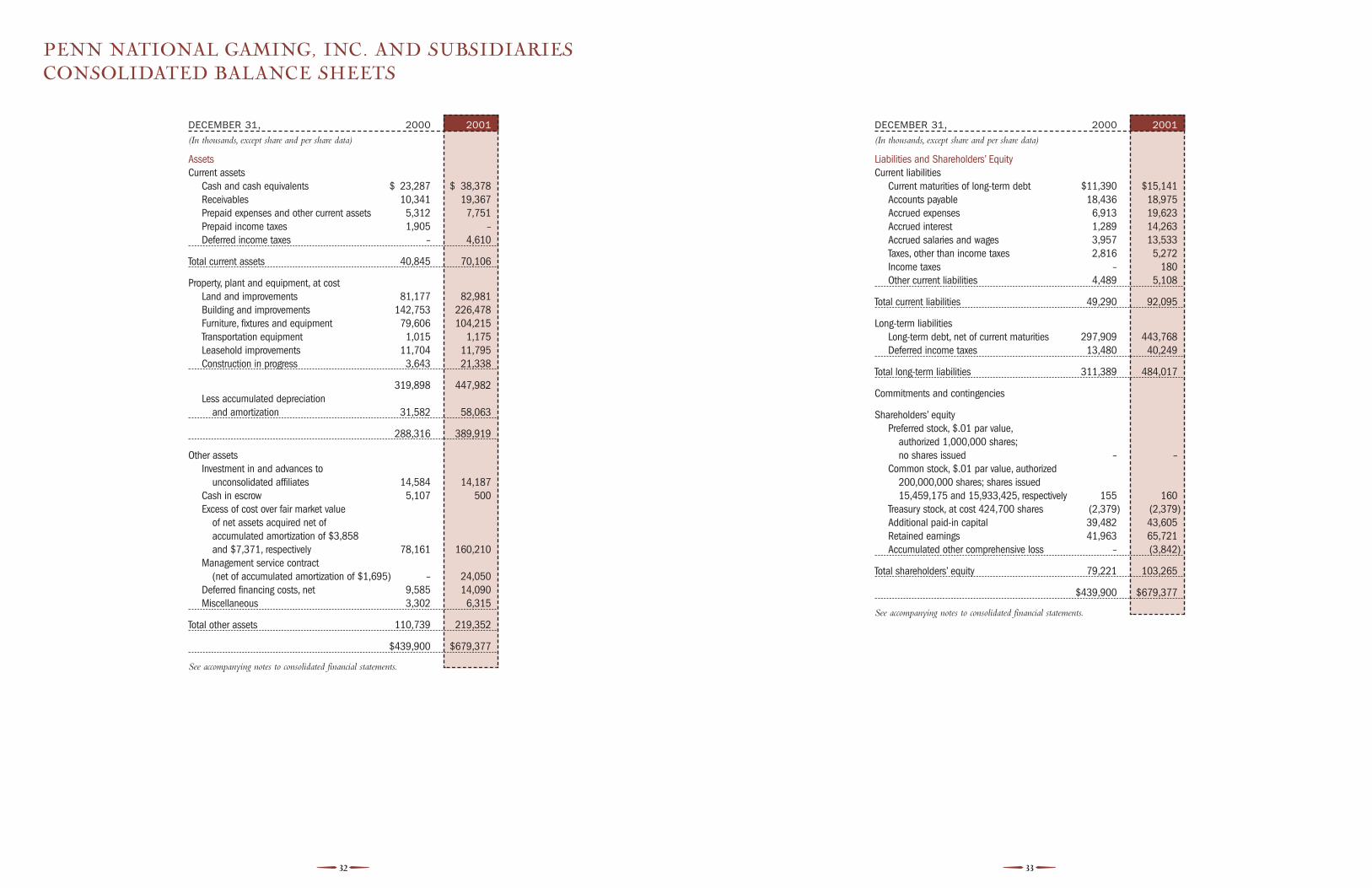

31

COVER

l e t ’s e m bar k on an adve nture . . .

and visit each of Penn National Gaming’s properties.

penn nat ional gaming has be en onan adventure of its own in recent years – operating in a

period of acquisition that has allowed the company to

become a leader in the gaming and entertainment industry.

our travels will take us to west virginia,Louisiana, Mississippi, Pennsylvania, New Jersey, Ontario

and Colorado. Let’s get started!

PENN NATIONAL GAMING

Consolidated Financial Highlights 2

The Year in Review 4

All About Us 6

Financial Information 15

YEAR ENDED DECEMBER 31, 1999 2000 2001

(In thousands, except per share data)

Income statement dataTotal revenues $170,360 $291,801 $519,392Income from operations 17,665 45,120 77,712Income before extraordinary item 6,733 18,575 23,758Net income 6,733 11,992 23,758

Per share dataBasic

Income before extraordinary item $.45 $1.24 $1.55Net income .45 .80 $1.55

DilutedIncome before extraordinary item .44 1.20 1.49Net income .44 .78 1.49

Weighted shares outstandingBasic 14,837 14,968 15,327Diluted 15,196 15,443 15,918

Balance data sheetCash $ 9,434 $ 23,287 $ 38,378Total assets 189,712 439,900 679,377Total debt 91,213 309,299 458,909Shareholders’ equity 66,272 79,221 103,265

EBITDA 26,496 59,481 112,336

TOTAL REVENUES (IN MILLIONS)

$0

$25

$50

$75

$10

0$

125

$15

0$

175

$20

0$

225

$25

0$

275

$30

0$

325

$35

0$

375

$40

0$

425

$45

0$

475

$50

0$

525

$55

0$

575

1999

2000

2001

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85

$90

$95

$10

0$

105

$11

0$

115

1999

2000

2001

$.0

0$

.10

$.2

0$

.30

$.4

0$

.50

$.6

0$

.70

$.8

0$

.90

$1.

00$

1.10

$1.

20$

1.30

$1.

40$

1.50

$1.

60$

1.70

$1.

80$

1.90

$2.

00$

2.10

$2.

20$

2.30

1999

2000

2001

EBITDA (IN MILLIONS)*

DILUTED EARNINGS PER SHARE BEFORE EXTRAORDINARY ITEM

CONSOLIDATED FINANCIAL HIGHLIGHTS

32

* Earnings before interest, taxes, depreciation and amortization (EBITDA)

54

This May we expect to open a new 1,500 space parking

facility at Charles Town which is an important element

in this facility’s overall expansion plan.We have also

commenced construction of nearly 100,000 square feet

of new gaming, restaurant, entertainment, and back-of-

house facilities at Charles Town that will open in two phases

through 2002. Following the parking facility opening in

May, the first phase of the casino expansion will open this

Summer – along with the placement of an additional 500

slot machines – with the balance of the facility completed

by December.Throughout 2003 we have been authorized

by the West Virginia Lottery Commission to place an

additional 1,000 new gaming machines at Charles Town,

so by year-end 2003, we will operate 75% more gaming

devices at Charles Town than we do at present.As a result

of these expansion plans we expect to see considerable

growth at Charles Town in 2002, 2003, and beyond.

FINANCING GROWTHEarly in 2002, Penn National raised approximately $270

million through the issuance of stock and bonds.This

new capital was used to repay indebtedness – which was

incurred as a result of our expansion – under our existing

credit facilities. By reducing debt, we gained the flexibility

to finance other expansion opportunities that we may

identify that meet our criteria for financial and strategic

growth. Importantly, these financings significantly improved

Penn National’s credit statistics and at present, we have

one of the best credit profiles in the gaming industry.

MANAGEMENTGaming properties are highly management intensive and

require strong leadership to remain competitive with

surrounding properties. In 2001 we strengthened our

team, both at the corporate and property level with very

good results.We expect a few additions to our management

in 2002, which should complete our outstanding corporate

and property management teams. Penn National now

possesses one of the strongest management teams in the

gaming industry in terms of the depth of our operational

and financial experience.

With our portfolio of diversified gaming assets, expansion

plans at key properties, financial flexibility to support

further growth and a corporate and property level

management team capable of deriving the potential from

our growing asset base, we are on track in 2002 to exceed

the tremendous results of 2001.

DEAR SHAREHOLDERSWe are pleased to report that 2001 was another record

year financially for Penn National and that we were

successful in our ongoing efforts to further build and

diversify our gaming operations.The acquisition early in

the second quarter of 2001 of Casino Rouge, a riverboat

gaming facility in Baton Rouge, Louisiana, and the man-

agement contract for Casino Rama, a large, successful

gaming facility located approximately 90 miles north

of Toronto, has extended Penn National’s transformation

into a slot-driven regional gaming company from a 100%

pari-mutuel racing operator at the time of our 1994 initial

public offering. Our expansion initiatives of the past several

years positioned us to overcome national and regional

horse racing declines and about 81% of our record 2001

revenues and 85% of our record 2001 EBITDA was

derived from gaming operations, with the balance coming

from racing.

The second half of 2001 highlighted the strength of our

operations and acquisition growth strategy as each of the

four gaming properties or contracts acquired since 2000

generated revenues and EBITDA ahead of the 2000 levels.

We entered 2002 with solid prospects for further growth

from owned and managed assets and continue to seek

acquisition opportunities which meet our financial and

strategic criteria for growth.

2002 PROPERTY EXPANSION In the second quarter of 2002, we will complete the

Casino Magic Bay St. Louis property expansion which

includes a new 300 room hotel adjacent to the casino.

