46

Competitive Analysis Between Islamic Banking & Conventional Banking

Competitive Analysis Between

Islamic Banking &

Conventional Banking

Page 1 of 45

20th August 2015 S.M. Arifuzzaman Asst. Professor BRAC Business School BRAC University Subject: Submission of internship report Dear Sir This is my pleasure to submit my internship report on “Future Leader of Banking Sector In Bangladesh, A Study on Islamic Banking @ IBBL”. It was a great opportunity for me to acquire knowledge and experience in respect of the functions, procedures and operational activity, other than my topic of study. I would like to take this opportunity to thank you for the guidance and support you have provided me during the course of this report. Without your help, this report would have been impossible to complete. With deep gratitude, I also acknowledge the help provided by Md. Tanjelur Rahman, Senior Officer, Islami Bank Bangladesh Ltd. for providing me utmost supervision during my internship in the organization. I have concentrated my best efforts to achieve the objectives of the assignment study and hope my endeavor will serve the purpose. However, I will always be ready to provide any further clarification that you may require. To prepare the report I have collected what I believe to be most relevant information to make my report as analytical and reliable as possible.

Thank you again for your support and patience. Yours Sincerely Hasan Ashif ID- 12264069 MBA Program, BRAC Business School BRAC University

Page 2 of 45

Acknowledgement

First of all, I would like to thank our honorable academic supervisor S.M. Arifuzzaman, Asst. Professor, BRAC Business School, BRAC University for his continuous support and supervisions, suggestions.

Then, I express my sincere gratitude to Md. Nizamul Hoque (Senior Vice President & Head of Branch), Md. Ibrahim Bhuiyan (Vice President & Manager Operations) in IBBL Narayangonj Branch & Md. Tanjelur Rahman, Senior officer for supervising me the entire internship time. I would like to also express my gratitude to Mohammad Aminul Ehshan Bhuiyan (Senior Officer) for teaching me and supporting me for my internship experience. And a special thanks to Md. Aiebur Rahman, Project Office (RDS), Mohammad Abdur Rahman (Principle officer), Lautfar Rahman, Md. Salauddin, Md Aminul Islam, Nasiruddin, Bashar, Anower Hossain, Mohammad Ali & Hasan for their valuable advice and information. Besides I am also grateful to the authors, researchers and articles writer whose Books, Reports, Thesis papers and journals that have helped me to prepare my internship report successfully. Finally my sincere gratitude goes to my family, friend’s classmates and colleagues who helped me whenever I needed.

Page 3 of 45

Table of Contents

Abbreviations 5

Executive Summary 6

Chapter 1 Introduction

1.1 Introduction 7

1.2 Objectives 7

1.3 Scope of Study 8

1.4 Methodology 9

1.5 Limitation 9

Chapter 2 Concept of Islamic Banking

2.1 Definition of Islamic Banking 11

2.2 Historical Background of Islamic Banking 12-13

2.3 Islamic Banking & Bangladesh 14

2.3.1 Islamic Banking: Bangladesh Scenario 14

2.3.2 Development of Islamic Banking: Network 15

2.3.3 Development of Islamic Banking: Deposit & Investment 15

2.3.4 Development of Islamic Banking: Assets 16

2.3.5 Selected Ratios of Islamic Banks and the Banking Sector 16

2.3.6 Summary of Islamic Banking: Bangladesh Scenario 17

2.4 Islamic Banking Regulation 17

Chapter 3 Islami Bank Bangladesh Limited (IBBL)

3.1 Background 19-20

3.2 Overview of Islami Bank Bangladesh Limited 1. IBBL’s Vision 21

2. Mission of IBBL 22

3. Strategic Objectives of IBBL 22

4. Core Value 23

5. Commitment 23

Page 4 of 45

3.3 Nature of Business 23

3.4 Functions of IBBL 24

3.5 Branches of IBBL 24

3.6 Capital Structure 24

3.7 Management Structure of IBBL 25

Chapter 4 Overall Performance of IBBL

4.1 The Corporate Information of IBBL 27

4.2 Performance Analysis 28

4.3 Contribution to Economy: IBBL Prospective 29

Chapter 5 what sets IBBL apart?

5.1 Differences between Islamic Banking & Conventional Banking 31-32

5.2 Superiority of Islamic Banking 33-35

5.3 Islamic Principles of Deposit Mobilization 36

5.4 Investment Mechanism of IBBL 37-38

5.5 Profit Distribution Policy

5.5.1 Principle of profit Distribution to Mudaraba depositors 39

5.5.2 What is weightage? 39

5.5.3 Factor considering for Fixing up of weightage 39

5.5.4 Weightage of various Mudaraba Deposits 40

5.5.5 Profit calculation with an example 41

Findings 42

Recommendation 43

Conclusion 44

References 45

Page 5 of 45

List of Abbreviations

IBBL Islami Bank Bangladesh Limited RDS Rural Development Scheme ATM Automated Teller Machines EMI Equal Monthly Installment CIB Credit Information Bureau CRO Customer Relationship Officer GDP Gross Domestic Product AAOIFI Accounting and Auditing Organization

for Islamic Financial Institutions.

IFSB Islamic Financial Service Board IAIB International Association of Islamic Banks

OIC Organization of Islamic Conference MOU Memorandum of Understanding PPG Product Program Guide ROA Return on Asset IIFM Islamic Interbank Fund Market ISRB Islamic Economic Research Bureau BIBA Bangladesh Islamic Bankers Association

IBCF Islamic Banks Consultative Forum BB Bangladesh Bank IDB Islamic Development Bank

Page 6 of 45

Executive Summary

This report is titled as “Comparative Analysis between Islamic Banking & Conventional Banking” is submitted as a partial requirement for the fulfillment of MBA Program. This report is prepared based on analyzing the Functions like routine activities and administrative work, the training and development program of IBTRA & the practical experiences appraised from the employees of IBBL. I have tried my best to provide the best accurate and true information regarding the report and its relevant information’s without which the report is not considered to be completed. The report is basically divided into several parts based on report criteria. The Different parts of the report are Objective, scope and limitations of the study, organization overview, findings and analysis of the Functions, Recommendations and conclusion. Which is chronologically organized and can easily understandable?

Page 7 of 45

Chapter 1 1.1 Introduction Islamic Banking is shariah complainant financing. More than 500 institutions are functioning in 65 countries. The Quantum of Islamic Finance is $2.0 trillion (assets) which is expected to touch $5.0 trillion mark by 2019. It has a growth rate of 18% with more than 38 million clients; which is expected to grow rapidly in coming years. More than 120 Institutions & 50 Universities around the world are offering degree programs specializing on Islamic Finance and Banking Education. 1.2 Objective The prime objective of the study is to fulfill the course requirement and to know about banking functions like General Banking, Investment & Foreign Exchange. This report seeks to explore the reasons behind the success of Islamic Banks in the recent past, what are the reasons behind the 17 more banks in the pipe line for conversion. To explore the reasons I have selected IBBL (the only bank in Bangladesh to secure its spot to the top 1000 global banks) to know how Islamic Banks run interest free banking system, what are the difference between profit and interest, how Islamic banks invest & earn profits. Secondary Objective:

Reasons behind the success of Islamic Banks. What is Interest free banking system, Is it possible? Difference between profit & loss? How Islamic Banks Invests and earn profit. To know about the management system of Islamic Bank. What is the reason behind their huge customer base without having a marketing

department?

