14

Considering a Health Savings Account (HSA)?

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | rosemary-jacobs |

| View: | 223 times |

| Download: | 0 times |

Considering a Health Savings Account (HSA)?

What is a Health Savings Account-HSA?

http://youtu.be/GTHQ04IAPLI

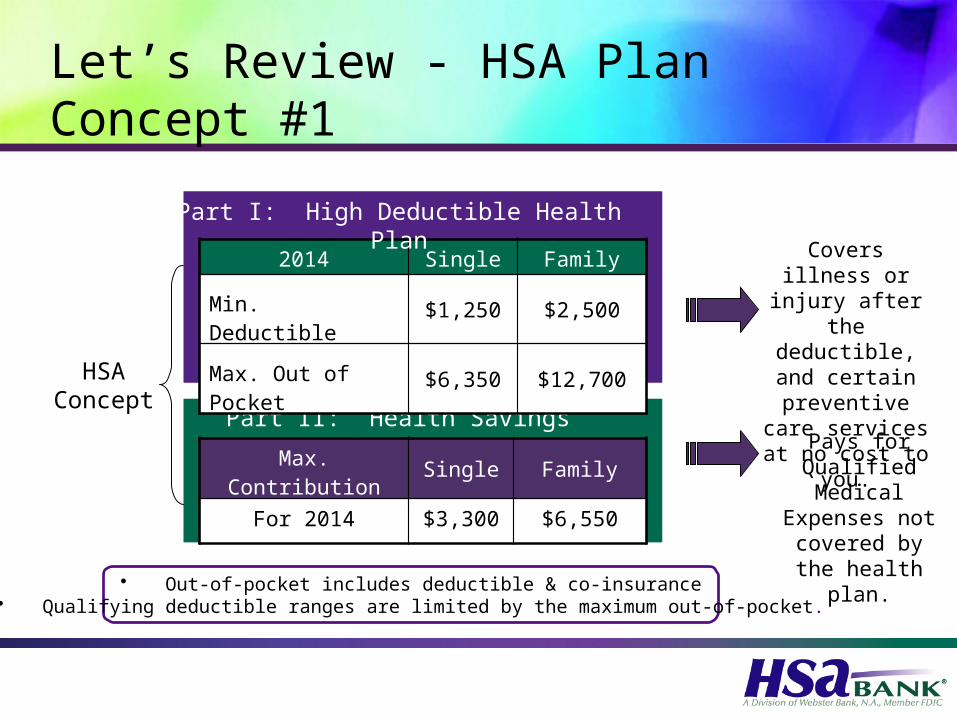

Let’s Review - HSA Plan Concept #1

Part II: Health Savings Account

HSA Concept

Covers illness or injury after

the deductible, and certain

preventive care services at no cost to you.

Pays for Qualified Medical

Expenses not covered by the

health plan.• Out-of-pocket includes deductible & co-insurance• Qualifying deductible ranges are limited by the maximum out-of-pocket.

