CONSOLIDATED MINERALS LIMITED – 2007 Annual General Meeting 10.00am (WST), 25 October 2007 Managing Director’s Address – Rod Baxter [Title Slide] Thank you Mr Chairman. Good morning, Ladies and Gentlemen. I would like to extend a warm welcome to shareholders and other investors, supporters and advisers who are here today. The past year has undoubtedly been one of the most remarkable years in Consolidated Minerals’ history. At last year’s Annual General Meeting, and almost 3 months into my tenure, I outlined my agenda for the Company, based on what I described as a clear and simple optimisation and growth strategy. I also emphasised the strength of our operating base, the quality of our assets, and the potential of the management team to turn around a disappointing, loss-making performance in the 2006 financial year, and reposition the company for strong and sustainable growth. I am pleased to say that our delivery against these objectives is well on track and is delivering the results expected, and I would like to take this opportunity to congratulate our staff and contractors, and the management team, for their contributions to the substantial turnaround that has been achieved to date. It is true to say that our strong share price performance, at least in recent months, has reflected both the extensive corporate activity surrounding the Company and the substantial turnaround in the manganese market. However, I believe that the real achievements of the 2007 financial year were at the operational level and it is those achievements that provide the foundation for business performance going forward. I will talk to you in a little more detail today about our performance over the past financial year and update you on how the business is performing during the first quarter of the 2008 financial year. I hope to give you a sense of why the significant increase in the Company’s value over the past six months is being driven as much by our underlying operational performance as it is by the current competing takeover offers. [Slide 2 – Forward Looking Statement] Firstly our standard disclaimer, as I will be making some forward-looking statements during the course of this presentation. [Slide 3 – Corporate Overview] At the beginning of last year, we gave a lot of thought to where we wanted to be as an organisation, and what we needed to do in order to realise our Vision. The strategic changes which we initiated last year were primarily focused around a return to ‘core business values’. Our strategic approach was based on three elements – optimising our existing 1 For personal use only

Transcript

CONSOLIDATED MINERALS LIMITED – 2007 Annual General Meeting

10.00am (WST), 25 October 2007

Managing Director’s Address – Rod Baxter

[Title Slide] Thank you Mr Chairman. Good morning, Ladies and Gentlemen. I would like to extend a warm welcome to shareholders and other investors, supporters and advisers who are here today. The past year has undoubtedly been one of the most remarkable years in Consolidated Minerals’ history. At last year’s Annual General Meeting, and almost 3 months into my tenure, I outlined my agenda for the Company, based on what I described as a clear and simple optimisation and growth strategy. I also emphasised the strength of our operating base, the quality of our assets, and the potential of the management team to turn around a disappointing, loss-making performance in the 2006 financial year, and reposition the company for strong and sustainable growth. I am pleased to say that our delivery against these objectives is well on track and is delivering the results expected, and I would like to take this opportunity to congratulate our staff and contractors, and the management team, for their contributions to the substantial turnaround that has been achieved to date. It is true to say that our strong share price performance, at least in recent months, has reflected both the extensive corporate activity surrounding the Company and the substantial turnaround in the manganese market. However, I believe that the real achievements of the 2007 financial year were at the operational level and it is those achievements that provide the foundation for business performance going forward. I will talk to you in a little more detail today about our performance over the past financial year and update you on how the business is performing during the first quarter of the 2008 financial year. I hope to give you a sense of why the significant increase in the Company’s value over the past six months is being driven as much by our underlying operational performance as it is by the current competing takeover offers. [Slide 2 – Forward Looking Statement] Firstly our standard disclaimer, as I will be making some forward-looking statements during the course of this presentation. [Slide 3 – Corporate Overview]

