CONSTRUCTING MARKETS AND SHAPING BOUNDARIES: ENTREPRENEURIAL POWER IN NASCENT FIELDS FILIPE M. SANTOS INSEAD KATHLEEN M. EISENHARDT Stanford University We examine how entrepreneurs shape organizational boundaries and construct mar- kets through an inductive, longitudinal study of five ventures. Our central contribution is a framework of how successful entrepreneurs attempt to dominate nascent markets by co-constructing organizational boundaries and market niches using three processes: claiming, demarcating, and controlling a market. We propose that power is the un- derlying boundary logic and indicate the “soft-power” strategies by which entrepre- neurs compete in highly ambiguous markets. Overall, we develop a holistic view of organizational boundaries and offer insights into institutional entrepreneurship and resource dependence theories. Our most important contribution is reinvigorating the study of interorganizational power. Organizational boundaries are fundamental. Ev- ery organization needs to establish its boundary to distinguish the organization from the environment and define its domain of action (Aldrich & Ruef, 2006; Scott, 2003). Given this central role, the phe- nomenon of organizational boundaries has been addressed with a set of rich theoretical perspectives (Santos & Eisenhardt, 2005). A first line of research adopts an exchange efficiency view, looking at cost minimization as a key driver of boundaries (Dyer, 1996; Williamson, 1981, 1991). In a second stream, organizational boundaries are examined through a power lens, with a focus on how organizations can control their exchange relations (Pfeffer & Salancik, 1978; Thompson, 1967). Other research relies on a competence view, in which the evolving resources and capabilities of organizations shape their boundaries (Brusoni, Prencipe, & Pavitt, 2001; Pen- rose, 1959; Peteraf, 1993). A fourth line of research adopts an identity perspective, focusing on the cog- nitive frames of organization members that define “who we are” as an organization and shape the choice of boundaries (Dutton & Dukerich, 1991; Porac, Thomas, Wilson, Paton, & Kanfer, 1995; Tripsas, 2009). Yet, in contrast to the richness of these theoreti- cal perspectives, the range of research designs for studying organizational boundaries has been nar- row. Indeed, much empirical research represents an atomistic view that focuses primarily on the antecedents of single-boundary decisions in cross- sectional samples (David & Han, 2004). The origin of the atomistic view lies primarily in the early influence of exchange efficiency conceptions of boundaries, notably transaction cost economics (TCE), for which the canonical problem is whether to internalize or outsource a specific transaction (Williamson, 1985). This problem formulation has led to the dominant approach of analyzing organi- zational boundaries as discrete structural alterna- tives such as make or buy. As a result, much em- pirical research examines boundary decisions in isolation, as if the shaping of organizational bound- aries were simply the accumulation of independent boundary decisions in well-structured settings. Al- though research has moved from efficiency-based theoretical explanations to include other decision drivers, such as competencies (Argyres, 1996; Jaco- bides & Hitt, 2005; Poppo & Zenger, 1998), the earlier mind-set of focusing on independent bound- We gratefully acknowledge the research support pro- vided by the Stanford Technology Ventures Program and INSEAD R&D. We appreciate the thoughtful comments of Charles Galunic, Morten Hansen, Sarah Kaplan, Riitta Katila, Woody Powell, Ray Levitt, Rory McDonald, Huggy Rao, Kaye Schoonhoven, Wes Sine, Bob Sutton, Patricia Thornton, and seminar participants at Stanford University, INSEAD, the University of Colorado, the Uni- versity of California, Berkeley, Harvard University, the University of Maryland, and Oxford University; and at the Queen’s University Alliance Edge Conference, Prince Bertil Symposium, West Coast Research Symposium on Technology Entrepreneurship, Atlanta Competitive Ad- vantage Conference, and inaugural LBS Entrepreneur- ship Conference. We also acknowledge the valuable con- tributions of Sara Rynes-Weller and three anonymous AMJ reviewers. Academy of Management Journal 2009, Vol. 52, No. 4, 643–671. 643 Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s express written permission. Users may print, download or email articles for individual use only.

Transcript

CONSTRUCTING MARKETS AND SHAPING BOUNDARIES:ENTREPRENEURIAL POWER IN NASCENT FIELDS

FILIPE M. SANTOSINSEAD

KATHLEEN M. EISENHARDTStanford University

We examine how entrepreneurs shape organizational boundaries and construct mar-kets through an inductive, longitudinal study of five ventures. Our central contributionis a framework of how successful entrepreneurs attempt to dominate nascent marketsby co-constructing organizational boundaries and market niches using three processes:claiming, demarcating, and controlling a market. We propose that power is the un-derlying boundary logic and indicate the “soft-power” strategies by which entrepre-neurs compete in highly ambiguous markets. Overall, we develop a holistic view oforganizational boundaries and offer insights into institutional entrepreneurship andresource dependence theories. Our most important contribution is reinvigorating thestudy of interorganizational power.

Organizational boundaries are fundamental. Ev-ery organization needs to establish its boundary todistinguish the organization from the environmentand define its domain of action (Aldrich & Ruef,2006; Scott, 2003). Given this central role, the phe-nomenon of organizational boundaries has beenaddressed with a set of rich theoretical perspectives(Santos & Eisenhardt, 2005). A first line of researchadopts an exchange efficiency view, looking at costminimization as a key driver of boundaries (Dyer,1996; Williamson, 1981, 1991). In a second stream,organizational boundaries are examined through apower lens, with a focus on how organizations cancontrol their exchange relations (Pfeffer & Salancik,1978; Thompson, 1967). Other research relies on acompetence view, in which the evolving resources

and capabilities of organizations shape theirboundaries (Brusoni, Prencipe, & Pavitt, 2001; Pen-rose, 1959; Peteraf, 1993). A fourth line of researchadopts an identity perspective, focusing on the cog-nitive frames of organization members that define“who we are” as an organization and shape thechoice of boundaries (Dutton & Dukerich, 1991;Porac, Thomas, Wilson, Paton, & Kanfer, 1995;Tripsas, 2009).

Yet, in contrast to the richness of these theoreti-cal perspectives, the range of research designs forstudying organizational boundaries has been nar-row. Indeed, much empirical research representsan atomistic view that focuses primarily on theantecedents of single-boundary decisions in cross-sectional samples (David & Han, 2004). The originof the atomistic view lies primarily in the earlyinfluence of exchange efficiency conceptions ofboundaries, notably transaction cost economics(TCE), for which the canonical problem is whetherto internalize or outsource a specific transaction(Williamson, 1985). This problem formulation hasled to the dominant approach of analyzing organi-zational boundaries as discrete structural alterna-tives such as make or buy. As a result, much em-pirical research examines boundary decisions inisolation, as if the shaping of organizational bound-aries were simply the accumulation of independentboundary decisions in well-structured settings. Al-though research has moved from efficiency-basedtheoretical explanations to include other decisiondrivers, such as competencies (Argyres, 1996; Jaco-bides & Hitt, 2005; Poppo & Zenger, 1998), theearlier mind-set of focusing on independent bound-

We gratefully acknowledge the research support pro-vided by the Stanford Technology Ventures Program andINSEAD R&D. We appreciate the thoughtful comments ofCharles Galunic, Morten Hansen, Sarah Kaplan, RiittaKatila, Woody Powell, Ray Levitt, Rory McDonald,Huggy Rao, Kaye Schoonhoven, Wes Sine, Bob Sutton,Patricia Thornton, and seminar participants at StanfordUniversity, INSEAD, the University of Colorado, the Uni-versity of California, Berkeley, Harvard University, theUniversity of Maryland, and Oxford University; and atthe Queen’s University Alliance Edge Conference, PrinceBertil Symposium, West Coast Research Symposium onTechnology Entrepreneurship, Atlanta Competitive Ad-vantage Conference, and inaugural LBS Entrepreneur-ship Conference. We also acknowledge the valuable con-tributions of Sara Rynes-Weller and three anonymousAMJ reviewers.

� Academy of Management Journal2009, Vol. 52, No. 4, 643–671.

643

Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s expresswritten permission. Users may print, download or email articles for individual use only.

ary decisions at specific stages in the “value chain”has largely prevailed.