In addition to the hotel, this $37 million project includes

significant improvements to the casino floor and our

entertainment facilities including a variety of restaurants,

a spa and 10,000 square feet of conference space - all the

amenities necessary to make Casino Magic an outstanding

regional overnight destination and one of the most complete

resorts in the region.

THE YEAR IN REVIEW

WITH OUR PORTFOLIO OF DIVERSIFIED GAMINGASSETS, EXPANSION PLANS AT KEY PROPERTIES,FINANCIAL FLEXIBILITY TO SUPPORT FURTHERGROWTH AND A CORPORATE AND PROPERTY

LEVEL MANAGEMENT TEAM CAPABLE OF DERIVINGTHE POTENTIAL FROM OUR GROWING ASSET BASE,WE ARE ON TRACK IN 2002 TO EXCEED THETREMENDOUS RESULTS OF 2001.

Peter M. Carlino

Chairman of the Board & Chief Executive Officer

March 31, 2002

Kevin DeSanctis

President & Chief Operating Officer

BATON ROUGE

there ’s much moreto Baton Rouge than the

state capital – it’s the home

of Casino Rouge, the city’s

premier gaming hot spot.

Nothing is better than being

on a riverboat – especially at

night. And with over 1,000

slot machines and 38 table

games, not to mention live

entertainment and a number

of dining choices, there’s

always something to do!

located in the eastern panhandle near historic harper’s ferry,Charles Town Races is nestled in the quaint town of Charles Town, West

Virginia. But there’s nothing quaint about Charles Town Races – it’s a complete

entertainment complex that offers both coin-in, coin-out and video slots, live

and simulcast horseracing, live entertainment and a variety of dining options.

CHARLES TOWN

6 7

WEST VIRGINIA

LOUISIANA

penn national has twice the excitementin this gulf state!

cas ino mag ic, in bay st. louis ,is the only all-inclusive resort on the Mississippi

Gulf Coast.Along with all the slots, table games,

entertainment and food you’d expect at a Penn

National facility, this property features an 18-hole

Arnold Palmer golf course at the Bridges Golf

Resort, an RV park with all the amenities and

a 200-room hotel. Wait, there’s more – opening

in May 2002 – a brand new hotel tower with

300 additional guest rooms.

situated along mississippi’s historicback bay in Biloxi, Boomtown Casino boasts

a western theme that’s a real crowd pleaser.

Plus, the Family Fun Center features a motion

theater ride and arcade games for the kids.

BAY ST. LOUIS

BILOXI

MISSISSIPPI

8 9

for penn national gaming, pennsylvania represents the roots of the company. And these roots

mean horseracing.

penn national race course, a thoroughbredracetrack in Grantville, has been one of the industry leaders

for nearly thirty years. Penn National features year-round

thoroughbred racing that is simulcast to racetracks around

the country.

fans in wilkes-barre have known the excitementof live harness racing for over thirty-five years – thanks to

The Downs at Pocono.This venerable racetrack features live

racing eight months of the year and simulcast racing year-round.

both racetracks offer simulcast racingfrom thoroughbred and harness venues around the country.

The same simulcast offerings can be found at one of the

eleven off-track wagering facilities found in Allentown,

Carbondale, Chambersburg, East Stroudsburg, Erie, Hazleton,

Johnstown, Lancaster, Reading,Williamsport and York.

ERIE

JOHNSTOWN

CHAMBERSBURGYORK

LANCASTER

READINGGRANTVILLE

WILLIAMSPORT

HAZELTON

WILKES-BARRE

CARBONDALE

E.STROUDSBURG

10 11

boasting the nation’s oldest and fastest daytimehalf-mile harness racetrack, Freehold Raceway has achieved

legendary status among horseplayers over the years. With live

racing ten months of the year, the track also features simulcast

racing from domestic tracks seven days a week, 52 weeks a year.

FREEHOLD

ORILLIA

ONTARIO

in the land of ice and snow lies another hot spot that is managed by Penn National Gaming.

Casino Rama, just north of Toronto, is an entertainment complex beyond

compare.With over 2,100 slot machines, 122 gaming tables, seven restaurants

and a state-of-the-art 5,000 seat Entertainment Centre for concerts, theatrical

productions and sporting events, there’s never a lack of excitement.

13

NEW JERSEY

12

BLACK HAWK

oh, the wild west!

in august 2001, penn national agreed to acquireBullwhackers Casino, the adjoining Bullpen Sports Casino and the Silver

Saloon and Casino.With its prime location near both downtown Denver and

Colorado’s finest ski resorts, its Rocky Mountain locale draws many visitors.

The anticipated closing of this transaction is the second quarter of 2002.

Selected Consolidated Financial and Operating Data 16

18Management’s Discussion and Analysis of Financial Condition and Results of Operations

Consolidated Financial Statements 32

Summary of Significant Accounting Policies 38

Acquisitions 41

Long-Term Debt 43

Commitments and Contingencies 45

Income Taxes 48

Supplemental Disclosures of Cash Flow Information 49

Stock Based Compensation 49

Shareholder Rights Plan 52

Segment Information 53

Summarized Quarterly Data (Unaudited) 54

Pending Acquisition 54

Subsequent Events 55

Report of Independent Certified Public Accountants 55

COLORADO

14 15

17

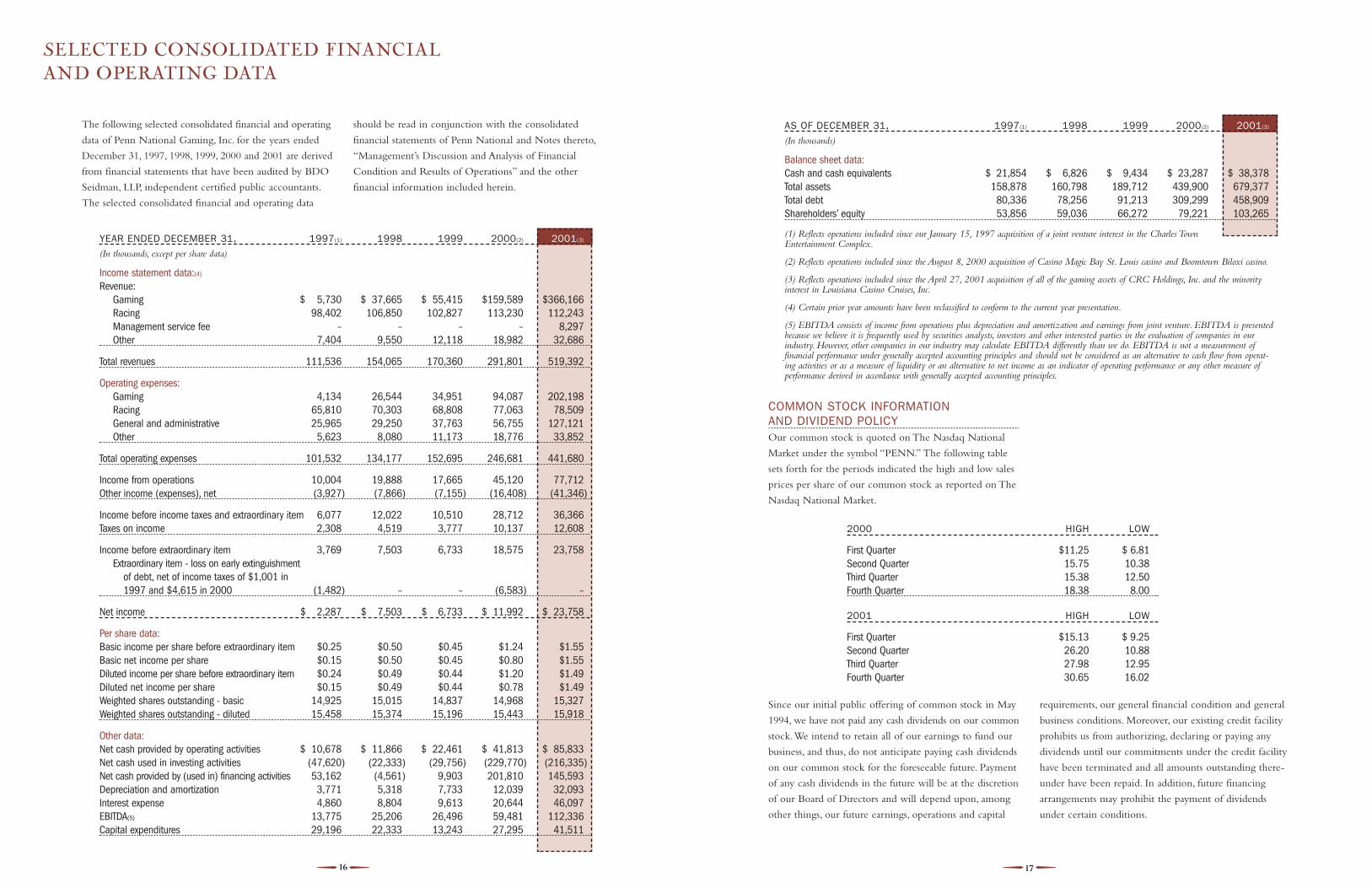

COMMON STOCK INFORMATION AND DIVIDEND POLICYOur common stock is quoted on The Nasdaq National

Market under the symbol “PENN.” The following table

sets forth for the periods indicated the high and low sales

prices per share of our common stock as reported on The

Nasdaq National Market.