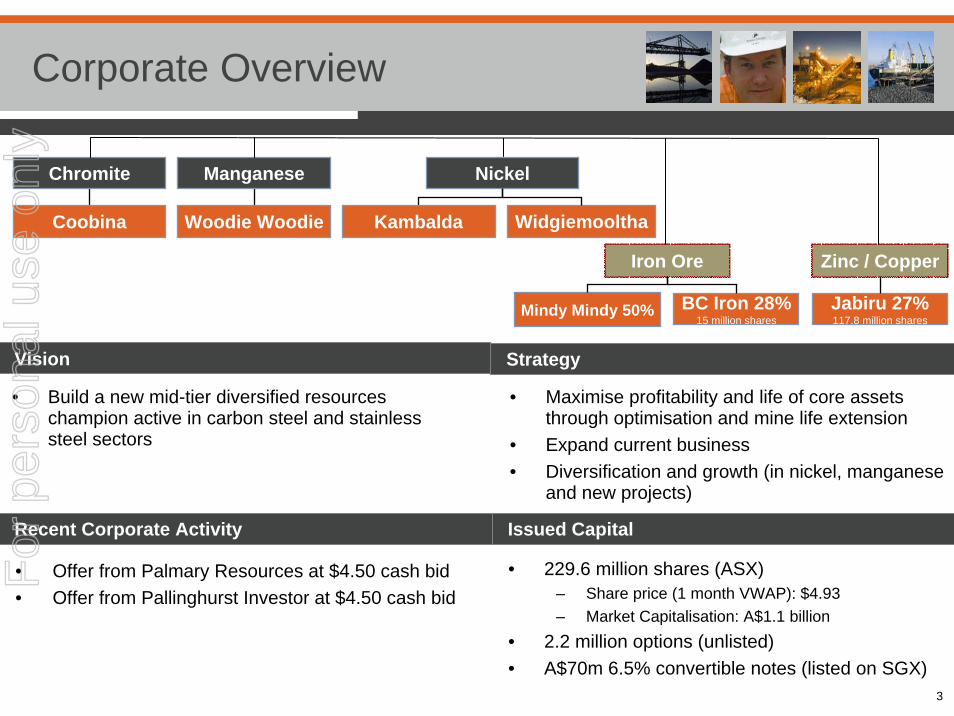

At the beginning of last year, we gave a lot of thought to where we wanted to be as an organisation, and what we needed to do in order to realise our Vision. The strategic changes which we initiated last year were primarily focused around a return to ‘core business values’. Our strategic approach was based on three elements – optimising our existing

1

For

per

sona

l use

onl

y

operations, expanding production in our existing operating divisions, and pursuing other diversification or growth opportunities to strengthen the business. We introduced a number of important new personnel, management and operational changes designed to assist us in achieving our vision of building a new mid-tier diversified resources champion, active in the carbon steel and stainless steel sectors. Our growth strategy has at its foundation our exposure to the global carbon steel and stainless steel sector, through our operating business units, namely: manganese (with production from Woodie Woodie), nickel (now with production from both Kambalda and Widgiemooltha) and chromite (with production from Coobina). Because of the strength of these sectors globally – underpinned by the strong growth of the world economy and, in particular, China – we believe that we have the correct strategy and are operating in the most appropriate space to continue to add shareholder value. Our exposure to the carbon and stainless steel sectors – and our strategic position as a key supplier of 10% of the world's high-grade manganese market – are key reasons why I believe the Company has attracted so much corporate interest this year. [Slide 4 – CSM FY2007 Highlights] The Chairman has already discussed the substantial increase in our market capitalisation and excellent shareholder return achieved for the 2007 financial year – and I would like to begin by briefly recapping our key achievements in this period. They included:

• A return to solid profitability with a pleasing $37 million profit turnaround for the year; • A resumption in dividend payments; • A significant turnaround in our 3 key operating Divisions with strong contributions from all

Divisions;

• New discoveries in manganese and nickel, highlighting the innovation and vitality within our Company;

• Strong performance of our investments in zinc/copper and iron ore; and • Good market fundamentals for our core commodity suite.

[Slide 5 – FY2007 Financial Performance] Turning to our financial results for the 2007 financial year: the Company posted a net profit after tax of $31.0 million for the financial year. This translated to earnings per share of 13.7 cents, equating to a return on equity of 14%, and enabled us to reinstate dividend payments with a final fully franked dividend of 4.5 cents paid on 31 August 2007. This brought the total annual dividend payout for the year to 6.25 cents per share. This was achieved on a 27% increase in sales revenue (net of hedging losses) to $271.4 million and was driven by solid earnings contributions from each of our core producing businesses. The substantial turnaround in financial performance reflected a combination of cost containment and a continued focus on improving and optimising our operations, coupled with a strengthening in manganese prices towards the end of the financial year.

2

For

per

sona

l use

onl

y

Before turning to our operations in more detail, I would like first discuss our safety record, which was sadly a disappointing aspect of our performance for the year. [Slide 6 –Safety Performance] The health and safety of our employees and contractors remains our number one priority, and we continued to work during the year on strengthening the safety culture at all of our sites and improving our safety performance. However, as I reported at last year’s AGM, tragically one of our Air-leg operators was fatally injured by a falling rock in the Beta Hunt nickel mine in September 2006. The findings of the official investigation into the incident have not as yet been released. The lost time injury frequency rate (LTIFR) for the 2007 financial year increased to 6.8, compared with 5.24 for the previous year. This is very disappointing and is, in my view, a totally unacceptable outcome. Rest assured, we will be working even harder to improve our safety performance over the next 12 months and we have allocated additional resources to achieve this. I am pleased to report that the Group LTIFR to the end of September had fallen modestly to 5.3. Furthermore, by the same period, our Kambalda nickel operations have recorded 12 months without a Lost Time Injury, an LTIFR of zero. This is a pleasing result, and a credit to the efforts of the Kambalda team. Our commitment to continuous improvement in occupational safety and health was recognised during the year with the Woodie Woodie exploration team winning the Chamber of Minerals and Energy Occupational Safety and Health Award. The award was in recognition of their contribution to the design of a purpose-built exploration drilling rig which addresses many safety and health issues inherent in standard rig designs. Continuous improvement and innovation are important aspects of our safety culture. We have a long way to go and there is a lot more work to do in this area. I will continue to work closely with our safety teams to strive to achieve our goal of zero harm to our people. In this regard, we are busy implementing a number of initiatives, including:

• Further strengthening our safety structures and developing our front-line supervisors. • Focusing on work practices and procedures to drive out unsafe activities and acts. • Engendering a culture of employee care and respect for our people's safety.

Our overreaching objective is to build a safety culture through visible leadership, ongoing education and training and a high level of participation by all employees and contractors. We will be continuing to take an uncompromising approach to engaging all of our employees and contractors in this regard. [Slide 7 – Our People] One of the biggest challenges currently facing our industry is maintaining the human resources necessary to underpin the rapid expansion of the sector.

