and the repercussions of the natural disasters in Japan – but we know that we can rely on our solid and sustain-able growth model.A model inspired by the integrat-ed management system typical of excellence-oriented companies, which makes the development of new prod-ucts one of its fundamental features.

Our level of innovation is constantly increasing and today about 30% of the turnover is generated by new solutions introduced in the last three years.Thanks to this solid foundation, in 2010 we could concentrate on the identification of new development drivers, represented – in the produc-tion area – by transmissions for elec-tric applications in the automotive sector and – in the sales area – by the focus on emerging markets, such as Brazil, Russia and India.

Still together, towards new goalsWhen people manage to unite around shared values and join together in a common mission, they can achieve extraordinary results. This is what we’ve realized in our first forty years, and this is how we will con-tinue to grow, ready to meet the new global challenges.

Fabio StorchiPresident and CEOComer Industries Spa

5

Financial data

Revenues

EBITDA

2010 27,818 + 86.3%

2009 14,930 - 51.0%

2008 30,489 (thousand euros)

2010 10,690 +735.2%

2009 1,280 - 89.6%

2008 12,352 (thousand euros)

2010 79,104 + 19.0%

2009 66,472 - 1.4%

2008 67,440 (thousand euros)

2010 276,534 + 14.6%

2009 241,328 - 27.0%

2008 330,785 (thousand euros)

Net profit

Net shareholders’ equity

6

Turnover by sector

Turnover by geographical area

Net financial position

2010 27,870 - 42.2%

2009 48,187 - 39.7%

2008 79,898 (thousand euros)

2010 1,217 + 6.3%

2009 1,145 - 15.2%

2008 1,350 (units)

Personnel

51.3%Agriculture

47.6%Industry

1.1%Other

35.3%EU countries

27.7% North America

14.9%Italy

17.2%China

4.9%Rest of the world

7

Comer Industries is a global leader in the design and production of advanced engineering systems and mechatronic solutions for power transmission. Our customers are the main manufacturers of agricultural equipment, industrial machinery and renewable energy applications worldwide.

Comer Industries at a glance

» Combine harvester and self-propelled machines » Fertilizing machines » Forage harvesting, processing and distribution machines » Forestry machines » Harvesting machines » Irrigation and crop treatment equipment » Land preparation machines » Multi-utility vehicles » Professional gardening and landscaping equipment » Soil tillage machines

» Airport equipment » Construction and earth moving machinery » Cranes and lifting equipment » Marine industry » Material handling and logistics vehicles » Municipal equipment » Parks and entertainment » Road construction equipment » Stationary industry

» Wind generators » Biogas machines » Solar panels

Agricultural applications

Industrial applications

Energy applications

COMER INDUSTRIES Inc. - Charlotte, NC, USA

Applications

8

» Control systems and electronic adjustment devices for hydrostatic transmissions

» Driveshafts, safety devices for driveshafts, mechanical clutches and safety devices

» Electric wheel drive units, electric and hydraulic steering gears » Gearboxes, speed changes gears, parallel and right angle shaft speed

increasers and reducers » Modular planetary gear drives, planetary track and wheel drives, slew drives,

special planetary gear drives for industrial applications » Orbital motors » Rigid and steering axles

Advanced engineering systems and mechatronic solutions

COMER INDUSTRIES U.K. Ltd. - Desford, LE, United Kingdom

COMER INDUSTRIES Sarl - St. Thibault des Vignes, France

COMER INDUSTRIES GmbH - Kornwestheim, GermanyShanghai Branch Office, China

COMER INDUSTRIES (SHAOXING) CO. Ltd. - Shaoxing, China

Products

COMER INDUSTRIES Spa - Headquarters, Reggiolo (RE), Italy

Mechatronics Research Center - Reggiolo (RE), Italy

Comer Academy - Reggiolo (RE), Italy

Operating Units:

• AXLES & WHEEL DRIVE UNITS - Reggiolo (RE), Italy

• GEARBOXES - Reggiolo (RE), Italy

• DRIVESHAFTS - Pegognaga (MN), Italy

• PLANETARY DRIVES - Cavriago (RE), Italy

• COMER INDUSTRIES COMPONENTS Srl - Matera, Italy

• COMER INDUSTRIES (SHAOXING) CO. Ltd. - Shaoxing, China

9

Comer Industries is finalist in Confindustria’s“Awards for Excellence”February, Turin, Italy

The innovating force of Comer Industries is highlighted among the

examples of “Made in Italy” excellence at the 2010 edition of the

“Awards for Excellence”, the event organized by Confindustria to

celebrate its anniversary.

Comer Industries is chosen among the three finalists in the category

“Business champion of innovation” for its promotion and exploita-

tion of innovation interpreted as the ability to invest in research and

development, human resources and technology.

The award is presented to Fabio Storchi by the President of

Confindustria Emma Marcegaglia (see picture).

2010 highlights

The company celebrates its first forty yearsMarch, Reggiolo, Italy

Comer Industries celebrates 40 years of business. The notarial deed

with which Fabio, Fabrizio and Oscar Storchi founded the unlimited

partnership CO.ME.R. – Costruzioni Meccaniche Riduttori – special-

ized in the manufacture of mechanical transmissions for agricultural

machinery, is dated March 24, 1970.

It was the beginning of the success story of Comer Industries, global

leader in the design and production of advanced engineering sys-

tems and mechatronic solutions supplied to major manufacturers of

agricultural equipment, industrial machinery and renewable energy

applications worldwide (see picture, 40th anniversary logo).

Smart irrigation gives rise to a new approachApril, Reggio Emilia, Italy

Comer Industries presents its mechatronic GP2 solution for hose reel

irrigators during the “Innovation Day”, the research and development

event organized by the Faculty and Department of Sciences and

Engineering Methods in the University of Modena and Reggio Emilia.

The revolutionary system (see picture), developed in collaboration

with other companies in the industry and with public bodies includ-

ing ENAMA (National Institute for Agricultural Mechanization), helps

to safeguard the environment, ensuring a smart management of the

irrigation process and optimizing water distribution.

Comer Academy, second year of activityMay, Reggiolo, Italy

Comer Academy, the internal training and management school with

the objective of enhancing the professional skills of personnel and of

promoting organizational and cultural change, continues its intensive

training activities. 88 courses held, 8,600 training hours offered, 71%

of personnel involved in 2010.

The new MyComer.com portalJune, Reggiolo, Italy

A new structure, new contents and a new look for Comer

Industries’ intranet portal on SAP platform.

MyComer.com has been developed to provide staff with a tool

for collecting and sharing information and company procedures.

Aimed at optimizing relations both internally and with partner or-

ganizations, the project is destined to grow over time, supporting

change for the continuous improvement of processes.

SECOND quARTERFIRST quARTER

10

The innovation of Comer Industries at Expo 2010July, Shanghai, China

Comer Industries takes part in the “Italy of innovators” exhibition,

during Expo 2010, with its mechatronic hose reel irrigation system

E-GPF, selected among 454 projects to represent the cutting edge

technology of Italian companies.

The event was held from July 24 to August 7 in the Italian pavil-

lion (see picture), one of the most visited during the great show in

Shanghai. The solution developed by Comer Industries receives

unanimous appreciation for its ability to integrate the drive with the

electronic wireless control and the GPS positioning system for a

complete automation of all the operating phases and for a sustain-

able use of the water resources.

Awarded as one of the most innovative Italian companiesJuly, Rome, Italy

Comer Industries, selected out of 671 participating companies,

receives a special mention (see picture) in the 2010 edition of the

“Enterprise Award for Innovation”, a competition organized by

Confindustria in collaboration with Associazione Premio Qualità Italia

(Italian Quality Award Association).

ThIRD quARTER

Meeting with the Kaizen guru October, Reggiolo, Italy

A day at Comer Industries with Professor Masaaki Imai. The father of

the Kaizen method (Kaizen = change for the better) and founder of

the Kaizen Institute is the company’s guest for a public conference on

the Kaizen concepts concerning organization excellence.