Although understanding single-boundary deci-sions is valuable, this emphasis neglects potentialrelationships among decisions, ignores the inter-play of different boundary-setting mechanisms(e.g., alliances with key partners, identity position-ing, acquisitions), and does not address the evolu-tion of organizational boundaries (Santos & Eisen-hardt, 2005). Thus, it constrains understanding ofhow organizational actors actually conceptualizeand execute boundary work. In particular, this at-omistic emphasis leads to “losing sight of the forestfor the trees” (Jacobides & Hitt, 2005: 1209) byobscuring how individual boundary decisionsmight fit into overall patterns of strategic action.Thus, research designs that permit exploring theevolution of organizational boundaries and capturethe micro details of boundary work may reveal newinsights. Our aim is to address this research oppor-tunity by exploring the shaping of organizationalboundaries over time by new firms in nascent mar-kets. In this setting, the very beginning of organiza-tional life, boundary work is both crucial for sur-vival and poorly explained by current theories.

Nascent markets are business environments in anearly stage of formation, often appearing in emerg-ing “organizational fields” (Aldrich & Fiol, 1994).Nascent markets are characterized by undefined orfleeting industry structure (Eisenhardt, 1989a;Rindova & Fombrun, 2001), unclear or missingproduct definitions (Hargadon & Douglas, 2001),and lack of a dominant logic to guide actions(Kaplan & Tripsas, 2008; Porac, Ventresca, &Mishina, 2002). Thus, nascent markets constituteunstructured settings with extreme ambiguity. Fol-lowing organizational theory (Davis, Eisenhardt, &Bingham, in press; Weick, 1995), we define ambi-guity as lack of clarity about the meaning and im-plications of particular events or situations. Ambi-guity arises from unknown cause-effect relationsand lack of recurrent, institutionalized patterns ofrelations and actions (Aldrich & Fiol, 1994). Ambi-guity thus leads to confusion and multiple poten-tial interpretations. It differs from uncertainty,which refers to inability to predict the probabilityof specific outcomes (Davis et al., in press; Weick,1995), a situation that current boundary theories,especially those based on efficiency and resourcedependence logics, can deal with well.

Nascent markets are an intriguing setting inwhich to explore organizational boundaries be-cause these markets pose unique problems for or-ganizational actors. Executives operating in nas-cent markets typically lack a clear view of industrystructure; they may not know, for instance, which

organizations are their best prospects as customers,partners, competitors, and suppliers (Rindova &Fombrun, 2001). Thus, they are often unable tospecify cost functions (Gilbert, 2005), primary de-pendence relationships (Rao, 1994), competenciesthat are strategically valuable within the industry(Bingham, Eisenhardt, & Davis, 2009), and legiti-mated industry logics to guide action (Aldrich &Fiol, 1994; Kaplan & Murray, forthcoming). Suchmarkets both enable and reward strategic action byorganizational actors (Ozcan & Eisenhardt, 2009),yet it is unclear how existing theories of organiza-tional boundaries might apply in nascent marketswhere the basic elements of industry structure areambiguous, evanescent, or nonexistent.

New firms compound the problems of nascentmarkets. In contrast to established firms, youngventures typically have incipient activities and re-sources (Burton & Beckman, 2007; Rindova &Kotha, 2001), a fluid or nonexistent identity(Lounsbury & Glynn, 2001; Rindova & Kotha,2001), and little power to influence other firms(Hallen, 2009; Ozcan & Eisenhardt, 2008). Also,they face major strategic hurdles that make sur-vival, not efficiency, crucial (Graebner, 2004).These characteristics imply a set of firm attributesthat are not well addressed by existing boundarytheories, with their focus on established firms withsubstantial resources. Yet, at the same time, it islikely that the vulnerability of new firms makesorganizational boundaries pivotal. Given these ob-servations, the research setting of new firms in nas-cent markets seems likely to provide an excellentopportunity to extend current theories and revealnovel insights.

Scholars have begun to study boundary-relatedissues for new firms in nascent markets. One themecenters on cognitive and sociopolitical legitimacy(Aldrich & Fiol, 1994; Rao, 1994). Although muchof this work explores how institutional actors actcollectively to legitimate an emerging set of activi-ties (Leblebici, Salancik, Copay, & King, 1991;Rindova & Fombrun, 2001; Sine & David, 2003), afew studies address how entrepreneurs organizetheir own firms. For example, Rindova and Kotha(2001) examined how Yahoo executives used iden-tity to shape their actions in the nascent Internetsearch market. Similarly, Hargadon and Douglas(2001) studied Edison’s tactics for establishing thenascent electricity industry by framing it as cogni-tively proximate to the established gas lighting in-dustry. Although useful, these and other studies ofcognitive processes in ambiguous environmentsneither focus on boundaries per se nor address therich set of possible boundary theories and availablemechanisms (Santos & Eisenhardt, 2005).

644 AugustAcademy of Management Journal

A second theme is interfirm relationships (Pow-ell, Koput, & Smith-Doerr, 1996). Much of this workcenters on single-boundary decisions using re-source dependence and social network logics(Eisenhardt & Schoonhoven, 1996; Gulati & Hig-gins, 2003), but a few studies examine entrepre-neurs as they form holistic patterns of ties. Forexample, Powell and colleagues (1996) observedthat biotechnology ventures that form many tiesearly on gain valuable resources and attain morecentral network positions. Similarly, Ozcan andEisenhardt (2009) found that entrepreneurs whoengage in a strategy of forming multiple ties simul-taneously create more successful alliance portfo-lios. Hallen (2009) observed several alternativestrategies for forming successive ties in the garner-ing of resources from venture investors. But like theresearch on cognitive and sociopolitical legitimacy,these efforts neither focus directly on boundariesnor include a rich set of boundary mechanisms andtheoretical logics.

Overall, extant boundary research primarily ex-amines atomistic boundary choices in well-struc-tured organizations and environments. A few stud-ies take a longitudinal view and focus on emergingfields, yet they typically use a single theoreticallens and do not address boundary setting per se.Thus, there is a superb opportunity to develop amore complete and theoretically rich understand-ing of boundaries. We seek to extend current theoryand create new insights by studying the boundary-shaping processes of new firms in nascent markets.We ask, How do entrepreneurs addressing nascentmarkets shape their organizational boundariesover time?

Our research design is a multiple-case, inductivestudy that uses in-depth archival and field data totrack closely how entrepreneurs at five new firmsin different nascent markets shaped their organiza-tional boundaries during the initial years of organ-izational life. This design uses a research setting inwhich organizational boundaries are crucial, un-derexplored, and underserved by current theories.It also enables a longitudinal view and addresses abroad range of boundary mechanisms and theories,thus ensuring that we capture the richness andinterrelationships of boundary work. As such, ourresearch is consistent with recent calls for strategicand longitudinal studies of boundaries (Jacobides &Billinger, 2006; Santos & Eisenhardt, 2005).

Our central theoretical contribution is a holisticframework of the longitudinal processes by whichsuccessful entrepreneurs shape their organizationalboundaries and construct new markets. We findthat actors rely on multiple boundary mechanismscentered on three processes: claiming a market,

demarcating the market, and controlling it. Theseprocesses generate cognitive (identity-based), rela-tional (alliance-focused), and resource (acquisition-driven) structures for firm boundaries and nascentmarkets. We contribute to institutional entrepre-neurship by emphasizing novelty and dominance,not just fitting in and legitimacy. We also extendresource dependence theory to ambiguous environ-ments and entrepreneurial actors. Our key insightis that power is the unifying boundary logic. Bypower, we mean the ability of an actor to influencethe behavior of others in ways that produce out-comes favored by the focal actor (Pfeffer & Salancik,1978). In particular, we highlight how entrepre-neurs use soft-power strategies based on subtle per-suasion to dominate new markets, rather than tra-ditional hard-power tactics of coercion based onextensive resource control (Nye, 2004). Our keycontribution is thus reinvigorating the study ofinterorganizational power and reaffirming thatagency and strategic action often rest on the ration-ale of power, however subtly exercised.

METHODS

Research Design and Setting

We used an inductive, multiple-case research de-sign (Eisenhardt, 1989b). Multiple cases permit areplication logic in which cases are treated as ex-periments, with each serving to confirm or discon-firm inferences drawn from the others (Yin, 1994).This process typically yields more robust, general-izable theory than single cases (Eisenhardt & Graeb-ner, 2007). Our design embeds three units of anal-ysis: boundary decision, organization, and market.

The research setting is the confluence of comput-ing, electronics, and telecom industries in the midnineties. At this time, many innovations, such asdistributed computing, electronic messaging, andInternet commerce, began to gain widespread ac-ceptance. This setting was attractive because of theemergence of numerous nascent markets in thisindustry confluence and the related burst of entre-preneurial foundings. Our focus is the evolution ofthe organizational boundaries of five new firms.These firms were selected in mid 2000 from thepopulation of U.S. firms founded in late 1994 andearly 1995. This timing was attractive because itcorresponded to the period of highest ambiguity—that is, just prior to the take-off of the Internet-related sector (Sine, Mitsuhashi, & Kirsch, 2006).This period was sufficiently distant to allow longi-tudinal patterns to emerge and yet sufficiently re-cent to allow accurate, detailed data collection atthe time of our study.