2014 Single Family

Min. Deductible $1,250 $2,500

Max. Out of Pocket

$6,350 $12,700

Part I: High Deductible Health Plan

Max. Contribution Single Family

For 2014 $3,300 $6,550

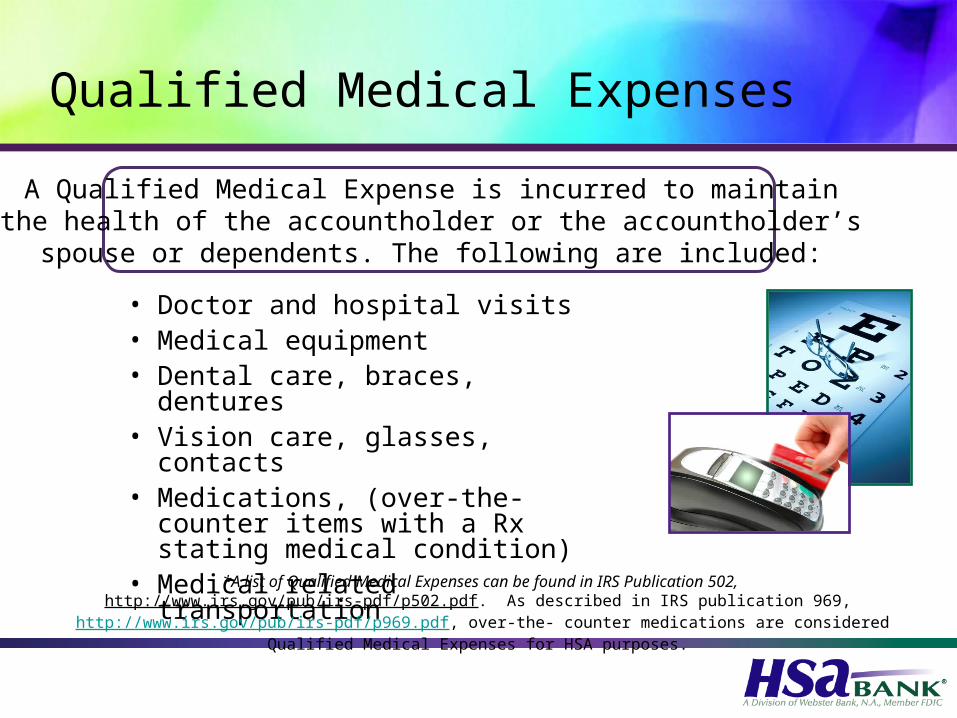

Qualified Medical Expenses

• Doctor and hospital visits• Medical equipment• Dental care, braces, dentures• Vision care, glasses, contacts• Medications, (over-the-counter

items with a Rx stating medical condition)

• Medical related transportation

*A list of Qualified Medical Expenses can be found in IRS Publication 502, http://www.irs.gov/pub/irs-pdf/p502.pdf. As described in IRS publication 969,

http://www.irs.gov/pub/irs-pdf/p969.pdf, over-the- counter medications are considered Qualified Medical Expenses for HSA purposes.

A Qualified Medical Expense is incurred to maintain the health of the accountholder or the accountholder’s

spouse or dependents. The following are included:

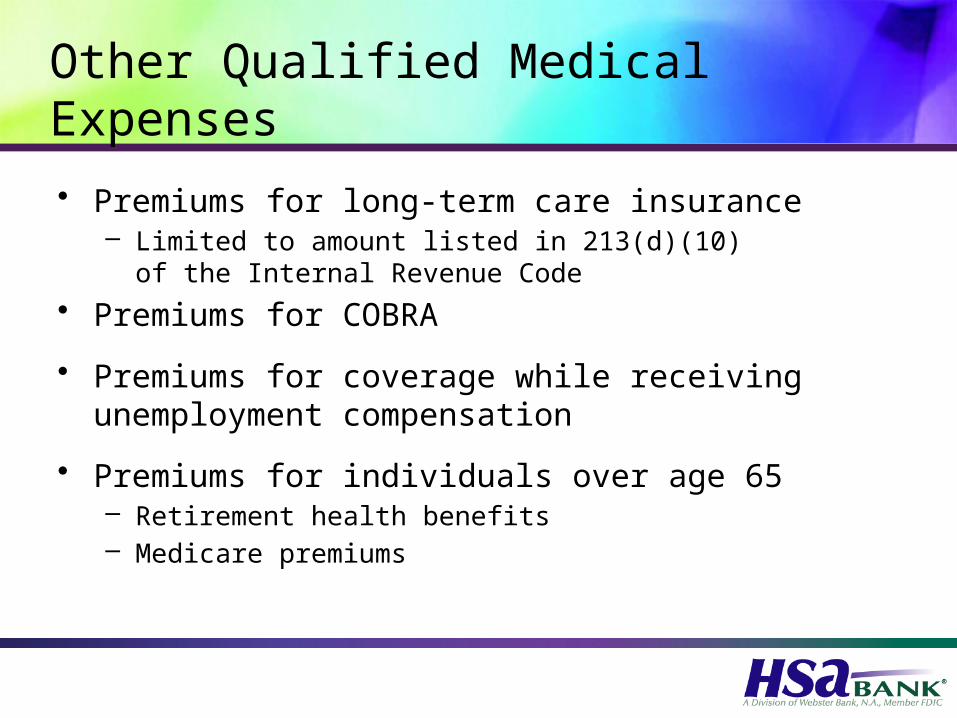

Other Qualified Medical Expenses

• Premiums for long-term care insurance– Limited to amount listed in 213(d)(10)