3

For

per

sona

l use

onl

y

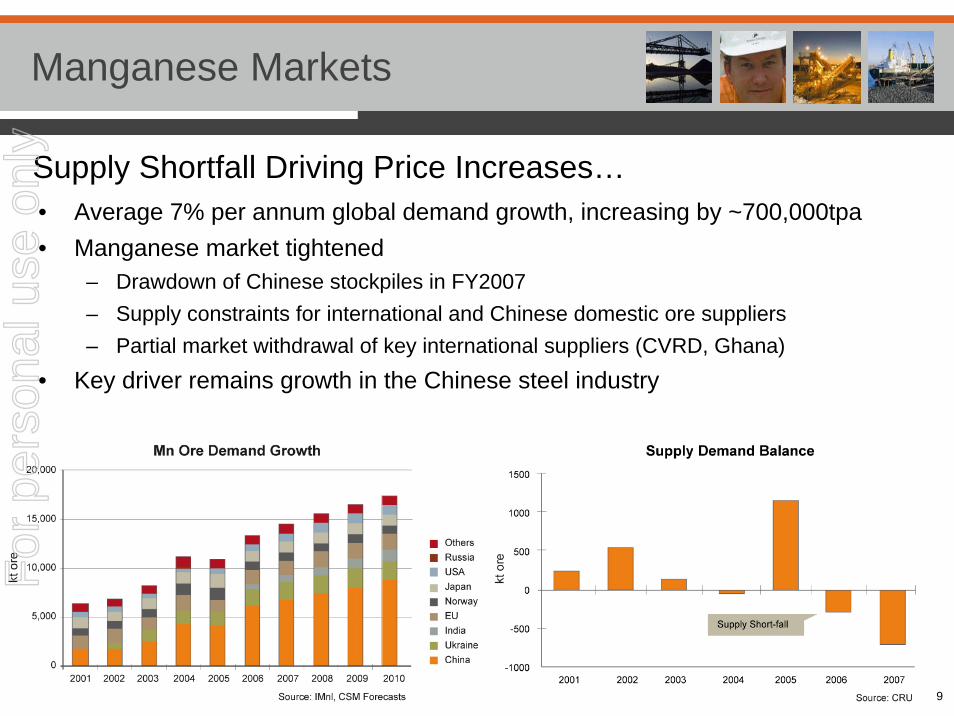

We recognise this and have taken a number of steps during the year to position ourselves to be able to compete successfully in this regard. We established a fully-fledged Human Resources Department for the first time in the Company’s history – and we are continuing to allocate additional resources to this very important and crucial part of our business, with a focus on attraction, retention, and development of our people. To further strengthen the depth of capability within management team, we have recently introduced a company-wide leadership development program. We see the continued development of a high-performance team-oriented culture of operational and technical excellence across the Group as being a key to our future growth success. We will continue to work hard at strengthening our human resource capacity and I believe you will see the results of these efforts becoming evident in our performance in the years ahead. I would now like to briefly review the performance and outlook of each of our business divisions. [Slide 8 – Manganese Division – Overview] Our world-class manganese operations at Woodie Woodie are the backbone of the Company, with production capacity of 1 Mtpa of premium quality manganese ore, giving us a strong strategic position as a niche supplier of up to 10% of the world’s high-grade, internationally traded, manganese ore. The quality of our ore is well recognised in world markets because of its high manganese content, low phosphorus and iron levels, and structural integrity of the product. Another key advantage is the longevity of the Woodie Woodie operation, with a resource base of 15.4 million tonnes and reserves of 8.7 million tonnes, with substantial exploration upside. The Manganese Division delivered a strong overall production performance for the year with a 1.5% increase in production volumes to just over 900,000 tonnes. This was achieved in spite of the significant operational challenges associated with the cyclones that passed through the Pilbara region in March. The response of our operations team to the various business challenges was excellent, with cash operating costs increasing by only 3% to A$2.31/dmtu (compared to A$2.24/dmtu for the previous year). I believe that this is a significant and noteworthy achievement in the current inflationary environment in the Australian resources sector. Manganese prices remained weak for much of the year until supply constraints resulted in a dramatic increase in prices towards the end of the financial year. As a result we saw the average for lump ore for the Second Half of the year increase to US$2.64/dmtu FOB, against a First Half average of US$2.09/dmtu. The price strength of the second half of last year has continued into this financial year. Sales finalised in June for shipment to China between August and October achieved record landed prices in the range of US$7.25-7.50/dmtu CIF for lump ore. [Slide 9 – Manganese Division – Markets] In the main, this is being driven by a combination of unexpected supply shortages on the back of strong demand.