Page 8 of 45

1.3 Scope of Study Learning knowledge becomes worthy and useful when it is implemented in the practical field. That is why learned people say, “Theoretical knowledge tests its perfection with application” or “Theoretical education must be backed by real life practice”. The importance of practical knowledge along with academic education is increasing day by day. For this the report has been introduced as an integral part of MBA degree. We are very much delighted to have the opportunity to prepare this report. The collected data and information has been tabulated, processed and analyzed carefully and report has been prepared on the basis of Practical experiences during the internship period in IBBL branches. This shorted duration is not adequate for experiment research world. The study would have been more informative and determined, if adequate time could have been utilized. However it is felt that the findings represented a partial view of Islami Bank Bangladesh Limited of it’s in house activities & functions.

Page 9 of 45

1.4 Methodology The methodology of this report is totally different from conventional reports. We have emphasized on the practical observation. Almost the entire report consists of our practical observation. While preparing the report, I have collected information from the following sources: Two sources of data and information have been used widely: Primary sources of data:

❑ Face to face conversation with the official of IBBL ❑ Practical deskwork.

Secondary sources of data:

❑ Website of Bangladesh Bank, IBBL, IBTRA and other essential websites. ❑ Text Book- Guidelines about Islamic Economics, Banking &Finance ❑ Library Study ❑ Newspaper Articles

.

1.5 Limitation of Our Study This Research Project work was prepared carefully with full concentration to avoid any kind of misinformation or mistakes. But still like all other research work this report may also have some limitations. From our view some obstacles in this report are given bellow:

Primary and Secondary data were not available in organized form. This report was prepared in very tight time schedule. Lack of opportunity to access to internal data Legal action related information was not available.

Page 10 of 45

Page 11 of 45

Chapter 2 Concept of Islamic Banking

2.1 Definition of Islamic Bank Islamic Banking means Shariah Compliant Finance. We know finance is the flow of fund from surplus unit and subsequently transfer the same to the deficit unit. Here Sharia Compliant states the guidelines. Shariah is the set of rules derived from both the Holy Quran and the authentic traditions (Sunnah) of the Prophet (peace be upon him) and the scholarly opinions (ljtehad) based on Quran and Sunnah” – IDB The legal system developed and established by the close associates of the prophet (PBUH) and the scholars and jurists through ages, in the light of teachings of the holy Quran and Sunnah and on the basis of their own ljma and Qiyas is known as Shariah According to Imam Ghazali, “The very objective of the shariah is to promote the well-being of the people, helping in every welfare and preventing from harm.” Yousuf Al Karzavi “The instinctive/ inherent goal/Maqasid/ objective of shariah is to ensure the welfare and prevention of ill-being/ evil.” Islamic banking is the financing activities which will try to ensure the welfare of people and at the same time it will try to prevent and eliminate the ill- being / evil practices. What is Islamic Bank? “Islamic Bank is a financial institution whose statutes, rules and procedures expressly state its commitment to the principles of Islamic Shariah and to the banning of the receipt and payment of interest on any of its operations.” – The general Secretariat of the Organization of the OIC OIC’s definition consists of two approaches –

1. Commitment to the principles of Islamic Shariah (Maqasid/ Objective) 2. Banning of receipt & payment of interest (Mechanism)

Page 12 of 45

2.2 Historical Background of Islamic Banking

Islamic banking came from the concept of – “Ownership of Allah (SWT) where Man is trustee (khalifah)” The development movement of Islamic Banking can be looked at into 4(four) stages period.

1) The First Stage (1950-1969)

i. The first attempt to establish Islamic Financial Institution took place in Pakistan in the late 1950.

ii. 1962 | Pilgrims Savings Corporation, Malaysia.

iii. 1963 | Savings Bank in Mitgamar, Egypt by Ahmad al Najjar, The pioneer in Islamic Banking.

iv. 1969 | Tabung Haji, Malaysia

2) The second Stage (1970-1979)

i. 1970 | Foreign Ministers of OIC countries agree to establish Islamic Banks in the Muslim Countries.

ii. 1973 | Finance Ministers of OIC countries decided to form an international Islamic Bank.

iii. 1974 | Finance Ministers of OIC countries signed a charter to establish Islamic Development Bank.

iv. 1975 | Islamic Development Bank, Jeddah

v. 1975 | Dubai Islami Bank

vi. 1977 | Faisal Islamic Bank, Sudan; Kuwait Finance House

vii. 1978 | Jordan Islamic Bank for Finance & Investment

viii. 1978 | The House Building Corporation of Pakistan; National Investment Trust; Mutual Trust Funds of Investment Corporation of Pakistan.

Page 13 of 45

3) The third stage (1980- 1989)

1980 | Bangladesh Bank sent a representative to study the operation of several Islamic banks abroad. Bangladesh foreign minister proposed in 11th OIC meeting to establish Islamic common market and banking

1981 | The president while addressing the 3rd Islamic Summit Conference held at Makkah suggested: “The Islamic Countries should develop a separate banking system to facilitate trade and commerce.”

4) The fourth stage (1990 onwards)

The fourth stage where we are now and witnessing the stage of consolidation and strengthening its operations.

i. 1990 | the agreement of association signed in Algiers for the establishment of AAOIFI (Accounting and Auditing Organization for Islamic Financial Institutions).

ii. 1991 | AAOIFI was registered in Bahrain as an International autonomous non -profit making corporate body

iii. 3rd November 2002 | The Islamic Financial Service Board (IFSB) was established

iv. IFSB Started its operation in 10th March, 2003 in Malaysia

v. Jaiz Bank Plc, the first ever non-interest (Islamic) bank in Nigeria was established in 2011 with the technical support of IBBL.

Page 14 of 45

2.3 Islamic Banking & Bangladesh

Banking plays an important role in the economy of any country. 80% of population of Bangladesh is Muslims and Bangladesh is also one of the largest Muslim countries of the world. People of Bangladesh have strong faith and belief on Allah and Prophet(SM). They like to lead their lives as per Quran and Sunnah. But there was no Islamic banking system in our country before March 13, 1983. IBBL is the first Islamic Bank in south East Asia who operates its banking activities on the basis of profit-loss sharing system. 2.3.1 Islamic Banking Bangladesh Scenario

8 Eight Full Fledged Islamic Banks IBBL (1983) ICB (1987) AIBL (1995) SIBL (1995)

Sahjalal (2001) EXIM (2004) FSIBL (2009) Union (2013)

More banks are in the pipe line of conversion

17 Banks having Islamic branches/ windows

Page 15 of 45

Other Private banks,

67%

Islamic Banks 33%

Market Share: Deposit (2014)

2.3.2 Development of Islamic Banking: Network

2.3.3 Development of Islamic Banking: Deposit & Investment

Total Deposit of Islamic Banks is TK.1,44,149 Crore. Which is equivalent to 32.78% of total Deposit of Private Commercial Banks or 20.46% of total Deposit of Banking Sector of Bangladesh.

Total Investment of Islamic Banks is TK.1,23,950 Crore.

