18

Conference call First nine months of 2019

Conference callFirst nine months of 2019

Slide 2

Agenda

Conference call First nine months of 2019

Highlights and key events

R&D update

Financials and outlook

Sales update

Slide 3

Forward-looking statements

Novo Nordisk’s reports filed with or furnished to the US Securities and Exchange Commission (SEC), including this presentation as well as the company’s statutory Annual Report 2018 and Form 20-F, which were both filed with the SEC in February 2019 in continuation of the publication of the Annual Report 2018, and written information released, or oral statements made, to the public in the future by or on behalf of Novo Nordisk, may contain forward-looking statements. Words such as ‘believe’, ‘expect’, ‘may’, ‘will’, ‘plan’, ‘strategy’, ‘prospect’, ‘foresee’, ‘estimate’, ‘project’, ‘anticipate’, ‘can’, ‘intend’, ‘target’ and other words and terms of similar meaning in connection with any discussion of future operating or financial performance identify forward-looking statements. Examples of such forward-looking statements include, but are not limited to: • Statements of targets, plans, objectives or goals for future operations, including those related to Novo Nordisk’s products, product research, product development, product

introductions and product approvals as well as cooperation in relation thereto,• Statements containing projections of or targets for revenues, costs, income (or loss), earnings per share, capital expenditures, dividends, capital structure, net financials and

other financial measures,• Statements regarding future economic performance, future actions and outcome of contingencies such as legal proceedings, and• Statements regarding the assumptions underlying or relating to such statements.

These statements are based on current plans, estimates and projections. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific. Novo Nordisk cautions that a number of important factors, including those described in this presentation, could cause actual results to differ materially from those contemplated in any forward-looking statements.

Factors that may affect future results include, but are not limited to, global as well as local political and economic conditions, including interest rate and currency exchange rate fluctuations, delay or failure of projects related to research and/or development, unplanned loss of patents, interruptions of supplies and production, product recalls, unexpected contract breaches or terminations, government-mandated or market-driven price decreases for Novo Nordisk’s products, introduction of competing products, reliance on information technology, Novo Nordisk’s ability to successfully market current and new products, exposure to product liability and legal proceedings and investigations, changes in governmental laws and related interpretation thereof, including on reimbursement, intellectual property protection and regulatory controls on testing, approval, manufacturing and marketing, perceived or actual failure to adhere to ethical marketing practices, investments in and divestitures of domestic and foreign companies, unexpected growth in costs and expenses, failure to recruit and retain the right employees, and failure to maintain a culture of compliance.

For an overview of some, but not all, of the risks that could adversely affect Novo Nordisk’s results or the accuracy of forward-looking statements in this presentation, reference is made to the overview of risk factors in ‘Risk management enables better decision-making’ on pp 41-43 in the Annual Report 2018.

Unless required by law, Novo Nordisk is under no duty and undertakes no obligation to update or revise any forward-looking statement after the distribution of this presentation, whether as a result of new information, future events or otherwise.

Important drug information• Victoza® is approved for the management of type 2 diabetes only• Saxenda® is approved in the USA and the EU for the treatment of obesity only

Conference call First nine months of 2019

Slide 4

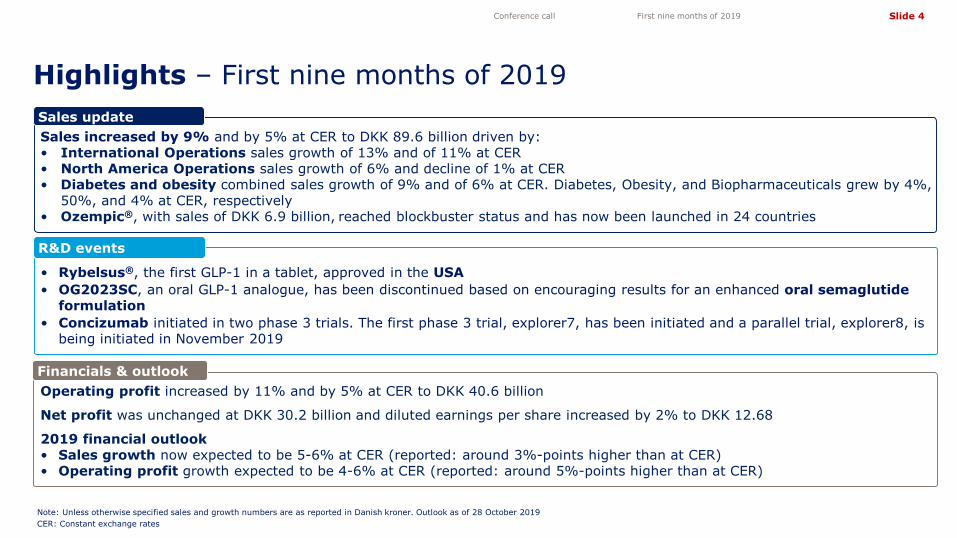

Sales increased by 9% and by 5% at CER to DKK 89.6 billion driven by:• International Operations sales growth of 13% and of 11% at CER• North America Operations sales growth of 6% and decline of 1% at CER• Diabetes and obesity combined sales growth of 9% and of 6% at CER. Diabetes, Obesity, and Biopharmaceuticals grew by 4%,