Visiting the production sites in Reggiolo, Professor Imai (see picture,

between Fabio and Fabrizio Storchi) appreciates the progress made

by Comer Industries since the introduction of this method and gives

useful advice for continuing along the path of change.

EIMA 2010 Technical Innovation AwardNovember, Bologna, Italy

A new prize for Comer Industries’ capacity for innovation. The

AJC (Active Jump Control) mechatronic system wins the Technical

Innovation Award at the 2010 edition of EIMA, the most important

trade fair dedicated to farming mechanization.

The AJC patented system – designed for cutting bars and other har-

vesting equipment – ensures uniform results in variable land surface

conditions.

The Comer Industries case study at SAP World TourNovember, Milan, Italy

The ICT model project supporting the Comer Production System

(CPS) is presented at a conference during the “SAP World Tour

2010”, held at the Congress Center in Assago Milanofiori. The event

is an opportunity for the multinational German leader in the manage-

ment software sector to meet and exchange views with a number of

its important Italian customers.

FOuRTh quARTER

11

12

Competence

13

Involvement, constructive attitude, com-mon aims, attainment of objectives for continuous improvement. These are the aspects characterizing the partici-pation of Comer Industries’ employees and collaborators in the deep cultural change introduced in the company since 2009.To face the evolution in the macroe-conomic scenario and with a view to promoting growth in the long-term, the company is committed to simplify and rationalize its processes, to create a lean organization able to react quickly to evolving demand. The excellence of Comer Industries is achieved through its people, called upon to upgrade their professional level and broaden their skills.

Comer Academy, a driver of changeIn its second year of activity – estab-lish mid-2008 – Comer Academy, the in-house training and management school, has played an important role in developing human resources and en-hancing abilities through an intensive and targeted training program. The 88 courses held in 2010, for a total of around 8,600 education hours of-fered, involved 71% of company per-sonnel. The main areas covered were the CPS-Kaizen (accounting for 35.1% of the Academy’s activities), safety and the environment (26.1%), technical-spe-cialist (22.3%) and managerial (16.5%) (see p. 15).

The main training projects started in 2010Comer Academy has been an es-sential vehicle for ensuring the ef-fective implementation of the Comer Production System (CPS) (see p. 22). During 2010 the school held a course at an inter-departmental level for pre-paring Kaizen Coaches: experts in the use of tools associated with this meth-odology lending their professionalism to their colleagues and encouraging the opening of CPS workshops.The personnel in the Production, Times and Methods, Logistics and Quality areas was involved in Total Flow Management (TFM) program, with the goal of learning the principles and techniques for the improvement of flows, with significant benefits in terms

People: at the heart of change

14

of productivity, space arrangement, re-jects reduction and the optimization of process times. Besides lessons held in the classroom, also TWI (Training Within Industry) was applied, a pro-gram based on the learning-by-doing approach, with sessions organized in the production sites where the Kaizen workshops are already operating. A specific training program was set up for the Purchasing department: in particular, a course was designed to examine negotiation tools and tech-niques, with the objective of achieving better results in negotiations with sup-pliers.Executive personnel took part in the Public Speaking workshop, aimed at ameliorating communication in Comer Industries at all levels, and in the Time & People Management course, to identify areas for improvement in time scheduling and for the effective lead-ership of people and work groups. To encourage the diffusion of a par-ticipative culture, Comer Industries arranged meetings with workers, in which the projects for change were explained and shared.

A new work organization: the effects on business and peopleThanks to more productive com-munication, which have gener-ated a strong team spirit, people have welcomed the new approach

focused on better results and ef-ficiency. As a consequence, it was possible to introduce a new work organization model which optimizes the plant exploitation: weekly sched-ules of 17 and 16 shifts were started in the production sites of Moglia and Reggiolo. This allowed Comer Industries to return to growth in the second half of 2010, interrupting the use of social safety net provisions al-most everywhere – Cassa Integrazione Guadagni Ordinaria – Wages Guarantee

Fund – and Contratto Di Solidarietà – Job-security agreements – widely used during 2009.This renewed competitiveness also had positive effects on employment levels: in the last 12 months staff numbers grew by 6%, reaching 1,217 people. Of these, 12% are female, while non-Italian workers account for 16% of total workforce.

Evolution of the ASC projectThe Appraisal System Comer (ASC) project also continued in 2010: after its debut by courses held by Comer Academy, the company system for appraising workers’ performance and conduct, within a growth perspective, was extended to the entire office staff, more than 450 people in Italy and abroad.

Involvement, constructive attitude, common aims, achievement of objectives for continuous improvement. These are the aspects characterizing the participation of Comer Industries’ employees and collaborators in the deep cultural change introduced in the company since 2009.

Comer Academy, the in-house training and management school, has played an important role in developing human resources and enhancing skills through an intensive and targeted training program.

26.1%training re safety-environment

16.5%managerial training

35.1%trainingre CPS-Kaizen22.3%

technical-specialisttraining

Comer Academy - training areas

(% of total internal training hours - 2010 data)

15

Ensuring real and sustainable growth while minimizing pollution, global warming and the exploitation of natu-ral resources: this is the foundation of the green economy, a commit-ment involving the governments of the most developed countries and a rising number of companies.According to the latest “Green Economy” report issued by the United Nations Environment Program, renew-able sources account for around 15% of the global energy demand: a percent-age expected to double by 2050.Closely focused on the evolution of the global scenario, over the years Comer Industries has acquired the ability to respond to the increas-ingly changing requirements of the customers. Its technological and process specialization allows the company to be actively involved in this green revolution, designing and implementing solutions for strategic partners sharing the same environ-ment sustainability goals.

The future of automobiles: electric vehiclesIn 2010, the most interesting improve-ments concerned electric cars. As con-firmed by the increasing investments in Research and Development of automo-bile manufacturers, this is a market with exponential growth rates.According to a survey by the US Department of Energy, considering both private mobility and metropolitan service fleets, the number of electric hybrid vehicles sold jumped from 9,350

in 2000 to 274,210 in 2010. In addition, in line with the forecasts of the Obama Administration, by 2015 one million elec-tric vehicles will be driven on US roads.

Mechanical drive for Mia Electric electric city carsFor Mia Electric, a French company and global leader in the manufacturing of electric vehicles, Comer Industries has designed a mechanical drive for city cars (see pictures). This solution consists of a differential gear distin-guished by high rotation speed able to satisfy demanding efficiency and silent-operation requirements.The drive was developed by Comer Industries starting from partner speci-fications and adopting a New Product

Development pattern typical of the au-tomotive industry. The reference model is the Advanced Product Quality Plan (APQP): to minimize the risk of faults, product and production process are planned jointly. The system is currently undergoing tests and validation at the Reggiolo Mechatronics Research Center.

New development drivers from the green economy

Comer Industries has acquired the ability to respond to the increasingly changing requirements of the customers.Its technological and process specialization allows the company to be actively involved in the green revolution.

16

Comer Industries growth strategies are based on product innovation, as confirmed over recent years by the impact of new solutions on total turn-over: one third of the 2010 revenues comes from products developed in the last three years.Besides the mechanical drive de-signed for electric city cars (see p. 16), Comer Industries also presented other innovative products: the S128 differen-tial axles, solutions for multi-megawatt (MW) wind turbines and drives for high capacity combine harvesters.

S128 differential axles The S128 rigid and steering differen-tial axles can be used both for road vehicles such as sweepers and air-port tractors and for off-road applica-tions such as the telehandler, with a load capacity of up to 3 tons, and the compact front loader, with an empty weight of 6 tons.

This solution features compact di-mensions, excellent load and power transmission capacity, thanks to the top quality of the critical components and cutting-edge CAD simulation programs. Compared to old genera-tion axles, the S128 model ensures upgraded efficiency in order to cater for the growing needs of manufactur-ers in terms of energy saving and cut-ting emissions.