0 1983 1987 1991 1995 1999 2003 2004 2009 2012 2013 2014

Series1 0 3 24 84 123 186 243 268 517 635 802 890

0

100

200

300

400

500

600

700

800

900

1000

Number of Islamic Banking Branches

Islamic Banks 28%

Other Private banks,

72%

Market Share: Investment (2014)

Page 16 of 45

2.3.4 Development of Islamic Banking : Assets

Asset Size doubled in last 4 years

2.3.5 Selected Ratios of Islamic Banks and the Banking Sector (2013)

Ratio Overall Banking

Sector

Islamic Banking

Sector

Return on Asset 0.90 0.89

Return of Equity 10.70 11.71

Net Profit Margin 2.10 3.32

Profit Income to Total Asset 7.74 9.79

Investment- Deposit Ratio 71.18 84.13

Capital Adequacy Ratio 11.50 12.00

Classified Investment to investment 8.90 4.20

Classified Investment to Capital 59.80 39.88

Type of Bank Amount of CSR Expenses During the year 2013

Full Fledged Islamic Bank 118

Conventional Banks 324

Total 442

0

200

400

600

800

1000

1200

1400

1600

1800

0 2009 2010 2011 2012 2013 2014

Tota

l Ass

ets

(A

mo

un

t in

Bill

ion

BD

T)

Page 17 of 45

2.3.6 Summary of Islamic Banking: Bangladesh Scenario

One fifth of country’s Banking Sector Under Islamic System

18% average asset growth in last 5 years

35% of 38 million Global Islamic Banking Clients (11.70 million)

50% of Global Islamic Micro Finance

Total Deposit of Islamic Banks is 1,44,149 crore.

32.78% of Total Deposit of Private Commercial Banks

20.46% of Total Deposit of Banking Sector of Bangladesh.

Total Investment of Islamic Banks is TK 1,23,950 Crore

32.78% of Total Investment of Private Commercial Banks

17.15% of Total Investment of Banking Sector of Bangladesh.

2.4 Islamic Banking Regulation Organizations promoting Islamic Banking

1. Islamic Economic Research Bureau (IERB) 1976 2. Bangladesh Islamic Bankers Association (BIBA) 1979 3. Islamic Banks Consultative Forum (IBCF) 1995 4. Central Shariah Board for Islamic Banks of Bangladesh (2001)

Regulatory Steps for Islamic Banking

1. Provision made in Bank Company Act 1995 2. Bangladesh Government Islamic Investment Bond 2004 3. Guidelines for Islamic Banking 2009 4. Islamic Interbank Fund Market – IIFM 2012 5. Separate inspection department for Islamic Banks 2013 6. Refinance Facilities to Islamic Banks for SME 2013 7. IFSB-BB seminar on Islamic Finance 2013 8. Meeting of Islamic banks with parliamentary standing committee 9. Meeting of Islamic bankers with BB Governor

Page 18 of 45

Page 19 of 45

Chapter 3 Islami Bank Bangladesh Limited (IBBL)

3.1 Background

In August 1974, Bangladesh signed the Charter of Islamic Development Bank and committed

itself to reorganize its economic and financial system as per Islamic Shariah.

In January 1981, Late President Ziaur Rahman while addressing the 3rd Islamic Summit

Conference held at Makkah and Taif suggested, ''The Islamic countries should develop a

separate banking system of their own in order to facilitate their trade and commerce.''

This statement of Late President Ziaur Rahman indicated favorable attitude of the

Government of the People's Republic of Bangladesh towards establishing Islamic banks and

financial institutions in the country. Earlier in November 1980, Bangladesh Bank, the

country's Central Bank, sent a representative to study the working of several Islamic banks

abroad.

In November 1982, a delegation of IDB visited Bangladesh and showed keen interest to

participate in establishing a joint venture Islamic bank in the private sector. They found a lot

of work had already been done and Islamic banking was in a ready form for immediate

introduction. Two professional bodies -Islamic Economics Research Bureau (IERB) and

Bangladesh Islamic Bankers' Association (BIBA) made significant contributions towards

introduction of Islamic banking in the country. They came forward to provide training on

Islamic banking to top bankers and economists to fill-up the vacuum of leadership for the

future Islamic banks in Bangladesh. They also held seminars, symposia and workshops on

Islamic economics and banking throughout the country to mobilize public opinion in favor of

Islamic banking.

Page 20 of 45

Their professional activities were reinforced by a number of Muslim entrepreneurs working

under the aegis of the then Muslim Businessmen Society (now reorganized as Industrialist &

Businessmen Association). The body concentrated mainly in mobilizing equity capital for the

emerging Islamic bank.

At last, the long drawn struggle to establish an Islamic bank in Bangladesh became a reality

and Islami Bank Bangladesh Limited was established in March 1983 in which 19

Bangladeshi national, 4 Bangladeshi institutions and 11 banks, financial institutions and

government bodies of the Middle East and Europe Including IDB and two eminent

personalities of the Kingdom of Saudi Arabia joined hands to make the dream a reality.

Islami Bank Bangladesh Limited (IBBL) is considered to be the first interest free bank in

Southeast Asia. It was incorporated on 13-03-1983 as a Public Company with limited

liability under the companies Act 1913. The bank began operations on March 30, 1983.

The establishment of Islami Bank Bangladesh Limited was on March 13, 1983 as the true

reflection of this inner urge of people, which started functioning with effect from March 30,

1983. This Bank is the first of its kind in Southeast Asia. It is committed to conduct all

banking and investment activities on the basis of interest-free profit-loss sharing system. In

doing so, it has unveiled a new horizon and ushered in a new silver lining of hope towards

materializing a long cherished dream of the people of Bangladesh for doing their banking

transactions in line with what is prescribed by Islam. With the active co-operation and

participation of Islamic Development Bank (IDB) and some other Islamic banks, financial

institutions, government bodies and eminent personalities of the Middle East and the Gulf

countries, Islami Bank Bangladesh Limited has by now earned the unique position of a

leading private commercial bank in Bangladesh.

Page 21 of 45

3.2 Overview of IBBL

Islami Bank Bangladesh Limited is a well-known organization which is reflecting the mass banking example in Bangladesh. With highly reputed knowledge and concern in banking sector, Islami bank is doing its tremendous business expansion with outstanding performance in deposit and remittance. Bangladesh is a mass populated country where poverty level is highly significant with a developing sign in economic. Although there are lots of banks in Bangladesh to invest to earn and finally to serve customers the people of Bangladesh but the efficiency in serving the mass poor population is not significant toward development. In this case, Islami Bank Bangladesh Ltd. is quite different with tagging massage AMAR BANK. This specific tag shows the real concinnity toward mass population who are not only poor but also doing their best to develop their life with country prosperity. Another targeting issue is the majority of Muslim. Most people in Bangladesh are the follower of Islam. Overall mass population is pious toward their religious activity. Islami bank has targeted their values and views according to Islami Shariah which represent the Islami process to continue the business terms. That’s another secret view behind the success of Islami Bank Bangladesh Ltd. Not only the Muslims but also people from other religion have chosen IBBL as their preference. 3.2.1 IBBL’s Vision The vision of IBBL is to always strive to achieve superior financial performance, be

considered a leading Islamic Bank by reputation and performance.