50%, and 4% at CER, respectively• Ozempic®, with sales of DKK 6.9 billion, reached blockbuster status and has now been launched in 24 countries

Sales update

Highlights – First nine months of 2019

Conference call First nine months of 2019

Note: Unless otherwise specified sales and growth numbers are as reported in Danish kroner. Outlook as of 28 October 2019 CER: Constant exchange rates

• Rybelsus®, the first GLP-1 in a tablet, approved in the USA• OG2023SC, an oral GLP-1 analogue, has been discontinued based on encouraging results for an enhanced oral semaglutide

formulation• Concizumab initiated in two phase 3 trials. The first phase 3 trial, explorer7, has been initiated and a parallel trial, explorer8, is

being initiated in November 2019

R&D events

Operating profit increased by 11% and by 5% at CER to DKK 40.6 billion

Net profit was unchanged at DKK 30.2 billion and diluted earnings per share increased by 2% to DKK 12.68

2019 financial outlook • Sales growth now expected to be 5-6% at CER (reported: around 3%-points higher than at CER)• Operating profit growth expected to be 4-6% at CER (reported: around 5%-points higher than at CER)

Financials & outlook

Slide 5

05

101520253035404550

IO RegionEurope

RegionAAMEO

RegionChina

RegionJ&K

RegionLATAM

NAO

11%

Reported sales split for first nine months of 2019

Sales growth of 5% driven by solid sales growth in International Operations

Conference call First nine months of 2019

GLP-1 Other diabetesInsulinBiopharmDKK

billion

-1%

6%

16%13%

6% 26%

Obesity

International Operations regions

IO: International Operations; AAMEO: Africa, Asia, Middle East & Oceania; J&K: Japan & Korea; LATAM: Latin America; NAO: North America Operations

Growth at CER

Growth drivers for first nine months of 2019

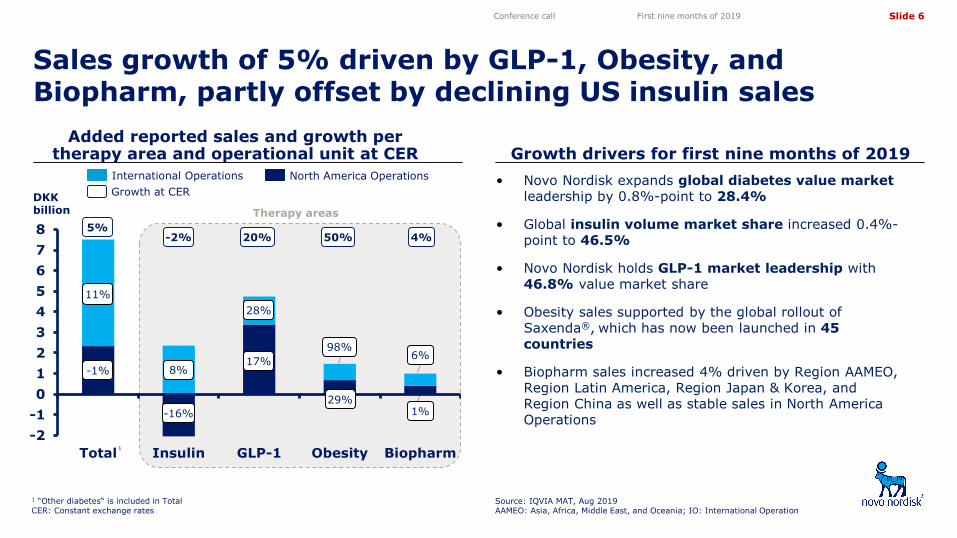

International Operations sales growth of 11% at CER supported by all regions • Increasing sales across all therapy areas • Broad innovative portfolio of products and new product

launches• Solid commercial execution using a Market Fit approach• Underlying demographic trends across IO countries

North America Operations sales declined by 1% at CER driven by the US partly offset by Canada• Sales growth in GLP-1 (+17%), Obesity (+29%), and

stable Biopharm sales, offset by declining insulin sales (-16%)

Slide 6

-2-1012345678

Total Insulin GLP-1 Obesity Biopharm

Sales growth of 5% driven by GLP-1, Obesity, and Biopharm, partly offset by declining US insulin sales