4

For

per

sona

l use

onl

y

Towards the latter part of the last financial year, international manganese supply became very tight. This followed the partial withdrawal of two key international suppliers from the market (namely CVRD and Ghana Manganese). This was exacerbated by a number of smaller supply constraints from other international and Chinese domestic ore producers. Although manganese is typically a non-supply constrained commodity, these emerging supply constraints were the key factors which precipitated the recent price rises. In addition, demand remains strong. The world manganese trade is forecast to grow at around 7% per annum for the next five years, equating to an annual increase of approximately 700,000-800,000 tonnes of high grade ore demand per year. As announced to the market this morning in our Quarterly Report, I am pleased to report that Manganese prices remain firm, with prices negotiated for the December quarter in the range of US$7.65 to US$9.10/dmtu on a landed (CIF) basis. These price increases reflect two messages: the first is the expectation that the manganese market will remain robust this financial year. One of the other main factors behind the increase over the previous quarter is the further increases in freight costs. Freight cost increases are being driven by the global demand for bulk commodities such as iron ore and coal, exacerbated by port infrastructure constraints at some of the major export ports around the world. Indeed we have seen increases in some shipping rate indexes of over 100% this calendar year. These freight costs do impact on the FOB net back price to the company. Notwithstanding the freight increases, the landed prices being negotiated for the November/December period will compensate, with FOB prices net back to the company remaining firm for the period. We expect the manganese market to remain strong in this financial year, with a robust earnings outlook for our manganese division for the current year. [Slide 10 – Manganese Division – Exploration] We continue to step up our exploration activities to replace and expand our resources and reserves position and increase mine life. Last year saw us spend $5.2 million on manganese exploration activities and this will increase significantly this year to $12.2 million. This reflects our increased effort as part of a 2-year programme aimed at expanding our exploration efforts across our highly prospective and extensive 7,500km² land holding. Encouraging results were returned from exploration drilling at several regional prospects including Sardine-Ranchu-Minnow, which are considered to be part of one system, Chutney East, Ghost, and Topvar. Follow-up drilling during the September quarter has confirmed Topvar to be a significant discovery. [Slide 11 – Exploration Success – Rhodes Pit] One of the more exciting discoveries last year was the Rhodes resource underneath and adjacent to the historic Rhodes Mining Pit. Successful drilling programs at the historic Rhodes pit enabled an initial resource of 1.4 million tonnes at 44.4% Mn to be determined, confirming this discovery as the second largest to date in the history of the Woodie Woodie field.

5

For

per

sona

l use

onl

y

[Slide 12 – Manganese Division – Outlook] Looking ahead, we are targeting an increase in manganese production for FY2008 of up to 5% over FY2007 levels, and maintaining a strong focus on cost management. Currently, year to date, the manganese operations are about 40,000 tonnes off budget, due to some challenging mining conditions in our 3 existing operating pits. However, the team is focusing heavily on increasing mining and stripping activity levels, and at this stage we do not expect this to impact our full year guidance. Although cash operating costs are forecast to increase by up to 15% for the year, most of this increase relates to higher manganese royalties as a result of the increase in prices. Our strategy for the manganese business is to continue to seek cost and efficiency improvements and to position this asset to take advantage of market-led production growth. Over $20 million is budgeted for new capital investment at Woodie Woodie to enhance and improve the operation and, as I mentioned, $12.2 million is budgeted for exploration in FY2008 to continue to enhance the resource base. The key driver for this business moving forward will be the significant price increases achieved during the early part of FY2008, which can be expected to flow through to our earnings for the year. The manganese business is ideally placed to benefit from the current tight global market. [Slide 13 – Nickel Division – Overview] Our nickel business comprises an established production base at Kambalda, an emerging production centre nearby at Widgiemooltha, and a substantial portfolio of advanced exploration and development prospects. Together these are providing the foundation for development of a long-life nickel business. Our nickel resource inventory totals 73,300 tonnes at Kambalda and 129,000 tonnes at Widgiemooltha – equating to a total inventory of over 200,000 tonnes of contained nickel, which positions Consolidated Minerals as one of the more significant mid-tier nickel companies in Australia. Nickel is an important growth focus for the company, complementing our established manganese and chromite business units and further enhancing our position as a supplier of raw materials to the carbon steel and stainless steel industries. The 2007 financial year was a particularly challenging year for the Nickel business. Production of 4,178 contained nickel tonnes was below budget, reflecting lower than budgeted initial production volumes from the East Alpha hangingwall ore body, which in turn was due to grade variability in the central mining blocks. As a result, cash unit costs were 47.3% higher at A$7.66/lb against a strongly improved average nickel price of US$11.47/lb (FY2006: US$6.90/lb) – although the carry over of residual hedging positions prevented us from realising the full benefits of the record nickel prices seen during the year. The Beta Hunt mine continued to perform well during the year, with considerable effort on expediting underground mine development in this section to access the Beta West area at the end of the year and bring the 2440 surface into operation at the southern-most portion of the mine.