Since our initial public offering of common stock in May

1994, we have not paid any cash dividends on our common

stock.We intend to retain all of our earnings to fund our

business, and thus, do not anticipate paying cash dividends

on our common stock for the foreseeable future. Payment

of any cash dividends in the future will be at the discretion

of our Board of Directors and will depend upon, among

other things, our future earnings, operations and capital

requirements, our general financial condition and general

business conditions. Moreover, our existing credit facility

prohibits us from authorizing, declaring or paying any

dividends until our commitments under the credit facility

have been terminated and all amounts outstanding there-

under have been repaid. In addition, future financing

arrangements may prohibit the payment of dividends

under certain conditions.

16

The following selected consolidated financial and operating

data of Penn National Gaming, Inc. for the years ended

December 31, 1997, 1998, 1999, 2000 and 2001 are derived

from financial statements that have been audited by BDO

Seidman, LLP, independent certified public accountants.

The selected consolidated financial and operating data

should be read in conjunction with the consolidated

financial statements of Penn National and Notes thereto,

“Management’s Discussion and Analysis of Financial

Condition and Results of Operations” and the other

financial information included herein.

SELECTED CONSOLIDATED FINANCIAL AND OPERATING DATA

YEAR ENDED DECEMBER 31, 1997(1) 1998 1999 2000(2) 2001(3)

(In thousands, except per share data)

Income statement data:(4)

Revenue:Gaming $ 5,730 $ 37,665 $ 55,415 $159,589 $366,166Racing 98,402 106,850 102,827 113,230 112,243Management service fee – – – – 8,297Other 7,404 9,550 12,118 18,982 32,686

Total revenues 111,536 154,065 170,360 291,801 519,392

Operating expenses:Gaming 4,134 26,544 34,951 94,087 202,198Racing 65,810 70,303 68,808 77,063 78,509General and administrative 25,965 29,250 37,763 56,755 127,121Other 5,623 8,080 11,173 18,776 33,852

Total operating expenses 101,532 134,177 152,695 246,681 441,680

Income from operations 10,004 19,888 17,665 45,120 77,712Other income (expenses), net (3,927) (7,866) (7,155) (16,408) (41,346)

Income before income taxes and extraordinary item 6,077 12,022 10,510 28,712 36,366Taxes on income 2,308 4,519 3,777 10,137 12,608

Income before extraordinary item 3,769 7,503 6,733 18,575 23,758Extraordinary item - loss on early extinguishment

of debt, net of income taxes of $1,001 in 1997 and $4,615 in 2000 (1,482) – – (6,583) –

Net income $ 2,287 $ 7,503 $ 6,733 $ 11,992 $ 23,758

Per share data:Basic income per share before extraordinary item $0.25 $0.50 $0.45 $1.24 $1.55Basic net income per share $0.15 $0.50 $0.45 $0.80 $1.55Diluted income per share before extraordinary item $0.24 $0.49 $0.44 $1.20 $1.49Diluted net income per share $0.15 $0.49 $0.44 $0.78 $1.49Weighted shares outstanding - basic 14,925 15,015 14,837 14,968 15,327Weighted shares outstanding - diluted 15,458 15,374 15,196 15,443 15,918

Other data:Net cash provided by operating activities $ 10,678 $ 11,866 $ 22,461 $ 41,813 $ 85,833Net cash used in investing activities (47,620) (22,333) (29,756) (229,770) (216,335)Net cash provided by (used in) financing activities 53,162 (4,561) 9,903 201,810 145,593Depreciation and amortization 3,771 5,318 7,733 12,039 32,093Interest expense 4,860 8,804 9,613 20,644 46,097EBITDA(5) 13,775 25,206 26,496 59,481 112,336Capital expenditures 29,196 22,333 13,243 27,295 41,511

AS OF DECEMBER 31, 1997(1) 1998 1999 2000(2) 2001(3)

(In thousands)

Balance sheet data:Cash and cash equivalents $ 21,854 $ 6,826 $ 9,434 $ 23,287 $ 38,378Total assets 158,878 160,798 189,712 439,900 679,377Total debt 80,336 78,256 91,213 309,299 458,909Shareholders’ equity 53,856 59,036 66,272 79,221 103,265

(1) Reflects operations included since our January 15, 1997 acquisition of a joint venture interest in the Charles Town Entertainment Complex.

(2) Reflects operations included since the August 8, 2000 acquisition of Casino Magic Bay St. Louis casino and Boomtown Biloxi casino.

(3) Reflects operations included since the April 27, 2001 acquisition of all of the gaming assets of CRC Holdings, Inc. and the minority interest in Louisiana Casino Cruises, Inc.

(4) Certain prior year amounts have been reclassified to conform to the current year presentation.

(5) EBITDA consists of income from operations plus depreciation and amortization and earnings from joint venture. EBITDA is presentedbecause we believe it is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in ourindustry. However, other companies in our industry may calculate EBITDA differently than we do. EBITDA is not a measurement offinancial performance under generally accepted accounting principles and should not be considered as an alternative to cash flow from operat-ing activities or as a measure of liquidity or an alternative to net income as an indicator of operating performance or any other measure ofperformance derived in accordance with generally accepted accounting principles.

2000 HIGH LOW

First Quarter $11.25 $ 6.81Second Quarter 15.75 10.38Third Quarter 15.38 12.50Fourth Quarter 18.38 8.00

2001 HIGH LOW

First Quarter $15.13 $ 9.25Second Quarter 26.20 10.88Third Quarter 27.98 12.95Fourth Quarter 30.65 16.02

1918

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

OVERVIEWWe derive substantially all of our revenues from gaming

and pari-mutuel operations. Since September 1997,

revenues from our gaming machines at the Charles Town

Entertainment Complex have accounted for an increasingly

large share of our total revenues. Our pari-mutuel revenues

have been derived from wagering on our live races, wagering

on import simulcasts at our racetracks and OTWs and

through telephone account wagering, and fees from

wagering on export simulcasting our races at out-of-state

locations. Our other revenues have been derived from

admissions, program sales, food and beverage sales,

concessions and certain other ancillary activities.

Our acquisitions of Casino Magic Bay St. Louis, Boomtown

Biloxi, Casino Rouge and the management contract for

Casino Rama will continue to impact our revenue mix

between gaming and pari-mutuel revenues on a prospective

basis.We expect that in future periods gaming revenue as

a percentage of our total revenues will continue to increase

as we continue to focus on our gaming operations. For

the years ended December 31, 1999, 2000 and 2001, gaming

revenue represented approximately 32%, 54% and 71% of

our total revenue, respectively.

RECENT AND PENDING ACQUISITIONS

CASINO MAGIC AND BOOMTOWN BILOXI

On August 8, 2000, we completed our acquisition of the

Casino Magic Bay St. Louis casino and the Boomtown

Biloxi casino from Pinnacle Entertainment, Inc. for

approximately $201.3 million in cash, including acquisition

costs of $6.3 million. The purchase price was funded with

a portion of the proceeds from our $350 million senior

secured credit facility.As a result of the refinancing and

repayment of existing debt, we recorded an $11.2 million

pre-tax extraordinary charge, which was included in our

results of operations for the year ended December 31, 2000.

The results of operations for these properties from the

period August 8, 2000 to December 31, 2001 are included

in the results of operations discussed below.

CASINO ROUGE AND CASINO RAMA

On April 27, 2001, we completed our acquisition of Casino

Rouge in Baton Rouge, Louisiana and the management

contract for Casino Rama in Orillia, Ontario, Canada for

approximately $182 million, including the repayment of

existing debt of CRC and its subsidiaries. The purchase

price of the acquisition was funded by the proceeds of our

offering of 11⅛% senior subordinated notes due 2008,

which was completed in March 2001. The results of oper-

ations for these properties for the period April 28, 2001 to

December 31, 2001 are included in the results of operations

discussed below.

BULLWHACKERS CASINO

In August 2001, we signed an agreement to acquire the

operations of Bullwhackers Casino, the adjoining Bullpen

Sports Casino and Silver Hawk Saloon and Casino in

Black Hawk, Colorado for $6.5 million cash.We expect

to close the acquisition in the second quarter of 2002.

CRITICAL ACCOUNTING POLICIESFinancial Reporting Release No. 60, which was recently

released by the Securities and Exchange Commission,

requires all companies to include a discussion of critical

accounting policies or methods used in the preparation

of financial statements. Our significant accounting policies

are described in Note 1 of the Notes to the Consolidated

Financial Statements. The significant accounting policies

that we believe are the most critical to aid in fully under-

standing our reported financial results include the following:

REVENUE RECOGNITION

In accordance with common industry practice, our casino

revenues are the net of gaming wins less losses. Racing

revenues include our share of pari-mutuel wagering on

live races after payment of amounts returned as winning

wagers, and our share of wagering from import and export

simulcasting as well as our share of wagering from our

OTWs.The vast majority of wagers for both businesses

are in the form of cash and we do not grant credit to our

customers to a significant extent. Our receivables consist

principally of amounts due from simulcasting of our races

to other racetracks and their OTWs.We also have receiv-

ables due under our management contract with Casino

Rama for management fees and for expenses, primarily

salaries and wages, payable in accordance with our contract.

Historically, we have not experienced any significant bad

debts from uncollectable receivables.