Conference call First nine months of 2019

Added reported sales and growth per therapy area and operational unit at CER

International Operations North America Operations

1 “Other diabetes“ is included in TotalCER: Constant exchange rates

-1%

11%

8%

-16%

17%

28%

29%

98%6%

1%

1

5%-2% 20% 50% 4%

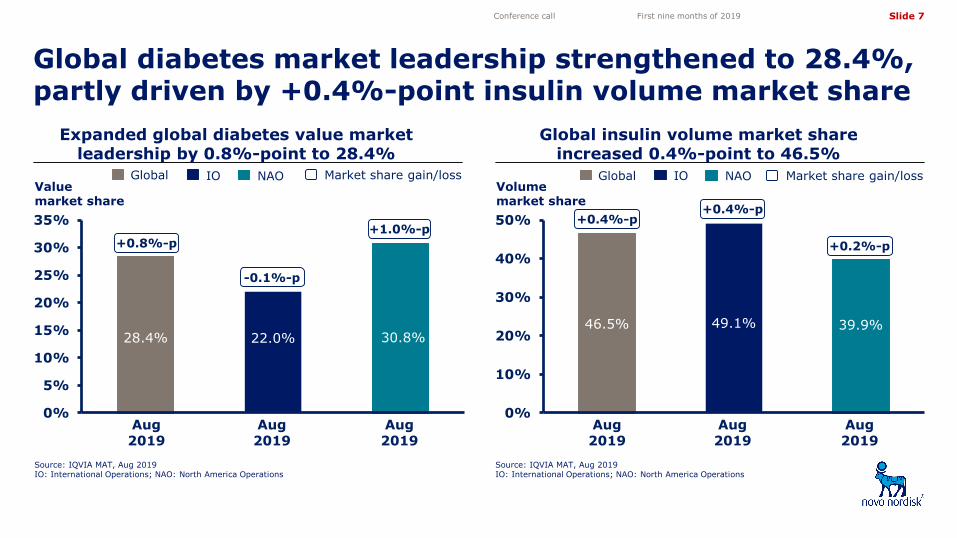

Growth at CER• Novo Nordisk expands global diabetes value market

leadership by 0.8%-point to 28.4%

• Global insulin volume market share increased 0.4%-point to 46.5%

• Novo Nordisk holds GLP-1 market leadership with 46.8% value market share

• Obesity sales supported by the global rollout of Saxenda®, which has now been launched in 45 countries

• Biopharm sales increased 4% driven by Region AAMEO, Region Latin America, Region Japan & Korea, and Region China as well as stable sales in North America Operations

Growth drivers for first nine months of 2019

Therapy areas

Source: IQVIA MAT, Aug 2019AAMEO: Asia, Africa, Middle East, and Oceania; IO: International Operation

DKKbillion

Slide 7

28.4% 22.0% 30.8%

0%

5%

10%

15%

20%

25%

30%

35%

Global IO NAO

Source: IQVIA MAT, Aug 2019IO: International Operations; NAO: North America Operations

Expanded global diabetes value market leadership by 0.8%-point to 28.4%

Global insulin volume market share increased 0.4%-point to 46.5%

Global diabetes market leadership strengthened to 28.4%, partly driven by +0.4%-point insulin volume market share

Source: IQVIA MAT, Aug 2019IO: International Operations; NAO: North America Operations

Conference call First nine months of 2019

46.5% 49.1% 39.9%

0%

10%

20%

30%

40%

50%

Global IO NAO

+0.8%-p+1.0%-p

+0.4%-p+0.4%-p

+0.2%-p

Value market share

Volume market share

Market share gain/lossGlobal IO NAO

Aug 2019

Aug 2019

Aug 2019

Aug 2019

Aug 2019

Aug 2019

Market share gain/lossGlobal IO NAO

-0.1%-p

Slide 8

38%

37%

16%

8%

54%

0%

10%

20%

30%

40%

50%

60%

45%

19%

27%

9%

47%

0%

10%

20%

30%

40%

50%

USA GLP-1 NBRx market share

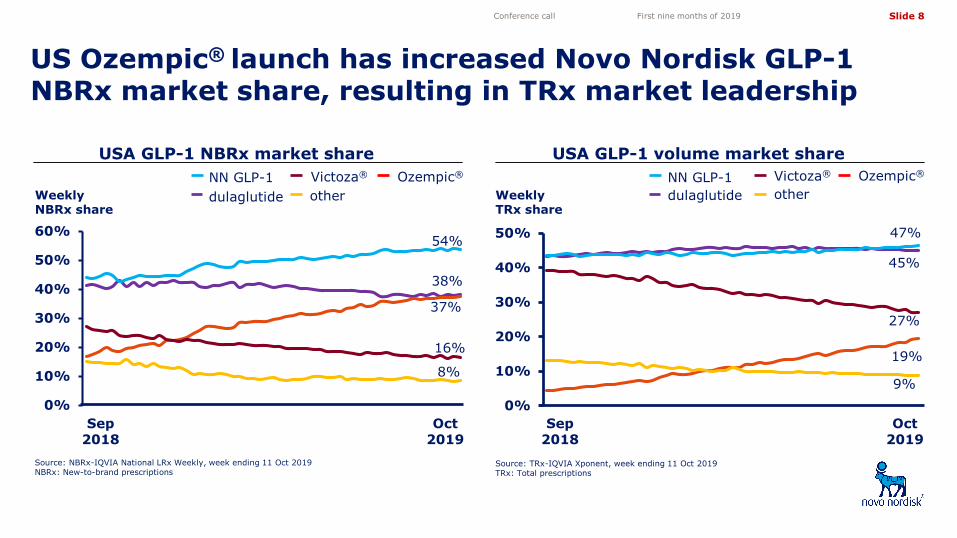

US Ozempic® launch has increased Novo Nordisk GLP-1 NBRx market share, resulting in TRx market leadership