Our goal is to establish and maintain the modern banking techniques, to ensure

soundness and development of the financial system based on Islamic principles and to

become the strong and efficient organization with highly motivated professional,

working for the benefit of people, based upon accountability, transparency and

integrity in order to ensure stability of financial systems

We will try to encourage savings in the form of direct investment

We will also try to encourage investment particularly in projects which are more

likely to lead to higher employment.

Page 22 of 45

3.2.2 Mission of IBBL

To established Islamic Banking through the introduction of welfare oriented banking system and also ensure equity and justice in the field of all economic activities.

Achieve balanced growth and equitable development through diversified investment

operations particularly in the priority sectors and less development areas of the county.

To encourage socio-economic development and financial services to the low income

community particularly in the rural areas. 3.2.3 Strategic Objectives

To ensure customers' satisfaction. To ensure welfare oriented banking. To establish a set of managerial succession and adopting technological changes to

ensure successful development of an Islamic Bank as a stable financial institution. To prioritize the clients welfare. To emerge as a healthier & stronger bank at the top of the banking sector and continue

stable positions in ratings, based on the volume of quality assets. To ensure diversification by Sector, Size, Economic purpose & geographical location

wise Investment and expansion need based Retail and SME/Women entrepreneur financing.

To invest in the thrust and priority sectors of the economy. To strive hard to become a employer of choice and nurturing & developing talent in a

performance-driven culture. To pay more importance in human resources as well as financial capital. To ensure lucrative career path, attractive facilities and excellent working

environment. To ensure zero tolerance on negligence in compliance issues both sharia’h and

regulatory issues. To train & develop human resources continuously & provide adequate logistics to

satisfy customers’ need. To be excellent in serving the cause of least developed community and area. To motivate team members to take the ownership of every job. To ensure development of devoted and satisfied human resources. To encourage sound and pro-active future generation. To achieve global standard. To strengthen corporate culture. To ensure Corporate Social Responsibilities (CSR) through all activities. To promote using solar energy and green banking culture and echo logical balancing.

Page 23 of 45

3.2.4 Core Values

Trust in Almighty Allah Strict observance of Islamic Shariah Highest standard of Honesty, Integrity & Morale Welfare Banking Equity and Justice Environmental Consciousness Personalized Service Adoption of Changed Technology Proper Delegation, Transparency & Accountability

3.2.5 Commitments

To Shariah To the Regulators To the Shareholders To the Community To the Customers To the Employees To other stakeholders To Environment

3.3 Nature of Business

The Islami Bank Bangladesh Limited is pioneer in introducing Shariah based interest free

utilize banking in Bangladesh with a mission to establish welfare oriented banking system

and to ensure equity and justice in the field of all economic activities. All of its activities are

directed on the principles of Islamic Shariah. There is Shariah council, which is entrusted

with the responsibility for ensuring that the activities of the bank are being conducted on the

precepts of Islam. IBBL is one of the leading first generation private sector banks in

Bangladesh, which provides all kinds of commercial banking service.

Page 24 of 45

3.4 Functions of IBBL

Islamic banks render almost similar services to their customers conventional banks do.

However, differences exist in administering incentives for deposits and charging for capital

investments, in so far as techniques of calculating the incentive or the cost of the capital are

concerned. Like a conventional bank, the Islami bank also accepts deposits from customers

and advances loans. The bank invests its funds for short as well as long term deposits. The

Islami bank also acts as a custodian of its customers and performs all foreign transactions on

behalf of them. The functions of Islami Bank Bangladesh Limited are as under:

To maintain all types of deposit accounts.

To make investment.

To conduct foreign exchange business.

To extend other banking services.

To conduct social welfare activities through Islami Bank Foundation.

3.5 Branches of IBBL in Bangladesh

Islami Bank Bangladesh Limited conduct it is business very successfully. It is one of the

largest banking systems in Bangladesh. It has many branches around the country. It is started

the journey with only one branch which is situated in the heart of the Motijheel. Now at this

moment it is belong 279 Branches among the private sector Banks in Bangladesh.

3.6 Capital Structure

Islami Bank Bangladesh Limited is a Joint Venture Public Limited Company engaged in

commercial banking business based on Islamic Shariah with 63.09% foreign shareholders. It

is listed with Dhaka Stock Exchange Ltd. and Chittagong Stock Exchange Ltd. Authorized

Capital of the Bank is Tk. 20,000.00 Million ($257.23 Million) and Paid-up Capital is Tk.

14,636.28 Million ($188.25 Million) having shareholders as on 30th June 2013. Islami Bank

Bangladesh Ltd. (IBBL) is the pioneer of Islamic banking in Bangladesh. It became

incorporated on March 13, 1983. It has 41.77% local and 58.23% foreign shareholders.

Page 25 of 45

3.7 Management of IBBL Islami Bank Bangladesh Limited is being managed by Board Directors comprising foreigners

and local. An Executive committee is formed by the Board of Directors for efficient and

smooth operation of the Bank. Besides, a Management Committee looks after the affairs of

the Bank.

Management Structure of IBBL

Figure 1.1: Management structure of IBBL

Chairman

Managing Director (MD)

Deputy Managing

Director (DMD)

Executive Vice President (EVP)

Senior Vice President (SVP)

Vice - President (VP)

Assistant Vice - President (AVP)

Senior Principle Officer (SPO)

Principle Officer (PO)

Senior Officer (SO)

Officer

Assistant Officer (AO)