6

For

per

sona

l use

onl

y

[Slide 14 – Nickel Division – Growth Strategy] For a number of reasons, we believe the nickel business is turning the corner. The focus of our strategy in nickel is to drive our existing operations further down the cost curve and to pursue further production growth. In support of this strategy, we are extending our underground infrastructure to create exploration and mining platforms at our underground operations at Kambalda, and actively developing our Widgiemooltha assets. We continued to invest capital and effort during the year, laying the foundation for future production from our nickel business. A significant proportion of the capital expenditure was directed towards accelerating mine development at East Alpha, and addressing severe ventilation constraints underground. The recent completion of the ventilation shaft provides the necessary ventilation to proceed with the planned underground exploration and mine development drives on the Kambalda Dome, which will commence at the end of the December quarter. [Slide 15 – Nickel Division – Widgiemooltha Development] We also continued to progress the development of our Widgiemooltha nickel tenements during the year, with the overall objective to establish at least two mines in this region over the next two years. In June of this year, we received all of the required environment and mining approvals to enable mining to re-commence at the 132 North deposit. Ore from this deposit will be treated at BHP Billiton’s nickel concentrator under terms similar to the existing arrangement covering our Kambalda operations. The initial development at 132N will comprise a small-scale open pit operation to extract a mining reserve of 40,000 tonnes at 2.6% nickel. Approximately 1,100 contained nickel tonnes will be mined over an estimated 8-month mine life resulting in target production of approximately 600 tonnes of payable nickel. We are also conducting a feasibility study on a potential future underground mining operation at 132N to extract the remaining deeper resource. 132N represents the Company’s first mine development at Widgiemooltha and is expected to be part of a staged development strategy on the Widgiemooltha Dome. [Slide 16 – Nickel Division – Exploration] Our Widgiemooltha portfolio occupies an extensive and high-quality land position covering 227km2, with resources of almost 130,000 tonnes across eight existing deposits. We are working hard to develop a pipeline of growth projects from this region in the coming years. Our exploration effort is focusing on five highly prospective areas. This effort has already paid dividends with the new Gillet discovery, which appears to be one of the more significant deposits seen in this region in many years. [Slide 17 – Nickel Division – Outlook] Looking ahead - Nickel will continue to be a key growth driver for the Company, with our focus during the 2008 financial year on increasing production by up to 50%. In addition, we are making a strong push towards investment in exploration, new infrastructure, and mine development, while continuing to progress the East Alpha production base.

7

For

per

sona

l use

onl

y

Nickel production this year will be largely sourced from Kambalda. The improvement in production is expected to become more apparent in the second half of the current financial year, underpinning our objective to continue to grow production over the next 5 years. Cash operating costs are targeted at similar levels to FY2007. On the exploration front, our nickel exploration budget this year is $10 million, and forms part of a two-year program designed to convert nickel endowment into mineral resources. Furthermore, given the expiry of the metal hedges, the nickel division is better placed to take advantage of any price upside. [Slide 18 – Chromite Division – Overview] Our chromite business has been a solid contributor to the Group. The Division delivered a very strong operational performance for the 12 months to 30 June 2007, with production of 256,936 tonnes and a 7% reduction in cash costs to A$120.07/tonne. The operation also generated a strongly improved cash margin for the year, with the average received price for chromite for the year increasing by 27% to US$160.51/tonne (FY2006: US$125.73/tonne). The continued strength that we are observing in the global chromite market is largely driven by the growth in Chinese stainless steel production, coupled with additional pressure on supply through a new export tax imposed on Indian exports. The recent increase in chromite prices to around US$200/tonne for the September 2007 Quarter highlights the continued strong market for chromite. [Slide 19 – Other Commodities] Our investments in new business performed particularly well during the year, as we continued to broaden our portfolio of investments. Late in 2006 we reached agreement to combine our non-core Shaw River iron ore exploration assets with the neighbouring assets of Alkane Exploration Limited in a new company, BC Iron, and went on to complete a successful listing on the Australian Securities Exchange in December of 2006. Our investments in both BC Iron (27.7%) and Jabiru Metals Ltd (27.4%) appreciated considerably during the year and, as at 30 June 2007, our unrealised profit from these investments was around $170 million. Pilbara Iron Ore Pty Ltd, a 100% owned subsidiary of Consolidated Minerals, holds our other Pilbara iron ore interests, which are focused on the Mindy Mindy Project, 60 kilometres northwest of Newman. This is a 50/50 venture with Fortescue Metals Group Limited. Drilling at Mindy Mindy has defined a resource of 44.8 million tonnes at grades of 55.2% Fe, over approximately one third of the total channel iron deposit strike length of 16 kilometres. This includes a high-grade component of 15.5 million tonnes at iron grades of 57.1%. A Feasibility Study on the development of an ore project at Mindy Mindy is currently underway and is due to be completed by the end of this calendar year.

8

For

per

sona

l use

onl

y

The recent Supreme Court decision relating to the rights of the Joint Venture over one of the tenements of the Mindy Mindy tenement package has provided welcome certainty around the Joint Venture arrangement with our JV partner. [Slide 20 – Summary Guidance] In summary, this slide captures our previously announced guidance for the financial year, showing our production targets and cost targets. [Slide 21 – Outlook] To sum up, the return to solid profitability and the turnaround in operational performance achieved during the 2007 financial year has provided a strong platform for Consolidated Minerals to take advantage of increased commodity prices and production volumes during the 2008 financial year. Importantly, we have been able to restore the financial health of the Company and turn around our core businesses during what was, in many respects, a challenging year. The Company will continue to focus on enhancing and optimising the Woodie Woodie manganese operation, while at the same time growing production to meet demand. Nickel will also continue to be a key growth driver with our focus on increasing production and achieving higher returns, along with a major push towards investment in new infrastructure and mine development with the commencement of the Twin decline exploration and development project, and new mines at Widgiemooltha. With strong levels of planned investment across the Company, production growth, a high level of exploration, and a strong commitment to continue to build the business, I believe that we are very well placed to build on what we have started last financial year and enjoy a year of strong growth, profitability and returns to our shareholders. In conclusion, I would like to thank my fellow Directors and the members of our senior management team, who have provided outstanding support to me throughout what has been a very challenging but ultimately very rewarding year. It is thanks to their efforts and commitment that the Company is now well placed to reap the benefits of strong commodity prices, new opportunities and high levels of investor interest in our Company. I would like to thank you for your attention, and I would be happy to answer any questions on any aspect of our business and operations. Thank you.