RECENT ACCOUNTING STANDARDS

In June 2001, the Financial Accounting Standards Board

finalized FASB Statements No. 141,“Business Combinations”

(“SFAS 141”) and No. 142,“Goodwill and Other

Intangibles Assets” (“SFAS 142”). SFAS 141 requires the use

of the purchase method accounting and prohibits the use

of pooling-of-interests method of accounting for business

combinations initiated after June 30, 2001. SFAS 141 also

requires that we recognize acquired intangible assets apart

from goodwill if the acquired intangible assets meet cer-

tain criteria. SFAS 141 applies to all business combinations

initiated after June 30, 2001 and for purchase business

combinations completed on or after July 1, 2001. It also

requires, upon adoption of SFAS 142, that we reclassify

the carrying amounts of intangible assets and goodwill

based on certain criteria in SFAS 141.

SFAS 142 requires, among other things, that companies

no longer amortize goodwill, but instead test goodwill for

impairment at least annually. In addition, SFAS 142 requires

that we identify reporting units for the purpose of assessing

potential future impairments of goodwill, reassess the useful

lives of the other existing recognized intangible assets, and

cease amortization of intangible assets with an indefinite

useful life.Any intangible asset with an indefinite useful

life should be tested for impairment in accordance with

the guidance in SFAS 142. SFAS 142 is required to be

applied in fiscal years beginning after December 15, 2001

to all goodwill and other intangible assets recognized

at that date, regardless of when those assets were initially

recognized. SFAS 142 requires us to complete a transitional

goodwill impairment test six months from the date of

adoption.We are also required to reassess the useful lives

of the other intangible assets within the first interim quarter

after adoption of SFAS 142.

Our previous business combinations were accounted for

using the purchase method.As of December 31, 2001, net

carrying amount of goodwill is $160.2 million and other

intangible assets (management service contract for Casino

Rama) is $24.1 million.Amortization expense for goodwill

and other intangible assets for the year ended December

31, 2001 was $3.5 million and $1.7 million, respectively.

Currently, we are assessing but have not yet determined

how the adoption of SFAS 142 will impact our financial

position and results of operations.

In October 2001, the FASB issued SFAS No. 144,

“Accounting for the Impairment or Disposal of Long-Lived

Assets” (“SFAS 144”).This statement addresses financial

accounting and reporting for the impairment or disposal

of long-lived assets.This statement supersedes SFAS

Statement No. 121,“Accounting for the Impairment

of Long-Lived Assets and for Long-Lived Assets to Be

Disposed Of,” and the accounting and reporting provisions

of APB Opinion No. 30, “Reporting the Results of

Operations-Reporting the Effects of Disposal of a Segment

of a Business, and Extraordinary, Unusual and Infrequently

Occurring Events and Transactions.” This statement also

amends ARB No. 51 “Consolidated Financial Statements,”

to eliminate the exception to consolidation for a subsidiary

for which control is likely to be temporary.This statement

requires that one accounting model be used for long-lived

assets to be disposed of by sale, whether previously held

and used or newly acquired.This statement also broadens

the presentation of discontinued operations to include

more disposal transactions. SFAS 144 is effective for fiscal

years beginning after December 15, 2001 and interim

periods within those fiscal years. Currently, we are assessing

but have not determined how the adoption of SFAS 144

will impact our financial position and results of operations.

2120

CRC properties also accounted for $54.3 million of the

increase. Operating expenses increased at the Charles Town

Entertainment Complex by $48.3 million, or 46.5%, to

$152.2 million in 2001 from $103.9 million in 2000 due

in large part to additional gaming machines in 2001 and

a higher percentage of more expensive coin-out machines

compared to video voucher machines. Operating expenses

at the Pennsylvania racetracks and OTWs increased by $.4

million. Corporate overhead increased by $4.2 million, or

64.6%, to $10.7 million in 2001 from $6.5 million in 2000

primarily due to additional corporate staff needed to support

the recent acquisitions.

EBITDA increased by $52.8 million, or 88.7%, to $112.3

million in 2001 from $59.5 million in 2000. EBITDA

increased at our Mississippi properties by $22.6 million to

$32.2 million in 2001 from $9.6 million in 2000. The CRC

properties accounted for $22.6 million of the increase.

EBITDA at the Charles Town Entertainment Complex

increased by $15.8 million, or 44.5%, to $51.3 million in

2001 from $35.5 million in 2000. The Pennsylvania race-

tracks and OTWs and New Jersey joint venture EBITDA

accounted for a decrease of $3.2 million over last year.

Corporate overhead increased by $3.9 million, or 65.0%,

to $9.9 million in 2001 from $6.0 million in 2000.

Net interest expense increased $24.3 million in 2001 due

primarily to additional borrowings in August 2000 of

approximately $200.0 million to finance the Mississippi

acquisitions and $200.0 million in April 2001 to finance

the CRC acquisition.

CHARLES TOWN ENTERTAINMENT COMPLEX

Total revenues for the year ended December 31, 2001

increased by $58.3 million, or 43.1%, to $193.6 million

in 2001 from $135.3 million in 2000. Gaming revenues

increased by $55.7 million, or 51.0%, to $165.0 million

in 2001 from $109.3 million in 2000, primarily due to

expansion of the gaming floor, which was completed in

December 2000.As a result of the expansion, we added

500 reel-spinning, coin-out gaming machines, bringing

the total average number of machines to approximately

2,000 for the year 2001, compared to approximately 1,500

gaming machines for the year 2000. These additional

gaming machines, and the continued shift in machine mix

to a higher percentage of reel-spinning, coin-out machines,

resulted in an increase in average win per machine of $224

for the year ended December 31, 2001 compared to $199

for the year ended December 31, 2000. Racing revenues

increased by $1.8 million, or 8.9%, to $22.1 million in 2001

from $20.3 million in 2000. This increase was primarily

due to 25 additional racing days and an increase in export

wagering by $43.1 million, or 28.2%, to $196.2 million as

a result of additional racing days and overall larger per day

wagering averages. Other revenue increased by $.8 million,

or 14.0%, to $6.5 million in 2001 from $5.7 million in

2000 primarily as a result of higher food and beverage

revenues from opening of the Sundance Café in November

2000, and expansion of the concession areas, dining room

and the buffet.

Total operating expenses for the year ended December 31,

2001 increased $48.3 million, or 46.5%, to $152.2 million

in 2001 from $103.9 million in 2000. The increase was

primarily due to an increase in gaming and racing related

taxes of $32.5 million attributable to increased gaming

and racing revenues and a change in gaming legislation

that resulted in higher gaming taxes and a higher net

administrative fee paid to the State of West Virginia. Salaries

and wages increased by $5.2 million primarily due to

additional staffing associated with increased gaming units,

gaming square footage, and expanded concession and dining

facilities. Total marketing expenses increased $1.9 million

in 2001 as a result of additional media advertising and

promotional campaigns to increase awareness of the facility.

Other expenses increased due to an increase in property

insurance premiums and operating costs associated with

the expanded capacity of the facility. Depreciation and

amortization increased by $4.8 million as a result of higher

capital expenditures in 2001. EBITDA for the year ended

December 31, 2001 increased by $15.8 million, or 44.5%,

to $51.3 million in 2001 from $35.5 million in 2000.

MISSISSIPPI CASINOS

Operating results in 2000 for Casino Magic Bay St. Louis

and Boomtown Biloxi only include the period from

August 8, 2000 through December 31, 2000. For the year

ended December 31, 2001, Casino Magic Bay St. Louis

YEAR ENDED DECEMBER 31, 2001 COMPARED TO YEAR ENDED DECEMBER 31, 2000Revenues for the year ended December 31, 2001 increased

by $227.6 million, or 78.0%, to $519.4 million in 2001

from $291.8 million in 2000. Revenues increased at our

Mississippi properties by $101.9 million to $158.1 million

in 2001 from $56.2 million in 2000 (which represented

revenues from the August 8, 2000 acquisition date through

December 31, 2000). The CRC properties, which were

acquired on April 27, 2001, accounted for $70.3 million

of the increase. Revenues also increased at the Charles Town

Entertainment Complex by $58.3 million, or 43.1%, to

$193.6 million in 2001 from $135.3 million in 2000 as

a result of an increase in the number of gaming machines

from 1,500 to 2,000 in 2001 and a higher percentage in

2001 of coin-out machines compared to video voucher

machines. Revenues from the Pennsylvania racetracks and

OTWs decreased by approximately $3.2 million due to

a Commonwealth of Pennsylvania racing subsidy of $1.6

million received in 2000 but not in 2001 and a decrease

in wagering.