The new solutions for multi-MW wind turbinesAccording to the Global Wind Energy Council, in 2010 installed wind power capacity rose at global level by 22.5% compared to the 12 pre-vious months, reaching 194.4 GW. For the first time, more than half of such power increase has involved markets other than traditional North America and Europe: 16.5 GW of the new 35.8 GW were in fact installed in China, the new world leader in terms

of capacity, followed by the USA.In the Asiatic region, Comer Industries has strengthened its presence in the wind power sector. Thanks to the contribution of the Mechatronics Research Center, in late 2010 the company presented the first drive prototypes for 5 MW wind turbines; this is a specific class of multi-MW turbines, destined to become the standard of the future for offshore wind farms. The Comer Industries product range now includes multi-stage planetary drives such as the PG 3000 pitch drive system, and the PG 6500 yaw drive system. These products adopt engineering solutions to ensure reduced weight and overall dimensions, providing for the specific requirements of the multi-MW class turbines in terms of efficiency, reliability, aerodynamic performance, production capacity in case of low wind speeds and noise reduction.

Cutting-edge engineering and technological solutions

What our customers say about us > Claas

The cutterbar drive for highcapacity combine harvesters

The company Claas, leading German manufacturer of agricultural

machines, is using a drive from Comer Industries in its 10.5 meter

and 12 meter cutterbars for combine harvesters.

«Ever larger combine harvesters with ever higher performance call for cut-terbars with similarly enhanced dimensions and capacity. And, of course, the great thing about higher performance is that it means lower costs.Claas’s cutterbars are driven on both sides via transmissions and driveshafts and are therefore able to meet the most demanding requirements. The tele-scopic driveshaft allows the divided knife to operate at a high cutting fre-quency in all table positions. The synchronized transmission drive makes for optimum low-noise operation while the driveshafts ensure slip-free power transmission – and all with minimal maintenance requirements.The knife drives on each side are protected against overload by shear bolts while protection for the intake auger is provided by a cam-type power inter-ruption clutch. These features mean that harvesting operations can proceed quickly and safely».

17

Investing in organization, product and process innovation is the policy that enabled Comer Industries to grow significantly during its first forty years of business and become global leader in the power transmission sector.

The Mechatronics Research CenterThe Mechatronics Research Center of Reggiolo plays an essential role in developing new solutions. In this fa-cility, which extends over a total sur-face area of 1,500 m2 and features 11 soundproofed test rooms, in 2010, 150 customer requests were complet-ed with a total of about 36,000 testing activities hours.

The partnership between Comer Industries and ENAMAComer Industries can also rely on stra-tegic alliances with the academic world and with public Research Institutes in terms of innovation and research.The important partnership with the National Institute for Agricultural Mechanization (ENAMA) started in

2009 with the mechatronic hose reel irrigation system E-GPF, which took the Gold Medal at the SIMA Innovation Awards 2009; cooperation between Comer Industries and ENAMA contin-ued through 2010, concretizing in the AJC smart package, the first feedback control solution in the agricultural field for the active management of the ad-herence of cutting bars and other har-vesting machinery to the soil.The patented system grants uniform results in variable soil surface condi-tions thanks to a system of anti-detach-ment springs, electronically-controlled shock absorbers, accelerometers and a control unit.The AJC system ensures remarkable advantages: maximization of the prod-uct, reduction of cut irregularities and operating time, lower product contam-ination and less need for maintenance.The great usefulness of the AJC me-chatronic system developed by Comer Industries in increasing the quality of the performed operations is confirmed by the EIMA 2010 Technical Innovation Award.

The future-oriented program of R&D

18

19

20

Competitiveness

21

Comer Production System: the road to excellence

In 2010, Comer Industries has ex-tended the application of the Comer Production System (CPS) to the newly integrated manufacturing pro-cess control model adopted in 2009.Based on Lean Organization princi-ples and according to Kaizen prac-tices, the CPS was introduced in all Operating Units through pilot work-shops in the critical areas of each facility. This method is enabling the compa-ny to boost its performance ratings to world class level, to cater to cus-tomer requirements, reduce stocks and achieve greater flexibility and speed in the logistics and process-ing chain.

Involvement of all personnelCrucial for achieving these results is the deep and widespread involve-ment of all the personnel: more than a technical and process revolution, for Comer Industries CPS is a deep cultural change. All people have been asked to provide ongoing commit-ment to gradually elevate work stand-ards, with a real savings in terms of cost and higher quality: the goal is

excellence, obtained through the zero defects, inventories and acci-dents.In Comer Industries, improvements are departmental, determining the workstation where the problem has appeared. The root causes are iden-tified and eliminated while implemen-tation of a standardized solution pre-vents it from reoccurring.

Thanks to the deep and widespread involvement of all the personnel, the CPS is enabling to boost the company’s performance ratings to world class level, to cater to customer requirements and achieve greater flexibility and speed in the logistics and processing chain.

In 2010, the application of the CPS model has yelded financial benefits to Comer Industries for approximately one million euros. The expectation for 2011 is to decrease production costs by another 1.4 million euros.

22

The CPS temple

A temple is the symbol of CPS struc-ture, whose base contains the main values and seven methodological pil-lars supporting the strategic objectives of Comer Industries:

1. flow production and workplace or-ganization: in order to speed up the production flow, workplaces must be arranged to reduce useless move-ments and upgrade neatness and cleanliness;

2. logistics: Comer Industries requires the integration of its suppliers, asking them to constantly and smoothly supply the lines according to Just In Time logistics. This method allows

the company to produce what the customer demands when necessary, without restrictions of minimum quan-tities while reducing cost and lowering inventories;

3. Total Productive Maintenance (TPM):operator and service technician skills are upgraded to reduce and prevent plant breakdowns and keep them working properly;

4. Total Quality Management (TQM): all people are involved on a daily basis in analyzing any faults detected along the process line with the aim to optimize efforts and total quality (zero defects);

5. safety and environment: procedures are standardized and people are ac-tively committed to reducing accident risks and environmental impacts to the utmost (no injuries, no damage to the environment, see p. 37);

6. New Product Development (NPD): Comer Industries has adopted an automotive model for the product development process, which consid-ers interaction between design, pro-duction, supply chain and quality, to develop innovative solutions able to satisfy customer demands in terms of performance, cost, launch time and reliability;

7. continuous improvement: this re-quires the direct and widespread in-volvement of human resources. In this perspective and with training sessions organized by Comer Academy, Comer Industries set its organization on a path towards excellence, with a CPS Manager in charge of the transforma-tion program. The CPS Manager is supported by seven pillar leaders, with the task of implementing each pillar.

The introduction of CPS is a radical change positively influencing people’s job performances and focusing them on constant improvement. Comer Industries is strongly committed to encouraging the progressive application of this method in all its Operating Units, increasing the efficiency of each of them and of the company as a whole.

People

Continuous Growth

Product and Process Excellence

People involvement

Standard PDCA Motivation Teamwork

1. F

low

pro

duct

ion

and

wor

kpla

ce o

rgan

izat

ion

2. L

ogis

tics

3. T

PM –

Tot

al P

rodu

ctiv

eM

aint

enan

ce

4. T

QM –

Tota

l Qua

lity

Man

agem

ent

5. S

afet

y an

d en

viro

nmen

t

6. N

PD –

New

Pro

duct

De

velo

pmen

t

7. C

ontin

uous

impr

ovem

ent

23

The CPS workshops set up in Comer IndustriesCPS workshops have been set up in all Comer Industries Operating Units, with a total of 25 projects. The most im-portant experiences in terms of results achieved – which received the end-of-year CPS Award – were conducted at Cavriago, Moglia and Reggiolo.In Planetary Drives, the project in-volved the shipping department and the assembly lines of construction machinery products: facility layout was changed to set up a dedicated area, obtaining a significant savings of space and improved workplace organization. Productivity increased from 10% to 30%, depending on the initial conditions of the line involved.In the Moglia plant, machines were positioned according to the machining cell criteria, to produce one piece at a time, reducing inventories and inter-mediate dead times: this allows shorter delivery times to customers by over 10 days. Furthermore, thanks to the “We Make Quality” project, rejects were re-duced by 50%, decreasing the faulty Parts Per Million (PPM). At Reggiolo, in the Gearboxes Operating Unit, 50% of the assembly lines were transformed according to the Kaizen model, elimi-nating activities with no added value, maximizing ergonomics and optimiz-ing occupied space. Overall produc-tivity increased by 20% (with peaks of 35%). In the Zero Defects workshop of the Gearboxes machine department, the number of rejects has already been reduced by 50%.