END

9

For

per

sona

l use

onl

y

2007 Annual General Meeting25 October 2007

Rod BaxterManaging Director

For

per

sona

l use

onl

y

2

Forward Looking Statements

This presentation may include forward-looking statements.

These forward-looking statements are based on management’s expectations and beliefs concerning future events.

Forward-looking statements are necessarily subject to risks, uncertainties and other factors, many of which are outside the control of Consolidated Minerals Limited, that could cause actual results to differ materially from such statements.

Consolidated Minerals Limited gives no assurance that the eventsexpressed or implied in the forward looking statements in this presentation will actually occur and makes no undertaking to subsequently update or revise the forward-looking statements made in this presentation to reflect events or circumstances after the date of this release.

Record FY2008 prices: Aug – Oct US$7.25-7.50/dmtu CIF

Manganese DivisionOverview

For

per

sona

l use

onl

y

9

• Average 7% per annum global demand growth, increasing by ~700,000tpa• Manganese market tightened

– Drawdown of Chinese stockpiles in FY2007– Supply constraints for international and Chinese domestic ore suppliers– Partial market withdrawal of key international suppliers (CVRD, Ghana)

• Key driver remains growth in the Chinese steel industry

Supply Shortfall Driving Price Increases…

Manganese MarketsF

or p

erso

nal u

se o

nly

10

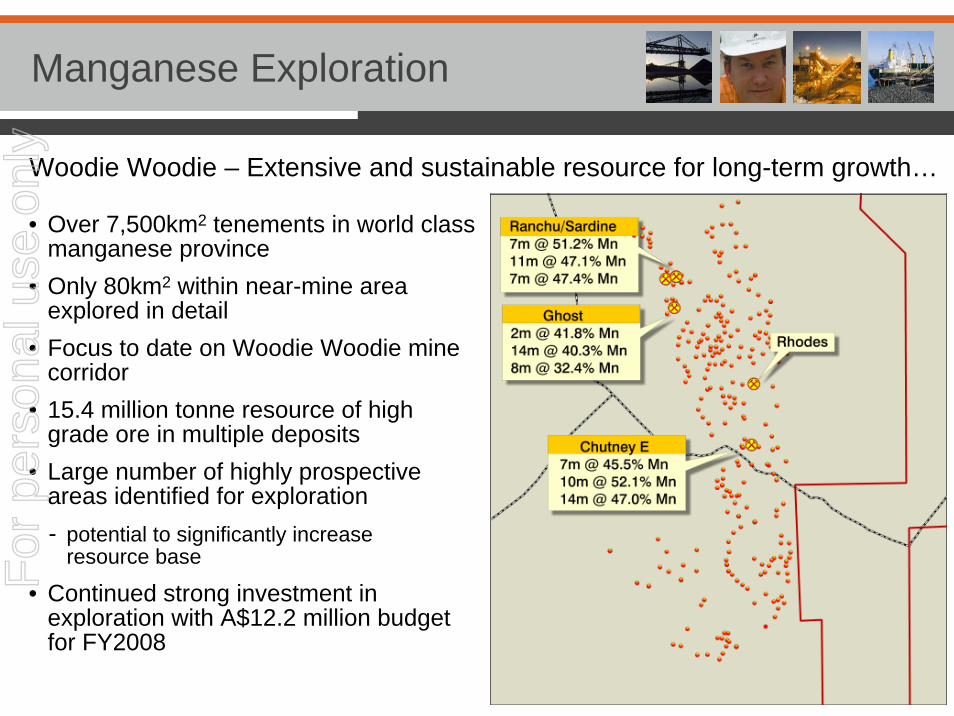

Woodie Woodie – Extensive and sustainable resource for long-term growth…

• Over 7,500km2 tenements in world class manganese province

• Only 80km2 within near-mine area explored in detail

• Focus to date on Woodie Woodie mine corridor

• 15.4 million tonne resource of high grade ore in multiple deposits

• Large number of highly prospective areas identified for exploration- potential to significantly increase

resource base

• Continued strong investment in exploration with A$12.2 million budget for FY2008

Manganese ExplorationF

or p

erso

nal u

se o

nly

11

Rhodes Discovery – Further exploration success…• Significant new manganese discovery• Adjacent to historic pit mined in the 1950s• 2nd largest discovery in Woodie Woodie

manganese field• Initial resource of 1.4mt @ 44.4% Mn

Plan view of Rhodes Pit resource shapes

Rhodes Pit Discovery Hole

Manganese Exploration

DISCOVERY HOLE70M @ 51.2% Mn

DISCOVERY HOLE70M @ 51.2% Mn

For

per

sona

l use

onl

y

12

• Targeting production increase by up to 5% for FY2008 with emphasis on operational improvement and cost management

• Cash operating costs expected to rise by up to 15% (led by higher manganese royalties)

• $20 million budgeted in new capital investment • Growing production to meet demand• Strong price outlook• Continued strong investment in exploration, substantial resource upside