Operating expenses for the year ended December 31, 2001

increased by $195.0 million, or 79.0%, to $441.7 million

in 2001 from $246.7 million in 2000. Operating expenses

increased at our Mississippi properties by $87.9 million to

$138.4 million in 2001 from $50.5 million in 2000. The

REVENUES EBITDA(1)

1999 2000 2001 1999 2000 2001

Charles Town Entertainment Complex $ 80,015 $135,290 $193,612 $16,023 $35,469 $ 51,252Casino Magic-Bay St. Louis(2) – 31,571 87,752 – 6,092 18,658Boomtown Biloxi(2) – 24,634 70,370 – 3,460 13,546Casino Rouge(3) – – 61,981 – – 15,444Casino Rama Management Contract(3) – – 8,297 – – 7,632Penn National Race Course and its OTWs 55,609 64,364 59,821 9,065 10,380 7,582Pocono Downs and its OTWs 36,324 37,573 38,945 8,955 7,791 7,127New Jersey Joint Venture – – – 1,098 2,322 2,531Corporate eliminations(4) (1,588) (1,631) (1,386) – – –Corporate overhead – – – (5,361) (6,033) (9,946)Corporate overhead CRC Holdings(3) – – – – – (490)

Total before non-recurring charges 170,360 291,801 519,392 29,780 59,481 113,336Non-recurring charges and expenses – – – (3,284) – (1,000)

Total $170,360 $291,801 $519,392 $26,496 $59,481 $112,336

(1) EBITDA consists of income from operations plus depreciation and amortization and earnings from joint venture. EBITDA is presented because we believe it is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. However, other companies in our industry may calculate EBITDA differently than we do. EBITDA is not a measurement of financial performance under generally accepted accounting principles and should not be considered as an alternative to cash flow from operating activities or as a measure of liquidity or an alternative to net income as an indicator of operating performance, or any other measure of performance derived in accordance with generally accepted accounting principles.

(2) Reflects results since the August 8, 2000 acquisition from Pinnacle Entertainment.

(3) Reflects results since April 27, 2001 acquisition of CRC Holdings, Inc., including corporate overhead at CRC’s executive office in Miami, Florida.

(4) Primarily reflects intracompany transactions related to import/export simulcasting.

RESULTS OF OPERATIONSThe results of operations by property level for the years

ended December 31, 1999, 2000 and 2001 are summarized

below (in thousands):

had revenues of $87.8 million consisting mainly of gaming

revenue. Operating expenses for Casino Magic totaled

$76.5 million consisting of gaming ($44.0 million), other

($6.7 million), general and administrative ($18.4 million),

and depreciation and amortization expense ($7.4 million).

For the year ended December 31, 2001, Boomtown

Biloxi had revenues of $70.4 million consisting mainly

of gaming revenue. Operating expenses for Boomtown

totaled $61.8 million consisting of gaming ($28.9 million),

other ($8.8 million), general and administrative ($19.1

million), and depreciation and amortization expense ($5.0

million). EBITDA for the Mississippi casinos totaled $32.2

million for the period. Our Mississippi casino operations

have numerous competitors, many of which have greater

name recognition and financial and marketing resources

than we do. Competition in the Mississippi gaming markets

is significantly more intense than the competition that our

gaming operations face in West Virginia or our pari-mutuel

operations face in Pennsylvania and New Jersey.

CASINO ROUGE AND CASINO RAMA

The CRC acquisition was completed on April 27, 2001

and includes the purchase of Casino Rouge in Baton Rouge,

Louisiana, and a management contract to operate Casino

Rama in Orillia, Canada. For the period from April 28,

2001 to December 31, 2001, Casino Rouge had revenues

of $62.0 million consisting mainly of gaming revenues.

Operating expenses for Casino Rouge totaled $51.3 million

consisting of gaming ($29.4 million), other ($3.4 million),

general and administrative ($13.8 million) and depreciation

and amortization expense ($4.7 million). For the period

from April 28, 2001 to December 31, 2001, management

fees from the Casino Rama management contract totaled

$8.3 million for which there was $.7 million of direct

operating expenses relating to the associated revenues and

amortization of $1.7 million related to the management

services contract. EBITDA for Casino Rouge and Casino

Rama totaled $22.6 million for the same period.

PENN NATIONAL RACE COURSE AND ITS OTW FACILITIES

Revenues for the year ended December 31, 2001 decreased

by $4.6 million, or 7.1%, to $59.8 million in 2001 from

$64.4 million in 2000. Live racing revenue accounted for

$1.4 million of the decrease as a result of a decline in

attendance, inclement weather and smaller fields in the

first five months of 2001. Full card simulcasting accounted

for $2.0 million of the $4.6 million decline, again due to

lower attendance in 2001. Other racing revenue declined

by $1.0 million in 2001 compared to 2000 as a result of

a Commonwealth of Pennsylvania racing subsidy received

in 2000 but not in 2001.Although the Commonwealth

passed a similar subsidy measure in 2001, subsidy payments

by the Commonwealth were frozen and were not received.

Operating expenses for the year ended December 31, 2001

decreased by $1.8 million, or 3.2%, to $55.7 million in 2001

from $55.8 million in 2000. Racing-related expenses such

as purses, simulcast fees and pari-mutuel taxes declined by

$1.6 million, in part due to lower racing revenues. EBITDA

for the year ended December 31, 2001 decreased by $2.8

million, or 26.9%, to $7.6 million in 2001 from $10.4

million in 2000.

POCONO DOWNS AND ITS OTW FACILITIES

Revenues for the year ended December 31, 2001 increased

by $1.3 million, or 3.4%, to $38.9 million in 2001 from

$37.6 million in 2000. Revenues increased approximately

$2.3 million due to the opening of a new OTW facility

in East Stroudsburg, Pennsylvania, that was in operation

for all of 2001 compared to five months in 2000. This

increase was offset by a decline of $.6 million as a result

of a Commonwealth of Pennsylvania racing subsidy

received in 2000 but not in 2001, and a net decline in

revenues at the other Pocono Downs OTWs.

Operating expenses for the year ended December 31, 2001

increased by $2.3 million, or 7.2%, to $34.2 million in 2001

from $31.9 million in 2000. Other operating expenses,

administrative expense and concessions expenses increased

$.9 million to $11.6 million compared to $10.7 million

for the same period the previous year due to a full year of

operations at the East Stroudsburg OTW. Racing-related

expenses, such as purses, simulcast fees and pari-mutuel

taxes, increased $1.0 million, in part due to higher racing

revenues. For the year ended December 31, 2001 EBITDA

decreased by $.7 million to $7.1 million in 2001 from

$7.8 million in 2000.

CORPORATE OVERHEAD EXPENSES

Corporate overhead expenses increased by $4.2 million, or

64.6%, to $10.7 million in 2001 from $6.5 million in 2000.

Salaries and wages, payroll taxes, employee benefits, reloca-

tion expenses and office rent increased by $2.0 million due

to the addition of new staff at the corporate office to support

the Mississippi and CRC acquisitions. Liability insurance

increased by $.5 million due to increased limits for general

liability, fiduciary and directors and officers liability insurance

and increased insurance rates as a result of market conditions.

Consulting and professional services increased by $1.0

million due to acquisition-related activities and regulatory

expenses. Travel expenses increased by $.4 million as

a result of supporting properties in Mississippi, Louisiana

and Canada.

NEW JERSEY JOINT VENTURE

We have an investment in Pennwood Racing, Inc., which

operates Freehold Raceway in New Jersey and, until May

2001, operated Garden State Park. In May 2001, Garden

State Park was sold and the joint venture ceased operating

Garden State Park. Our 50% share of net income was $2.5

million in 2001 compared to $2.3 million in 2000 and

was recorded as other income on the income statement.

The increase in the joint venture’s net income is due in

part to impairment expenses recorded in December 2000

related to the then-proposed May 2001 closure of Garden

State Park and decreased interest expense in 2001, offset

by the decrease in operating income in 2001 as a result

of the closure of Garden State Park.

NON-RECURRING CHARGES AND EXPENSES

Non-recurring charges and expenses for the year ended

December 31, 2001 were $1.0 million as a result of the

settlement of the Showboat litigation.

YEAR ENDED DECEMBER 31, 2000COMPARED TO YEAR ENDED DECEMBER 31, 1999Revenues for the year ended December 31, 2000 increased

71.2% or $121.4 million to $291.8 million, from $170.4

for the year ended December 31, 1999. Operating expenses

increased 61.6%, or $94.6 million, to $248.2 million in 2000,

from $153.6 million in 1999. The increases in revenues and

operating expenses were primarily a result of the Casino

Magic and Boomtown Biloxi acquisition in August 2000,

the change to more reel-spinning, coin-out gaming machines

at the Charles Town Entertainment Complex and the

addition of 500 new machines at Charles Town.As a result,

income from operations increased 160.5%, or $26.8 million,

to $43.5 million in 2000 from $16.7 million in 1999.

Total other expense increased 138.7%, or $8.6 million,

to $14.8 million in 2000 from $6.2 million in 1999.

Net interest expenses increased $9.9 million in 2000 due

to additional borrowings of $200 million to finance the

Mississippi acquisition. Earnings from the New Jersey

joint venture increased by $1.2 million compared to 1999.

Taxes on income increased by 168.4%, or $6.4 million, due

to the factors discussed above. Income before extraordinary

item was $18.6 million in 2000 compared to net income

of $6.7 million in 1999. In 2000, we incurred an extraor-

dinary charge net of taxes of $6.6 million for the early

extinguishment of debt; after giving effect to this change,

our net income was $12.0 million for the year ended

December 31, 2000.