of the Internal Revenue Code• Premiums for COBRA

• Premiums for coverage while receiving unemployment compensation

• Premiums for individuals over age 65 – Retirement health benefits– Medicare premiums

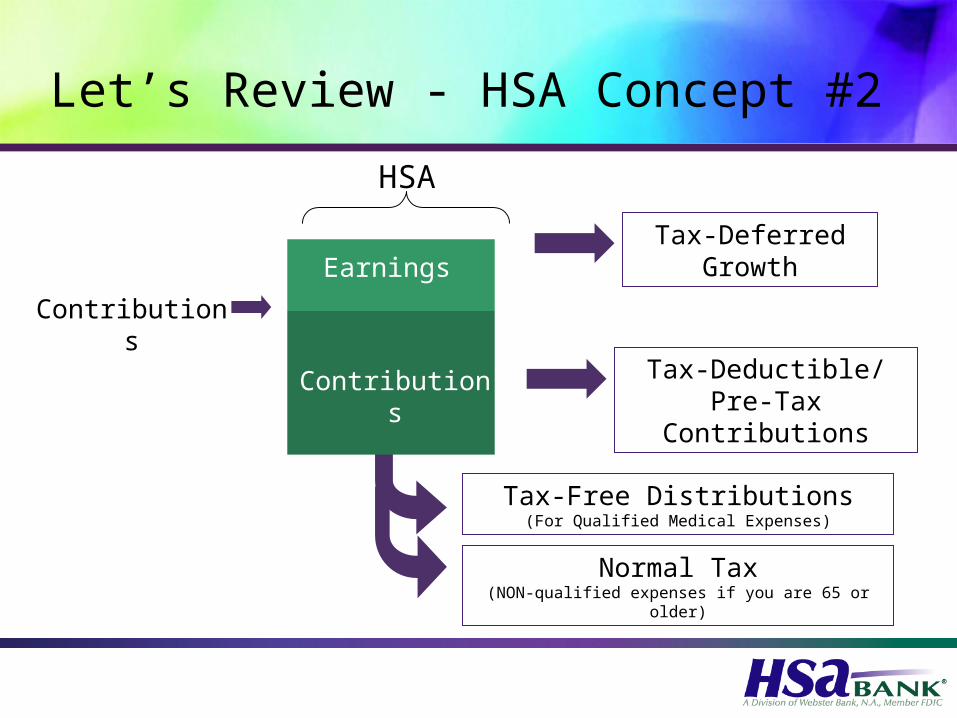

Let’s Review - HSA Concept #2

Contributions

Contributions

EarningsTax-Deferred

Growth

Tax-Deductible/ Pre-Tax Contributions

Tax-Free Distributions(For Qualified Medical Expenses)

HSA

Normal Tax(NON-qualified expenses if you are 65 or older)