2009 645Santos and Eisenhardt

Having defined the study’s population, we thencreated a diverse sample. We selected firms ad-dressing five distinct types of nascent markets: vir-tual marketplace, digital services, online com-merce, distributed enterprise software, andnetworking hardware. We also selected firms withdistinct founding contexts, founding teams, andinitial funding. The entrepreneurs ranged from alone engineer who stumbled serendipitously intoan opportunity, to entrepreneurs who owned atechnology and were searching for a market oppor-tunity, to seasoned executives with detailed busi-ness plans and strong ties to professional investors.Table 1 summarizes the diverse characteristics ofthe sampled firms. Studying such a diverse set offirms offered firmer grounding of theory thanstudying a more homogeneous one (Harris & Sut-ton, 1986).

Given our aim of understanding how organiza-tional actors shape boundaries, we employed a lon-gitudinal design that comprehensively tracks mul-tiple boundary decisions during the firms’ initial

five years. This design required that we study firmswith rich archival histories and willingness to grantdiverse, multiple interviews. These criteria furthernarrowed our choice to the five firms that we se-lected. Although our firms may be longer-livedthan many new firms, a sufficient history for eachfirm was necessary to understand the temporal dy-namics of setting boundaries. This requirementoutweighed having a random sample, especially ina process-focused and theory-building study suchas ours (Siggelkow, 2007). Similarly, although ourfirms were more successful than most new firms,they nonetheless exhibited much variation in theirboundary decisions and outcomes, such as failedactions and major mistakes, bringing useful vari-ance to our theory building.

Data Collection

We focused data collection on tracking theboundary decisions of each firm during its first fiveyears. In keeping with our interest in a rich and

External informants Industry expert Industry expert Industry expert Industry expert Industry expertCompetitor Partner Competitor Competitor CompetitorEx-employee Ex-employee Ex-employee PartnerPartner

a All firms were founded between late 1994 and mid 1995 in the United States and eventually went public. The names used here arepseudonyms.

646 AugustAcademy of Management Journal

longitudinal understanding of organizational bound-aries, we broadly defined a boundary decision as anorganizational choice that shapes the demarcationof an organization relative to its environment (San-tos & Eisenhardt, 2005; Scott, 2003). This broaddefinition allowed us to focus our inquiry on shap-ing boundaries while avoiding a restrictive theoret-ical or empirical lens. For example, this expansiveapproach includes boundaries specified by a firm’sresource portfolio (Brusoni et al., 2001), sphere ofinfluence (Pfeffer & Salancik, 1978), organizationmembers’ cognitive mind-set (Tripsas & Gavetti,2000), and governance of activities (Williamson,1991). Examples of boundary decisions are acquir-ing a firm, ending an alliance, redefining organiza-tional identity, and making an outsourcing choice.

We relied on two primary data sources: archivesand interviews. We began data collection by gath-ering extensive archival data from both internaland external sources. The internal sources in-cluded all press releases since firm founding (about50 per year per firm), Securities and ExchangeCommission (SEC) filings and initial public offer-ing (IPO) prospectuses (approximately 1,000–1,200pages per firm), internal reports and presentations(about 70–150 pages per firm), as well as video andaudio archives of presentations made by firm exec-utives at various points in time (an average of fourper firm). The external sources included media ar-ticles about each firm identified using ABI Inform.We located about 80 to 200 articles per firm, usingthe firm name as a keyword. We complementedthese sources with analyst reports, books abouteach firm when available, and media articles aboutcompetitors and the relevant nascent markets. Us-ing these very extensive archival data, we devel-oped chronological case histories for each firm.Each case was about 60 pages long and took abouttwo months to write. We began by developing achronological list of boundary decisions for eachfirm and then used these decisions to structure thecase histories. We organized the cases by year, de-tailing the relevant boundary decisions. We devel-oped tables and graphs for each case, includingtracking key metrics (e.g., revenue, market share,employees, and growth rates) and changes in thecomposition of the executive team (Miles & Huber-man, 1994).

We continued data collection using a second pri-mary source: semistructured interviews with inter-nal and external informants. We conducted an av-erage of 9 interviews per firm, accumulating a totalof 46 interviews from early 2001 to mid 2002. Ourfirst interview was typically with the CEO and/orfounder and lasted several hours. We used thisinterview to identify major boundary decisions,

which we then matched with those identified inthe archival material, thus triangulating the data.We defined a boundary decision for our informantsusing our formal definition (given above) andadded conceptually consistent lay language, de-scribing such decisions as “choices that shape firmscope and its domain of action.” These first inter-views were very helpful in validating the initial listof boundary decisions. A key advantage was iden-tifying decisions that were unavailable in archivalsources (e.g., major acquisitions not consummated,alternative identities not chosen, and outsourcingopportunities not pursued). After these initial in-terviews, we identified 13 to 15 major boundarydecisions for each firm and at least three internalinformants who could provide firsthand accountsof how each decision evolved.

We based selection of internal informants onthree criteria: (1) long tenure in their firm, whichwould provide a temporal perspective on the firm’sboundaries; (2) direct involvement in at least somemajor boundary decisions, which would providedeep, first-hand knowledge; and (3) functional andhierarchical variety, which allowed us to obtain avariety of perspectives. We complemented theseinternal informants with four types of external in-formants: former employees, business partners,competitors, and industry experts. Use of multipleinformants mitigates the potential biases of anyindividual respondent by allowing information tobe confirmed by several sources (Golden, 1992;Miller, Cardinal, & Glick, 1997). Use of multipleinformants also enables inducing richer and moreelaborated models because different individualstypically focus on complementary aspects of majordecisions (Dougherty, 1990; Schwenk, 1985).

The interviews ranged from 45 minutes to twohours in length. We recorded and transcribed them,generating about 800 double-spaced pages. The in-terview guide had two main sections. The first sec-tion was composed of open-ended questions thatenabled the informants to provide a broad view ofthe evolution of the relevant nascent market, thefocal firm, and its boundaries. The second sectionfocused on specific boundary decisions in whichthe informant was directly involved. We asked in-formants to relate the chronological story of thedecision as they observed it, prompted by probingquestions from the interviewer. At this stage thequestions concentrated on facts, events, and directinterpretations, rather than hearsay or vague com-mentary (Eisenhardt, 1989b). We further reducedthe potential for retrospective bias by triangulatingdata, matching real-time archival data with the ret-rospective accounts. Our epistemological approachwas thus to understand the meaning making and

2009 647Santos and Eisenhardt

conceptualizations of informants, while ensuringthat those interpretations had substantively in-formed behaviors and were not a product of laterimpression management.

The informants usually agreed about the factsand events of a given boundary decision. But theyoften also revealed complementary information.This allowed reconstruction of the histories ofboundary decisions in rich detail from variousviewpoints. Often informants described extensiveconflicts related to given boundary decisions.These accounts of conflicts were invaluable for ourexploring the roles of different boundary concep-tions in shaping boundaries. A key strength of ourdesign is that these interviews revealed details andmotives for decisions that were unavailable in thearchival data. Another strength is the use of exter-nal informants who offered an outsider perspectiveon boundary decisions and brought a “realitycheck” to the internal accounts.

Over six months, we then blended the interviewdata into the archive-based cases. The final casechronologies are about 100 pages long for eachfirm. We analyzed the context, decision process,implementation, and outcome of each boundarydecision and assessed its impact on firm and mar-ket boundaries. Overall, the combination of archi-val sources and interview data from internal andexternal informants enabled a rich, triangulated,and relatively accurate understanding of the phe-nomena (Kumar, Stern, & Anderson, 1993). For ex-ample, media articles identified key organizationalevents and clarified the industry context affectingeach boundary decision, while interview data re-vealed debates within the firms, hidden intents,and decision processes. The result is a relativelycomplete, robust understanding of the emergenceand evolution of boundaries.

Analysis

We began with an in-depth analysis of each casethrough the lens of our research question (Eisen-hardt, 1989b): How do entrepreneurs addressingnascent markets shape their organizational bound-aries over time? We had no theoretical preferencesor a priori hypotheses. We read the cases indepen-dently to form our own views of each case. The goalwas to identify independently the theoretical con-structs, relationships, and longitudinal patternswithin each case and with respect to our researchquestion. We used tables and graphs to facilitateanalyses (Miles & Huberman, 1994). We each de-veloped an understanding of the major boundarydecisions, which we reconciled by going back tothe data and, occasionally, back to the informants.