CHARLES TOWN ENTERTAINMENT COMPLEX

Revenues increased at Charles Town by approximately

$55.3 million, or 69.1%, to $135.3 million in 2000 from

$80.0 million in 1999. Gaming revenue increased by

$53.9 million, or 97.3%, to $109.3 million in 2000 from

$55.4 million in 1999 due to the addition of 136 new video

lottery machines in mid-1999, 565 new reel-spinning,

coin-out gaming machines in late 1999 and 452 gaming

machines in the OK Corral slots center, which opened on

November 25, 2000. The average number of machines in

play increased to 1,494 in 2000 from 923 in 1999 and the

average win per machine increased to $199 in 2000 from

$163 in 1999. Racing revenue increased by $1.0 million,

or 5.2%, to $20.3 million in 2000 from $19.3 million in

1999. This increase is due primarily to a change in the

schedule from a Wednesday afternoon race program to a

Thursday evening race program in 2000 to accommodate

export simulcasting. Charles Town began exporting its live

race program to tracks across the country on June 5, 1999

2322

25

executed in January 2000 accounted for most of the

increase in expenses. EBITDA decreased $1.2 million, or

13.3%, to $7.8 million in 2000 from $9.0 million in 1999.

CORPORATE OVERHEAD EXPENSES

Corporate overhead expenses increased by $0.7 million, or

13.2%, to $6.0 million in 2000 from $5.3 million in 1999.

Salaries and wages, payroll taxes, and benefits increased by

$0.7 million due to new positions created for business

development, employee training, and marketing. Expenses

also increased for SEC and annual reporting ($73,000),

office space ($30,000) and corporate travel for acquisitions

and Mississippi operations ($246,000).These increases were

partially offset by a decrease in outside services, professional

fees and consulting fees in the amount of $0.4 million.

NEW JERSEY JOINT VENTURE

We completed our investment in Pennwood Racing, Inc.,

the New Jersey joint venture, on July 29, 1999. Pennwood

Racing operates Freehold Raceway and Garden State Park.

Revenues of the joint venture increased to $61.5 million

in 2000 from $28.0 million in 1999 as a result of the

operating results in 2000 reflecting a full twelve-month

period. Net income was $5.6 million in 2000, before non-

recurring charges of $1.0 million relating to the termination

of the Garden State lease, compared to $2.2 million in 1999.

Our 50% share of net income was $2.3 million, after a

non-recurring charge of $0.5 million, in 2000 compared

to $1.1 million in 1999.

NON-RECURRING CHARGES AND EXPENSES

Non-recurring charges and expenses totaled $3.3 million

for the year ended December 31, 1999. In connection

with our gaming operations in West Virginia, we recorded

litigation expense of $1.5 million for liquidated damages

awarded to Amtote International, Inc. in a wagering services

contract dispute. In Tennessee, the Tennessee Supreme

Court declined to review the substantive issue of whether

pari-mutuel wagering on horse racing is lawful under the

existing statute without the Tennessee Racing Commission.

As a result of this decision we recorded a charge against

earnings of $0.5 million for costs incurred for our Tennessee

racing license. In Pennsylvania, we incurred expenses totaling

$1.3 million as a result of the Horsemen’s action that closed

Penn National Race Course and its OTWs from February

16 to March 24, 1999 and resulted in the loss of 46 race

days in 1999.

LIQUIDITY AND CAPITAL RESOURCESHistorically, our primary sources of liquidity and capital

resources have been cash flow from operations, borrowings

from banks and proceeds from the issuance of debt and

equity securities.

Net cash provided by operating activities was $85.8 million

for the year ended December 31, 2001. This consisted

of net income ($24.4 million), adjusted for non-cash

reconciling items ($36.8 million) and net increases in cur-

rent liability accounts along with net decreases in current

asset accounts ($24.6 million), net of assets and liabilities

acquired in the CRC acquisition. Net income, non-cash

items and the net change in the balance sheet accounts

increased by $12.4 million, $12.3 million and $19.1 mil-

lion, respectively, in 2001 as compared to 2000.

Cash flows used in investing activities totaled $216.3 million

for the year ended December 31, 2001. Expenditures for

property, plant, and equipment totaled $41.5 million and

included renovations of the buffet restaurant and new hotel

construction at Casino Magic Bay St. Louis ($18.0 million),

new gaming equipment at Casino Magic ($1.6 million),

new gaming equipment and slot system at Boomtown

Biloxi ($2.4 million), land and building acquisitions at the

Charles Town Entertainment Complex ($1.0 million),

the OK Corral slot center at Charles Town ($0.6 million),

property additions at Charles Town ($0.3 million), con-

struction of parking garage and expansion at Charles Town

($3.2 million), construction and design of a steak house at

Casino Rouge ($1.6 million), other small projects ($1.3

million) and maintenance capital expenditures at our

properties ($11.5 million). The CRC acquisition totaled

$182.7 million. Cash received from the New Jersey joint

venture totaled $2.9 million. Cash in escrow decreased

by $4.6 million as a result of the closing of the CRC

acquisition on April 27, 2001.

24

and generated export simulcasting revenues of $2.2 million

in 2000 compared to $1.0 million in 1999. Operating

expenses increased by $36.5 million, or 54.2%, to $103.9

million in 2000 from $67.4 million in 1999. The increase

was primarily due to an increase in gaming expenses of

$30.1 million, or 86.0%, to $65.1 million in 2000 from

$35.0 million in 1999. This increase was mainly due to

increased lottery taxes, purses, salaries and wages and

administrative expenses related to the increase in gaming

revenues. Racing, other and general and administrative

expenses increased by $4.1 million, or 13.4%, to $34.7

million in 2000 from $30.6 million in 1999. The increase

was due to an increase in direct costs associated with

additional wagering on horse racing and gaming machine

play, the addition of gaming machines and floor space (new

temporary facility for gaming machines and the opening

of the OK Corral slot center), export simulcast expenses

and expanded concession and dining capability and capacity.

Depreciation expense increased by $2.3 million, or 127.8%,

to $4.1 million in 2000 from $1.8 million in 1999 due to

additional gaming machines and improvements in 2000.

EBITDA attributable to Charles Town increased by $19.5

million, or 121.9%, to $35.5 million in 2000 from $16.0

million in 1999.

MISSISSIPPI CASINOS

The Casino Magic Bay St Louis and Boomtown Biloxi

acquisitions were completed on August 8, 2000. For the

period August 8 to December 31, 2000, Casino Magic

Bay St. Louis had revenues of $31.6 million consisting

mainly of gaming revenue. Operating expenses for Casino

Magic totaled $27.8 million consisting of gaming ($18.0

million), other ($2.5 million), general and administrative

($5.0 million), and depreciation and amortization expense

($2.3 million). For the period August 8 to December 31,

2000 Boomtown Biloxi had revenues of $24.6 million

consisting mainly of gaming revenue. Operating expenses

for Boomtown totaled $22.7 million consisting of gaming

($11.0 million), other ($3.2 million), general and adminis-

trative ($7.0 million), and depreciation and amortization

expense ($1.5 million). EBITDA for the Mississippi casinos

totaled $9.6 million for the period. Our Mississippi casino

operations have numerous competitors, many of which

have greater name recognition and financial and marketing

resources than we do. Competition in the Mississippi gaming

markets is significantly more intense than the competition

that our gaming operations face in West Virginia or our

pari-mutuel operations face in Pennsylvania and New Jersey.

PENN NATIONAL RACE COURSE AND ITS OTW FACILITIES

Penn National Race Course had an increase in revenue of

approximately $8.8 million, or 15.8%, to $64.4 million in

2000 from $55.6 million in 1999. Pari-mutuel wagering

was $386.6 million in 2000 compared to $333.8 million

in 1999. The increase in wagering and revenues is attrib-

uted to Penn National Race Course running 201 live race

days in 2000 compared to 153 live races days in 1999.

Penn National only ran 153 live race days in 1999 due to

the Horsemen action in the first quarter that resulted in

the closure of all of the facilities from February 16 to

March 24, 1999. Operating expenses increased by approxi-

mately $6.2 million, or 12.5%, to $55.8 million in 2000

from $49.6 million in 1999. The increase was primarily

due to an increase in racing expenses of $5.6 million, or

16.0%, to $40.5 million in 2000 from $34.9 million in

1999. This increase was due to the temporary closure of

Penn National Race Course and its OTWs in 1999 and

a limited live race schedule during a portion of 1999 due

to the Horsemen action described above.Adjusting for the

Horsemen action in 1999, EBITDA attributable to these

properties increased by $1.3 million, or 14.3%, to $10.4

million in 2000 from $9.1 million in 1999.

POCONO DOWNS AND ITS OTW FACILITIES

Revenues at Pocono Downs increased by $1.3 million,

or 3.6%, to $37.6 million in 2000 from $36.3 million in

1999. Pari-mutuel wagering was $161.6 million in 2000

compared to $160.2 million in 1999. Operating expenses

increased by approximately $2.4 million, or 8.1%, to $31.9

million in 2000 from $29.5 million in 1999. The increase

was primarily due to an increase in racing expenses of

$2.0 million, or 9.9%, to $22.3 million in 2000 from $20.3

million in 1999. The opening of the new OTW facility in

East Stroudsburg, Pennsylvania, and the increase in purse

expense per the terms of the new Horsemen’s contract

2726

Cash flows from financing activities provided net cash flow

of $145.6 million for the year ended December 31, 2001.

Aggregate proceeds from the issuance of notes were $200.0

million, a portion of which were used to pay financing

costs associated with the issuance ($6.9 million). Principal

payments on long-term debt under our existing credit

facility, net of additional borrowings on the revolving line

of credit, were $50.4 million. Proceeds from the exercise

of stock options totaled $2.9 million.