Conference call First nine months of 2019

USA GLP-1 volume market share

WeeklyTRx share

Source: TRx-IQVIA Xponent, week ending 11 Oct 2019TRx: Total prescriptions

Sep2018

Oct2019

Weekly NBRx share

Source: NBRx-IQVIA National LRx Weekly, week ending 11 Oct 2019NBRx: New-to-brand prescriptions

NN GLP-1 Victoza® Ozempic®

dulaglutide otherNN GLP-1 Victoza® Ozempic®

dulaglutide other

Sep2018

Oct2019

Slide 9

56%48%

24%

20%

-60%

-35%

-10%

15%

40%

65%

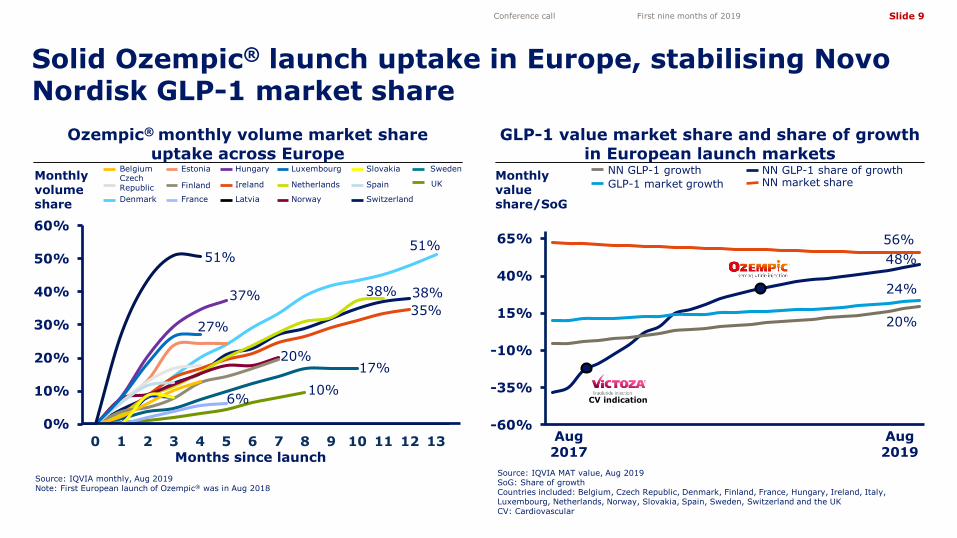

Solid Ozempic® launch uptake in Europe, stabilising Novo Nordisk GLP-1 market share

Conference call First nine months of 2019

NN GLP-1 share of growthGLP-1 market growthNN GLP-1 growth

NN market share

Aug 2017

Aug2019

Monthly value share/SoG

CV indication

Ozempic® monthly volume market share uptake across Europe

GLP-1 value market share and share of growth in European launch markets

Source: IQVIA MAT value, Aug 2019SoG: Share of growth Countries included: Belgium, Czech Republic, Denmark, Finland, France, Hungary, Ireland, Italy, Luxembourg, Netherlands, Norway, Slovakia, Spain, Sweden, Switzerland and the UK CV: Cardiovascular

Denmark Switzerland

Ireland Netherlands

Norway

Finland UK

Source: IQVIA monthly, Aug 2019Note: First European launch of Ozempic® was in Aug 2018

Belgium Hungary

France

Months since launch

51%

38%35%

38%

17%10%

20%

6%

37%

27%

51%

0%

10%

20%

30%

40%

50%

60%

0 1 2 3 4 5 6 7 8 9 10 11 12 13

Latvia

LuxembourgEstoniaCzech Republic Spain

SlovakiaMonthly volume share

Sweden

Slide 10

0.0

0.4

0.8

1.2

1.6

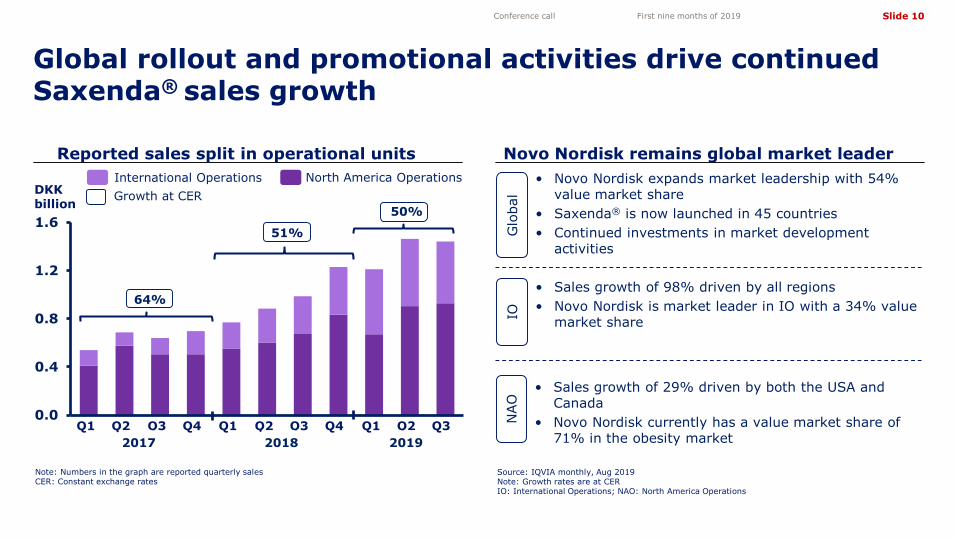

Reported sales split in operational units Novo Nordisk remains global market leader