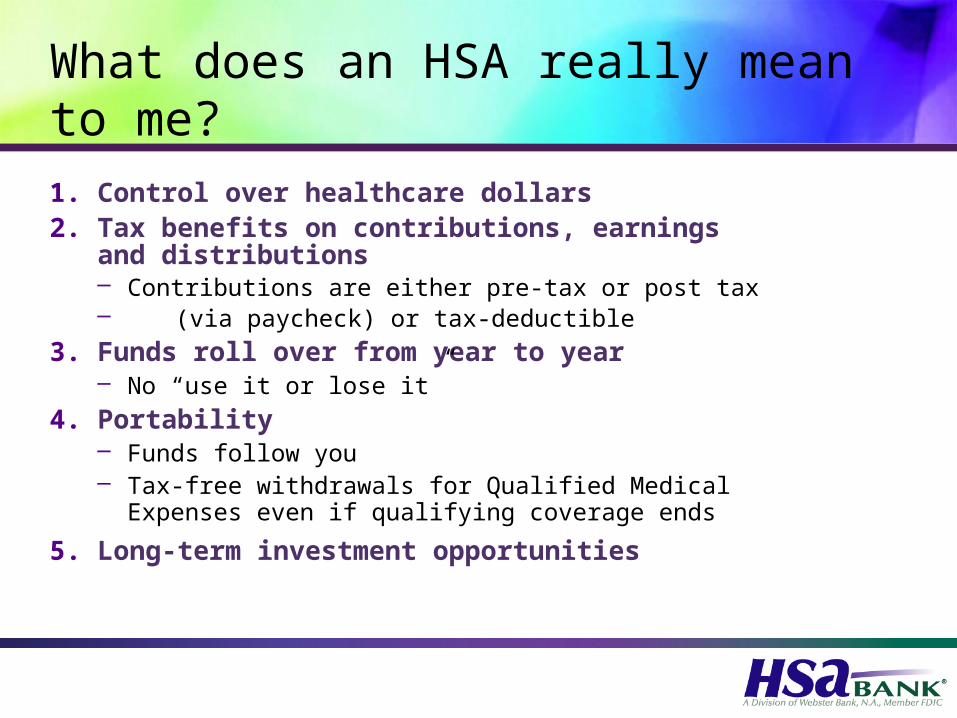

What does an HSA really mean to me?1. Control over healthcare dollars2. Tax benefits on contributions, earnings and

distributions– Contributions are either pre-tax or post tax– (via paycheck) or tax-deductible

3. Funds roll over from year to year– No “use it or lose it”

4. Portability– Funds follow you – Tax-free withdrawals for Qualified Medical Expenses

even if qualifying coverage ends

5. Long-term investment opportunities

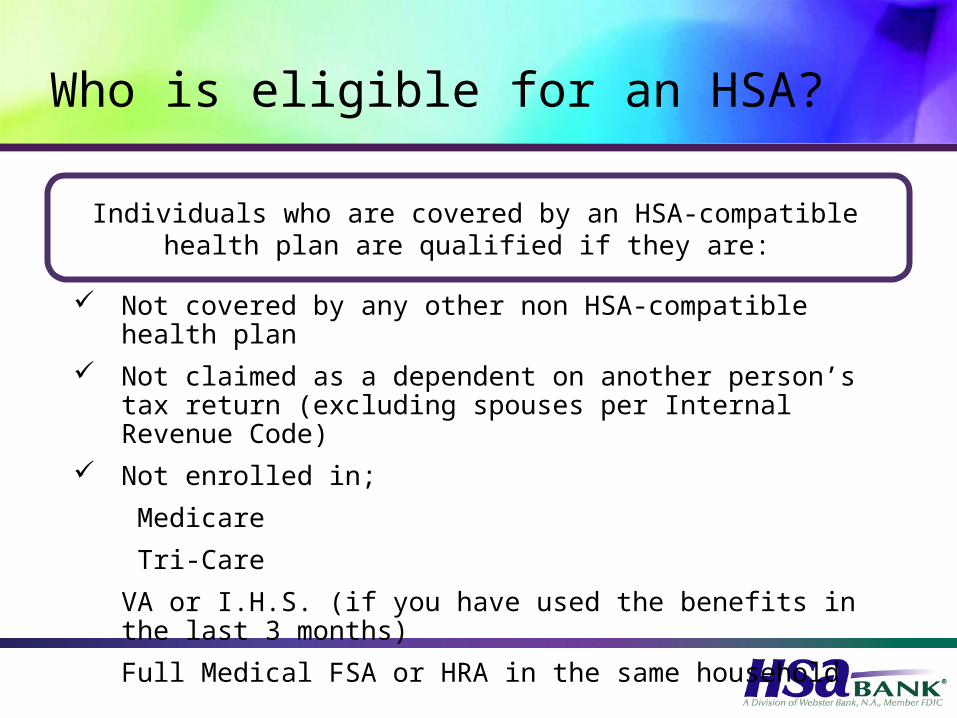

Who is eligible for an HSA?