CAPITAL EXPENDITURES

The following table summarizes our planned capital

expenditures, other than maintenance capital expenditures,

by property level for fiscal years ended December 31, 2002

and 2003:

YEAR ENDING DECEMBER 31, 2002 2003

(in thousands)

PropertyCharles Town Entertainment Complex $41,400 $10,000Casino Magic Bay St. Louis 20,700 -Boomtown Biloxi - 4,500Bullwhackers Casino(1) 9,000 -

Totals $71,100 $14,500

(1) Pending acquisition.

Beginning in late 2001 and continuing through the end

of 2002, we expect to expend significant amounts on

capital expenditures at the Charles Town Entertainment

Complex and Casino Magic Bay St. Louis.At Charles

Town, we expect to spend an additional $41.4 million in

2002 on capital expenditures that were begun in 2001.

Specifically, we expect to complete construction of a

structured parking facility, at an estimated additional cost

of $10.2 million in 2002, and expand the gaming and

entertainment facility at Charles Town, at an estimated

cost of $31.2 million in 2002, which includes the purchase

of 500 additional gaming machines. In 2003, we expect

to expend approximately $10.0 million to purchase and

install an additional 1,000 machines at Charles Town. On

February 28, 2002, the West Virginia Lottery Commission

approved our request to add up to 1,500 additional gaming

machines to the 2,000 machines already in place at Charles

Town. Depending on future market conditions in the West

Virginia gaming market, we will continue to evaluate our

plans to build a 300-room hotel at Charles Town.

At Casino Magic, we have begun construction of a 300-

room hotel with meeting and conference facilities, three

new restaurant venues, renovations to the existing buffet

restaurant and certain amenities to the gaming floor.

Through December 31, 2001, we spent approximately

$18.0 million on these projects. In 2002, we expect to spend

an additional $20.7 million to complete these projects.

In January 2002, we signed an option to purchase approx-

imately 4 acres of land adjacent to our Boomtown Biloxi

property for $4.0 million. The purchase is contingent upon

receiving certain governmental and third-party consents,

authorizations, approvals and licenses which we expect could

occur in 2003. If successful, we expect to use the land for

additional parking for our Boomtown facility. In addition,

we expect to make certain property improvements in 2003

at Boomtown at a cost of approximately $0.5 million.

On August 30, 2001, we entered into a definitive agreement

to acquire all of the assets of the Bullwhackers Casino

operations, in Black Hawk, Colorado, from Colorado

Gaming and Entertainment Co., a subsidiary of Hilton

Group plc, for $6.5 million in cash. The Bullwhackers assets

consist of the Bullwhackers Casino, the adjoining Bullpen

Sports Casino, the Silver Hawk Saloon and Casino, an

administrative building and a 475-car parking area, all

located in Black Hawk, Colorado. The Bullwhackers

properties comprise a total of 63,800 square feet of

interior space, 20,700 square feet of which is devoted

to gaming, consisting of 1,002 slot machines and 16 table

games. The properties are located on leased land as well

as 3.25 acres of land included in the acquisition, much of

which is utilized for parking.We currently expect that the

transaction will close in the second quarter of 2002.As of

December 31, 2001, we had made a deposit of $500,000

under the terms of the agreement. In the year 2002, we

expect to spend $9.0 million for the acquisition, closing

costs and improvements to the Bullwhackers Casino.

For 2002 and 2003, we expect to expend approximately

between $14.0 million and $16.0 million each year for

maintenance capital expenditures at our properties.

We expect to use cash generated from operations and cash

available under the revolver portion of our existing senior

secured credit facility to fund our anticipated capital

expenditure and maintenance capital expenditures in 2002

and 2003. See “Outlook” below.

SENIOR SECURED CREDIT FACILITY

On August 8, 2000, we entered into a $350 million senior

secured credit facility with a syndicate of lenders led by

Lehman Brothers Inc. and CIBC World Markets Corp. that

replaced our then-existing credit facilities. The credit facility

is comprised of a $75 million revolving credit facility

maturing on August 8, 2005, a $75 million Tranche A term

loan maturing on August 8, 2005 and a $200 million

Tranche B term loan maturing on August 8, 2006. Up to

$10 million of the revolving credit facility may be used

for the issuance of standby letters of credit, of which there

was $2.6 million outstanding as of December 31, 2001. In

addition, up to $10 million of the revolving credit facility

also may be used for short-term credit to be provided to us

on a same-day basis, which must be repaid within five days.

At our option, the revolving credit facility and the Tranche

A term loan may bear interest at (1) the highest of ½ of

1% in excess of the federal funds effective rate or the rate

that the bank group announces from time to time as its

prime lending rate plus an applicable margin of up to 2.25%,

or (2) a rate tied to a eurodollar rate plus an applicable

margin up to 3.25%, in either case with the applicable

rate based on our total leverage.At our option, the

Tranche B term loan may bear interest at (1) the highest

of ½ of 1% in excess of the federal funds effective rate or

the rate that the bank group announces from time to time

as its prime lending rate plus an applicable margin of up

to 3.25%, or (2) a rate tied to a eurodollar rate plus an

applicable margin up to 4.00%, in either case with the

applicable rate based on our total leverage. The eurodollar

rate is defined as the rate that appears on page 3750 of the

Dow Jones Telerate Screen as of 11:00 a.m. London time

two days before the applicable funding date (adjusted for

statutory reserve requirements for eurocurrency liabilities)

at which eurodollar deposits for one, two, three or six

months, as selected by us, are offered in the interbank

eurodollar market.At December 31, 2001, the weighted

average loan rate for the Tranche A and Tranche B loans

was 8.4%. In addition, as of December 22, 2000, we entered

into a $100.0 million interest rate swap contract obligating

us to pay a fixed rate of 5.825% against a variable interest

rate based on the 90-day LIBOR rate, which expires on

December 22, 2003. On August 3, 2001, we entered into

a $36.0 million interest rate swap contract obligating us

to pay a fixed rate of 4.8125% against a variable interest

rate based on the 90-day LIBOR rate, which expires on

June 30, 2004.

As of December 31, 2001, $61.9 million was outstanding

on the Tranche A term loan, $197.0 million was outstand-

ing on the Tranche B term loan and there was no outstanding

balance under the revolving credit portion of the facility.

Proceeds from the credit facility to date have been used to

finance the acquisition of the Mississippi properties, to

replace our existing term loan and revolving credit facilities,

to complete a tender offer for our 1997 senior notes and

for working capital purposes.

11 1/8% SENIOR SUBORDINATED NOTES DUE 2008

On March 12, 2001, we completed a private offering of

$200,000,000 of our 11⅛% senior subordinated notes due

2008. The net proceeds of the 11⅛% notes were used, in

part, to finance our acquisition of Casino Rouge and the

management contract at Casino Rama, including the

repayment of certain existing indebtedness at CRC.

Interest on the 11⅛% notes is payable on March 1 and

September 1 of each year. The 11⅛% notes mature on

March 1, 2008.As of February 28, 2002, all of the principal

amount of the 11⅛% notes are outstanding.

We may redeem all or part of the 11⅛% notes on or after

March 1, 2005 at certain specified redemption prices.

Prior to March 1, 2004, we may redeem up to 35% of

the 11⅛% notes from proceeds of certain sales of our

equity securities. The 11⅛% notes also are subject to

redemption requirements imposed by state and local

gaming laws and regulations.

The 11⅛% notes are general unsecured obligations and are

guaranteed on a senior subordinated basis by certain of

our current and future wholly-owned domestic subsidiaries.

28

The 11⅛% notes rank equally with our future senior

subordinated debt and junior to our senior debt, including

debt under our senior credit facility. In addition, the 11⅛%

notes will be effectively junior to any indebtedness of our

non-U.S. or unrestricted subsidiaries, none of which have

guaranteed the 11⅛% notes.

The 11⅛% notes and guarantees were originally issued in

a private placement pursuant to an exemption from the

registration requirements of the Securities Act of 1933.

On July 30, 2001, we completed an offer to exchange the

11⅛% notes and guarantees for 11⅛% notes and guarantees

registered under the Securities Act having substantially

identical terms.

RECENT FINANCING TRANSACTIONSEQUITY OFFERING

On February 20, 2002, we completed a public offering of

4,600,000 shares of our common stock at a public offering

price of $30.50 per share. Of the common shares sold

in the offering, 3,350,000 shares were sold by us and

1,250,000 shares were sold by The Carlino Family Trust,

a related party.We have used the net proceeds from the

offering, totaling approximately $96.1 million after deducting

underwriting discounts and related expenses, to repay term

loan indebtedness under the existing senior secured credit

facility.We did not receive any proceeds from the offering

by The Carlino Family Trust.

8 7/8% SENIOR SUBORDINATED NOTES DUE 2010On February 28, 2002, we completed a public offering of$175,000,000 of our 8⅞% senior subordinated notes due2010. Interest on the 8⅞% notes is payable on March 15and September 15 of each year, beginning September 15,2002. The 8⅞% notes mature on March 15, 2010.As ofFebruary 28, 2002, all of the principal amount of the 8⅞% notes is outstanding.We have used the net proceedsfrom the offering, totaling approximately $170.1 millionafter deducting underwriting discounts and relatedexpenses, to repay term loan indebtedness under the existing senior secured credit facility.

We may redeem all or part of the 8⅞% notes on or afterMarch 15, 2006 at certain specified redemption prices.Prior to March 15, 2005, we may redeem up to 35% ofthe 8⅞% notes from proceeds of certain sales of our equitysecurities. The 8⅞% notes also are subject to redemptionrequirements imposed by state and local gaming laws andregulations.