The benefits of the CPS modelIn 12 months, the application of the CPS model has yielded financial ben-efits to Comer Industries for approxi-mately one million euros. The expecta-tion for 2011 is to decrease production costs by another 1.4 million euros, to partially offset the strong rise in the raw materials costs of the recent months.The importance of the CPS results in boosting the performance of Comer

Industries has been acknowledged by Professor Masaaki Imai, President of the Kaizen Institute, during his visit on October 13, 2010 at the company’s Gearboxes Operating Unit. After seeing the progress made, Imai delivered to Fabio Storchi, President and CEO of Comer Industries, the Kaizen Spirit certificate, affirming that «[…] the application of Kaizen in Comer Industries is achieving, step after step, standards of excellence at

global level. The Kaizen spirit and its values are widely and constantly ap-plied».

The extension of the CPS to the supply chain In 2011 Comer Industries expects to extend the CPS method to the rest of its supply chain, including provid-ers and clients.Considering the important role of the suppliers for the customer value

24

creation process (80% of the cost of the company’s products comes from external supplies), Comer Industries has decided to support them in changing their organiza-tions to attain excellent quality and

service standards.In the customer service area, a new project will review the order man-agement process and sales plan-ning to further upgrade the reliability of information and market delivery.

Masaaki Imai, President of the Kaizen Institute: «The applicationof Kaizen in Comer Industries is achieving, step after step, standards of excellence at global level. The Kaizen spirit andits values are widely and constantly applied».

25

Investments in the Information and Communication Technology (ICT) sys-tem have made a significant contribu-tion to Comer Industries’ competitive-ness during 2010. The entire technological infrastructure has been updated as part of a con-tinuous improvement approach, with a view to optimizing performances, reli-ability and flexibility, and at the same time considerably reducing manage-ment costs.

Strengthening the data network and the benefits of virtualizationIn 2010 Comer Industries moved its SAP systems onto a new technologi-cal platform that allows for virtualiza-tion and for sharing available hardware resources without leaving any of them unexploited, adding equipment as re-quired, ensuring continuity and flexibil-ity for business operations. Comer Industries’ electronic mail system is also new (the server manages around 700 mailboxes): this choice comes from the need to grant greater security and to manage an increasing volume of data for internal and external communication.The strengthening of the 23 data lines that connect the company’s sites to the central Datacenter is the important final complement of a reorganized and updat-ed infrastructure able to support Comer Industries’ growth in the coming years.

ICT supporting the CPSThe evolution of the Information Technology system has fostered Comer Industries’ adoption of a Kaizen approach, started with the introduc-tion of the Comer Production System. In 2010, a new manufacturing flow scheme was set up in the Operating Unit of Matera, identified as a pilot workshop with the aim of improving planning ability, starting from the fore-cast of market trends and the analysis of their impact on the internal produc-tion line and on the supply chain.At the same time in the Reggiolo fac-tory, the procurement system for the assembly lines was optimized and the programs were implemented for inte-grating customers and suppliers deliv-ery schedules into the company’s ICT system. The factory of Cavriago hosted the de-velopment team working on the proto-type for interfacing the machine tools with the central information system, for monitoring the plant in real time.

The entire technological infrastructure has been updated as part of a continuous improvement approach, with a view to optimizing performances, reliability and flexibility, and at the same time considerably reducing management costs.

The renewal of the ICT infrastructures

26

BI projectsBusiness Intelligence (BI), the activities directed towards collecting, organiz-ing and examining data for supporting company strategies, got under way in Comer Industries with the creation of a Data Warehouse for the sales area. Information is now acquired us-ing uniform criteria and codes, mak-ing it possible to extend the range of analyses and to improve the reliability and punctuality of its processing and distribution.In 2011 the BI tools will be consoli-dated and extended to other company areas, with the objective of summariz-ing them in a series of key indicators for management.

ICT for human resourcesDuring the year Comer Industries laid the base for the introduction of a cen-

tralized Human Capital Management system. The functions provided by a special SAP module allow for central administration of all the events con-cerning employees’ working lives: it’s an essential foundation on which to build future development, training and assessment projects for Comer Industries’ personnel.

The new MyComer.com portal Comer Industries’ ICT activities in 2010 included the introduction of the MyComer.com portal: created as an evolution of the Intranet, it is an inte-grated tool for gathering and sharing all company procedures and informa-tion. Further developments are planned in order to strengthen online communi-cation both internally and with partner organizations.

27

Competing and developing on the global markets requires a careful manage-ment of production resources. As part of the changes implemented by Comer Industries for continuous improvement, an analysis of all operating sites has been carried out in relation to company strat-egies. The result has been the approval of an important investment program for the period 2011-2014. The plan takes into consideration many variables: the expected scenario in the next 3-5 years with reference to volumes with break-down of the different market sectors by geographic areas, including emerging countries; the technical evolution of prod-ucts and processes; the manufacturing and service demands of main custom-ers; current output capacities and man-agement costs of the production sites.

The strengthening of Comer Industries ComponentsExtension works of the Matera plant are expected to finish in 2011, with an in-crease of around 8,200 m2 of the total surface area. With an overall investment of around 18 million euros, the manufac-turing lines of planetary drives for wind turbines and their main components will be expanded with the introduction of new robotic machine tools and new systems for heat treatments and for painting finished products.

As a result, the annual output capacity of the Matera Operating Unit will ex-ceed 100 million euros, against the cur-rent value of approximately 60 million.

Integration of the production unitsin CavriagoDuring 2011, the production units of drives for industrial applications and of drive axles will be united into the Cavriago facility with an investment of around 2 million euros. The operation will foster a more efficient

The new industrial plan will allow Comer Industries to make significant enhancements in efficiency and to push qualitative levels towards zero defects, optimize internal logistical resources and improve operators’ working environment and conditions.

The new industrial plan

28

utilization of the site’s industrial capac-ity which, at full stretch, will achieve more than 120 million euros per year.

Rationalization of the agricultural application sector in ReggioloWorks for integration and extension of the Reggiolo factories for the as-sembly of products for agricultural applications will also start in 2011. Investments for more than 12 million euros are planned, with a new in-dustrial area of around 5,000 m2, the complete refurbishment of another 4,800 m2, new assembly plants, a modern painting system and a lo-gistics center. As a result, the output capacity of the Reggiolo facilities for agricultural applications will exceed 135 million

euros per year, against the current value of approximately 90 million. Thanks to the gradual implemen-tation of the Comer Production System (CPS), the new industrial plan will allow the company to make significant enhancements in effi-ciency and to push qualitative lev-els towards zero defects, optimize internal logistical resources and im-prove operators’ working environ-ment and conditions.

Future programs in a globalperspectiveIn the coming years, further invest-ments will involve other product lines and the working processes current-ly in place in China. The goal is to strengthen Comer Industries’ com-

petitiveness on international mar-kets – consistently with consolidated policies that provide for keeping in Italy Research and Development strategic activities and the manu-facture of goods with a high tech-nological content – with a significant consequential increase and upgrade of human resources.The adopted changes aim at satis-fying the demands of large global manufacturers needing for reliable partners throughout the world, also in other countries, where they have established or intend to establish new production sites: to ensure them high value solutions at com-petitive prices directly to their as-sembly lines, with a punctual and efficient service.