Global rollout and promotional activities drive continued Saxenda® sales growth

Conference call First nine months of 2019

DKK billion

Source: IQVIA monthly, Aug 2019Note: Growth rates are at CERIO: International Operations; NAO: North America Operations

Q2 Q3 Q4 Q2

North America OperationsInternational Operations

ION

AO

• Sales growth of 98% driven by all regions • Novo Nordisk is market leader in IO with a 34% value

market share

• Sales growth of 29% driven by both the USA and Canada

• Novo Nordisk currently has a value market share of 71% in the obesity market

Glo

bal

• Novo Nordisk expands market leadership with 54% value market share

• Saxenda® is now launched in 45 countries• Continued investments in market development

activities

Growth at CER

Q1Q3 Q1Q4Q2Q1

64%

50%

Note: Numbers in the graph are reported quarterly salesCER: Constant exchange rates

51%

2017 2018 2019Q3

Slide 11

0.0

0.2

0.4

0.6

0.8

1.0

Haemophilia

Conference call First nine months of 2019

Solid commercial execution and new product launches drive 4% Biopharm sales growth

Increase in reported Biopharmsales across products

Biopharm sales driven by global commercial execution

Biopharm sales growth driven by 6% in International Operations and by 1% in North America Operations

Haemophilia sales increased by 5% driven by• Stable NovoSeven® sales, reflecting the solid position in a

competitive market• Continued global rollout of NovoEight® and Refixia®

Novo Nordisk retains global market leadership in the human growth disorder market with a 32% value market share

‘Return Biopharm to growth’ strategy on track• Continued focus on commercial execution, progressing

internal pipeline and adding complementary assets

Note: ‘Other haemophilia’ comprises Esperoct®, NovoThirteen® and Refixia®

Total Novo-Seven®

Novo-Eight®

Other haemo-philia

Nordi-tropin®

Other biopharm

4% 0% 14% 101% 2% 3%

Growth at CERDKK billion

Note: Sales growth reported in constant exchange rates

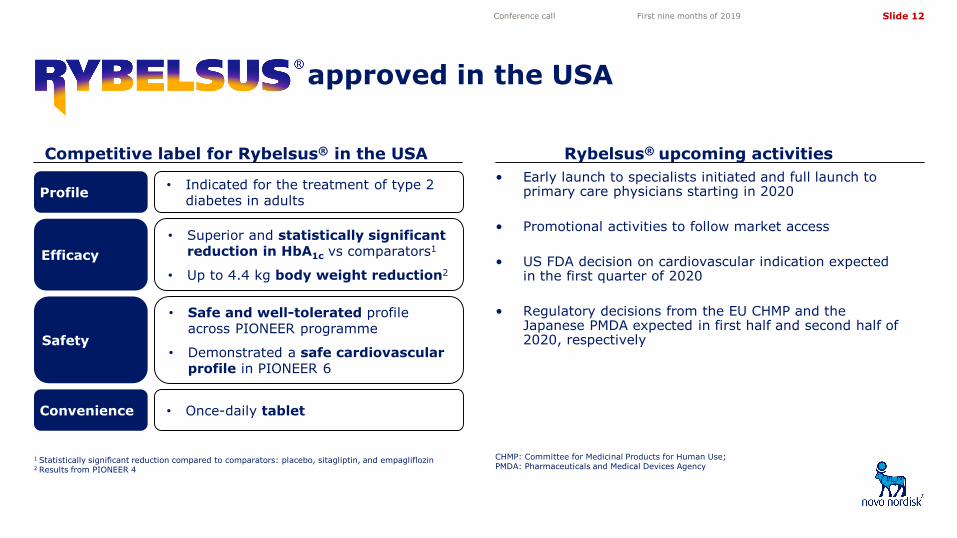

Slide 12

• Early launch to specialists initiated and full launch to primary care physicians starting in 2020

• Promotional activities to follow market access

• US FDA decision on cardiovascular indication expected in the first quarter of 2020

• Regulatory decisions from the EU CHMP and the Japanese PMDA expected in first half and second half of 2020, respectively

Competitive label for Rybelsus® in the USA Rybelsus® upcoming activities

approved in the USA

Conference call First nine months of 2019

• Once-daily tablet

Efficacy

Safety

• Indicated for the treatment of type 2 diabetes in adults

• Safe and well-tolerated profile across PIONEER programme

• Demonstrated a safe cardiovascular profile in PIONEER 6

Convenience

Profile

• Superior and statistically significant reduction in HbA1c vs comparators1

• Up to 4.4 kg body weight reduction2

1 Statistically significant reduction compared to comparators: placebo, sitagliptin, and empagliflozin2 Results from PIONEER 4