Not covered by any other non HSA-compatible health plan Not claimed as a dependent on another person’s tax

return (excluding spouses per Internal Revenue Code) Not enrolled in;

Medicare

Tri-Care

VA or I.H.S. (if you have used the benefits in the last 3 months)

Full Medical FSA or HRA in the same household

Individuals who are covered by an HSA-compatible health plan are qualified if they are:

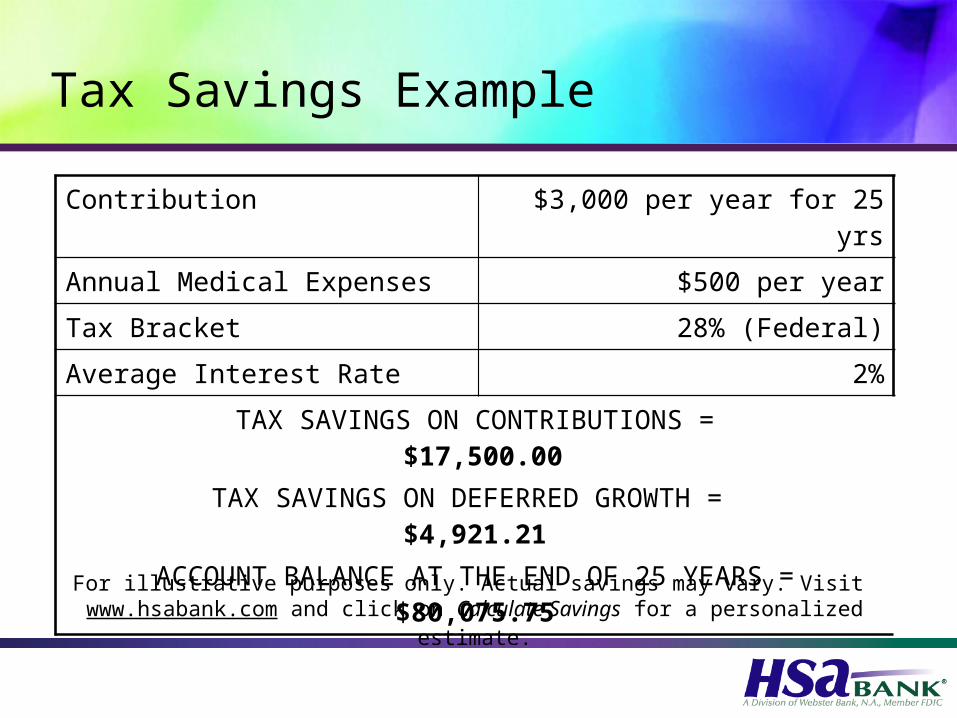

Tax Savings Example

Contribution $3,000 per year for 25 yrs

Annual Medical Expenses $500 per year

Tax Bracket 28% (Federal)

Average Interest Rate 2%

TAX SAVINGS ON CONTRIBUTIONS = $17,500.00

TAX SAVINGS ON DEFERRED GROWTH = $4,921.21

ACCOUNT BALANCE AT THE END OF 25 YEARS =$80,075.75

For illustrative purposes only. Actual savings may vary. Visit www.hsabank.com and click on Calculate Savings for a personalized

estimate.