29

The growth in volumes and revenues during 2010, apart from the obvious economic-financial benefits, has made Comer Industries more competitive for the future: in particular, it will allow making the necessary industrial invest-ments to recover efficiency and further improve the processes.

Less waste, better qualityWith the production increase for the wind power sector, the Matera facility – once expansion has been com-pleted – will be equipped with a plant for the heat treatment of components before grinding and final release for as-sembly. The result of the new industrial plan will be the optimization of all manufactur-ing areas in each Operating Unit and a reduction in process and delivery times: Comer Industries will benefit in terms of less waste, greater flexibility

and better quality.Thanks to higher purchasing volumes, the company will select an even better-qualified class of suppliers able to pro-vide more efficient services, consistent with the needs of Comer Industries and of the large manufacturers of agri-cultural equipment, industrial machin-ery and renewable energy applications worldwide.

Growth, cornerstone of competitiveness

30

Business development in China

In 2010, China became the world second-largest economy after the United States, pushing Japan to third place.Comer Industries has achieved posi-tive results in a market that grew by 10.3% compared to 2009. In 12 months the turnover generated by Comer Industries (Shaoxing) Co. Ltd. almost quadrupled, thanks in particu-lar to the strengthening of the part-nership with the leading Chinese pro-ducers of wind energy. This goal was reached by supplying them planetary drives for pitch and yaw systems. Many of the major European wind pow-er players have also chosen Comer Industries for their local production in China, confirming the company’s strategy of geographical proximity.

Reorganization of the Shaoxing structure The remarkable volume increase in China has been supported by an ex-pansion of the resources dedicated to the administration of the Shaoxing factory, setting up a recruitment and upgrading program for management and for second-level employees. Around fifty new workers were hired, for a total workforce at the end of 2010 of 118 people (in addition to the 17 people working in the sales office in Shanghai).This strengthening has mainly in-volved the production, quality control and logistics departments. Targeted

training – compatible with Comer Industries’ general objectives – and specific courses dedicated to the de-mands of the Chinese market were held for all key personnel.

Strategic suppliesThe reorganization of the Chinese plant also involves the selection and development of qualified local suppli-ers who can adequately support the growth in volumes. The purchasing structure has been enhanced with the introduction of new management personnel for the coor-dination of materials and goods con-nected with Shaoxing’s manufacturing site and of finished products handledby the sales office. With regards to the future, the new set-up of the production structures as part of the general industrial ration-alization plan is currently under review (see p. 28).

Not only wind powerComer Industries is also present in the large Asian market with other products and mechatronic solutions for agricul-tural and industrial application; the de-mand from these sectors is destined to raise significantly in coming months.

The future from the Orient’sperspectiveChina, where Comer Industries has been operating for more than two decades, is getting more and more important as part of the company’s development strategy, a trend that will continue to characterize the next few years. The Chinese Prime Minister, Wen Jiabao, has announced a decrease of the economic growth target for his country to 7% for the five-year period 2011-2015 (the previous forecast of 7.5% in the last six years was always widely exceeded), and a commitment to contain inflation, with a view to more sustainable expansion, also regarding environmental impact.According to the International Monetary Fund, in 2011, economic growth is ex-pected to be slightly under 10%.

In 12 months the turnover generated by Comer Industries (Shaoxing) Co. Ltd. almost quadrupled, thanks to the strengthening of the partnership with the leading Chinese producers of wind energy.

31

BRIC, emerging markets for growth

Comer Industries is a global organiza-tion that adopted geographical prox-imity to its customers as an important competitive strategy: this involves in-vesting in countries where the major manufacturers of machines for agri-culture, industry and the production of renewable energy are focusing their activities, with the aim of meeting their demand in terms of production and service in an increasingly effective way.

The future of businessComer Industries is paying great atten-tion to the development area known as the “BRIC” group of countries (Brazil, Russia, India and China). According to the International Monetary Fund’s World Economic Outlook, China (together with India) is the economy with the highest growth in 2010: GDP expanded by 10.3% over the previous 12 months. To make a comparison, in the same

period the GDP of the advanced econ-omies rose by 3%. Brazil had a bet-ter performance after a difficult 2009, seeing its GDP increase by 7.5%. Russia also registered growth.

Brazil, a new leading playerFor Comer Industries, China and Brazil are enjoying an increasing role in the world economy (see p. 31).In the South American country, where the company is examining the possibil-ity of setting up a sales subsidiary, the agricultural mechanization business is expected to grow at double digit rates and the prospects of expansion of the road and construction industry are even more significant. In view of the football World Cup in 2014 and of the Olympic Games in 2016, Brazil will implement a renewal project including its infrastruc-ture network and city planning.

32

Geographical proximity to the customers as an important competitive strategy: Comer Industries is investing in countries where the major manufacturers are focusing their activities,with the aim of meeting their demand in terms of production and service in an increasingly effective way.

33

34

Continuity

35

A solid financial base for development

The prospects for development of Comer Industries are closely linked to its financial stability. Also in 2010, the company continued to consist-ently and effectively increase its fi-nancial cash position, achieving a sharp reduction in indebtedness: from around 48 million euros in 2009, this figure fell to an amount of less than 28 million euros.

Almost equal to EBITDA This ratio, nearly the same of EBITDA, proves the economic soundness and confirms the company’s poten-tial ability to reimburse its debt in a single fiscal year: an excellent finan-cial condition, especially considering that only a part of Comer Industries’ debt position is short-term. In a competitive global scenario that is only partially recovered in pro-ductivity and profitability, but is still facing financial difficulties, Comer

Industries can put renewed trust in its approach towards the new mar-ket challenges and with regards to the significant investments it is com-mitted to make.This positive situation is the result of the company’s efforts to react quick-ly to an unprecedented economic and financial turmoil: thanks to its solid foundations and evolutionary approach to process controls, all measures have been implemented with determination and flexibility.

Also in 2010, Comer Industries continued to consistently and effectively increase its financial cash position, achieving a sharp reduction in indebtedness.

36

Committed to sustainability and safety

In the last few years, Comer Industries has paid increasing attention to the environmental sustainability of its pro-duction activities and to safety.With the creation of the Environmental Quality Health and Safety (EQHS) Department, these themes have be-come an integral part of company management.

The commitment to sustainabilityWith the aim of gradually reducing its environmental impact, Comer Industries has fixed some voluntary targets, monitoring their achievement by the EQHS department. In 2010, action was focused on the production and supply chain. In the first case, the company implemented strategies for the separate collec-tion of consumable waste materials, replacing throwaway packaging with reusable and returnable solutions and a great effort has been devoted to the process for the disposal of used oils. With regards to the supply chain, Comer Industries’ commitment was reflected in the increased use of raw materials with less environmental im-pact.

Environmental certificationThanks to these improvements, Planetary Drives and Comer Industries Components have obtained the envi-ronmental certification. The company is planning to extend ISO 14001 stand-

ard certification to all Operating Units and to Subsidiaries by the end of 2011.

The focus on safetyOne of the main tasks of EQHS de-partment concerned safety: as set out in the Code of Practice and Conduct, adopted in accordance with Italian Legislative Decree 231/2001, Comer Industries is committed to safeguard-ing the health and safety of its person-nel in the workplace.Thanks to special training courses held in 2009 by Comer Academy to promote safe conduct based on indi-vidual responsibility (see p. 14), in 2010 the company set up the Safety for Us (SFU) pilot project in the Driveshafts and Gearboxes Operating Units. This schedule involves the organiza-tion of daily or weekly meetings in which the relevant team investigates the risks associated with single proc-esses: “near-miss” is the basic con-cept, and focuses on the indicators of potential accidents, even if the event fortunately does not occur. Near-miss management is a powerful tool for assessing risks and identifying system weaknesses and dangers.