Woodie Woodie – World class asset, premium product…

Manganese DivisionFY2008 Outlook

For

per

sona

l use

onl

y

13

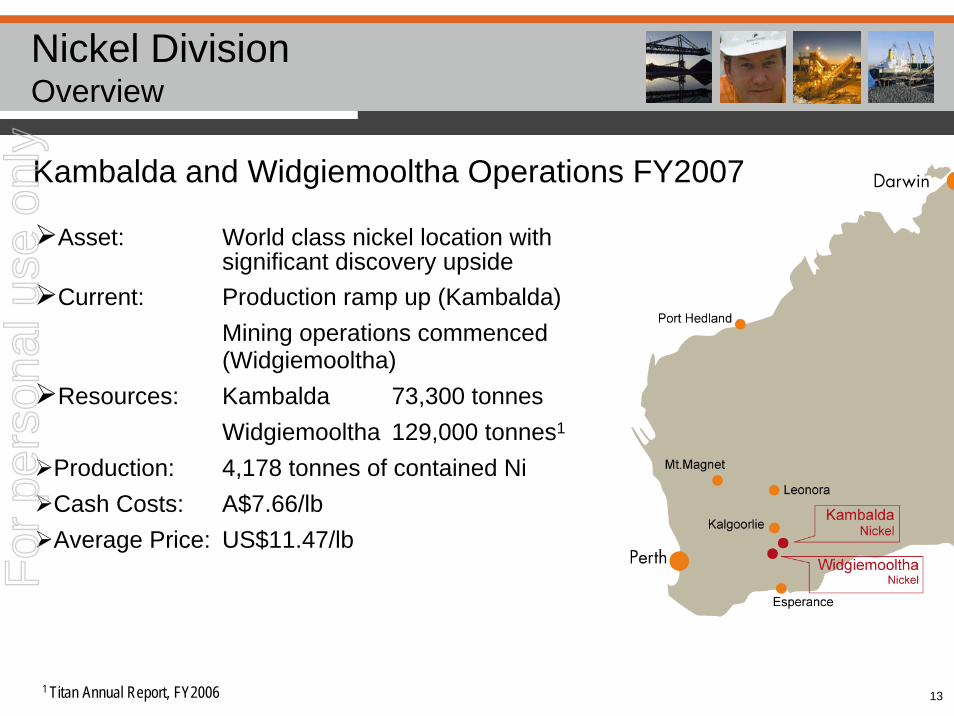

Kambalda and Widgiemooltha Operations FY2007

Asset: World class nickel location withsignificant discovery upside

Current: Production ramp up (Kambalda)Mining operations commenced (Widgiemooltha)

Production: 4,178 tonnes of contained NiCash Costs: A$7.66/lbAverage Price: US$11.47/lb

1 Titan Annual Report, FY2006

Nickel DivisionOverview

For

per

sona

l use

onl

y

14

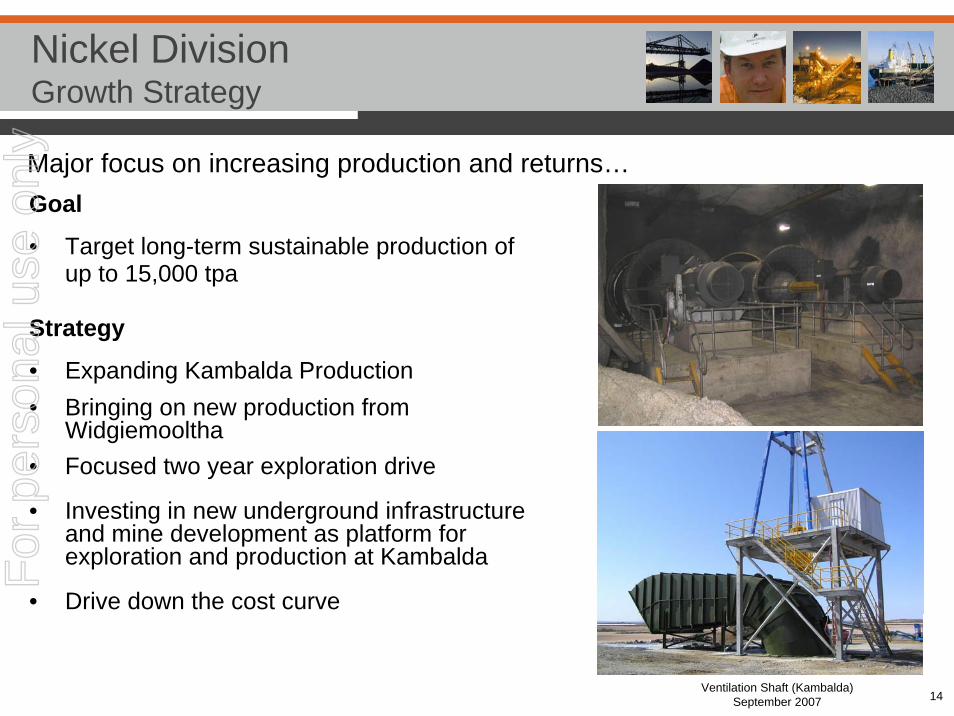

Major focus on increasing production and returns…Goal

• Target long-term sustainable production of up to 15,000 tpa

Strategy

• Expanding Kambalda Production• Bringing on new production from

Widgiemooltha• Focused two year exploration drive

• Investing in new underground infrastructure and mine development as platform for exploration and production at Kambalda

• Drive down the cost curve

Nickel DivisionGrowth Strategy

Ventilation Shaft (Kambalda) September 2007

For

per

sona

l use

onl

y

15

• Potential for 2-3 mining operations within 2 years• First mine development underway at 132 North • Pipeline of growth projects

132 North: - Mining Reserve of 40,000t Ni @ 2.6%- Extraction of 1,100t contained nickel - 8 month mine life for 600t of payable nickel- Feasibility study underway to mine deeper resource