We also identified interactions among boundarydecisions and found connections among emergingcategories, which led to the specific patterns ofdecisions that emerged from the data.

We then turned to cross-case analysis, in whichthe insights that emerged from each case were com-pared with those from other cases to identify con-sistent patterns and themes (Eisenhardt & Graeb-ner, 2007). Focal firms and decisions were groupedrandomly and by variables of potential interest tofacilitate comparisons and develop propositions.Comparisons were initially made between variedpairs of cases. As patterns emerged, other caseswere added to develop more robust theoretical con-cepts and causal relations. Discrepancies andagreements in the emergent theory were noted andinvestigated further by revisiting the data. We fol-lowed an iterative process of cycling among theory,data, and literature to refine our findings, relatethem to existing theories, and clarify our contribu-tions. The data analyses took another six monthsand resulted in a theoretical model of how entre-preneurs shape boundaries in nascent markets.

Our data suggest that successful entrepreneurs innascent markets adopt a strategic approach to shap-ing organizational boundaries. For them, settingboundaries is central to the challenge of succeedingin highly ambiguous, competitive markets. We findthat, to address this challenge, entrepreneurs inter-twine organizational boundaries with market con-struction to achieve market leadership and a defen-sible position. That is, they adopt an almostmonopolistic imperative of dominating a distinctmarket that they construct. As a CEO explained,“These are the times that new technology fran-chises are being built and the way you win is thatyou have to be #1 by a long shot.”

Our data indicate that entrepreneurs enact thismonopolistic imperative using patterns of interre-lated boundary decisions that are organized intothree processes: claiming, demarcating, and con-trolling. That is, they attempt to: (1) claim a newand distinct market space and become its “cogni-tive referent” through identity-based actions; (2)demarcate this market by specifying firm and mar-ket boundaries through alliances with establishedfirms; and (3) control the market by overlapping theboundaries of the firm and market over timethrough acquisitions that eliminate entrepreneurialrivals. Underlying these processes is the unex-pected use of power tactics, such as creating illu-sions, using strategic timing, and exploiting the

648 AugustAcademy of Management Journal

tendencies of others, that form the strategic arsenalof entrepreneurs in nascent markets. Together,these processes enable a new firm with limitedinitial resources and potentially high dependenceon established firms to construct a distinct marketand achieve dominance in it. We develop eachprocess in detail next.

Claiming the Market

Entrepreneurs in nascent markets face an ambig-uous environment with unclear customers, unde-fined product attributes, and no well-establishedindustry value chain. Our data suggest that, in lightof this ambiguity, entrepreneurs in nascent marketsoften devote significant effort to claiming the mar-ket—that is, defining a distinct identity for both thefirm and market so that the two become synony-mous. If entrepreneurs are successful, their firmbecomes the cognitive referent for the claimed mar-ket: the organization that relevant others (e.g., cus-tomers, partners, analysts, and employees) auto-matically recognize as epitomizing the nascentmarket. For example, Google is widely seen as thecognitive referent for Internet search.

Our data indicate that entrepreneurs use threeidentity mechanisms to claim a market: adopt tem-plates, signal leadership, and disseminate stories.“Adopt templates” is defined as using well-knowncognitive models from other domains (either in iso-lation or combination) to convey a unique identity.This identity simultaneously makes a firm and itsnascent market distinct, yet also familiar and un-derstandable to market audiences. “Disseminatestories” is defined as spreading symbolic narratives(real or fictitious) to raise awareness about the firmand its market, and communicate the firm’s iden-tity. “Signal leadership” is defined as taking con-crete actions that convey superior power and ex-pertise within the market.

A good example is Secret, one of the firms westudied. Secret’s founders began with a sophisti-cated cryptography technology, but without a clearidentity or a well-defined product or customer set.They experimented with several ideas before gain-ing traction with an unexpected service: providinga secure environment for digital communications.But although this idea seemed promising, it wasalso very ambiguous. As the venture capitalist (VC)who backed the firm put it,

There was a product out there but it was not verywell-defined and it was searching for a market.

A Secret executive concurred:

At the time, it was the wild wild west—there was noplaybook for the Internet or our space—we createdthe playbook.

Secret’s executives spent considerable time try-ing to hone this idea by grappling with questionssuch as: What are we selling? Who are we? Who’sthe customer? In particular, they debated “secu-rity” versus “trust” as the core element of theiridentity. One executive describes the decision infavor of trust, which was an unusual identity in thisnascent market:

We believed that we had a broader obligation to theInternet at that time, which was to have this under-lying trust infrastructure. . . . Trust was not just se-curity in terms of keeping people out but it also wasletting people in. And we realized that a lot of whatwe did—digital certificates, digital signatures, thatwas not really security technology. . . . It was a trusttechnology.

Though Secret’s executives designated trust ascentral to the firm’s identity and conception of themarket, ambiguity remained. For example, one ex-ecutive noted, “It was a trust technology” but thenwent on to ask: “Is it a trusted service? Is it trustservices? Is it trust in infrastructure services?” AsSecret executives struggled to define their identity,they began adopting templates from seemingly dis-tant but cognitively related areas to describe theiractivities for would-be customers, other stakehold-ers, and even themselves. They used well-knownterms such as “ID card,” “wallet,” and “passport”as part of their vocabulary. Secret’s VC backer de-scribed how they explained their market: “Youknow, you have kind of an electronic wallet andhave all your IDs on one thing, and it would be-come your passport around the Net.”

To further clarify their identity and win accep-tance as the cognitive referent of the nascent mar-ket, Secret executives also began to signal leader-ship. For example, they hired a high-profile lawyerto convert the venture’s emerging operating proce-dures into a “best practices” framework that waspromoted at numerous venues. This framework be-came the market standard, serving to further clarifythe meaning of the nascent market to Secret’s ad-vantage and bolster the perception of the venture asthe market expert. Secret’s CEO explained:

One of the most significant early employees wasGeorge. He was very well thought of in both theacademic as well as the legal community. Georgespearheaded all our efforts . . . on encryption, digitalsignature law, what we call certificate authoritypractices. And we created the first set of industrypractices. The policies by which you should hirepeople, the policies by which we issue a certificate,

2009 649Santos and Eisenhardt

the policies by which we should revoke it. . . . So weinvented this as we went along and George’s abilityto put legal underpinnings to it really separated usfrom the would-be competitors that started in thegarage with a website.

Secret’s executives also relied on disseminatingstories that differentiated Secret and conveyed itsunique “trust identity.” For example, they orga-nized elaborate ceremonies for opening data cen-ters and invited the media (note: Secret operatedgeographically distributed data centers to deliverits service). These ceremonies were designed totransmit the image of trust through features such asarmed personnel and bunker-like facilities. Secretexecutives brought together players from the offline(e.g., notaries) and online (e.g., network securityexecutives) “trust worlds” to attend the ceremo-nies. Given the novelty of these ceremonies, Secretsucceeded in enticing the media into covering theventure in detail. For example, one reporterobserved:

An unusual ceremony at the new bunker-like oper-ations facilities of Secret grabbed the attention ofcertificate authorities such as notaries and accoun-tants, as well as corporate and network securityexecutives. Complexity and importance were ele-ments of Secret’s events. Witnessing the ceremonywere representatives from various organizations,armed officers, and a notary-videographer to recordthe ceremony for archiving.

A year later, Secret executives adjusted theiridentity by adding the template of a “public utility”that conveyed the ubiquity and high reliability of atrusted service. This identity guided later boundarydecisions such as which activities to pursue. Theyshunned even profitable activities that rivals ac-tively pursued if those activities fell outside Se-cret’s identity boundary. An example is the bound-ary decision to not engage in software sales. As aSecret vice president (VP) explained:

We decided that strategically we were a servicescompany. . . . We told a whole bunch of people:“Here is why the services model works, here is whyit is great, here is why we’re a services company todo these types of things. . . .” So you would notdecide: “Well, we are selling some software aswell.” You have to be consistent and that gives youcredibility. A key part there is that we did not reallywaffle. There were always people in sales or otherparts of the company saying: “Hey we can sell soft-ware too, it’s easy to sell, the customer can touch it,you get the revenue recognition in the current quar-ter for it, etc.” We said, “No, we are a service com-pany, we are staying on course here and stay in thisservices space.”