Results of the SFu projectThe adopted model has had positive effects on the absolute number of accidents, on the Frequency Index, calculated as the ratio between the accidents occurring in a year and the number of working hours in the same period of time, and on the Severity Index, which expresses the average number of days lost by each worker as a consequence of accidents. Since the introduction of SFU in March 2010 in the Gearboxes machine de-partment in Moglia, no accidents were reported in the following nine months, while in the Gearboxes assembly plant, where the project was applied to a specific production line, the level of accidents decreased by 30% over the previous year.

Future safety initiativesIn 2011 SFU will be extended to other Comer Industries Operating Units, with the objective of implementing an effective safety management system at a general level, to obtain the OHSAS 18001 (Occupational Health and Safety Assessment Series) certification by the end of 2012.

Comer Industries is planning to extend ISO 14001 environmental certification to all Operating Units and to Subsidiaries by the end of 2011. The Safety For Us project has had positive effects on the absolute number of accidents and will be applied in all O.U.

37

According to the International Monetary Fund, the recovery start-ed in 2010 will continue in 2011. On the basis of IMF forecasts, the global economy will grow this year by 4.4%, with an estimate of +4.5% for 2012.

The IMF’s outlookThe large oriental markets will once

again play an increasing role, led by China (+9.6%) and India (+8.2%). The GDP of the United States should rise by 2.8%, in the euro zone by 1.6% (only +1.1% in Italy). Among the emerging countries, the forecast is +4.5% for Brazil and +4.8% for Russia. The prospect of a generalized upturn for the period 2011-2014 is confirmed but the recovery will still, however, be slow in western countries, and particu-

larly in Europe. The macro-economic scenario also contains several elements of risk, such as the repercussions of the natu-ral disasters in Japan at the beginning of March, the impact of political ten-sions in North Africa on oil and energy prices, the return of inflationary trends due to the rising costs of raw materials and the high debt in many countries, especially in the US and euro areas.

Outlook for 2011

38

A year of growth Despite the general situation, Comer Industries’ outlook for development is very positive: the signs for 2011 show a significant recovery of the company’s reference sectors. Total turnover will grow substantially in 2011, with an expected return to the levels of 2008, before the crisis began. Notwithstanding the climate of uncertainty involving a rebound in

demand as a result of the inventory build-up and a rise in commodity prices, a significant volumes expan-sion is foreseen in both the European and North American markets, in the agricultural and industrial segments. For the Chinese area, 2011 should be a year of consolidation for Comer Industries, with a reduced margin-ality due to tougher competition on prices characterizing the wind

power sector, the company’s main business area in the Far East.

The industrial plan For 2011, Comer Industries an-nounced the reorganization plan of manufacturing activities (see p. 28): the first measures involve the exten-sion of the Matera plant, the consol-idation of production units for indus-trial application drives and of rigid and steering axles into the Cavriago facility and, at the end of the year, the expansion of the Reggiolo plant in Via Fermi.These investments, which will af-fect all Operating Units in the period 2011-2014, are aimed at containing costs and optimizing synergies be-tween different company divisions, to respond more effectively to the global customers’ demands and to gain competitiveness on the mar-kets. The new plan provides for the imple-mentation of the Comer Production System throughout the organiza-tion, in the factories as well as in the offices. The CPS method will be applied to the new product develop-ment process and gradually also to the supply chain (see pages 24-25).

New drivers for development 2011 is expected to generate new growth opportunities for Comer Industries, both in the production area, with transmissions for electric applications in the automotive sec-tor (see p. 16), and in the sales area, with a focus on emerging markets, such as Brazil, Russia and India (see p. 32).The company intends to reinforce its commitment to sustainabil-ity expanding standard ISO 14001 to all Operating Units and foreign Subsidiaries, and to safety, with the Safety for Us project in every fac-tory after the positive results ob-tained in 2010 with Driveshafts and Gearboxes (see p. 37).

Despite the general situation, Comer Industries’ outlook for development is very positive. Total turnover will grow substantially in 2011, with a significant volumes expansion in both the European and North American markets, in the agricultural and industrial segments.

39

1985Four foreign subsidiaries are set up to market products in France, Germany, Great Britain and the United States.

1998Opening of the representative office in Beijing for the industrial partner-ship with local suppliers: the first step of the company’s development in China.

1985-1990Comer grows both organically and through acquisitions, thanks to which the strategic diversification of the product range is implement-ed. The industrial line is introduced. Custom-designed solutions for the major customers are offered along-side standard products.

1970The Storchi family founds CO.ME.R. - Costruzioni Meccaniche Riduttori - specialized in the manufacture of mechanical transmissions for agri-cultural machinery.

Our first 40 years

1996Opening of the Mechatronics Research Center, a state-of-the-art laboratory dedicated to the company’s R&D activities. First mechatronic systems.

40

1999Creation of Comer Group: thebrand identifies all the Groupcompanies and Operating Units.

2010Comer Industries celebrates its first 40 years of activity: a long story of growth and innovation, a great industrial adventure, with solid foundations to continue on its path of development.

2009Implementation of the Comer Production System (CPS), the new organizational philosophy based on the Kaizen method for continuous product and service improvement.

2007The Comer Industries Components Operating Unit is officially inaugu-rated in Matera. Comer (Shanghai) Trading Co. Ltd., the new sales Subsidiary, and the Operating Unit Comer Industries (Shaoxing) Co. Ltd. are also opened in China.

2002Comer Group becomes Comer Industries, changing from a group of companies into a single large en-terprise, global leader in the design and production of advanced engi-neering systems and mechatronic solutions.

2008Establishment of Comer Academy, the internal training and management school focused on organizational and cultural change in the company.

41

Extract from the report on operations accompanying the consolidated financial statements at December 31, 2010

42

The figures presented here have been extracted from the report on operations accompanying the 2010 consolidated financial statements of Comer Industries Spa, approved on April 29, 2011 by the Shareholders’ Meeting.For more complete information, please see the full version duly filed at the Milan Chamber of Commerce.

43

Income statement overview

44

Revenues from sales and servicesThe sales figure slightly exceeded 276,500 thousand euros, with a net growth from 2009 of more than 35,000 thousand euros, or +14.59%. Once again this economic indicator was affected by the relationships among currencies, as the US dollar gained 5.2% in average value on the euro, while the Chinese yuan gained approximately 6.2%. Therefore, the net result of these dyna-mics generated a positive effect on the consolidated sales figures, compared to 2009, at approximately 4,900 thousand euros, offsetting a 3,900 thousand euros deconsolidation due to the sale of the Fluid Power Operating Unit at the end of last year. Overall we can observe a general reprise in our reference markets. Specifically, we registered significant performances in the industrial sector, particularly in the segments for compact construction and road machinery. As regards renewable energies, revenues from our wind generator applications increased further – thanks to the brilliant results achieved on the Chinese market. The agricultural application market also delivered more reassuring signs of recovery, driven by a widespread increase in demand, a consequence of the general growth in the prices of agricultural commodities, also linked to contingent factors in the second half of 2010.

Operating result (EBIT)The final absolute result was close to 19,500 thousand euros, with a 7.04% profitability on turnover; this represented a peak of excellence for the Group even compared to the recent pre recession past, as in 2008 this figure was 6.88%.Simplification and rationalization of Comer Industries organization started in 2009, a favourable monetary scenario (with the US dollar and Chinese yuan gaining on the euro), plus early relevant sign of saving and production efficiencies from the new CPS, are the key elements justifying these results, together with a physiological decrease in amortisation and depreciation as a tangible consequence of a reflective spell in production investments. The picture is completed by the internationalisation of certain critical production processes, as a direct consequence of investments mainly carried out between 2007 and 2008 and proximity in logistic and production aspects to a few key clients in the Chinese region.