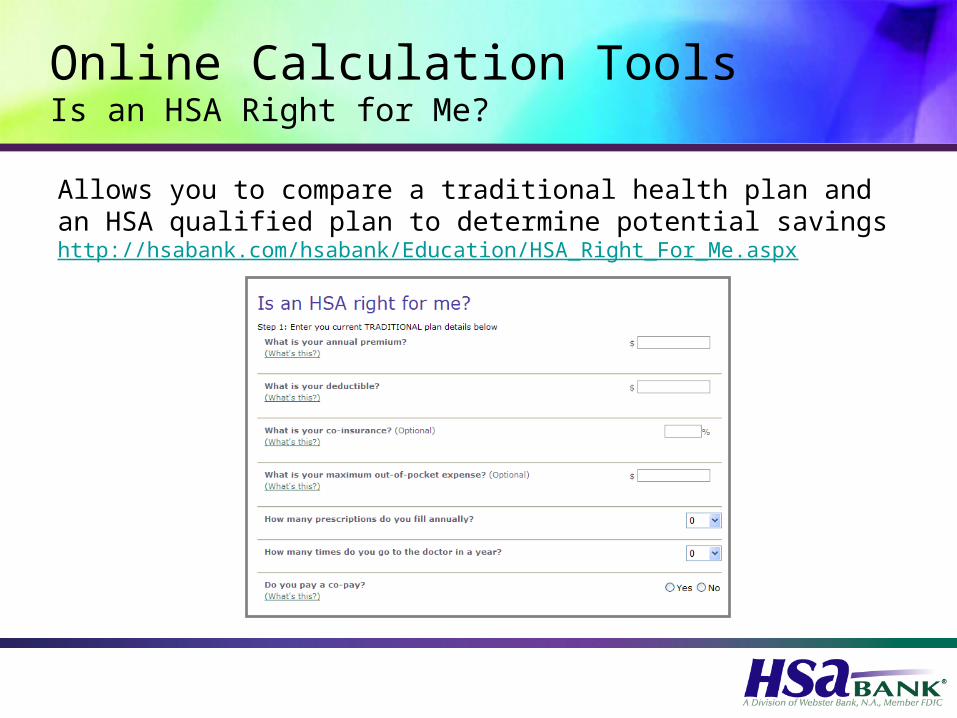

Online Calculation ToolsIs an HSA Right for Me?

Allows you to compare a traditional health plan and an HSA qualified plan to determine potential savings http://hsabank.com/hsabank/Education/HSA_Right_For_Me.aspx

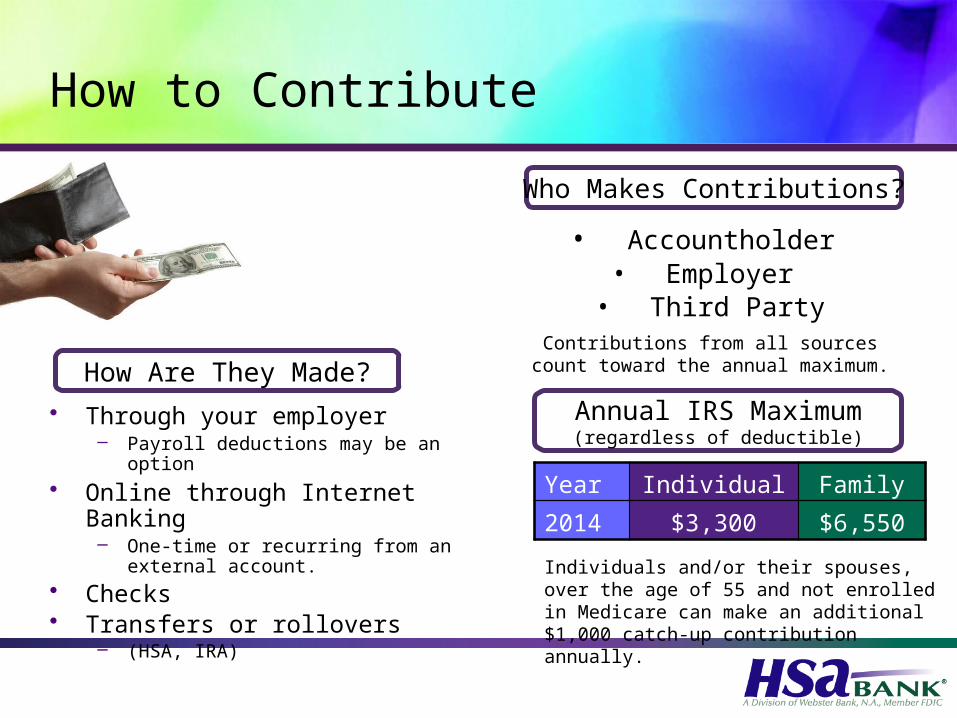

How to Contribute

• Through your employer– Payroll deductions may be an option

• Online through Internet Banking– One-time or recurring from an

external account.• Checks• Transfers or rollovers

– (HSA, IRA)

• Accountholder • Employer • Third Party

Contributions from all sources count toward the annual maximum. How Are They Made?