Assistant Officer Grade 1

Assistant Officer Grade 2

Assistant Officer Grade 3

Security Guard Grade 2

Security Guard Grade 1

Messenger Come Guard 2

Messenger Come Guard

Page 26 of 45

Page 27 of 45

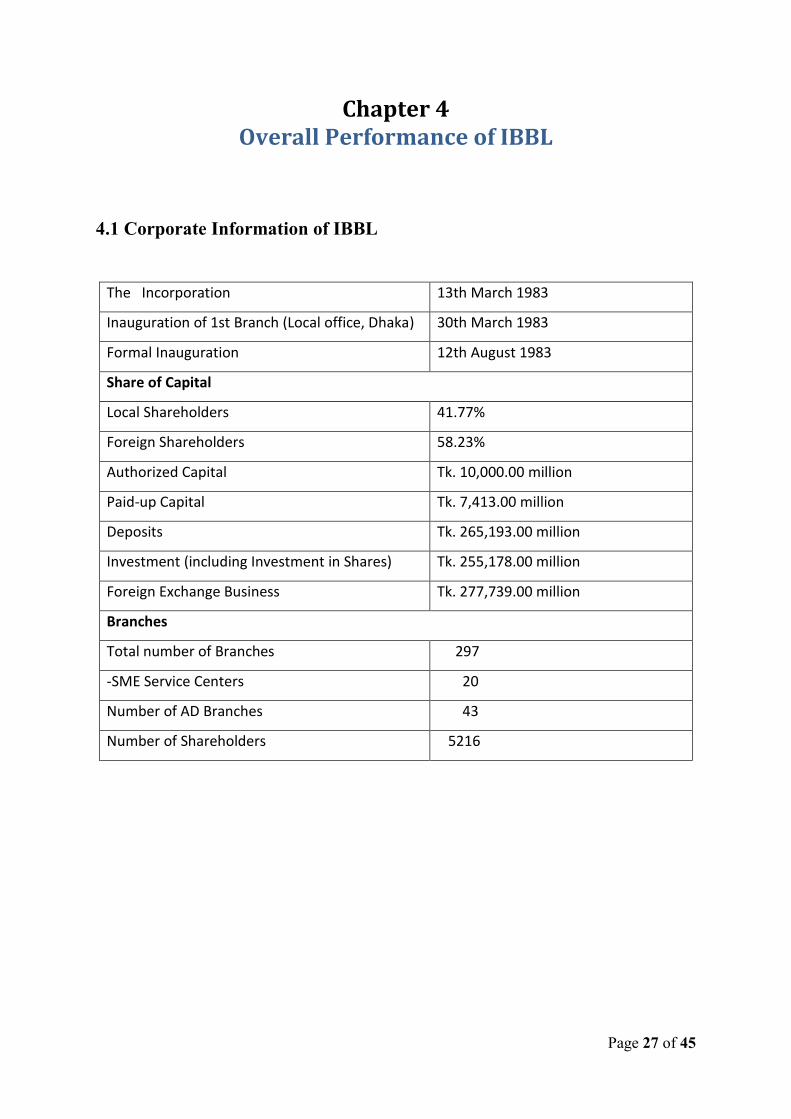

Chapter 4 Overall Performance of IBBL

4.1 Corporate Information of IBBL

The Incorporation 13th March 1983

Inauguration of 1st Branch (Local office, Dhaka) 30th March 1983

Formal Inauguration 12th August 1983

Share of Capital

Local Shareholders 41.77%

Foreign Shareholders 58.23%

Authorized Capital Tk. 10,000.00 million

Paid-up Capital Tk. 7,413.00 million

Deposits Tk. 265,193.00 million

Investment (including Investment in Shares) Tk. 255,178.00 million

Foreign Exchange Business Tk. 277,739.00 million

Branches

Total number of Branches 297

-SME Service Centers 20

Number of AD Branches 43

Number of Shareholders 5216

Page 28 of 45

4.2 Financial Analysis: Paidup Capital & Reserve The Authorized Capital of the Bank is and Paid-up capital is in --. The Paid-up Capital was Taka 67.50 million in 1983. The Reserve Fund of the Bank has been increasing steadily. on 31st December 1983, it was Taka 0.36 million and stood at

31-12-2014 16,099.91 million

30-09-2014 16,099.90 million

30-06-2014 16,099.9 million

31-12-2013 14,636.28 Million

31-12-2012 12,509.64 Million

30-09-2012 12,509.64 Million

Source: http://www.islamibankbd.com/abtIBBL/paidup_capital.php

Performance of IBBL as on 31.07.2015 at a glance

SL

Particulars

Position as on

31.12.2014

Position as on

31.07.2015

Growth % Over

31.12.2014

1 Total Property & Assets 651,579,483,721 688,819,685,231

5.715374

2 Cash In Hand 46,219,359,839 53,875,247,061 16.56424

3 Total Deposit 559,713,580,029 595,695,858,328 6.428695

4 Total Investment 460,385,467,466 487,327,306,849 5.852018

5 Total profit before (taxes) 4,598,994,773 6,722,442,578 46.172

6 Net profit/ (loss) after tax 974,059,548 3,395,244,209 248.5664

7 Consolidated Earnings Per share (EPS)

0.61

2.11 245.9016

Page 29 of 45

4.3 Contribution to Economy: IBBL Prospective

Only Bank in Bangladesh (Top 1000 Global Banks, 970th Position in 2014) 50% of total global Islamic microfinance. Microfinance: 900 Thousand Family in 18000 villages Best Entrepreneur Friendly Bank (One million entrepreneur including 600

thousand woman entrepreneur) Highest taxpayer in Banking Sector Pioneering Two “R” of the economy (RMG 21%& Remittance 27%) More than 4000 industry financed by IBBL Market share of IBBL (Spinning 25%, Steel & Iron 21%, Transport 15%,

Agriculture 13%, Housing 11%, SME 16%)

Page 30 of 45

Page 31 of 45

Chapter 5 What sets IBBL apart?

Islami Bank Bangladesh Limited Undoubtedly a financial institution. It’s main features deal

in services. It is the pioneer of Islamic Bank in Bangladesh. It is the largest private

commercial bank in Bangladesh. The general bank is given priority to the Riba which is

called interest. For Muslims interest is totally Haram. To escape from this problem IBBL has

distributed their dividends on the basis of the Profit Loss Sharing (PLS) system.

5.1 Differences between Islamic Banking & Conventional Banking

Conventional Banking Islamic Banking

1. The functions and operating modes of conventional banks are based on man-made principles.

The functions and operating modes of Islamic Banks are based on Islamic Shariah.

2. The investor is assured of a predetermined rate of interest.

In contrast, it promotes risk sharing between provider of capital (investor) and the user of funds (entrepreneur).

3. It aims at maximizing profit without any restriction.

It also aims at maximizing profit but subjected to shariah restrictions.

4. It does not deal with Zakat and does not pay any zakat.

In the modern Islamic Banking system it has become one of the service oriented functions of the Islamic banks to collect and distribute zakat.

5. Lending money and getting it back with interest is the fundamental function of conventional banks.

Participation in partnership business is the fundamental function of the Islamic Banks.

6. Its scope of activities is narrower when compared to Islamic Bank

Its scope of activities is wider when compared with a conventional bank.

7. It can charge additional money (compound rate of interest) in case of defaulters.

Islamic bank have no provision to charge any extra money from the defaulters.

Page 32 of 45

8. Very often, Bank’s own interest becomes prominent. It makes no effort to ensure growth with equity.

It gives due importance to the public interest. Its ultimate aim is to ensure growth with equity.

9. For interest based commercial banks, borrowing from money market is relatively easier.

For Islamic Banks it is comparatively difficult to borrow money from the money market.

10. Since income from the advances is fixed, it gives little importance to developing expertise in project appraisal and evaluations.

Since it shares profit and loss, Islamic bank pay greater attention to developing project appraisal project appraisal and evaluation.

11. Conventional Banks give greater emphasis on credit worthiness of the clients.

Islamic banks on the other hand, give greater emphasis on the viability of the projects.

12. The status of a conventional bank, in relation to its clients, is that of creditor and debtors.

The status of Islamic Bank in relation to its clients is that of partners, investors and trader.

13. A conventional bank has to guarantee all its depositors.

Strictly speaking, an Islamic bank cannot guarantee all its deposits.

Page 33 of 45

5.2 Superiority of Islamic Banking

Islamic Bank is a shariah compliant financing institution. Where the Maqasid al Shariah aims at maximization of welfare and at the same time as a financial institution tries to maximize its wealth.

5.2.1 Maqasid – al – shariah # Elimination of all Evils

1. Prohibition of Interest/ Riba: Interest means predetermined & excess over the principle of any debt/loan for a fixed period of time. Extra amount over the principle is interest. Extra goods if received against exchange of same commodities are also Interest

Literally Interest means Surplus, Excess, Increase, expansion, additional etc.

