16

1 Management Presentation Leadership in Metal Processing and Distribution Lourenço Gonçalves Chairman, President and CEO October 2, 2009 NASPD Fall Conference Chicago, IL

| Date post: | 01-Apr-2015 |

| Category: |

Documents |

| Upload: | elisabeth-molde |

| View: | 225 times |

| Download: | 6 times |

CONFIDENTIAL

1

April 11, 2005

Management Presentation

Leadership in Metal Processing and Distribution

Lourenço GonçalvesChairman, President and CEO

October 2, 2009

NASPD Fall Conference

Chicago, IL

CONFIDENTIAL

22

Forward-Looking Statement

Certain statements in this presentation and our response to various questions may constitute “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and applicable Canadian securities law. Such forward-looking statements are based on current expectations and involve certain risks and uncertainties. Actual results might differ materially from those projected in the forward-looking statements. In some cases, information regarding certain important factors that could cause actual results to differ materially from any such forward-looking statements appears or is discussed together with such statements. Additional information concerning factors that could cause actual results to differ materially from those in the forward-looking statements is contained in filings with the Securities and Exchange Commission made by Metals USA, Inc. In particular, the factors described under “Risk Factors” in those filings and other possible factors not listed, could affect our actual results and cause such results to differ materially from those expressed in forward-looking statements.

CONFIDENTIAL

3

The Ups and Downs of the Steel Market

More Ups Than Downs

CONFIDENTIAL

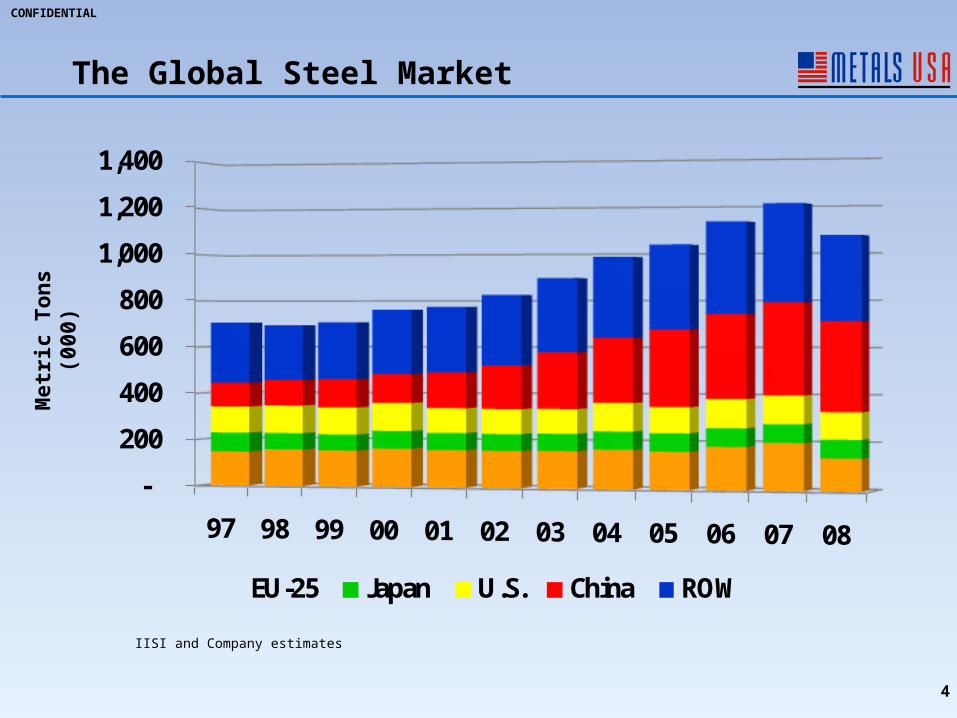

The Global Steel MarketM

etri

c T

on

s (0

00)

4

IISI and Company estimates

-

200

400

600

800

1,000

1,200

1,400

97 98 99 00 01 02 03 04 05 06 07 08

EU-25 Japan U.S. China ROW

CONFIDENTIAL

Global Steel Trade Flows

5

World Steel Dynamics

Steel Net Imports(Million Tonnes Annualized)

2Q07 4Q07 2Q08 4Q08 2Q09

Europe 24 16 15 13 7

N America 17 9 12 17 7

Japan (36) (38) (38) (33) (24)