Over time, Secret executives succeeded in mak-ing the venture’s identity synonymous with thenascent market. By combining a trust vocabularywith the public utility template, disseminating sto-ries through symbolic ceremonies and press re-leases, and signaling leadership by setting onlinecertification standards for the market, the entrepre-neurs both clarified their venture’s identity andintertwined it with their conception of a market fortrust services (a conception that was distinct fromcompeting market conceptions such as selling se-curity products). This reinforcing pattern of bound-ary actions helped Secret to become the cognitivereferent for the nascent online certification market.Media reports from the period confirm this, callingSecret “the leading authority for certifying Webserver encryption keys.”

Magic, another sample firm, is a second example.Secret’s identity was initially poorly defined, butMagic began with a sharp sense of identity. Thecore of this identity was “customer-centric onlineshopping.” Nonetheless, Magic executives still hadto convince relevant others (e.g., customers andfinancial backers) that theirs was a winning iden-tity. Indeed, when Magic was founded, onlineshopping was a novel concept and one that wasdifficult to understand because it involved a verydifferent user experience than did traditional retailshopping. There was confusion even around basics,such as how to evaluate products and how to pay.Although the new technology offered striking fea-tures that were not available offline, Magic’s exec-utives nonetheless adopted templates from thebroad domain of offline shopping that were veryfamiliar to end users. For example, Magic’s userinterface was based on well-known, offline retail-ing concepts such as “shopping cart” and “checkout.” Their purpose was to reduce ambiguity andaccelerate user adoption.

Magic executives also signaled leadership bypurposefully offering the world’s widest selectionin their product category. They also located a fewfar-flung customers so that they could accuratelyclaim to be sending products to 45 countries and all50 U.S. states in their first month. They widelybroadcasted this achievement to the media, pro-claiming Magic to be the largest retailer in theworld in their category. But although this claimwas symbolically true in terms of geographic andproduct breadth, actual revenue was miniscule.Magic executives continued signaling leadershipby launching ads featuring high-profile figuresfrom academia, business, and sports comfortablyusing Magic’s offering. These actions supportedMagic’s identity as “customer-centric” and the ven-

650 AugustAcademy of Management Journal

ture’s positioning as the leading company in thenascent market.

Magic was also active in disseminating storiesthat reinforced its identity. For example, executivesreleased stories about the founder’s personal pas-sion for the customer (for instance, a story about acustomer with an unusual need that the founderinsisted that Magic satisfy) and corporate frugality(e.g., cheap office furniture) that reinforced theidentity of favoring customers over employeeperks. They also widely disseminated another storythat used a vocabulary that drew an analogy to U.S.history, portraying the founder as a “pioneer mov-ing west” to open up “a new frontier.” This storyfurther emphasized the venture as familiar, yetnovel.

This combination of identity mechanisms in-creased the likelihood of Magic becoming the cog-nitive referent for a distinct nascent market. In fact,media and analyst reports from the time stronglysupport the view that Magic became the cognitivereferent of its new market. As an outside expertconfirmed, “Magic has become the default namewhen you think of buying on the Net.” Moreover, itwas clear from the interviews and internal archivaldata that Magic executives purposefully craftedthese strategic actions to shape outsiders’ cognitiveunderstanding of their venture. As a senior execu-tive noted,

We knew that by the end of 2000, we would prettymuch have defined what the company stood for incustomers’ minds. . . . So you have to do that stuffpretty fast otherwise by the time you get around todo it you’re done! You can’t change people’s per-ceptions about what you are.

Although all firms engaged in practices aimed atclaiming a market, they were not equally effective.An example is Haven. Haven’s founder stumbledupon the nascent market of online marketplaceswhen his hobby unexpectedly became a success.He personally valued egalitarianism highly. Oneobserver described the founder as seeking “a fair,open, honest marketplace.” Another noted, “Havenwas capitalism for the rest of us.” To coalesce thesepersonal values into an organizational identity, thefounder adopted a “community” template, empha-sizing related vocabulary such as how “friends”could connect, share information, and trade in a“safe neighborhood.” Haven even installed “streetsigns” at the firm’s office to reinforce the commu-nity identity.

However, though this identity became very clearwithin Haven, it was unclear whether the identitywould become the cognitive referent. One chal-lenge was communicating this identity. An indus-

try expert recalled, “It was a totally different ani-mal; they [customers] didn’t know what to make ofit.” A second challenge was winning against doz-ens of competing market conceptions. For example,while Haven’s identity was a community of friendstrading with one another, Haven’s leading compet-itor (an older, larger firm) conceptualized its iden-tity as “Las Vegas style shopping excitement” andoffered a gambling format aimed at men. It wasunclear which (if any) of these very disparate iden-tities and related market conceptions would win inthe nascent market.

Haven’s founding team tried to gain traction inthe media with their identity by promoting a veryrational (and factual) account for the firm’s exis-tence based on a balanced, fair marketplace forbuyers and sellers. When this approach failed, afrustrated employee came up with the idea of dis-seminating a story about the company’s foundingthat illustrated Haven’s “community identity.” Un-like the rational account, this story had warm, per-sonal (albeit fictitious) details about the founderand illustrated how customers might use the ser-vice. This unusual and romantic story was pickedup by the press, embellished, and repeated in manyarticles featuring Haven. This media attention rein-forced the firm’s community identity and sharp-ened understanding of how customers could use itsservices. Haven executives followed up with mar-keting initiatives that further reinforced the coreidentity features of the story.

In addition, Haven executives then signaled lead-ership through preemptive litigation threats thatblocked potential competitors’ access to Haven’scustomers. Although they justified this hostile ac-tion in the media as protecting the “security” and“privacy” of the “community,” they were alsosignaling aggressive defense of Haven’s claim onthe market, despite its having lower resourcesthan some competitors. Overall, although Ha-ven’s late start in claiming the market probablyprecluded the firm from becoming the cognitivereferent in its first years, these persistent effortshelped to construct a distinct market and enabledHaven to be a leading firm within it. A mediareport confirmed that the “consumer-to-con-sumer online model is a new niche that Havenwas able to foster.”

Finally, as Saturn illustrates, entrepreneurs weresometimes unable to construct a distinct market inwhich they became the cognitive referent. Saturn’sfounders targeted an “empty space” located nearthe telecom equipment and networking markets.The founder explained:

2009 651Santos and Eisenhardt

Not one customer in the telecom business said theyneeded such an IP router for the core. Everyone withno exception was using Internet switches. Not onetelecom provider was even thinking of buildingsuch a router for the public telecommunicationsnetwork because no customer had ever askedfor one.

Although Saturn executives wanted to claim themarket, they did not use identity mechanisms well.For example, they did not adopt a template from adistant but cognitively related area. Rather, theyfollowed the template and vocabulary of the nearbynetworking market. They also kept their technologysecret early on, which impaired their ability to sig-nal leadership. Although they created a rationalefor the firm, it took the form of a “theory” to explainthe existence of their market. As such, it was sim-ilar to Haven’s failed initial rationale. Haven exec-utives, however, then created a memorable storywith compelling characteristics; Saturn executivesdid not. Moreover, they narrowly disseminatedtheir “theory” to industry analysts. Overall, lesseffective use of identity mechanisms limited Sat-urn’s ability to become the cognitive referent in adistinct nascent market. Saturn executives and in-vestors strongly believed that the firm was creatinga distinct market; for instance, its CEO argued, “Wehave a combination of a fortunate timing equationand a focused objective in what will become, whenhistory is written, a fundamentally different mar-ket.” Yet market audiences considered Saturn’smarket to be an extension of an existing market. Asa media report of the period noted, “Saturn iswidely perceived as a threat to [the market leader’s]hold on the networking market.”

Overall, our data indicate much variation in theuse of identity mechanisms to claim a market. Ta-ble 2 summarizes our data on claiming the market.More significantly, entrepreneurs who proactivelyuse reinforcing identity mechanisms (i.e., adopttemplates, disseminate stories, and signal leader-ship) are more likely to become the cognitive refer-ents in the distinct markets that they claim. Thus,claiming is a “sensegiving” process by which anentrepreneur can achieve cognitive dominance in anascent market.

The claiming process is effective for several rea-sons. First, adopting templates exploits the ten-dency of individuals to be attracted to the blend ofnovelty and familiarity (Davis, 1971). In keepingwith prior research, we observe that adoption offamiliar templates makes it easier for outsiders tounderstand a firm and its innovations (Hargadon &Douglas, 2001) and for insiders to grasp their firm’sidentity (Rindova & Kotha, 2001). But we also con-tribute the insight that having a distant template is

important as well. Adopting templates and relatedvocabulary from very proximate markets makes itless likely audiences will be intrigued and perceivea firm as having a distinct market and identity (e.g.,Saturn). In contrast, templates drawn from seem-ingly distant contexts, related by analogy, are morelikely to be understood and remembered (e.g., Se-cret). Adopting a template that combines the famil-iar and the distant thus enhances the likelihood ofacceptance and so developing a winning identityfor a distinct market.