Riba/ Interest technically refers to the Premium that must be paid by the borrower to the lender along with the principal amount as a condition for the loan

From Hazrat Ali (RA), MohaNabi (SM) said “Any load repaid with any benefit is Riba” The hadith described in “Musnad” by Hazrat harish Ibn Abi Usamah- jalal Uddin Al-Suyuti, Jame Al Sagir (V.2,P94)

ISLAMIC BANK

Shariah Compliant Financing Institution

Elimination of All Evils

Activities Promoting Welfare of People

Ensure Liquidity with Efficient Fund MGT

Ensure Profitability taking acceptable risk

Maximization of Welfare Maqasid – al – Shariah Maximization of Wealth

Strategic Objectives of Islamic Bank

Page 34 of 45

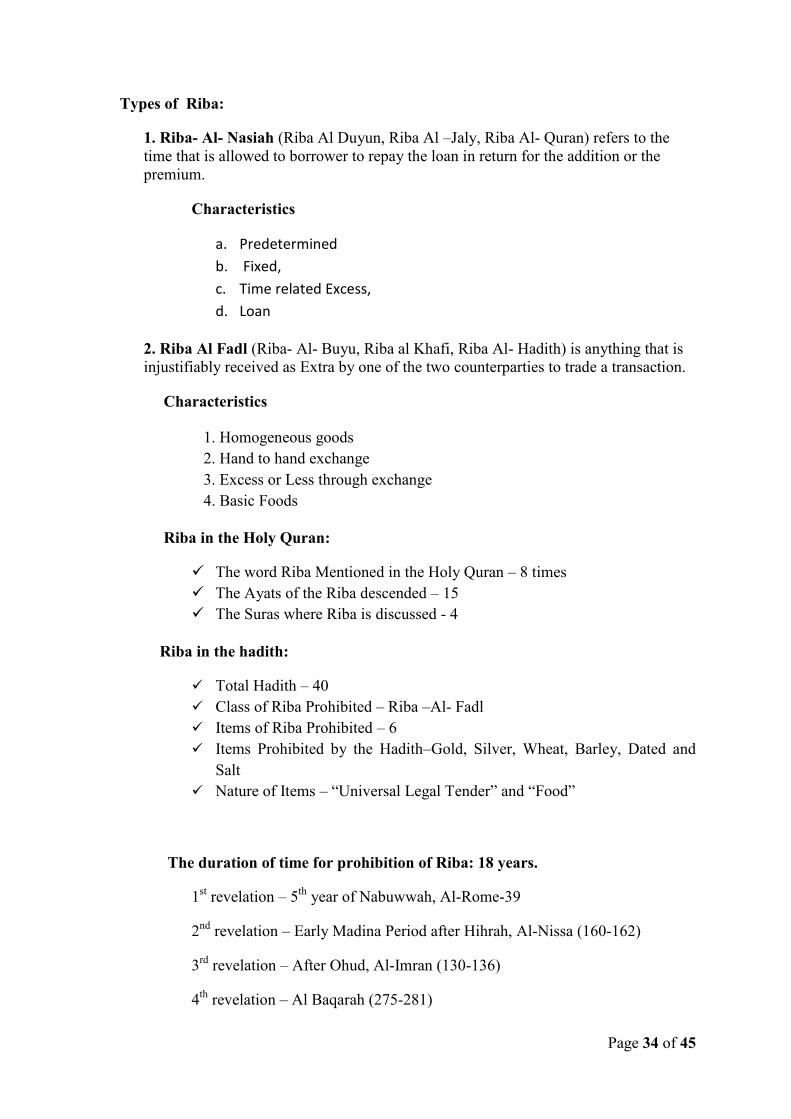

Types of Riba:

1. Riba- Al- Nasiah (Riba Al Duyun, Riba Al –Jaly, Riba Al- Quran) refers to the time that is allowed to borrower to repay the loan in return for the addition or the premium.

Characteristics

a. Predetermined

b. Fixed,

c. Time related Excess,

d. Loan

2. Riba Al Fadl (Riba- Al- Buyu, Riba al Khafi, Riba Al- Hadith) is anything that is injustifiably received as Extra by one of the two counterparties to trade a transaction.

Characteristics

1. Homogeneous goods 2. Hand to hand exchange 3. Excess or Less through exchange 4. Basic Foods

Riba in the Holy Quran:

The word Riba Mentioned in the Holy Quran – 8 times The Ayats of the Riba descended – 15 The Suras where Riba is discussed - 4

Riba in the hadith:

Total Hadith – 40

Class of Riba Prohibited – Riba –Al- Fadl Items of Riba Prohibited – 6

Items Prohibited by the Hadith–Gold, Silver, Wheat, Barley, Dated and Salt

Nature of Items – “Universal Legal Tender” and “Food”

The duration of time for prohibition of Riba: 18 years.

1st revelation – 5th year of Nabuwwah, Al-Rome-39

2nd revelation – Early Madina Period after Hihrah, Al-Nissa (160-162)

3rd revelation – After Ohud, Al-Imran (130-136)

4th revelation – Al Baqarah (275-281)

Page 35 of 45

The Condemned Parties of The Riba:

a. Those who take it b. Those who give it c. Those who record the transaction d. Those who act as witnesses

Why interest should be abolished:

Increases the commodity prices Decreases the wages of laborers Purchasing power decreases Morality gets lost Unemployment and gap between rich and poor rises Ensure Justice Remove all form of injustice or exploitation through unfair exchanges

2. Elimination of Gharar/ Maisir :'Gharar' is an Islamic finance term describing a risky or hazardous sale, where details concerning the sale item are unknown or uncertain. Gharar is generally prohibited under Islam, which explicitly forbids trades that are considered to have excessive risk due to uncertainty.

Maisir exists when; the policy holder contributes a small amount of premium in the hope to gain a larger sum

3. Avoiding abuses/ overuses and misery

5.2.2 Maqasid – al – shariah # Activities Promoting Welfare of the People / CSR

Page 36 of 45

5.3 Islamic Principles of Deposit Mobilization

Deposit is the Life Blood of a bank. Maximum utilization of resources is deposit principle of Islamic Banking. It aims at bringing the unbanked people under the financial services. Islami Bank has so far developed 16 Deposit Products for mobilization of its deposit.

1. Mudaraba Savings Account

2. Mudarabah Term Deposit Account: 3/6/12/36 months (MTDRA)

3. Mudaraba Special Notice Account (MSNA)

4. Mudaraba Hajj Saving Scheme (MHSA)

5. Mudaraba Special Savings (Pension) Account (MSSA)

6. Mudaraba Savings Bond (MSB)

7. Mudaraba Monthly Profit Deposit Scheme (MMPDA)

8. Mudaraba Muhor Savings Account (MMSA)

9. Mudaraba Waqf Cash Deposit Account (MWCDA)

10. Mudaraba NRB Saving Bond (MNSB)

11. Mudarabah Foreign Currency Deposit (Savings) Account (MFCD)

12. Student Mudarabah Savings Account (SMSA)

13. Mudarabah Farmers Savings Account (MFSA)

14. Non-Resident Investor Taka Account (NITA)

15. Mudarabaha Upohar Deposit Scheme

16. Mudarabah Industry Employee Savings Account (MIESA).

Deposit Mobilization

Al-Wadeeah Current Account Mudarabah Savings Account

1. It is a contract by which a person empowers someone else to keep and protect his property.

2. There must have prior permission from the owner of the fund to use/ invest the same in their business with other fund.