Interest expense and other net financial chargesThe effect of net financial charges on turnover decreased from 0.87% in 2009 to 0.28% in 2010, so that the “interest co-verage ratio” operational index, as calculated on the EBITDA index, is a non-significant 35.39 times over positive. On the other hand, we should highlight that the EBITDA/net financial debt ratio is getting very close to 1. The financial operation results at -1,305 thousand euros compared to 2009, albeit apparently extraordinary, were expected and actually forecast since the early review of the operating budget, as a consequence of a decrease in the 3-month Euribor rate from a 1.2185% average in 2009 to a 0.815% average on 2010, amplified by an average approximately decrease by 50% of the Group’s debt as a further confirmation of the one-off year-end result of -42.16%.

Foreign exchange gains and lossesHere we have a negative result in absolute value of approximately 1,600 thousand euros (in 2009 Comer Industries registered a negative result of approximately 1,400 thousand euros), partly as a consequence of a constant gain of all major currencies on the euro that generated a 2,700 thousand euros loss to the parent company in coverage operations; these were only partially recove-red through a 1,100 thousand euros profit from foreign branches, in particular from transactions towards the Chinese currency. For coverage policies and exchange risk analysis, please refer to the corresponding section in the notes to the financial statements.

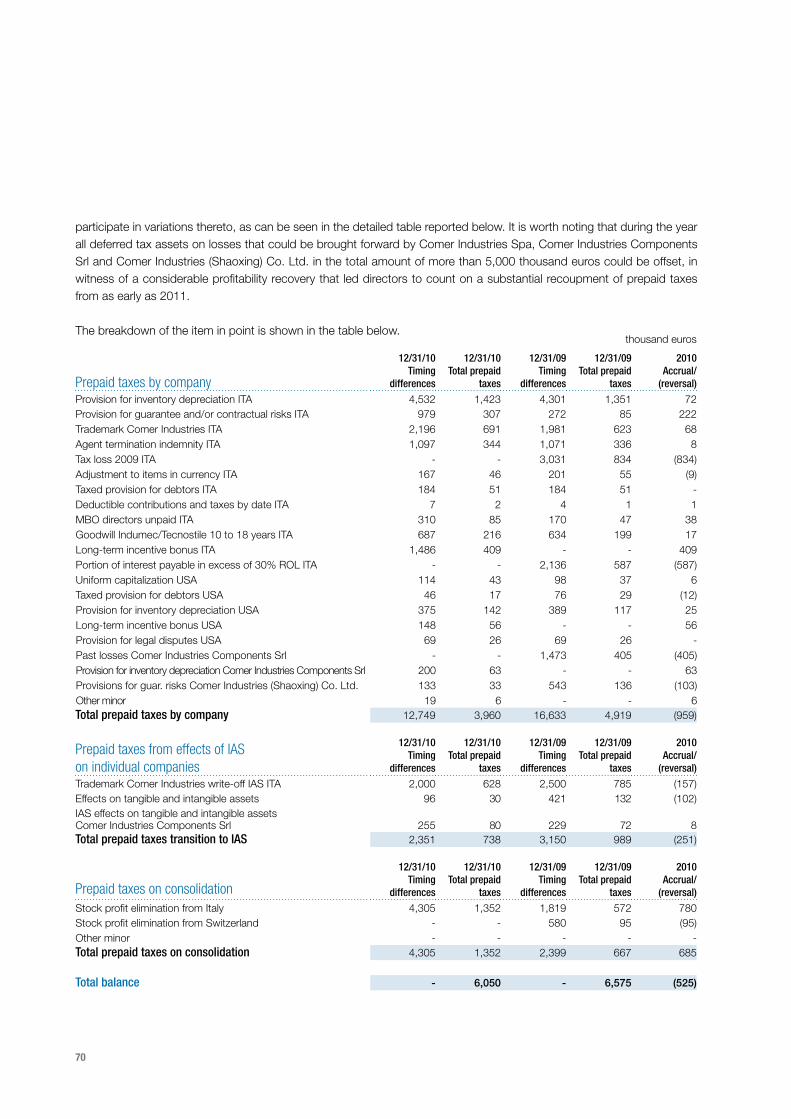

TaxationThis entry includes current income taxes of 5,875 thousand euros (3,111 thousand euros in 2009) and deferred tax costs of 622 thousand euros (compared to 1,823 thousand euros profit in the previous year). In 2009 the overall tax burden was an exceptional 50.16% due to dividend repatriation expenses and the Italian IRAP cost which, being non-proportional to the income, affected the gross operating margin gross of a relevant portion of the working cost that generated it. On the other hand, higher intermediated volumes in 2010 mitigated such distortion effects (particularly IRAP), thus improving the ratio to an adequate 37.80%, more consistent to the Group’s previous historic readings.

thousand euros

Actual IAS12/31/10

Actual IAS12/31/09

A) Revenues from sales and services 276,534 241,328

Other income and revenues 2,451 3,167

Changes in inventories 4,813 (37,520)

B) Ordinary production value 283,798 206,975

Material consumption/purchase costs (171,665) (115,018)

Service supply expenses (25,852) (23,612)

Other operating expenses (302) (385)

C) Added value 85,979 67,960

Labour cost (including effects IAS 19) (53,381) (48,443)

D) Gross operating margin 32,598 19,517

Amortization and depreciation (8,352) (8,796)

Other correction allocations (1,359) (900)

Third-party asset fruition fees (3,421) (3,687)

E) Operating result 19,466 6,134

Interest expense and other net financial charges (786) (2,091)

Foreign exchange gains/(losses) (1,618) (1,422)

Financial assets/liabilities fair values 125 (53)

F) Result before extraordinary entries and taxes 17,187 2,568

Income/(charges) from disposals - -

G) Profit before taxes 17,187 2,568

Income taxes (6,497) (1,288)

H) Result for the year 10,690 1,280

Third-party profit/(loss) - -

I) Parent company profit for the year 10,690 1,280

Consolidated income statement of production realized

45

Financial overview

«Profits are an opinion, cash is a fact».The quote, cited for the first time in 1986 in Alfred Rappaport’s work “Creating Shareholder Value”, is today still considered a landmark in the field of corporate management.The importance of controlling cash flow is now more essential than ever, also with regards to the calculation of the value of an enterprise for which, besides the criteria founded on the application of market multiples, the only credible algorithm is Discounted Cash Flow (DCF), based on the ability to generate liquidity in future periods. With the introduction of the Basle 2 criteria on the part of the banks, the focus on the possibility for a company to repay its debts in short time has become even greater. Today, the aforementioned affirmation is much more pertinent and important considering the increasingly reduced resources made available by the credit system. The global competitive scenario, still facing financial difficulties, is seeing the costs for raising money exacerbated and inflex-ible due to the continuous declassification of sovereign debts. In this context, Comer Industries has organized all its cash management activities in an effective manner, handling liquidity and cash collection successfully to minimize funding costs and to maximize the generation of free cash flow.With the collaboration of a few number of banking institutes, Comer Industries has been able to guarantee correct credit development, while continuing to maintain its economic-financial balance, appropriate equity index and a solid credit rating.The company’s treasury management has secured elasticity in the supply of funds (maintaining revolving, stand-by, im-mediately available and flexible credit lines) and, at the same time, efficiency in terms of the conditions applied, the use of different types of sources of funds and the rational use of overall supplies. The current financial debt structure is balanced between short-term credit lines (necessary to finance working capital) and long/medium-term credit lines (to cover non-current asset investments). For the issue of two new unsecured long/medium-term loans, made in the second half-year for a total of 6 million euros, Comer Industries Spa has not entered into any financial covenants in order to back them. Reference should be made, on the other hand, to the specific chapter of the notes to the accounts for more details regarding covenants in force on previously issued loans. In any case, is should be noted that as at December 31, 2010 all financial covenants had been fully complied with.The loan issued to the American subsidiary, Comer Industries Inc., by the Fifth Third Bank, guaranteed by financial cov-enants, is still in force for a residual amount. New lines of credit were opened in China to support the financial requirements of the Comer Industries (Shaoxing) Co. Ltd. Operating Unit.The prudent management of liquidity risk has required the maintenance of suitable bank credit lines, which at December 31, 2010 were still on the increase, despite the credit crisis, rising to 147,600 thousand euros compared to 139,400 thousand euros in the previous year, with an average use during the year of 35%.At December 31, 2010 the ratio between the net financial position and equity had clearly improved (+51%) compared to the previous year, with a gearing ratio of 0.35. Likewise, the ratio between the net financial position and EBITDA fell to parity for the first time in Comer Industries’ history, against 3.23 of the previous year.The net passive financial position dropped from 48,187 thousand euros at December 31, 2009 to 27,870 thousand euros at December 31, 2010.The continuous decrease in the company’s financial debt is mainly due to the improved result for the year, alongside a situ-ation of substantial balance between net flows of working capital and disbursements for investments.