Who Makes Contributions?

Year Individual Family

2014 $3,300 $6,550

Annual IRS Maximum(regardless of deductible)

Individuals and/or their spouses, over the age of 55 and not enrolled in Medicare can make an additional $1,000 catch-up contribution annually.

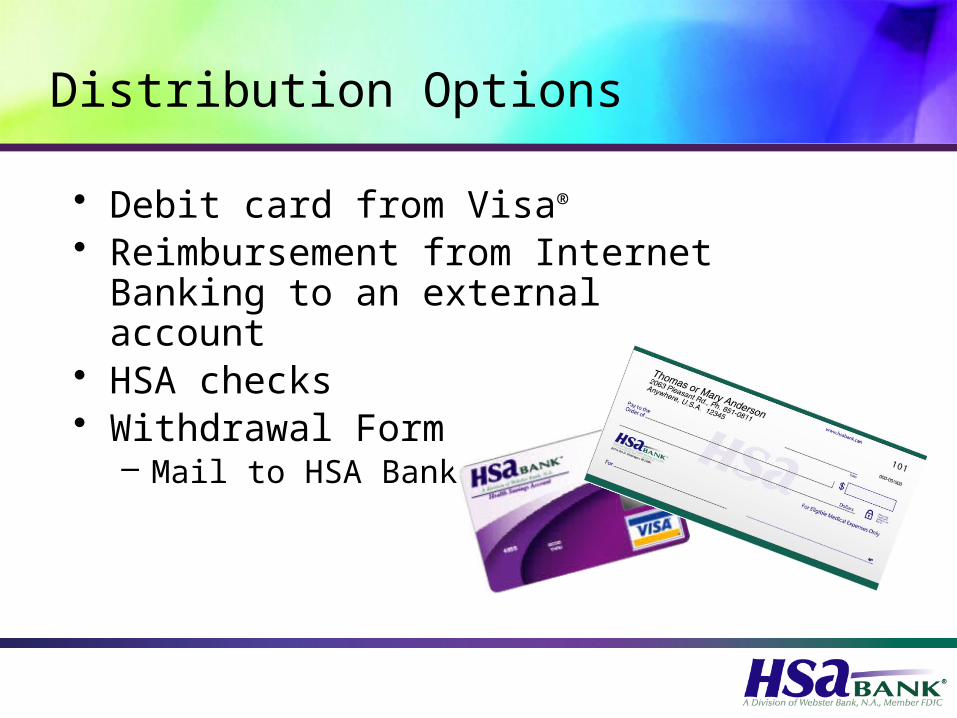

Distribution Options

• Debit card from Visa®

• Reimbursement from Internet Banking to an external account

• HSA checks• Withdrawal Form

– Mail to HSA Bank

Investment Options

HSA Bank offers a unique opportunity to invest HSA funds in self-directed investment accounts. HSA Bank offers: • TD AMERITRADE investment accounts • Mutual Fund Selection investment accounts

**Investment products are not FDIC insured, are not a deposit or other obligation of or guaranteed by the bank, and are subject to investment risks including possible loss of

principal amount invested.

Service and Support

• Toll-free Bankline24-hour account access via touch tone phone(800)-565-3512

• Toll-free Client Assistance Center (800) 357-6246

7 a.m. – 9 p.m., CT, Monday – Friday

• Toll-free Spanish Language Assistance Line (866) 357-6232 7 a.m. – 9 p.m., CT, Monday – Friday