3. No profit is allowed – bearing no risk, no loss.

4. The fund is returnable to the owner on demand as it was in original shape.

1. It is a contract of Partnership where the “Shaib-al-maal, the Depositor” provides capital to “Mudarib, the Bank” for investing it in a commercial enterprise by applying his labor and endeavor.

2. According to weightage, 65 % Earnings from the investment of Mudarabah Deposited Fund will be distributed among Shahib al Maal. 3. But the loss, if any, will be borne by the provider of funds.

Page 37 of 45

5.2.2 Investment Mechanism of IBBL

Trading/ Bai: Trading means purchase and sell of goods on agreed profit . Where –

1. Bai Murabaha

a. To offer an order by the client to the bank. b. To make the promise binding upon the client to prophase from the bank and

also to indemnity the damages caused by breaking the promise. c. To take security in the form of cash/kind/collaterals d. To document the debts resulting from Bai0 Murabaha e. Stock and availability of goods is a basic condition f. Bank must bear the risk until delivery of goods to the client. g. Bank may sell it at a higher price h. Price once fixed cannot be changed.

2. Bai- Muajjal- Deffered payment sale at fixed price

3. Bai -Salam – Advance sale and purchase

4. Bai – Istisna – Products can be sold without having the same existence.

Share/ Partnership: is a partnership contract between banks and the clients, entrepreneurs where banks supply the capital and the clients invest their labor, wisdom, skill etc. On the condition that the profit will be shared between them as per agreed ratio and the actual loss (if any) will be born by the bank.

1. Features of Mudaraba – profit is distributed among the partners in pre-

determined ratio while the loss is born by each partner in proportion to his

contribution.

a. Capital should be specific

b. Equal share is not must

c. Nature of capital may ne money or valuable

d. Active participation of the partners

e. Business record is to be maintained

f. Profit is shared as per agreed ratio

g. Loss must be born as per equity ratio.

Investment

Trading/ Bai Partnership Mechanism

Leasing/ Ijara

Bai- Murabaha

Bai- Muajjal

Bai- Salam

Bai- Istisna

Musharaka

Mudaraba

HPSM - Commercial

HPSM-Industry

HPSM- Transport

HPSM- Agriculture

Page 38 of 45

2. Features of Mudaraba

a. Capital must be specific

b. Capital must be in currency

c. Capital is not a liability debt on Mudarib

d. Shaib al mal can not take part in business directly but may supervise

the business.

e. Mudarib is not entitled to wages/slary but may get actual expenses

incurred

f. Profit must be shared as per agreed ratio

g. Moss must be borne by the owner of the capital

h. Profit and loss is ascertained after expiry of the contract period.

i. Shaib al mal loses its capital and Mudarib loses his lobour in case of

actual loss incurred in the business.

Leasing/ Ijara: It is the combination of Bai, sharing and leasing for transferring the ownership of an asset.

1. HPSM (Commercial)

2. HPSM (Industrial)

3. HPSM (Agriculture)

4. HPSM (Transport)

Investment Principle of IBBL:

1. Balanced Distribution of Wealth 2. Need-based Financing 3. Prioritizing need fulfillment (necessary, comfort & beautification) 4. Diversification By size, sector & locations 5. Avoiding concentration in few hands 6. Promoting real asset based / real asset baked financing

For borrower IBBL does not provide money but act as supplier or agent to purchase goods/ raw materials that’s why client cannot flow the money out of business even if he wants. Thus he cannot avoid the responsibility to repay the money of bank because of proper monitoring.

Page 39 of 45

5.5 Profit Distribution Policy

5.5.1 Principle of profit Distribution to Mudaraba depositors

The principles of calculation and distribution of profit to Mudaraba depositors generally followed by the Islami Banks are as follows –

1. Mudaraba depositors share income derived from investment fund

2. They do not share any income derived from miscellaneous banking services where he

use of depositors fund is not involved, such as commission, exchange, service charges

and other income earned by the bank.

3. Mudaraba depositors get priority in case of investment over banks equity and other

cost free funds.

4. The gross income derived from investment from investment during the accounting

year is at first allocated to Mudaraba depositors as per agreed ratio like 65:35 and then

equity and cost free funds according to their proportion in the total investment.

5. Then the share of gross investment profit of Mudaraba deposits are distributed as per

principle shown below-

a. 20% is retained by the bank as management fee.

b. 15% is transferred to a reserve fund for offsetting investment loss.

c. The remaining 65% distributable to Mudaraba depositors applying

weightages.

5.5.2 What is weightage?

Weightage means giving the value or importance or preference of one product in comparison to other product.

5.5.3 Factor considering for Fixing up of weightage

The more risk, the more weightage The longer the period of sacrifices, the more weightage More the uses of Banks facility, less the weightage More the interest of the Bank/ Society, more the weightage and vise versa.

Page 40 of 45

5.5.4 Weightage of various Mudaraba Deposits

Mudaraba Deposit Products Weightage

Mudaraba Savings Account 0.35-0.75 Mudarabah Term Deposit Account: 3/6/12/36 months (MTDRA) 0.88-1.00 Mudaraba Special Notice Account (MSNA) 0.25-0.55 Mudaraba Hajj Saving Scheme (MHSA) 1.30-1.35 Mudaraba Special Savings (Pension) Account (MSSA) 1.30-1.10 Mudaraba Savings Bond (MSB) 1.25-1.10 Mudaraba Monthly Profit Deposit Scheme (MMPDS) 1.20-1.10 Mudaraba Muhor Savings Account (MMSA) 1.10-1.30 Mudaraba Waqf Cash Deposit Account (MWCDA) 1.35 Mudaraba NRB Saving Bond (MNSB) 1.25-1.35 Mudarabah Foreign Currency Deposit (Savings) Account (MFCD) 0.75 Student Mudarabah Savings Account (SMSA) 0.75 Mudarabah Farmers Savings Account (MFSA) 0.75 Non-Resident Investor Taka Account (NITA) 0.75 Mudarabaha Upohar Deposit Scheme 0.75 Mudarabah Industry Employee Savings Account (MIESA) 0.75

5.5.5 Profit calculation with an example

The XYZ bank has provided you the following information:

XYX Bank Ltd.

a. Fund of Share holders (Equity) Tk. 500

b. Fund of Al Wadeeah Depositors TK. 1,500

C. Fund of Mudaraba Depositors Tk. 3,000

D. Total Fund invested Tk. 5,000

Total Income 1200

Miscellaneous Income 100

Doubtful Income 100

Page 41 of 45

Step 1. Calculate Distributable Gross income to (65%) to Mudaraba depositors:

Total Income

1200

less: Miscellaneous Income 100

Total Investment Income 1100

less: Doubtful Income 100

Total Distributable Income (DTI) 1000

Proportionate amount of Mudaraba depositors (DTI/Total Fund Invested) x Mudaraba depositors Investment

600

Distributable income to Mudaraba Depositor (65%) 390

Step 2. Distribute the income to each account and show the percentage of Income/ Profit.