46

The most significant balance sheet headings are referred to below:

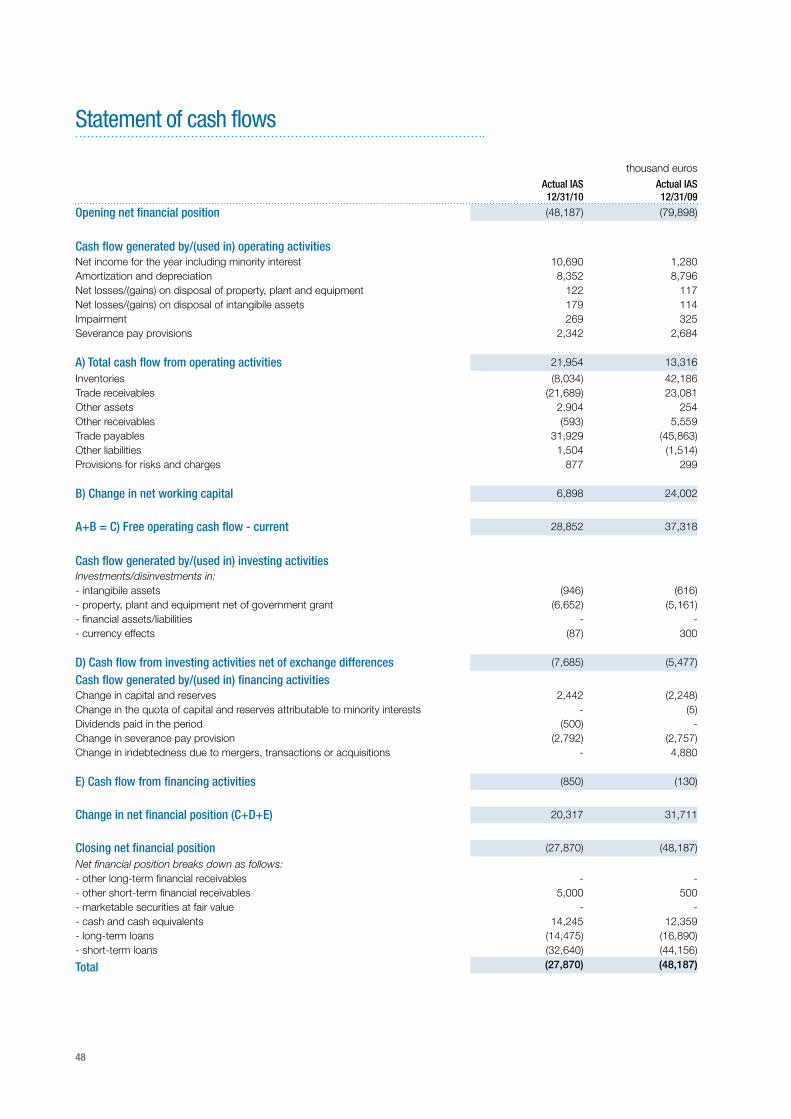

Despite a significant rise in sales, Comer Industries has limited the increase in net working capital, generating a free cash flow a little under that generated in 2009, a year in which the considerable decrease in sales volumes led to a big reduction in working capital.In 2010, together with an operating working capital cash flow (self-financing cash flow) of 21,954 thousand euros, growing sharply compared to the previous year, there was a positive current operating free cash flow of 28,852 thousand euros, arising after changes in working capital.The combined effects of changes in inventories, in receivables, in expenditure for investments, in sales payables and in financial-equity management have generated a positive modification of the net financial position, resulting in a further de-crease in bank debt of 20,317 thousand euros, over 40% more than in the previous year. The positive trend of this indicator, which has fallen by more than 80% from 2009 to today, is therefore confirmed.

The Group’s debt at the end of 2010 breaks down as follows:thousand euros

Short-term for 13,395

Net short-term bank loans 13,395

Medium/long-term for 14,475

Medium/long-term bank loans 12,409

Medium/long-term bonds 2,066

thousand euros

Cash flow generated/(used)Inventories (8,034)

Trade receivables (21,689)

Other receivables/payables 4,667

Trade payables 31,929

Investments (7,685)

47

Statement of cash flows

thousand euros

Actual IAS12/31/10

Actual IAS12/31/09

Opening net financial position (48,187) (79,898)

Cash flow generated by/(used in) operating activitiesNet income for the year including minority interest 10,690 1,280Amortization and depreciation 8,352 8,796Net losses/(gains) on disposal of property, plant and equipment 122 117Net losses/(gains) on disposal of intangibile assets 179 114Impairment 269 325Severance pay provisions 2,342 2,684

A) Total cash flow from operating activities 21,954 13,316

Inventories (8,034) 42,186Trade receivables (21,689) 23,081Other assets 2,904 254Other receivables (593) 5,559Trade payables 31,929 (45,863)Other liabilities 1,504 (1,514)Provisions for risks and charges 877 299

B) Change in net working capital 6,898 24,002

A+B = C) Free operating cash flow - current 28,852 37,318

Cash flow generated by/(used in) investing activitiesInvestments/disinvestments in:- intangibile assets (946) (616)- property, plant and equipment net of government grant (6,652) (5,161)- financial assets/liabilities - -- currency effects (87) 300

D) Cash flow from investing activities net of exchange differences (7,685) (5,477)

Cash flow generated by/(used in) financing activitiesChange in capital and reserves 2,442 (2,248)Change in the quota of capital and reserves attributable to minority interests - (5)Dividends paid in the period (500) -Change in severance pay provision (2,792) (2,757)Change in indebtedness due to mergers, transactions or acquisitions - 4,880

E) Cash flow from financing activities (850) (130)

Change in net financial position (C+D+E) 20,317 31,711

Closing net financial position (27,870) (48,187)

Net financial position breaks down as follows:- other long-term financial receivables - -- other short-term financial receivables 5,000 500- marketable securities at fair value - -- cash and cash equivalents 14,245 12,359- long-term loans (14,475) (16,890)- short-term loans (32,640) (44,156)

Total (27,870) (48,187)

48

Balance sheet overview

Tangible and intangible fixed assetsInvestments in tangible and intangible fixed assets totalled approximately 7,590 thousand euros, meaning 2.75% of turnover, obviously inconsistent with later trends and historic readings that fixed such value around 5%, yet representing a sign of prudence towards the extraordinary difficulties we experimented during 2009, partly mitigated by encouraging signs of recovery in 2010, as we already remarked when analysing the Group’s sales figures. Investments were actually operated in an ordinary way, together with narrowly focussed (high added value and return rate) industrial projects and the launch of new strategic products for the company.Concerning industrial projects, we would like to remark: - completion of gear cutting and grinding lines (with robotic loading/unloading station) in Matera and Moglia plants; - new metallography lab, to be completed, and flushing system for wind turbine transmissions in China; - innovative equipment supporting Kaizen workshops serving CPS.

On the other hand, in equipment and test benches serving new products, we should highlight the 128 axle series and new mechanical drive for electric city cars.In addition, the Group expended approximately 500 thousand euros to update ICT structures, servers and licences in order to migrate SAP systems onto a new technological platform that allows virtualisation.Current assets as at December 31, 2010 were substantially reduced to 3,300 thousand euros compared to the previous year, in accordance to commissioning plans for new gear cutters and grinders.