Second, stories are effective because they exploita second tendency of individuals—that is, to over-value vivid stories. Research shows that stories areparticularly effective because they memorably con-vey information. Individuals are much more likely,for example, to remember the implications of sim-ple, emotionally charged stories than to rememberfacts and quantitative information (Heath, Bell, &Sternberg, 2001; Nisbett & Ross, 1980). Moreover,our research contributes insight into the story char-acteristics that are especially helpful for promotingunderstanding of a new firm or nascent market.When stories take the user perspective, portray afirm or its members in unusual situations, and con-tain intriguing personal information, they are morelikely to become sensegiving devices that are am-plified by the media. Interestingly, even fictionalstories are effective if then enacted and made partof the perceived reality (e.g., Haven).

Third, leadership signals are effective becausethey convey firm importance while also often beingrelatively inexpensive (e.g., Secret’s lawyer; Mag-ic’s few distant customers). As such, entrepreneurscreate illusions that they are more prominent,larger, and important than they actually are. Al-though Zott and Huy (2007) found that effectiveentrepreneurs use symbols to convey their quality,we add that symbols such as leadership signals canalso be illusory exaggerations that are nonethelesshighly influential for gaining the attention and sup-port of market audiences.

Overall, the claiming process is a reinforcingblend of sensegiving activities that define the iden-tity of a new firm as synonymous with the nascentmarket. As suggested by the research in “institu-tional entrepreneurship,” these types of identity-defining activities can enhance legitimacy (Harga-don & Douglas, 2001; Lounsbury & Glynn, 2001).Institutional entrepreneurship research empha-sizes creating legitimacy, whereby an organization-al form or institution becomes “desirable, proper,and appropriate” (Suchman, 1995: 574). We, on theother hand, emphasize creating cognitive domi-nance, whereby an individual firm constructs amarket and becomes its cognitive referent. By rely-

652 AugustAcademy of Management Journal

ing on soft-power strategies of nuanced influencebased on early timing, self-serving illusions, andexploitation of others’ tendencies, entrepreneurstransform an ambiguous, contested opportunityinto a winning claim.

Demarcating the Market

Although cognitive dominance is crucial, com-petitive dominance is also imperative. Even as en-trepreneurs begin establishing their identities and

TABLE 2Claiming the Market

OverallRatinga

Identity Mechanisms

ResultbAdopt Templates Signal Leadership Disseminate Stories

Definition Use of cognitive models fromother areas, together withvalues, practices andvocabulary.

Concrete actions that conveysuperior expertise and/orpower.

Spreading of symbolicnarratives about thecompany and/ormarket (fictitious orreal).

Rationale Sensegiving by analogy tohelp internal and externalactors understand ventureand market.

Create legitimacy andperception of leadershipin the eyes of internal andexternal actors.

“Magic has become the defaultname when you think ofbuying on the Net.”

Secret ������ ��Adopted “trusted services”

template and vocabulary.Added “public utility”

template.

��Defined and disseminated

legal framework of“certification bestpractices.”

��Organized unusual

ceremoniesw/armed guardsand bunkerfacilities to attractthe media.

Cognitive referent, distinctmarket

“The market [analysts andcustomers] . . . establishedSecret as leading authorityfor certifying Web serverencryption keys.”

Haven ���� ��Adopted “community”

template, vocabulary, andrelated social values.

�Reactive use of litigation

against would-be rivals.

�After early misstep,

widely publicized(and false) romanticstory about founder.

Not cognitive referent, distinctmarket

“The consumer-to-consumeronline auction model is anew niche that Harbor wasable to foster.”

Midway ���� �Late adoption of the template

of “operating system forthe Internet.”

��Acquired several high-

profile firms.

�Created new category

of end users, the“E-generation,” butdid not promote itmuch.

Not cognitive referent, distinctmarket

“The company has carved outa marketplace that hasproven crucial tocomputing.”

Saturn ��Did not adopt a distinct

template from anotherarea.

�Belatedly secured three

flagship clients.Kept technology secret for

two years.

�Created “theory” to

justify new market,but it was neitherwidelydisseminated normemorable.

Not cognitive referent, notdistinct market

“Saturn is widely perceived asa threat to [market leader’s]hold on the [existing]networking market.”

a To rate the use of identity mechanisms, we assigned each firm a score of “�” for use of a particular action. We assigned “��” if a firmwas particularly early and proactive in using this mechanism.

b We measured becoming the cognitive referent for a market by whether the firm was portrayed in the media as the market referencethree years after founding. We measured the existence of a distinct market by whether the market was described in the media as uniqueand independent of related markets.

2009 653Santos and Eisenhardt

claiming their nascent markets, they also face con-siderable ambiguity regarding key dependenciesand exchange partners. Moreover, they are usuallysurrounded by powerful established firms that maydefine the nascent market as part of their own ex-isting market or as an attractive new market to enter(Markides & Gerosky, 2005). It is often unclear howexecutives in these large, established firms mayultimately perceive their roles in a nascent market.If they choose to be competitors, they can become asignificant threat.

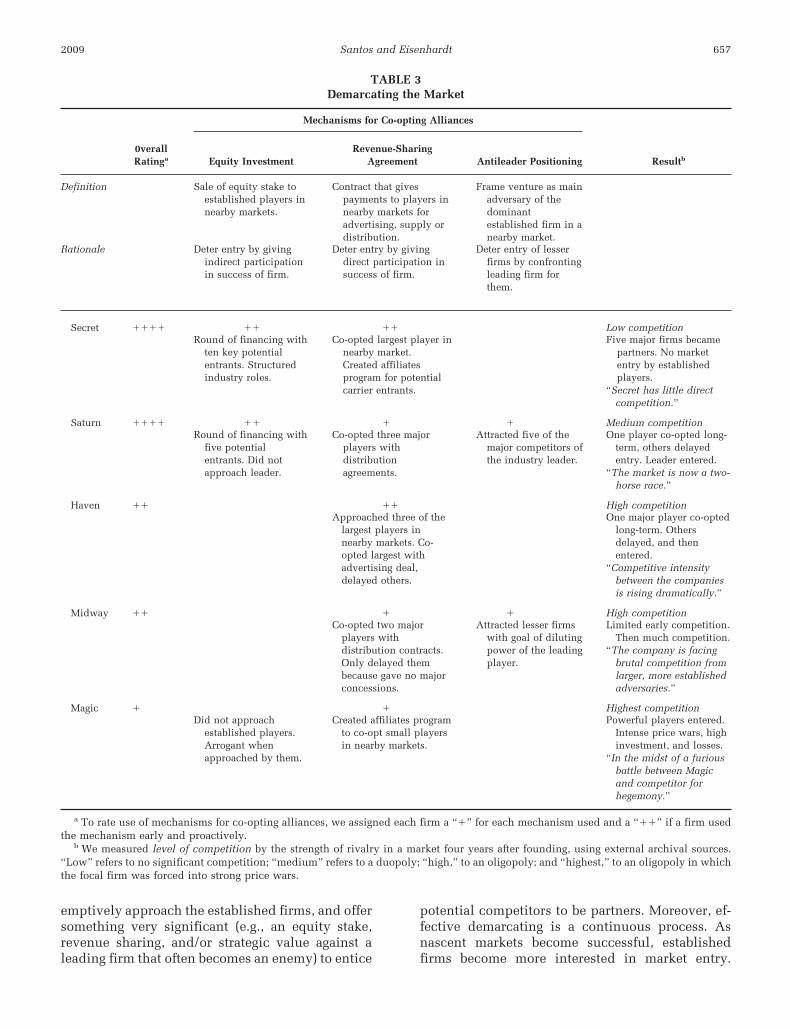

Anticipating this threat, our data suggest thatentrepreneurs in nascent markets attempt to avoidcompetition with powerful firms from nearby mar-kets by co-opting them with alliance mechanisms.These mechanisms create viable industry roles(e.g., supplier, complementer, buyer) for these po-tential competitors. In so doing, entrepreneurs de-lineate the perimeters of their firms and shape thesurrounding industry structure to gain clarity andsupport for their constructed market and avoidcompetition from powerful firms. It is this processthat we call “demarcating the market.”