Name of the Deposit Products

Deposit Product Amount

W

Weighted Product

Profit for Each Taka

Total Profit

Profit in %

1 2 3 4 = 2x3 5= DI/TWP 6 = 4x5 7=(6/2)x100 Mudaraba Hajj Savings 1000 1.35 1350 0.126 170 17% Mudaraba Term Deposit 1000 1.00 1000 0.126 126 12.6% Mudaraba Savings Account 1000 0.75 750 0.126 94 9.4%

Total 3000 3100 390

W= Weightage; DI= Distributable Income; TWP= Total weighted Product

Page 42 of 45

Our Findings:

1. Overall Business & Financial performance of Islamic Banks are better than that of conventional Banks.

2. Wage earners remittance handling by Islamic banks particularly by IBBL is spectacular

3. Islamic Banks are much ahead in Inclusive Banking, Green Banking, SME & Microfinance and CSR activities.

4. Upholding ethics is in the top of the agenda in Islamic Banks. 5. Islamic Banks Investments are largely concentrated in trading and rent sharing modes. 6. IBBL spends more money on CSR as an inherit objective of marketing. 7. There is no Marketing Department. How do they do marketing Activities? Reasons of

increasing its client base? Though IBBL doesn’t have marketing department it has a huge customer base. The reasons behind their huge customer base is – It’s an integrated marketing system through CSR activities through the intense focus on Humanity rather than business & Mass Banking (for all class of people). As a part of their CSR activities they run Internship Program for the students of different universities. Their internship program is different than of other conventional banking internship program. It is a 60 (sixty) day’s internship program of which 10 days at IBTRA premises for theoretical classes. IBTRA aims at familiarizing the internee with the principles of Islamic Shariah and its implementation in the financial system. IBBL converts these internees into IBBL’s ambassador through rewarding for account opening, Deposit collection and other activities. I was in 124th Internship batch, we the 97 students from different university had collected 15 crore & about 450 new account opened in 50 days in IBBL’s different branches.

Secret behind IBBL’s Success

Investment Depost Mobilization

Trading/ Bai

Passive Partnership

Partnership

Risk Sharing

Leasing/ Ijara

Emphasis on Productivity & Mass Welfare

Corporate Culture (Moral Filtering)

Fund Diversification is almost impossible

Page 43 of 45

Recommendations From the above discussion, we can recommend the followings:

There are ways to encourage more participation in financial services

o From my practical experience what a I a have seen, IBBL is only using their

Bai & Leasing Investment Mode ignoring Partnership Investment Mode.

o As we know most of the entrepreneur are not well trained with Management

Skills. According a study most of the entrepreneur business extinct within

three years or so. May be Banks participation in Management through

partnership is appreciable

IBBL should run an Entrepreneur Development Programme

IBBL need to in Power Sector of the country such as in electricity and in finding of

new mine resources of the country.

IBBL can introduce Education Scheme without giving it through Islami Bank

Foundation.

The authority of IBBL should Conveyance pressure on Government bodies to run

proper and sufficient application of Islamic banking law in Bangladesh.

There are limited scopes to deal women entrepreneurs and professionals for making

investment by women entrepreneurs.

IBBL should appoint a sufficient number of women employees to deal women

entrepreneurs and professionals and understand their needs and thus create demand

for investment.

IBBL grants investment to group not individual in rural areas for low income

community As a result, the mission, using invested money in income generating

activities the poor needy population can become self reliant - is failed . Moreover, it

enhances group dependence.

Inclusion of more subjects based on the Quran and Sunnah in the Training courses of

the Islami Bank Training & Research Academy in order to develop human resources

having morally.

To fulfill the vision of "mass banking" this Bank should grants investment portfolio to

new entrepreneurs /new businessmen new companies etc.

New and ‘innovative’ products are designed for financing under Profit and Loss

sharing basis.

Page 44 of 45

Conclusion

IBBL today is the leader among the all best commercial banks in Bangladesh. They are doing

according to the proper banking system should have utilized & they are following the Islamic

Shariah for a long time. They are ahead among the distant areas people who love the Islam &

the rules of Islam. Today IBBL whatever doing in the banking systems they are completely

innovative & very much carrying to the clients. With the appropriate resolution of Islamic

point of view & the business dilemma IBBL has set a standard in the banking environment.

Comparing to other conventional bank IBBL is also providing greater customer service.

Through SME’s they are providing opportunities to rural area to cheer up & grow up with

new & massive possibilities in business. IBBL being the pioneer in Islamic Banking has this

responsibility to identify such investment opportunities through research. Therefore, it

expects that IBBL will take utmost care to overcome the problems. In the economic

development of the country IBBL is contributing and playing a vital role. Islami Bank

Bangladesh Limited Investment modes are most helpful to generate more employment and

more productive than conventional banking because Islami bank concerns with the purpose of

investment not with only invested money, its create assets.

Page 45 of 45

References 1. Research Paper: Issues & Challenges for Islamic Banking in Bangladesh, (BIBM) May

2015 2. Principles of distribuytion of profit to the Mudaraba depositors – Central Accounts

Department at present Financial and Administration Department (FAD), IBBL, HO, Dhaka

3. Profit Payout to Mudaraba Depositors ( Bangladesh Prospective) – M. Azizul Huq 4. Guidelines for Islamic Banking (November -2009) Bangladesh Bank. 5. Islamic Bank Management by Mohammad Abdul Mannan 6. Islamic Banking – A Developed Banking System – Prof. Md Sharif Hossain 7. Islamic Economics – M.A Hamid 8. Islamic Economics & Banking – Iqubal Kabir Mohon 9. Interest & Islamic Banking – Md. Fazlur Rahman Ashrafi Articles on Islamic Banking:

1. Banking In the Light of Maqasid al Shariah, Mohammad Abdul Mannan , Managing Director & CEO, IBBL

2. Islamic Economics Vs Conventional Economics: Superiority of Islamic Economics, Mohammad Rokon Udin, EVP & Director (Admin) IBTRA.

3. Meaning & Types of Riba, Differences among Riba, Bai, Profit, Rent etc. and Socio Economic Impact of Riba by Mst. Zakiya Akhter Khanam, PO & Faculty member IBTRA

4. Islamic Principles of deposit Mobilization and Account Opening Procedure for different types of Account Holders & Profit Distribution Policy. By Md Maznuzzaman, Vice President & Head of Mirpur -1 Branch, IBBL.

5. An Overview on Various Modes of Investment in IBBL Familiarizing the concern Manuals by Masuma Begum, SPO & Faculty Member, IBTRA.

6. Import & Export Finance under Islamic Mode, Mohammad Hossain Akhter, AVP & FM, IBTRA

7. CSR the Built in Mechanism, Under Islamic Banking System by A.H.M Latif Uddin Chawdhury, EVP, IBBL

8. Poverty Alleviation: Concept, Programme and Strategies under Islamic Perspective Covering Zakat, Waqf, Quard etc. by Masuma Begum, SPO & Faculty Member, IBTRA

9. Zakat – based Poverty Alleviation Strategies by Dr. Mohammad Ayub Miah, CEO, Center for Zakat Management & Ex Secretery, GOB

10. Responsibility of the Youth in the 21st Century by Dr. Mohammad Ayub Miah, CEO, Center for Zakat Management & Ex Secretery, GOB

Newspaper Articles # Based on Islamic Banking

1. Islamic Banking Leads the Market. Source: The Banikbarta 29.03.2015

Web based Articles: 2. http://www.islamibankbd.com/

3. http://ibtra.com/

4. https://www.bb.org.bd/