Nickel DivisionWidgiemooltha Development

For

per

sona

l use

onl

y

16

Broadening the growth horizon…

• Extensive and prospective land position ( 227km2)

• Eight existing deposits with combined resource of up to 130,000 tonnes

• Multiple prospects from EM targets

• Focus on five highly prospective areas

• Significant deposit found at Gillet Prospect

Nickel DivisionWidgiemooltha Exploration

For

per

sona

l use

onl

y

17

Nickel DivisionFY2008 Outlook

• Key growth division – targeting 50% increase in production in FY2008

• $10m exploration budget for FY2008

• Targeting expansion up to 15,000 tonnes contained Ni production

• Move down the cost curve through cost management, operational efficiencies, and economies of scale

• Production unhedged at this stage

For

per

sona

l use

onl

y

18

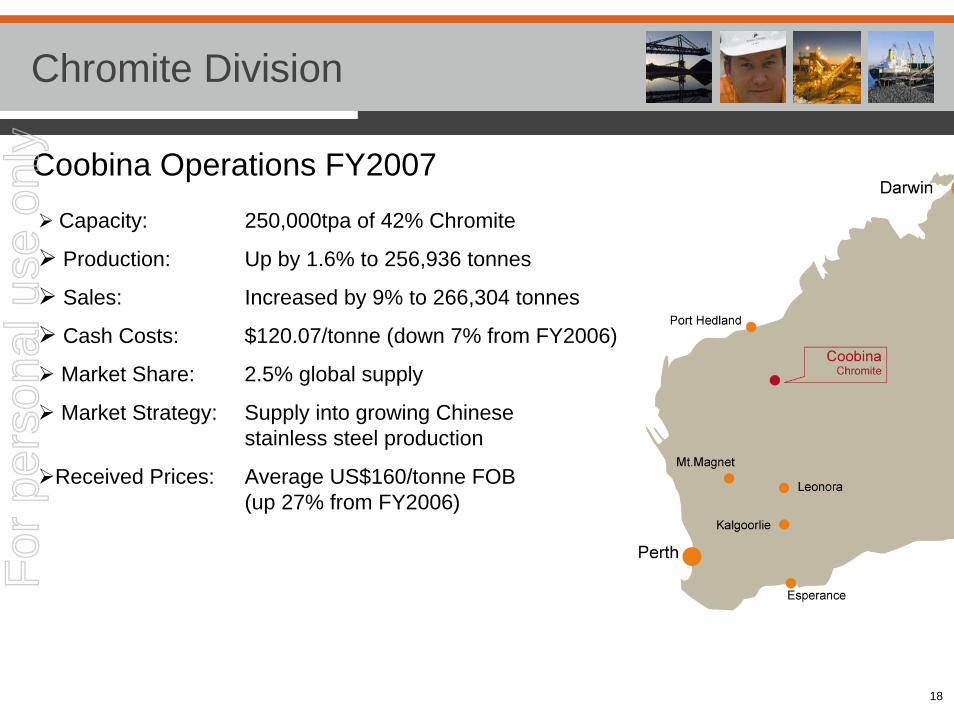

Coobina Operations FY2007Capacity: 250,000tpa of 42% Chromite

Production: Up by 1.6% to 256,936 tonnes

Sales: Increased by 9% to 266,304 tonnes

Cash Costs: $120.07/tonne (down 7% from FY2006)

Market Share: 2.5% global supply

Market Strategy: Supply into growing Chinese stainless steel production

Received Prices: Average US$160/tonne FOB (up 27% from FY2006)

Chromite DivisionF

or p

erso

nal u

se o

nly

19

Copper/Zinc/Iron Ore…Jabiru Metals Limited (JML) (CSM 27.4%)• Now in production• Significant exploration upside• Unrealised profit of A$138.2 million (as at 30 June 2007)

Mindy Mindy Iron Ore Joint Venture (CSM 50%)• Strategic option on future iron ore production in Pilbara region• Mindy Mindy resource estimate over 1/3 CID strike = 44.8

million tonnes @ 55.2% Fe

BC Iron Limited (BCI) (CSM 27.7%)• Early exploration success in targeting Channel Iron Deposits

to 58% Fe, have been identified within Nullagine Project• New phase of drilling underway• Potential to delineate strategically located resources• Unrealised profit of A$26.6 million (as at 30 June 2007)

Other CommoditiesF

or p

erso

nal u

se o

nly

20

Summary Guidance

Commodity Production (tonnes) Cash Costs

Increase by up to 5%

Increase by up to 50%

Steady state

Manganese A$2.45 - 2.65/dmtu

Nickel A$6.75 – 7.50 /payable lb*

Chromite A$127-140 / tonne

• Manganese: major profit driver, production to increase, prices remaining robust

• Nickel: key growth driver, target up to 15,000 tpa

• Chromite: steady cash flow generator

Forecast Targets for FY2008

*Kambalda Operations

For

per

sona

l use

onl

y

21

• Significant turnaround achieved in FY2007

• Highly motivated management team focused on building a strong, diversified Australian mining company

• Significant investment in growth across the company

• Nickel production expansion blueprint now in place

• Strong potential for further exploration success

• Company now has solid foundation following operational enhancements, new productivity initiatives and cost containment

• Commodities price strength

Substantial increase in profitability expected

Continued strength through growth and acquisitions…