The 8⅞% notes are general unsecured obligations and areguaranteed on a senior subordinated basis by certain ofour current and future wholly-owned domestic subsidiaries.The 8⅞% notes rank equally with our future senior sub-ordinated debt, including the 11⅛% senior subordinatednotes, and junior to our senior debt, including debt underour senior credit facility. In addition, the 8⅞% notes willbe effectively junior to any indebtedness of our non-U.S.or unrestricted subsidiaries, none of which have guaranteedthe 8⅞% notes.

Although we repaid the term indebtedness under theexisting senior secured credit facility, we did not cancelthe related interest rate swap agreements.We continue tomaintain these agreements.The changes in the fair valuesof the interest rate swaps as well as the amortization of theamounts recorded in other comprehensive income will berecognized as components of interest expense subsequentto the payoff of the floating rate debt.

COMMITMENTS AND CONTINGENCIES

CONTRACTUAL CASH OBLIGATIONSAs discussed above, in February 2002 we completed publicofferings of common stock and 8⅞% senior subordinatednotes and used the proceeds of those offerings to repaythe outstanding term loan indebtedness under the seniorsecured credit facility.As of March 8, 2002, there was noindebtedness outstanding under the credit facility and therewas approximately $71.0 million available for borrowingunder the revolving credit portion of the credit facility.The following table reflects these recent offerings and the repayment of the senior secured credit facility as ofMarch 8, 2002.

OTHER COMMERCIAL COMMITMENTSThe following table presents our material commercialcommitments as of March 8, 2002 for the followingfuture periods:

29

PAYMENTS DUE BY PERIOD

2003- 2005- 2007 TOTAL 2002 2004 2006 & AFTER

(In thousands)

Senior secured credit facility(1) $ – $ – $ – $ – $ –11 1/8% senior subordinated notes due 2008(2)

Principal 200,000 – – – 200,000Interest 159,458 22,250 44,500 44,500 48,208

8 7/8% senior subordinated notes due 2010(3)

Principal 175,000 – – – 175,000Interest 124,248 7,766 31,063 31,063 54,356

Operating leases 11,929 3,530 5,474 1,978 947Bullwhackers Casino purchase agreement 6,500 6,500 – – –

Total $677,135 $40,046 $81,037 $77,541 $478,511

(1) Subsequent to December 31, 2001, we completed public offerings of common stock and 8 7/8% senior subordinated notes and used theproceeds of those offerings to repay the outstanding term loan indebtedness under the credit facility.As of March 8, 2002, there was noindebtedness outstanding under the credit facility and there was approximately $71.0 million available for borrowing under the revolvingcredit portion of the credit facility.

(2) The $200.0 million aggregate principal amount of 11 1/8% notes matures on March 1, 2008. Interest payments of approximately$11.1 million are due on each March 1 and September 1 until March 1, 2008.

(3) The $175.0 million aggregate principal amount of 8 7/8% notes matures on March 15, 2010. Interest payments of approximately$7.8 million are due on each March 15 and September 15 until March 15, 2010.

AMOUNT OF COMMITMENTEXPIRATION PER PERIOD

TOTAL AMOUNTS 2003- 2005- 2007 COMMITTED 2002 2004 2006 & AFTER

(In thousands)

Revolving Credit Facility(1) $70,600 $ - $ - $70,600 $ -Letters of Credit(1) 4,400 4,400 - - -Guarantees of New Jersey Joint

Venture Obligations(2) 10,400 767 9,633 - -

Total $85,400 $5,167 $9,633 $70,600 $ -

(1) The available balance under the revolving portion of the $75.0 senior secured credit facility is diminished by outstanding letters of credit.

(2) In connection with our 50% ownership interest in Pennwood Racing, our joint venture in New Jersey, we have entered into a debt service maintenance agreement with Pennwood’s lender to guarantee up to 50% of Pennwood’s $23.0 million term loan. Our obligation as of March 8, 2002 under this guarantee is approximately $10.4 million.

30

LITIGATION

On August 20, 2001, Showboat Development Company

brought a lawsuit against us and certain other parties

related to the Charles Town Entertainment Complex.

The suit alleges, among other things, that our operation

of coin-out video lottery terminals at the Charles Town

facility constitutes the operation of a casino, thereby trig-

gering Showboat’s option to manage the casino. The suit

also alleges that our March 2000 acquisition of the 11%

minority interest in Charles Town Races from BDC Group,

our former joint venture partner, was made in violation

of a right of first refusal that Showboat holds from BDC

covering the sale of any interest in any casino at Charles

Town Races.We filed in federal district court in Nevada

a motion to dismiss this action for lack of personal

jurisdiction and, in the alternative, a motion to transfer

the case to the state of West Virginia. On January 25, 2002,

the district court granted our motion to dismiss. On

February 13, 2002, Showboat filed a lawsuit in the

United States District Court for the Eastern District of

Pennsylvania.The substance of the lawsuit was substantially

similar to Showboat’s previous claim filed in Nevada.

On March 28, 2002, Penn National and Showboat agreed

to settle all litigation related to this matter. Under the

settlement, we agreed to make a one-time payment of

$1.0 million to Showboat, which was recognized in

general and administrative expenses in our operating

results for the fourth quarter of 2001.

In July 2001, a lawsuit was filed against us by certain

surveillance employees at the Charles Town facility claiming

that our surveillance of those employees during working

hours was improper. The lawsuit claims damages of $7.0

million and punitive damages of $15.0 million.We currently

are conducting discovery in the case but, at this time, believe

that all of the claims of the employees are without merit.

On February 12, 2002, we filed a motion for summary

judgment that is pending before the court.We intend to

vigorously defend ourselves against this action and do not

believe that this action will have a material adverse effect

on our financial condition or results of operations.

In January 2002, an employee at our Charles Town facility

initiated a suit against us alleging invasion of privacy. The

employee claims in the suit that she was subjected to an

involuntary strip search by other Charles Town employees

as part of a theft investigation and is seeking punitive

damages. The lawsuit claims damages of $0.5 million and

punitive damages of $3.5 million.We believe we have

meritorious defenses and intend to vigorously defend

ourselves against this suit.

We also are parties to certain other litigation but do not

believe it will have a material adverse effect on our financial

condition or results of operations if any of these legal pro-

ceedings were adversely adjudicated or settled. Furthermore,

the nature of our business subjects us to the risk of lawsuits

filed by customers and others in the ordinary course. In

general, litigation can be expensive and time consuming

to defend and could result in settlements or damages that

could significantly impact results of operations or financial

condition.

INTEREST RATE SWAP AGREEMENTS

We currently use interest rate swaps to assist in managing

interest incurred on our long-term debt. The difference

between amounts received and amounts paid under such

agreements, as well as any costs or fees, is recorded as

a reduction of, or addition to, interest expense as incurred

over the life of the swap or similar financial instrument.

On December 20, 2000, we entered into a forward interest

rate swap with a notional amount of $100 million, which

has an effective date of December 22, 2000 and a termi-

nation date of December 22, 2003. Under this agreement,

31

we pay a fixed rate of 5.835% against a variable interest

rate based on the 90-day LIBOR rate. On August 3, 2001,

we entered into a forward interest rate swap with a notional

amount of $36 million, which has an effective date of

August 7, 2001 and a termination date of June 30, 2004.

Under this agreement, we pay a fixed rate of 4.8125%

against a variable interest rate based on the 90-day LIBOR

rate.At December 31, 2001, the 90-day LIBOR rate was

1.92%.We entered into these interest rate swap agreements

to reduce the impact of future variable interest payments

related to our senior secured credit facility.We account for

the interest rate swap agreements as cash flow hedges. The

changes in the fair values of the interest rate swaps are

recorded as adjustments to accrued interest in the accom-

panying consolidated balance sheet with the offset recorded

in accumulated other comprehensive loss, which as of

December 31, 2001 amounted to $3.8 million, net of an

income tax benefit of $2.0 million.Any hedge ineffectiveness

was not material for the year ended December 31, 2001.

Amounts recorded in accumulated other comprehensive

income will be amortized as an adjustment to interest

expense over the term of the related derivative.We estimate

$1.8 million of net derivative losses included in other

comprehensive income will be reclassified into interest

expense within the next twelve months.

The interest rate swap agreements hedge a portion of our

exposure on our outstanding floating rate obligations, which

were $258.9 million at December 31, 2001. For the year

ended December 31, 2001, we increased interest expense

by approximately $1.7 million as a result of the interest

rate swap agreements.We are exposed to credit loss in the

event of nonperformance by our counter parties to the

interest rate swap agreements.We do not anticipate non-

performance by these financial institutions, and no material

loss would be expected from the nonperformance of these

financial institutions.

Although we repaid the term indebtedness under the

existing senior secured credit facility, we did not cancel

the related interest rate swap agreements.We continue to

maintain these agreements.The changes in the fair values

of the interest rate swaps as well as the amortization of the

amounts recorded in other comprehensive income will be

recognized as components of interest expense subsequent

to the payoff of the floating rate debt.

OUTLOOKBased on our current level of operations, and anticipated

revenue growth, we believe that cash generated from

operations and amounts available under our credit facility

will be adequate to meet our anticipated debt service

requirements, capital expenditures and working capital

needs for the foreseeable future.We cannot assure you,

however, that our business will generate sufficient cash

flow from operations, that our anticipated revenue growth