Our data indicate three alliance mechanisms thatentrepreneurs use to entice powerful firms to ac-cept industry roles other than that of competitor:revenue-sharing agreement, equity investment, andantileader positioning. A “revenue-sharing agree-ment” is an alliance mechanism by which a partnerfirm benefits from a nascent market through distri-bution, advertising, or supplier contracts with afocal venture. Such agreements provide the partnerwith an industry role and revenues from the nas-cent market without directly participating. Thus,established firms have an incentive (and often alegal obligation) to support the new firm and nas-cent market.

“Equity investment” is an alliance mechanismby which entrepreneurs allow partner firms topurchase financial stakes in their ventures.Again, this enables these firms to benefit from thenascent market without participating directly.Thus, although entrepreneurs sacrifice owner-ship and may need to share private information,they also reduce the incentive of powerful firmsto become competitors.

“Antileader positioning” is an alliance mecha-nism used when there is a very strong firm domi-nating a proximate market. Entrepreneurs seekother established firms to join an alliance opposingthis leader. For such an invitation to be credible,the market claimed by the venture must be seen asattractive for the leader to enter. If that is the case,the other established firms will support the newfirm in order to distract and counter the leader’sdominance. The downside is that entrepreneurs

often alienate this dominant firm and are likely tobecome its rival.

Saturn is an excellent example. As noted earlier,Saturn began in a nascent market that was proxi-mate to the networking and telecom equipmentmarkets. Saturn anticipated competitive threatsfrom established firms in both markets. These firmsmight regard the nascent market either as an exten-sion of their own market or as an attractive marketto enter, especially if Saturn succeeded. Therefore,Saturn executives proactively attempted to definetheir organizational boundary and that of the nas-cent market by pursuing alliances with five estab-lished firms. Saturn’s enticement was twofold: Itoffered equity investment to give these firms a fi-nancial stake in the nascent market while leavingthem free to focus their time and resources else-where. Then, in addition to this important lure,Saturn was willing to be the antileader to thedominant firm. This willingness was key. Thepotential partners feared the leader and battledthis dominant firm in multiple markets (e.g., op-tical, landline, wireless). As Saturn’s CEO ex-plained: “All of them were worried about [theleader] and we were the anti-[leader], so it was achance for them to team up with somebody thatwas taking [the leader] on.” To the surprise ofSaturn executives, all five target partners agreedto ally. Two then agreed to equity investments.When the others found out, they clamored toinvest as well. These alliances were costly toSaturn because they required disclosure of pri-vate information and diluted ownership whenthe firm already had sufficient financial re-sources. However, the goal of demarcating a clearperimeter that clarified Saturn’s boundary rela-tive to threatening firms outweighed the draw-backs. Antileader positioning and equity invest-ment thus transformed five very large firms frompotential competitors into partners and furtherdefined the industry structure. An industry ex-pert noted:

They pulled together a beautiful deal on the strate-gic side that was tried to be copied by many othercompanies. This is difficult when you are dealingwith so many gorillas.

As the market grew, successful co-optation ofSaturn’s partners required continual attention andfurther incentives to keep them from becomingcompetitors. For example, a year later, Saturn ex-ecutives deepened their alliances with several part-ners via revenue-sharing agreements. These weredistribution ties that legally obligated the partnersto stay out of Saturn’s market and promote Saturn’sproducts. In return, these partners gained a share of

654 AugustAcademy of Management Journal

the products’ revenues. An industry expert com-mented on the success of one of these agreements:“Saturn’s partner was selling a remarkable amount,like a hundred million dollars, of their gear. Thatwas a great partnership.”

Overall, Saturn was successful in demarcatingthe market by using alliance mechanisms to createviable industry roles for potential competitors anddeter their market entry. Of course, Saturn did notdeter the market leader, which became a competi-tor. Still, the combination of a strong technology,growing awareness of Saturn by key market audi-ences, and the transformation of some potentialcompetitors into partners enhanced Saturn’s com-petitive strength, leading to a duopoly between Sat-urn and the leader. As an analyst noted, “The mar-ket became a two-horse race.”

Secret is a second example. As noted earlier, itsexecutives were constructing a nascent market fo-cused on trust services in digital commerce. Theyanticipated that several large firms in the banking,telecom, and software markets might become com-petitors, especially if Secret succeeded. Soon afterthe firm’s founding, Secret’s executives organizedseveral brainstorms to identify the firms most likelyto become competitors in order to try to deter theirentry. Secret’s CEO explained:

One of the things that separate us is that we arealways worried about who could take this awayfrom us and we tend to find a way to cooperatewhen there is a win-win scenario. Before they rec-ognize us and turn their attention to us, we find away for them to benefit from their associationwith us.

Secret’s executives chose equity investment astheir initial alliance mechanism to co-opt thesefirms. They spent a few months negotiating a roundof equity financing with several of them. Muchlike Saturn’s executives, those at Secret were notparticularly concerned with young firms thatwere perceived by others as their rivals. An ex-ecutive confirmed: “We were not afraid of our[entrepreneurial] competitors. We were alwaysafraid of the bigger people . . . whether it’s FirstData or IBM or Microsoft.” So, their strategy was toanticipate the future moves of these establishedfirms before their executives recognized the prom-ise of the nascent market. They hoped that an eq-uity stake in Secret would encourage these poten-tial competitors to focus elsewhere. As Secret’s VCexplained:

I wanted to get all people believing in what we weredoing and starting to sell the vision of certificate usefor identification. And I wanted to keep them out ofthe market. . . . Everybody was doing a hundred

things. But if we took this one off their plate, hope-fully they would become our partner.

A few months later, Secret announced an equityinvestment round that included several large po-tential competitors from proximate markets. Al-though these alliances provided attractive re-sources and prestige for Saturn, our interview andarchival data clearly reveal that Secret executiveswere strategically focused on deterring competitionand demarcating the nascent market. They wantedSecret’s position clarified and wanted these poten-tial competitors to take on supporting industryroles. Thus, their actions were designed to set theorganizational boundary, demarcate the marketperimeter, and define nonrival industry roles.The CEO explained: “We have kind of also cre-ated a demilitarized zone for ourselves. I thinkthat was very important.” Secret’s VC went fur-ther: “They [the equity investment alliances] didhave material consequences. They established usas the leader.”

Anticipating that the effectiveness of equity in-vestments to deter competition might wane if thenascent market grew, Secret executives proactivelycontinued to discourage competition by offeringrevenue-sharing agreements. For example, Secretsuccessfully sought an alliance with a leading po-tential competitor by redirecting some of Secret’sactivities so that this firm became a supplier, not acompetitor. Secret executives also created an affil-iates program to entice potential international com-petitors to sign revenue-sharing agreements. Secretgave these firms a portion of in-country revenuesand a complementer role in their geographic re-gions. According to the CEO, “The affiliate modelwas put out so that we could get into bed withphone companies.” As a result, Secret avoidedcompetition with another group of powerful es-tablished firms. Overall, Secret’s alliances de-terred competition. In fact, no established firmchose to compete directly with Secret. As oneindustry expert noted, “Secret has little directcompetition.”

Saturn and Secret executives anticipated com-petitive threats from established firms and proac-tively blunted them; other entrepreneurs were nei-ther as prescient nor as effective. Nonetheless, evenmodest attempts at demarcating often sharpenedorganizational boundaries, further defined markets,and delayed competition. Haven illustrates thesepoints. Haven executives began using alliances todeter competition and demarcate the firm’s marketseveral years after founding (in contrast, Secret andSaturn began much earlier). Because of this delay,the nascent market was less ambiguous and more

2009 655Santos and Eisenhardt

attractive for established firms. Haven executivesidentified three powerful established firms thatwere significant competitive threats because oftheir well-known aggressiveness and proximatemarkets. These firms possessed crucial resourceadvantages (including much larger customer bases,deeper pockets, and more reliable technologies).Although Haven’s executives approached all threefirms with revenue-sharing agreements, they weresuccessful with only one. Even that deal was pain-ful for Haven. It deeply divided the executive teambecause it required Haven to sign an agreement thatincluded an expensive advertising contract (the ini-tial down payment consumed half of Haven’s an-nual marketing budget) in exchange for exclusiveaccess to that firm’s customers and a “noncompete”agreement. On the one hand, the business develop-ment team argued that the deal was necessary togain customers and avoid competition. On theother hand, senior executives were loath to give upso much money since Haven was already gainingcustomers. The deciding factor was their belief thatblocking competition from this leading firm wasworth the price. As a board member put it: “Wewere paying that amount to prevent [the large po-tential competitor] from entering the business.” Asin the other ventures, a power-driven, monopolisticlogic was decisive in shaping organizational andmarket boundaries.