CHMP: Committee for Medicinal Products for Human Use;PMDA: Pharmaceuticals and Medical Devices Agency

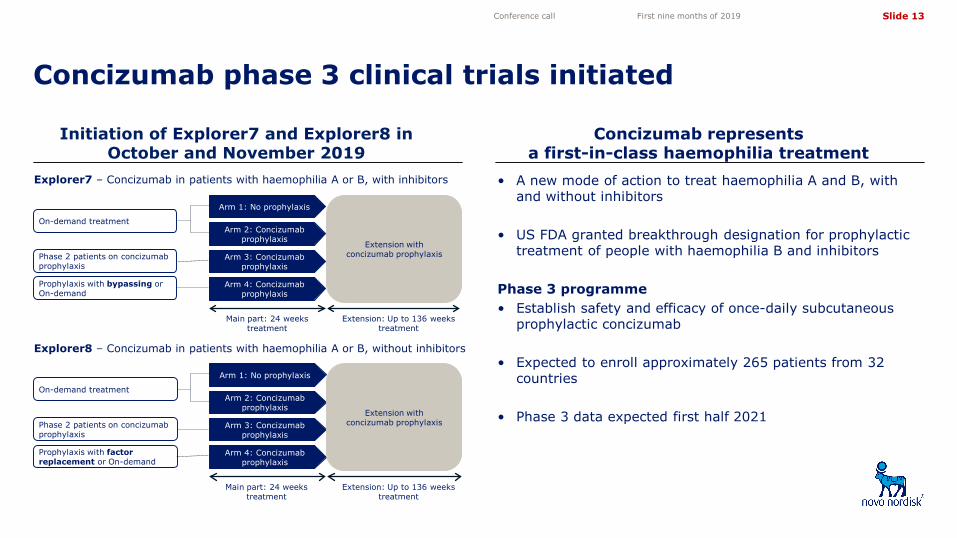

Slide 13

Concizumab represents a first-in-class haemophilia treatment

Initiation of Explorer7 and Explorer8 in October and November 2019

Concizumab phase 3 clinical trials initiated

Conference call First nine months of 2019

Explorer7 – Concizumab in patients with haemophilia A or B, with inhibitors

Explorer8 – Concizumab in patients with haemophilia A or B, without inhibitors

On-demand treatment

Phase 2 patients on concizumabprophylaxis

Prophylaxis with bypassing or On-demand

Arm 1: No prophylaxis

Arm 2: Concizumabprophylaxis

Arm 3: Concizumabprophylaxis

Arm 4: Concizumabprophylaxis

Main part: 24 weeks treatment

Extension: Up to 136 weeks treatment

On-demand treatment

Phase 2 patients on concizumabprophylaxis

Prophylaxis with factor replacement or On-demand

Arm 1: No prophylaxis

Arm 2: Concizumabprophylaxis

Arm 3: Concizumabprophylaxis

Arm 4: Concizumabprophylaxis

Main part: 24 weeks treatment

Extension: Up to 136 weeks treatment

• A new mode of action to treat haemophilia A and B, with and without inhibitors

• US FDA granted breakthrough designation for prophylactic treatment of people with haemophilia B and inhibitors

Phase 3 programme• Establish safety and efficacy of once-daily subcutaneous

prophylactic concizumab

• Expected to enroll approximately 265 patients from 32 countries

• Phase 3 data expected first half 2021

Extension with concizumab prophylaxis

Extension with concizumab prophylaxis

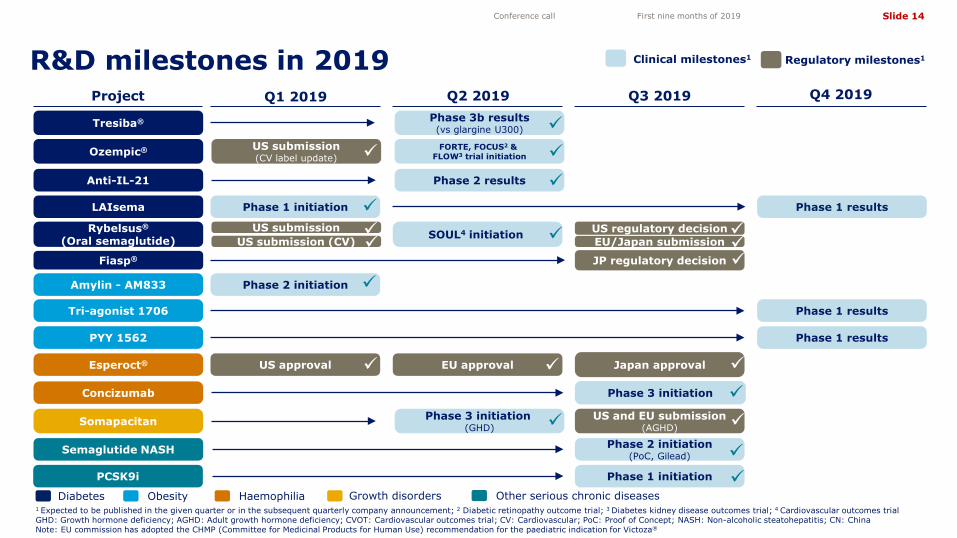

Slide 14

R&D milestones in 2019Project Q1 2019 Q2 2019 Q3 2019 Q4 2019

Rybelsus®

(Oral semaglutide)