China (57) (34) (42) (27) 4

CONFIDENTIAL

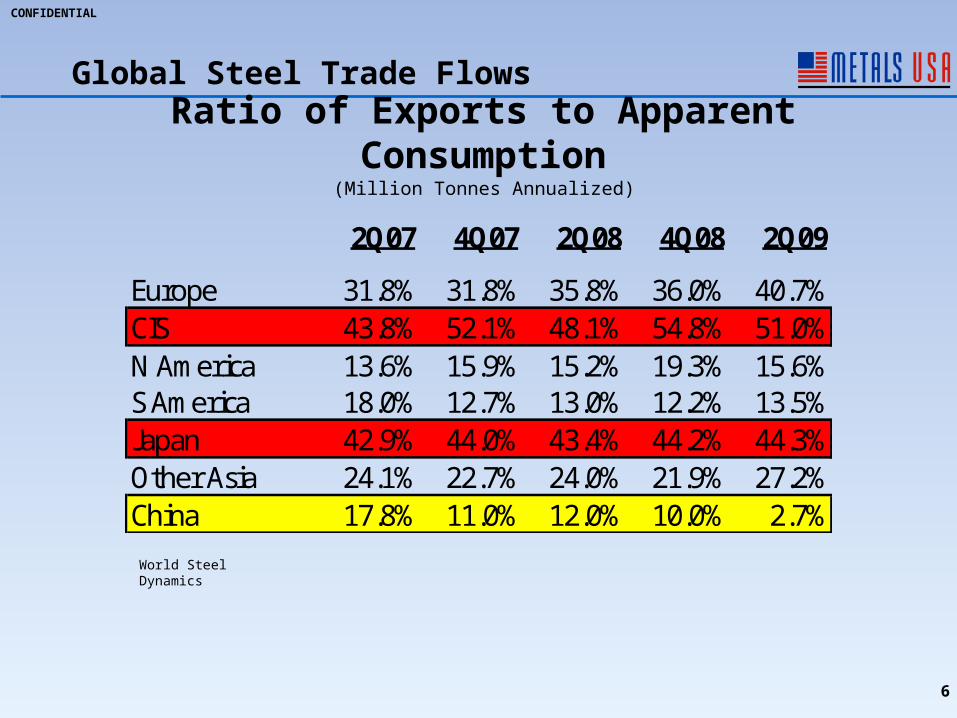

Global Steel Trade Flows

6

World Steel Dynamics

Ratio of Exports to Apparent Consumption(Million Tonnes Annualized)

2Q07 4Q07 2Q08 4Q08 2Q09

Europe 31.8% 31.8% 35.8% 36.0% 40.7%CIS 43.8% 52.1% 48.1% 54.8% 51.0%N America 13.6% 15.9% 15.2% 19.3% 15.6%S America 18.0% 12.7% 13.0% 12.2% 13.5%Japan 42.9% 44.0% 43.4% 44.2% 44.3%Other Asia 24.1% 22.7% 24.0% 21.9% 27.2%China 17.8% 11.0% 12.0% 10.0% 2.7%

CONFIDENTIAL

7

CHINAUS

Different Stimulus FromDifferent Packages

CONFIDENTIAL

US Industrial Production Trend

Source: Federal Reserve

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

50

62

74

86

98

110

122 Ja

n-81

Jul-8

2

Jan-

84

Jul-8

5

Jan-

87

Jul-8

8

Jan-

90

Jul-9

1

Jan-

93

Jul-9

4

Jan-

96

Jul-9

7

Jan-

99

Jul-0

0

Jan-

02

Jul-0

3

Jan-

05

Jul-0

6

Jan-

08

Jul-0

9

YoY Change index

Ind

ex:

200

2 =

100 Y

-o-Y

Ch

ang

e

8

CONFIDENTIAL

9

US Steel Demand Has Changed

Domestic steel consumption’s remarkable resiliency has been shattered

Source: AISI and WSD

0

20

40

60

80

100

120

140

98 99 00 01 02 03 04 05 06 07 08 09e

Mil

lio

n T

on

s

Production Consumption

CONFIDENTIAL

10

US Mills

The Good:

World class cost structures

Consolidation has allowed some rationalization

Located in the heart of the most sustaining economy in the world

The Bad:

Distracted by defensive focus

Still reacting the old-fashioned way (reducing prices)

Not looking forward or prepared for the next cycle

CONFIDENTIAL

11

US Mills

The Good:

World class cost structures

Consolidation has allowed some rationalization

Located in the heart of the most sustaining economy in the world

The Bad:

Distracted by defensive focus

Still reacting the old-fashioned way (reducing prices)

Not looking forward or prepared for the next cycle

The US Steel Industry must grow steel consumption

CONFIDENTIAL

12

The Most Protected Market In The World

Special interests and trade lawyers are major contributors

Anti-dumping

Countervailing Duties

Section 201

Section 232

Section 421

The Weak Dollar

CONFIDENTIAL

13

The Most Protected Market In The World

Special interests and trade lawyers are major contributors

Anti-dumping

Countervailing Duties

Section 201

Section 232

Section 421

The Weak Dollar

An Effective Barrier To Imports

CONFIDENTIAL

14

Macro Economic Conditions Setting The Tone

Banks still not lending as before

For the majority – tomorrow looks worse than today

As a result:

Capital markets not fully recovered

Employment levels still weak

Businesses and individuals deleveraging

No capital spending

No construction

CONFIDENTIAL

15

My View:

Current conditions are unsustainable

Smart Investors will eventually perceive value and return to market

US Government stimulus yet to be realized – must be realized

Unless we assume that the US has changed for good, we should conclude that demand will grow in 2010 and beyond

CONFIDENTIAL

16