Simultaneously, Haven executives were also ne-gotiating alliances with the two other possible com-petitors. Unfortunately, executives at these firmsperceived Haven’s nascent market as a very attrac-tive extension of their own markets. After severalmonths of secret negotiations, they each offered toacquire Haven instead of allying. Haven executivesdeliberately prolonged the subsequent acquisitiontalks to gain more time to establish Haven in themarket. They had no intention of being acquired.Eventually the acquisition offers were withdrawn.The CEO of one of those firms described his finalnegotiating instructions: “OK, then let’s stop talk-ing to them because we really want to build ourown. Then we’ll go kill them!” These two firmsintensely competed against Haven for two years.Nonetheless, the alliance with the first firm and thenegotiation delays with the others gave Haven alead. This lead, coupled with fortuitous networkeffects and an increasingly compelling identity (seethe prior section), helped Haven win over thecompetition.

As in claiming, in demarcating the market oursample exhibits useful variation: not all the sam-pled entrepreneurs engaged in market demarcation.At Magic, for example, executives were aware ofestablished firms that might compete with their

venture, but they did not pursue alliances to detertheir entry. Instead, when several large firms pro-posed alliances, Magic’s executives rudely rejectedthem. A Magic VP noted, “We thought that thosecompanies were old-fashioned and that they couldnever really compete with us.” Rather, Magic in-vested in equity alliances with small ventures. Un-fortunately, two rejected suitors entered the marketand competed surprisingly well against Magic.They forced the company into price wars and highexpenditures that brought four years of losses. Iron-ically, not only did Magic fail to avoid strong com-petition from established firms—the venture alsolost most of its investment in its small allies whenmany of these firms failed.

Table 3 compares the firms’ use of alliancemechanisms to demarcate markets. As shown,entrepreneurs who proactively use a mix of alli-ance mechanisms (i.e., equity, revenue sharing,antileadership) to define their organizationalboundaries are likely to face less competition fromestablished firms and create a more delineated in-dustry structure around their markets. Thus,though claiming activities help entrepreneurs toachieve cognitive dominance, demarcating is apowerful co-opting process that helps firmsachieve competitive dominance. Demarcating alli-ances cancel or at least delay competition fromestablished firms, thus favorably shaping competi-tive dynamics.

The demarcating process is effective for severalreasons. First, alliances exploit the natural ten-dency of large firms to delay entry into nascentmarkets until these markets are well defined(Ozcan & Eisenhardt, 2009). Executives in estab-lished firms often believe (and rightly so) that theycan delay entry and still be effective competitors(Markides & Gerosky, 2005). Moreover, they oftenprefer to approach nascent markets by creating“real options” such as ties to new firms that pro-vide learning opportunities and potential stepping-stones to accelerated market entry.

Second, these alliances are also effective becausethey enable entrepreneurs to use self-serving illu-sions. For example, entrepreneurs were more effec-tive in demarcating their markets when they cre-ated the impression that they were open to beingacquired by their partners even when they werenot. Similarly, when alliance attempts failed, entre-preneurs sometimes pretended that they wanted tobe acquired when they were actually delaying theirwould-be buyers to postpone competition and in-crease their own strength.

Third, the demarcating process relies on timing.We observe that demarcating is most effectivewhen entrepreneurs anticipate threats early, pre-

656 AugustAcademy of Management Journal

emptively approach the established firms, and offersomething very significant (e.g., an equity stake,revenue sharing, and/or strategic value against aleading firm that often becomes an enemy) to entice

potential competitors to be partners. Moreover, ef-fective demarcating is a continuous process. Asnascent markets become successful, establishedfirms become more interested in market entry.

TABLE 3Demarcating the Market

0verallRatinga

Mechanisms for Co-opting Alliances

ResultbEquity InvestmentRevenue-Sharing

Agreement Antileader Positioning

Definition Sale of equity stake toestablished players innearby markets.

Contract that givespayments to players innearby markets foradvertising, supply ordistribution.

Frame venture as mainadversary of thedominantestablished firm in anearby market.

Rationale Deter entry by givingindirect participationin success of firm.

Deter entry by givingdirect participation insuccess of firm.

Deter entry of lesserfirms by confrontingleading firm forthem.

Secret ���� �� �� Low competitionRound of financing with

ten key potentialentrants. Structuredindustry roles.

Co-opted largest player innearby market.Created affiliatesprogram for potentialcarrier entrants.

Five major firms becamepartners. No marketentry by establishedplayers.

“Secret has little directcompetition.”

Saturn ���� �� � � Medium competitionRound of financing with

five potentialentrants. Did notapproach leader.

Co-opted three majorplayers withdistributionagreements.

Attracted five of themajor competitors ofthe industry leader.

One player co-opted long-term, others delayedentry. Leader entered.

“The market is now a two-horse race.”

Haven �� �� High competitionApproached three of the

largest players innearby markets. Co-opted largest withadvertising deal,delayed others.

One major player co-optedlong-term. Othersdelayed, and thenentered.

“Competitive intensitybetween the companiesis rising dramatically.”

Midway �� � � High competitionCo-opted two major

players withdistribution contracts.Only delayed thembecause gave no majorconcessions.

Attracted lesser firmswith goal of dilutingpower of the leadingplayer.

Limited early competition.Then much competition.

“The company is facingbrutal competition fromlarger, more establishedadversaries.”

Magic � � Highest competitionDid not approach

established players.Arrogant whenapproached by them.

Created affiliates programto co-opt small playersin nearby markets.

Powerful players entered.Intense price wars, highinvestment, and losses.

“In the midst of a furiousbattle between Magicand competitor forhegemony.”

a To rate use of mechanisms for co-opting alliances, we assigned each firm a “�” for each mechanism used and a “��” if a firm usedthe mechanism early and proactively.

b We measured level of competition by the strength of rivalry in a market four years after founding, using external archival sources.“Low” refers to no significant competition; “medium” refers to a duopoly; “high,” to an oligopoly; and “highest,” to an oligopoly in whichthe focal firm was forced into strong price wars.

2009 657Santos and Eisenhardt

Thus, co-optation incentives need to be enhanced.For example, Midway (a venture establishing a newsoftware market) was able to form demarcating al-liances with major firms, turning potential compet-itors into complementers and buyers. But Midwaydid not enhance the enticements for these firmsover time. As the market blossomed, their partnersbecame competitors.

Finally, the demarcating process relates to therole of alliances in theories ranging from transac-tion cost economics and resource dependence tothe resource-based view of the firm. Advocates ofthese theories often regard alliances as a means toaccess resources (Dyer & Singh, 1998; Gulati, 1998;Hallen, 2009; Katila, Rosenberger, & Eisenhardt,2008). Although our data confirm that gaining re-sources can be a rationale for alliances, it is notalways the driving force. Rather, alliances can beused to delay competition and define a favorableindustry structure by deterring the entry of strongpotential competitors, clarifying a firm’s bound-aries vis-a-vis others, and creating supporting rolesfor potential competitors as suppliers, comple-menters, and buyers. Thus, we assert that powerand co-optation, not just resources, are central towhy firms seek alliances.

Controlling the Market

Entrepreneurs in nascent markets typically faceentrepreneurial rivals, and these may have differ-ent resource combinations and alternative marketconceptions. Given high ambiguity, entrepreneursare usually unable to anticipate whether these en-trepreneurial rivals will outcompete them, be irrel-evant, or be acquired by established firms as step-ping-stones into the market. Given the possiblecompetitive threat from these rivals, our data indi-cate that entrepreneurs try to control the market byoverlapping their organizational boundary with themarket boundary in such a way that their firmoccupies as much of the market space as possible.This is achieved through acquisition (and oftendestruction) of the resources of entrepreneurialrivals.

Our data indicate that entrepreneurs use threetypes of acquisition mechanisms to control mar-kets: elimination of competing models, increasingcoverage, and blocking entry. “Elimination of com-peting models” is an acquisition mechanism aimedat destroying the resources of threatening rivals.These rivals usually have resources or businessmodels that could be superior or otherwise damag-ing to a focal entrepreneur’s control of a nascentmarket. After the acquisition, these resources aredestroyed or blended into the acquiring firm to

make its resource portfolio more robust. “Increas-ing coverage” is an acquisition mechanism that ex-pands an acquirer’s presence into emerging areas ofa nascent market (e.g., new geographical regions,new categories of users) so that the boundaries ofthe market and firm continue to be aligned as themarket expands. “Blocking entry” is an acquisitionmechanism aimed at removing possible stepping-stones into a market. The possibility that estab-lished firms could easily enter the market by ac-quiring these rivals is the main concern beingaddressed, not fear of the rivals per se. This type ofacquisition often concludes with disposal of theacquired resources.