Clinical milestones1 Regulatory milestones1

√

Conference call First nine months of 2019

1 Expected to be published in the given quarter or in the subsequent quarterly company announcement; 2 Diabetic retinopathy outcome trial; 3 Diabetes kidney disease outcomes trial; 4 Cardiovascular outcomes trialGHD: Growth hormone deficiency; AGHD: Adult growth hormone deficiency; CVOT: Cardiovascular outcomes trial; CV: Cardiovascular; PoC: Proof of Concept; NASH: Non-alcoholic steatohepatitis; CN: ChinaNote: EU commission has adopted the CHMP (Committee for Medicinal Products for Human Use) recommendation for the paediatric indication for Victoza®

Phase 1 initiationLAIsema

SOUL4 initiation EU/Japan submission

Phase 1 results

US regulatory decision

Anti-IL-21 Phase 2 results

Tresiba® Phase 3b results(vs glargine U300)

Ozempic® US submission(CV label update)

Somapacitan

PYY 1562

Esperoct®

Tri-agonist 1706

US approval EU approval

Phase 3 initiation (GHD)

US and EU submission(AGHD)

Phase 1 results

Phase 1 results

Concizumab Phase 3 initiation

US submission (CV)US submission

FORTE, FOCUS2 & FLOW3 trial initiation

Fiasp® JP regulatory decision

Japan approval

Semaglutide NASH Phase 2 initiation(PoC, Gilead)

Diabetes Haemophilia Growth disordersObesity Other serious chronic diseases

Amylin - AM833 Phase 2 initiation

PCSK9i Phase 1 initiation

Slide 15

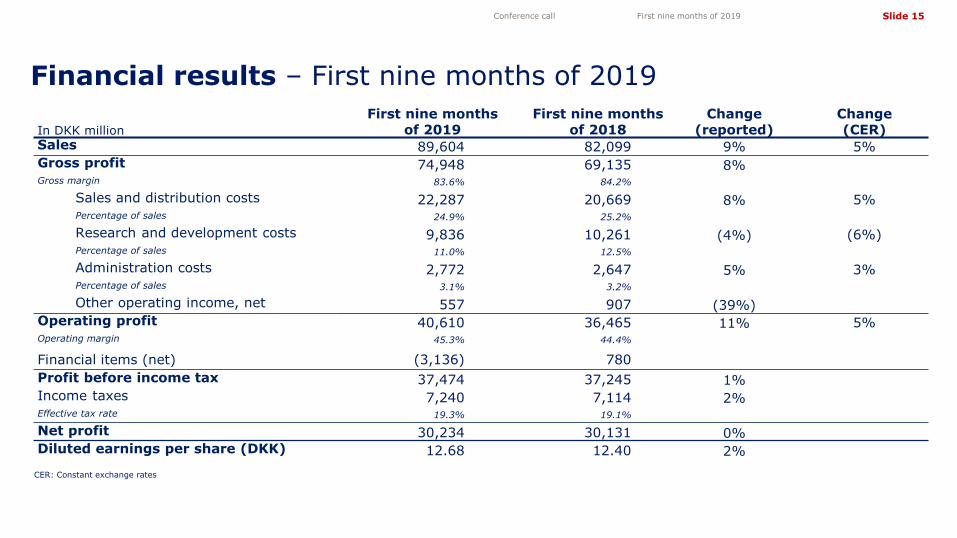

Financial results – First nine months of 2019

Conference call First nine months of 2019

In DKK millionFirst nine months

of 2019First nine months

of 2018Change

(reported)Change(CER)

Sales 89,604 82,099 9% 5%Gross profit 74,948 69,135 8%Gross margin 83.6% 84.2%

Sales and distribution costs 22,287 20,669 8% 5%Percentage of sales 24.9% 25.2%

Research and development costs 9,836 10,261 (4%) (6%)Percentage of sales 11.0% 12.5%

Administration costs 2,772 2,647 5% 3%Percentage of sales 3.1% 3.2%

Other operating income, net 557 907 (39%)Operating profit 40,610 36,465 11% 5%Operating margin 45.3% 44.4%

Financial items (net) (3,136) 780Profit before income tax 37,474 37,245 1%Income taxes 7,240 7,114 2%Effective tax rate 19.3% 19.1%

Net profit 30,234 30,131 0%Diluted earnings per share (DKK) 12.68 12.40 2%

CER: Constant exchange rates

Slide 16

Financial outlook for 2019

The financial outlook is based on an assumption of a continuation of the current business environment and given the current scope of business activities and has been prepared assuming that currency exchange rates remain at the level as of 28 October 2019.CER: Constant exchange rates

Conference call First nine months of 2019

Sales growth – at CER

Sales growth - reported

Operating profit growth – at CER

Operating profit growth - reported

Financial items (net)

Effective tax rate

Capital expenditure

Free cash flow

Depreciation, amortisation and impairment losses

Expectations1 Nov 2019

5% to 6%

4% to 6%

Loss of around DKK 3.9 billion

19% to 21%

Around DKK 9.0 billion

Around DKK 5.5 billion

DKK 31 to 35 billion

Around 3%-points higher

Around 5%-points higher

Expectations9 Aug 2019

4% to 6%

4% to 6%

Loss of around DKK 3.5 billion

20% to 22%

Around DKK 9.0 billion

Around DKK 4.5 billion

DKK 30 to 34 billion

Around 3%-points higher

Around 5%-points higher

Slide 17

Diabetes franchise grew by 4% and Novo Nordisk expands global market leadership to 28.4% (up from 27.6%, YoY)

• Insulin sales decreased by 2% while volume market leader position expanded to 46.5% insulin market share (up from 46.1%)

• GLP-1 sales grew by 20% and Novo Nordisk remains global market leader with 47% value market share. Ozempic®, with sales of DKK 6.9 billion, reached blockbuster status and has now been launched in 24 countries

• Rybelsus®, the first GLP-1 in a tablet, approved in the USA

Sales growth of 5% driven by IO (11% sales growth), partly offset by NAO (1% sales decline)

Operating profit growth of 5% driven by sales performance and continued focus on cost control

Obesity sales increased by 50% driven by IO (+98%) and NAO (+29%) and expanding value market share to 54%. Saxenda®

is now launched in 45 countries

Key take-aways – First nine months of 2019

Conference call First nine months of 2019

Diabetes

Obesity

Note: Sales growth numbers are stated in constant exchange rates. Outlook as of 28 October 2019. IO: International Operations; NAO: North America Operations; YoY: Year on Year

Financials

Biopharm sales increased by 4%, driven by sales growth in International Operations (+6%) and North America Operations (+1%)Biopharm

Sales growth in 2019 is now expected to be 5-6% with a positive currency impact of 3%-points

Operating profit growth in 2019 is expected to be 4-6% with a positive currency impact of 5%-pointsOutlook

Slide 18

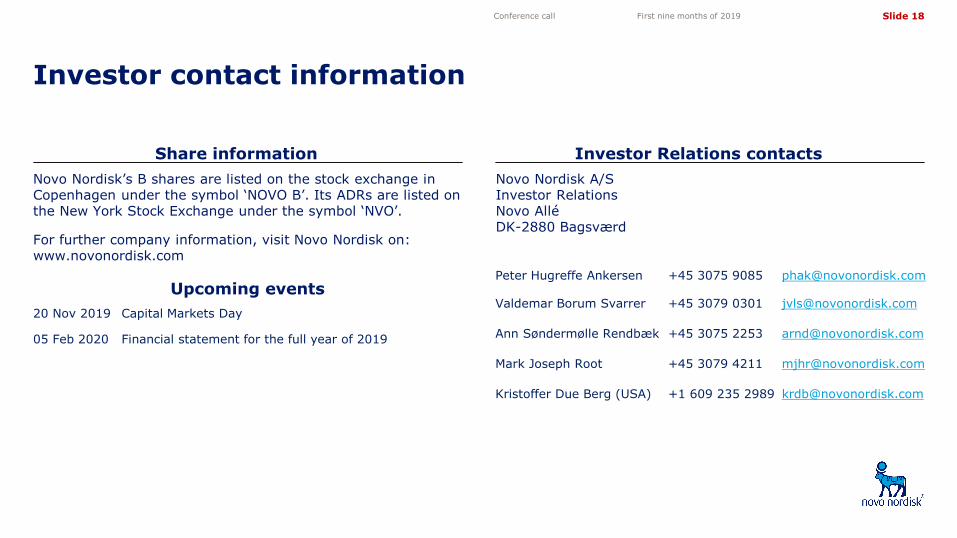

Share information Investor Relations contacts

Investor contact information

Conference call First nine months of 2019

Novo Nordisk’s B shares are listed on the stock exchange in Copenhagen under the symbol ‘NOVO B’. Its ADRs are listed on the New York Stock Exchange under the symbol ‘NVO’.

For further company information, visit Novo Nordisk on: www.novonordisk.com

Peter Hugreffe Ankersen +45 3075 9085 [email protected]

Valdemar Borum Svarrer +45 3079 0301 [email protected]

Ann Søndermølle Rendbæk +45 3075 2253 [email protected]

Mark Joseph Root +45 3079 4211 [email protected]

Kristoffer Due Berg (USA) +1 609 235 2989 [email protected]

Novo Nordisk A/S Investor Relations Novo Allé DK-2880 Bagsværd

Upcoming events20 Nov 2019 Capital Markets Day

05 Feb 2020 Financial statement for the full year of 2019